realestate finance101 01

TRANSCRIPT

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 1/26

Introduction to

Cash Flow Analysis and

Real Estate Investing

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 2/26

Getting Rich in Real Estate

– “get-rich-quick” methods of

real estate investment often

assume self-management

while ignoring your

opportunity cost of time andthe risks of high leverage

– Many make more money

off of the seminars than

they do on their real estate

investments

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 3/26

Real Estate Does Provide Many

Opportunities Including Adding Value Through:

– Real estate acquisition

– Development

– Financing

– Site Analysis

– Controlling Operating Costs

– Innovative Marketing

– Innovative Management

No Secret Way To AttainSuccess

Only hard work with goodresearch and systematicanalysis

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 4/26

Business Goals Might Include

Maximize Long Term Shareholder Wealth

Short-Term Financial Goals, I.e. cash flow

Or Non-financial goals such as

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 5/26

Non-Financial Goals

Maintain a family friendly place to work

Maintain affirmative action hiring policies

Retain quality employees through tough marketsand tough times

Develop or own only the highest quality properties

in prestige locations

Be the largest owner in terms of market share of a

certain type of property in a local market

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 6/26

Short Term Financial Goals

Might IncludeSatisfy the requirements of the lender in terms of

pre-leasing or debt coverage cash flows

Satisfy the minimum required first year cash oncash returns required of investors

Project minimum internal rates of return for the

entire holding period of some minimum

percentageMaintain occupancy levels above 95% in all

portfolio properties

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 7/26

Financial Analysis Decision

ModelsSingle period model such as

– Cash on Cash

– Gross Rent Multipliers – Capitalization “Cap” Rate

Multiple period model

– IRR - Internal Rate of Return

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 8/26

IRR Model

Multiple period return on investment

Calculates the average discount rate that

equates all future returns over the projectedholding period back to the present value of

the initial equity investment

Should be used for capital allocation andinitial investment decisions

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 9/26

Real Estate Financial Analysis

Developer’s Goal: To invest capital in

projects that generate after tax returns that

exceed those of alternative risk-adjustedinvestment

Investor’s Goal: To buy property assets or

property securities for less than theirintrinsic value (the present value of a firm’s

future free cash flows)

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 10/26

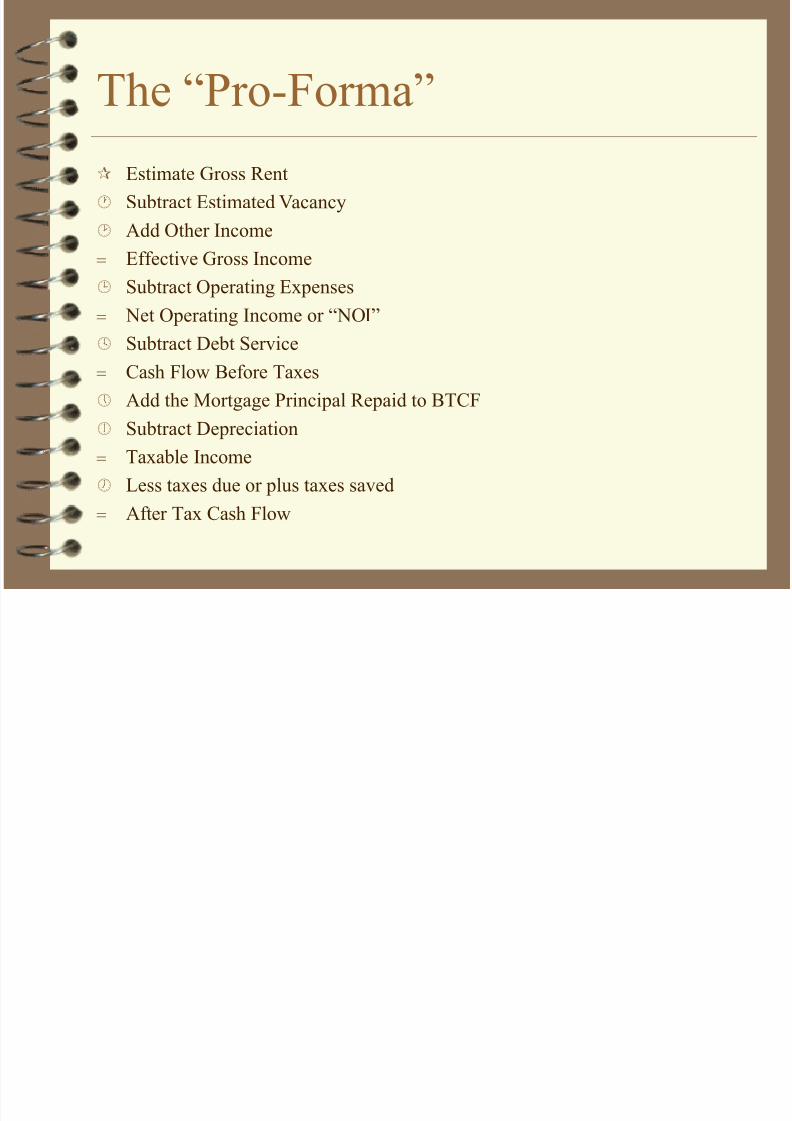

The “Pro-Forma”

Estimate Gross Rent

Subtract Estimated Vacancy

Add Other Income

Effective Gross Income

Subtract Operating Expenses

Net Operating Income or “NOI”

Subtract Debt Service

Cash Flow Before Taxes

Add the Mortgage Principal Repaid to BTCF

Subtract Depreciation

Taxable Income

Less taxes due or plus taxes saved

After Tax Cash Flow

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 11/26

“Pro-Forma” (cont.)

