reinsurance topics: impact on insurance rates alabama affordable homeowners insurance commission...

TRANSCRIPT

Reinsurance Topics: Impact on Insurance RatesAlabama Affordable Homeowners Insurance Commission

November 21, 2011

Bob Fox, ACAS, MAAA

Director, Catastrophe Actuarial

Aon Benfield

2

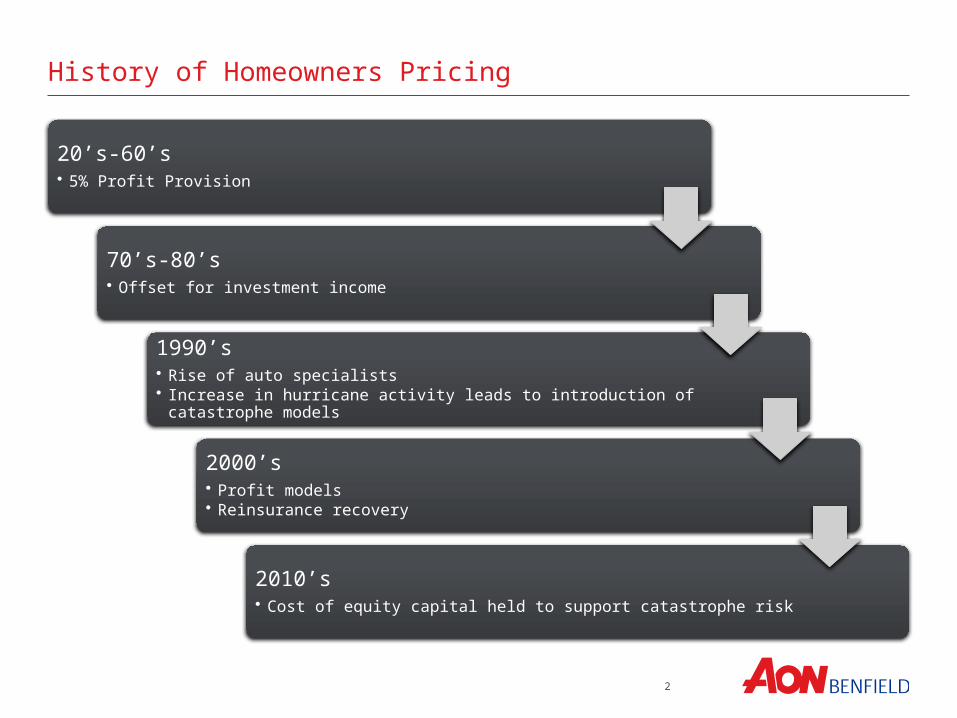

History of Homeowners Pricing

20’s-60’s• 5% Profit Provision

70’s-80’s• Offset for investment income

1990’s• Rise of auto specialists• Increase in hurricane activity leads to introduction of catastrophe models

2000’s• Profit models• Reinsurance recovery

2010’s• Cost of equity capital held to support catastrophe risk

3

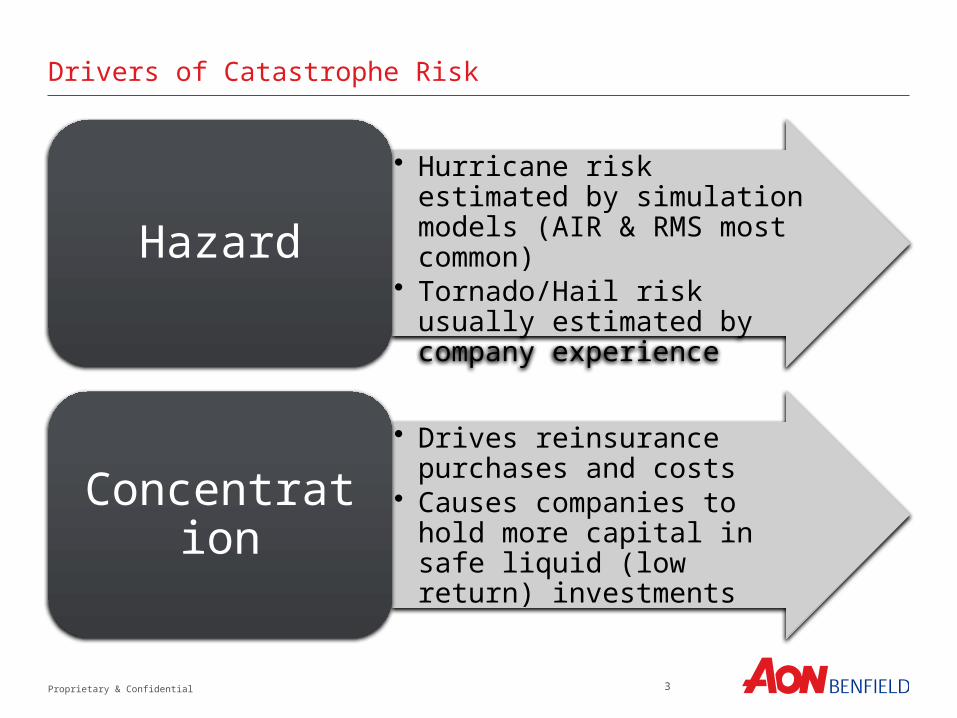

Drivers of Catastrophe Risk

• Hurricane risk estimated by simulation models (AIR & RMS most common)

