reforms in indian money n capital market

TRANSCRIPT

REFORMS IN INDIAN MONEY AND CAPITAL

MARKETPresented By-

PUNEET BANDHU(09)

AMRIT MOHANTY(28)

MISHAYE KAPOOR(35)

VARSHA LAWRENCE

ABHISHEK KUMAR(48)

NAINCY SHAHDEO

INTRODUCTION

Financial Market

Capital Market Money Market

CAPITAL MARKET :

Capital market is the part of financial system which is concerned with raising capital funds by dealing in share, Bonds, and other long term investments.

The market where investment instruments like bonds, equities and mortgages are traded is known as capital market.

EXAMPLE

ABC TEXTILE PVT. LTD WANTS TO EXPANDS ITS BUSINESS

MAKES A BUSINESS DEAL WITH GUCCI BRAND TO EXPORT TEXTILE CLOTHS TO THEIR MANUFACTURING UNIT

WHERE CAN HE GET MONEY FROM?

1. FROM BANK

ABC Textile can approach banks, but it will not prove to be healthy option because :

Bank will charge high rate of interest.

Lendings of loans is a very tedious task. Bank first scrutinizes the papers/ documents, verifies them.

Very time consuming.

Thus, this idea is not an effective one.

2. Can go public and get listed on the Stock companies.

Major suppliers of funds in Capital Market

•Commercial banks.

• Insurance companies.

•Business corporation.

Types of Capital Market

Primary market.

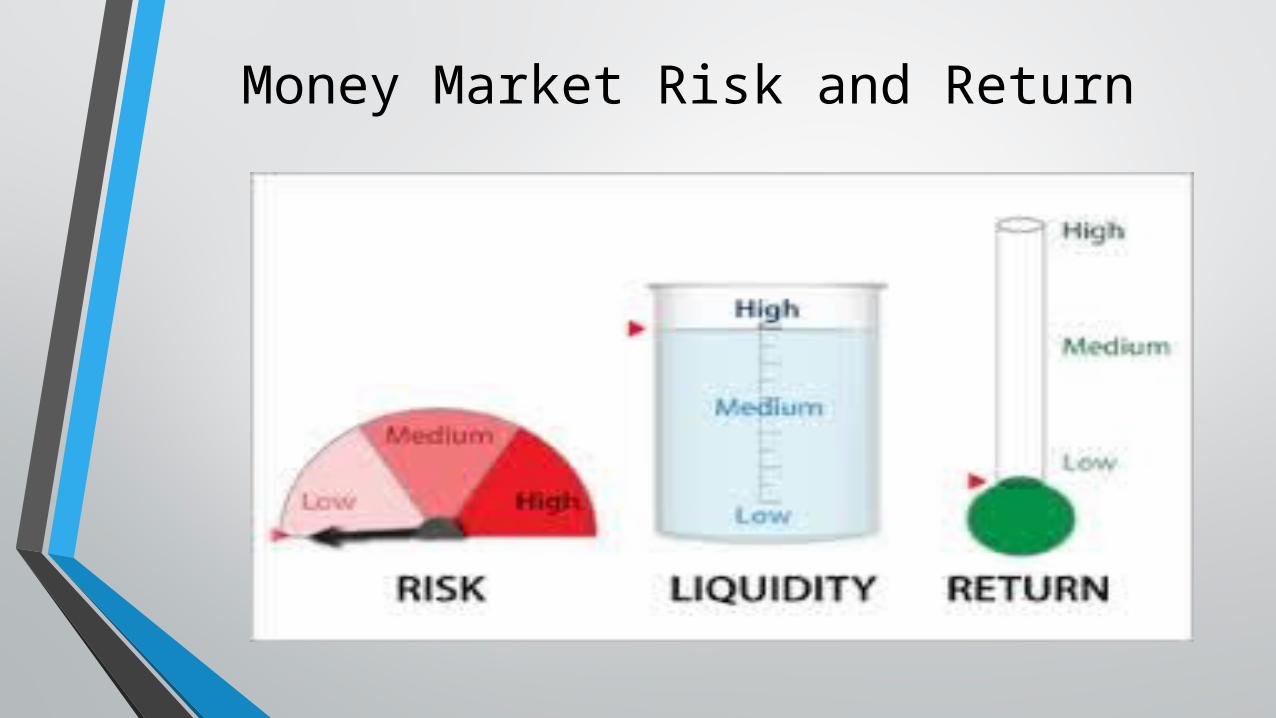

Money Market

• Money market is a mechanism that’s deals with short term funds ( less than 1 year)

• A segment of financial market in which financial instrument with high liquidity and very short maturities are traded.

Need for Money Market

• Need for short term funds by banks.

• Outlet for deploying funds on short term basis.

• Need to keep the SLR as prescribed.

• Regulate the liquidity and interest rates.

Instruments of Money Market

• Certificate of Deposit

• Call money/notice money

• Commercial paper

• Treasury bills

Money Market Risk and Return

Some problems which leads to financial market reform in india in 1991.

• Economic instability/fiscal deficit.

• Gulf war/ crisis.

• Shortage of foreign exchange reserves.

• Burden of debt/ liquidity crisis.

• Inefficient industrial growth.

• Fall growth rate.

• Inflationary pressure.

• Poor performance in financial sector.

• The Indian currency, the rupee, was inconvertible and high tariffs and import licensing prevented foreign goods reaching the market.

Reforms package included in Financial Market in INDIA

• There was a economic reform in INDIA in 1991 to provide an environment of sustainable growth and stability.

• Liberalisation and globalisation was the principle instrument for achieving the aim of reform

• The govt. therefore, adopted a phased approach to liberalise the various sector of economy.

Contd.

• Deregulation of interest rates.

• Encouraging direct foreign investment as a source of technology upgradation.

• Disinvestment of PSUs

• Reform of tax system to create a broader base of taxation by moderating tax rates.

• India also operated a system of central planning for the economy, in which firms required licenses to invest and develop.

Hence, the steps to improve the financial system were an integral part of the economic reform initiated in 1991.

MONEY MARKETCondition of Money Market in the pre-reform

period (before 1991)Financial system functioned in an environment of constriction, driven primarily by fiscal compulsions. It was geared to provide significant support for Government expenditure.

The monetary and debt management policy was underlined by excessive monetisation of Central Government's fiscal deficit.

Money and Govt. Securities market did not display any vibrancy and had limited significance in the indirect conduct of monetary policy.Money Market instruments were few.

Market had a narrow base and limited to a few participants - commercial banks and six all India Financial Institutions

