recent developments in corporate taxation 7 2017... · 2017 recent developments in corporate...

TRANSCRIPT

2017

Recent Developments in

Corporate TaxationPost-Mortem Tax Planning – A Case Study

Pamela Cross, Borden Ladner Gervais, LLP

David Mason, Deloitte

June 7, 2017, OTTAWA

2

Agenda - Post Mortem Planning

1. Why is it important?

2. What are the “tools in the tool-box” and how do they work?

3. The Case Study

3

Post-Mortem Planning – Why is it important?

• To ensure that assets cannot be passed from one generation to the next, there is

a deemed disposition of assets on death (subject to certain exceptions and/or

deferrals such as the spousal rollover)

• For the vast majority of individuals, the deemed disposition is a one time event,

and little or no post-mortem planning is necessary. The most common exception

is where assets decline in value after death

• For individuals holding private company shares, there is a potential for double (or

worse) taxation on the same value (tax on the deemed disposition, tax in the

company on a liquidation of its assets, and tax on a deemed dividend extracting

value from the corporation)

4

Post-Mortem Planning: Tools in the Tool Box

• Surprisingly, given the significance of the issue, there is no specific post-mortem

regime in the Income Tax Act (the “Tax Act”) to deal with private company shares

• Three main strategies are used (all statutory references are to the Tax Act):

• S. 164(6) Loss Carryback

• Pipeline Transaction

• Para. 88(1)(d) Bump Planning (for certain capital property owned by the

company other than “ineligible assets”)

5

S. 164(6) Loss Carryback - Mechanics

• Deemed disposition of shares on death, increasing adjusted cost base of shares

to Estate

• Shares held by Estate of Deceased are redeemed before first year-end of the

Estate, triggering deemed dividend to Estate (ss. 84(3))

• Deemed dividend excluded from proceeds of disposition of shares (para. 54(j)),

resulting in capital loss to Estate (subject to stop-loss rules)

• Carryback of capital loss to terminal return to eliminate capital gain reported on

deemed deposition

Result: Double tax avoided, but tax paid on dividend (at dividend rates), not capital

gain (at capital gains rates)

6

S. 164(6) Loss Carryback – Selected Considerations

• Corporate tax attributes (capital dividend account (CDA), refundable dividend tax

on hand (RDTOH), ability to pay eligible dividends can reduce the effective tax

cost of the rate differential (dividends/capital gains)

• Creating additional tax attributes?

• Corporate owned life insurance: confirm adjusted cost basis of policy and

amount available to be added to CDA.

• Consider limiting capital dividend to 50% of full dividend to avoid grind of capital

loss under ss. 112(3.2).

• Will Estate be affiliated with Corporation after redemption (ss. 40(3.6) & (3.61)).

• Spousal “roll and redeem” strategy available?

• Redemption of shares or wind up of company (IT-126R2)

• One taxation year deadline.