• Tornado/Hail risk usually estimated by company experienceHazard

• Drives reinsurance purchases and costs

• Causes companies to hold more capital in safe liquid (low return) investmentsConcentration

Proprietary & Confidential

4

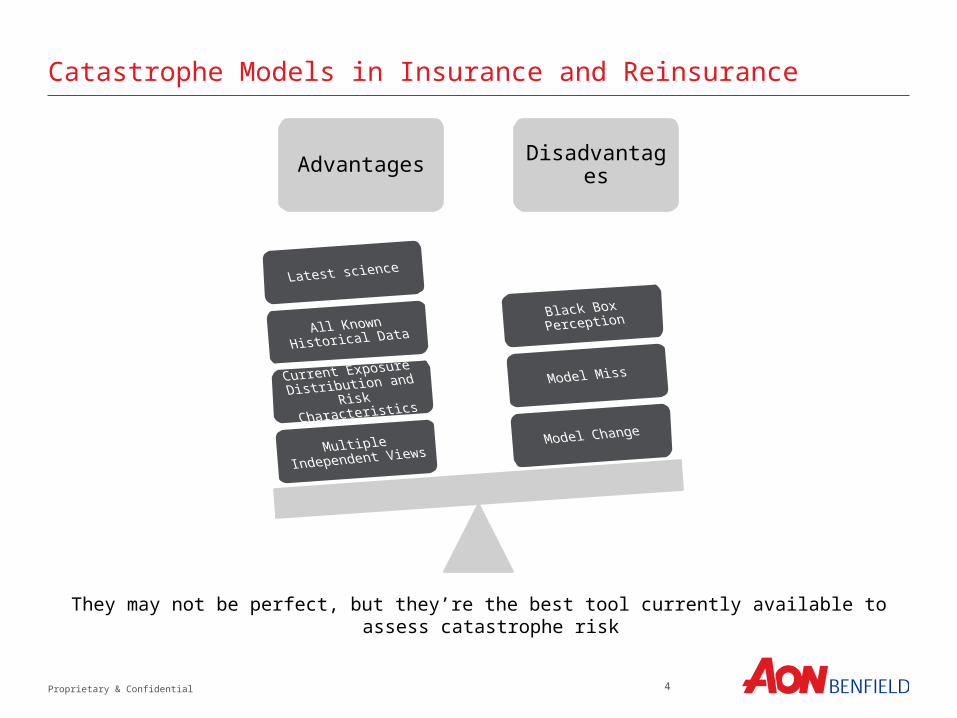

Catastrophe Models in Insurance and Reinsurance

Advantages Disadvantages

Multiple Independent

Views

Current Exposure

Distribution and Risk

Characteristics

All Known

Historical Data

Latest science

Model Change

Model Miss

Black Box Perception

Proprietary & Confidential

They may not be perfect, but they’re the best tool currently available to assess catastrophe risk

