re: otter tail power company resource plan filing update

TRANSCRIPT

January 3, 2008 Dr. Burl W. Haar Executive Secretary Minnesota Public Utilities Commission 350 Metro Square Building 121 7th Place East St. Paul, MN 55101-2147 RE: Otter Tail Power Company Resource Plan Filing Update Docket No. E017/RP-05-968 Dear Dr. Haar: Otter Tail Corporation, dba Otter Tail Power Company, hereby submits via electronic means to the Commission both proprietary and public versions of updated information on Otter Tail’s 2006 – 2020 resource plan filing in the docket noted above. The updated information and analysis is being provided as a result of the change in participation in the proposed Big Stone Unit II project and recent legislative changes in renewable energy and conservation requirements. A copy of the public version has been provided to all other parties on the official service list. Questions can be addressed to me at 218-739-829 or via email at [email protected]. Sincerely, /s/ Bryan D. Morlock Bryan D. Morlock, P.E. Manager, Resource Planning c: Service List Bruce Gerhardson Mark Bring

STATE OF MINNESOTA ) )

COUNTY OF OTTER TAIL )

AFFIDAVIT OF SERVICE Re: In the Matter of Otter Tail Power Company’s 2006 – 2020 Resource Plan

MPUC Docket No. E017/RP-05-968

Bryan D. Morlock, being first duly sworn, deposes and says that on the 3rd day of January, 2008, he will serve the attached filing in the above-referenced matter:

X by electronic delivery to the Minnesota Public Utilities Commission and to the Minnesota Department of Commerce

X by depositing in the United States Mail at the City of Fergus Falls, a true

and correct copy thereof, properly enveloped with postage prepaid to all other parties on the distribution list

by personal service

by facsimile transmission followed by first class mail

by Overnight mail (MPUC and DOC)

by delivery service

to all persons at the addresses indicated below or on the attached lists. /s/ Bryan D. Morlock Bryan D. Morlock Subscribed and sworn to before me this 3rd day of January, 2008. /s/ Nancy D. Tollerson Notary Public My Commission Expires January 31, 2010

Dr. Burl W. Haar Executive Secretary MN Public Utilities Commission 121 7th Place East, Suite 350 St. Paul, MN 55101-2147 Sharon Ferguson MN Department of Commerce 85 7th Place East, Suite 500 St. Paul, MN 55101-2198 Julia Anderson MN Office of Attorney General 1400 BRM Tower 445 Minnesota Street St. Paul, MN 55101-2130 Curt Nelson OAG-RUD 900 BRM Tower 445 Minnesota Street St. Paul, MN 55101-2130 Michele Beck Great River Energy 17845 East Highway 10 P.O. Box 800 Elk River, MN 55330-0800 Elizabeth Goodpaster Minnesota Center for Envrionmental Advocacy 26 E. Exchange St., Suite 206 St. Paul, MN 55101 Shalini Gupta Izaak Walton League of American Suite 202 1619 Dayton Avenue St. Paul, MN 55104

William Harrington Excelsior Energy Inc. Suite 305 11100 Wayzata Boulevard Minnetonka, MN 55305 Jeffrey C. Paulsen Jeffrey C. Paulson & Associates, Ltd. Suite 325 7301 Ohms Lane Edina, MN 55439 Robert H. Schulte Schulte Associates LLC 9072 Palmetto Driver Eden Prairie, MN 55347 Matthew J. Schuerger, P.E. Energy Systems Consulting Services, LLC P.O. Box 16129 St. Paul, MN 55116

Service List Docket E017/RP-05-968

BEFORE THE MINNESOTA PUBLIC UTILITIES COMMISSION

LeRoy Koppendrayer Chair David C. Boyd Commissioner Marshall Johnson Commissioner Thomas W. Pugh Commissioner Phyllis A. Reha Commissioner In the Matter of Otter Tail Power DOCKET NO. E-017/RP-05-968 Company’s 2006 – 2020 Resource Plan

OTTER TAIL POWER COMPANY SUPPLEMENTAL INFORMATION AND ANALYSIS RESULTS ON ITS RESOURCE PLAN

PROCEDURAL HISTORY

On June 30, 2005, Otter Tail Corporation, dba Otter Tail Power Company (Otter Tail or the

Company), filed its proposed Resource Plan covering the period 2006 – 2020, pursuant to

Minnesota Statutes §216B.2422 and Minnesota Rule Chapter 7843.

On August 9, 2006, the Commission issued its ORDER DEFERRING CONSIDERATION OF

OTP’S RESOURCE PLAN, DIRECTING UPDATED INFORMATION, ALLOWING

COMMENT, FINDING GOOD FAITH REO EFFORTS AND DIRECTING NEXT

RESOURCE PLAN FILING. In this Order the Commission deferred consideration of whether to

approve, reject or modify the Company’s proposed Resource Plan. The Commission also

required Otter Tail to submit supplemental information based on modeling re-runs, using updated

cost figures for the Big Stone II project and starting from the modeling adjustments included in

the Company’s May 1, 2006 reply comments. The Commission also indicated that the Company

should file its next resource plan before or simultaneous with the rate case it plans to file in 2007.

On October 26, 2006, the Commission issued its ORDER DENYING RECONSIDERATION, in

response to a petition filed by the Izaak Walton League of American-Midwest Office, Fresh

Energy, the Union of Concerned Scientists, and the Minnesota Center for Environmental

Advocacy (the Joint Intervenors).

Also on October 26, 2006 Otter Tail Power submitted supplemental information, responding to

requirements in the Commission’s August 9, 2006 ORDER.

PUBLIC DOCUMENT – TRADE SECRET DATA HAS BEEN EXCISED

On November 15, 2006, the Department of Commerce (Department) and the Joint Intervenors

each filed supplemental comments in response to the Company’s October 26 filing.

