regulatory approach to promote micro and small enterprises financial access the peruvian case...

TRANSCRIPT

Regulatory Approach to Promote Micro and Regulatory Approach to Promote Micro and Small Enterprises financial accessSmall Enterprises financial access

The Peruvian caseThe Peruvian case

Fiorella Arbulú DiazFiorella Arbulú Diaz

Superintendency of Banking, Insurance Companies and Pension Superintendency of Banking, Insurance Companies and Pension FundsFunds

Regional Symposium “Best Practice Regulatory Principles Supporting MSME Regional Symposium “Best Practice Regulatory Principles Supporting MSME Access to Finance”Access to Finance”

June, 2011June, 2011

Peruvian socio-economic context

Peru

• Population:

29´475,856 inhabitants

• Area:

1´285,215 km²

• Population density:

23 (/km²)

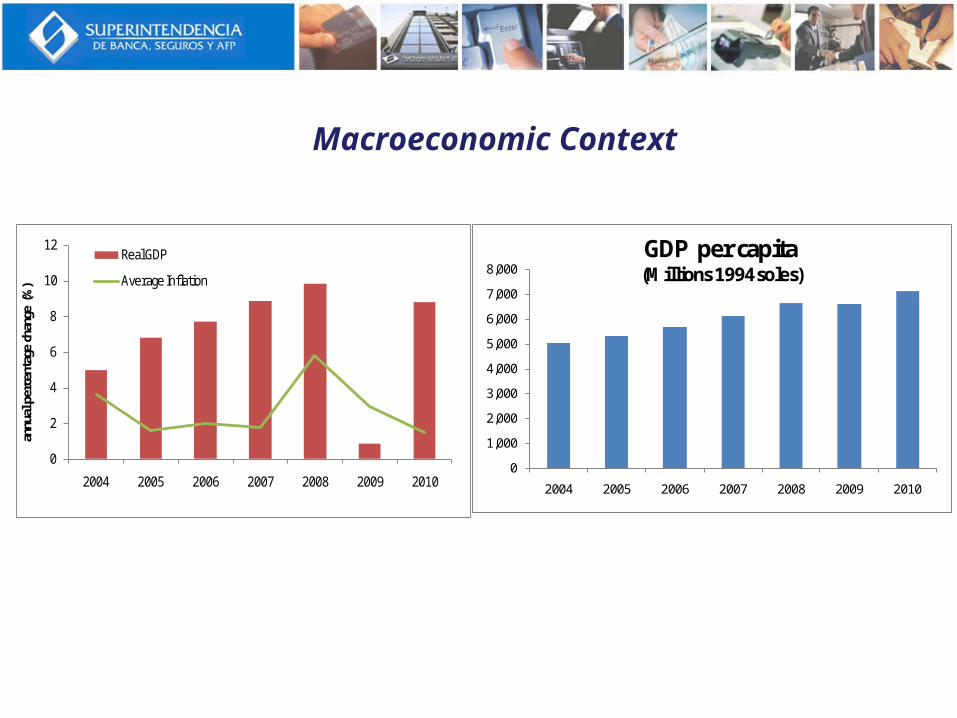

Macroeconomic Context

0

2

4

6

8

10

12

2004 2005 2006 2007 2008 2009 2010

annu

al pe

rcen

tage

chan

ge (%

)

Real GDP

Average Inflation

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2004 2005 2006 2007 2008 2009 2010

GDP per capita(Millions 1994 soles)

0

10

20

30

40

50

60

70

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

54.8 54.3 52.348.6 48.7

44.539.3 36.2 34.8

31.3

Poverty reveals a downward trend in the last decade

Poverty rate

(as a percentage of population)

Source: National Institute for Statistics and Information (INEI)

Peruvian business is predominantly composed by microenterprises. However, a great percentage of these

firms is still within the informal sector

Source: INEI-ENAHO 2007, SUNAT 2007.