5

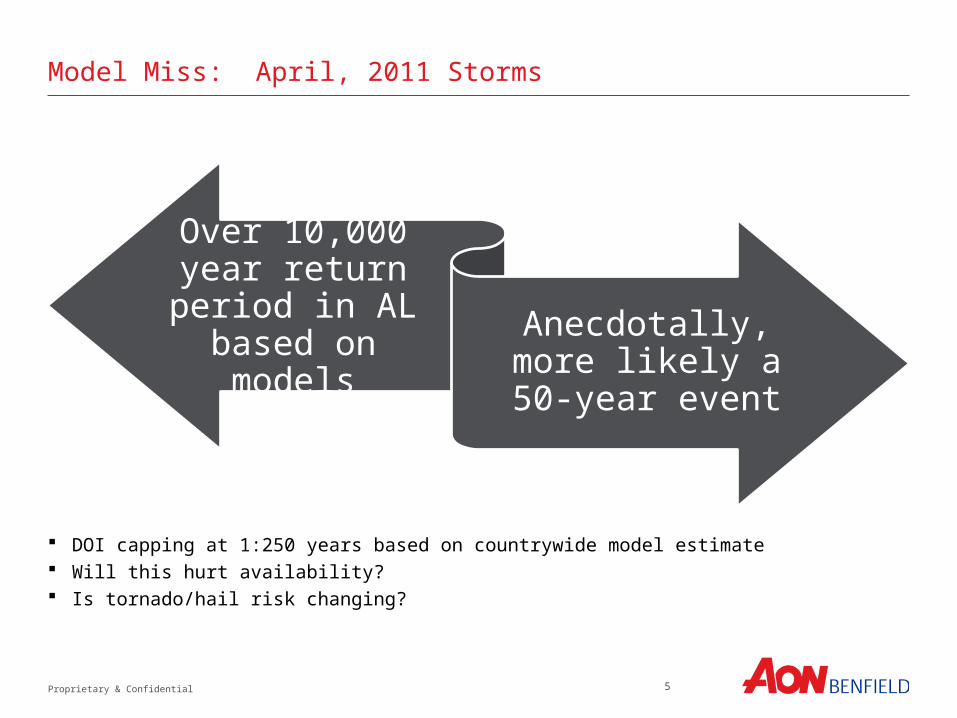

Model Miss: April, 2011 Storms

Over 10,000 year return period in AL based on models Anecdotally, more

likely a 50-year event

Proprietary & Confidential

DOI capping at 1:250 years based on countrywide model estimate Will this hurt availability? Is tornado/hail risk changing?

6

Model Change: RMS Hurricane

Use of multi-model average cuts expected loss reduction in half, to 20% Fixed expenses of 20-30% limit required premium reduction to 14-16% Expected loss from other perils (5-10%) limit required premium reduction to 12-15% Further reduction to reinsurance and capital costs likely, if included in rates and allocated properly Premium reductions realized ONLY if rates were fully adequate based on prior model

“In both Baldwin and Mississippi’s Jackson counties, expected hurricane losses are projected to be more than 40 percent lower under RMS’ new model. That, in turn, could mean an average 34 percent drop in overall premiums in Baldwin County, RMS found.”

AL.com, September 4, 2011

7

Property Cat Excess of Loss Reinsurance

• More insurers• More capacity for each insurer• Makes the market work

Global Pooling of Risk

• Especially for diversifying risk• Sufficient/flexible capacity• Brokers working on behalf of insurers

Competitive Market

• High returns when cat activity is low• Potentially large losses in high activity years