On November 29, 2006, Otter Tail filed reply comments.

The Commission met to consider the matter on January 25, 2007 to consider this matter and on

February 20, 2007 issued its ORDER POSTPONING DECISION ON MERITS, EXTENDING

FILING DATE, AND AMENDING PRIOR ORDER. In this Order the Commission postponed

its final decision until the Commission considers Docket No. E-017 et al./CN-05-619 on its

merits. The Commission also extended the date for the Company to file its next Integrated

Resource Plan to April 1, 2008 and required Otter Tail to file its energy and peak demand forecast

with the Department of Commerce by July 1, 2007. The Commission’s August 9, 2006 ORDER

was amended to approve the wind portion of the Company’s proposed Resource Plan, thereby

allowing the Company’s RFP process for up to 160 MW of wind generation to go forward.

INTRODUCTION

The Minnesota legislature passed two key energy bills during the 2007 session, aimed at

increasing the usage of renewable energy and reducing energy requirements by increasing

conservation efforts.

On September 17, 2007 Big Stone II project officials announced that Great River Energy (GRE)

had chosen to withdraw from the project due to a number of factors unique to GRE, including the

future loss of load and the presence of other resources being developed and/or acquired by GRE.

The announcement also stated that Southern Minnesota Municipal Power Agency (SMMPA)

would not be participating as an equity owner due to ongoing litigation with SMMPA’s largest

member. Absent new participants, the change in project participation would likely result in a

reduced project size and thus experience a likely increase in capital costs on a per kW basis.

The decision was made to update the resource plan analysis to determine if the Big Stone II

project is still an economic resource within the context of the resource plan. The majority of this

filing is a report on the updated analysis and the results, as well as providing information on the

incorporation and impacts of the legislative changes.

Updated Planning Process

Otter Tail used the same planning process and planning software, IRP-Manager, which was used

for the original resource plan development and updated capacity expansion analysis, most

recently submitted in October 2006. The database from the previously updated plan served as the

starting point. Where new data was available, Otter Tail incorporated the information into the

analysis. The goal or objective of the planning model is to reduce total revenue requirements.

The following topics identify data changes that were made in the model.

Load Forecast

Otter Tail submitted a new load forecast to the Department of Commerce (Department) by July 1,

2007 as required by the Commission’s February 20, 2007 ORDER in this docket. Following the

reporting of the new load forecast, Otter Tail was informed that it would be serving a new North

Dakota based ethanol plant with an estimated peak demand of 14.5 MW1. This new load was

added to the load forecast, and incorporated into the model.

Manitoba Hydro Long-Term Proposal

Otter Tail had previously received a long-term 20-year capacity and energy proposal from

Manitoba Hydro in August 2006. Manitoba Hydro was contacted and verbally verified that the

100 MW was still available. The original proposal was included in the analysis, although the

pricing was no longer valid. In this updated analysis, Otter Tail did include consideration of

some of the contingency provisions of the proposal, which had previously not been included. The

Manitoba Hydro proposal was not selected in the capacity expansion modeling. Subsequent to

the completion of the analysis, a letter was received from Manitoba Hydro stating that the 100

MW contained in the proposal was no longer available.

Fuel Prices

Otter Tail updated two fuel forecasts within the model. For natural gas prices Otter Tail used the

2007 Annual Energy Outlook forecast developed by the Energy Information Administration

1 Since the completion of the analysis, Otter Tail has been informed that the peak demand is likely to be closer to 22 MW. The updated analysis does not consider the additional increased load.

(EIA) and released in February 2007. The EIA forecasts have been historically low. A number

of studies over time have documented the tendency of the EIA forecasts to understate natural gas

prices. One of the most recent was a study by the Ernest Orlando Lawrence Berkeley National

Laboratory (LBNL) which compared the forecast to the NYMEX futures prices. The latest study

results2 from LBNL indicated that the EIA Annual Energy Outlook 2007 was understating the

price of natural gas by an average of $0.73/MBTU over the 72-month NYMEX strip. The EIA

forecast was adjusted by this amount, and also for basis differential between the Henry Hub

location of the EIA forecast and a Minnesota natural gas delivery location. Otter Tail

benchmarked the resultant adjusted forecast against the Fall 2007 Gas Reference Case forecast

developed by Global Energy Decisions with reasonable results.

The coal price forecast for the proposed Big Stone II project was updated using information from

a recent Hills & Associates Powder River Basin study. The forecast includes a delivered freight

forecast, fuel surcharges, railcar lease, railcar maintenance, and sales tax.

Demand-side Alternatives

In all previous analysis in this docket the IRP-Manager model has been allowed to evaluate and

select the demand-side alternatives. The 2007 Legislature passed the Next Generation Act of

2007. With the passage of this Act, MN Statute §216B.241 Subd 1c was modified to require each

individual utility to have an annual energy savings goal equivalent to 1.5% of gross annual retail

energy sales to retail customers in the utility’s Minnesota service territory by 2010. The savings

goal is to be calculated based on the most recent three-year weather normalized average sales

data. Based on the prior analysis it was clear that the IRP-Manager model would not select

enough demand-side alternatives to comply with the goal. Otter Tail has been involved in

discussions with the Department on the implementation of this goal and the possible means and

methods for compliance. That process is still ongoing.

In lieu of modeling demand-side alternatives for this updated analysis, the demand-side savings

goal was assumed to be met, and the required energy savings were treated as a model input. The

demand-side savings curves from a prior CIP filing were scaled upward so that the required

2 Memo from Mark Bolinger and Ryan Wiser, Lawrence Berkeley National Laboratory, dated December 6, 2006.

demand-side savings goal was achieved. Since the compliance costs have not yet been

determined, costs to attain these savings were not included in the model.

