renegotiation design with unverifiable info dylan b. minor

Post on 21-Dec-2015

215 views

TRANSCRIPT

Renegotiation Design with Unverifiable Info

Dylan B. Minor

Overview

• Motivation of the Problem

• Model: two instruments, three assumptions

• 3 Designs/ Solutions for 3 Settings

• Empirical Implications (and questions)

The Problem

• Contracting is done ex-ante• Future contingencies happen ex-post contract, ex-ante trade• These events are not contractible because outcomes are either not observable or more

likely they are not verifiable (and thus not enforceable in court)• Creates opportunity for improvement via redesign of contract ex-post contract (and

realization of state of the world), ex-ante trade (and perhaps ex-post investment)• Problem: how to design a contract to deal with non-contractibles?

The (Potential) Solution

• Add two contractual instruments in the original contract:• 1) Specify a Default Option in the Event of Renegotiation• 2) Assign bargaining power ALL to one individual• (possibly both instruments are a function of signals sent from each party)

Compared to Hart-Moore (1988): HM only assume “no trade” as default option and thus do not reach our first best from allowing a richer default option set

Renegotiation Design Time Line

Observable, but Non-Contractible

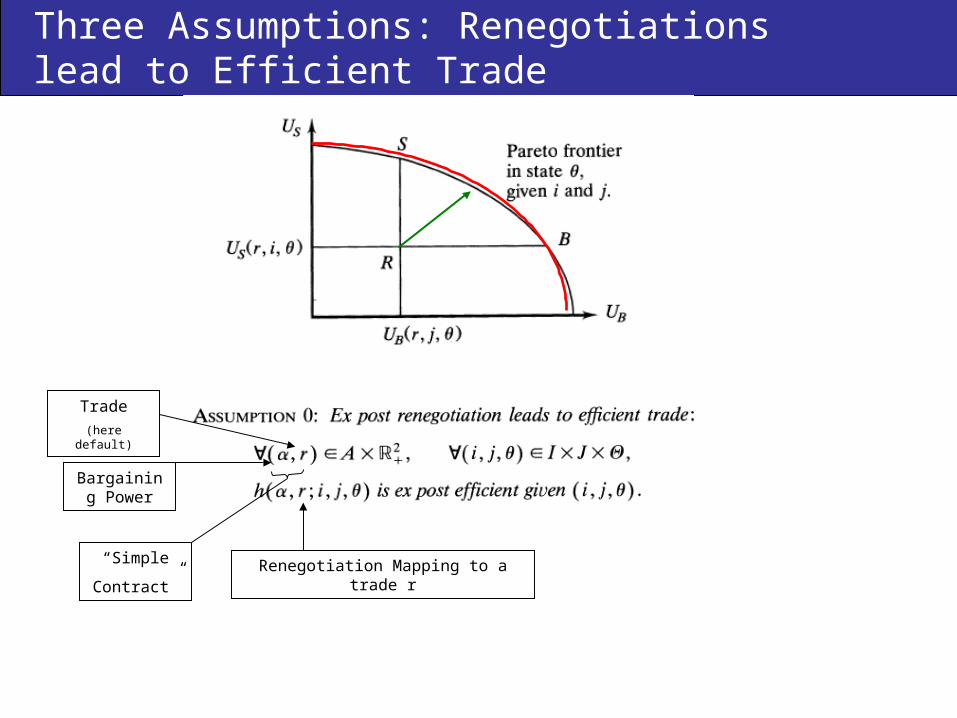

Three Assumptions: Renegotiations lead to Efficient Trade

Bargaining Power

Trade(here default)

Renegotiation Mapping to a trade r“Simple

Contract”