Reasonable Risk-Adjusted Returns

Proprietary & Confidential

8

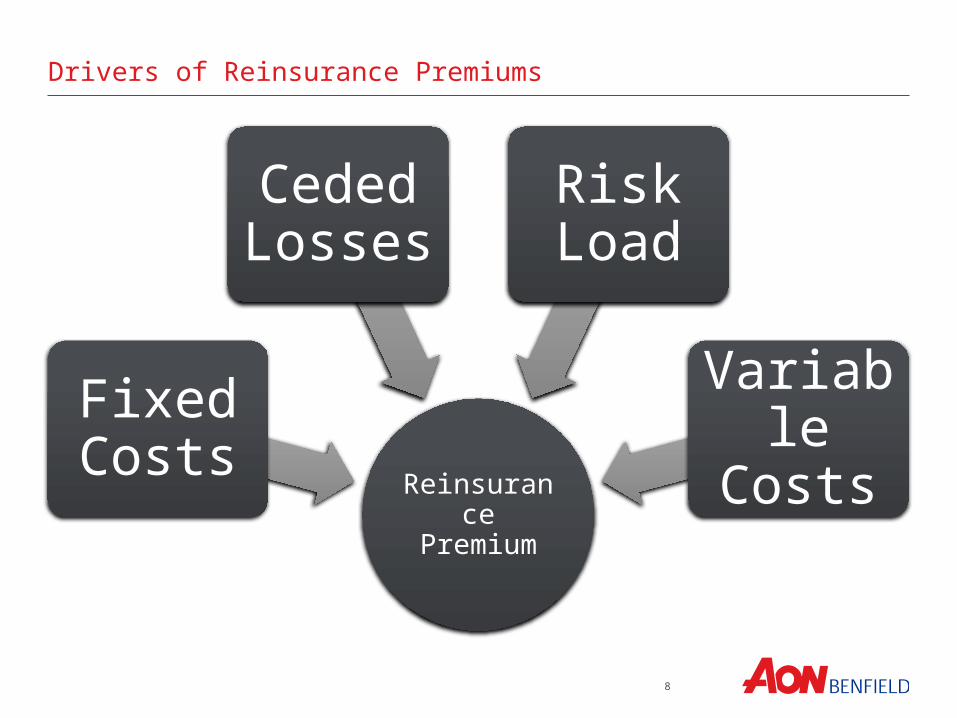

Reinsurance Premium

Fixed Costs

Ceded Losses

Risk Load

Variable Costs

Drivers of Reinsurance Premiums

9

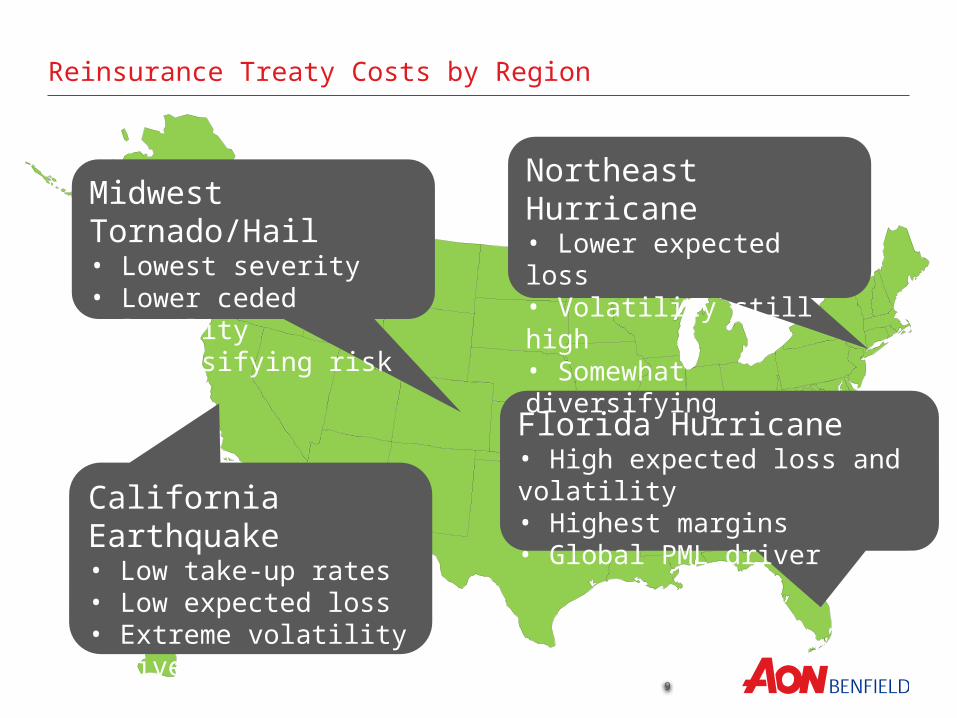

Reinsurance Treaty Costs by Region

Florida Hurricane• High expected loss and volatility • Highest margins• Global PML driver

California Earthquake• Low take-up rates• Low expected loss • Extreme volatility• Diversifying risk

Midwest Tornado/Hail• Lowest severity• Lower ceded volatility• Diversifying risk

Northeast Hurricane• Lower expected loss • Volatility still high• Somewhat diversifying