Pequeña empresa

1.5%

Mediana y gran empresa

1.4%

Microempresa97.1%

26.7%

73.3%

69.3%

30.7%

27.4%

72.6%

Microempresas Pequeña Empresa MYPE

Composición de la Mype según formalidad tributaria

Informal

Formal

Small Enterprise

Big & Medium Enterprise

Micro Enterprise

Compositon of Small & Micro Business according to taxing formality

Micro Enterprise Small Enterprise SME´s

Peruvian Microcredit Supply

Peruvian Microcredit Supply

March 2011Number of

entitiesMSE loans

(US$ million)

Participation in total gross loans

(%)Non-specialized banks, finance and leasing companies

18 3,416 8.4

MICROFINANCE SYSTEM 38 4,586 74.7Specialized banks and finance companies 5 1,755 87.9Non-banking Microfinance Institutions 33 2,831 68.3

Municipal Savings and Loans Institutions 13 2,080 66.7Rural Savings and Loans Institutions 10 468 70.3Micro & Small Enterprise Development Entities 10 283 79.4

Total Financial System 56 8,002 17.1

The Supply of Microcredit in the Peruvian Financial System

More than 50% of the micro and small enterprise credit supply is explained by specialized institutions

Municipal Savings and

Loans Institutions

26%

Rural Savings and Loans

Institutions6%

Micro & Small Enterprise

Development Entities

3%Specialized banks and

finance companies

22%

Non-specialized banks, finance

and leasing companies

43%

* As of March 2011.

MFI account for more than 70% of micro and small enterprise debtors

Specialized banks and

finance companies

35%

NBMFI47%

Non-specialized

banks, finance and leasing companies

18%

* As of March 2011.

Recent Trends

Micro and Small Enterprise loans have grown significantly

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000D

ec-0

2

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Mic

ro a

nd S

mal

l En

terp

rise

Loa

ns/

Gro

ss lo

ans

(%)

Mic

ro a

nd S

mal

l En

terp

rise

s Lo

ans

Loans (US$ million)% of Gross loans

During the last five years, the number of micro and small clients has notably increased

Source: SBS.

Dec-10

0 500 266 447 181 19.59500 1 000 123 260 138 14.95

1 000 3 000 157 392 235 25.463 000 7 000 67 216 148 16.117 000 10 000 19 68 49 5.3010 000 30 000 23 146 123 13.29

Más de US$ 30 000 1 50 49 5.29Total 656 1 578 922 100.00

Number of borrowers according to debt size

Range(US$)

Var. Dec10/ Dec05

N° borrowers %Dec-05

N° borrowers

Microcredit interest rates have experienced a downward trend

MFI: Interest rate for microcredits and consumption loans granted in domestic currency

(In percentage)