• Estate must be a graduated rate estate

7

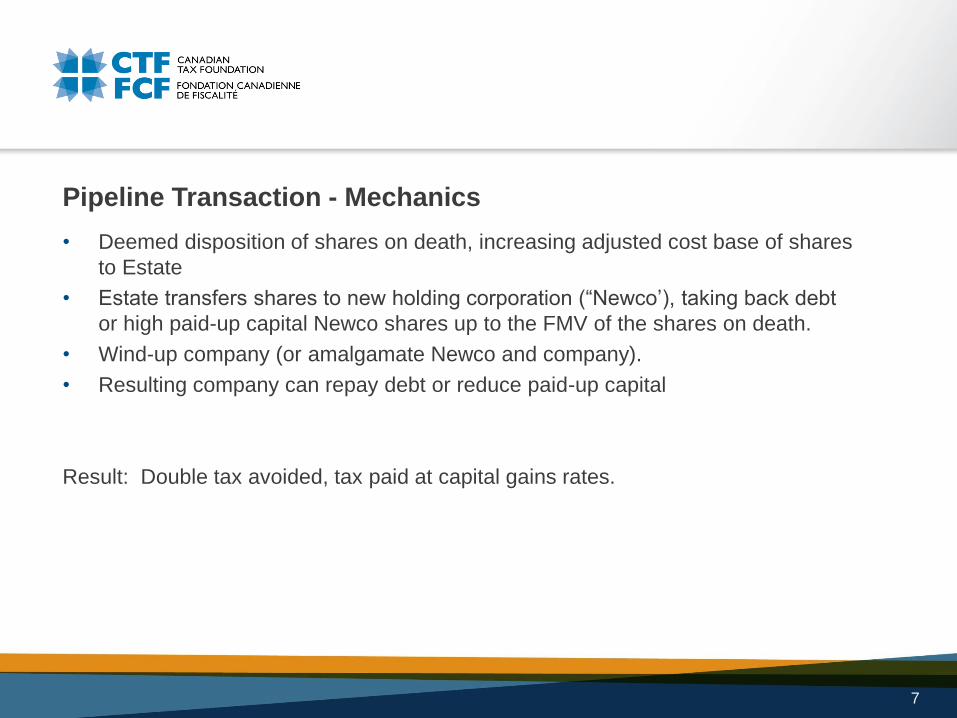

Pipeline Transaction - Mechanics

• Deemed disposition of shares on death, increasing adjusted cost base of shares

to Estate

• Estate transfers shares to new holding corporation (“Newco’), taking back debt

or high paid-up capital Newco shares up to the FMV of the shares on death.

• Wind-up company (or amalgamate Newco and company).

• Resulting company can repay debt or reduce paid-up capital

Result: Double tax avoided, tax paid at capital gains rates.

8

Pipeline Transaction – Selected Considerations

• Anti “surplus stripping” rule #1 (s. 84.1), applies where:

• Taxpayer (Estate) disposes of shares

• Taxpayer is resident in Canada and not a corporation

• Shares were capital property to taxpayer

• Shares are shares of a resident Canadian corporation (subject corporation)

• Shares are disposed of to another corporation (purchaser corporation)

• Taxpayer is non arm’s length with purchaser corporation

• Immediately after disposition, subject corporation is connected with

purchaser corporation (ss. 186(4))

• Implications:

• Paid up capital of purchaser shares reduced to extent of “soft ACB” (i.e.

look for capital gains exemption and V-Day value issues). Hard ACB can

be converted to debt or paid-up capital.

• Taxpayer deemed to receive a deemed dividend for excess

9

Pipeline Transaction – Selected Considerations

• Anti “surplus stripping” rule #2 (s. 84(2)) applies where:

• The corporation is resident in Canada

• The corporation is winding-up, discontinuing or reorganization its business

• A distribution or appropriation of the corporation’s funds or property (in any

manner whatever)

• The distribution or appropriation is to or for the benefit of the corporation’s

shareholders

• Implications:

• Amount of distribution/appropriation deemed to be a dividend

10

Pipeline Transaction – Surplus Stripping Issues

• Does (should?) the specific rule in s. 84.1 supersede s. 84(2)?

• CRA position: both can apply to same transaction (2011-0401861C6 2011

STEP National Conference)

• Is Estate a “creditor” or a “shareholder”?

• What does on the “winding up, discontinuance or reorganization” mean?

• Fact specific. See 2006-0170641E5 which suggested continuance of

business for at least 1 year and distribution over a further period of time

• 2011-0426371C6 where CRA indicates these “conditions” are not “required”

but may be evidence that there is no discontinuance of business

• 2010-0389551R3 (ruling withdrawn) Cash company – CRA may apply 84(2)

• Surplus Stripping Jurisprudence:

• Most involve “accommodation” party transactions, not post-mortem planning

• No “general scheme” in the Act against surplus stripping

• Should there be specific post mortem rules?