10

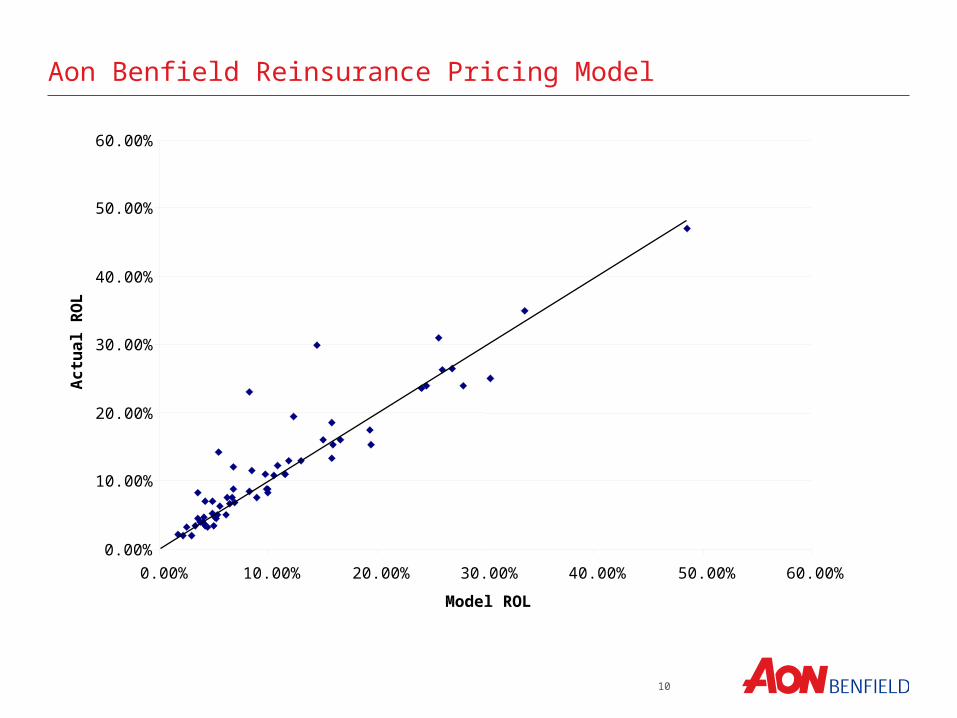

Aon Benfield Reinsurance Pricing Model

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00%

Model ROL

Ac

tua

l R

OL

11

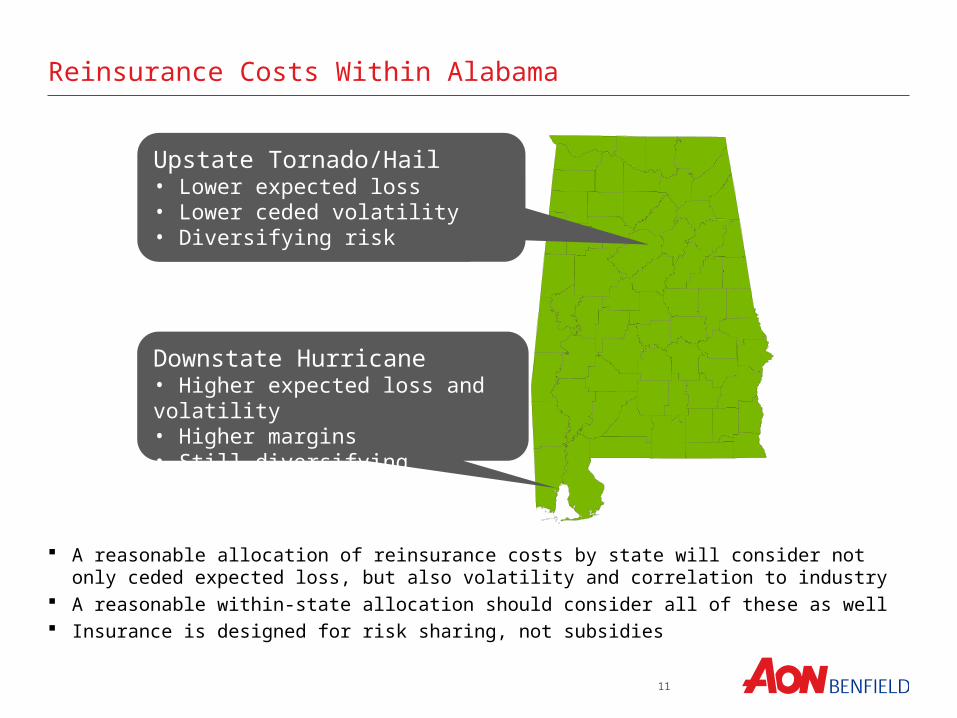

Reinsurance Costs Within Alabama

Upstate Tornado/Hail• Lower expected loss• Lower ceded volatility• Diversifying risk

Downstate Hurricane• Higher expected loss and volatility • Higher margins• Still diversifying

A reasonable allocation of reinsurance costs by state will consider not only ceded expected loss, but also volatility and correlation to industry

A reasonable within-state allocation should consider all of these as well Insurance is designed for risk sharing, not subsidies