Should forecast previous numbers for at

least 5 to 10 years

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 12/26

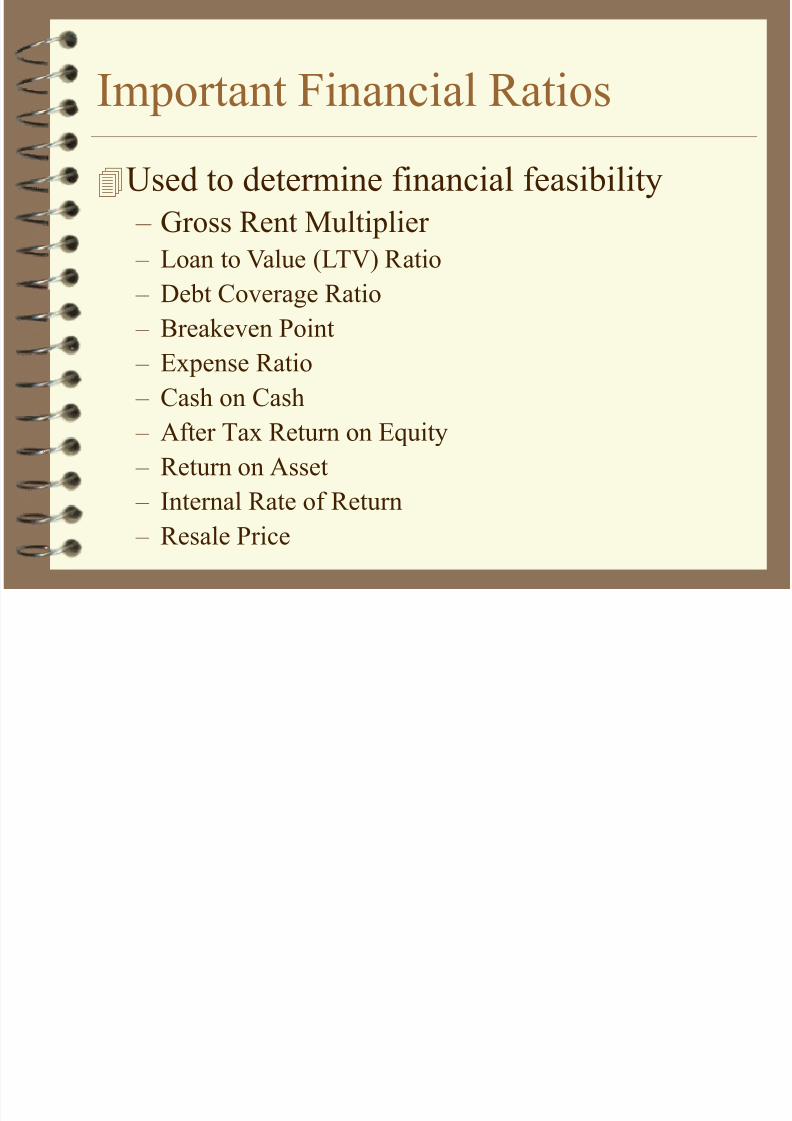

Important Financial Ratios

Used to determine financial feasibility

– Gross Rent Multiplier

– Loan to Value (LTV) Ratio

– Debt Coverage Ratio

– Breakeven Point

– Expense Ratio

– Cash on Cash

– After Tax Return on Equity

– Return on Asset

– Internal Rate of Return

– Resale Price

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 13/26

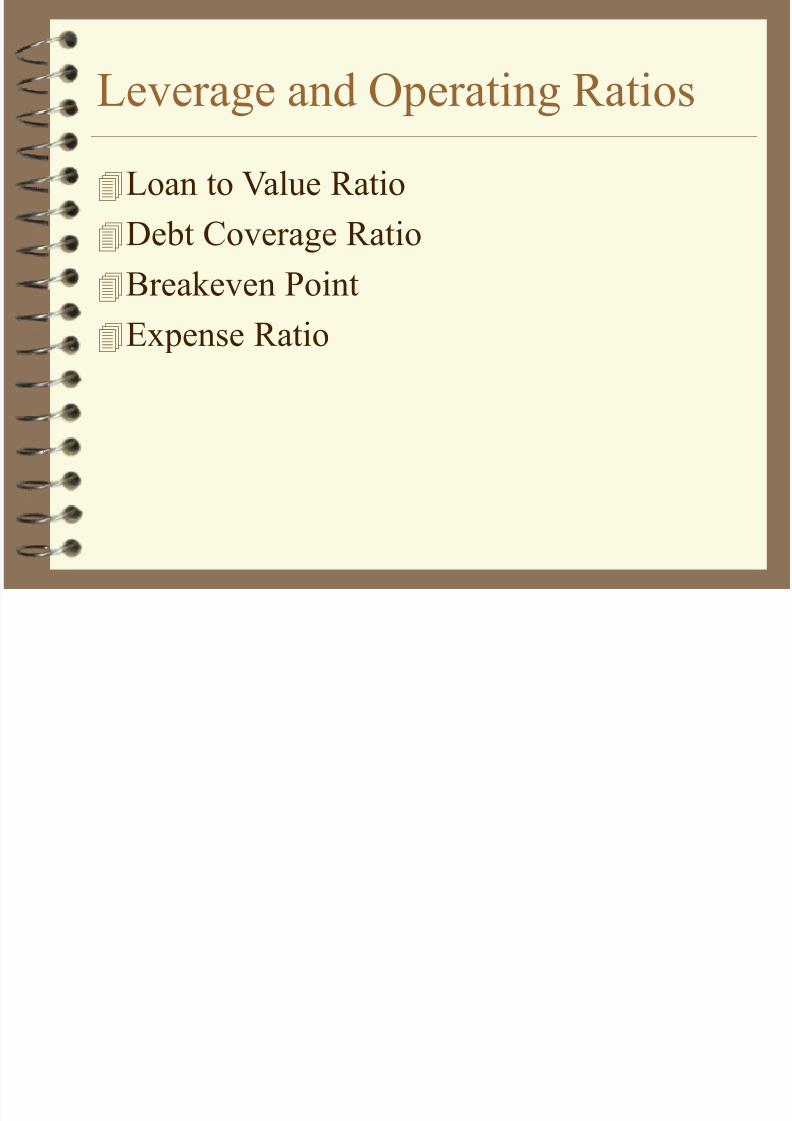

Leverage and Operating Ratios

Loan to Value Ratio

Debt Coverage Ratio

Breakeven Point

Expense Ratio

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 14/26