11

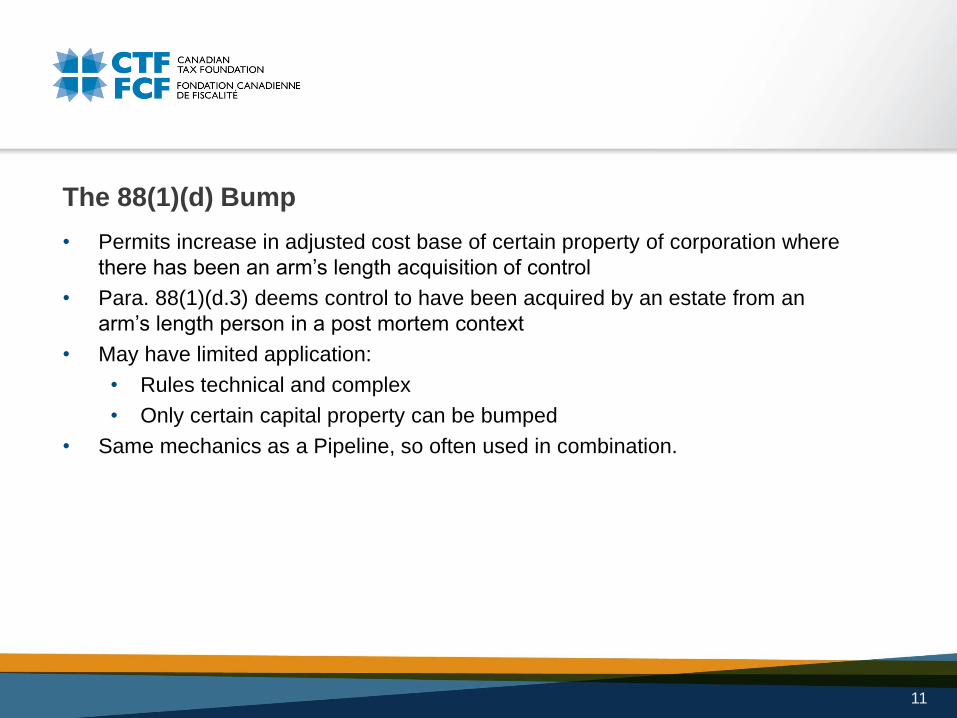

The 88(1)(d) Bump

• Permits increase in adjusted cost base of certain property of corporation where

there has been an arm’s length acquisition of control

• Para. 88(1)(d.3) deems control to have been acquired by an estate from an

arm’s length person in a post mortem context

• May have limited application:

• Rules technical and complex

• Only certain capital property can be bumped

• Same mechanics as a Pipeline, so often used in combination.

12

The Case Study

• Harry owns preferred shares in an operating company

(OpCo)

• ACB and PUC are nil

• FMV = $2M

• Harry is a widow and has three adult children: Ron, Lily

and Phoebe. They currently own all issued common

shares of OpCo in equal parts.

• He passed away on December 31, 2016

• The children do not wish to carry on their father’s business

• The corporation had the following tax attributes:

• GRIP of $500K

• CDA of $400K

• RDTOH of $25K

*Assumption: Harry and his children are taxed at the highest marginal

income tax rate

Harry

OpCo

1,000 Preferred Shares

ACB = nil

PUC = nil

FMV = $2M

13

Scenario #1: No Tax Planning (if Opco has cash only)

Harry’s Terminal Tax Return

Deemed disposition on death $2,000,000

Less adjusted cost base -

Capital gain 2,000,000

Taxable capital gain 1,000,000

Personal tax rate 53.53%

Harry’s income tax payable $535,300

OpCo

1,000 Preferred Shares

ACB = $2M

PUC = nil

FMV = $2M

Harry’s

Estate

14

Scenario #1: No Tax Planning (cont.)

On the wind-up of OpCo, the Estate will receive deemed dividend on which personal tax

liabilities are created.