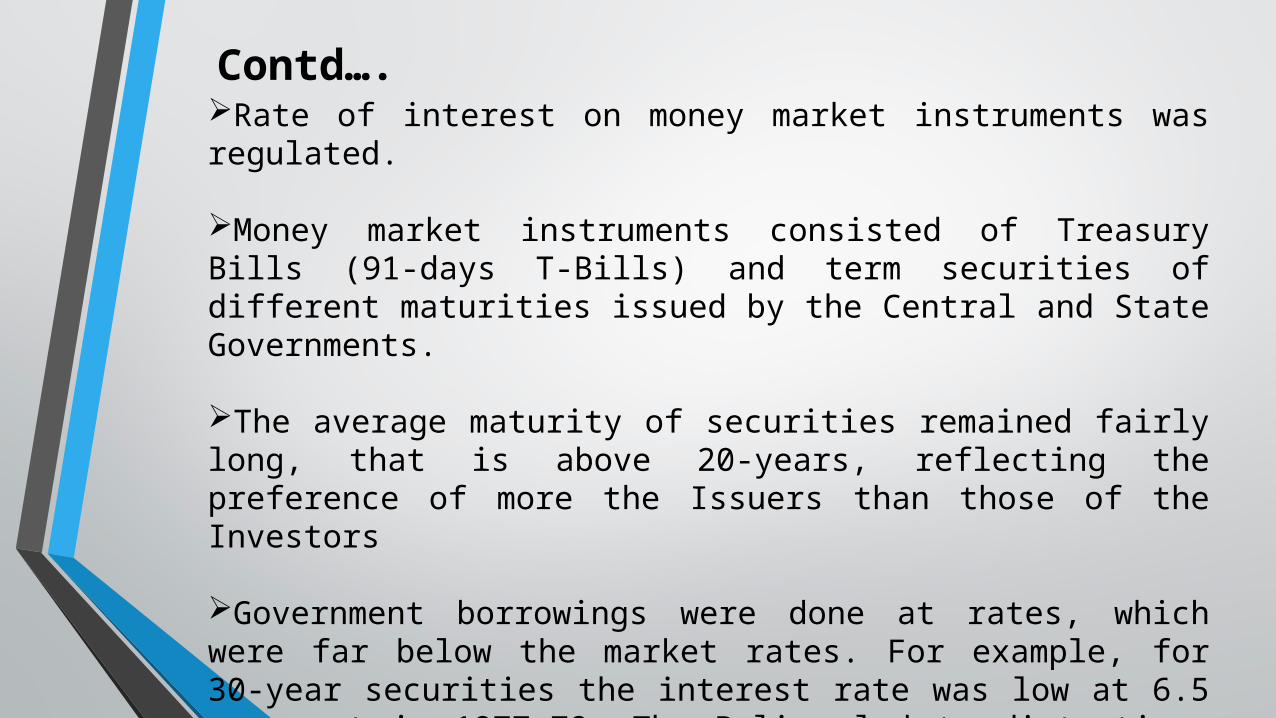

Rate of interest on money market instruments was regulated.

Money market instruments consisted of Treasury Bills (91-days T-Bills) and term securities of different maturities issued by the Central and State Governments.

The average maturity of securities remained fairly long, that is above 20-years, reflecting the preference of more the Issuers than those of the Investors

Government borrowings were done at rates, which were far below the market rates. For example, for 30-year securities the interest rate was low at 6.5 per cent in 1977-78. The Policy led to distortions in the Banking System with high lending rates on certain segments combined with relatively low interest rates on deposits.

Contd….

REFORMS IN THE INDIAN MONEYMARKET

Indian Government appointed a committee under the chairmanship of Sukhamoy Chakravarty in 1984 to review the Indian monetary system. Later, Narayanan Vaghul working group and Narasimham Committee was also set up. As per the recommendations of these study groups and with the financial sector reforms initiated in the early 1990s, the government has adopted following major reforms in the Indian money market.Deregulation of the Interest Rate : In recent period the government has adopted an interest rate policy of liberal nature. It lifted the ceiling rates of the call money market, short-term deposits, bills rediscounting, etc. Commercial banks are advised to see the interest rate change that takes place within the limit. There was a further deregulation of interest rates during the economic reforms. Currently interest rates are determined by the working of market forces except for a few regulations.

Money Market Mutual Fund (MMMFs) : In order to provide additional short-term investment revenue, the RBI encouraged and established the Money Market Mutual Funds (MMMFs) in April 1992. MMMFs are allowed to sell units to corporate and individuals. The upper limit of 50 crore investments has also been lifted. Financial institutions such as the IDBI and the UTI have set up such funds.

REFORMS IN THE INDIAN MONEYMARKET

Establishment of the DFI : The Discount and Finance House of India (DFHI) was set up in April 1988 to impart liquidity in the money market. It was set up jointly by the RBI, Public sector Banks and Financial Institutions. DFHI has played an important role in stabilizing the Indian money market.Liquidity Adjustment Facility (LAF) : Through the LAF, the RBI remains in the money market on a continue basis through the repo transaction. LAF adjusts liquidity in the market through absorption and or injection of financial resources.Electronic Transactions : In order to impart transparency and efficiency in the money market transaction the electronic dealing system has been started. It covers all deals in the money market. Similarly it is useful for the RBI to watchdog the money market.Establishment of the CCIL : The Clearing Corporation of India limited (CCIL) was set up in April 2001. The CCIL clears all transactions in government securities, and repose reported on the Negotiated Dealing System.Development of New Market Instruments : The government has consistently tried to introduce new short-term investment instruments. Examples: Treasury Bills of various duration, Commercial papers, Certificates of Deposits, MMMFs, etc. have been introduced in the Indian Money Market.

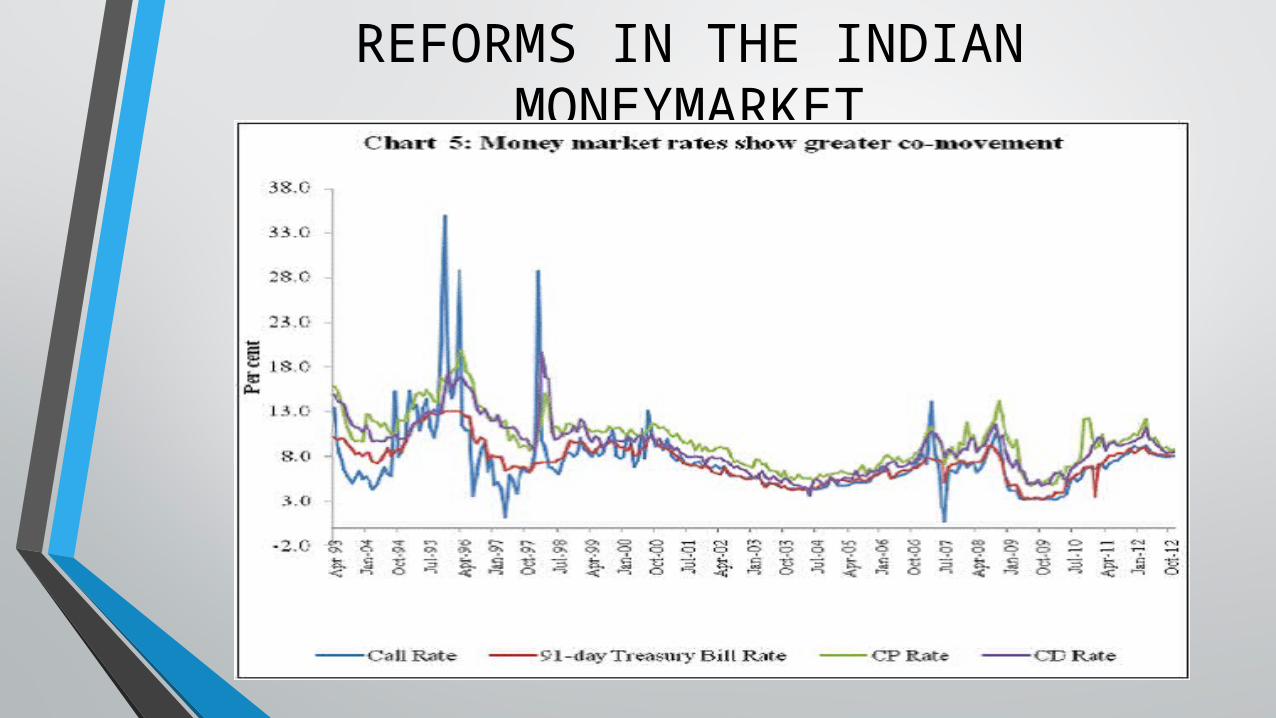

These are major reforms undertaken in the money market in India. Apart from these, the stamp duty reforms, floating rate bonds, etc. are some other prominent reforms in the money market in India. Thus, at the end we can conclude that the Indian money market is developing at a good speed.

REFORMS IN THE INDIAN MONEYMARKET

REFORMS IN THE INDIAN MONEYMARKET

CAPITAL MARKET REFORMSPrimary Capital Market:

• SEBI was set up in 1988 as non statutory body. It was given statutory powers through the enactment of SEBI Act, 1992 for regulating securities market.

• Diversification of infrastructure of Primary Capital market by setting up large number of merchant bankers, investment and consulting agencies.

