regulation of credit providers and finance brokers

TRANSCRIPT

Regulation of Credit Providers and Finance Brokers

Updated 4 November 2008

Contents

Part 1

- Registration and licensing requirements – finance brokers

Part 2

- Registration and licensing requirements – credit providers

Part 3

- Specific legislative requirements for finance brokers

Part 4

- Australian Financial Services licences

Part 5

- Disclosure of commission – industry rules

Part 6

- Finance Brokers Control Act (WA)

Part 7

- WA Credit Provider Licensing

Part 8

- Door to Door Sales legislation

Part 9

- The Hawking Provisions in the Corporations Act

Part 10

- eMarketing Code of Practice including the SPAM Act

Part 11

Financial Sector (Collection of Data) Act

This information is provided as a general guide. Neither the MFAA nor Gadens Lawyers accept responsibility for people relying on this guide.

Brokers should also read the MFAA modules dealing with the Privacy Act, the Anti-Money Laundering and Counter-Terrorism Financing Act, Finance Broking Contracts, and Australian Financial Services Licensing.

2

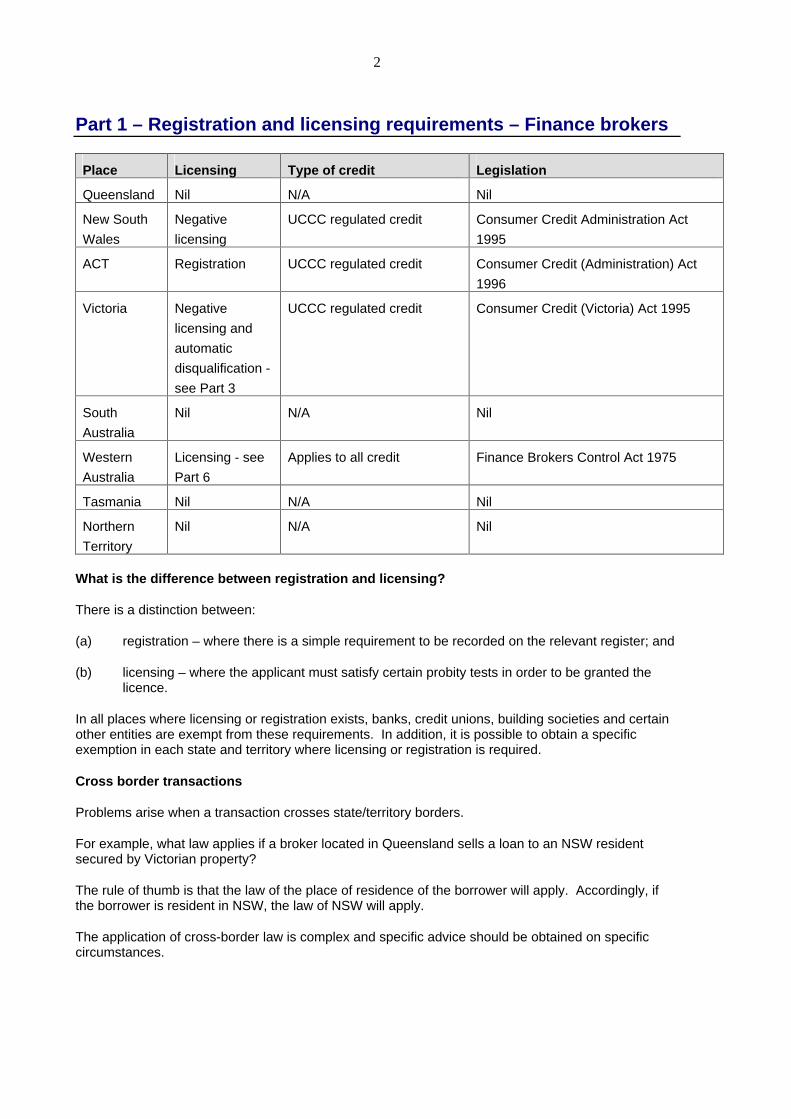

Part 1 – Registration and licensing requirements – Finance brokers

Place Licensing Type of credit Legislation

Queensland Nil N/A Nil

New South

Wales

Negative

licensing

UCCC regulated credit Consumer Credit Administration Act

1995

ACT Registration UCCC regulated credit Consumer Credit (Administration) Act

1996

Victoria Negative

licensing and

automatic

disqualification -

see Part 3

UCCC regulated credit Consumer Credit (Victoria) Act 1995

South

Australia

Nil N/A Nil

Western

Australia

Licensing - see

Part 6

Applies to all credit Finance Brokers Control Act 1975

Tasmania Nil N/A Nil

Northern

Territory

Nil N/A Nil

What is the difference between registration and licensing?

There is a distinction between:

(a) registration – where there is a simple requirement to be recorded on the relevant register; and

(b) licensing – where the applicant must satisfy certain probity tests in order to be granted the licence.

In all places where licensing or registration exists, banks, credit unions, building societies and certain other entities are exempt from these requirements. In addition, it is possible to obtain a specific exemption in each state and territory where licensing or registration is required.

Cross border transactions

Problems arise when a transaction crosses state/territory borders.

For example, what law applies if a broker located in Queensland sells a loan to an NSW resident secured by Victorian property?

The rule of thumb is that the law of the place of residence of the borrower will apply. Accordingly, if the borrower is resident in NSW, the law of NSW will apply.

The application of cross-border law is complex and specific advice should be obtained on specific circumstances.

3

What is negative licensing?

A negative licensing scheme means that an order may be granted prohibiting a person from conducting the business of a credit provider or finance broker. There are no clear guidelines as to when such an order will be made, and no relevant history of any orders being made.

This arrangement is known as negative licensing because, although there is no positive obligation to obtain a licence or register, if a credit provider or finance broker acts improperly, it can be prevented from conducting business much in the same way as if it had been deleted from a register or had a licence forfeited.

Other legislation

Remember, in addition to licensing and registration regimes, finance brokers are subject to other laws, including in particular:

Trade Practices Act, ASIC Act, and Fair Trading Act – must not act in a misleading and deceptive fashion or unconscionably;

UCCC – use comparison rates and comparison rate schedules where required;

Privacy Act;

Industry codes of conduct (eg. MFAA’s code of practice);

Door to Door Trading Acts - see Part 8;

The hawking prohibitions in the Corporations Act – see Part 9;

e-marketing Code of Conduct - see Part 10;

the Spam Act - see Part 10.

"Debt Collector's Licence".

Debt collectors licence

All states and territories except ACT license people who conduct the business of commercial and private enquiry agents. This includes carrying on the business of debt collection.

Debt collection is defined in the Commercial Agents and Private Inquiry Agents Act 2004 (NSW) as "an activity carried out by a person on behalf of a second person (not being his/her employer) in the exercise of the second person's rights under a debt owed by a third person". The definition is similar in legislation of other places. The relevant legislation is Property Agents and Motor Dealers Act 2000 (Qld), Commercial Agents and Private Inquiry Agents Act 2004 (NSW), Private Agents Act 1966 (Vic), Security and Investigations Agents Act 2002 (Tas), Security and Investigation Agents Act 1995 (SA), Debt Collectors Licensing Act 1964 (WA), and Commercial and Private Agents Licensing Act 1979 (NT)

There is potential for a mortgage manager to fall within this definition because mortgage managers collect debts on behalf of a third party, namely the lender.

Generally mortgage managers are not licensed under this Act in the same way as real estate agents who collect rental are not licensed under this Act. This is because the legislation is intended to regulate people whose predominant business is debt collection.

Mortgage managers who do not hold themselves out as providing a stand alone service of debt collecting and collect debts only as an ancillary function of mortgage management will not be "carrying on the business" of debt collecting.

4

Requirements for finance broking contracts (“FBC”)

Place Requirements

NSW UCCC regulated loans only. FBC required with the borrower irrespective of who pays commission. No limits on commission amounts. (Consumer Credit Administration Act 1995).