12

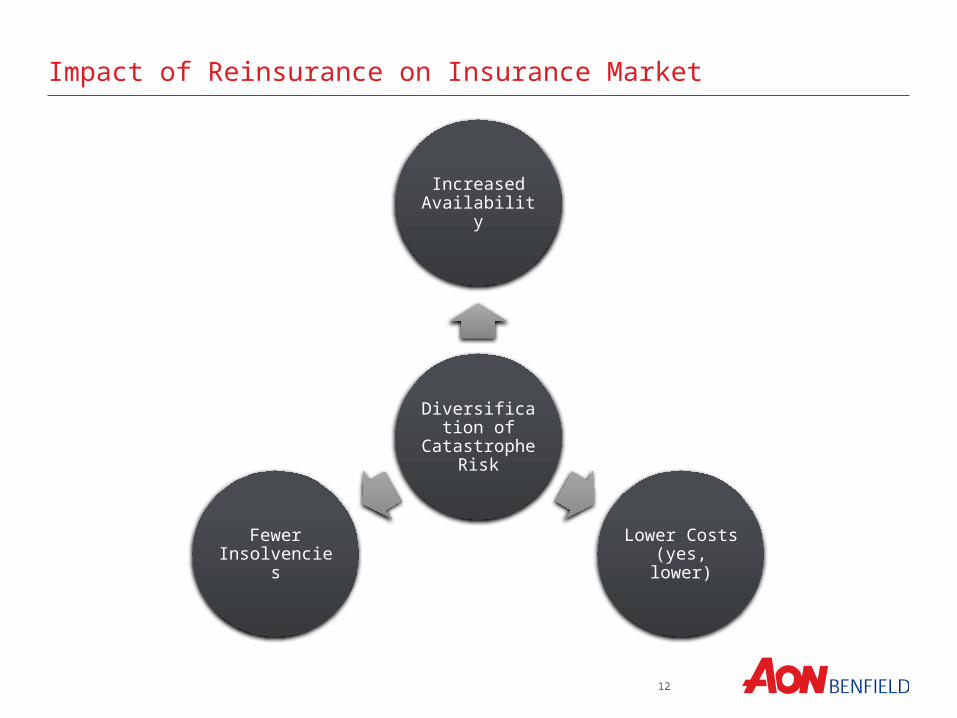

Diversification of Catastrophe Risk

Increased Availability

Lower Costs (yes, lower)Fewer Insolvencies

Impact of Reinsurance on Insurance Market

13

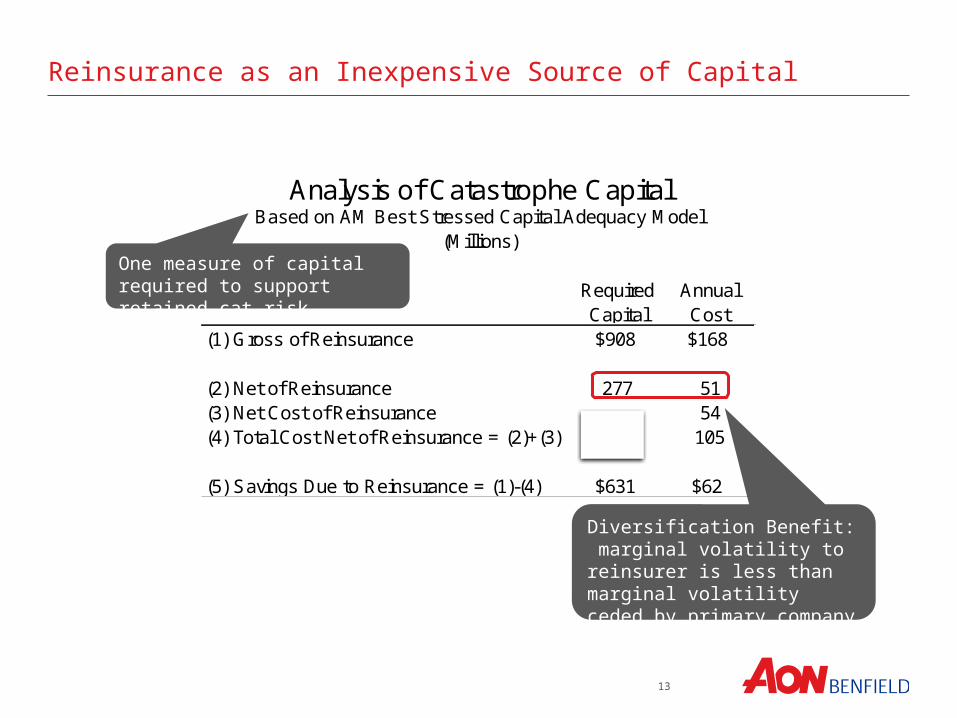

Reinsurance as an Inexpensive Source of Capital

Analysis of Catastrophe CapitalBased on AM Best Stressed Capital Adequacy Model

(Millions)

RequiredCapital

AnnualCost

(1) Gross of Reinsurance $908 $168

(2) Net of Reinsurance 277 51(3) Net Cost of Reinsurance 54(4) Total Cost Net of Reinsurance = (2)+(3) 277 105

(5) Savings Due to Reinsurance = (1)-(4) $631 $62

Diversification Benefit: marginal volatility to reinsurer is less than marginal volatility ceded by primary company