Deemed dividend on distribution of assets

Eligible dividend $500,000

Capital dividend 400,000

Non-eligible dividend 1,100,000

Total deemed dividend 2,000,000

Personal tax on eligible dividends (39.34%) 196,700

Personal tax on non-eligible dividends (45.30%) 498,300

Total personal tax payable 695,000

Less: corporate dividend refund (25,000)

Net income tax liability $670,000

15

Scenario #1: No Tax Planning (cont.)

Note: A capital loss of $2M would be created on the wind-up. Stop loss rules may apply to postpone

the availability of the capital loss.

Harry

$535,300

Children

$670,000

Total

$1,205,300

16

Scenario #2: Pipeline Transaction

Harry’s Terminal Tax Return

Note: OpCo’s RDTOH and CDA balances may not be

fully utilized in the pipeline transaction

Deemed disposition on death $2,000,000

Less adjusted cost base -

Capital gain 2,000,000

Taxable capital gain 1,000,000

Personal tax rate 53.53%

Total income tax payable $535,300

HoldCo

100 Common Shares

Harry’s

Estate

OpCo

1,000 Preferred Shares

ACB = $2M

PUC = nil

FMV = $2M

Promissory

note of $2M

17

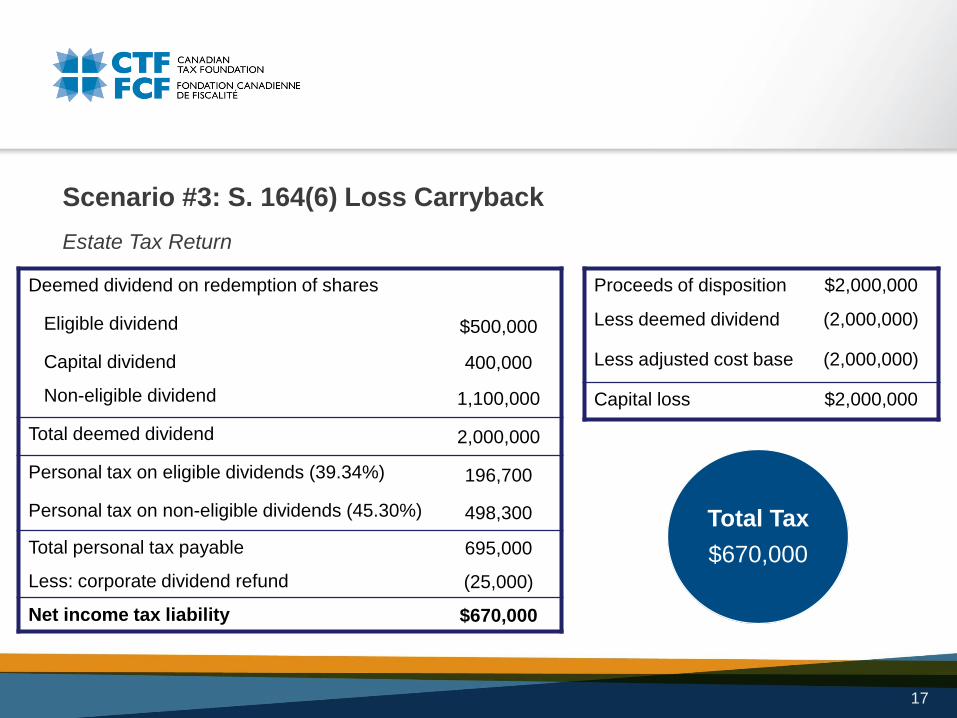

Scenario #3: S. 164(6) Loss Carryback

Estate Tax Return

Deemed dividend on redemption of shares

Eligible dividend $500,000

Capital dividend 400,000

Non-eligible dividend 1,100,000

Total deemed dividend 2,000,000

Personal tax on eligible dividends (39.34%) 196,700

Personal tax on non-eligible dividends (45.30%) 498,300

Total personal tax payable 695,000

Less: corporate dividend refund (25,000)

Net income tax liability $670,000

Proceeds of disposition $2,000,000

Less deemed dividend (2,000,000)

Less adjusted cost base (2,000,000)

Capital loss $2,000,000

Total Tax

$670,000

18

Scenario #3: S. 164(6) Loss Carryback (cont.)