10

20

30

40

50

60

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

MFI: Interest rate for microcredit granted in local currency

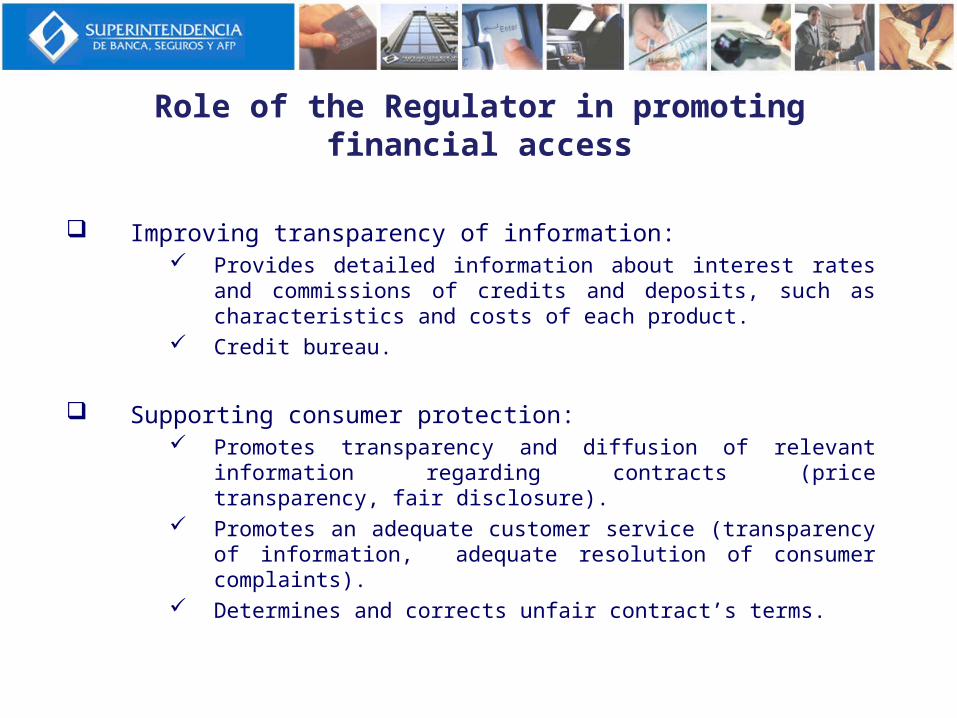

Role of the Regulator in promoting greater access to financial

markets

Improving transparency of information: Provides detailed information about interest rates and

commissions of credits and deposits, such as characteristics and costs of each product.

Credit bureau.

Supporting consumer protection: Promotes transparency and diffusion of relevant information

regarding contracts (price transparency, fair disclosure). Promotes an adequate customer service (transparency of

information, adequate resolution of consumer complaints). Determines and corrects unfair contract’s terms.

Role of the Regulator in promoting financial access

Improving the regulatory and supervisory framework: Municipal Savings and Loan Institutions were allowed to

operate in other regions (even in the Capital). SBS expands the operations undertaken by non-banking

institutions. Currently, NBMFI are allowed to offer factoring, leasing, rebates, financial consulting.

Additionally, services of non-banking microfinance institutions were expanded by allowing greater access to capital markets.

Improves prudential regulation.

Promoting the use of new technologies to deliver financial services at lower costs:

Improves financial outreach through banking agents (from 1,689 to 9,204 banking agents in the last years).

Relaxes anti money-laundering conditions for the use of agents to open deposits.

Promotes mobile phone banking (E-money law proposed).

Role of the Regulator in promoting financial access

Promoting financial literacy: SBS has launched a financial literacy program for training

school teachers about the financial and insurance systems and pension funds (in coordination with the Ministry of Education).

Virtual classroom available online.

Role of the Regulator in promoting financial access

Microfinance Regulation

Regulatory Framework for Microfinance Institutions

Equal regulatory treatment to all financial institutions:

General Law of the Financial and Insurance Systems (Law N° 26702).

Rules for evaluation and classification of debtor (SBS Resolution N° 11356-2008).

No special treatment for Microfinance Intitutions (create a level playing field).

Regulation of microfinance activity instead of regulation of microfinance institutions.

Credit Types

(*) Effective since July 2010.

Credit Types Criteria to define

Corporate Sales higher than US$/ 71 MMBig enterprise Sales from US$ 7 MM to US$ 71 MMMedium enterprise Debt higher than US$ 109 MSmall enterprise Debt from US$ 7 M to 109 MMicro enterprise Debt lower or equal to US$ 7 MRevolving Consumer Up to US$ 109 MNo Revolving Consumer Up to US$ 109 MReal estate Not applicable