• Institutionalization of market started in 1987-88 when mutual funds sponsored by banks and financial institutions were set up and gained momentum in 1990 when mutual funds were set up in private sector.

• The requirement to issue shares at par value of Rs. 10 and Rs. 100 was withdrawn.

• Companies are required to disclose all material facts, specific risk factors associated with their projects while launching public issues and it must ensure fair and truthful disclosures.

• To reduce the cost of issue, underwriting by the issuer was made optional, subject to the conditions.

CAPITAL MARKET REFORMS• Allowing Foreign Institutional Investors (such as mutual funds, pension funds,

country funds, etc.) to operate in Indian market and invest in govt. securities and treasury bills.

• Besides merchant bankers some other intermediaries like mutual funds, portfolio managers, underwriters, custodian of securities also been brought under the purview of SEBI.

• A code of conduct for advertisement of mutual funds is issued for banning them making claims that might mislead the public.

• Shares will now be allotted on proportionate basis, with predetermined minimum allotment being equal to minimum application size.

• For issues priced below Rs. 500 per share, the face value of the share should be Rs. 10 per share and for the issue priced above Rs. 500, the minimum face value should not go below Rs. 1.

• Central Listing Authority was set up to ensure uniform and standard practices for listing the securities on stock exchanges.

• Electronic clearing services (ECS) was extended to refunds arising out of public issue to ensure fast and hassle-free refunds.

CAPITAL MARKET REFORMS Secondary Capital Market:

• The new stock exchange at national level was set up in the 1990s.

Over the Counter Exchange of India, 1994

Inter-connected Stock Exchange of India, 1999

• Framing and Implementing codes of corporate governance by the committee appointed by SEBI under the chairmanship of Kumar Mangalam Birla, to protect the interest of stakeholders.

• Companies are allowed to buy-back their own shares for capital restructuring, subject to conditions that buy-back must not exceed 25% of the paid up capital and it must be done to enhance liquidity and wealth of shareholders.

• In February 1999, trading terminals were allowed to be set up abroad to facilitate market participation by non-residents. Internet trading was permitted in February 2000.

CAPITAL MARKET REFORMS

• It is mandatory for all brokers to disclose all details of block deals. Block deals includes trading which accounts more than 0.5% of equity shares of that listed company

• FII’s and NRI’s were permitted to invest in all exchange-traded derivative contracts and participate in delisting offers and disinvestment by the government in listed companies.

• Securities Contract Regulation Act, 2004 was introduced to protect the interest of minority shareholder.

SCAM

obtaining money by means of deception including fake personalities, fake photos, fake template letters, non-existent addresses and phone numbers, forged documents.

HARSHAD MEHTA

• was an Indian stockbroker.

• is alleged to have engineered the rise in the BSE stock exchange in 1992

• Exploiting several loopholes in the banking system, Mehta and his associates siphoned off funds from inter-bank transactions and bought shares heavily at a premium across many segments, triggering a rise in the Sensex.

Overview of the Scam

• Triggered a rise in the BSE between April 1991 to May 1992.

• Traded shares at premium

• Diverted funds of Rs 40 billion- The “Securities Scam” refers to a diversion of funds to the tune of Rs. 3,500 crores from the banking system to various stockbrokers in a series of transactions (primarily in Government securities) during the period April 1991 to May 1992.

•

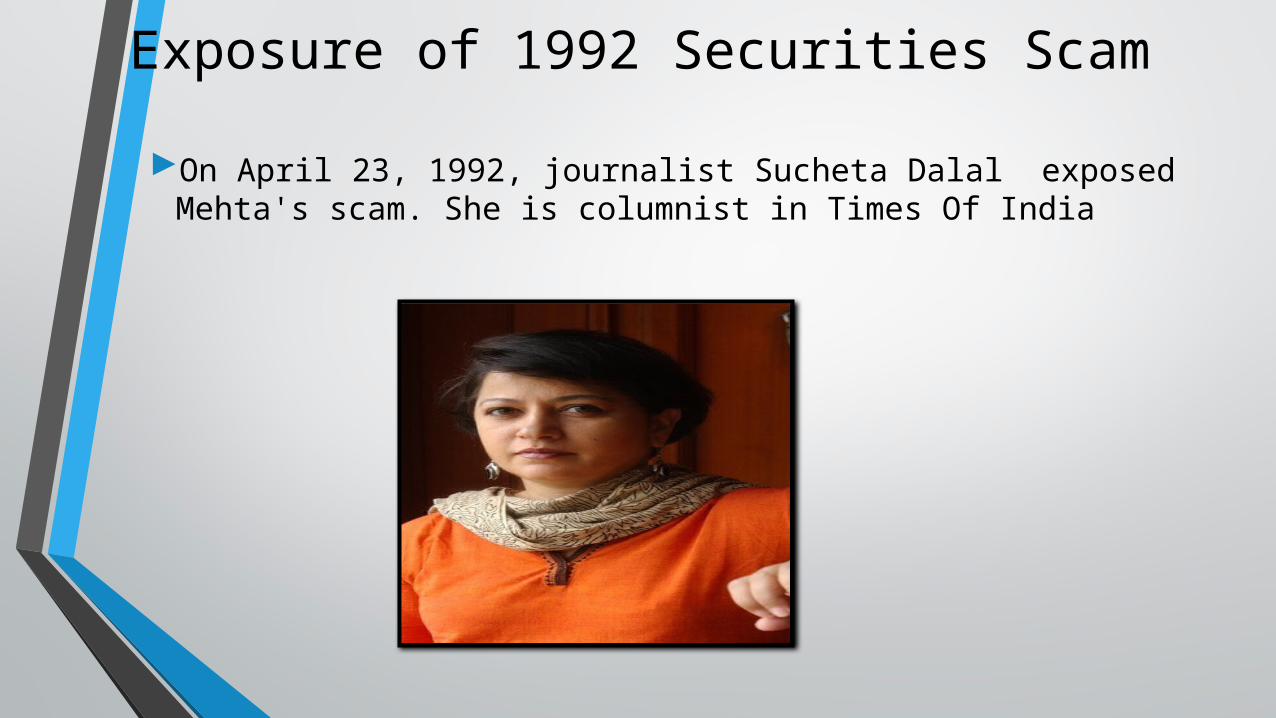

On April 23, 1992, journalist Sucheta Dalal exposed Mehta's scam. She is columnist in Times Of India

Exposure of 1992 Securities Scam

•Capital market scam-It is basically fraud done in the capital market with the investors by manipulating the facts in order to attain enormous profit

• The story is quit similar only the star cast has changed .

• Both are big bulls

• Both big bulls used to buy stocks at rock-bottom prices and push it up.

BOTH GAINED POPULARITY FOR

• In both these scams banks were involved. The HM scam was related to bankers receipt while it was pay orders in KP scam

• In HM scam foreign banks including citibank, standard chartered and ANZ grindlays were involved and in KP scam foreign instituional investors including credit suisse and JM Morgan stanley were invovled.

• In HM scam state Bank of India suffered a loss of 660 crores while KP owes around Rs. 130 crore to Bank of India.