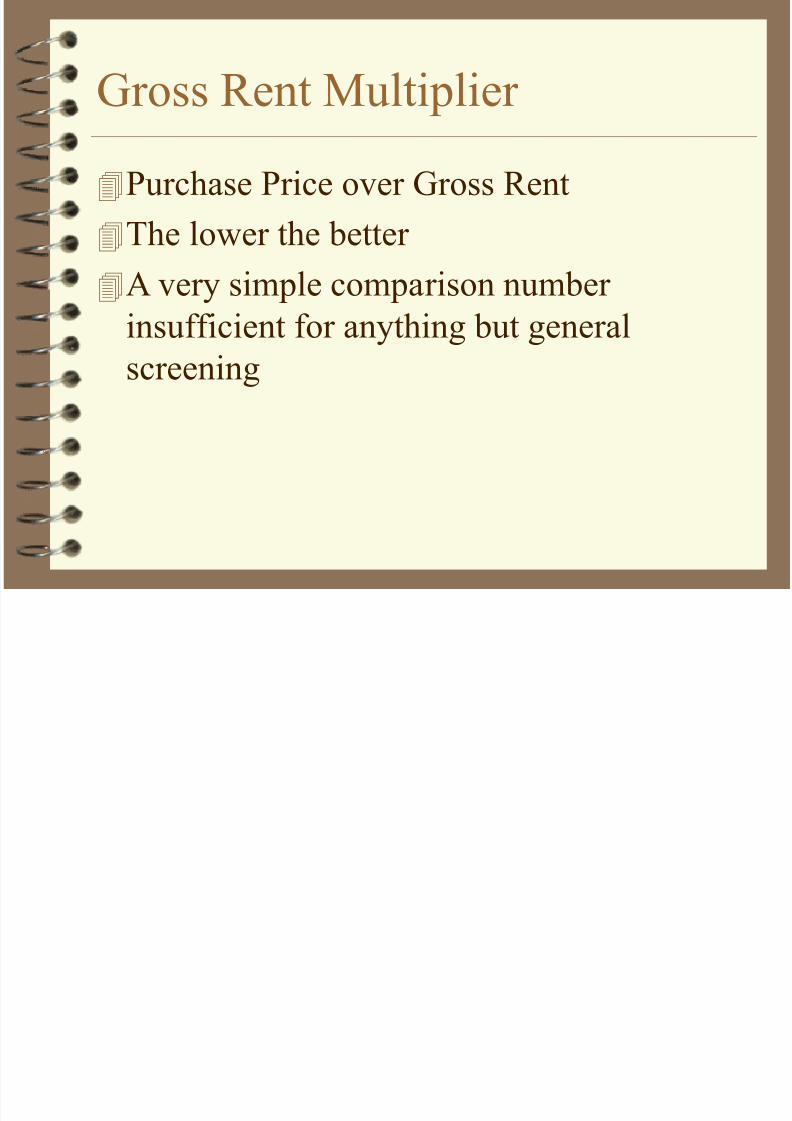

Gross Rent Multiplier

Purchase Price over Gross Rent

The lower the better

A very simple comparison numberinsufficient for anything but general

screening

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 15/26

Loan to Value Ratio

Measures real estate

financial risk

Default risk rises

proportionally with the

LTV ratio

Typical LTV in the

industry is 75%

Mortgage Loan Balance

------------------------------

Purchase Price

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 16/26

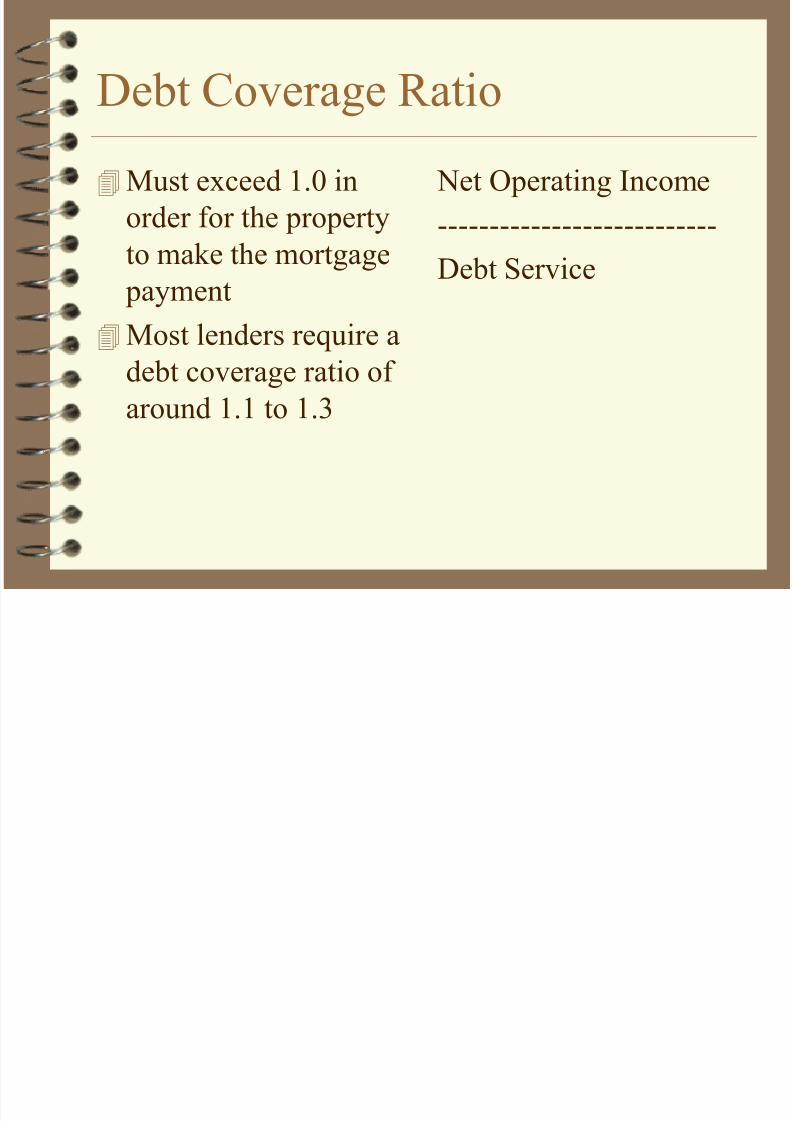

Debt Coverage Ratio

Must exceed 1.0 in

order for the property

to make the mortgage

