real estate investment chapter 8 single-family dwellings and condominiums © 2011 cengage learning

TRANSCRIPT

Real Estate Investment Real Estate Investment

Chapter 8Chapter 8

Single-Family Dwellingsand Condominiums

© 2011 Cengage Learning

© 2011 Cengage Learning

Key TermsKey Terms

Acquisition debt

Adjusted basis of the home

Advance rentals

Business use of a home

Capital gain

Capital improvement

Exclusion

Home equity debt

Long-term lease

Part-time for rental purposes

Realized selling price

Time-sharing ownership

© 2011 Cengage Learning

The Principal Residence

That place where the taxpayer actually lives most of the time and calls “home.”

Condominium

Single-family house

Vacant lot with mobile home or tent

Retirement units

Etc….

© 2011 Cengage Learning

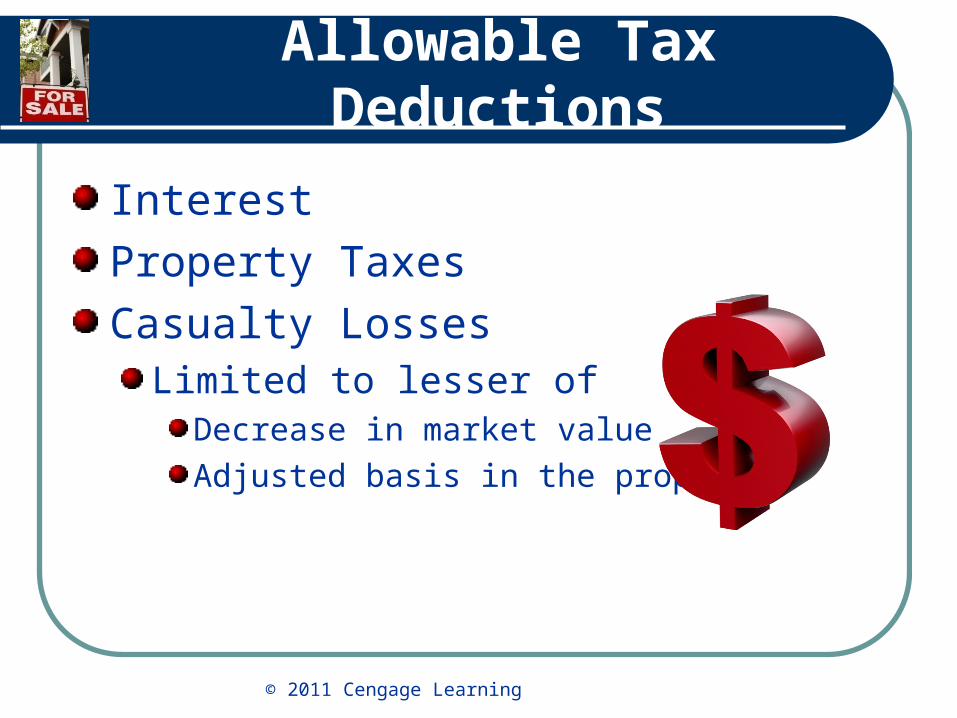

Allowable Tax Deductions

Interest

Property Taxes

Casualty LossesLimited to lesser of

Decrease in market value

Adjusted basis in the property

© 2011 Cengage Learning

Limits on Interest Deductions

Home acquisition debtDebt that incurred in acquiring, constructing, or substantially improving any qualified residence.

principal residence plus one

For such mortgages originated after 10/13/87, interest is deductible on debt that does not exceed $1 million.Debt limited to $500,000 married taxpayer filing separately or a single person.