Vic UCCC regulated loans only. Although the law appears to require an FBC only when the borrower pays the commission, Consumer Affairs Victoria considers an FBC is required to be entered with the borrower irrespective of who pays commission. The MFAA agrees to encourage its members to comply with that view. No limits on commission amounts. (Consumer Credit (Victoria) Act 1995).

ACT UCCC regulated loans only. An FBC is required only with the person paying the commission. Where only the lender is paying commission, the FBC is comprised in the Origination Agreement and no FBC is required with the borrower.

There are limits on commissions – see later detailed information. (Consumer Credit (Administration) Act 1996).

WA Applies to all loans, not just UCCC regulated loans. From 29 June 2007, an FBC is required with the borrower irrespective of who pays commission. The WA Finance Brokers Supervisory Board (prior to its undertaking being moved to DOCEP) considered that fees charged to borrowers in budget management/wealth creation/debt reduction plans are “so integrally and intimately connected with” arranging the loan, that fees charged for these services are fees charged for negotiating and arranging the loan. Accordingly, commission maximums, and requirements for FBCs will apply.

There are limits on commissions – see later detailed information.

SA No requirement to have an FBC as such, but the Criminal Law Consolidation Act requires benefits received by a fiduciary (which will normally include a finance broker) to be disclosed including:

(a) the nature of the benefit;

(b) the value (or approximate value) of the benefit; and

(c) the identity of the third party from whom the benefit has been or is to be received.

This obligation to make disclosure is most conveniently effected by having an FBC.

The MFAA recommends that brokers enter a finance broking contract (”FBC”) with borrowers and disclose commissions and other benefits in all cases (ie even though the loan is not UCCC regulated, the borrower is paying no commission, and there is no legislative requirement to do so).

In addition brokers should get a privacy consent to allow the broker (as distinct from the lender) to use and collect personal information regarding the customer, and which also allows the broker to pass on information to appropriate investigatory bodies if necessary. Brokers should also provide a statement which describes the services the broker provides (eg whether the broker provides advice or is simply selling loans).

5

Part 2 - Registration and licensing requirements – credit providers

Place Licensing Type of credit Legislation

Queensland Negative

licensing

UCCC regulated credit Consumer Credit (Queensland) Act

1994

New South

Wales

Negative

licensing

UCCC regulated credit plus

loans for investment in housing

Consumer Credit Administration Act

1995

ACT Registration UCCC regulated credit Consumer Credit (Administration) Act

1996

Victoria Registration UCCC regulated credit Consumer Credit (Victoria) Act 1995

South

Australia

Negative

licensing

UCCC regulated credit Credit Administration Act 1995

Western

Australia

Licensing UCCC regulated credit. See

further information in Part 6.

Credit (Administration) Act 1984

Tasmania Nil N/A Nil

Northern

Territory

Negative

licensing

UCCC regulated credit Consumer Affairs and Fair Trading Act

Part 12

Additional regulation

Remember, in addition to licensing and registration regimes, credit providers are subject to other laws including in particular:

Trade Practices Act, ASIC Act, Fair Trading Acts, and in NSW Contracts Review Act – must not act in a misleading and deceptive fashion or unconscionably;

UCCC – use comparison rates and comparison rate schedules where required;

Privacy Act;

Industry codes for conduct (eg. MFAA’s code of practice);

Door to Door Trading Acts - see Part 8;

The hawking prohibitions in the Corporations Act – see Part 9;

e-marketing Code of Conduct - see Part 10;

the Spam Act - see Part 10; and

the Financial Sector (Collection of Data) Act (Cth) – see Part 11.

Queensland

The Consumer Credit (Queensland) Act establishes a regime of negative licensing for credit providers (ie a lender of UCCC regulated credit or a lender of home loan investment credit).

Under s19 if a credit provider has repeatedly engaged in unjust conduct in the course of a credit business, the credit provider can be asked to execute a Conduct Deed, or an application can be made to court to restrain the conduct. Further, under s23 a court can prohibit a person from providing

6

consumer credit or restrict the way in which a person can provide consumer credit if the court considers the person is not appropriate to provide that service taking into account any breach of the UCCC, convictions for dishonesty, conducting a business dishonestly or unfairly, the reopening of a credit contract under s70 or s72, or a breach of a Conduct Deed.

Unjust conduct is defined (rather unhelpfully) as dishonest or unfair conduct for breaching any provision of the UCCC.

It is very rare for any action to be taken under these provisions.

New South Wales

The Consumer Credit (Administration) Act establishes a regime of negative licensing for credit providers (ie a lender of UCCC regulated credit).

Under s17 if a credit provider has engaged in unjust conduct in the course of a credit business, the credit provider can be asked to execute a Deed containing undertakings as to discontinuing the unjust conduct, its future conduct, or the action it will take in rectifying its unjust conduct. Further, under s19 a court can prohibit a person from providing consumer credit or restrict the way in which a person can provide consumer credit.

Unjust conduct is defined (rather unhelpfully) as dishonest or unfair conduct for breaching any provision of the UCCC.

It is very rare for any action to be taken under these provisions.

Northern Territory

The Consumer Affairs and Fair Trading Act establishes a regime of negative licensing for credit providers (ie a lender of UCCC regulated credit).

Under s227 if a credit provider has engaged in unacceptable activity in the course of a credit business, the credit provider can be asked to execute a Deed of Assurance containing undertakings as to discontinuing the unjust conduct, its future compliance with the Act or the UCCC, or the action it will take in rectifying its unjust conduct. Further, under s231 a court can prohibit a person from providing consumer credit or restrict the way in which a person can provide consumer credit.

Unacceptable activity is defined as conduct that is improper, negligent or unfair.

It is very rare for any action to be taken under these provisions.

7

Part 2A -State unique credit provisions

NSW, ACT and QLD – cap on cost of interest rates and fees

The aggregate of interest and fees and charges payable under UCCC regulated contracts must not exceed 48% per annum. Credit fees and charges do not include enforcement expenses, but include default fees. These provisions are contained in the Consumer Credit (New South Wales) Act, the Consumer Credit Act (ACT) and the Consumer Credit (Queensland) Act.

There is an exemption for fees and charges relating to temporary credit facilities provided in relation to an existing credit or debit account (eg overdrafts and short term excesses) established by an authorised deposit taking institution (“ADI” - eg banks, building societies, and credit unions).

In NSW a Statement of Regulatory Intent dated 19 April 2006 makes it clear that although fees and charges must be taken into calculation in determining whether the cap has been breached, there is no need to show this aggregate rate in the credit contract - ie the interest rate and fees and charges can still be shown separately.

Victoria - cap on interest rates

A UCCC regulated credit contract is unenforceable if the interest rate exceeds 48% per annum. Any mortgage which relates to a UCCC regulated contract is void if the interest rate exceeds 30% per annum. There is no cap on fees and charges. These provisions are contained in s.39 and s.40 of the Consumer Credit (Victoria) Act.

Early repayment cost exceeding cap

Sometimes a borrower under even a “standard” credit contract will be paying more than these limits if the borrower repays early (eg the combination of establishment and repayment fees may push the effective rate over these limits). This will not breach these laws because the borrower is not obliged to pay in excess of these maximums -- rather the cap is breached as a result of a voluntary act of the borrower repaying early.

Victoria – Actions by Director of Consumer Affairs and class actions

What actions can the Director take?

Under provisions introduced by the Consumer Credit (Victoria) and Other Acts Amendment Act 2008, the Director of Consumer Affairs (the Director) may take or defend proceedings brought by or against a debtor, mortgagor, guarantor, or lessee under a consumer lease in respect of any "consumer credit matter".

A "consumer credit matter" means any matter in respect of which proceedings may be brought under the UCCC or under Division 5 of Part 4A of the Consumer Credit (Victoria) Act 1995 relating to regulation of finance brokers.