payment

Most lenders require a

debt coverage ratio of

around 1.1 to 1.3

Net Operating Income

---------------------------

Debt Service

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 17/26

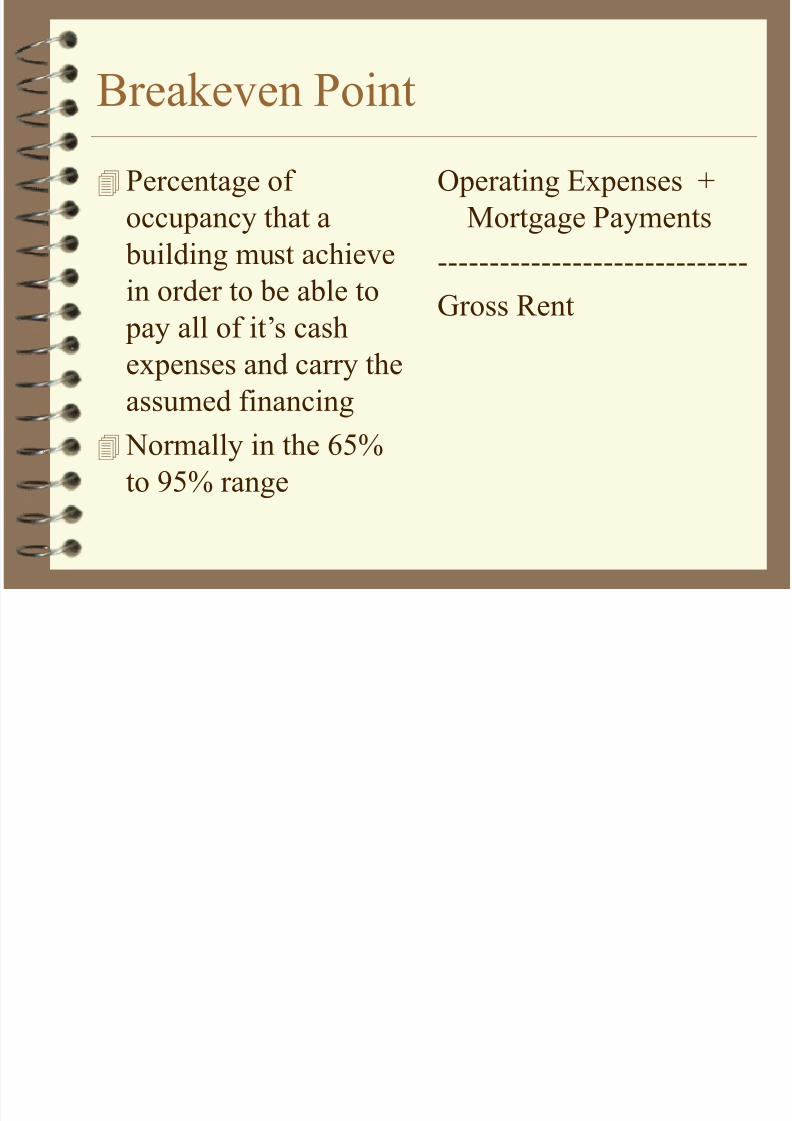

Breakeven Point

Percentage of

occupancy that a

building must achieve

in order to be able to

pay all of it’s cash

expenses and carry the

assumed financing Normally in the 65%

to 95% range

Operating Expenses +

Mortgage Payments

------------------------------

Gross Rent

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 18/26

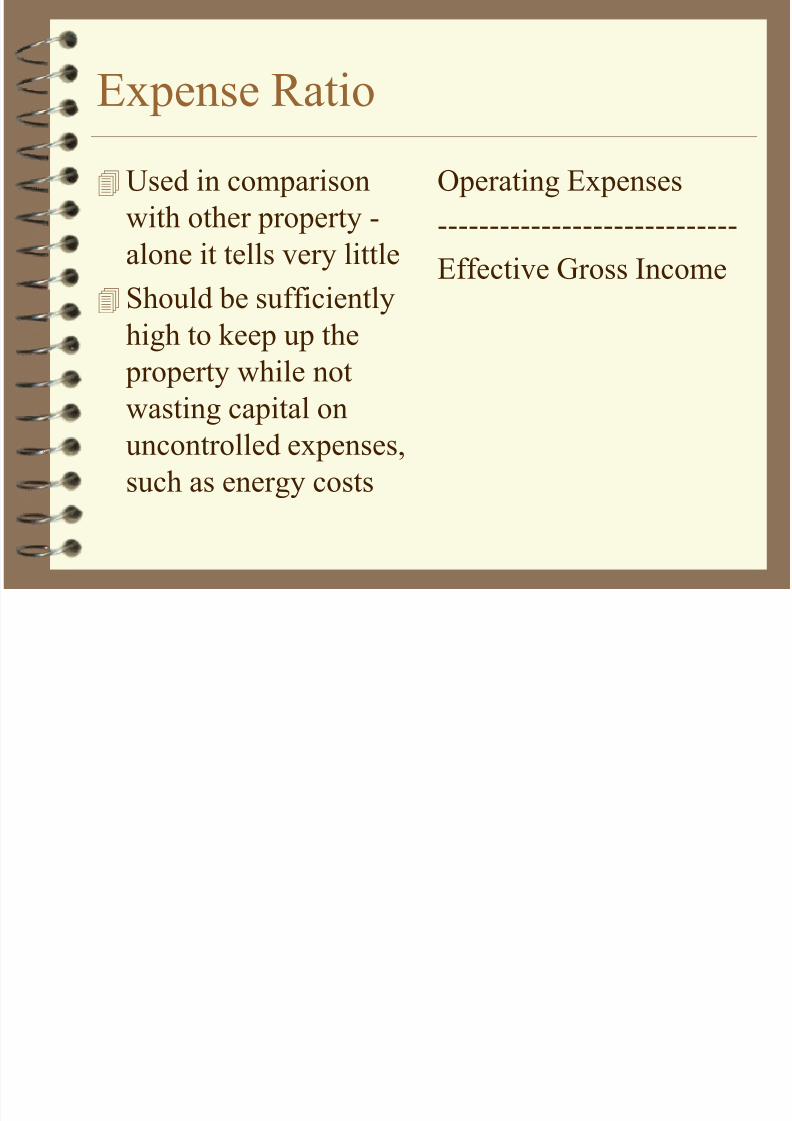

Expense Ratio

Used in comparison

with other property -

