real estate & financial markets (refm)...

TRANSCRIPT

Real Estate & Financial Markets (REFM) Lab

Mission and Organization

10/11/2013 1 Fisher Center for Real Estate & Urban Economics

REFM Lab Mission

• Provide modeling and analytic technology, data, hardware, software,

and personnel needed to conduct economic analyses of real estate

asset and capital markets. Develop scientific advances in valuation

methods and systemic risk management practices needed for

trading and monitoring activities in these markets.

10/11/2013 Fisher Center for Real Estate & Urban Economics 2

REFM Lab – Goals

• Our Goals:

– Contribute to the policy debate on the risk channels associated with real estate and mortgage markets in the U.S.

• Macro and micro-economic foundations of real estate cycles,

• Effects of monetary policy on mortgage capital market flows.

• Supply and demand dynamics in housing and commercial real estate markets, including the effects of transportation infrastructure, job creation, and migration.

• Develop and monitor house price indices.

– Develop real estate and mortgage market risk management tools.

• Interest rate, credit, and energy risk.

• New metrics for systemic and regional components of these risks.

– Establish risk analytics for the primary real estate energy sources – natural gas and electricity

• Identify optimal capital market incentives for improving the energy efficiency of U.S. real estate markets.

10/11/2013 Fisher Center for Real Estate & Urban Economics 3

REFM Lab – Where we want to be

• Overarching Goals:

– Develop a large research data center focused on real estate asset and capital markets.

• Center design includes IT infrastructure and security systems for large and often proprietary data sets.

– Undertake high-quality academic research, to publish the findings of this research in academic journals and other practitioner outlets, and to promote data-based graduate student training that is focused on these markets.

• Immediate Needs:

– Establish a high-performance and flexible hardware / software architecture that • Provides concurrent access to the REFM Lab datasets through a high-speed network

• Benefits from the existing processing power

– Users already holding powerful computers at their desktops can run processes locally

– All users, including those without powerful local computational resources, have access to a shared processing facility composed of powerful compute servers

– Implement a structured approach for granting user access to the lab datasets and running processes for analyzing data

– Create a systematic approach for backing up lab datasets

10/11/2013 Fisher Center for Real Estate & Urban Economics 4

REFM Lab Cluster Implementation (cont.)

10/11/2013 Fisher Center for Real Estate & Urban Economics 5

VPN

Wide Area

Network

Private High Speed Network

Haas LANAirBears

Bear Compute Node

Ethernet

REFM Lab Compute Node

Bear NAS

Wireless access point

Switch

Laptop computer

Desktop

Bear Master Node

REFM Lab NAS

Firewall

Symbol Description

Legend

4 x 1.0 Gb/s4 x 1.0 Gb/s

iSCSI

16 x 1.0 Gb/s

iSCSI

16 x 1.0 Gb/s

iSCSI

16 x 1.0 Gb/s

Purchase

Provided by Haas

REFM Lab Architecture – Next Steps

• Integrate REFM Lab with other scientific Labs such as Computer Science’s,

Lawrence Berkeley, etc…

• Continue to expand the datasets

– USGS National Elevation Dataset (Geospatial Data)

– NRCS Gridded Soil Survey Geographical Database (Geospatial Data)

– DataQuick – Nationwide residential house price and transaction data

– Bridge into other external datasets such as Nielsen’s data

– Etc…

• Establish a data model for REFM’s datasets

10/11/2013 Fisher Center for Real Estate & Urban Economics 6

REFM Data Sets

Mortgage markets

Financial Services

Asset Markets

10/11/2013 Fisher Center for Real Estate & Urban Economics 7

• FNMA/FHLMC: mortgage origination and performance (32M)

• Subprime: mortgage origination and performance (22M)

• GSE and Subprime pools: origination and performance

• Commercial mortgage: origination and performance (~100K)

• RMBS pricing (daily): Bloomberg.

• CMBS pricing (index): NAICs mortgage insurer investments.

• Call reports (FFIEC0041): Depositories.

• Bank Holding Company Reports (BHC FR9C).

• Survey of Deposits (SOD): FDIC branching data.

• HMDA: bank/ geography loan-level origination.

• HMDA crosswalk: links between above.

• Thrift call reports • Nets Establishment data:

All Employment and Sales, (22M).

• House Prices (Dataquick): Transactional data CA, option on all U.S. 1996-2012.

• House Prices (CMDC): Transactional data 1970-1996 (three counties).

• Assessors data: House-by-house characteristics.

• Electricity Forwards (Platts): (10 hubs, 1998-2009).

• Natural Gas Futures (NYMEX): (Henry Hub, 1998-2009).

