recession prep 101: investing in real estate during …...recession prep 101: investing in real...

TRANSCRIPT

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.1

Recession Prep 101: Investing in Real Estate During a Financial Crisis

It’s never fun to navigate stormy times—but economic downturns are just as much a part of investing as sunny upturns. Smart real estate investment strategies will keep you steady, despite rough waters.

This roller coaster start to 2020 might make you anxious about your investments, but the experts at BiggerPockets know exactly how to weather an economic downturn. Here’s what you need to know about today’s economy, including how to manage your existing investments and where to put your money next.

Mindy JensenExpertise: Real Estate Investing Basics, Real Estate News & Commentary, Personal Development, Flipping Houses, Landlording & Rental Properties, Personal Finance | 100+ Article Written

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.2

Table of Contents

How to Invest During an Economic Downturn Table of Contents Mapping the 2020 Economy Is a Recession Imminent? What Is Happening to the Economy? Don’t Repeat the Mistakes of the Past Protecting Your Investments During an Economic Downturn Patience Prevails Don’t Fall Into the Trap of 2008 Comparisons So What Should We Expect During This Downturn? Pay Attention to Interest Rates Real Estate Risk Factors During a Recession There May Be Relief in (Some) Rentals What Happens if a Recession Becomes a Depression? Current Real Estate Supply and Demand Dynamics Expect Dicey Times for Commercial Real Estate So What Should Real Estate Investors Expect in 2020? The Best Outcomes The Worst Outcomes Assessing Your Recession-Ready Investment Portfolio Recession-Proof Real Estate Investing Flipping Houses in a Recession Wholesaling Real Estate During a Recession Single-Family Buy-and-Hold Rentals During a Recession Multifamily Investing During a Recession Private and Hard-Money Lending During a Recession Note Investing During a Recession Investing in Commercial Real Estate During a Recession How to Make the Best Use of Your Time During a Downturn Increase Your Investing Knowledge Base Start Networking Dig Into Data Be Patient (But Pay Attention)

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.3

Mapping the 2020 Economy

An unprecedented global pandemic, the novel coronavirus—also known as COVID-19—has ground almost every nation on earth to a halt. What began as an outbreak within isolated regions in China has spread across the globe, growing exponentially. More people have now died from COVID-19 in Italy than in China, despite Italy being on lockdown for weeks.

There is currently no vaccine and early data shows it to be extremely transmittable. Mortality rate estimates vary, with current case fatality rate estimates hovering around 1.4 percent. The virus disproportionately affects the elderly and those with existing health conditions, especially autoimmune disorders.

The U.S. crossed 10,000 total infected persons on March 19th, accumulating 40 percent of that total in just 36 hours. We are still quite “behind the curve” on accurate data; we won’t know how widespread the virus is in America for a couple of weeks. We also don’t know how well our national healthcare infrastructure can handle shortages in protective gear, respirators, and ICU beds. This is due to several main factors:

• Coronavirus testing kits are in woefully short supply. Most people have to wait days to receive a test and another three to five days for the results.• The long incubation period lasts up to 14 days, or possibly even longer.

Because we don’t know when we’ll hit peak levels of infections, we can’t know how long the economy will be running at the drastically reduced level we’re seeing now. Logic dictates that some metro regions will have larger community outbreaks than others, but when it comes to interstate commerce, travel, and supply chains, a problem anywhere in the U.S.—especially in its largest cities—becomes a problem everywhere. The effects ripple and are felt by all.

As Larry Summers, former Harvard president and NEC chair under President Obama, put it recently, “Economic time has been stopped, but financial time has not been stopped.” We can seclude ourselves for a few weeks or months and our economy will “be there waiting for us,” financial time doesn’t pause. Rent and mortgage bills don’t stop. Credit card bills don’t stop. Suppliers don’t stop needing to get paid. Taxes are still collected.

It’s a different type of economic shock than what usually kicks off a recession. In essence, the world needs to limit economic activity in order to slow the spread of COVID-19.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.4

In short, nobody’s going anywhere and doing much of anything. It’s an otherworldly standstill—and we don’t know how long it will last.

Is a Recession Imminent?

We are most certainly headed for an economic recession. That is, for all intents, not up for debate anymore. Our current fiscal quarter, Q1 of 2020, will likely be considered the recession’s official start date.

LEARN MORE: What is a recession?

The National Bureau of Economic Research is the “official scorekeeper” of recessions. They have some discretion over what officially constitutes a recession, but the generally accepted definition is two fiscal quarters of declining economic output, as measured by gross domestic product (GDP).

NEARLY EVERY ECONOMIST AND INVESTMENT BANK NOW PREDICTS A GLOBAL RECESSION IN 2020—IN FACT, THE ECONOMIC CONSENSUS NOW IS THAT THE U.S. AND THE REST OF THE WORLD HAS JUST ENTERED A RECESSION WHICH COULD BE DEEPER THAN ANY RECESSION WE’VE SEEN IN OUR LIVES.

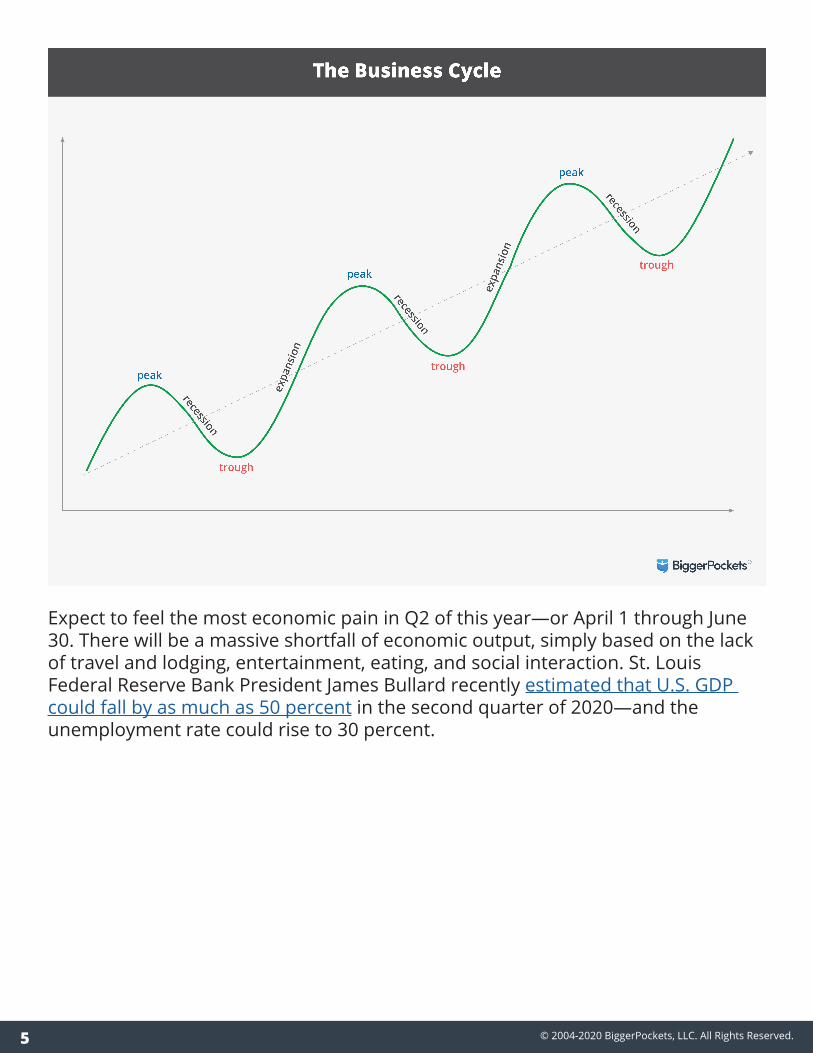

An economic recession is a natural byproduct of the business cycle, which acts like a wave. There are peak periods, where GDP growth is at its highest, and valleys, when GDP growth declines and a recession occurs. Why is the business cycle like this? Economies are made up of individual players, and individuals are prone to periods of greed, stagnation, optimism, and fear.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.5

Expect to feel the most economic pain in Q2 of this year—or April 1 through June 30. There will be a massive shortfall of economic output, simply based on the lack of travel and lodging, entertainment, eating, and social interaction. St. Louis Federal Reserve Bank President James Bullard recently estimated that U.S. GDP could fall by as much as 50 percent in the second quarter of 2020—and the unemployment rate could rise to 30 percent.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.6

In fact, nearly every economist and investment bank now predicts a global recession in 2020. Goldman Sachs estimates a six percent drop in U.S. GDP in the first three months of the year, followed by more than 25 percent cut to GDP in Q2.