© 2011 Cengage Learning

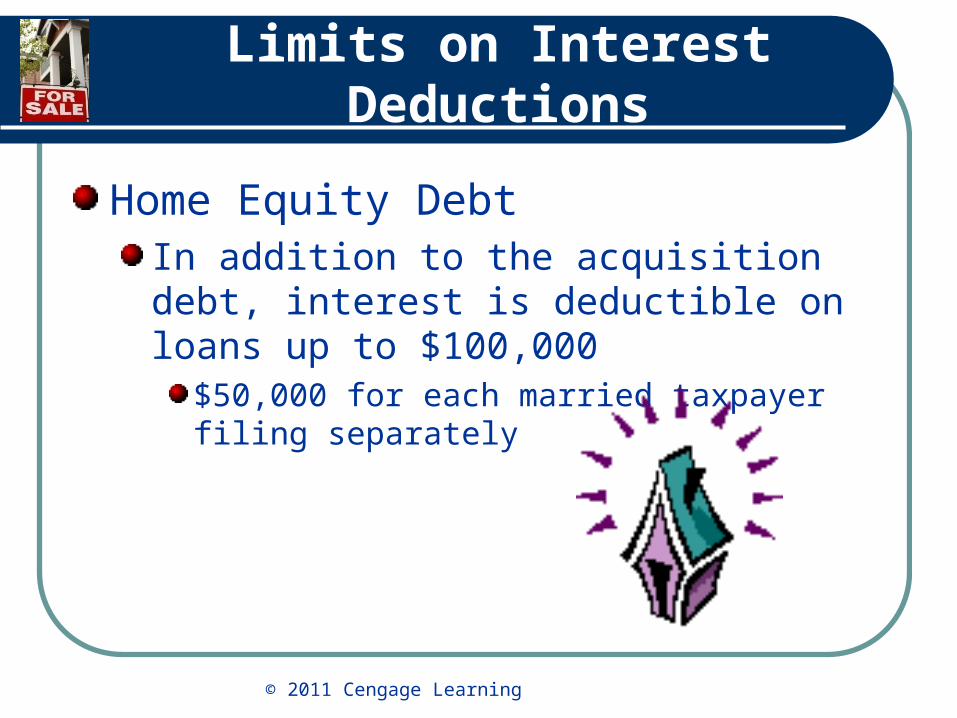

Limits on Interest Deductions

Home Equity DebtIn addition to the acquisition debt, interest is deductible on loans up to $100,000

$50,000 for each married taxpayer filing separately

© 2011 Cengage Learning

Limits on Interest Deductions

Additional Qualified Residential PropertyMobile homes, boats, vacation cabins….

Discount as a Deduction

Property Tax DeductionTaxpayer-owned residences without limitations

© 2011 Cengage Learning

Tax Treatment on Gain from Sale

$250,000 if single or $500,000 if married and filing jointlyRequirements:

House must be owned as taxpayer’s main home for 2 or more years during five-years prior to sale

If married, only one spouse needs to meet this requirement.

Taxpayer must not have sold or exchanged another main home over last 2 years.

© 2011 Cengage Learning

Calculation of Capital Gain on Sale of Personal Residence

Difference between the adjusted basis of the home and the realized selling price

Basis of Property ValueAdjusted basis

© 2011 Cengage Learning

Adjustments to Basis

Increases:Improvements

Additions

Other capital expenses

Special assessments for local improvements

Amounts spent to restore damaged property

© 2011 Cengage Learning

Adjustments to Basis

Decreases:Insurance reimbursements for casualty losses.

Deductible casualty losses not covered by insurance.

Payments received for easement or right-of-way granted.

Depreciation allowed, but only if the home is used for business or rental purposes.

© 2011 Cengage Learning

Realized Selling Price

Total Consideration ReceivedCash, notes, mortgages, fair market value of any real or personal property received.

Less Selling ExpensesSales commission, advertising, legal fees, loan placement fees or discount points.

Less Fixing-Up ExpensesDecorating and repair costs incurred solely to assist in the sale.

© 2011 Cengage Learning

Record Keeping

Proof of the home’s purchase price and purchase expenses.Receipts and records for all improvements, additions, and other items that affect the home’s adjusted basis.Worksheets concerning the adjusted basis of the home, the gain or loss on the sale, the exclusion, and the taxable gain.Form 982 regarding discharge of indebtedness.Form 2119 filed to postpone gain from the sale of a previous home. Worksheets that were used to prepare Form 2119.