The Director must be satisfied that:

(a) the consumer has a good cause of action or a good defence; and

(b) it is in the public interest (our bolding) to institute, continue or defend the proceedings.

The Director can represent:

(a) individuals, provided they have consented in writing; or

(b) groups – ie take a class action on behalf of seven or more people.

The Director can settle proceedings, enforce judgments, and can be liable for, or recover, costs.

8

Actions under the UCCC

The Director can take or defend any action that a consumer resident in Victoria could take or defend under the UCCC.

This section has significant implications for the mortgage industry because it allows the Director to take action in respect of virtually any matter relating to a credit contract. For example, action to vary or annul a contract could be taken on the basis that the contract is unjust (s.70), or to review unconscionable changes to interest rates, establishment fees, or early termination fees (s.72).

Consumers have always been able to take these actions, but there has been some doubt about whether class actions can be taken.

It will be interesting to see how this new power is exercised. This is certainly a "shot over the bows" of lenders who engage in dubious practices, and opens the risk of greater court challenge.

ACT - Assess ability to repay – credit cards only

Section 28 of the Fair Trading Act (ACT) makes it an offence in ACT for a credit provider to enter a continuing credit contract for a credit card or increase the limit under a continuing credit contract for a credit card without making a satisfactory assessment process. A continuing contract is an interest only come and go facility (like most credit cards and Line of Credit products).

A satisfactory assessment process is defined to mean that the credit

provider

must ask the debtor for a statement of the debtor's financial situation, including:

income; and

all credit accounts and applicable limits and balances; and

repayment commitments; and

and the credit provider must take the statement into account in making the assessment.

This provision may impact mortgage lenders who provide a credit card attached to their loans, however it is unclear whether a card attached to a mortgage product is provided pursuant to a continuing credit contract for a credit card – the contract is arguably for a mortgage loan.

Cross border transactions generally

Problems arise when a transaction crosses state/territory borders.

For example, what law applies if a lender located in Queensland sells a loan to an NSW resident secured by Victorian property?

The rule of thumb is that the law of the place of residence of the borrower will apply. Accordingly, if the borrower is resident in NSW, the law of NSW will apply.

The application of cross-border law is complex and specific advice should be obtained on specific circumstances.

9

Part 2B –Proposals for Commonwealth take over of the regulation of credit and finance brokers

Phase One

Phase one legislation to be in place by mid 2009. Key elements of the Phase One Action Plan will

include:

enacting the existing State legislation, the Uniform Consumer Credit Code (UCCC), into

Commonwealth legislation;

establishing a national licensing regime to require providers of consumer credit and credit-related

brokering services and advice to obtain a licence from ASIC;

extending the powers of the Australian Securities and Investment Commission (ASIC) to be the

sole regulator of the new national credit framework with enhanced enforcement powers;

requiring licensees to observe a number of general conduct requirements including responsible

lending practices;

requiring mandatory membership of an external dispute resolution (EDR) body by all providers of

consumer credit and credit-related brokering services and advice;

extending the scope of credit products covered by the UCCC to regulate the provision of

consumer mortgages over residential investment properties;

extending the operation of the Corporations Act to regulate margin lending;

regulation of trustee corporations.

Phase Two

Phase Two legislation to be in place by mid 2010. Key elements of the Phase Two Action Plan will

include:

enhancements to specific conduct obligations to stem unfavourable lending practices, such as a

review of credit card limit extension offers, an examination of State approaches to interest rate

caps; and other fringe lending issues as they arise.

sydney melbourne brisbane perth adelaide port moresby

10

5038568 JAD KQW

regulation of the provision of credit for small businesses;

regulation of investment loans other than margin loans and mortgages for residential investment

properties;

reform of mandatory comparison rates and default notices;

enhancements to the regulation and tailored disclosure of reverse mortgages;

examination of remaining existing State and Territory reform projects.

The Government will conduct continued consultation with industry, the community and the States and

Territories to inform the implementation of the action plan.

The final legislation may differ from this outline.

11

5038568 JAD KQW

Part 3 – Specific legislative requirements for finance brokers

New South Wales

The Consumer Credit Administration Act 1995 requires finance brokers negotiating UCCC regulated credit to enter a written finance broking contract (“FBC”) with the borrower and disclose commission, irrespective of who is paying the commission. Details of these requirements are available in a separate document titled “Finance Broking Contracts NSW – Practice Module”.

Details of these requirements are available in a separate document titled “Finance Broking Contracts NSW – Practice Module”.

The MFAA site provides sample finance broking contracts. There is also a version which is suitable for use in all states and territories.

A finance broker must not demand, receive or accept any commission from a client prior to "securing" the credit – see section 4D. We think that means approval not drawdown.

Under section 4I, a finance broker can collect prior to securing the credit:

valuation fees if paid to the valuer, the lender, or someone authorised to instruct the valuer; and

credit application fees or credit establishment fees if paid to the lender or someone who is authorised to act on behalf of the lender and who will incur the costs of determining the application for credit, or the initial administrative costs of providing the credit, or both.

Australian Capital Territory

Summary – Consumer Credit (Administration) Act

1. Applies only to UCCC regulated credit - s.3.

2. Finance brokers must be registered - s.32. This applies to brokers arranging UCCC regulated loans for individuals and strata corporations that are resident in ACT.

3. A finance broker must not publish an advertisement without specifying the name under which it is registered and the address of its place of business - s.33.

4. Maximum commission prescribed - s.35(2). The maximum commission which may be charged or received from a borrower is the greater of:

(a) in respect of the first $5,000 of the credit, not more than 2% plus GST;

(b) in respect of the portion of the loan exceeding $5,000, not more than 1.5% plus GST; or

(c) $6.50 plus GST (see s.35 and regulation 4).

There is no limit on the commission that can be charged to or paid by lenders.

5. FBC required only with the person paying the commission. Where only the lender is paying commission, the FBC is comprised in the Origination Agreement and no FBC is required with the borrower - s.35(1).

6. No commission may be received from the borrower unless the credit is "secured" – we think that means approval not draw down – s.35(3).

12

5038568 JAD KQW

7. Penalties apply for breach, and brokers may be unable to recover their commission.

8. Advertisements - section 33 provides that a finance broker must not publish an advertisement without specifying the name under which it is registered and the address of its place of business. This restriction is impractical and is largely ignored by national operators whose newspaper, television and radio advertisements will be available in ACT.

Who needs to be registered?

Generally, each business will need to be registered, because the finance broker must conduct the finance broking business in the registered name.

Employees who work under the brand and control of their employer will not need to be separately registered. There is doubt, however, regarding the position of contractors (as distinct from employees) who work solely under the brand and control of a single business. There is no express provision in the ACT legislation dealing with contractors.

On one view, if Big Broker operates through contractors who trade as Big Broker and are under the bona fide control of Big Broker, the contractors will be covered by Big Broker’s registration. On the other hand, if sub contractors trade under their own name, they will need their own licence.

In June 2005, the ACT Commissioner of Fair Trading released a statement indicating that generally contractors will be required to have their own registration. Brokers operating as contractors will need to consider their structure carefully to determine whether separate registration is required and if in doubt should obtain professional advice.

Victoria – Consumer Credit (Victoria) Act

1. Applies to UCCC regulated credit – s.37A.

2. An FBC containing prescribed information must be signed before a broker may charge or receive any commission from the borrower. Consumer Affairs Victoria considers that the legislation also requires an FBC where commission is payable only by someone other than the borrower. Although this view is not free from argument, the MFAA supports Consumer Affair’s initiative to have FBCs with borrowers irrespective of who is paying the commission and even where commission is payable only by the lender – s.37J. The MFAA site provides sample finance broking contracts for use in Victoria. There is also a version which is suitable for use in all states and territories.

3. No commission must be received from the borrower unless either:

the borrower "accepts" the credit that is actually obtained: or

the credit negotiated is reasonably comparable to credit specified in the FBC – ie approval is

obtained – s.37J(f).