Otter Tail has been involved in ongoing discussions with South Dakota Public Utilities

Commission staff on conservation efforts in that jurisdiction and has filed a conservation plan to

be implemented there. The Company is also anticipating resuming direct consideration programs

in its North Dakota service territory as well. To account for these estimated savings, the demand-

side savings curves were also escalated to include savings of approximately 0.5% of annual retail

sales in those jurisdictions.

Tables I and II below show the estimated demand-side savings impacts to retail sales for the

Minnesota and non-Minnesota jurisdictions.

Table I Estimated Minnesota Savings Due to Conservation

(All Units in GWh) Year MN Retail Sales

Forecast MN Annual

Conservation MN Cumulative

Conservation Net MN Retail Sales Forecast

2007 2,107.8 13.532 13.532 2,094.3 2008 2,204.9 14.074 27.607 2,177.3 2009 2,308.3 14.654 42.260 2,266.1 2010 2,349.5 32.716 74.976 2,274.5 2011 2,391.0 33.637 108.613 2,282.3 2012 2,440.2 34.189 142.801 2,297.4 2013 2,475.8 34.378 177.179 2,298.6 2014 2,518.6 34.532 211.711 2,306.9 2015 2,562.2 34.688 246.399 2,315.8 2016 2,613.9 34.814 281.213 2,332.6 2017 2,650.8 35.019 316.232 2,334.6 2018 2,695.8 35.191 351.423 2,344.4 2019 2,740.9 35.368 386.791 2,354.1 2020 2,795.0 35.510 422.302 2,372.7

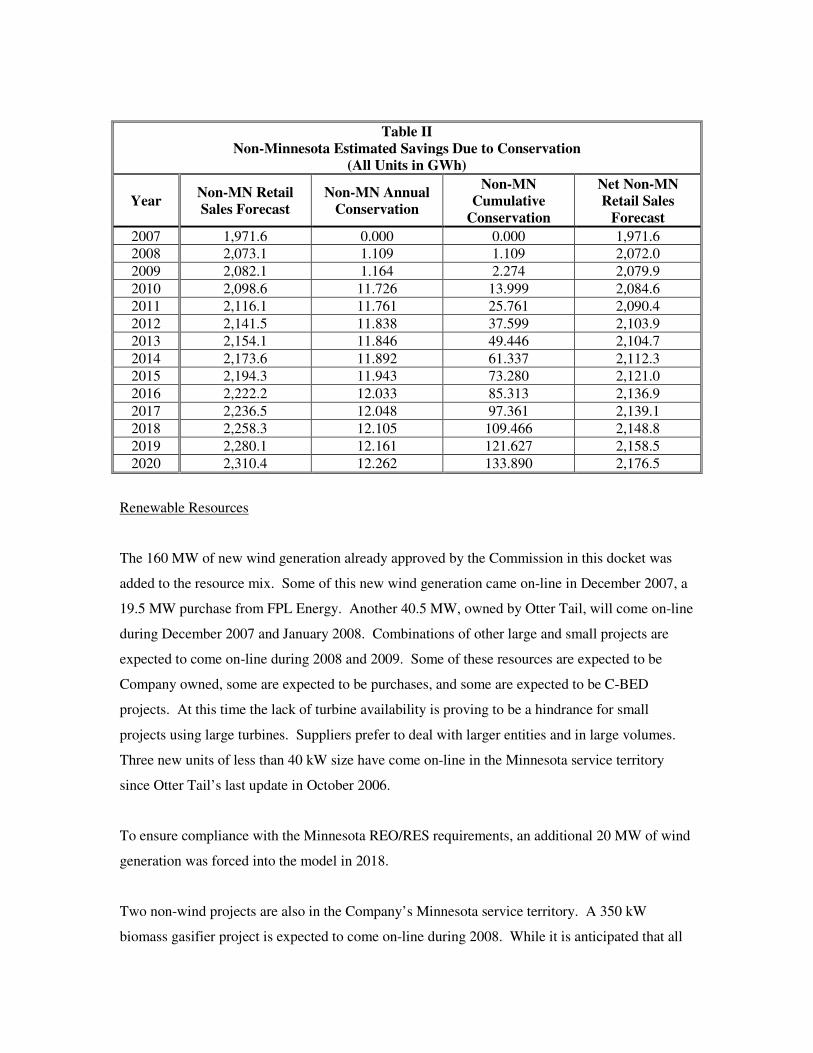

Table II Non-Minnesota Estimated Savings Due to Conservation

(All Units in GWh)

Year Non-MN Retail Sales Forecast

Non-MN Annual Conservation

Non-MN Cumulative

Conservation

Net Non-MN Retail Sales

Forecast 2007 1,971.6 0.000 0.000 1,971.6 2008 2,073.1 1.109 1.109 2,072.0 2009 2,082.1 1.164 2.274 2,079.9 2010 2,098.6 11.726 13.999 2,084.6 2011 2,116.1 11.761 25.761 2,090.4 2012 2,141.5 11.838 37.599 2,103.9 2013 2,154.1 11.846 49.446 2,104.7 2014 2,173.6 11.892 61.337 2,112.3 2015 2,194.3 11.943 73.280 2,121.0 2016 2,222.2 12.033 85.313 2,136.9 2017 2,236.5 12.048 97.361 2,139.1 2018 2,258.3 12.105 109.466 2,148.8 2019 2,280.1 12.161 121.627 2,158.5 2020 2,310.4 12.262 133.890 2,176.5

Renewable Resources

The 160 MW of new wind generation already approved by the Commission in this docket was

added to the resource mix. Some of this new wind generation came on-line in December 2007, a

19.5 MW purchase from FPL Energy. Another 40.5 MW, owned by Otter Tail, will come on-line

during December 2007 and January 2008. Combinations of other large and small projects are

expected to come on-line during 2008 and 2009. Some of these resources are expected to be

Company owned, some are expected to be purchases, and some are expected to be C-BED

projects. At this time the lack of turbine availability is proving to be a hindrance for small

projects using large turbines. Suppliers prefer to deal with larger entities and in large volumes.