The economic consensus now is that the U.S. and the rest of the world has just entered a recession which could be deeper than any recession we’ve seen in our lives. We most likely will not see a resumption of growth until 2021.

What Is Happening to the Economy?

The U.S. stock market is falling faster and steeper than at any point in modern history—the S&P 500 fell 30 percent in less than one month. To see something similar, you’d have to go back to the Great Depression era.

The Federal Reserve pushed through not just one but two emergency rate cuts in March. As a result, overnight discount rates—used by large banks for short-term borrowing—dropped to zero percent. That’s right. Zip. Zero. This zero-interest-rate policy is a drastic action, last taken at the depths of the housing crisis-led recession of 2008. It’s like turning a water faucet all the way to the left. It’s a maximum push to motivate lending and growth.

IF AMERICANS HAVE TO PRACTICE “SOCIAL DISTANCING” FOR SEVERAL MONTHS, WE COULD EASILY LOSE $3 TO $4 TRILLION IN ECONOMIC OUTPUT. THAT’S REAL DOLLARS THAT AREN’T BEING PAID OUT TO WORKERS—AND THUS AREN’T BEING SPENT.

The government didn’t stop there. On Monday, March 23rd, the Federal Reserve committed to buy unlimited amounts of government bonds and mortgage-backed securities, promising to use its “full range of tools to support households, businesses, and the U.S. economy overall.” The Fed sees the writing on the wall: “It has become clear that our economy will face severe disruptions,” they say.

This unprecedented move in scale and scope will increase the Fed’s balance sheet through what is called “quantitative easing”—economists’ fancy term for how the government injects money directly into the economy by allowing banks to swap assets for cash. The Fed used a similar device to spur growth while the global economy recovered from the 2008 recession.

While monetary policy attacks the problems in credit markets, Congress is working to provide sweeping fiscal stimulus. Multiple massive coronavirus relief packages are on the table; the first package was passed in the Senate on March 18. It sets aside funding for free coronavirus testing, expanded food security programs, and

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.7

paid medical and sick leave for small businesses.

A larger, more expansive bill to address the economic fallout is working its way through Congress now, and would allocate more than $1.5 trillion to help stem the economic slowdown.

Even though $1.5 trillion sounds like a huge number, it’s important to realize just how big the U.S. economy is—we generated $20 trillion in GDP last year. If the estimates of some medical experts are correct and Americans have to practice “social distancing” for several months, including travel bans, school closures, and all large gatherings shuttered, we could easily lose $3 to $4 trillion in economic output. That’s real dollars that aren’t being paid out to workers—and thus aren’t being spent.

LEARN MORE: The BiggerPockets Guide to Coronavirus Relief Programs

A third economic package being assembled by the Treasury Department would allocate $500 billion for two rounds of cash payments directly to individual taxpayers. The first payment would be made around April 6th, and the second payment on or around May 18th. These cash payments would be tiered based on household size and administered by the IRS.

The Treasury Department is also seeking $300 billion in emergency small business loans in addition to $50 billion for the airlines and $150 billion for other hard-hit industries like travel & leisure.

The Department of Housing and Urban Development (HUD) is joining municipalities and states across the country in efforts to keep people in their homes and apartments at this time. The Federal Housing Administration (FHA) is instituting an “immediate, 60-day moratorium on foreclosures and evictions for single-family homeowners with FHA-insured mortgages.” The Federal Housing Finance Agency (FHFA) is directing Fannie Mae and Freddie Mac to do the same with all mortgages backed by either enterprise.

In addition, Freddie Mac and Fannie Mae will also be presenting forbearance options to borrowers affected by the pandemic. This would allow borrowers to have their monthly mortgage bill suspended for up to 12 months due to economic hardship caused by the coronavirus outbreak.

If you have a mortgage and are worried about being laid off or having your income drastically reduced, be proactive and contact your lender or mortgage servicing company. Chances are there are remedies to help you through this year.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.8

Don’t Repeat the Mistakes of the Past

When I asked J. Scott, the author of Recession-Proof Real Estate Investing, his advice for investors who haven’t weathered economic downturns, he had— unsurprisingly—a lot to say.

“I remember a couple occasions in college stumbling back to my apartment after a few too many drinks, the room spinning, lying on the edge of my bed and thinking to myself, ‘I will never do this again,’” he says. “And for a few days, maybe even a few weeks, that memory was enough to keep me from doing it again.”

But the memory of the misery didn’t last. “The pain, sickness, and nausea was no longer fresh in my mind, and I was free to be the same stupid kid, making the same exact mistake,” he says.

What does this have to do with real estate investing? A lot, actually.In the early-aughts, before the effects of the 2008 recession started to fade, Scott spoke with a number of shell-shocked investors. All of them faced financial and investing struggles—“but we made it through, each of us with a new-found perspective on what a massive economic shift could do to our industry and with a healthy fear of it happening again,” he says. “At the time, it was hard to imagine the good times ever returning.”

AS INVESTORS, WE MUST ALWAYS REMEMBER THAT THINGS ARE NEVER AS GOOD OR AS BAD AS THEY SEEM. THE ECONOMY, THE MARKETS, AND REAL ESTATE ITSELF IS CYCLICAL. IT WILL GET BETTER. THINGS WILL RETURN TO NORMAL, AND WE MUST MAKE GOOD INVESTING DECISIONS THAT WILL PREPARE US FOR WHEN THAT SHIFT BACK TO ‘NORMAL’ OCCURS.

Things did get better. We’re here, a decade later—and like those hazy college nights, the memory of 2008 has faded away. “I still have the memories of feeling scared, confused, and overwhelmed, and feeling things would never return to normal,” Scott says. “But I just can’t put myself back in that place to really feel it. It’s more like a dream than a memory.”

He’s not the only investor that feels that way. Many have been operating like 2008 never happened, and have lost their perspective on how bad things can be. In this current crisis, Scott says he sees a lot of investors who are suddenly snapped back to reality, once again catching a glimpse of the potential bad times that real estate can bring.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.9

Except we’re not college students anymore. As real estate investors, we have the gift of hindsight—and we can’t hesitate to use it.

“As investors, we must always remember that things are never as good or as bad as they seem,” Scott says. During the bad times, “we have to remind ourselves that the economy, the markets, and real estate itself is cyclical. It will get better. Things will return to normal, and we must make good investing decisions that will prepare us for when that shift back to ‘normal’ occurs.”

Hindsight is important for the good times, too. “When it seems like the party isn’t going to stop, when it seems like real estate prices will never stop going up, we need to remind ourselves that every bull market has an expiration date,” Scott says. “As difficult as it can be to remember what it felt like last time, we must try to put ourselves back in those shoes so that we can adequately prepare ourselves for an unavoidable period of angst and uncertainty.”