One measure of capital required to support retained cat risk

14

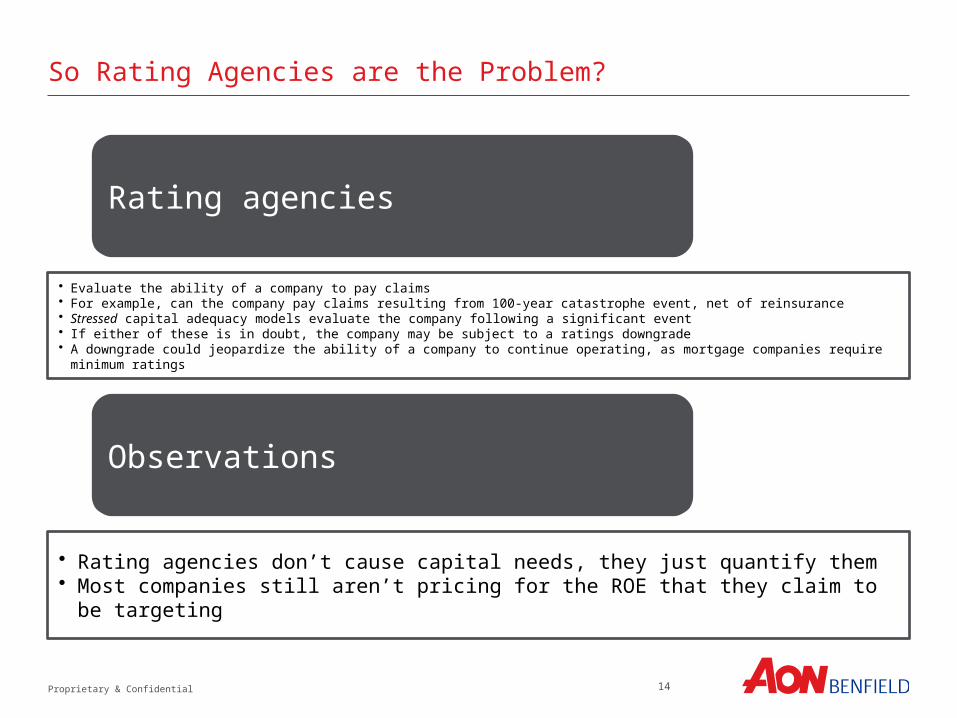

So Rating Agencies are the Problem?

Rating agencies

• Evaluate the ability of a company to pay claims• For example, can the company pay claims resulting from 100-year catastrophe event, net of reinsurance• Stressed capital adequacy models evaluate the company following a significant event• If either of these is in doubt, the company may be subject to a ratings downgrade• A downgrade could jeopardize the ability of a company to continue operating, as mortgage companies require minimum ratings

Observations

• Rating agencies don’t cause capital needs, they just quantify them• Most companies still aren’t pricing for the ROE that they claim to be