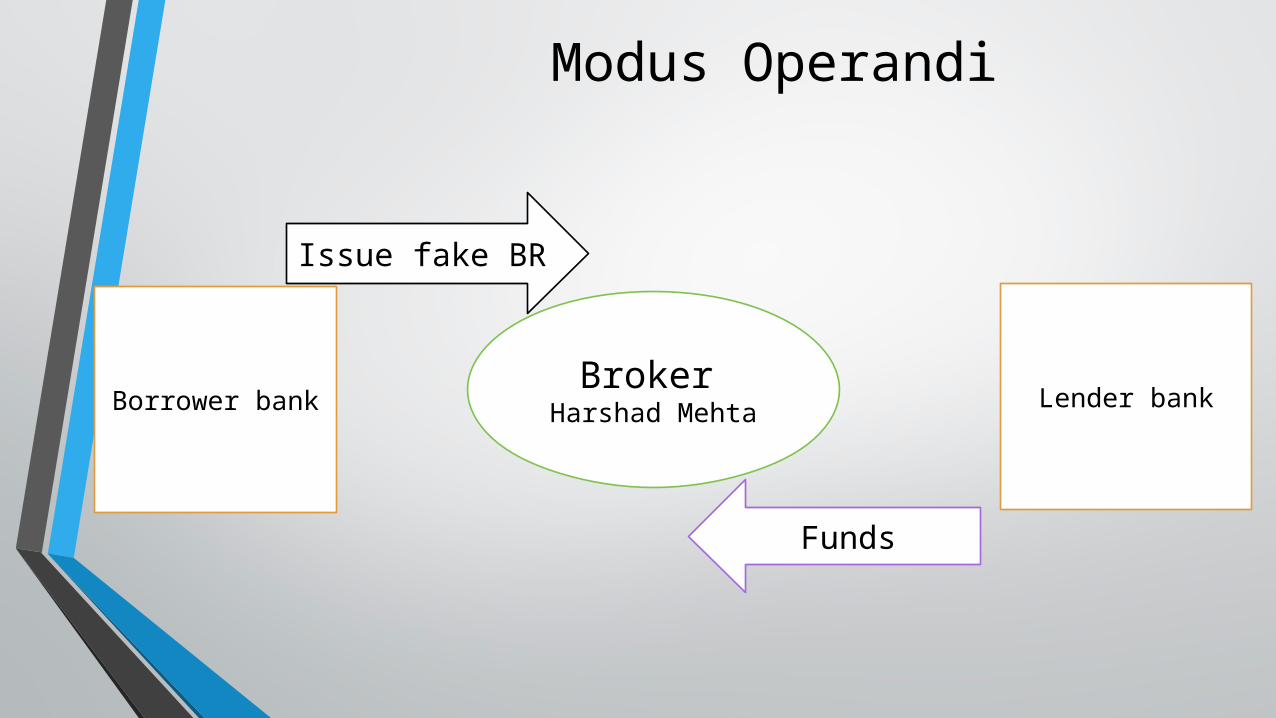

The Mechanics of the ScamSTEPS INVOLVED-

1) The settlement process in the govt securities market become broker intermediate that is delivery and payment started getting routed through a broker instead of being made directly between the transacting banks That is, the seller hands over the securities to the broker who passes them on to the buyer, while the buyer gives the cheque to the broker who then makes the payment to the seller.

2) The broker through whom the payment passed on its way from one bank to another found a way of crediting the money into his account though the account payee cheque was drawn in favor of bank