Ready to prepare yourself for a successful financial future? Here’s how.

Protecting Your Investments During an Economic Downturn Nobody ever feels adequately prepared when markets become unstable. The news flow comes fast and furious, and some people make a living peddling fear out of self-interest, compounding investor anxiety. Every investor should practice patience in times like this. Economic downturns present a valuable opportunity to revisit your allocations and your investment timeframe. Remember: Time has always rewarded consistency with strong returns in stocks, bonds, and real estate.

Patience Prevails Being a long-term investor means staying invested even when the market is in turmoil. In an average year, the S&P 500 has a decline of at least 13 percent at some point on the calendar. Yes, this decline is certainly steeper than most, but if you make regular contributions to a 401k or an IRA funding program, your next monthly contributions are buying more shares for the same amount of dollars. IN FACT, THE MOST SUCCESSFUL INVESTORS USE MARKET DOWN-TURNS TO SHARPEN THEIR EDUCATION, EXPAND THEIR TOOLKITS, AND PREPARE FOR THE NEXT OPPORTUNITY. AND THEY NEVER MAKE RASH DECISIONS.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.10

Here’s an example: Let’s say you own 100 shares of stock. They were worth $50 per share at the beginning of the year, making your investment worth $5,000. If the stock falls by 50 percent, your investment is now only worth $2,500—but, you can now buy another 100 shares for only $2,500 more. When the stock eventually rebounds and returns to $50 per share, you’ll own $10,000 worth of stock, with a cost basis of $37.50 per share (half at $50 per share and half at $25 per share), and you’ll have earned $2,500 on the position. This process of investing the same dollar amount in stocks or funds at specific times, regardless of what the market is doing, is called dollar-cost-averaging. This method is the most efficient way to invest in the stock market, assuming you plan to participate for 10 years or more. It takes emotion out of the process and allows time to be your ally. And opportunistic investors with long time horizons even come to appreciate finding the stock market on sale! Worried about your 401k? If you’re not retiring soon, make sure to keep contributing at minimum whatever percentage your employer is matching—these contributions are on pre-tax dollars and it’s just too much benefit to pass up. You are literally getting a 100 percent return on any matched amount your company contributes—even if you have to wait for that contribution to vest. And if you are close to retirement age, your financial plan should already include at least 60 percent of your assets in risk-averse, fixed-income securities. Most bond funds have held up very well so far in 2020, with some even putting up strong gains as investors fled stocks and searched for safer pastures. Economies and stock markets work in cycles, and every prior bad cycle in the history of time has worked out just fine, rewarding committed long-term investors. In fact, the most successful investors use market downturns to sharpen their education, expand their toolkits, and prepare for the next opportunity. And they never make rash decisions. LET ME REPEAT THAT FOR THOSE IN THE BACK! They NEVER make rash decisions. Markets fall. Economies run in cycles. This is inevitable—but your long-term investments won’t suffer, as long as you remain committed to strategizing and improving your financial education.

Don’t Fall Into the Trap of 2008 Comparisons Because it was the most recent recession, it’s natural to want to draw comparisons to the recession of 2008. But it’s an extremely poor comparison to make, and real

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.11

estate investors could wind up in trouble if they react according to ill-informed expectations. All signs point to this coming recession being nothing like 2008—or the 2001 recession, for that matter. In 2008, the housing market was flooded with subprime mortgages given to people that couldn’t even come close to affording a home. Lenders allowed zero-income verification loans with no cash down—so when the market crashed, they were forced into foreclosure. Additionally, people were flipping houses two or three times per month, and the rising prices validated their bad decisions. Builders were constructing new homes as fast as they could. All this formed a bubble focused squarely on real estate. As a result, real estate prices fell dramatically. Some markets saw valuations drop by more than 35 percent.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.12

But in most recessions, real estate holds up just fine. In fact, sometimes prices don’t fall at all, or simply remain flat for a couple of years. No problem at all for the buy-and-hold real estate investor. In fact, this historical housing market strength contributed to the 2005 through 2008 bubble. Everyone thought, “Well, real estate always goes up, it never goes down. Let’s plow in.” LEARN MORE: The Beginner’s Guide to Buy-and-Hold Real Estate Investing Wrong then. But not necessarily wrong now—because investors learned valuable lessons about excess from the 2008 recession. For example, housing starts (or new home constructions) were much lower in 2020 going into this downturn. Interest rates are also much lower, creating more demand.

So What Should We Expect During This Downturn?

First: We expect to see a stable real estate market in the months ahead. Some things are common across all recessions. Economic output falls. Stocks take a beating, for a little bit. Some industries are hit harder than others, and the government usually steps in to assist those hit the hardest. These are commonalities. But there is an extreme lack of precedent for this particular economic downturn. It’s not brought on by typical drivers like excess economic froth or greed. When we entered 2020, stocks were trading at multi-year valuation highs—but nothing compared to the 2000 stock market, for example. And this downturn isn’t being caused by a bad actor causing instability, like the subprime housing market and collateralized debt markets in 2007 and 2008. (Unless you want to call a microscopic virus the bad actor, which, yep, is fine by us.) Frankly, we’ve never seen a forced shutdown of the majority of the global economy all at once. This is unprecedented. This time is, well, different. And as such, we should keep an open mind, stay smart, and not rush to make comparisons to something that happened in the past.

Pay Attention to Interest Rates

Most real estate investors know that mortgage interest rates tend to move as so-called “benchmark” government bonds rates, like the Fed’s discount rates, move

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.13

higher or lower. When government bond yields are rising, mortgage rates typically rise as well, and vice versa. Mortgage rates, should they continue their historical pattern of tracking treasury rates, could hit new multi-decade lows in the months ahead—after all, 30-year Treasury bonds now yield less than 1.5 percent. That doesn’t mean that a 30-year fixed-rate mortgage will eventually drop to two percent, but it will likely fall further. Typically, it takes three to four weeks before mortgage rates adjust to market interest rates, because major banks must adjust their underwriting process and market their updated rates to customers and mortgage lenders. In times of severe financial distress, like we’re seeing now, this lag time usually increases: there’s more uncertainty on the part of both lenders and buyers.Real Estate Risk Factors During a Recession It’s not so simple as lower mortgage rates bringing more buyers to the table and keeping property prices on their upward trajectory. Back in January, CoreLogic estimated that residential real estate values would rise more than five percent in 2020; that estimate is no longer anyone’s expectation. The strong recent run of property appreciation will at least take a breather; whether the picture will darken into declines in property values over the course of 2020 is uncertain. Here are the biggest risk factors to property values in 2020:

1. Widespread layoffs and job losses from a protracted “social distancing” environment, leading to household incomes plummeting. Foreclosures and evictions would rise, lowering cash flow for rental investors and making lending a riskier proposition for banks. It could also increase the supply of vacant properties.2. Real estate investors “hunkering down” with cash, pulling away from buying real estate. Stock losses create a “negative wealth effect” feedback loop. (What’s a wealth effect? It comes from behavioral psychology: We spend more and “feel richer” as our assets in things like real estate and stocks appreciate in value. The same is true in reverse—when stocks or real estate fall in value, we spend less, and feel poorer, regardless of the actual impact to our monthly income and expenses.)3. Residential property buyers can’t visit open houses so traffic comes to standstill, further increasing the supply of available homes. We already see signs that large banks are more hesitant to lend capital. They have

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.14

no choice—in addition to mortgage lending, these banks also lend to airlines, hotels, and cruise ship operators. These industries and companies may default on large loans without a massive government bailout. Banks don’t want to take on extra risk. Why should they? Millions of consumers are being laid off or having their incomes drastically reduced. This could go on for 12 to 18 months, according to some medical experts—secondary and tertiary waves of the outbreak next fall and winter could happen because nobody has immunity to this new virus. Banks have to be ultra cautious.