Three new units of less than 40 kW size have come on-line in the Minnesota service territory

since Otter Tail’s last update in October 2006.

To ensure compliance with the Minnesota REO/RES requirements, an additional 20 MW of wind

generation was forced into the model in 2018.

Two non-wind projects are also in the Company’s Minnesota service territory. A 350 kW

biomass gasifier project is expected to come on-line during 2008. While it is anticipated that all

of this biomass energy will be used on-site, it will free up some wind generation currently being

used on-site for delivery to Otter Tail. An expansion at an existing municipal solid waste facility

(MSW) is currently undergoing engineering and evaluation. The project could be up to 4 MW in

size, but development is uncertain at this time. This project has not been included in the analysis

due to the high degree of uncertainty of development.

In this updated analysis the direct cost of wind generation was not changed, but the $4.50/MWh

integration cost identified in the Minnesota study was incorporated into the model. The wind

pricing in the model is currently representative of the costs of ownership of wind generation by

Otter Tail, but a little below the current pricing being received from wind developers. A

transmission cost of $200/kW was included in the wind analysis. Previous analysis had not

included any consideration of the transmission cost. Additional wind generation was made

available to the model.

A key assumption in the analysis is the Federal Production Tax Credit (PTC). The PTC is a

major component of the economics of wind development. The modeling assumed that the PTC

was available for new wind generation developed through 2013, but not beyond that point.

Discussions with the legislative staffs of area members of Congress, wind developers, and

presentations at wind conferences provide a variety of opinions on the future of the PTC. Many

believe that there will be some extension of the PTC, but that it will be limited and long-term

availability is doubtful. Indications are that implementation of a federal renewable resource

portfolio standard will eliminate the PTC.

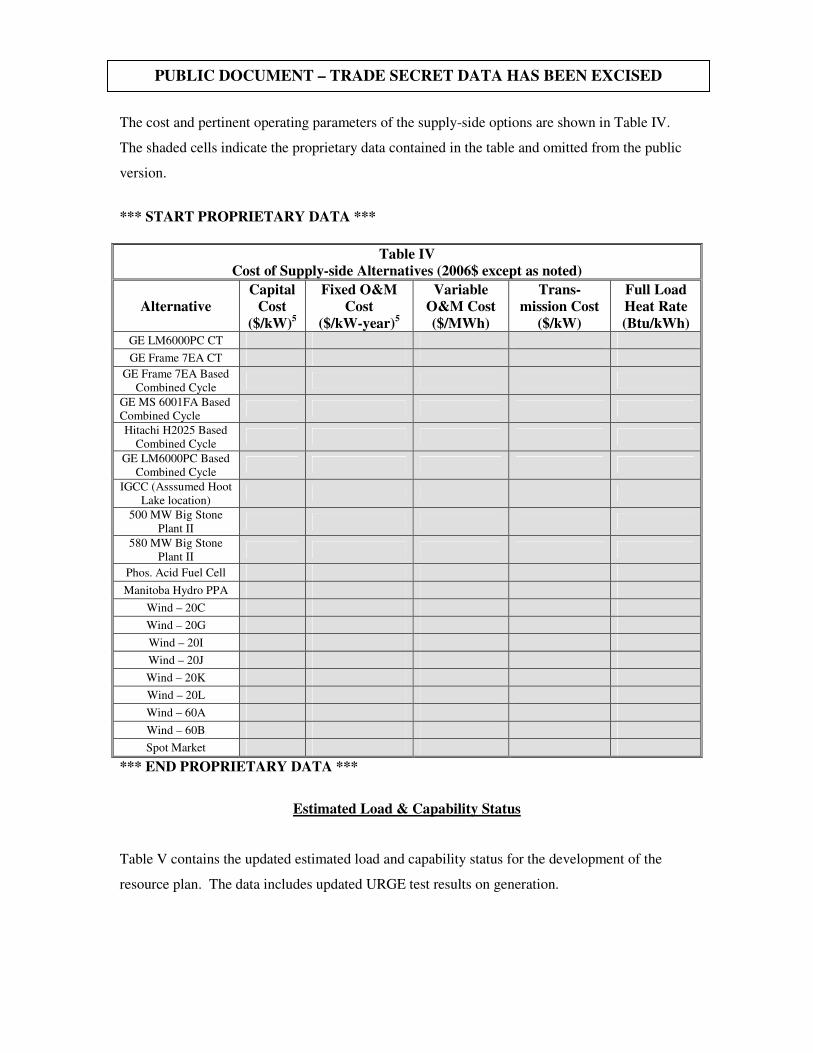

Supply-side Alternatives

In 2002 Otter Tail hired Black & Veatch to develop costs and operating parameters for a number

of supply-side alternatives. Following the Commission’s July 20, 2006 hearing, Otter Tail hired

Black & Veatch to complete an update to some of the supply-side alternatives, incorporating

information learned about commodity and labor costs in the BSPII process.

The cost of the Big Stone II proposal was revised to reflect potential smaller project sizes.

Updated costs for project sizes of 500 MW and 580 MW were developed by the project team and

used in the resource planning process. The transmission portion of the project does not change

with a smaller plant, but the same transmission additions with a smaller plant project do result in

a higher cost per kW.

Otter Tail used the updated Black & Veatch information, the 2006 Gas Turbine World handbook,

information from General Electric, data from Company owned facilities, and publicly available

information to develop updated supply-side alternatives. Table III identifies the resources made

available to the model, the number of units available, winter and summer season ratings, and the

years that the alternative was available to the model.