4. Penalties apply for breach, and brokers may be unable to recover their commission.

5. Certain persons are prohibited from engaging in financing broking, including people under the age of 18, individuals and corporations who are under some form of insolvency administration such as bankruptcy, liquidation, receivership or voluntary administration, or where a person is a disqualified person.

A disqualified person is someone who in the preceding 10 years has been found guilty of:

(d) in Victoria or elsewhere, an offence involving fraud, dishonesty, drug trafficking or violence;

(e) an offence under the Credit Act 1984 or other consumer credit legislation;

13

5038568 JAD KQW

(f) an offence under relevant finance broker legislation.

A person or a corporation is also a disqualified person if their occupation, profession or business is regulated under any enactment of Victoria or another State of Australia and they have had their licence, registration or permission to carry on that occupation, profession or business suspended or cancelled or have been disqualified from carrying on that occupation, profession or business:

(i) in the case of suspension during the period of suspension;

(ii) in the case of cancellation, during 5 years following the cancellation;

(iii) in the case of a disqualification, during the 5 years following the disqualification or the period of disqualification, whichever is longer.

6. Division 5 of Part 4A entitles a consumer to recover money paid to a finance broker if the finance broker has not complied with the finance broking law applicable in Victoria. The Director of Consumer Affairs Victoria can take that action for consumers.

The Director must be satisfied that:

(a) the consumer has a good cause of action or a good defence; and

(b) it is in the public interest (our bolding) to institute, continue or defend the proceedings.

The Director can represent:

(a) individuals provided they have consented in writing; or

(b) groups – ie take a class action on behalf of seven or more people.

The Director can settle proceedings, enforce judgments, and can be liable for, or recover, costs.

Western Australia

Summary

1. Applies to all credit.

2. License required - education requirements. Residential requirements for directors of companies.

3. Maximum commission and fees prescribed.

4. Restrictions on advertising.

5. Brokers must comply with a Code of Conduct.

Details

See Part 6.

South Australia

All states and territories have legislation making it a crime to accept secret commissions. With the exception of South Australia, the crime will only be committed if the commission is corruptly received. It is unlikely that commissions paid to brokers will ever be corrupt and so the legislation has no effect.

14

5038568 JAD KQW

The relevant legislation is Part IV A of the Criminal Code Act 1899 chapter 42A(Qld), Crimes Act 1900 (NSW), Criminal Code 2002 s352 to s359 (ACT), Crimes Act 1958 s175 to s180 (Vic), Tasmanian Criminal Code Act 1924 s266, 266A, 266B (Tas), Criminal Law Consolidation Act 1935 s145 to 151 (SA), Criminal Code s549 to s533 (WA), , and Criminal Code Act 2006 Division 5 (NT).

The situation in South Australia is different because s 146 of the South Australia Criminal Law Consolidation Act defines "fiduciaries" widely so that most finance brokers will probably be captured under paragraph (a) – the person (ie the broker) is the agent of the borrower :"under an express or implied authority to act on behalf of the other".

Despite attempts to negate agency in many finance broking contracts, it is likely that a broker is at least the limited agent of a borrower to assist in lodging the loan application. Also, from time to time courts have held that brokers are agents of the borrowers because of the nature of the relationship. It is likely that many brokers by their conduct constitute themselves as agent for the borrower.

Of course, it is open for individual brokers to argue that they are not agents but it is likely that argument may fail and so the appropriate disclosure should be made.

Under s 148(2) the disclosure must include:

(a) the nature of the benefit;

(b) the value (or approximate value) of the benefit; and

(c) the identity of the third party from whom the benefit has been or is to be received.

Accordingly, it is important for brokers to disclose these details in SA.

15

5038568 JAD KQW

Part 4 - Australian Financial Services licences

Normally credit is not a financial product, and so finance brokers dealing with “pure” credit will not need to hold an Australian Financial Services licence or be the authorised representative of an AFSL holder.

Intermediaries who provide additional services need to be aware of the types of activity governed by the AFSL regime. The MFAA and Gadens Lawyers have a separate module titled "Australian Financial Services Licensing".

Brief summary

A deposit product (eg, a bank account) is a financial product – accordingly, finance brokers will need to hold an AFSL, be an authorised representative, or provide “no advice”.

An off-set account involves a deposit account and so ordinarily would be a financial product. ASIC Class Order 03/1048 - Mortgage Offset accounts relieves finance brokers from holding an AFSL or being an authorised representative if the finance broker is a member of an eligible alternate dispute resolution scheme. Credit Ombudsman Service Limited (COSL, previously known as MIOS) is such a scheme. Brokers may continue advising in relation to mortgage loans with off-set accounts using the “no advice” model without joining such a scheme.

Fire insurance and CCI insurance are regulated products.

Any type of financial investment will normally be a regulated financial product.

A person is not taken to provide financial advice if they:

(a) only express an opinion or recommendation about the allocation of a person’s funds amongst certain types of products; and

(b) do not express an opinion or recommendation as to a specific financial product or class of financial products.

This is the so-called “no advice” or “tick and flick” exemption from the requirement to hold an AFS licence or be an authorised representative of an AFS licensee.

In summary there are three relevant exemptions for mortgage brokers:

no advice – tick and flick;

class order in respect of offset accounts;

brokers who are appointed insurance distributors - see below;

Insurance distributors.

Class order 05/1070 - general insurance distributors - allows an insurer or AFS licensee who is authorised to deal in general insurance products to appoint a broker as an insurance distributor provided the broker is not already an authorised representative of that particular AFS licensee.

The distributor must still not provide advice, and must only assist the customer to obtain the product, for example by filling out application forms and forwarding them to the insurer.

The class order relates to:

(a) general insurance which includes fire and contents insurance, motor vehicle insurance, consumer credit insurance (but not medical benefits insurance or life insurance); and

(b) bundled consumer credit insurance being CCI with a life insurance component.

16

5038568 JAD KQW

Although the AFS licensee does not need to comply with the requirements of appointing a person as an authorised representative, in order to benefit from the class order, the distributor must take reasonable steps to ensure retail clients are informed about:

the AFS licensee’s dispute resolution system;

the fact that the distributor is acting on behalf of the AFS licensee; and

any remuneration to be received by the distributor.

This information may be included in the AFS licensee’s Financial Services Guide (FSG) or it may be given to the retail client in a separate document.

In addition, as the AFS licensee is responsible for any distributors it appoints, the AFS licensee retains its responsibility to ensure that distributors are adequately trained and supervised and must take reasonable steps to ensure that distributors comply with financial services laws.

Benefits of CO 05/1070

There is no restriction on a distributor being appointed by more than one AFS licensee.

AFS licensees are not required to provide written notice to ASIC of the appointment or revocation of a distributor (as is the case when an authorised representative is appointed, removed, or changes its details).

Distributors may provide clients with the AFS licensee’s FSG. They are not required to personalise the FSG as is the case with authorised representatives.

A body corporate who has been appointed as a distributor may sub-authorise other distributors with the written consent of the AFS licensee.

17

5038568 JAD KQW

Part 5 - Disclosure of commission

Even where there is no legislation requiring disclosure of commission, finance brokers should disclose to borrowers full details of the commission they receive, irrespective of who is paying the commission, for the reasons specified below.

1. General law obligations

The general law (also called the common law) imposes a duty of care on finance brokers. The level of duty of care will depend on the relationship between the finance broker and the borrower.

If the finance broker purports to act as the agent for the borrower, a relationship of principal and agency arises. In those circumstances, the finance broker has a very high duty of care to the borrower indeed, and must disclose all commissions and any other benefits in full.

The duty of care to the borrower and the obligation to disclose commission is likely to be different depending on the business model adopted by the finance broker. For example:

(a) lowest duty - a mortgage manager who from the borrower’s perspective has similar characteristics to a lender;

(b) medium duty - an originator who from the borrower’s perspective has similar characteristics to a sales person, and who does not purport to represent the borrower in any way or have a specific duty of care to the borrower;

(c) highest duty - a finance broker, irrespective of whether a fee is payable by the borrower who gives advice to the borrower. In these circumstances, it is likely that the finance broker becomes the agent for the borrower and owes a fiduciary duty of care to the borrower.