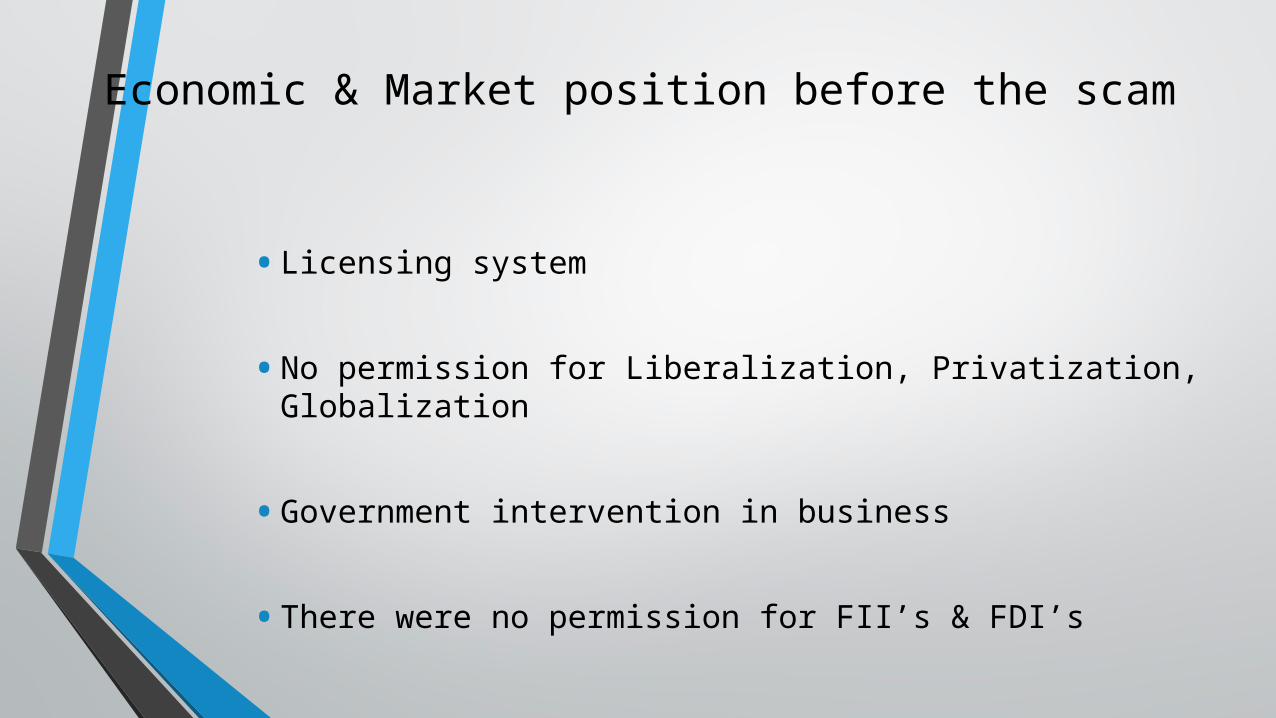

• Licensing system

• No permission for Liberalization, Privatization, Globalization

• Government intervention in business

• There were no permission for FII’s & FDI’s

Economic & Market position before the scam

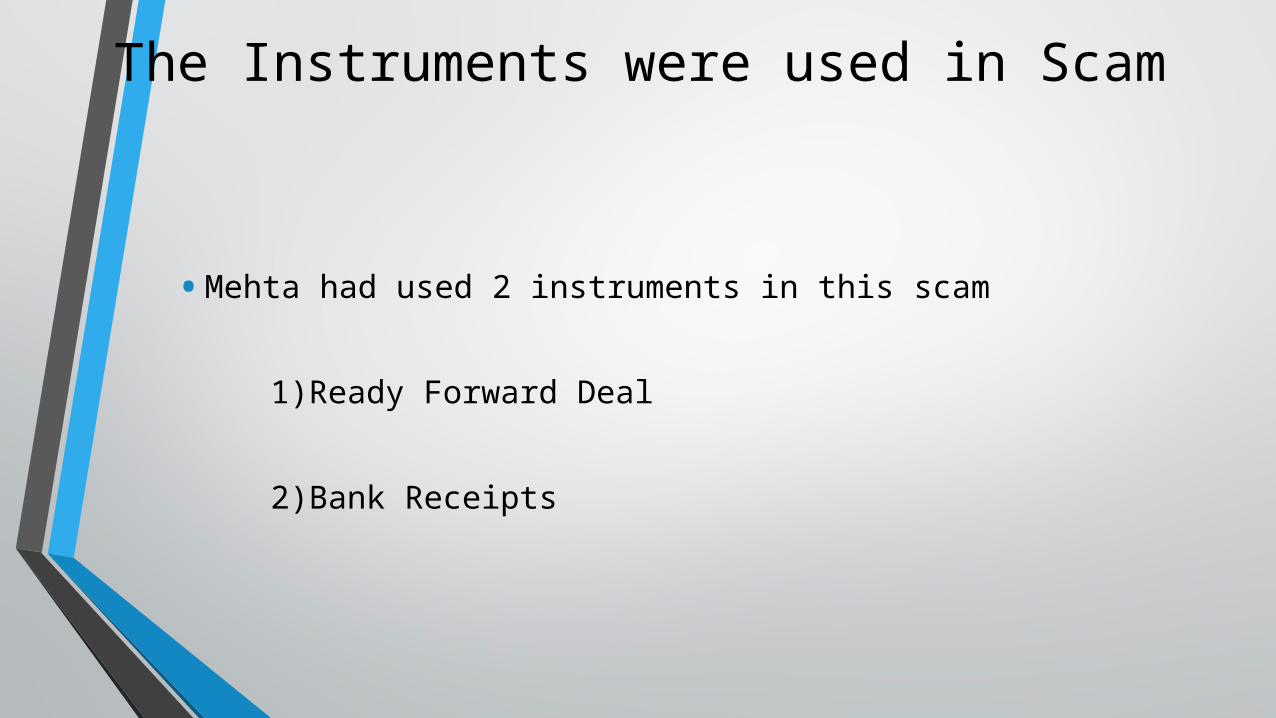

• Mehta had used 2 instruments in this scam

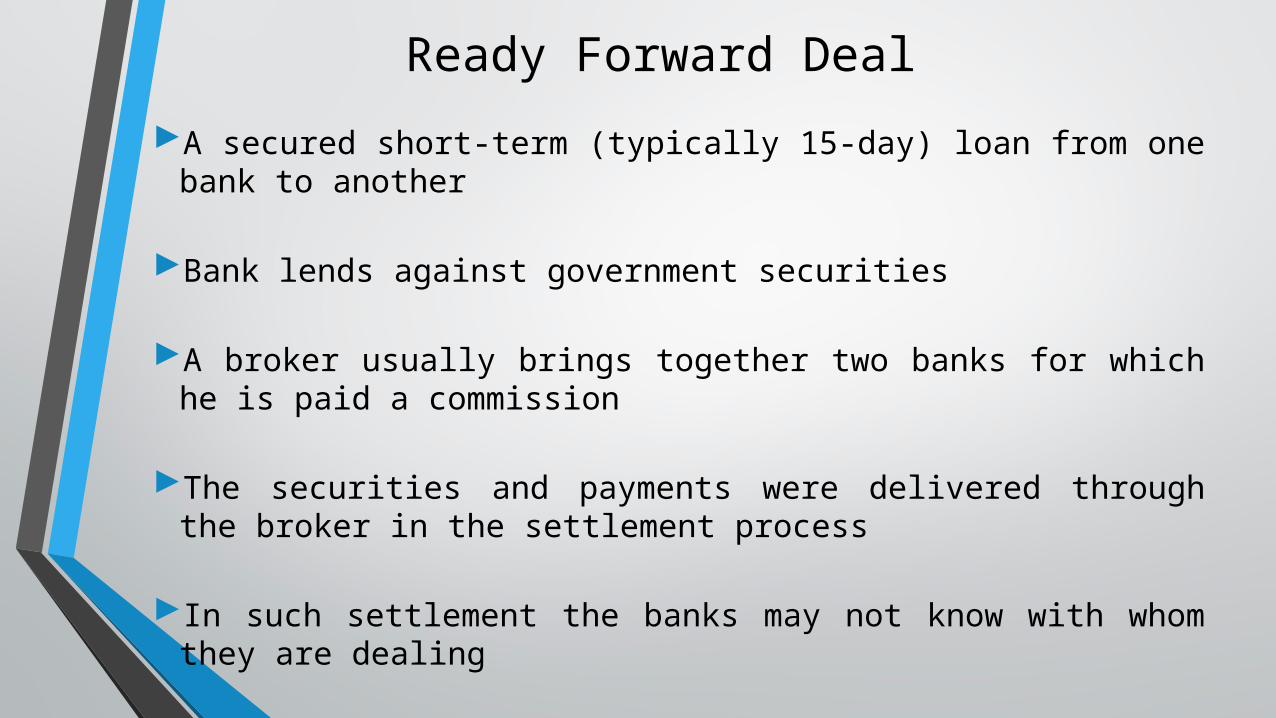

1)Ready Forward Deal

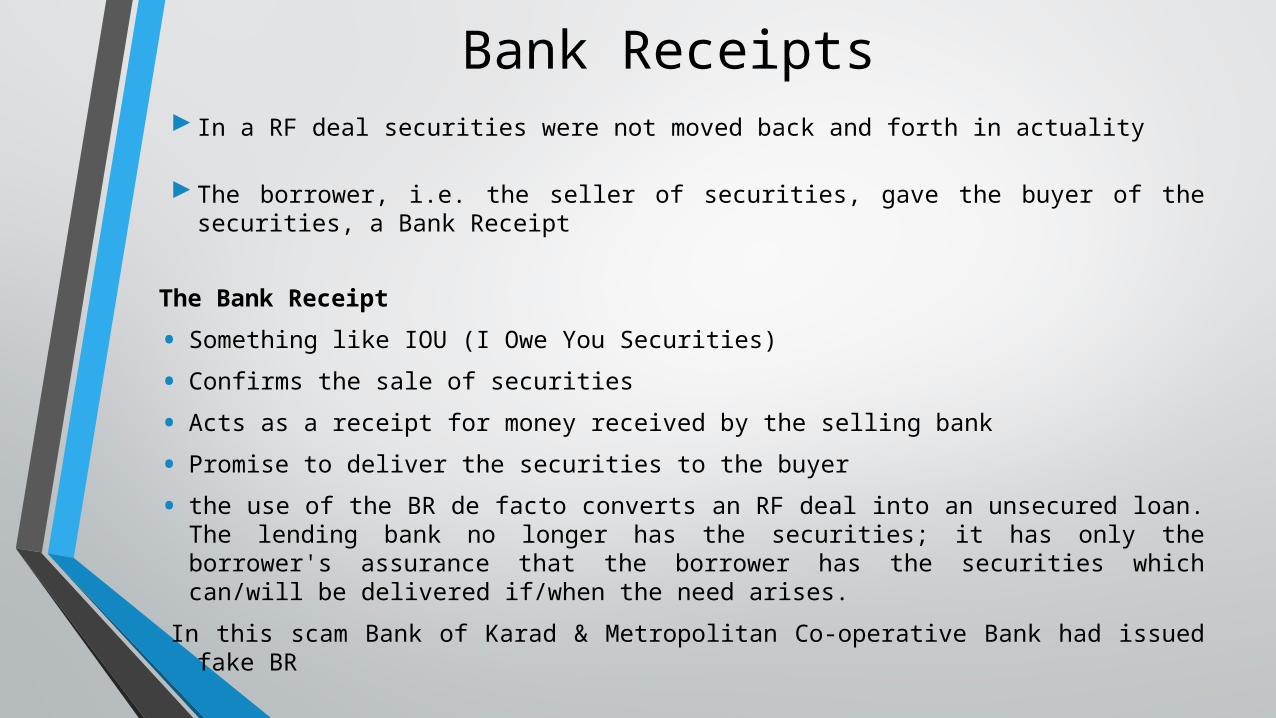

2)Bank Receipts

The Instruments were used in Scam

A secured short-term (typically 15-day) loan from one bank to another

Bank lends against government securities

A broker usually brings together two banks for which he is paid a commission

The securities and payments were delivered through the broker in the settlement process

In such settlement the banks may not know with whom they are dealing

Ready Forward Deal

In a RF deal securities were not moved back and forth in actuality

The borrower, i.e. the seller of securities, gave the buyer of the securities, a Bank Receipt

The Bank Receipt

• Something like IOU (I Owe You Securities)

• Confirms the sale of securities

• Acts as a receipt for money received by the selling bank

• Promise to deliver the securities to the buyer

• the use of the BR de facto converts an RF deal into an unsecured loan. The lending bank no longer has the securities; it has only the borrower's assurance that the borrower has the securities which can/will be delivered if/when the need arises.