Table III Supply-Side Alternatives Evaluated With IRP-Manager

Resource Type # of Units Available

Winter Season Rating (MW)

Summer Season Rating (MW)

Years Available

GE LM6000PC CT 3 48.4 42.5 2011 - 2020 GE Frame 7EA CT 2 95.3 74.8 2011 - 2020 Combined Cycle

Based on GE Frame 7EA

1 141.3 116.7 2013 - 2020

Combined Cycle Based on GE MS

6001FA 1 115.1 95.1 2013 - 2020

Combined Cycle Based on Hitachi

H2025 1 88.1 72.8 2013 – 2020

Combined Cycle Based on GE LM6000PC

1 59.3 44.9 2013 - 2020

IGCC 2 88.1 72.8 2013 – 2020

Big Stone Plant II Up to 170 MW Base

Rating

Up to 172 MW Winter Rating

Up to 161.8 MW Summer Rating 2013

Phosphoric Acid Fuel Cell 2 20 MW 20 MW 2013 – 2020

Manitoba Hydro Purchase 1 100 MW 100 MW 2011 - 2020

Manitoba Hydro Purchase 1 50 MW 50 MW 2011 – 2020

Manitoba Hydro Purchase 1 30 MW 30 MW 2011 - 2020

Wind 6 20 MW3 20 MW 2011 - 2020 Wind 2 60 MW 60 MW 2011 - 2020

Spot Market4 1 150/165 MW 150/165 MW 2011

3 Nameplate rating. Expected accreditation level for peak months is 20% winter and 15% summer. 4 The spot market capacity was only available in 2011, and only covered a two-year period, through 2012.

The cost and pertinent operating parameters of the supply-side options are shown in Table IV.

The shaded cells indicate the proprietary data contained in the table and omitted from the public

version.

*** START PROPRIETARY DATA ***

Table IV Cost of Supply-side Alternatives (2006$ except as noted)

Alternative Capital

Cost ($/kW)5

Fixed O&M Cost

($/kW-year)5

Variable O&M Cost ($/MWh)

Trans-mission Cost

($/kW)

Full Load Heat Rate (Btu/kWh)

GE LM6000PC CT GE Frame 7EA CT

GE Frame 7EA Based Combined Cycle

GE MS 6001FA Based Combined Cycle Hitachi H2025 Based

Combined Cycle GE LM6000PC Based

Combined Cycle IGCC (Asssumed Hoot

Lake location) 500 MW Big Stone

Plant II 580 MW Big Stone

Plant II Phos. Acid Fuel Cell Manitoba Hydro PPA

Wind – 20C Wind – 20G Wind – 20I Wind – 20J Wind – 20K Wind – 20L Wind – 60A Wind – 60B Spot Market

*** END PROPRIETARY DATA ***

Estimated Load & Capability Status

Table V contains the updated estimated load and capability status for the development of the

resource plan. The data includes updated URGE test results on generation.

PUBLIC DOCUMENT – TRADE SECRET DATA HAS BEEN EXCISED

Table V ����������� � � � � � �� �� � � �� � � � �� �� � � � �� � � � � � ����� �� � �� � ��� �� � � � � � �� �� �� �� � � � ��� �

Updated for 2007 URGE Results

For Demonstration Purposes Only - Do Not Use as Final OTP Load & Capability �! � � " # � �! � � " # � �! � � " # � �! � � " # � �! � � " # � �! � � " # � �! � � " # �# $ � � �� % $ & �� �

$ � $ � �� �' ( � $ � " � $ ' �% ! ���) � ����� ����� ���* � ���* � ���+ � ���+ � ��, �� ��, �� ��, , � ��, , � ��, �� ��, �� ��, - �

������������������� � �� �� � � � � � � � ��� � � � � � � � � � ��� � �� � � � �� � � �� � � � � �� �� � �� �

�� � ��� ������ � � � � ����� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

����������� �� ���

�������� �� �� � � � � � � � ��� � � � � � � � � � ��� � �� � � � �� � � �� � � � � �� �� � �� �

���� ����� �� ���

�������� �� � �� � � � � � � � � � � � � � � � � � ��� � ��� � � �� � � �� � � � � �� �� � �� �

� �� ��� � � � � �������

� �� ����� �� �� �� �� �� �� �� �� �� �� �� �� ��

� �� ����������� �� ��� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

����������� ���� �

�������� �� ���� � � � �� � � � � � � �� � �� � ��� � �� � � ��� � �� � � � � � � �� � � � �� �

���� ����� ���� �

�������� �� � � � � � � � �� � � � � � � � �� � ��� � �� � � ��� � �� � � � � � � �� � � � �� �

��� �! ���� �� ��! �� �� � � ��� � �� � � �� � � � � �� � �� � � � �� � �� � � � �� � �� � � � �� � �� � � � �� � �� �

� �� � �� � � � � ������� �� ���� ��� � �� � � �� � ��� ��� ��� ��� �� �� �� �� �� �� ��

� �� � ���������� �� ��� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

�� ���� �� �� �" ���� � � � �� � � �� � �� � � �� � � � ��� � � � ��� � � � � ��� � � � � ��� � � � � ���

��� �� ���� # ��� �� ��" ��! � � ��� � ��� � ��� � ��� � � � � � � � � � � � � � � � � � � �� � � �� � � � � � � � � � ��� � �� �

� �� ���� �� ��� �� ��" ��! � � �� � � � � � � �� � ��� � � � �� � � � � � �� � � � � � � � � � � ���

�� � � �� ���� ���� �� �� �� �� � ���� � � � ��� ��� � ��� � �� � � � � � �� �� � �� � � � �� � � �� ��� �� � � � �� �� ���� �

�

�! � � " # � �! � � " # � �! � � " # � �! � � " # � �! � � " # � �! � � " # � �! � � " # �# $ � � �� % $ & �� � $ � $ � �� �' ( �

$ � " � $ ' �% ! � ��, - � ��, . � ��, . � ��, / � ��, / � ��, ) � ��, ) � ��, �� ��, �� ��, * � ��, * � ��, + � ��, + � �����

������������������� � � � �� � ��� � � � � �� �� � � � � ��� �� � �� � �� � �� � � � � ��

�� � ��� ������ � � � � ����� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

����������� �� ���

������� � � � �� � ��� � � � � �� �� � � � � ��� �� � �� � �� � �� � � � � ��

���� ����� �� ���

������� � � � �� � ��� � � � � � � �� � �� � ��� ��� �� �� � �� � �� � � ��

� �� ��� � � � � �������

� �� ����� �� �� �� �� �� �� �� �� �� �� �� �� ��

� �� ����������� �� ��� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

����������� ���� �

������� � � � � � � � � �� � �� � �� � � � �� � �� � � �� �� � � �� � �� � ���

���� ����� ���� �

������� � � � � � � � � �� � � � � �� � �� �� � ��� � �� � � � � �� � � � ���

��� �! ���� �� ��! �� �� � � � �� � �� � � � �� � �� � � � �� � �� � � � �� � �� � �� �� ��� � �� �� ��� � �� �� ��� �

� �� � �� � � � � ������� �� ���� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

� �� � ���������� �� ��� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

�� ���� �� �� �" ���� � � � � � � ��� � � � � ��� � � � � ��� � � � � ��� �� � ��� � �� � ��� � �� � ��� �

��� �� ���� # ��� �� ��" ��! � � �� � � �� � � �� � � ��� � ��� � �� � � �� � � �� � � �� � � � � � � � � � � � � � � � � � � � ��

� �� ���� �� ��� �� ��" ��! � � �� � � � � � � � �� � �� � � ��� � � � � � � � � � �� � �� � ���� � � �� � ��� � � �� � � �� � �

�� � � �� ���� ���� �� �� �� �� � �� � � � ��� � � ���� � ���� � ��� � � ���� � ��� �� �� �� �� � � �� � � � �� � � � �� �� � �� � �� �� � �

5 The capital cost is based on the winter rating of the resource, except for the spot market purchases.

Planning Scenarios

The intent of the updated analysis was to consider six scenarios. The scenarios included:

• 580 MW BSPII alternative, no externalities or CO2 tax

• 580 MW BSPII alternative, high externality values, no CO2 tax

• 580 MW BSPII alternative, no externalities, $9/ton CO2 tax

• 500 MW BSPII alternative, no externalities or CO2 tax

• 500 MW BSPII alternative, high externality values, no CO2 tax

• 500 MW BSPII alternative, no externalities, $9/ton CO2 tax

The $9/ton CO2 tax scenarios would assume a tax on all CO2 from all resources, effective in

2013. The regional average CO2 emissions/MWh was used for energy from unknown sources.

For the CO2 tax scenarios, the price of energy from the MISO wholesale market and from the

Manitoba Hydro proposal was increased by the CO2 tax impact for natural gas-fired generation.

This assumption was made based on the report of the Independent Market Monitor for the

Midwest ISO which states: “…natural gas prices were the primary driver of energy prices.”6

Analysis Results

The 500 MW Big Stone II proposal, with the CO2 tax, was considered to be the highest cost

scenario with respect to the Big Stone II proposal. At 500 MW, the price impact from a smaller

project would be greater than the 580 MW proposal, and the CO2 tax implications on all

resources would be greater than the impact of the high environmental externality values.

The optimization run selected 170 MW of the Big Stone II proposal, additional wind resources,

and natural gas-fired peaking generation. The results of the scenario are shown in Table VI. As a

result of the Big Stone II proposal still being an economic choice at the 500 MW plant size, even

when considering a $9/ton CO2 tax, the other five scenarios were not completed.

6 Page 7, “2006 State of the Market Report,” David B. Patton, PhD, Potomac Economics, Midwest ISO Independent Market Monitor.