alone it tells very little

Should be sufficiently

high to keep up the

property while not

wasting capital onuncontrolled expenses,

such as energy costs

Operating Expenses

-----------------------------

Effective Gross Income

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 19/26

Single Period or “Static”

Profitability MeasuresCash on Cash

After Tax Return on Equity

Return on Asset or Going in Cap Rate

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 20/26

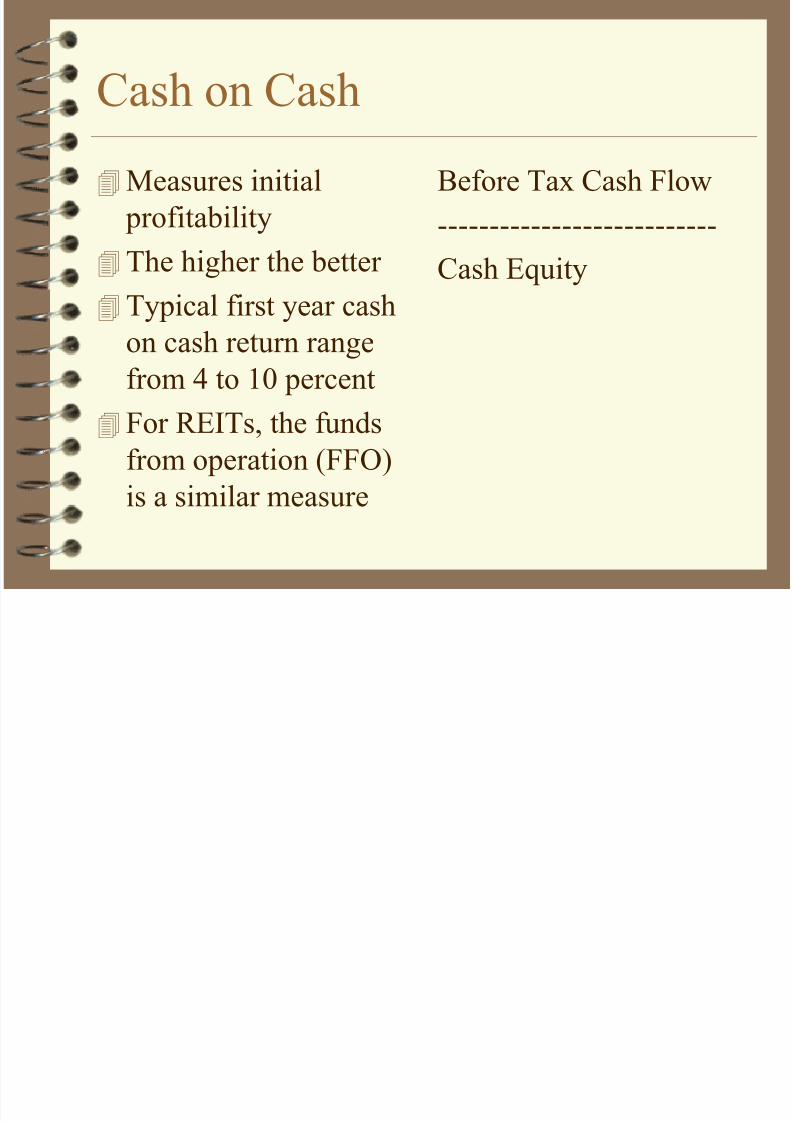

Cash on Cash

Measures initial

profitability

The higher the better

Typical first year cash

on cash return range

from 4 to 10 percent

For REITs, the fundsfrom operation (FFO)