In this scam Bank of Karad & Metropolitan Co-operative Bank had issued fake BR

Bank Receipts

Modus Operandi

Borrower bankBroker

Harshad Mehta Lender bank

Issue fake BR

Funds

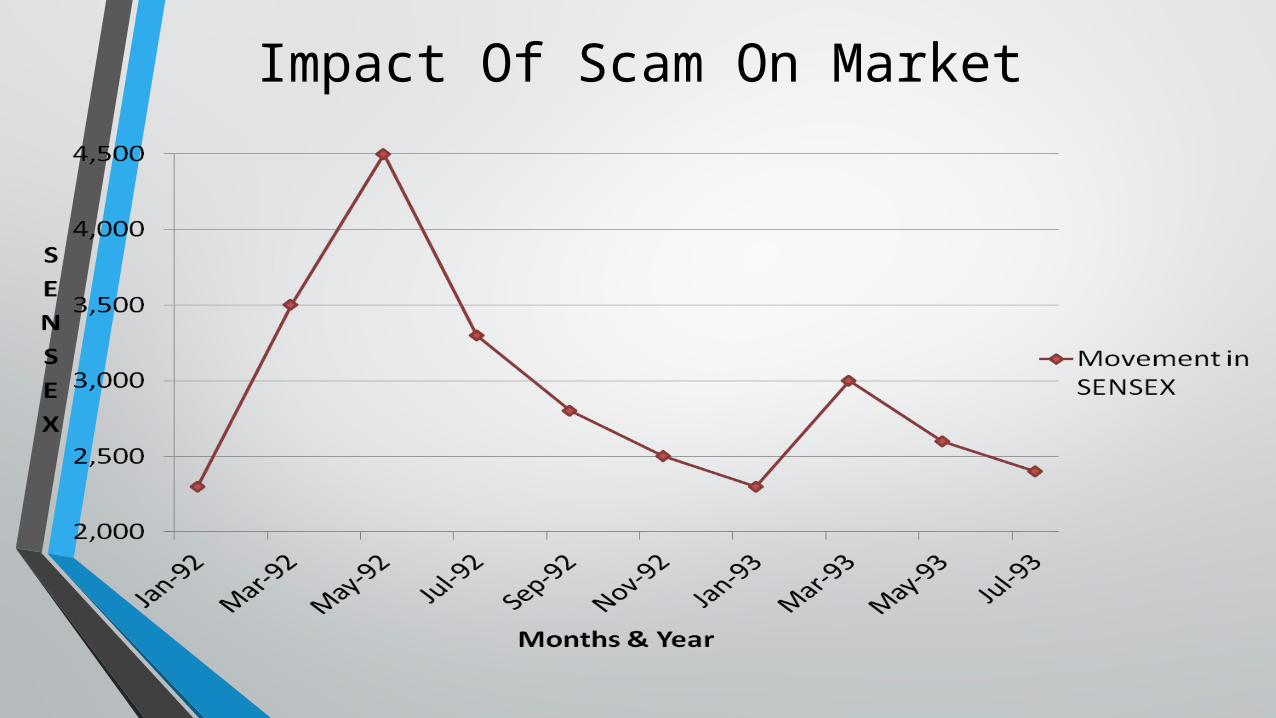

Impact Of Scam On Market

IMPACT OF THE SCAM

• The immediate impact of the scam was a sharp fall in the shares prices . The index fell from 4500 to 2500 representing a loss of Rs. 100000 crores in the market capitalization.

• The government liberalization policies came under sever criticism after the HM scam

• Bowing to the political pressure and the bad press it received during the scam, the liberalization was put on hold for a while by the government

• SEBI postponed sanctioning of private sector mutual fund

• Sensex fell from 4500 to 2500 loosing 100,000 crore in market capitalization

• The liberalization policies were put on hold by the government.

• Inability of Indian companies to raise capital in world markets

Steps taken by SEBI in response to the scam

• Special court set up for the trial

• Special ordinance passed- creation of tainted shares

• Banning of RF deals.

• Various committees were set up

• In order to increase liquidity, SEBI allowed banks to offer collateralized lending only through BSE and NSE

• On march 8,2001, the SEBI banned short sales.In simple words,it means that all short sales have to be covered by an equal amount of long purchases.

• Ketan Parekh is a former stock broker from Mumbai, India Popularly known as ‘Bombay Bull’.

• KP arrested on 30 march 2001 for the security market scam known as Ketan Parekh scam.

• He was convicted in 2008, for involvement in the Indian stock market manipulation scam in late 1999-2001.

• Currently he has been debarred from trading in the Indian stock exchanges till 2017

• He was a trainee of Harshad Mehta.

• Ketan Parekh can be best described as the Pied Piper of Dalal Street

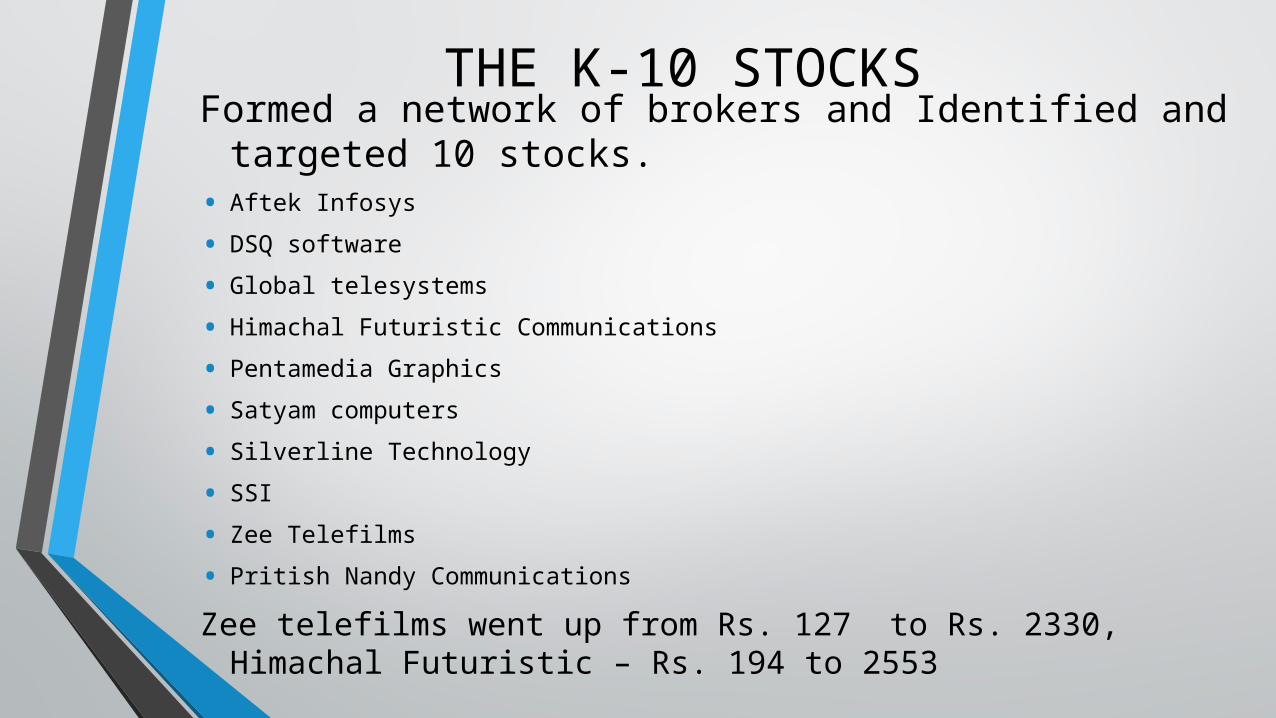

• KP took advantage of low liquidity in certain stocks which later came to be known as ‘K-10’ Stocks

• Held significant stakes in the K-10 companies

• The buoyant stock markets from January to July 1999 helped the K-10 stocks increase in value substantially

• As a result other brokers and fund mangers started investing heavily in these stocks.

KETAN PAREKH SCAM

Formed a network of brokers and Identified and targeted 10 stocks.