• Commercial RE Prices (US): (1996-2009)

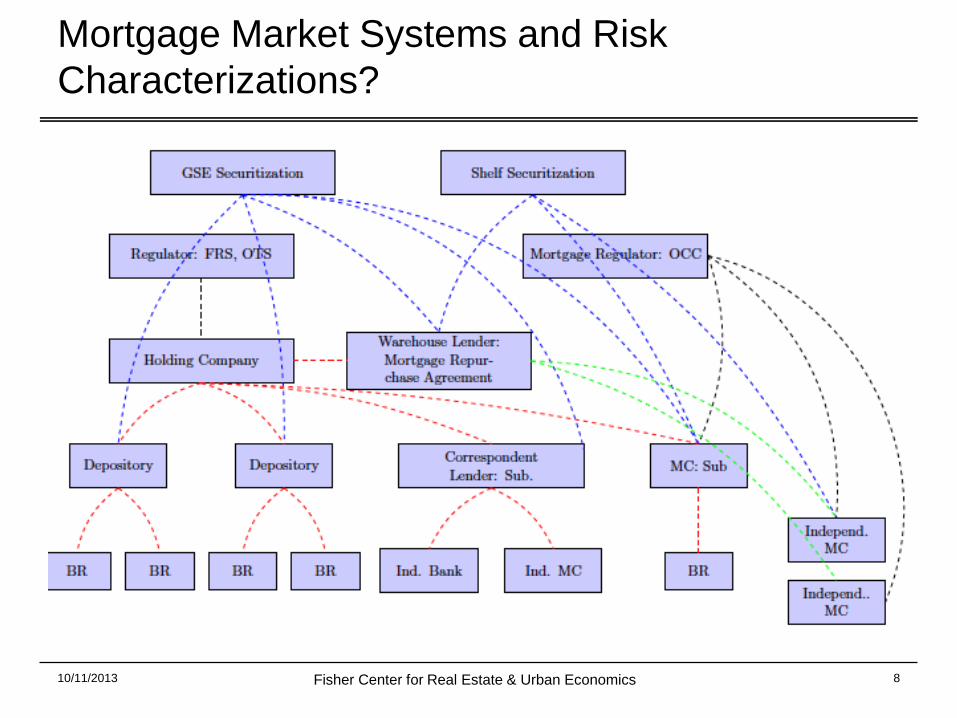

Mortgage Market Systems and Risk

Characterizations?

10/11/2013 Fisher Center for Real Estate & Urban Economics 8

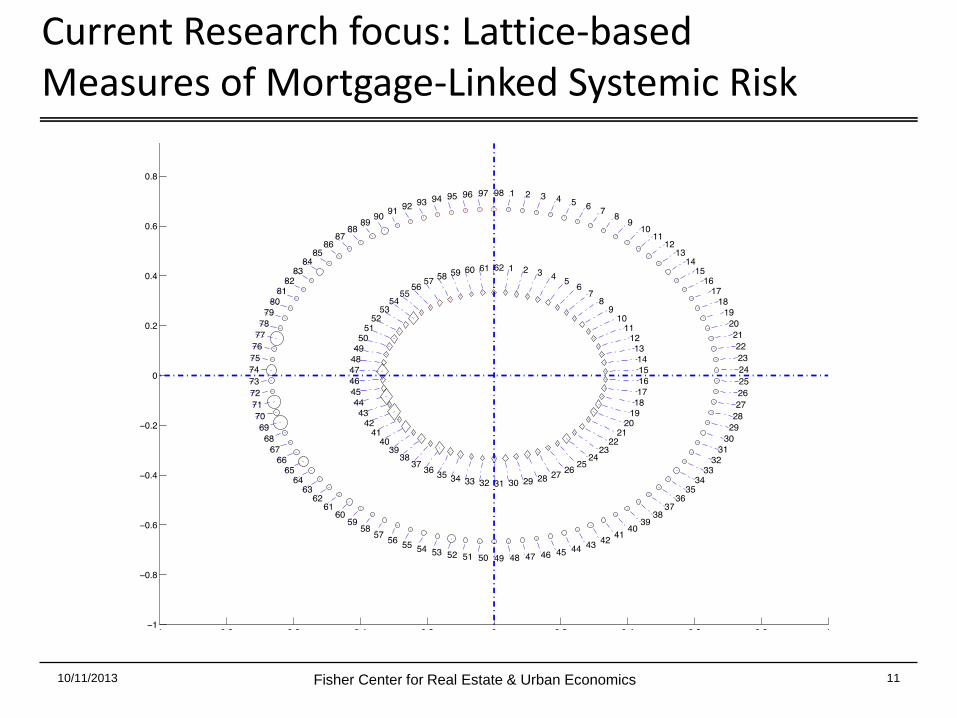

Current Research focus: Lattice-based Measures

of Mortgage-Linked Systemic Risk

10/11/2013 Fisher Center for Real Estate & Urban Economics 9

Current Research focus: Lattice-based Measures

of Mortgage-Linked Systemic Risk

10/11/2013 Fisher Center for Real Estate & Urban Economics 10

10/11/2013 Fisher Center for Real Estate & Urban Economics 11

Current Research focus: Lattice-based Measures of Mortgage-Linked Systemic Risk

Dynamic House Price Indices: Designed for

Fixed Income Valuation

• Price Indices Require: Controls for the evolution of “Prices” and for

the evolution of the “Characteristics” (Quantity of Housing Services)

for each house.

– Current repeat sales indices do not do this!

• Our estimator includes two Poisson processes: 1) likelihood of re-

modelling and 2) likelihood of sale.