There May Be Relief in (Some) Rentals

“Things aren’t all bad during a recession,” says Scott. Yes, renters have less money to spend on rent—and high-end rentals, often known as Class A rentals, might see drop in market rents as renters flee to cheaper units. Class B rentals may experience a similar effect.

But everyone needs a place to live.

“While renters will often move down in class, they generally aren’t going to go homeless,” Scott says. “Working class rentals often see increased demand and increased market rents due to all the renters moving from Class A and Class B rentals, as well as those transitioning out of homeownership during foreclosure.”

Another hot rental opportunity? College housing. “A lot of people tend to use temporary layoffs as an opportunity to go back to school,” Scott says. As a result, college rentals tend to outperform other residential real estate during a recession.

What Happens if a Recession Becomes a Depression?

What if we see not just a recession, but an economic depression—or a significant drop in GDP over several years? In that dire scenario, hundreds of billions of dollars in loans would be defaulted on by everyone from large corporations to individuals and households. A bank’s main concern at that point would be just staying solvent; running out to lend more money would be unthinkable. There’s evidence that banks are hesitating: Mortgage rates are actually creeping higher, despite large drops in benchmark bond rates. A surge of mortgage refinancing applications have oustripped the amount banks want to lend out. Essentially, banks and lenders want to disincentivize new applicants by raising the interest rate.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.15

This may only be a temporary pause, but we just don’t know when travel, work, and social restrictions will be lifted—so expect mortgage rates to move more based on lender morale than on the benchmark rates. One potential silver lining: rental rates traditionally aren’t impacted much by a recession. That model could go out the window if the economy gets into a multiyear slide, with unemployment rates of 15 percent or more. However, in the 2008 recession, rental rates for three-bedroom apartments actually rose, despite the steep drop in real estate prices. Demand for rental units increased as people downsized from homes, and the recession’s relatively short timetable—helped by massive government stimulus—kept the rental market from experiencing drops in average rates.

Current Real Estate Supply and Demand Dynamics New housing starts had been running at a good clip for the past few years as the industry emerged from the carnage of the 2007 and 2008 bubble. Millennials were starting to buy their first homes, Gen X were active rental investors, and Wall Street thought builders were entering a bullish phase. IT’S GOOD THAT THE CURRENT HOME INVENTORY IS ON THE LOW END. THIS SHOULD HELP KEEP AVERAGE SALE PRICES STURDY THROUGH THE DEMAND SHOCK PHASE. But like many supply chains across the country, housing production is now at a standstill. Even February’s housing starts data, while still positive, showed a drop of 1.5 percent year-over-year, with a notable 18 percent drop in multi-family housing starts. (This February data had just a hint of the coronavirus panic in the tail end of the measurement period.) Data from March—and likely April, too—will be much more stark, with steep declines expected due to social distancing, job and income insecurity, and materials shortages due to the supply chain disruptions in China and elsewhere. While the supply of new homes is about to slow to a trickle, the supply of existing homes was also trending lower at the end of 2019. Existing home inventories were at multi-year lows back in January. Why? Low prevailing rates, a strong labor market, active real estate investors, and several solid years of existing property sales and price appreciation—more than four percent annually. This is important going forward, because we’re about to have a demand shock

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.16

to real estate. It might not last long, it may last all year, but for some time period starting right now, there are far fewer active buyers in the market. So it’s good that supplies of homes are on the low end instead of the high end. This should help keep average sale prices sturdy through the demand shock phase. The fact that rates will remain low for a long time certainly helps the cause.

Expect Dicey Times for Commercial Real Estate

Commercial real estate will be an area of concern for some time. Commercial tenants and property owners will be seeing immediate cash flow hits, which will continue for several months at minimum. Restaurants, hotels, and any businesses relying on foot traffic are already seeing 50 to 90 percent hits to monthly revenue. There will be businesses that are never able to re-open, leading to high vacancy rates in commercial buildings—regardless of whether we see a two-quarter recession or a five- or six-quarter recession. FOR COMMERCIAL REAL ESTATE, GOVERNMENT BACKSTOP PROPOSALS WILL BE CRITICAL. SMALL BUSINESS LOANS, FORBEARANCE AGREEMENTS, AND EASED LENDING RESTRICTIONS COULD HELP COMMERCIAL PROPERTY OWNERS RETAIN THE MAJORITY OF THEIR CURRENT MONTHLY INCOME. There’s already evidence of investor nervousness—publicly-traded commercial property stocks and REITs have seen large drops in the past month. And the high-yield debt that funds most commercial real estate deals has also come under pressure, falling in price by between 15 and 25 percent the past month. For commercial real estate, government backstop proposals will be critical. Small business loans, forbearance agreements, and eased lending restrictions could help commercial property owners retain the majority of their current monthly income so long as the economy doesn’t falter into the summer. And for lenders of commercial property loans, the Fed’s unlimited checkbook for asset-backed securities purchases could relieve the fears of making fresh loans in 2020. Some geographic areas will see higher-than-average commercial property deterioration based on where the coronavirus spreads. And of course, where the rubber meets the road here in commercial real estate is in how long the U.S. economy remains shuttered. How many weeks will our largest states have shutdowns of all non-essential businesses? How long until people start taking vacations again—or even going out for Sunday brunch? But it’s not all bad news. “There are some bright spots as well,” says Scott. “As

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.17

people move to smaller rental units and smaller houses, they tend to not want to get rid of their stuff. Self-storage facility owners tend to do very well during a downturn.” As do industries that provide staples, like food and healthcare. Looking for a commercial investment? In addition to self-storage facilities, Scott says grocery-anchored retail centers and medical centers stand up well to a recession.

So What Should Real Estate Investors Expect in 2020?

It’s still very early in this process—far too early to make definitive statements about how long the “forced shutdown” will last and the eventual effects on the long-term health of the economy. What we do know is that the global economy was in a good place prior to the pandemic, and investors can take solace in that. If the spread of the virus is contained, we can recover quickly. REAL ESTATE INVESTORS SHOULDN’T FEEL PRESSURED INTO FOMO-FUELED SNAP DECISIONS. HISTORY SUGGESTS THERE WILL BE PLENTY OF TIME TO CAREFULLY ASSESS ONE’S OPTIONS—AND THAT TIME WILL BE BEST-SPENT SEEING HOW FAST THE ECONOMY REBOUNDS.