© 2011 Cengage Learning

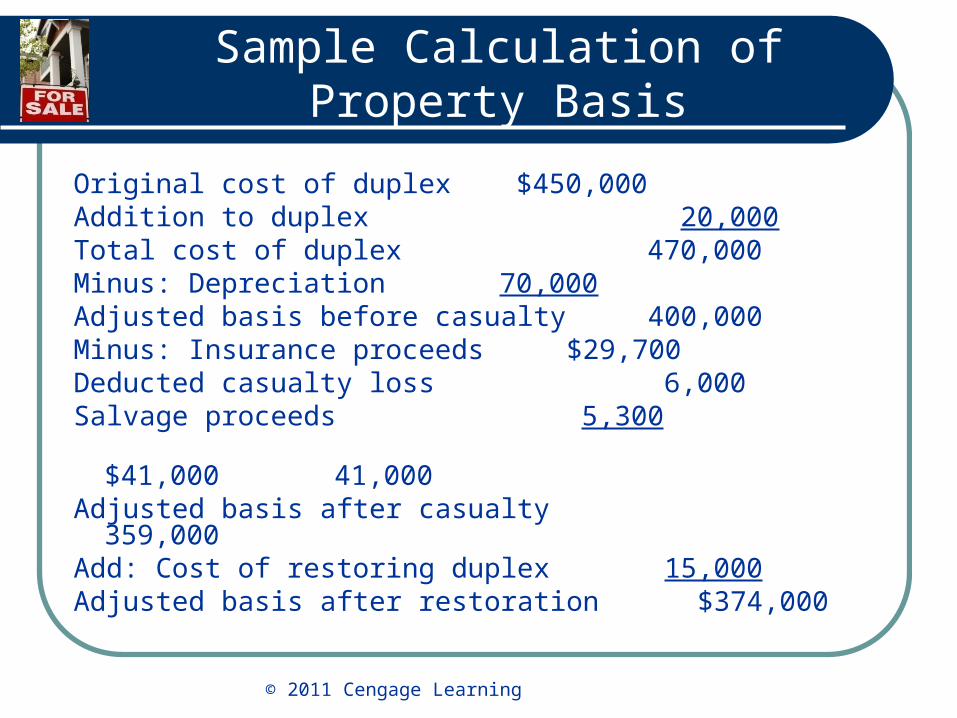

Sample Calculation of Property Basis

Original cost of duplex $450,000Addition to duplex 20,000Total cost of duplex 470,000Minus: Depreciation 70,000Adjusted basis before casualty 400,000Minus: Insurance proceeds $29,700Deducted casualty loss 6,000Salvage proceeds 5,300 $41,000 41,000Adjusted basis after casualty 359,000Add: Cost of restoring duplex 15,000Adjusted basis after restoration $374,000

© 2011 Cengage Learning

Sale of a Principal Residence Married Couple Filing Jointly

Purchase Price $180,000Purchase Costs $10,000Acquisition Basis $190,000Capital Improvements $30,000Adjusted Basis $220,000Sales Price $700,000Less Adjusted Basis $220,000Gain on the Sale $480,000Less Exclusion $500,000Taxable Gain -0-Capital Gains Tax Rate* 20%Tax Due -0-