– Controls for the housing characteristics and the probability that these

characteristics will change as a function of macro fundamentals.

– Controls for the probability of sale as a function of macro fundamentals.

• Conditioned on these intensities: Use classical linear filtering

techniques to estimate underlying “index”

– Model includes reasonable assumptions for the long term average

dynamics (mean reversion) of house prices and the dynamics of the

volatility of house prices.

10/11/2013 Fisher Center for Real Estate & Urban Economics 12

Differences in probabilities of sales by house

structure

10/11/2013 Fisher Center for Real Estate & Urban Economics 13

0%

20%

40%

60%

80%

100%

120%

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Two_Bedroom_Repeat Three_Bedroom_Repeat Four_Bedroom_Repeat

San Francisco County: Price Effects of New

Supply

10/11/2013 Fisher Center for Real Estate & Urban Economics 14

Augmented Commercial Mortgage Valuation

Models

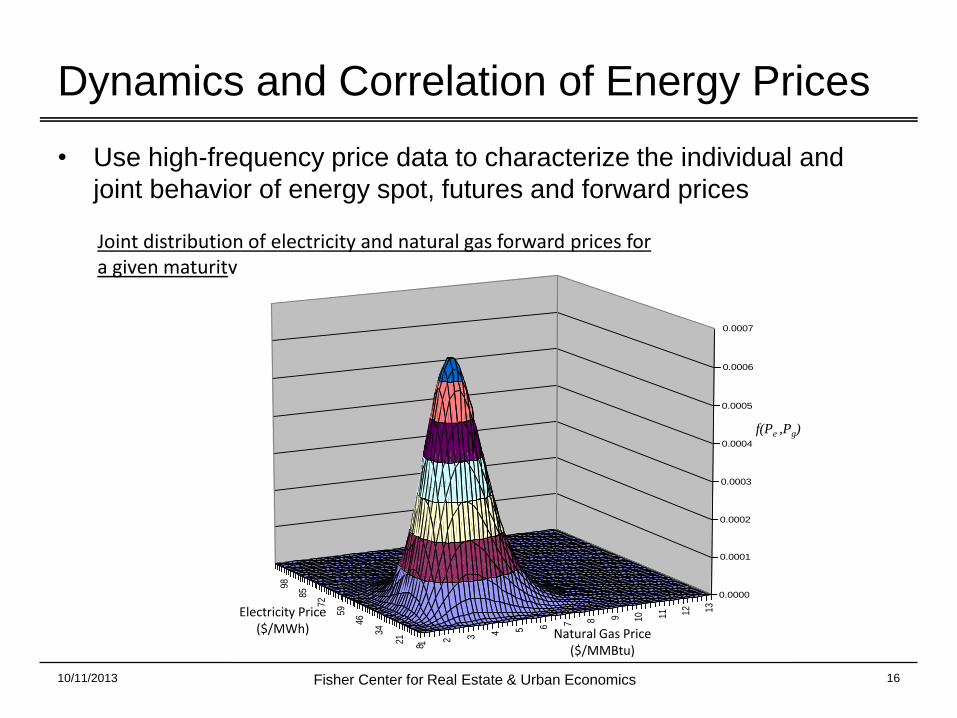

Dynamics and Correlation of Energy Prices

• Use high-frequency price data to characterize the individual and

joint behavior of energy spot, futures and forward prices

10/11/2013 Fisher Center for Real Estate & Urban Economics 16

Joint distribution of electricity and natural gas forward prices for a given maturity

1 2 3 4 5 6 7 8 9 10 11 12 13

821

34

46

59

72

85

98

0.0000

0.0001

0.0002

0.0003

0.0004

0.0005

0.0006

0.0007

Electricity Price ($/MWh) Natural Gas Price

($/MMBtu)

f(Pe ,Pg)

Seasonals in Futures Prices: Nymex Henry Hub

Futures

Energy Asset Valuation and Risk Management

• Real-option approach for valuing energy assets – a foundation for

asset securitization

10/11/2013 Fisher Center for Real Estate & Urban Economics 18

At a certain time, price, and generation level, What is the best decision?

Ramp-up? Ramp-down? Keep the same generation?

Which strategy gives more value?

Generation (MW)

Time

Spark Spread ($/MWh)

Ramp-up

Ramp-down

Conclusions

• REFM is already up and running.

– Successfully hired REFM Lab Director, Paulo Issler, Ph.D.

– Completed short-term and long term planning objectives.

– Completed proposal for lab cluster design.

• Data sets are in place as analytical tools: working to verify all

contractual obligations for access.

• Research papers are in progress:

– “Risk Monitoring and the Industrial Organization of the U.S. Residential

Mortgage Origination Market,” Richard Stanton, Johan Walden, and

Nancy Wallace.

– “Energy Efficiency and Commercial-Mortgage Valuation,” Dwight Jaffee,

Richard Stanton, and Nancy Wallace.

– “The Myth of the Constant Quality Home: A New Unbiased House Price

Index,” Anna Amirdjanova, Richard Stanton, and Nancy Wallace.

10/11/2013 Fisher Center for Real Estate & Urban Economics 19