is a similar measure

Before Tax Cash Flow

---------------------------

Cash Equity

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 21/26

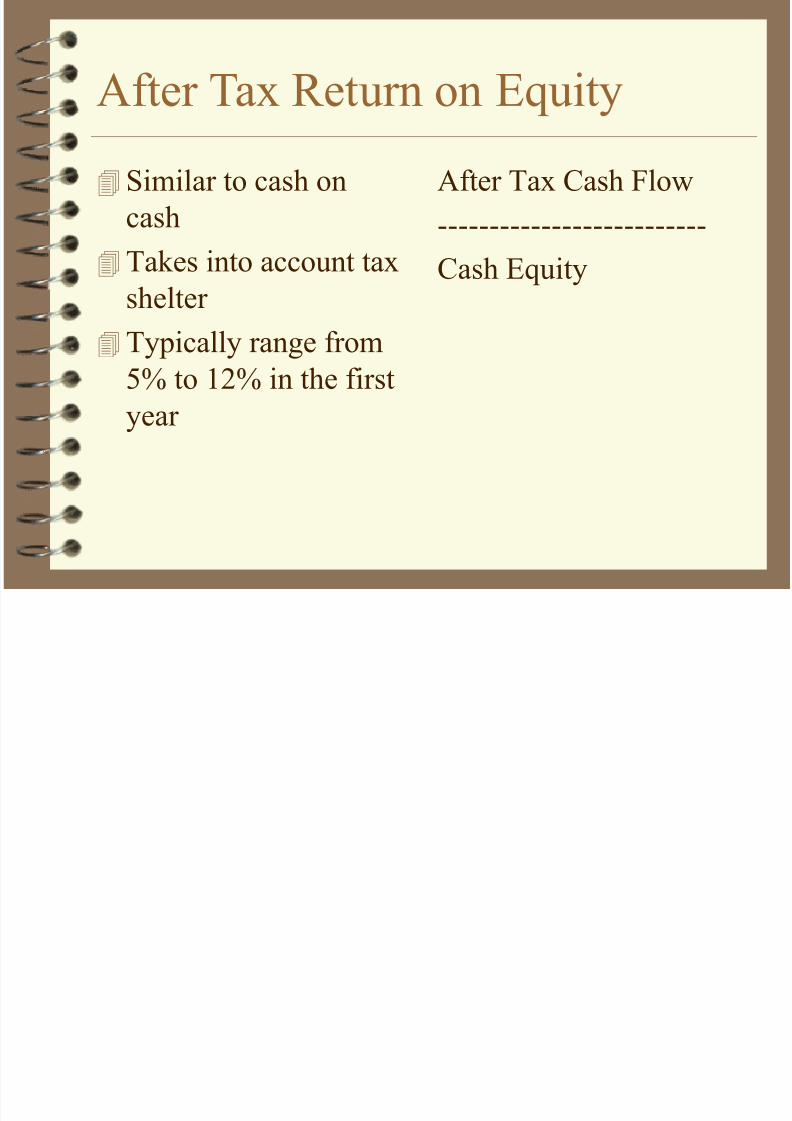

After Tax Return on Equity

Similar to cash on

cash

Takes into account tax

shelter

Typically range from

5% to 12% in the first

year

After Tax Cash Flow

--------------------------

Cash Equity

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 22/26

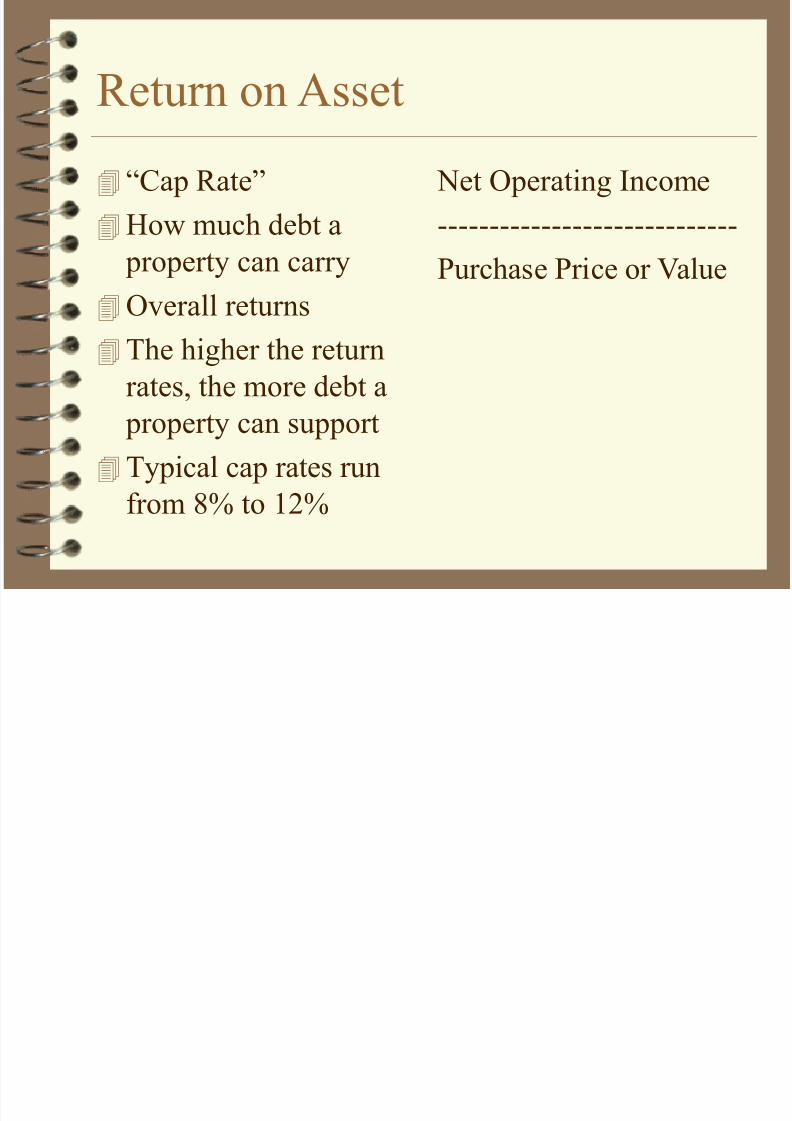

Return on Asset

“Cap Rate”

How much debt a

property can carry

Overall returns

The higher the return

rates, the more debt a

property can support

Typical cap rates run

from 8% to 12%

Net Operating Income

-----------------------------

Purchase Price or Value

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 23/26

Multiple Period or “Dynamic”

Return MeasuresInternal Rate of Return (IRR)