It is desirable for finance brokers to enter a contract with customers, or at least give a disclosure note to customers, specifying:

(a) the level of disclosure which will be adopted; and

(b) the duty of care which will apply.

Finance brokers may owe a fiduciary obligation to their client, as well as general law obligations, if their relationship is one of principal and agent.

2. Industry codes

Members of the MFAA will be obliged under clause 33 and 34 of the MFAA’s Code of Practice.

Clause 33

Fees and Commissions

If a fee or on going commission will or may be paid by or to the Member for or in connection with a loan or an

application for a loan, the Member must always disclose to the applicant:

(a) that fact; and

(b) the person by whom the fee or commission is payable; and

(c) the person to whom the commission is payable; and

(d) the amount of the fee or commission if ascertainable; and

18

5038568 JAD KQW

(e) if the fee or commission is unascertainable, the basis of or formula for such fee or commission;

but this paragraph does not apply to:

(f) fees payable by a supplier under a merchant service agreement with a credit provider; or

(g) the amount payable in connection with a credit related insurance contract; or

(h) commission paid to employees of the Member.

Clause 34

A Member will never charge an applicant a non-refundable application fee for a loan submission where the Member

knows or suspects that there is little or no chance of the loan being approved.

The application of clause 33 has been clarified by the following resolution of the National Council of the MFAA.

Statement of Interpretation adopted by MFAA National Council 27 May 2003

“A member will have satisfied clause 33 of the Code of Practice and will not be guilty of Misconduct if:

(a) where the member is paid by or on behalf of the lender, the member discloses that:

(i) a commission may be paid;

(ii) the commission will be paid by or on behalf of the lender (there is no need to identify the name of

the lender);

(iii) that the commission is payable to the member;

(iv) the amount of the fee or commission if ascertainable;

(v) if the fee or commission is unascertainable, a statement that the commission comprises (as

appropriate):

an upfront payment equal to a percentage of the principal sum; and

an ongoing commission throughout the term of the loan based on a percentage of the

amount owing from time to time.

Where the member is a mortgage manager or aggregator who distributes loans through sub-originators, and the

mortgage manager or aggregator does not deal directly with the relevant customer, that member will not need to make

a disclosure under clause 33. In these circumstances the relevant disclosure will be made by the sub-originator who

deals with the customer. In reaching this conclusion the Council notes that the Consumer Credit Code will require the

lender to comply with s 15(M) of the Consumer Credit Code in relation [to] total commissions paid by the lender.

(b) Where a member is being paid a commission by a manager or an aggregator the member must disclose the

following:

a commission may be paid;

the commission will be paid by or on behalf of the lender, manager, or aggregator (there is no need to

identify the name of the lender, manager, or aggregator);

that the commission is payable to the member;

the amount of the fee or commission if ascertainable;

if the fee or commission is unascertainable, a statement that the commission comprises (as appropriate):

19

5038568 JAD KQW

an upfront payment equal to a percentage of the principal sum; and

an ongoing commission throughout the term of the loan based on a percentage of the

amount owing from time to time.

The Council approves the form of disclosure attached. Members can use any form of disclosure so long as it

complies with the above interpretation of clause 33.

Sample form of disclosure [Not suitable in states which prescribe a form of disclosure -- as at February 2006,

this is NSW and WA]

[BROKER NAME] arranges loans for borrowers.

In providing these services [BROKER NAME] is an independent contractor.

You acknowledge that we may be paid a commission by funders, managers, product suppliers or other people with

whom we do business. We also may pay referral fees or commissions to people who referred you to us. No

commission is payable by you.

In respect of most loans, we may be paid an upfront commission, which is a percentage of your loan amount, and a

trail commission, which is a percentage of the ongoing loan balance. In respect of other products and services we

may be paid a commission which may consist of an initial commission plus an ongoing commission calculated by

reference to the loan or product amount. It is not practical at the date of this disclosure to specify the exact amount of

commission payable.

[BROKER NAME] is a member of the Mortgage & Finance Association of Australia, the peak body for mortgage

intermediaries. We and any of our representatives will comply with the Code of Practice binding on its members. We

will use our experience to present to you products which we consider are suitable for your requirements, but the final

choice to acquire any of those products is yours.”

20

5038568 JAD KQW

Part 6 – Finance Brokers Control Act (WA)

For information specific to trust, securitisation, and mortgage managers see the "WA Finance Brokers Licensing – Mortgage Managers Practice Module".

For information in relation to the Code of Conduct commencing on 29 June 2007 and finance broking contracts for WA, see the "WA Code of Conduct Module" and the WA finance broking contract.

When is a licence required?

1. Required for both UCCC regulated and non-UCCC regulated credit

The regulation of finance brokers and mortgage managers applies to all credit, and not just UCCC regulated credit. This extension beyond UCCC regulated credit is unique to WA. (In contrast, the requirement for credit providers to be licensed in WA applies only to lenders of UCCC regulated credit).

This means that businesses which arrange or manage commercial loans may need to be licensed.

2. When is a loan covered by this regulation?

The legislation only applies if the broker or manager arranges or manages loans which have a relevant nexus to WA. The Finance Brokers Control Act does not specify what the relevant nexus is and therefore businesses are required to make their own assessment of the jurisdictional limit.

As a rule of thumb, there will be a relevant nexus and a licence will be required if:

the business has a physical office in WA; or

the business advertises specifically in WA;

the borrower lives in WA.

However, if a business located outside WA makes occasional loans to WA residents without specifically targeting WA residents as customers, the legislation is unlikely to apply and the business need not be licensed. DOCEP considers that ongoing repetitive business of one loan per month (or even less depending on the circumstances) could constitute carrying on business in WA.

Compare this situation with ACT where the requirement to register as a finance broker is clearly limited to cases where the borrower is resident in the ACT and the loan is regulated by the UCCC.

3. What kind of business activities require a license?

A finance broker is a person who “as an intermediary, in the course of business negotiates or arranges loans of money for or on behalf of other persons, or in the course of business, manages loans of money arranged or negotiated by the person for or on behalf of other persons”.

Finance brokers and aggregators

The WA Department of Consumer and Employment Protection (DOCEP) considers that any entity involved in the origination process (eg aggregators as well as loan writers) must be licensed. In the diagram below, each of the aggregator, head originator and loan writers would need to be licensed. However, loan writers would not need to be licensed if they are employees of the head originator and under the bona fide control of the head originator.

21

5038568 JAD KQW

Example 1: Big Aggregator is based in Sydney, and markets through sub-originators. Both Big Aggregator and the sub-originators need to be licensed in WA.

However, if the business has no physical presence in WA and does not specifically target WA residents, a licence will not be required if an occasional loan is made to WA residents.

Mortgage managers, trust managers and securitisation managers

Mortgage managers, trust managers, and securitisation managers will need to be licensed if they originate loans. Managers who solely manage loans originated by others will not need to be licensed. This flows from the definition of a finance broker as a business which "manages loans of money arranged or negotiated by [the business]" – ie not a business that manages loans negotiated or arranged by others.

DOCEP considers that a manager is involved in negotiating or arranging if it is involved in the credit process. This is the case even if the manager only deals through introducers who are licensed brokers and does not ordinarily deal direct with the borrower.

Only the legal lender is clearly outside this definition. Any intermediary whether acting for the lender or the borrower who arranges loans is captured. In this regard, it is relevant to remember that WA had problems with brokers who arranged risky loans for investors, and so the WA regime focuses on intermediaries who act for lenders as well as borrowers.

Example 2: Mortgage Manager markets commercial loans both direct and through brokers. Mortgage Manager is involved in the approval process of the loan. The lender is a trustee. Mortgage Manager will need a licence as it is arranging loans.