targeting

Proprietary & Confidential

15

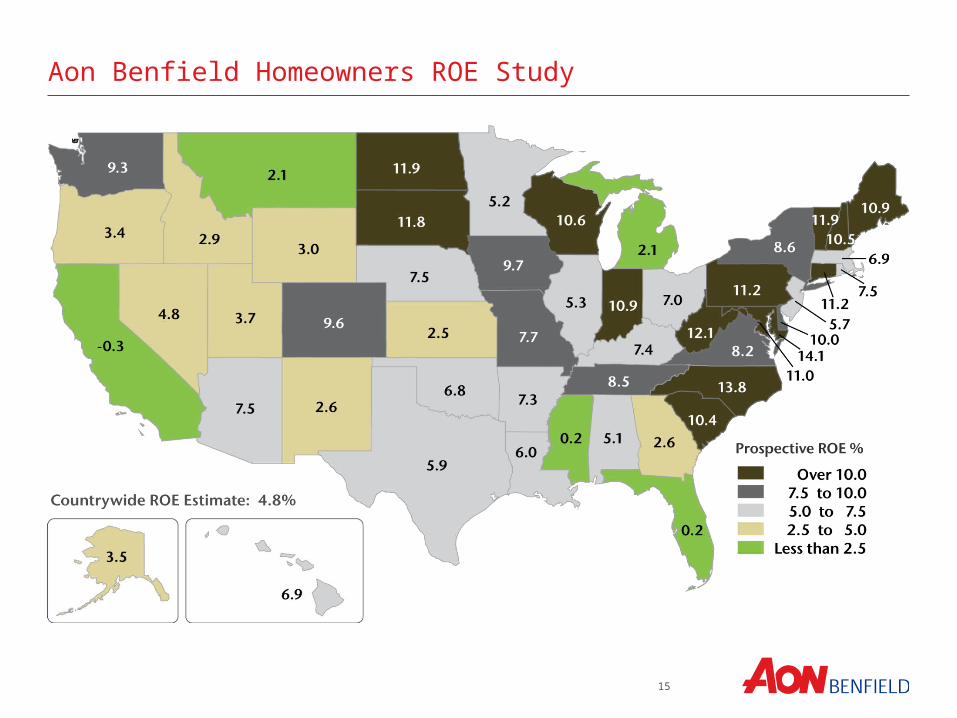

Aon Benfield Homeowners ROE Study

16

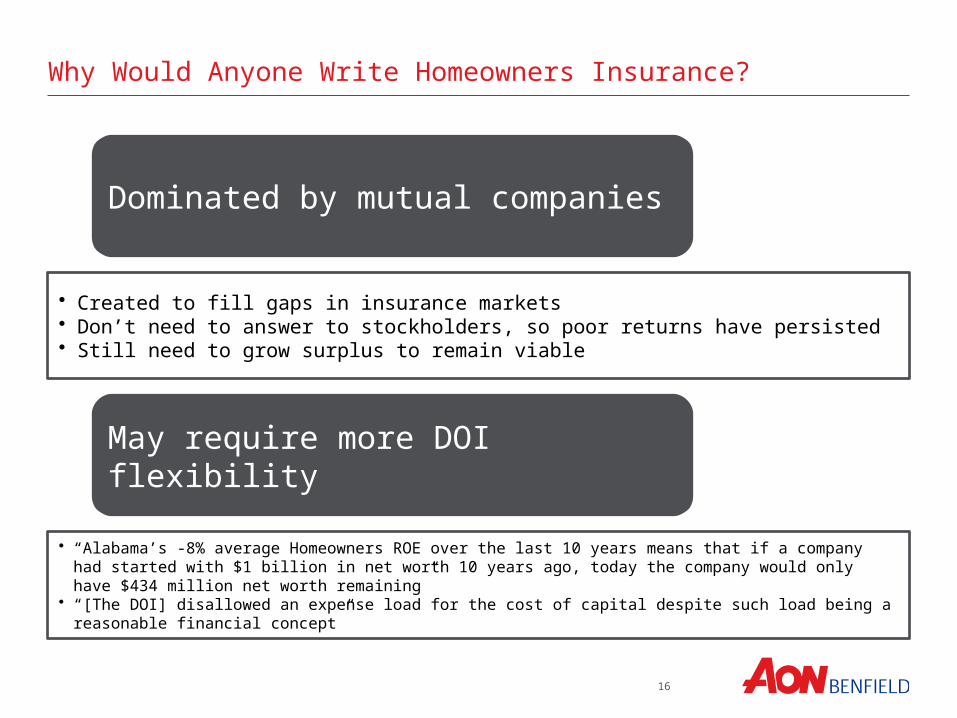

Dominated by mutual companies

• Created to fill gaps in insurance markets• Don’t need to answer to stockholders, so poor returns have persisted• Still need to grow surplus to remain viable

May require more DOI flexibility

• “Alabama’s -8% average Homeowners ROE over the last 10 years means that if a company had started with $1 billion in net worth 10 years ago, today the company would only have $434 million net worth remaining”

• “[The DOI] disallowed an expense load for the cost of capital despite such load being a reasonable financial concept”

Why Would Anyone Write Homeowners Insurance?

17

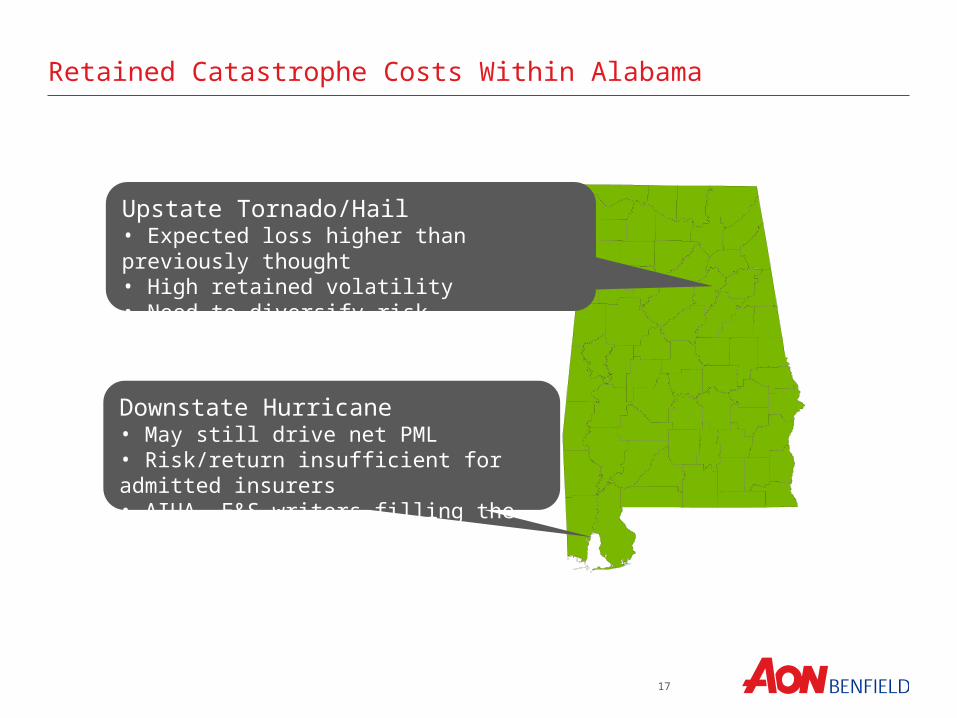

Retained Catastrophe Costs Within Alabama

Upstate Tornado/Hail• Expected loss higher than previously thought• High retained volatility• Need to diversify risk

Downstate Hurricane• May still drive net PML• Risk/return insufficient for admitted insurers• AIUA, E&S writers filling the gaps

18

Concentrations Drive Reinsurance and Capital CostsPeople Tend to Live in Concentrated Areas

The Problem of Concentrations

The April storms woke Alabama insurers to the risk of concentrations, even away from the coast If companies can’t price for tail risk, they will try to reduce it by cutting policies If returns are perceived as adequate, more companies will share the load on the coast and inland The more the risk is spread among different companies, the lower capital needs will be for each

Proprietary & Confidential