Consider Appreciation Through Resale

Price or Refinancing

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 24/26

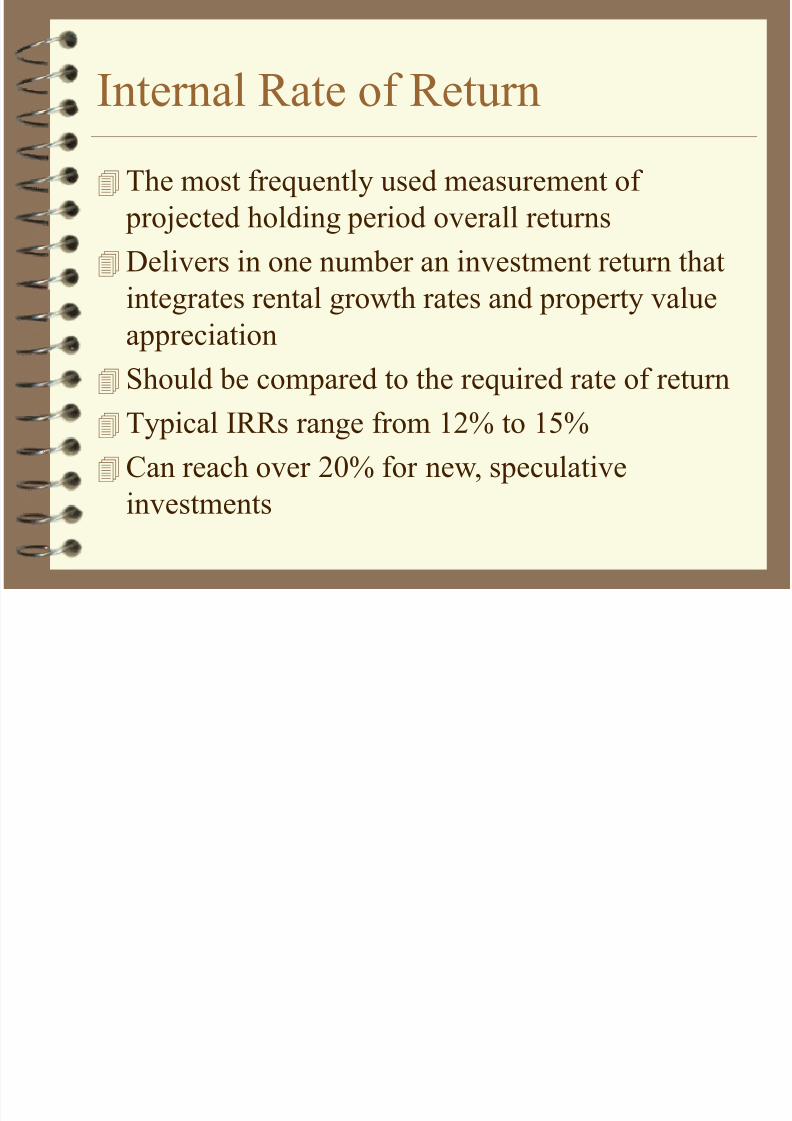

Internal Rate of Return

The most frequently used measurement of

projected holding period overall returns

Delivers in one number an investment return that

integrates rental growth rates and property value

appreciation

Should be compared to the required rate of return

Typical IRRs range from 12% to 15%

Can reach over 20% for new, speculative

investments

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 25/26

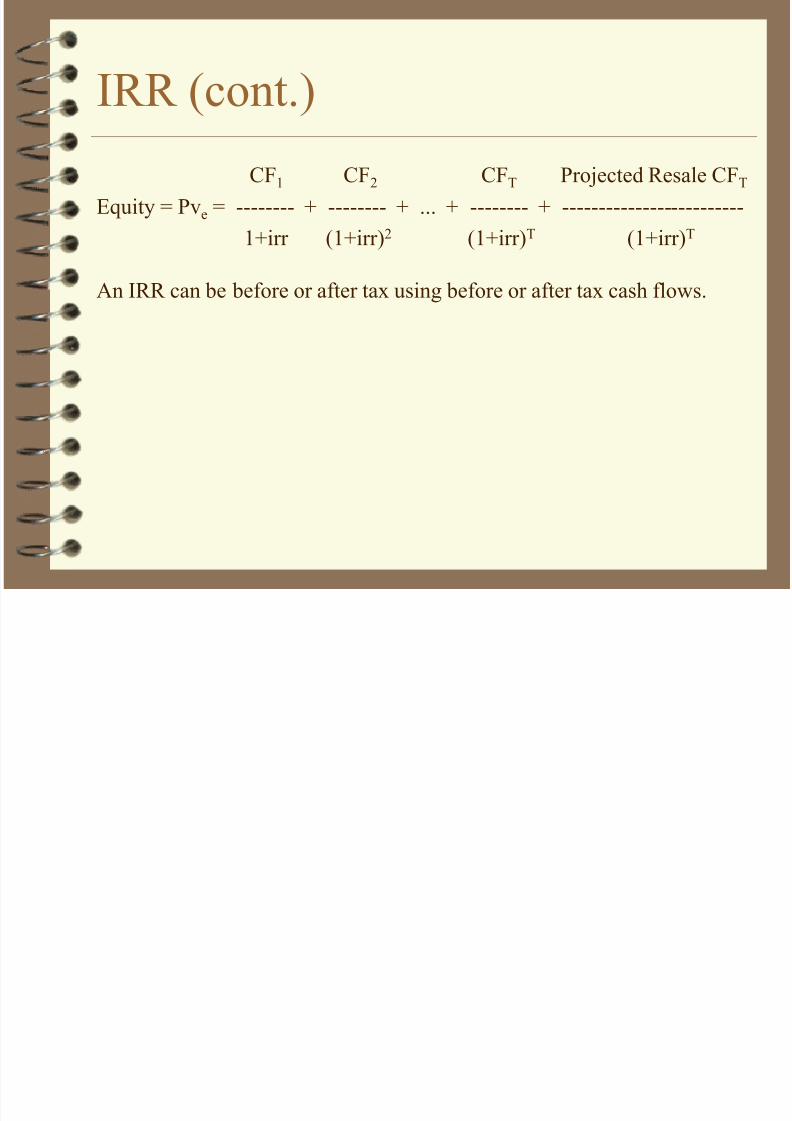

IRR (cont.)