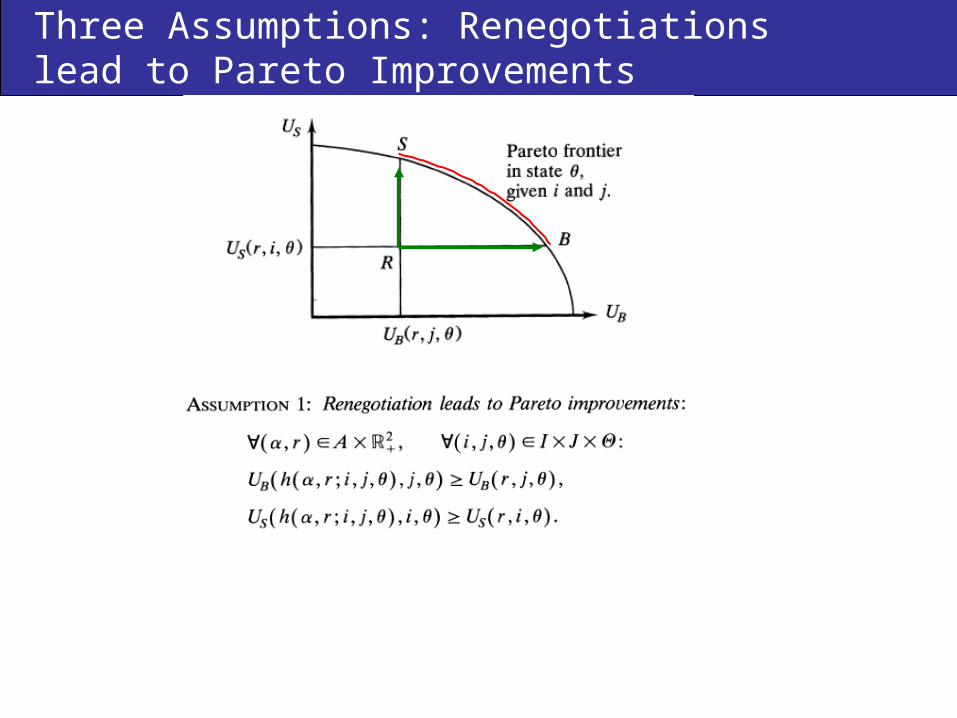

Three Assumptions: Renegotiations lead to Pareto Improvements

Three Assumptions: Contracts allocate all bargaining power to either agent

Game Theoretic Construct Intuition

• Complete information and sequential bargaining ensures ex-post efficiency (i.e., assumption 0) per Rubinstein model (1982)

• A contractual provision allows either party to unilaterally impose a common default option (i.e., assumption 1)

• Deadlines and penalties force an immediate resolution (i.e., assumption 2)

I. Investment under Risk Neutrality

I. Investment under Risk Neutrality

• Proof:• Through continuity of the 1st derivatives, we know such a q_o exists• Choosing q_o, the optimum quantity given the mean state, (along with no buyer bargaining power) produces best response j*• Since the seller is the residual claimant, he fully internalizes the effect of his investment and thus responds with i* (note

optimum invest level is independent of the state, only the quantity/ price pair depends on state).• Ex-post renegotiation ensures efficient trades take place (default option ensures it is Pareto improving)• P_o then chosen to yield desired division of the total surplus.• Thus, buyer always gets same utility ex-post, whereas the seller gets more or less ex-post depending on the realized state-

i.e., the full return on his investment minus a fixed amount (and he’s risk neutral so it doesn’t matter).

I. Investment under Risk Neutrality

• H-M (1988): (Generally) Underinvestment• This paper: first best (thanks to other than “no trade”

default options)

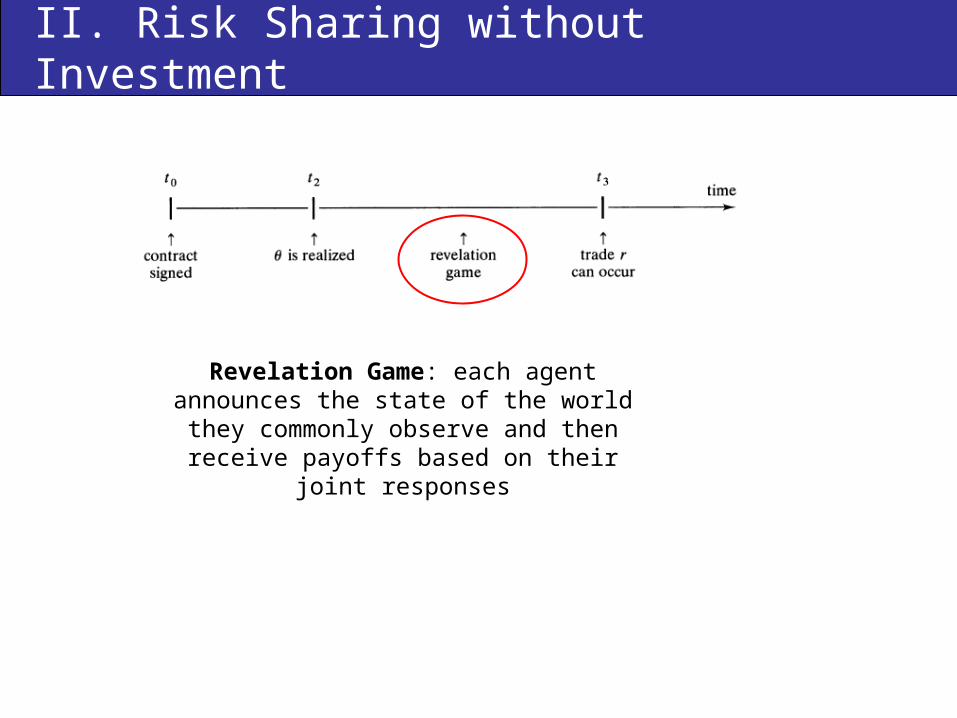

II. Risk Sharing without Investment

Revelation Game: each agent announces the state of the world they commonly observe and then receive