Example 3: Trust/Securitisation Manager markets loans both direct and through brokers. Trust/Securitisation Manager is involved in the approval process of the loan. The lender is a trustee. Trust/Securitisation Manager will need a licence as it is arranging loans.

Lender Lender Lender

Aggregator

Head Originator

Loan Writer

Loan Writer

Loan Writer

Loan Writer

22

5038568 JAD KQW

Example 4: Trust/Securitisation Manager manages loans. The final credit approval (at least from a legal point of view) can only be given by the Trust/Securitisation Manager. The Trust/Securitisation Manager is acting as the manager of the lender, and may even be the agent of the lender. However, the Trust/Securitisation Manager has contracted for XYZ company (possibly in the same corporate group) to undertake the arranging and negotiating process, including the right to approve loans (ie a DLA) The Trust/Securitisation Manager does not need a licence as it is not arranging or negotiating loans. XYZ company would need to be licensed.

If Trust/Securitisation Manager had not outsourced the approval process, Trust/Securitisation manager would need to be licensed if dealing with loans with sufficient nexus with WA. It is irrelevant whether Trust/Securitisation Manager deals direct with borrowers or not.

If Trust/Securitisation Manager is legally the agent of the lender, it may be argued that Trust/Securitisation Manager is acting as the lender and not as an intermediary. If this is correct, Trust/Securitisation Manager would not need to be licensed.

4. Exemptions

Section 5 of the Finance Brokers Control Act exempts a number of businesses from obtaining a licence or complying with any of the other provisions of the Act, including the following:

banks;

friendly societies;

insurance companies;

pastoral companies;

an AFSL licensee but when dealing in securities (but a licence will be required to deal with

other loans);

lawyers when acting incidentally to the practice of law (but a licence will be required to deal

with other loans);

a retailer or other supplier of goods who arranges finance for payment of the purchase price.

Types of licences

There are 4 types of licences.

A class licence (unrestricted licence)

No restriction on the type of lenders with whom the licensee may negotiate or arrange loans of money.

Applicants for an unrestricted licence may apply for a restricted licence so that they can practice under a restricted licence whilst studying their Diploma course.

B class licence (restricted licence)

Most brokers hold a B class licence.

B class licensees are restricted to arranging loans with lenders who are:

a registered managed investment scheme;

a credit provider licensed in WA;

23

5038568 JAD KQW

banks and building societies; and

registered as a financial corporation under the Commonwealth Financial Sector (Collection of Data)

Act 2001. A lender (except ADIs) should register as a financial corporation if:

- its total assets exceed $5,000,000 and its sole or principal business in Australia is borrowing

money and the provision of finance; or

- its assets arising from the provision of finance exceed 50% of its total assets in Australia.

C class licence (restricted licence)

C Class licensees are subject to the same restrictions as B class licensees, but in addition, the licensee must carry on business under the exclusive supervision of a nominated broker who holds an A or B class licence.

This class of licence is designed for new entrants to the industry who cannot satisfy the two years' experience requirements.

It is the finance broker's responsibility to take reasonable steps to ensure that C class licensees have up to date qualifications or experience relevant to their duties in the finance broker's business and keep up to date with current laws and practices. Ongoing training and development should include induction programs, mentored/joint client interviews, routine training schedules (eg fortnightly training sessions), lender accreditations and training from relevant industry bodies. Training must cover information about the relevant provisions of the Code of Conduct including disclosure, appropriate loan selection and refinancing.

The finance broker must take reasonable steps to ensure that C class licensees comply with any conditions on their licence, the provisions of the Act and regulations, the Maximum Remuneration Schedule, and the requirements of the Code of Conduct. This may include documented procedure manuals, loan application/file audits, obtaining and assessing feedback from customers and lenders, and effective dispute resolution services.

Where supervision and mentorship responsibilities are delegated, the delegates must hold the appropriate qualifications and experience. DOCEP expect larger businesses to have a dedicated officer to assist with the training, development and supervision of C class licensees. The supervisor is ultimately responsible for the supervision of the C class licensee. Supervisors should undertake loan application/file audits, assess feedback from customers/lenders, have appropriate contracts of engagement and have a dispute resolution service. Levels of supervision should be intensive during the early stage and reduce over time when the supervisor becomes satisfied that the C class licensee has sufficient skills, knowledge and is compliant with the legislation.

Methods used to monitor, assess and manage the performance of C class licensees included setting monetary targets for loan approvals, loan application/file audits, written performance plans and assessing feedback from customers and lenders. Performance management should be used in supervision and should include an assessment of compliance and quality control measures.

Where the supervised C class licensee is located in a remote or country location or the supervisor is located interstate, supervisors should ensure they have adequate measures in place to undertake their supervision and mentoring responsibilities.

If the C class licensee employs staff involved in finance broking activities (eg loan writers), it is the responsibility of supervisors to ensure that those employees receive appropriate levels of supervision and operate in accordance with the legislation.

24

5038568 JAD KQW

Evidence of supervision should be retained (eg records substantiating the loan application/file audits conducted such as register of loans examined, signature/initials on documents reviewed) and formal training attendance records. This will assist supervisor in the event there is an allegation of inadequate supervision.

D class licence (education and experience requirements do not apply)

The D class licence allows directors and partners to obtain a licence (thereby enabling their companies and partnerships to obtain a licence) where the directors or partners cannot satisfy the education and experience requirements, so long as the company or partnership has an A or B class licensee in bona fide control of the finance broking operations in WA of the business.

The licensee in bona fide control does not need to be physically located in WA if control can be exercised from elsewhere. However, the licensee will need to be physically located where the business is conducted (eg head office). Usually, each branch office will need a licensee in charge. The requirement for people to be WA residents was removed in 2006 and now licensees only need to be resident in Australia.

What is required to obtain a licence?

Individuals

Section 27 requires an individual to:

be resident in Australia (see regulation 5A);

be 18 years or older;

be a person of good character and repute (presumably police reports will continue to be required);

be a fit and proper person to hold a licence;

have sufficient material and financial resources available to comply with the Act;

understand the duties and obligations imposed by this Act on finance brokers;

have such other qualifications as may be prescribed by the regulations.

In addition, the regulations require:

for A, B, or C class licences: successful completion of Certificate IV in Financial Services

(Finance/Mortgage Broking), including relevant supplementary Western Australian material provided

by an approved training provider;

for A class licences: successful completion of a Diploma of Mortgage Lending or a Diploma of

Lending or a Diploma of Financial Services (Lending) provided by an approved training provider (the

Diploma of Financial Services (Lending) is currently only offered by Kaplan Professional);

for A or B class licenses: two years' full-time relevant experience in the preceding 5 years; and

for D class licences: nomination of an A or B class licensee who will be in bona fide control of the WA

finance broking operations of the company or partnership.

Partnerships

3 or less partners – at least one partner licensed.

4 or more partners – at least two partners licensed.

25

5038568 JAD KQW

If the partners hold a D class licence, they must have an A or B class licensee employed in bona fide

control of the WA finance broking business.

Companies

3 or less directors – at least one director licensed.

4 or more directors – at least two directors licensed.

If the directors hold a D class licence, they must have an A or B class licensee employed in bona fide

control of the WA finance broking business.

Where the finance broking business is a minor part of the business, the Commissioner may agree to

no directors being licensed and allowing the officer in bona fide control of the finance broking

business to be licensed.

Employees and contractors

Employees who work under the brand and control of their employer will not need to be separately licensed unless they are in control of a separate physical branch.

DOCEP considers that contractors (as distinct from employees) must be separately licensed.

Maximum commission

The maximum commission is prescribed in the WA Government Gazette dated 20 February 2004, ref CE301.

Different limits apply depending on whether the lender is a “Credit Provider” or not. A Credit Provider is a lender:

(a) regulated under the FSR or APRA;

(b) a licensed credit provider in WA; or

(c) registered as a financial corporation under the Commonwealth Financial Sector (Collection of Data) Act 2001).