• Aftek Infosys

• DSQ software

• Global telesystems

• Himachal Futuristic Communications

• Pentamedia Graphics

• Satyam computers

• Silverline Technology

• SSI

• Zee Telefilms

• Pritish Nandy Communications

Zee telefilms went up from Rs. 127 to Rs. 2330, Himachal Futuristic – Rs. 194 to 2553

THE K-10 STOCKS

• Though KP was a successful broker, he did not have money to buy large stakes as he held the stakes of more than Rs 750 million in July 1999, according to a report.

• Analyst claimed that he had borrowed from various companies and banks for this purpose.

• He bought shares when they were trading at low price and saw the prices go up in the bull market while continuously trading.

• When the prices was high enough, he pledged the shares with banks as collateral for funds, and also borrowed from the companies like HFCL.

• It could not have been possible without the involvement of banks.

FACTORS THAT HELPED KETAN PAREKH

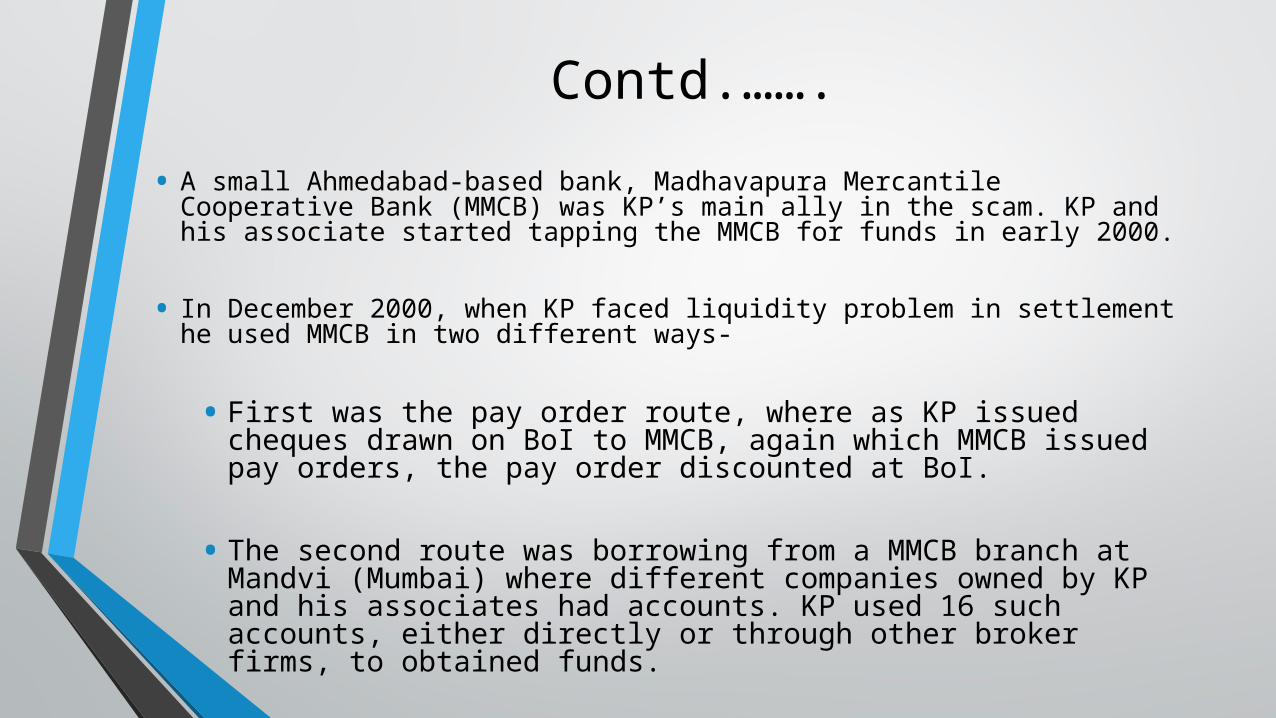

• A small Ahmedabad-based bank, Madhavapura Mercantile Cooperative Bank (MMCB) was KP’s main ally in the scam. KP and his associate started tapping the MMCB for funds in early 2000.

• In December 2000, when KP faced liquidity problem in settlement he used MMCB in two different ways-

• First was the pay order route, where as KP issued cheques drawn on BoI to MMCB, again which MMCB issued pay orders, the pay order discounted at BoI.

• The second route was borrowing from a MMCB branch at Mandvi (Mumbai) where different companies owned by KP and his associates had accounts. KP used 16 such accounts, either directly or through other broker firms, to obtained funds.

Contd.…….

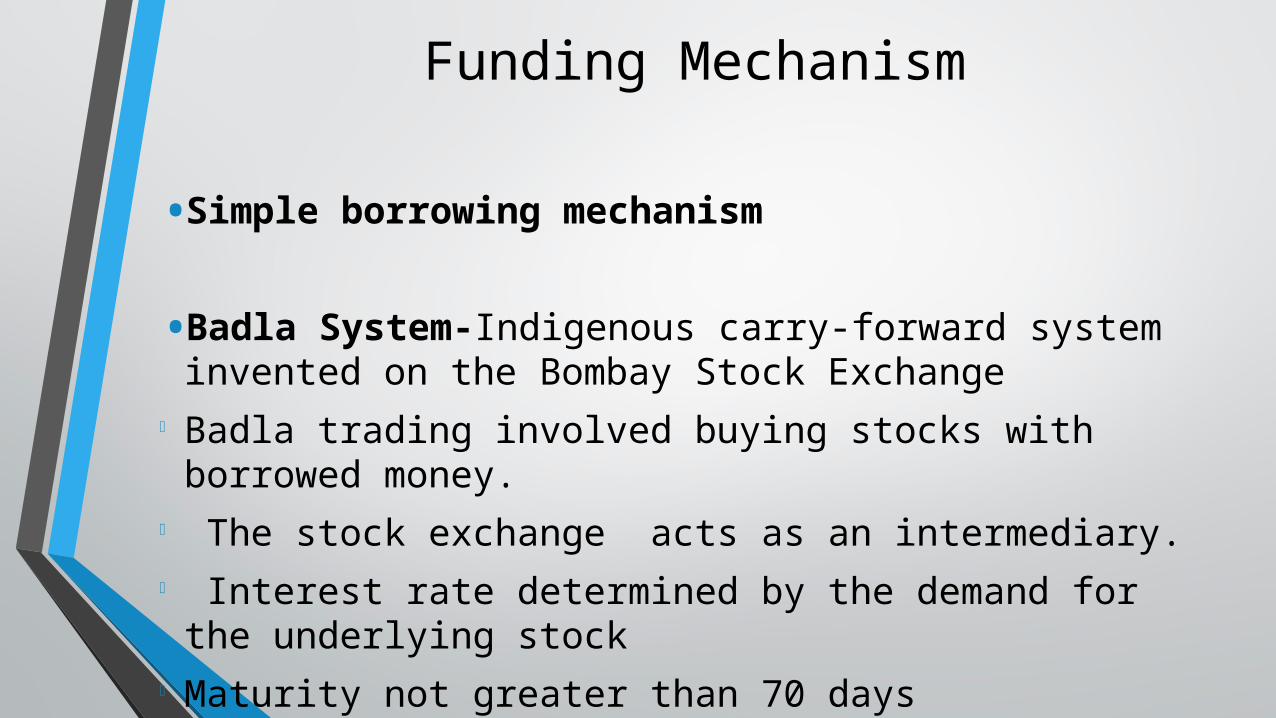

Funding Mechanism

•Simple borrowing mechanism

•Badla System-Indigenous carry-forward system invented on the Bombay Stock Exchange

Badla trading involved buying stocks with borrowed money.

The stock exchange acts as an intermediary. Interest rate determined by the demand for the

underlying stock Maturity not greater than 70 days

How was it detected

• Stock market crash of 2000

• KP started borrowing heavily

• Attempted to rig the price upwards and later sell.