payoffs based on their joint responses

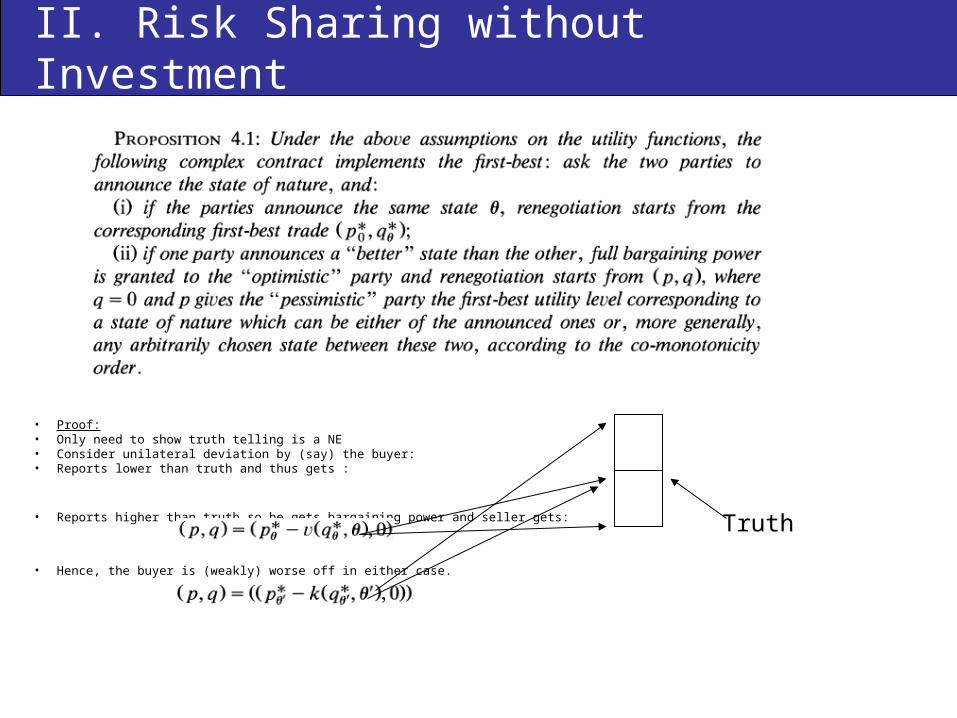

II. Risk Sharing without Investment

• Proof:• Only need to show truth telling is a NE• Consider unilateral deviation by (say) the buyer:• Reports lower than truth and thus gets :

• Reports higher than truth so he gets bargaining power and seller gets:

• Hence, the buyer is (weakly) worse off in either case.

Truth

II. Risk Sharing without Investment

• H-M (1988): First best if messages VERIAFIABLE• This Paper: First best even with UNFERIFIABLE