Harry’s Terminal Tax Return

Deemed disposition on death $2,000,000

Less adjusted cost base -

Capital gain 2,000,000

Less loss carryback (2,000,000)

Taxable capital gain -

Personal tax rate 53.53%

Harry’s income tax payable -OpCo

Harry’s

Estate

19

Scenario #4: Hybrid Approach

The hybrid approach consists of redeeming sufficient shares to use the CDA and RDTOH

balances, and performing a pipeline with the remaining shares held by the Estate

Estate Tax Return

Deemed dividend on redemption of shares

Eligible dividend (2.61 x RDTOH balance) $65,250

Capital dividend 400,000

Total deemed dividend 465,250

Personal tax on eligible dividends (39.34%) 25,670

Total personal tax payable 25,670

Less: corporate dividend refund (25,000)

Net income tax liability $670

Proceeds of disposition $465,250

Less deemed dividend (465,250)

Less adjusted cost base (465,250)

Capital loss $465,250

Total Tax

$456,243

20

Scenario #4: Hybrid Approach (cont.)

Harry’s Terminal Tax Return

Deemed disposition on death $2,000,000

Less adjusted cost base -

Capital gain 2,000,000

Less loss carryback* (297,875)

Adjusted capital gain 1,702,125

Taxable capital gain 851,063

Personal tax rate 53.53%

Harry’s income tax payable $455,574

HoldCo

100 Common Shares

Harry’s

Estate

OpCo

1,000 Preferred Shares

ACB = $1.5M

PUC = nil

FMV = $1.5M

Promissory

note of $1.5M

*Stop-loss rule applies to grind down capital losses

available for loss carryback

21

Summary of Scenarios

No Tax

Planning

Pipeline

Transaction

Loss

Carryback

Hybrid

Approach

Tax owing on

Terminal T1$535,300 $535,300 - $410,775

Tax owing by the

corporation- - - -

Tax owing by the

Estate670,000 - 670,000 670

Total Tax $1,205,300 $535,300 $670,000 $411,445

Available CDA - 400,000 - -

Available GRIP - 500,000 - 434,750

Available RDTOH - 25,000 - -

22

Scenario #5: Asset Liquidation

The asset liquidation approach consists on selling all

of OpCo’s assets to a newly incorporated

corporation (“NewCo”)