CF1 CF2 CFT Projected Resale CFT

Equity = Pve = -------- + -------- + ... + -------- + -------------------------

1+irr (1+irr)2 (1+irr)T (1+irr)T

An IRR can be before or after tax using before or after tax cash flows.

8/12/2019 Realestate Finance101 01

http://slidepdf.com/reader/full/realestate-finance101-01 26/26

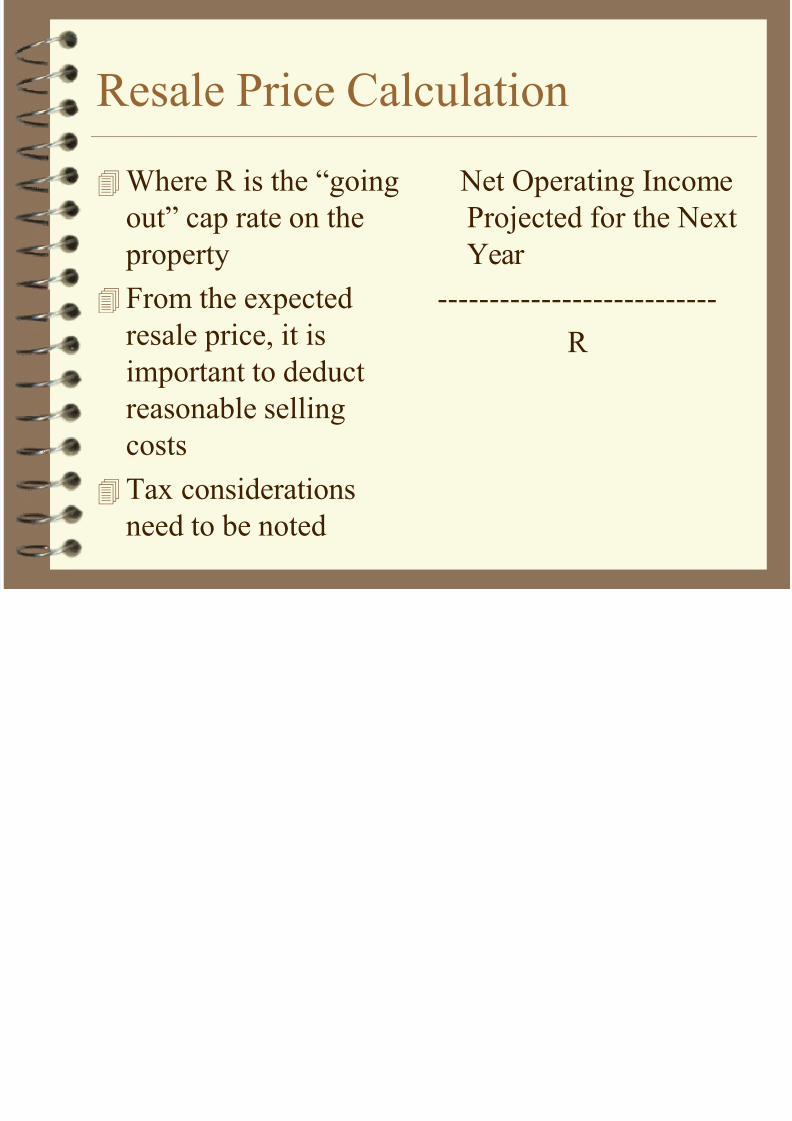

Resale Price Calculation

Where R is the “going

out” cap rate on the

property

From the expected

resale price, it is

important to deduct

reasonable sellingcosts

Tax considerations

need to be noted

Net Operating Income

Projected for the Next

Year

---------------------------

R