The Best Outcomes

If coronavirus fades out quickly, we may see limited damage to the economy. Positive potential outcomes include:

• Only one or two quarters of “base recession,” with a strong showing in the second half.• Equity markets quickly stabilize, and fear subsides quickly enough to “save the summer” for the U.S. economy, specifically around travel.• Real estate prices remain flat, and don’t drop more than one or two percent in the virus’s high-impact metro areas. • Lenders stay involved in the mortgage markets thanks to easy access to capital from the Federal Reserve and a moratorium on evictions and foreclosures. • Labor market remains intact, with only a small spike in layoffs and job losses. • Pretax incomes stay flat instead of falling.• Government checks mailed to taxpayers helps stem losses.• Interest rates remain lower for longer, bringing more real estate buyers to the table.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.18

The Worst Outcomes

Unfortunately, due to the unpredictability of the virus, we can’t guarantee all of the best outcomes. When planning your investment strategy, it’s important to consider the following possibilities:

• Protracted recession lasting three or more quarters.• Large spikes in job losses leading to mass unemployment. • Reduced hours and take home pay limiting consumers’ economic activity. • Plummeting consumer confidence.• Spike in vacancy rates straining real estate investors without cash reserves, especially in hard-hit areas.• Drop in new home starts, further reducing residential real estate activity by removing a new supply of product to sell. • Mortgage rates rise to reflect lender risk concerns, causing homebuyers to pause their search. • Real estate prices fall by seven to 10 percent. Across most scenarios, we anticipate that prevailing interest rates will remain low for quite some time. In general, the Federal Reserve has a harder time raising rates once it has lowered them. When rates were cut to zero during the 2008 recession, it took over 10 years before the overnight lending rates were back over 1%. So real estate investors shouldn’t feel pressured into FOMO-fueled snap decisions. It is unlikely that rates will quickly rise. History suggests there will be plenty of time to carefully assess one’s options—and that time will be best-spent seeing how fast the economy rebounds from the coronavirus shutdown and how renter’s incomes and property values are affected.

Assessing Your Recession-Ready Investment Portfolio Now is a fantastic time to assess your portfolio as a whole to ensure that it’s recession-proof. But first, remember: Making reactive, ill-advised moves is never smart, regardless of whether we’re in a recession or an expansion. Take the extra time to document all your assets in one place and monitor your cash flows closely. You never want to be rushing to the table to get a real estate sale done. Never. Stocks and bonds are more liquid than real estate, which can be good and bad. The good is easy to understand—liquid is great if you need cash in a pinch. And people’s ideas of what it means to “be in a pinch” can change a lot during a recession.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.19

Pros of stocks and bonds• Potential for high returns• Historically strong performance• Liquid Cons of stocks and bonds• Drawdowns can happen fast• Takes time to conduct due diligence on new investments Let’s compare that to the pros and cons of real estate investing: Pros of real estate investing• Diversification from stocks and bonds• Tax benefits• Monthly cash flow (if you own rental property) Cons of real estate investing• Illiquid• Prices move slowly Real estate has some additional benefits—especially when risker markets like stocks are spilling over. Prices on real estate assets are more market-to-market. They’re not priced and re-priced every second of the day like stocks and bonds. And for most long-term investors, having an asset in place for three-plus years brings a lot of peace. It takes some of the pressure to make a fast decision out of your hands. Time is always the long-term investor’s ally.

Recession-Proof Real Estate Investing

This section contains excerpts from Recession-Proof Real Estate Investing by J. Scott. The most common arenas where real estate investors choose to operate and specialize in include: • Flipping• Wholesaling• Single family buy-and-holds• Multifamily• Private and hard money lending• Note investing• Commercial

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.20

While most of these focus areas will work to some degree during any part of the business cycle, some are more effective during certain phases than others. To optimize your investment plan at any given time, you need to be flexible and use the strategy that’s most effective and profitable based on the current market conditions—not just one that you happen to like.

If you can only master one strategy because of limited time, comfort level, or capital base, then understand that there will be times when it’s best to just sit on the sidelines and wait for the market to come to you.

Patience is never a bad strategy.