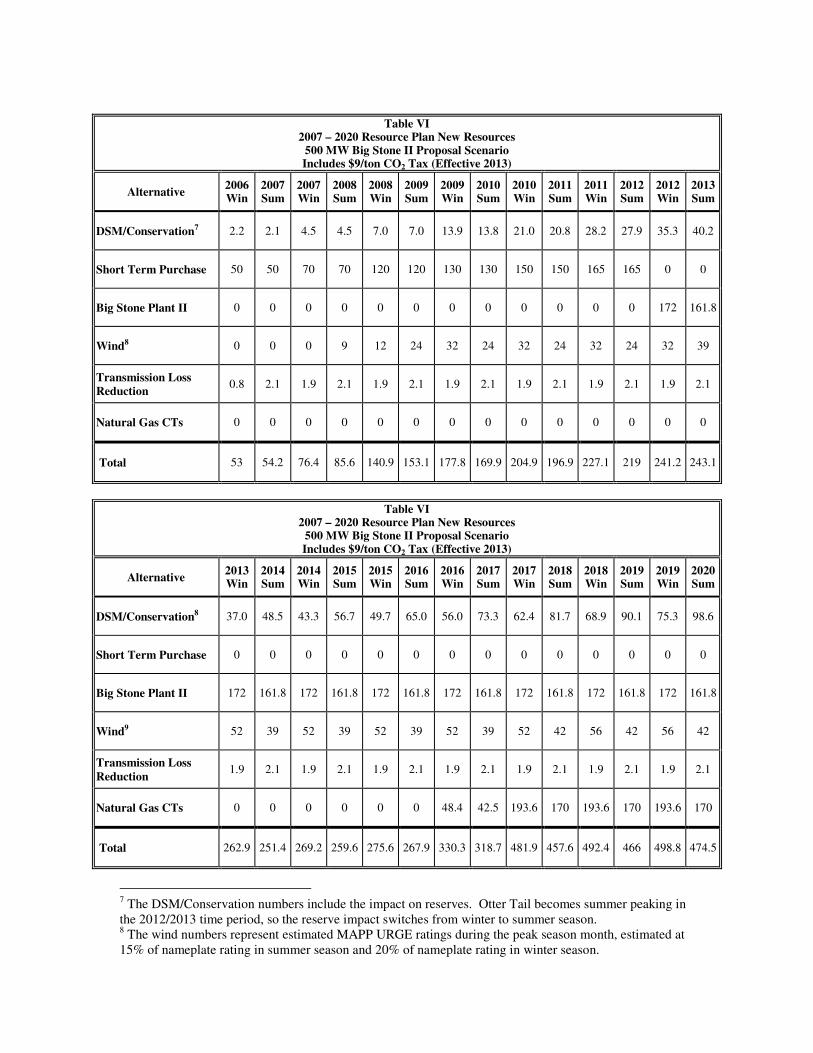

Table VI

2007 – 2020 Resource Plan New Resources 500 MW Big Stone II Proposal Scenario Includes $9/ton CO2 Tax (Effective 2013)

Alternative 2006 Win

2007 Sum

2007 Win

2008 Sum

2008 Win

2009 Sum

2009 Win

2010 Sum

2010 Win

2011 Sum

2011 Win

2012 Sum

2012 Win

2013 Sum

DSM/Conservation7 2.2 2.1 4.5 4.5 7.0 7.0 13.9 13.8 21.0 20.8 28.2 27.9 35.3 40.2

Short Term Purchase 50 50 70 70 120 120 130 130 150 150 165 165 0 0

Big Stone Plant II 0 0 0 0 0 0 0 0 0 0 0 0 172 161.8

Wind8 0 0 0 9 12 24 32 24 32 24 32 24 32 39

Transmission Loss Reduction 0.8 2.1 1.9 2.1 1.9 2.1 1.9 2.1 1.9 2.1 1.9 2.1 1.9 2.1

Natural Gas CTs 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Total 53 54.2 76.4 85.6 140.9 153.1 177.8 169.9 204.9 196.9 227.1 219 241.2 243.1

Table VI

2007 – 2020 Resource Plan New Resources 500 MW Big Stone II Proposal Scenario Includes $9/ton CO2 Tax (Effective 2013)

Alternative 2013 Win

2014 Sum

2014 Win

2015 Sum

2015 Win

2016 Sum

2016 Win

2017 Sum

2017 Win

2018 Sum

2018 Win

2019 Sum

2019 Win

2020 Sum

DSM/Conservation8 37.0 48.5 43.3 56.7 49.7 65.0 56.0 73.3 62.4 81.7 68.9 90.1 75.3 98.6

Short Term Purchase 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Big Stone Plant II 172 161.8 172 161.8 172 161.8 172 161.8 172 161.8 172 161.8 172 161.8

Wind9 52 39 52 39 52 39 52 39 52 42 56 42 56 42

Transmission Loss Reduction 1.9 2.1 1.9 2.1 1.9 2.1 1.9 2.1 1.9 2.1 1.9 2.1 1.9 2.1

Natural Gas CTs 0 0 0 0 0 0 48.4 42.5 193.6 170 193.6 170 193.6 170

Total 262.9 251.4 269.2 259.6 275.6 267.9 330.3 318.7 481.9 457.6 492.4 466 498.8 474.5

7 The DSM/Conservation numbers include the impact on reserves. Otter Tail becomes summer peaking in the 2012/2013 time period, so the reserve impact switches from winter to summer season. 8 The wind numbers represent estimated MAPP URGE ratings during the peak season month, estimated at 15% of nameplate rating in summer season and 20% of nameplate rating in winter season.

The updated resource plan has some significant changes from the previous resource plan. The 50

MW Manitoba Hydro purchase was replaced by an additional 50 MW of the Big Stone II

proposal. Incorporating the Manitoba Hydro proposal contingencies made the proposal more

expensive than additional Big Stone II capacity. Since the updated analysis was completed,

Manitoba Hydro has notified Otter Tail that the capacity and energy in the proposal is no longer

available.

The increased conservation had a significant impact later in the planning period. In total, the

resource plan now has 81 MW less baseload resources. Whereas the previous plan included 81

MW of IGCC in 2018 when the Hoot Lake coal-fired units are retired in the plan, the updated

resource plan does not include the IGCC option. Instead, all new capacity selected by the model

at that point is natural gas-fired peaking.

The analysis also selected an additional 100 MW of wind generation for reserve requirements in

2013, after it had selected the Big Stone II proposal. This 100 MW is clearly dependent upon the

availability of the federal PTC, as the model did not select any additional wind without the PTC

being available.