• But failed to do so.

• IT department found discrepancies in sources of funds of KP

• Routine market surveillance of 5 stocks

ImplicationsRBI ordered some banks to furnish data of Capital market exposure

BSE President Anand Rathi’s resignation added to continued downfall of sensex

One of the biggest Fall in BSE -700 points

KP and other traders were banned from trading for 17 years

Short selling was banned for 6 months.

Badla system was banned

All shares that were put as collaterals should be done so through NSE and BSE.

RS. 2000 billion lost

The Retail investors were the worst hit

SBI, BOI, PNB had to suffer huge losses and MMCB also suffered huge losses

Opened debate over banks financial capital market operations, Lending funds against collateral security, Dual control of co-operative banks

Ketan Parekh was arrested by CBI on 30th March 2001. He was charged befrauding Bank of India by almost $20 Million

• To revive the markets SEBI imposed restriction on short sales

• It suspended all the broker member directors of BSE’S governing board

• SEBI also banned trading by all stock exchange presidents, vice presidents and treasurers

• SEBI allowed banks for collateralised lending only through BSE and NSE

• SEBI launched immediate investigation on the scam and inspected the books of several brokers suspected of triggering the crash

• It suspended all the broker member directors of BSE’S governing board

• SEBI also banned trading by all stock exchange presidents, vice presidents and treasurers

• RBI started inspecting accounts and sub-accounts twice a year in spite of once in two year.

• SEBI allowed banks for collateralised lending only through BSE and NSE

SEBI’S ROLE AFTER SCAM

SATYAM COMPUTER SERVICE LIMITED

• Satyam Computer Services Limited was founded in 1987 by Mr. B Ramalinga Raju.

• The company offered consulting and information technology services spanning various sectors, including engineering and product development, supply chain management, client relationship management, business process management and business intelligence.

THE SATYAM SCAM

• The satyam computer services scandal was a corporate scandal that occurred in India in 2009 where chairman Ramalinga Raju confessed the company’s accounts had been falsified.

• This was perhaps India’s biggest corporate case where M/s Satyam Computer Services caused loss to the investors to the tune of Rs.14,162crores.

• Ramalinga Raju had mislead various investors and was arrested by The Andhra Pradesh police on charges of breach of trust, conspiracy, cheating, falsification of records.

• He admitted that satyam’s fixed deposits which supposedly grew from Rs. 3.35 crore in 1998-99 to a massive Rs.3320.19 crore in 2007-08 all were fake.

• Raju had also used dummy accounts to trade in Satyam's shares.

• Funds from Satyam were diverted to Maytas

• On 22 January 2009, CID told in court that the actual number of employees is only 40,000 and not 53,000 as reported earlier and that Mr. Raju had been allegedly withdrawing INR 20 crore rupees every month for paying these 13,000 non-existent employees.

• A botched acquisition attempt involving Maytas in December 2008 led to a plunge in the share price of Satyam.

• In January 2009, Raju indicated that Satyam's accounts had been falsified over a number of years.

• He admitted to an accounting dupery to the tune of 7000 crore rupees or 1.5 Billion US Dollars and resigned from the Satyam board on January 7, 2009.

REASONS FOR SATYAM SCAM:-• Raju wanted to take over his MAYTAS INFRA and MAYTAS

PROPERTIES.(company of his sons).

• He was blamed that he was using the funds of the investors for the family business.

• World bank had banned the satyam to take any services for 8 years (due to illegal profit and lack of essential document).

IMPACT OF SATYAM SCAM IN INDIAN ECONOMY

• Satyam shares witnessed biggest single day fall in stock market and sensex fell by 7.25%

• Jobs of 50000 technocrats were at risk

• GDP fell by 0.4%

• IT sector suffered a downturn.

• Before the scandal its share price was Rs 300 in oct2008. just after this scandal the share price went down to Rs 6.30.

• Indian firms are looking into methods to avoid scenarios of such scams within their companies.

CRB SCAM

The company offered various schemes like merchant banking , leasing and hire purchase , bill discounting and corporate funds management , fixed deposit and resources mobilization , mutual funds and asset management , international finance and forex operations.

CRB caps was also very active in stock-broking having a card both on the BSE and the NSE.

CRB Corporation Ltd raised another Rs.84 crores through three public issues between May 1993 and December 1995.

In August 1994 ,C R Bhansali launched CRB mutual funds (CRBMF) which raised Rs.230 crores from the market through Arihant Mangal Growth Scheme.

The Man and the Mess!!!!!!!!!!

Suspicions arose when CRB cap’s networth grew from Rs.2 crores in 1992 to Es.430 crores in 1996

It was in mid 1996 that reports regarding frauds being committed by the RBI group began appearing in the media.

Bhansali Was Charged With Fraud, Cheating , And Siphoning Off Of Funds From SBI.

Defrauding the SBI

In May’96 current account opened in SBI ‘s Mumbai branch

Only current account facility granted

No overdraft allowed

Dividend warrants treated as demand drafts

For about nine months all went well

SBI ‘s findings

In March’97 SBI discovered the fraud

Bhansali was investigated immediately

SBI accused Bhansali of printing 1800 fake dividend warrants

Bhansali used fake accounts in Chennai, Calcutta and Rajasthan to withdraw these dividends

CRB Caps had an outstanding liability on 50 crores

Action’s taken by SBI

SBI officials met with Bhansali in April 1997

SBI demanded immediate repayment of the over drafted amount

All property to be submitted as collateral security

The Systemic Rot

Lack of communication between the banks, RBI and the government officials

Blame game between RBI and SEBI

RBI claimed that it had no power to examine the asset quality

In Dec’94 SEBI conducted a routine investigation

9 months ban on CRBMF

The Aftermath

Far reaching impacts on the economy

Declining investor confidence in banks

Poor performance of NBFC’s

Making investors more aware

Creation of smart investors

CONTROLLING THE SCAMS•In addition to the present statutory requirement, companies should be required to institute sufficient internal management controls.

•Management should ensure that the internal audit staffs are able to prevent and detect financial statement fraud.

•Companies whose shares are publicly traded should be required to have audit committees to monitor the internal control system and provide important links to the internal audit staff.

•Sanctions against the perpetrators of financial statement fraud should be increased by imposing fines and other deterrent measures like barring from corporate office. However, in this case, there is a need to prevent innocent managers from being too risk averse.

CONCLUSION

The financial sector has a vital role in promoting efficiency and growth.It intermediates the flow of funds from those who want to save a part of their income to those who want to invest in productive assets. Till about two decades ago. a large part of household savings was either invested directly in physical assets, or put in bank deposits and Government small saving schemes.

lt is only since the late eighties that the equity market has started to play a role in this intermediation process. Other markets such as the medium to long term debt markets and short-term money markets, remain relatively segmented and underdeveloped. In recent decades, the Government and its subsidiary Institutions and agencies, have had an overwhelming and all encompassing rote. This has played a part in slowing the evolution and development of these markets. The extensive system of controls, rules, regulations and procedures, directly or indirectly affects the development of these markets. We need to clear this web in the interest of both savers and those who invest in productive assets.

CONCLUSIONThe two most serious problems in the financial system are •the lack of flexibility in intermediary behavior •the segregation of various markets and sets of financial intermediaries.

Well developed markets are interconnected; demand-supply imbalances in one market overflow into related markets thereby dampening shocks and disturbances. This inter-connection also ensures that interest rates and returns in any market, reflect the broad demand-supply conditions in the overall market for savings. A rise in the demand for funds for investment, above the existing flow of funds from savings, leads to a rise in the interest rate or rate of return in all markets. Conversely, a decline in demand for kinds for investment below saving, leads to a fall in interest rates across the board. This does not happen in segmented markets.

Consequently, adjustment to demand-supply imbalance m each segment was also very slow.. The widening and acceleration of reforms will increase the flexibility and responsiveness of the intermediaries and promote integration.

THANK YOU…