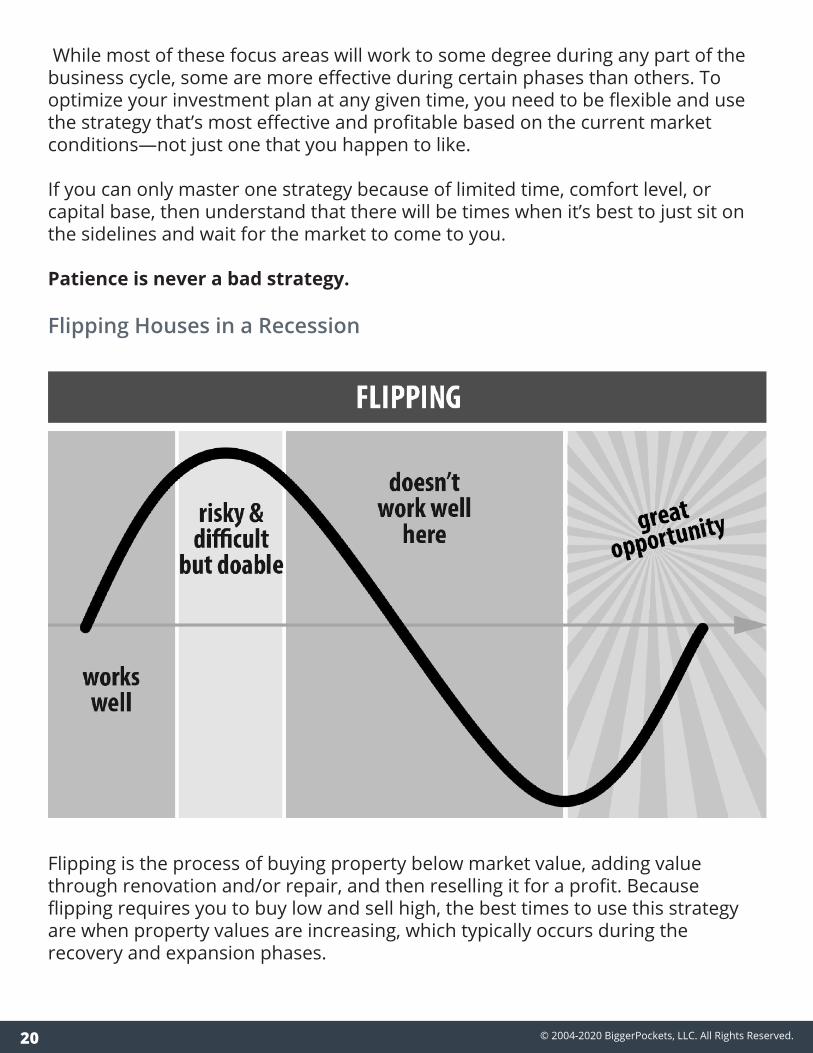

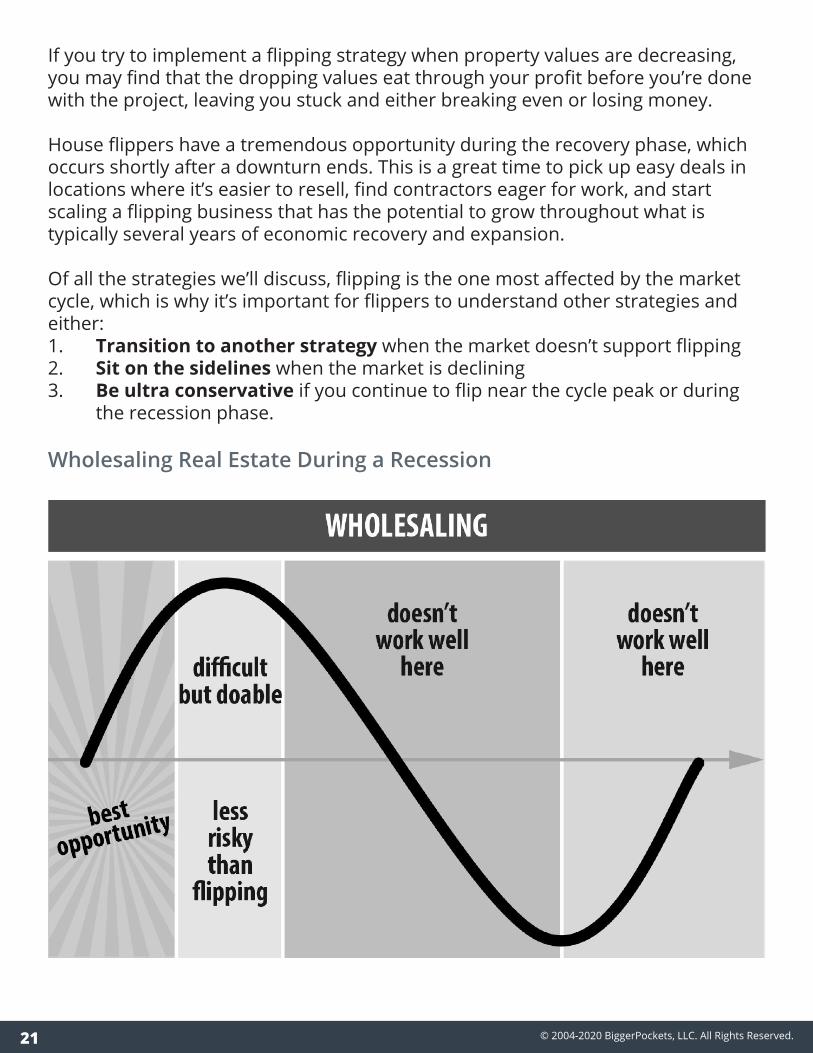

Flipping Houses in a Recession

Flipping is the process of buying property below market value, adding value through renovation and/or repair, and then reselling it for a profit. Because flipping requires you to buy low and sell high, the best times to use this strategy are when property values are increasing, which typically occurs during the recovery and expansion phases.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.21

If you try to implement a flipping strategy when property values are decreasing, you may find that the dropping values eat through your profit before you’re done with the project, leaving you stuck and either breaking even or losing money.

House flippers have a tremendous opportunity during the recovery phase, which occurs shortly after a downturn ends. This is a great time to pick up easy deals in locations where it’s easier to resell, find contractors eager for work, and start scaling a flipping business that has the potential to grow throughout what is typically several years of economic recovery and expansion.

Of all the strategies we’ll discuss, flipping is the one most affected by the market cycle, which is why it’s important for flippers to understand other strategies and either: 1. Transition to another strategy when the market doesn’t support flipping 2. Sit on the sidelines when the market is declining3. Be ultra conservative if you continue to flip near the cycle peak or during the recession phase.

Wholesaling Real Estate During a Recession

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.22

Wholesaling is the process of finding and/or negotiating the purchase of property below market value and immediately reselling it or the contract to another investor for a profit. Good wholesalers can negotiate prices that are low enough that they can resell for a profit, while also allowing their buyer to generate a profit as well.

Wholesalers must buy low and sell high just like flippers. But wholesaling has some additional requirements that must be met for the strategy to be effective:

• Wholesalers most often sell to flippers. So wholesaling will be most viable during phases of the cycle when flipping is viable.

• The best opportunities for wholesaling exist when deals are exceptionally difficult to find. Otherwise, flippers and landlords will find their own deals without the need for a wholesaler.• Wholesalers need to pay even less for properties than flippers because both the wholesaler and the flipper must be able to mark up the price of the property when reselling to make a profit. This can be nearly impossible in both an extremely hot market (many buyers seeking deals) and in a market where property values are declining.

Wholesaling is possible during all parts of the cycle. But because of the addition-al requirements listed above, it’ll be most successful in the phases where flipping works—the early recovery phase when coming out of a recession and the ensuing expansion phase.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.23

Single-Family Buy-and-Hold Rentals During a Recession

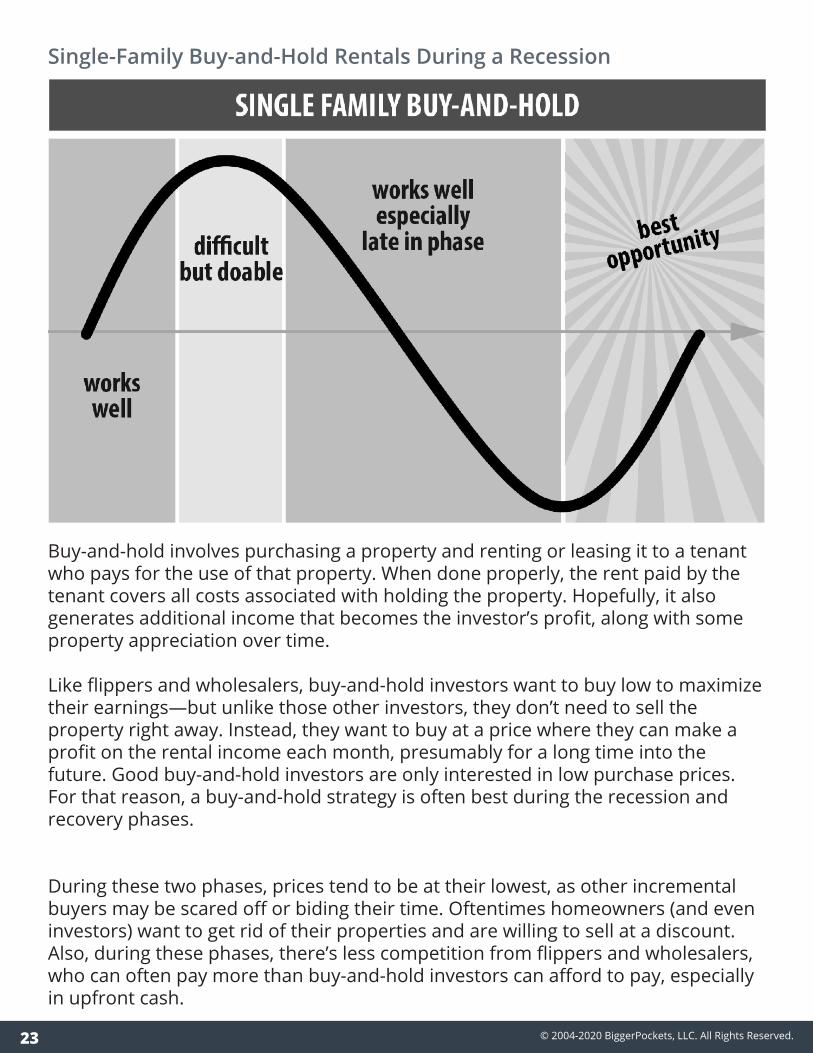

Buy-and-hold involves purchasing a property and renting or leasing it to a tenant who pays for the use of that property. When done properly, the rent paid by the tenant covers all costs associated with holding the property. Hopefully, it also generates additional income that becomes the investor’s profit, along with some property appreciation over time.

Like flippers and wholesalers, buy-and-hold investors want to buy low to maximize their earnings—but unlike those other investors, they don’t need to sell the property right away. Instead, they want to buy at a price where they can make a profit on the rental income each month, presumably for a long time into the future. Good buy-and-hold investors are only interested in low purchase prices. For that reason, a buy-and-hold strategy is often best during the recession and recovery phases.