© 2011 Cengage Learning

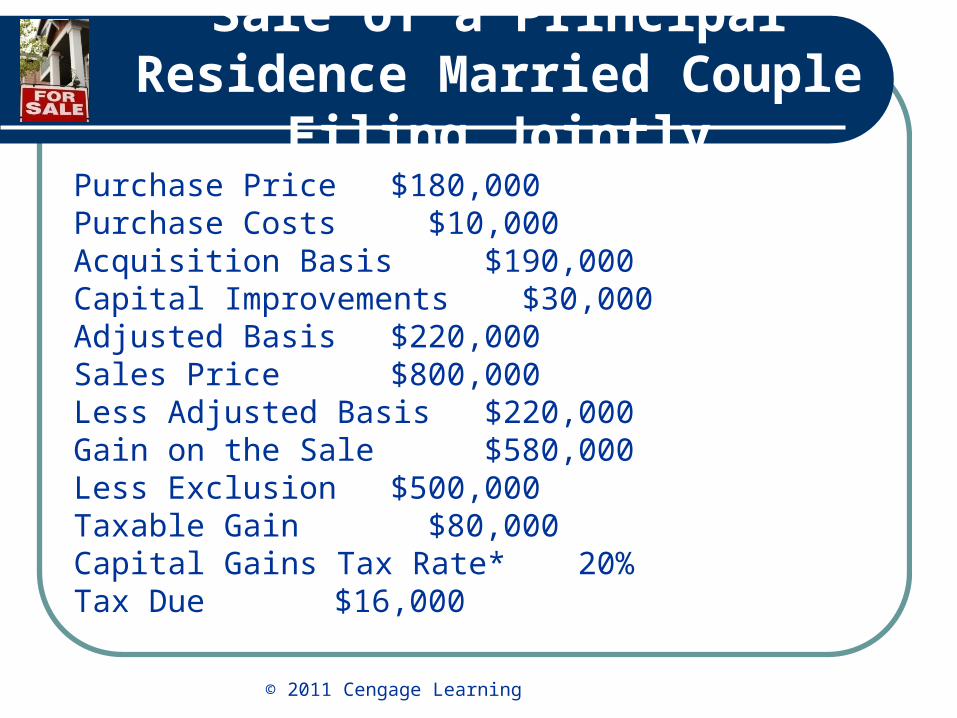

Sale of a Principal Residence Married Couple Filing Jointly

Purchase Price $180,000Purchase Costs $10,000Acquisition Basis $190,000Capital Improvements $30,000Adjusted Basis $220,000Sales Price $800,000Less Adjusted Basis $220,000Gain on the Sale $580,000Less Exclusion $500,000Taxable Gain $80,000Capital Gains Tax Rate* 20%Tax Due $16,000

© 2011 Cengage Learning

RESIDENCE CONVERTED TO RENTAL USE

Necessary to determine the basis from which the property may be depreciated. Basis is the lesser of:

1. The fair market value of the property on the date of conversion.

2. The adjusted basis of the property

© 2011 Cengage Learning

RESIDENCE CONVERTED TO RENTAL USE

The income and expenses of rental property are subject to IRS rules

Rental IncomeRegular Payments

Advance Rent

Payment for Lease Cancellation

Expenses Paid by Tenant

© 2011 Cengage Learning

RESIDENCE CONVERTED TO RENTAL USE

Rental ExpensesCost Recovery (Depreciation)

Repairs and Maintenance

Handicap Exception

Other Expenses

Rental of a room

© 2011 Cengage Learning

Business Use of the Home

Permissible deductions include depreciation, maintenance, insurance, and utility expenses

allocated to the portion of the house used for business

deduction taken for depreciation reduces the basis of value

Taxpayers may no longer lease a portion of a home to an employer and claim deductions as a business usage.

© 2011 Cengage Learning

Business Use of the Home

The limit on deductions is the gross income from that business minus the sum of:1. The business % of the otherwise deductible taxes and casualty and theft losses.2. The business expenses not attributable to the use of the home, such as salaries and supplies.

© 2011 Cengage Learning

Part-Time Rental Units

Most commonly used for vacation homesDwelling unit may be a house, apartment, condominium, mobile home, boat, or other similar property

Personal use occurs when a dwelling unit is used by:1. The taxpayer, a member of the family, or any other person with an interest in the property, unless a fair market rental is paid.2. Anyone under a reciprocal arrangement that enables the taxpayer to use some other dwelling unit.3. Anyone at less than a fair rental.

© 2011 Cengage Learning

Part-Time Rental Units

Allocation of ExpensesCategory 1—Rented Less Than 15 Days

Category 2—Part Rental, Part Personal UseLimitations on Allocation of Expenses

Category 3—Personal Use, Less Than 15 Days

© 2011 Cengage Learning

Time-Sharing Ownership

Time-sharing ownership means the holding of rights to exclusive use of real estate for a designated length of time

Long-Term Lease

Condominium Time-Sharing

© 2011 Cengage Learning

Condominiums

Typically a fee simple estate in a specific unit, while owning the community property as a tenant in commonThe Unit Owner

Mortgage InterestReal Estate TaxesMaintenance, Repairs, InsuranceDepreciation or Cost RecoveryCapital ImprovementsSale or Exchange of a unit