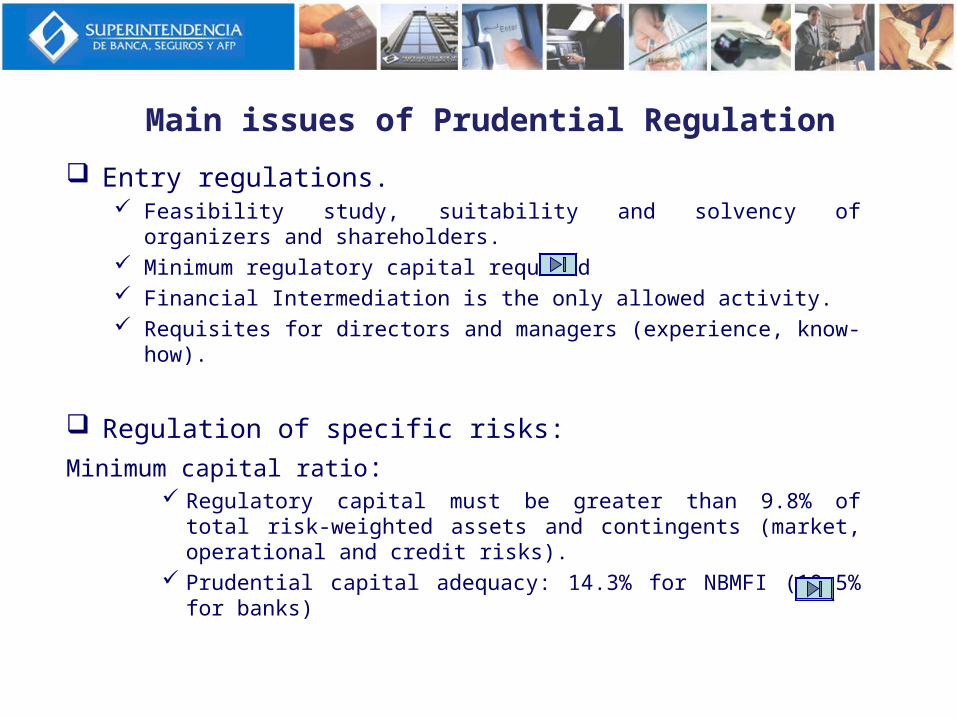

Main issues of Prudential Regulation

Entry regulations. Feasibility study, suitability and solvency of organizers and

shareholders. Minimum regulatory capital required Financial Intermediation is the only allowed activity. Requisites for directors and managers (experience, know-how).

Regulation of specific risks:Minimum capital ratio:

Regulatory capital must be greater than 9.8% of total risk-weighted assets and contingents (market, operational and credit risks).

Prudential capital adequacy: 14.3% for NBMFI (10.5% for banks)

Main issues of Prudential Regulation

Credit risk: Debtor classification and loan-loss provisions based on loan

status procyclical provisions Rules for managing over-indebtedness risk of retailer borrowers

(SBS Resolution N° 1237-2006).

Liquidity risk: Minimum requirements of liquidity ratios: National currency 8%,

Foreign currency 20% Reporting requirements of assets and liabilities mismatching, by

maturity, under regular and stress scenarios and a contingency funding plan.

Main issues of Prudential Regulation

Market risk:Adequate administration systems of market riskLimits for foreign exchange risk exposure: Long net position < 60% of capital, Short net position < 15% of capital.

Operational risk:Adequate administration systems of operational RiskSpecific regulation to manage technology risk Information Safety PlanBusiness Continuity Plan to ensure an acceptable level of operation of critical processes in case major internal or external failures occur.

Thank You

www.sbs.gob.pe

Entry Regulation

Minimum Capital requirement for entryApril- June 2011

Type of Institution US$ million

Banking entities 8.74Financial entities 4.39Municipal Savings and Loan Institutions 0.40Rural Savings and Loan Institutions 0.40Micro & Small Enterprise Development Entities 0.40

Minimum Capital Ratio

Capital ratio exceeds international standards and prudential requirements

Microfinance System Equity and Capital Ratio

9.8%

8%

0

200

400

600

800

1,000

1,200De

c-05

Mar

-06

Jun-

06Se

p-06

Dec-

06M

ar-0

7Ju

n-07

Sep-

07De

c-07

Mar

-08

Jun-

08Se

p-08

Dec-

08M

ar-0

9Ju

n-09

Sep-

09De

c-09

Mar

-10

Jun-

10Se

p-10

Dec-

10

Equi

ty (m

ill.$

)

0

5

10

15

20

25

Cap

ital r

atio

(%)

Equity (Mill. US$) MFI Capital Ratio (%)

Banking Law Minimum Requirement (%) International Standard (%)

Credit Risk Regulation

Debtor risk rating according to the number of days overdue

Normal 0 8 30With Potential Problems 60 30 60Deficient 120 60 120Uncertain 365 120 365Loss +365 +120 +365

Risk Category

Micro and Small Enterprise and

ConsumerMortgage

Type of CreditCorporate, Medium

and Large Enterprise

MFI liquidity ratios remain well above the minimum required by regulation

Microfinance System Liquidity Ratio(In percentage)

0

10

20

30

40

50

60

Dec

-05

Mar

-06

Jun-

06

Sep-

06

Dec

-06

Mar

-07

Jun-

07

Sep-

07

Dec

-07

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Domestic currency Foreign currency

Minimun ratio (foreign currency): 20%

Minimun ratio (domestic currency): 8%