During these two phases, prices tend to be at their lowest, as other incremental buyers may be scared off or biding their time. Oftentimes homeowners (and even investors) want to get rid of their properties and are willing to sell at a discount. Also, during these phases, there’s less competition from flippers and wholesalers, who can often pay more than buy-and-hold investors can afford to pay, especially in upfront cash.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.24

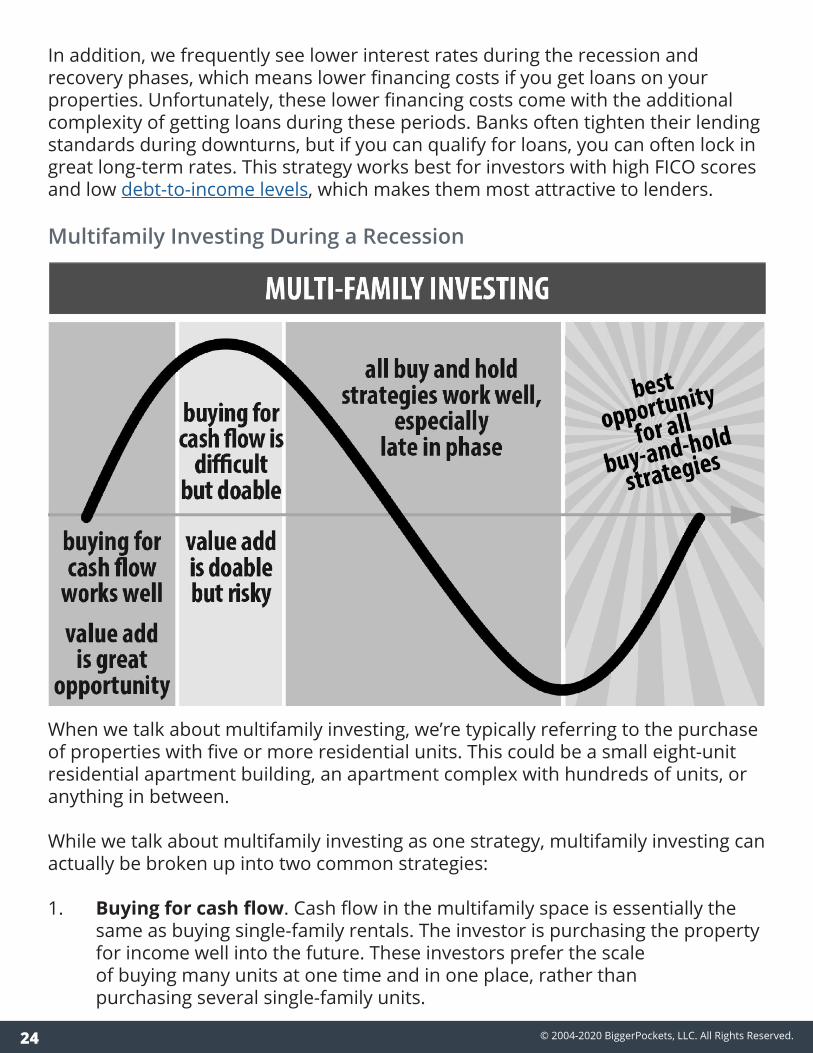

In addition, we frequently see lower interest rates during the recession and recovery phases, which means lower financing costs if you get loans on your properties. Unfortunately, these lower financing costs come with the additional complexity of getting loans during these periods. Banks often tighten their lending standards during downturns, but if you can qualify for loans, you can often lock in great long-term rates. This strategy works best for investors with high FICO scores and low debt-to-income levels, which makes them most attractive to lenders.

Multifamily Investing During a Recession

When we talk about multifamily investing, we’re typically referring to the purchase of properties with five or more residential units. This could be a small eight-unit residential apartment building, an apartment complex with hundreds of units, or anything in between.

While we talk about multifamily investing as one strategy, multifamily investing can actually be broken up into two common strategies:

1. Buying for cash flow. Cash flow in the multifamily space is essentially the same as buying single-family rentals. The investor is purchasing the property for income well into the future. These investors prefer the scale of buying many units at one time and in one place, rather than purchasing several single-family units.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.25

2. Buying as value-add. This is the apartment equivalent to flipping single-family houses. When we purchase a single-family home to flip, we are typically buying something that is in bad physical condition, renovating it, and then reselling at a profit based on the physical renovations we’ve done. In the apartment world, instead of just doing physical renovations, we are improving the financial performance of the property as well. We do this by fixing management, increasing rental income, and lowering expenses. We can then resell the property at a lower cap rate, which translates to a higher price.

The value-add strategy is often done as part of a syndication, which is a group of passive investors putting money into a project run by a syndicator. The syndicator is an active investor (typically the largest stakeholder in the deal) and is responsible for sourcing and executing on the deal and earning everyone, including themselves, a profit.

Like single-family rentals, buying multifamily properties for cash flow will work during any part of the cycle. However, this strategy will be most successful when it’s possible to purchase at low prices.

In the multifamily world, cap rates are intertwined with property values. When cap rates are high, prices paid for, or offered by, buyers will be low. This is common when interest rates are high and when sellers are getting desperate to get rid of their properties. Like with single-family, this is going to occur during the recession and recovery phases.

LEARN MORE: The BiggerPockets Guide to Calculating and Using Cap Rates

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.26

Private and Hard-Money Lending During a Recession

Private lenders don’t lend professionally but do lend to investors, who might be family members, friends, or investors they know and trust. These are individuals who often use money from their retirement accounts to invest in something other than the stock market. Or they may be investors who simply want to diversify their investments in taxable accounts by passively lending to other real estate investors.

Hard-money lenders are typically professional lenders who secure their investments with the borrower’s property. They have less of a relationship with the borrower, and are susceptible to risk should the value of the property—their collateral—drop.

Private lending can work in any part of the market cycle, especially for those lenders who can underwrite a wide variety of deals. Many successful lenders will diversify their portfolio and lend to different types of investors such as flippers, builders, buy-and-hold landlords, and commercial investors. If more investors are focused on buy-and-hold deals, good lenders will adjust their strategy to support these types of loans; if investors are focused on new construction, good lenders will figure out a lending strategy that incorporates new construction loans.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.27

But that doesn’t mean the phases of the cycle don’t impact lenders’ profits and margins. They do. Buyer demand for property impacts lender profits, and interest rates impact lender margins. When interest rates are high, lending profits and margins will be higher than when interest rates are low and cheap money is readily available.

During the recessionary and recovery phases, when there aren’t many professional lenders in the mix and some lenders are scared to deploy their cash, private lenders may be able to generate six percent or more above bank rates, plus several “points” upfront, on their loans. But during the expansion and peak phases, when lenders are fighting each other to loan money to investors, lenders often have to make loans that rival bank rates with few fees or points.

Note Investing During a Recession

A mortgage agreement is a kind of note. There are many different strategies around buying, selling, and holding notes.

READ MORE: What is a mortgage note?

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.28

A few of the most common strategies include:

• Selling property using seller financing and collecting cash flow from the note that’s created from the loan.• Buying “non-performing” notes where the borrower isn’t paying as promised at a deep discount and then negotiating repayment with the borrower or foreclosing on the property.• Creating or buying a note and then selling off part of the note for cash in hand, while also still getting monthly cash flow from the remaining stake in the note.

In addition, investors may purchase notes in either first position or as junior liens. A first position note is entitled to payment first should the borrower default—mortgages, for example, are typically first-position loans. If the property is fore-closed upon or the borrower is forced to settle debts as part of a bankruptcy, the first position note holders will be the first to get paid. This is the most secure position.

Junior liens are not in first position. This means that the note holder may not be able to foreclose or even get paid should the borrower default. They will typically only see a return if they can convince the borrower to pay or if there is money left over after the first-position note holder has been repaid their entire balance. If the first-position note holder isn’t fully paid off, the junior lien holder will typically receive nothing.