messages

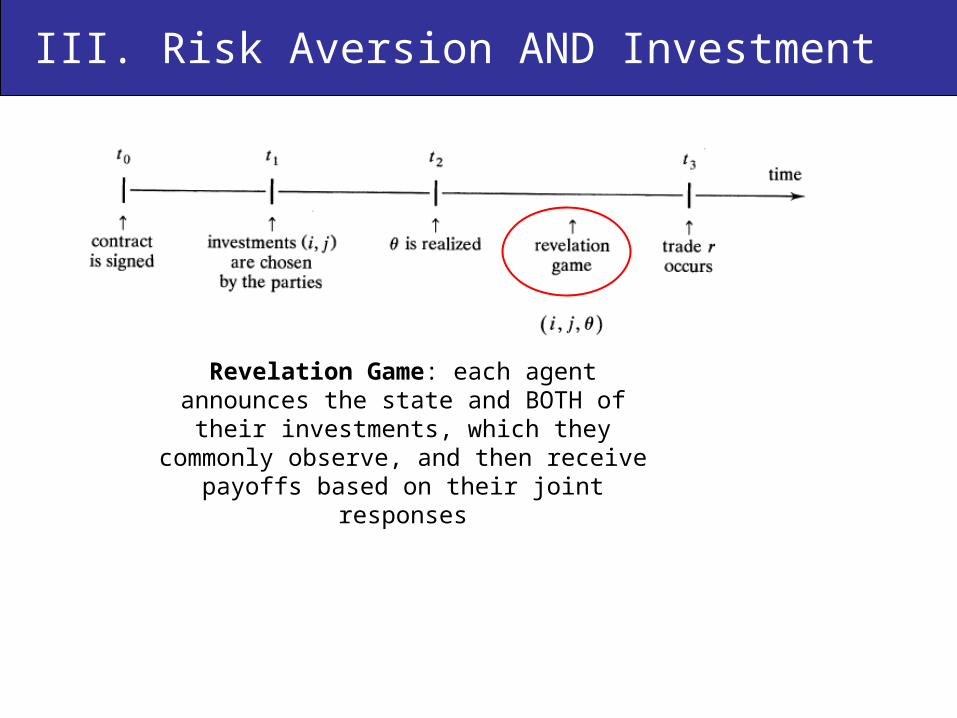

III. Risk Aversion AND Investment

Revelation Game: each agent announces the state and BOTH of their

investments, which they commonly observe, and then receive payoffs based

on their joint responses

III Risk Aversion AND Investment

• Proof (intuition of the intuition):• Assume various regularity assumptions on utilities and their components (and also discrete states).• If neither seller/buyer disagrees that efficient investment was chosen, we play a similar game g* to

the risk sharing game, insuring state truth telling• To keep optimum investment we create contracts that essentially allow party A to not be hurt by the

party B as long as party A invests at the optimum level, and yet either party is hurt if they do not invest at the optimum. This then deters unilateral ex-post deviations, providing our equilibrium.

III Risk Aversion AND Investment

• H-M (1988): What are you crazy?• This Paper: Yep First Best (with a wee bit of a

convoluted contract).

Empirical Implications

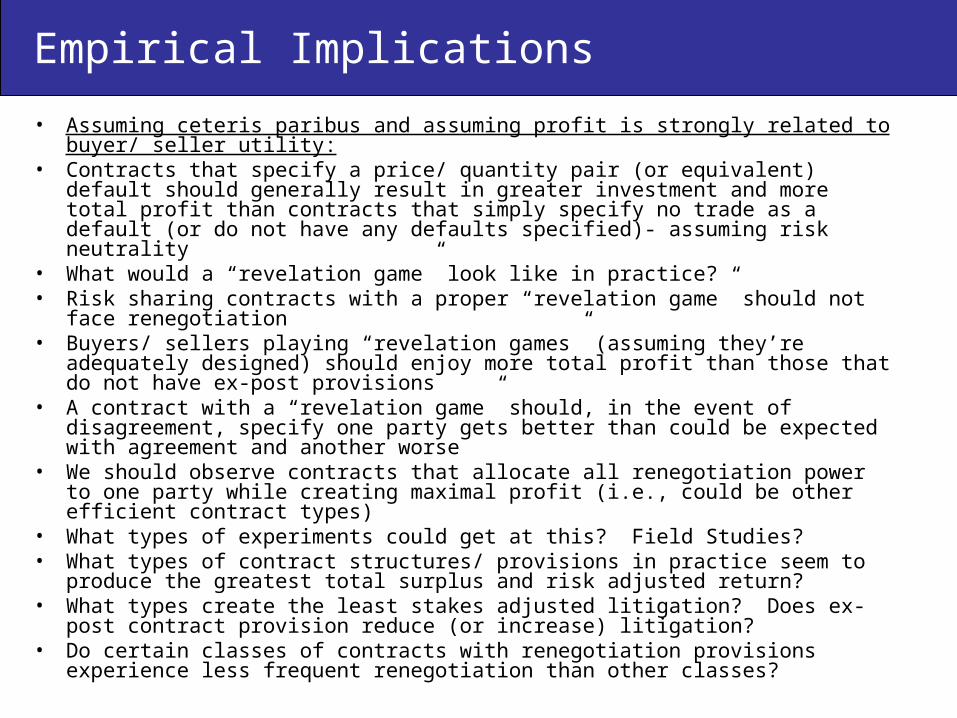

• Assuming ceteris paribus and assuming profit is strongly related to buyer/ seller utility:

• Contracts that specify a price/ quantity pair (or equivalent) default should generally result in greater investment and more total profit than contracts that simply specify no trade as a default (or do not have any defaults specified)- assuming risk neutrality

• What would a “revelation game” look like in practice?• Risk sharing contracts with a proper “revelation game” should not face

renegotiation• Buyers/ sellers playing “revelation games” (assuming they’re adequately

designed) should enjoy more total profit than those that do not have ex-post provisions

• A contract with a “revelation game” should, in the event of disagreement, specify one party gets better than could be expected with agreement and another worse

• We should observe contracts that allocate all renegotiation power to one party while creating maximal profit (i.e., could be other efficient contract types)

• What types of experiments could get at this? Field Studies?• What types of contract structures/ provisions in practice seem to produce the

greatest total surplus and risk adjusted return? • What types create the least stakes adjusted litigation? Does ex-post contract

provision reduce (or increase) litigation?• Do certain classes of contracts with renegotiation provisions experience less

frequent renegotiation than other classes?