If the lender is a Credit Provider, the maximum commission for loans other than equipment or personal finance loans) payable by either the borrower or the lender is in aggregate 2% of the loan amount upfront and 0.5% pa of the average outstanding loan balance "from time to time" trail.

If the lender is not a Credit Provider, the maximum commission is:

(a) upfront 2% for loans over $25,000 paid by the borrower and 1.5% paid by the lender; and

(b) trail 0.5% pa paid by the lender.

The maximums for equipment or personal finance is:

(a) upfront from either the lender or the customer (in aggregate), $800 for loans up to $10,000 and thereafter 8% of the loan amount;

(b) trail payable by the lender of 0.5% per annum.

A maximum is prescribed for “Total Mortgage Management”: 8% of interest collections.

26

5038568 JAD KQW

These figures appear not to have been adjusted to allow for GST. Accordingly, they must be treated as being GST inclusive. Many industry participants consider that the limits are too low. Other industry participants consider that there should be no limit on commission paid by lenders.

Higher brokerage fees are prescribed for personal and equipment finance.

There may be a written agreement between the borrower and the broker which specifies the time when commission is payable, but otherwise it is payable upon the loan being obtained (except where failure to obtain the loan was the fault of the borrower).

These maximums relate to the total received from all sources. Accordingly, the commission received from the borrower and the lender taken together, must not exceed these limits.

The WA Finance Brokers Supervisory Board (prior to its undertaking being moved to DOCEP) considered that fees charged to borrowers in budget management/wealth creation/debt reduction plans are “so integrally and intimately connected with” arranging the loan, that fees charged for these services are fees charged for negotiating and arranging the loan. Accordingly, commission maximums, and requirements for FBCs will apply.

Regulations limit the amount that can be charged for:

(a) application fees;

(b) inspection fees;

(c) transfer of mortgage between investor clients;

(d) extension of mortgage;

(e) discharge fee;

(f) commission on interest collections; and

(g) miscellaneous charges such as production of title, bank cheques etc.

Provision of credit contracts - s.46

A finance broker must send to the borrower a copy of the loan agreement and any other document relating to a loan, and receive from the borrower a written acknowledgment of receipt. Obviously, this is honoured in the breach as the lender usually provides the loan agreement. The Department of Consumer and Employer Protection (DOCEP) has informed the MFAA that is likely a court would read down this requirement so that a broker would only be required to provide a copy of the contract where the broker obtains the signature of the person to the document.

Disclosure of licence numbers in advertisements

An advertisement in relation to the licensee’s business must contain the licensee’s licence number – s.45(2). This could be difficult and misleading for national and electronic advertising.

In January 2007, DOCEP released a Statement of Regulatory Intent to assist brokers identify what the Commissioner considers is an advertisement. The Statement included the following list.

27

5038568 JAD KQW

Advertisements requiring licence number

Newspaper

Magazine/Journal

Published flyer

CDs/DVDs and other multimedia

Radio

Television

World Wide Web

Business Cards

Letterhead

Brochures

Office signage

Billboards

Motor Vehicles

Promotional items not requiring licence number

Pens

Clothing/Hats

Sporting equipment and accessories

Other promotional goods

This requirement needs to be read so that only items in respect of the business of finance broking in WA need have the licence number. This is our emphasis from the text of the section which reads in full as follows: "A duly authorised advertisement in respect of the business of a licensee shall contain (as a minimum) the licence number of the licensee, and such other details (if any) as are prescribed."

So, the licence number must be shown if the item needs to be one of the type of things on the list, but only if it relates to the WA finance broking business. Items that are not being used for marketing purposes (eg corporate letterhead not going to consumers) would not need to show the licence number as it cannot be an advertisement.

What else does a licensee have to do?

1. A licensee must comply with the Finance Brokers Code of Conduct – s.34. See separate module for details of the Code of Conduct and precedent finance broking contracts.

2. A person must not hold more than one licence and must not carry on more than one business as a finance broker – s.40.

3. A licensee must register each branch office with the Commissioner – s.38(1). There must be a licensee at each registered branch office – s.38(2).

28

5038568 JAD KQW

4. All licensees carrying on the business of a finance broker under a business name must have their surnames and initials at the head of all correspondence from them in that business. This applies to partnerships but not to companies – s.41.

5. A licensee must exhibit in its registered office and every branch office details of their registration as a licence broker – s.42. This should be limited to branch offices in WA.

6. A finance broker must enter a written finance broking agreement with the person who is to pay the commission. Where the lender is paying the commission, the “master” origination agreement would satisfy this requirement – s.43.

7. An advertisement must not mention an interest rate unless specified in respect of a specific amount and:

(a) in relation to UCCC regulated credit it complies with the UCCC comparison rate regime; and

(b) in respect of other credit the amount(s) of the loan and the interest rate are calculated as prescribed in a schedule to the Act – s.45(3).

(This is difficult to comply with when advertising regulated and unregulated loans in a single advertisement as the formulas produce different answers).

8. Every finance broker must maintain at least one trust account – s.48. However, no trust account is required if the broker receives no money to hold on behalf of another person, and within 3 months of the end of a calendar year provides a statutory declaration to this effect to the Commissioner.

9. The trust account must be audited – s.50. There are extensive audit provisions.

The Commissioner may make an interim order suspending a finance broker’s licence for up to 60 days if there are reasonable grounds for believing the broker has engaged in conduct that constitutes grounds for suspension or cancellation and there is a risk that persons may suffer significant loss or damage if immediate action is not taken.

The maximum penalty for unlawfully carrying on business as a finance broker is $50,000.

29

5038568 JAD KQW

Part 7 - WA Credit Provider Licensing

The Credit (Administration) Act 1984 (WA) requires credit providers who provide UCCC regulated credit to be licensed**. There is an exemption for banks and building societies.

**The legal analysis of why only lenders of UCCC regulated credit must be licensed is complex. The Credit (Administration) Act under s.6 requires persons who carry on a business of providing credit to be licensed. Section 4 defines credit widely. However, s.7(2) states that a reference to carrying on a business does not include providing credit “otherwise than under a contract to which this Act applies”. Section 4 defines a “contract to which this Act applies” as being UCCC regulated credit contracts.

Most WA finance brokers have restricted licences. Most restricted licences issued by the Finance Brokers Supervisory Board were endorsed as follows (and it is expected DOCEP will continue with a similar practice).

“The licensee shall not negotiate or arrange any loans of money unless, in respect of that loan, the lender is either:

regulated under chapter 5C or 7 of the Corporations Act or by the Australian Prudential

Regulation Authority (APRA) [ie, managed investment schemes and AFS licensing regime];

a licensed credit provider under the Credit (Administration) Act 1984 (WA);

a person exempt from the licensing requirements of s. 6 of the Credit Administration Act 1984

pursuant to s. 7(1) of that Act [basically banks and building societies]; or

a specific entity held on a list maintained by the Registrar which may be amended from time to

time. It is the broker’s responsibility to ensure the entities with which they are negotiating or

arranging any loans of money appear on the above list which may change from time to time.”

Only brokers who have had the “list condition” attached to their licence may introduce loans to “list lenders”. The application form to obtain the additional condition is available at www.financebrokers.wa.gov.au.

What you should do

1. If you are a credit provider lending non-UCCC regulated credit to residents of WA, you should get on the list maintained by DOCEP if you want brokers holding B and C class licences to sell your product to WA residents.

2. If you are a WA finance broker with a restricted licence, obtain the endorsement to allow you to deal with lenders on the list of lenders maintained by DOCEP.

30

5038568 JAD KQW

Part 8 – Door to door sales legislation

All states and territories have Acts regulating door to door sales. The legislation will probably apply if:

a broker charges for arranging credit or financial management or any other service; and

the sale is the result of an initial unsolicited approach; and

the sale is not made at the broker’s office; and

the purchase is not for business purposes.