Like lending, notes can be a profitable part of an investment portfolio during any part of the economic cycle, with different strategies providing advantages and disadvantages at different times.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.29

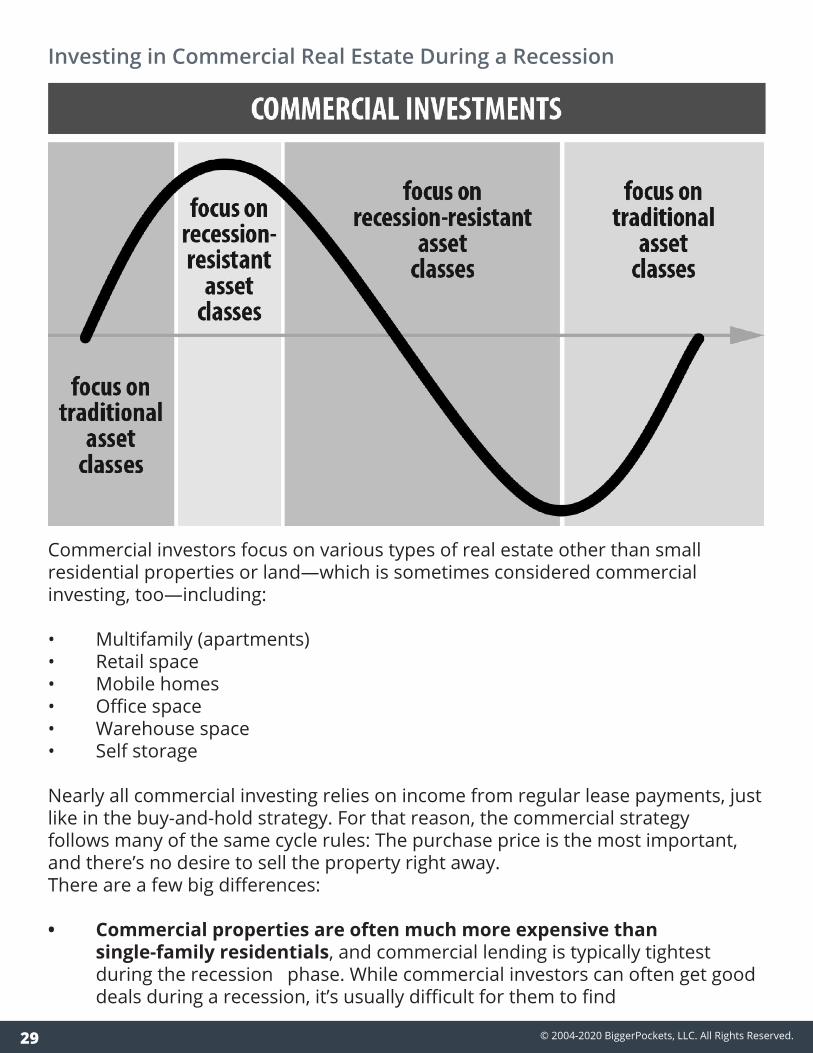

Investing in Commercial Real Estate During a Recession

Commercial investors focus on various types of real estate other than small residential properties or land—which is sometimes considered commercial investing, too—including:

• Multifamily (apartments) • Retail space • Mobile homes • Office space • Warehouse space • Self storage

Nearly all commercial investing relies on income from regular lease payments, just like in the buy-and-hold strategy. For that reason, the commercial strategy follows many of the same cycle rules: The purchase price is the most important, and there’s no desire to sell the property right away.There are a few big differences: • Commercial properties are often much more expensive than single-family residentials, and commercial lending is typically tightest during the recession phase. While commercial investors can often get good deals during a recession, it’s usually difficult for them to find

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.30

lending. Because of this, it’s often better to implement a commercial strategy once the economy has shown signs of recovering. At this point the lender’s purse strings should start to loosen up and improve borrowing terms. • Many commercial investors rely on private investors, like syndications, to fund part or all of their deals. Because of the reliance on individual investors, commercial investors are most likely to be able to put together these deals during times when smaller individual investors have access to cash and a willingness to risk that cash on a real estate deal. • Commercial property investments often focus on areas more recession-resistant than residential property investing. Some areas of commercial property actually thrive during recessionary periods—for example, self-storage facilities often see a sharp rise in demand during a recession, simply because more families are moving in together or moving into smaller spaces and need a place to store their extra stuff.

Focus on the purchase of traditional commercial investments during the recovery and expansion phases. And then focus on the purchase of recession-resistant commercial assets as the economy starts to turn south - it’s a good diversification strategy away from riskier investments like stocks at this point.

LEARN MORE: J. Scott’s Recession-Proof Real Estate Investing dives into the theory of economic cycles and the real-world strategies for harnessing them to your advantage.

How to Make the Best Use of Your Time During a Downturn

An economic slowdown is a good opportunity to build a strong real estate investment support system and to carefully think through your strategies. Proper planning gives you a head-start once the economy begins an upturn. Market dislocations—when fear separates prices from their underlying value and cash flow generation—are the best time for a prepared real estate investor to carve out an amazing deal. Here’s where to start.

Increase Your Investing Knowledge Base

How do you learn best? BiggerPockets offers a number of ways to learn about real estate—no matter whether you’re socially distancing at home or out on a run.

• Find expert guidance on every aspect of the real estate industry at our blog.• Pick up books from our network of pro investors—including Recession-Proof Real Estate—at our bookstore.

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.31

• Tune into our free webinars for in-depth looks at investment topics.• Read our guides, which offer a deep dive into a number of essential real estate questions.• Check out our real estate glossary to keep up with the conversation.• Listen to our podcasts—we have four, so pick the one that’s tailored to your interests: BiggerPockets Real Estate Podcast, BiggerPockets Money, BiggerPockets Business, and Real Estate Rookie.• Watch videos on our YouTube channel, which showcases real investors and their best (and worst!) deals.

Start Networking

While we love all of the great resources offered on BiggerPockets.com, investors can’t skip one of our most popular tools: the BiggerPockets forums. Even if you’re staying a firm six feet away from all other humans, you can still pick the brains of real estate investors just like you—and pros who’ve brokered hundreds of deals. Our local forums allow you to connect with nearby investors, agents, brokers, and lenders. Have a question about the market in your area? You’ll find all the information you need. Sheltering in place means in-person meetups are out of the question (right now). But check out our events page for many that are happening virtually! Once we’re freed to breath fresh air once again, take time to meet investors, contractors, and potential business partners. A good team is essential to real estate investment success—so start choosing yours.

Dig Into Data When you’re ready to start diving into the real estate market, make sure you know exactly what you’re diving into. Think about the type of investing you want to do, whether it’s wholesaling, buy-and-hold, commercial investment, or fix-and-flips. Then, figure out what pieces of data are going to be the most impactful to your investments. Not sure what data you need or how to interpret it? Ask the BiggerPockets forums. Speaking of data: Pay close attention to economic data. No big decisions should be made until we see how many jobs are lost, and worker hours lost, as we head into the summer months. Unemployment rates, especially in certain metropolitan areas, will be an important driver of average rent prices in related zip codes. The same goes for the average value of residential homes sold, and commercial properties transacted. Another key data point in the next 12 to 18 months is the Consumer Price Index

© 2004-2020 BiggerPockets, LLC. All Rights Reserved.32

(CPI), which measures inflation. Inflation spikes can drive mortgage rates higher. When the CPI demonstrates a growth rate of more than four percent annually, expect higher mortgage rates soon.

Be Patient (But Pay Attention)

Stalk your real estate prey, but be willing to be patient for that next deal. What seems like a “great deal” because it’s five percent cheaper than it was a month ago may end up being 15 percent cheaper two months from now.

Need something to work on during your search for that next great deal? Build your reserve fund. You can never be over-prepared in reserves. Recessions can be frightening, but don’t let them crush your investment dreams. Make smart real estate decisions and refuse to panic. With time, your net worth will increase—and you’ll be better-prepared to weather the next storm.