• This transaction resembles a 88(1)(d) bump with

less restriction on the type of assets on which it

can be performed

• If the assets are sold within a year, the capital

loss realized on the redemption of shares may

be carried back to Harry’s terminal return but

may be subject to the stop-loss rules

OpCo

100 Common Shares

Harry’s

Estate

NewCo

1,000 Preferred Shares

ACB = $2M

PUC = nil

FMV = $2M

23

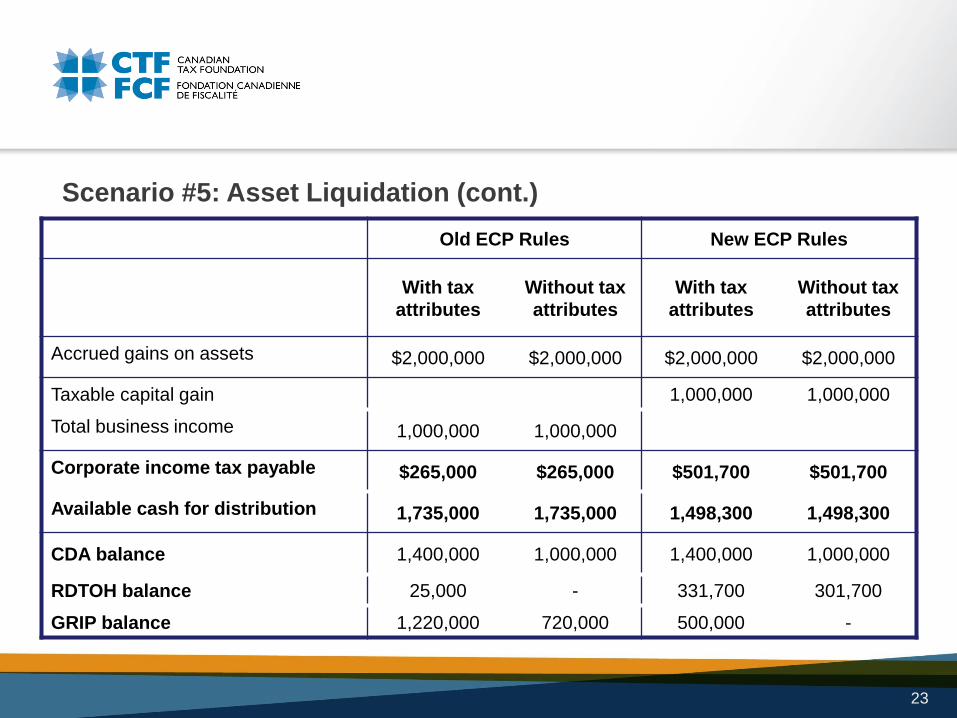

Scenario #5: Asset Liquidation (cont.)

Old ECP Rules New ECP Rules

With tax

attributes

Without tax

attributes

With tax

attributes

Without tax

attributes

Accrued gains on assets $2,000,000 $2,000,000 $2,000,000 $2,000,000

Taxable capital gain 1,000,000 1,000,000

Total business income 1,000,000 1,000,000

Corporate income tax payable $265,000 $265,000 $501,700 $501,700

Available cash for distribution 1,735,000 1,735,000 1,498,300 1,498,300

CDA balance 1,400,000 1,000,000 1,400,000 1,000,000

RDTOH balance 25,000 - 331,700 301,700

GRIP balance 1,220,000 720,000 500,000 -

24

Scenario #5: Asset Liquidation (cont.)Old ECP Rules New ECP Rules

With tax

attributes

Without tax

attributes

With tax

attributes

Without tax

attributes

Deemed dividend on distribution of

assets

Eligible dividend $335,000 $720,000 $98,300 -

Capital dividend 1,400,000 1,000,000 1,400,000 1,000,000

Non-eligible dividend - 15,000 - 498,300

Total deemed dividend $1,735,000 $1,735,000 $1,498,300 $1,498,300

Personal tax on eligible dividends 131,790 283,250 38,670

Personal tax on non-eligible

dividends- 6,795 - 225,730

Less corporate dividend refund (25,000) - (37,680) (191,015)

Net income tax liability $106,790 $290,045 $990 $34,715

Un-utilized RDTOH - - 294,020 140,685

25

Scenario #5: Asset Liquidation (cont.)

Old ECP Rules New ECP Rules

With tax

attributes

Without tax

attributes

With tax

attributes

Without tax

attributes

Tax owing on

Terminal T1$535,300 $535,300 $535,300 $535,300

Tax owing by the

corporation265,000 265,000 501,700 501,700

Tax owing by the

Estate106,790 290,045 990 34,715

Total Tax $907,090 $1,090,345 $1,037,990 $1,071,715

Available CDA - - - -

Available GRIP 885,000 - 401,700 -

Available RDTOH - - 294,020 140,685

26

Other Elements to Consider

• A hybrid approach, combining the pipeline transaction and loss carryback

strategy, typically yields the lowest overall tax to the estate

• The CRA has accepted the use of the pipeline transactions for investment type

corporations so long as the property distributed to the estate’s beneficiaries is

equal to the cost basis of the shares as a result of the deemed disposition on

death (i.e. the fair market value on time of death)

• Time is of the essence when performing post-mortem tax planning