The following will help you determine whether the Acts apply to your business.

Step 1. Is the sale a door to door sale?

The sale will be a door to door sale if the following tests are all satisfied:

the sale is made over the telephone or in the physical presence of the customer, but not if it occurs at the broker’s office. The sale does not need to be at the customer’s home as a result of a door knock campaign; and

the telephone call or the visit is unsolicited. The call or visit will be unsolicited if it is the result of an initial cold call (even if that cold call is the result of a referral); and

the purchaser is not entering the transaction in connection with a business carried on by the purchaser. Accordingly, only sales for primarily private or personal purposes will be regulated.

Step 2. Is the sale a regulated sale?

The Acts regulate the sale of ‘goods or services’ for more than $50 ($75 in Queensland and $100 in NSW).

Generally, contracts for the sale of credit are exempted from the Acts. If the broker is an agent of a specific lender, is not charging the borrower a fee, and is selling that lender’s products, the sale will not be regulated by the door to door Acts because the broker is only selling credit (which is exempt), and isn’t selling broking services. In NSW, brokers who telephone prospective customers in relation to consumer credit do have to comply with the restricted calling hours even though credit itself is exempted.

NB: However, if the broker is selling broking services (as most brokers do), the contract is for the supply of services, namely finance broking services. A finance broking contract will therefore be subject to the Acts but only if the borrower is paying a fee of more than the minimum price ($50/$75/$100). If the borrower is not liable to pay any commission to the broker, the sale of finance broking services will not be regulated by the Acts.

Step 3. What about budget coaching contracts?

Some brokers offer budget coaching programs.

It is important that these services do not involve advice or sale of financial products unless the finance broker holds an AFS licence. However, as long as the advice is confined to budget coaching, this is not advice on, or the sale of, a financial product and so the broker does not need an AFS licence to provide this service.

The sale of a budget coaching program is a supply of services, and so the Acts will apply to the sale of these services (provided the answers to steps 1 and 2 are yes).

31

5038568 JAD KQW

Step 4. Will the finance broking contract be impacted by the budget coaching contract?

Where two or more contracts relate substantially to the same transaction, the Acts provide that they are to be taken as a single contract. If the effect of this provision is to attach the finance broking contract to the budget coaching contract, then the broker will be unable to lodge the loan application until after the cooling off period.

Although not free from argument, the better view is that the two contracts do not relate substantially to the same transaction. One contract relates to arranging a loan which is a discrete service and capable of sale quite separately from the budget coaching program.

Accordingly, as long as the borrower is paying no commission under the FB contract, the Acts only apply to budget coaching contracts. A broker can sell a budget coaching contract (which will be regulated by the Acts) and broker services (which will not be regulated by the Acts) at the same time. Accordingly, the broker can proceed to lodge the application for a loan with the lenders.

NB: Remember, however, that if the FB contract provides for the borrower to pay any commission then the Acts will apply to the FB contract in its own right.

Step 5. What is required if the Acts apply?

You must give two prescribed forms to the customer before the customer signs the contract. In NSW there is no prescribed form, although the content of the form is the same as the content in the prescribed forms in all other states and territories.

The contract must be in no smaller than 10 point type.

The contract must state clearly in upper case, above the place provide for signature, ‘THIS CONTRACT IS SUBJECT TO A COOLING OFF PERIOD OF XXX DAYS’ in at least 18 point type. In NSW the cooling off period is five days, and ten days in other places.

The supplier must not receive any payment under the contract before the expiration of the cooling off period.

No services may be supplied under the contract before the expiration of the cooling off period. This is the provision which prevents finance brokers from lodging loan applications within the cooling off period if the FB contract provides for the borrower to pay commission for arranging the credit. Of course, the cooling off period only applies if the other requirements for a door to door sale are satisfied (ie Steps 1 and 2 apply).

Customers cannot waive their cooling off rights.

The contract must set out all the terms of the contract including the full price, including any GST.

The broker must sign the contract before the customer signs the contract.

The customer must be given a duplicate of the contract immediately after the making of the contract.

You must not call on a person’s residence in New South Wales after 8.00pm or before 9.00 am on any day. In other states and territories you must not call at a person’s residence:

at any time on a Sunday or a public holiday.

before 9.00am.

after 8.00 pm on weekdays (6.00pm in Queensland).

after 5.00 pm on Saturdays.

32

5038568 JAD KQW

These time restrictions only apply if your visit is regulated by these Acts.

On arrival at the property you must make known to the person the purpose of the call and produce an identity card with your full name and address.

Commentary

The Acts will have a very major impact on brokers who charge borrowers a commission and use marketing methods which result in sales captured under Step 1. These brokers will need to comply with the Acts and they must not lodge the application with any lender until after the cooling off period has expired.

Details of legislation

Place Legislation

Qld Fair Trading Act 1989

NSW Fair Trading Act 1987

ACT Door to Door Trading Act 1991

Vic Fair Trading Act 1999

Tas Door to Door Trading Act 1986

SA Fair Trading Act 1987

WA Door to Door Trading Act 1987

NT Consumer Affairs and Fair Trading Act

33

5038568 JAD KQW

Part 9 – The Hawking Prohibitions in the Corporations Act

Some mortgage brokers may fall under the hawking prohibitions in the Corporations Act. These provisions only apply to the sale of financial products to “retail clients”. Credit is not a financial product but other products such as deposits, insurance, and investment products are financial products.

Sections 736, 992A and 992AA of the Corporations Act 2001 provide that a person (the “offeror”) must not offer financial products (other than securities or managed investments) for issue or sale to retail clients in the course of, or because of, an unsolicited meeting. There are also procedures which must be complied with if there is an unsolicited telephone call.

When is a meeting or telephone call “unsolicited”?

For a breach of the hawking prohibitions to occur, the offer of financial products to the consumer must be made during or because of, a meeting or telephone call that is “unsolicited”. In ASIC’s view, a meeting or telephone call will be unsolicited unless it takes place in response to a positive, clear, and informed request. A positive request involves an active step by the consumer. A meeting or call is not solicited merely because the consumer fails to request that the meeting or telephone call not take place after being given an opportunity to do so.

The nature of the meeting or telephone call being requested by the consumer should be clear from the language of the request. The request should make clear which financial products or classes of financial products the consumer wishes to discuss.

What is the purpose of the meeting or telephone call?

ASIC considers that a meeting or telephone call requested by a consumer is only solicited in relation to any financial products (or classes of financial products) that are reasonably within the scope of the request. Brokers need to consider each consumer separately, to ensure that they do not offer products which could be considered to be unsolicited.

Is the person an existing client?

Depending on the circumstances, a meeting or telephone call with an existing client may still be unsolicited for the purposes of the hawking provisions. As indicated above a meeting or telephone call will be unsolicited unless it takes place in response to a positive, clear and informed request. This indicates that there are no special rules for existing clients, unless the client requests that the offeror contact them on an ongoing basis.

34

5038568 JAD KQW

Part 10 – The eMarketing Code of Practice (‘the Code’)

1.1 What are the objectives of the Code?

The Code’s objectives are to:

(a) reduce the volume of unsolicited commercial electronic messages received by consumers;

(b) provide a plain English outline of how the Spam Act 2003 (the Spam Act) applies to current eMarketing practices; and

(c) promote best practice use of commercial electronic messages in compliance with the Spam Act.

1.2 Why was the Code developed?

The Code establishes comprehensive, industry-wide rules and guidelines for the sending of commercial electronic messages (‘CEMs’) in compliance with the Spam Act. The Code also provides a framework by which industry can handle complaints about spam and monitor industry compliance with code provisions.

1.3 SPAM Act

The Spam Act prohibits the sending of unsolicited commercial electronic messages linked with Australia. In summary:

it is illegal to send most commercial electronic messages to or from Australia without the recipient's consent;

certain commercial electronic messages designated in the Act (“designated commercial electronic messages”), are exempt from the consent requirement;