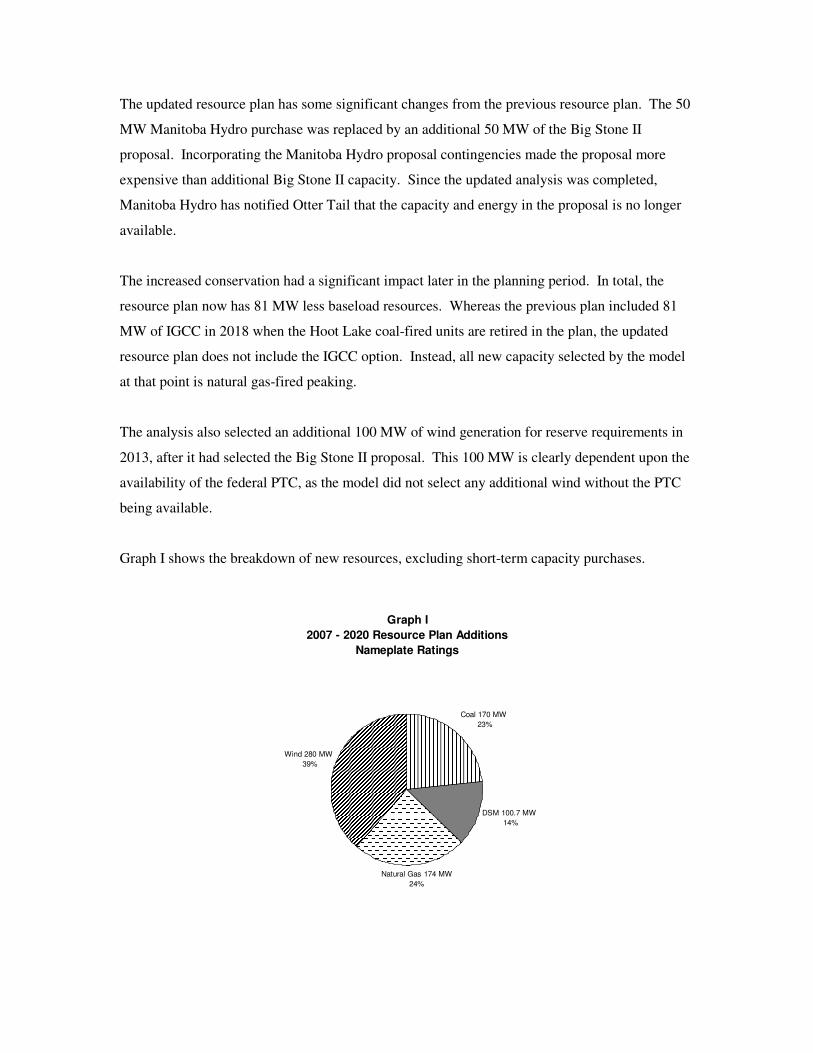

Graph I shows the breakdown of new resources, excluding short-term capacity purchases.

Graph I2007 - 2020 Resource Plan Additions

Nameplate Ratings

Coal 170 MW 23%

DSM 100.7 MW 14%

Natural Gas 174 MW 24%

Wind 280 MW 39%

Graph II shows the net change to the resource mix by 2020 with the resource plan, including the retirement of the Hoot Lake #2 and #3 units.

Graph II2007 - 2020 Net Resource Mix Changes

Includes RetirementsNameplate Ratings

Coal 25 MW 4%

DSM 100.7 MW 17%

Natural Gas 174 MW 30%

Wind 280 MW 49%

Sensitivity Analysis

Two additional sensitivity scenarios were completed after the initial analysis. The first sensitivity

scenario included a capital price sensitivity relative to the Big Stone Unit II proposal. The capital

cost was increased by 10% above the current estimate. The resource plan did not change. The

second sensitivity scenario was to combine the high environmental externality values with the

$9/ton CO2 tax value. The CO2 tax value was used in place of the CO2 externality value and

applied to all fossil-fueled resources without regard for location. Again, the resource plan as

identified by the model did not change.

CO2 Emissions

The resource plan impacts result in a reduction in CO2 emissions for serving retail load. The CO2

reductions, both in total annual emissions and in CO2 emissions/kWh result from the significant

increase in wind generation, improvements in the efficiency of existing generation, and the

efficiency improvement. Additionally, the total annual CO2 emissions are being reduced by the

increase in conservation. Graph III shows the annual CO2 emissions associated with the energy

to serve total Company retail load.

Graph III2007 - 2020 Annual Tons of CO2 for Retail Load

4,000,000

4,100,000

4,200,000

4,300,000

4,400,000

4,500,000

4,600,000

4,700,000

4,800,000

4,900,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Annual Tons CO2

Graph IV shows the CO2 emissions/kWh over the 2007 – 2020 time period, including the

consideration of conservation activities.

Graph IV2007 - 2020 CO2 lbs/kWh for Retail Load, Including Conservation

Includes CO2 for Unknown Purchases

0

0.5

1

1.5

2

2.5

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Year

lbs/

kWh

CO2 lbs/kWh

Renewable Energy Objective/Standard Compliance

Otter Tail is subject to the Minnesota Renewable Energy Objective/Standard requirements

contained in MN Statutes §216B.1691, and to a North Dakota Renewable Energy Objective of

10% of retail sales by 2015. The South Dakota portion of the service territory does not have any

requirements at this time, but efforts are underway by the South Dakota legislature to implement

a renewable energy objective in that state. Current expectations are that it will be somewhat

similar to the North Dakota requirement.

The resource plan, as identified in this update filing, has more than enough resources to meet the

requirements of all three state jurisdictions. If resource implementation continues as currently

expected Otter Tail will be in the position of having surplus renewable energy credits. The

Commission has already approved 160 MW of new wind resources in this docket. 19.5 MW of

new wind generation being received under a PPA from the Langdon Wind Energy Center came

on-line in December 2007. Another 40.5 MW of Company owned wind generation at the same

site is coming on-line in December 2007 and January 2008. A number of customer-owned wind

generating facilities, ranging in size from 1.8 kW to approximately 2.5 MW each have recently

come on-line or are expected to come on-line in 2008 or 2009. It is possible that some of the

proposed customer-owned projects may not reach a successful conclusion, but some of them have

a very high degree of probability that they will be completed. Otter Tail is working with these

entities to the extent possible to help these projects along.

Otter Tail is currently in negotiations with developers on other large wind generation

developments, likely to come on-line in the 2008 – 2010 time period. These additions, combined

with others should substantially complete or exceed the 160 MW of approved wind additions.

Otter Tail was the first utility fully enrolled in M-RETS. The Company’s renewable energy

resources have been tracked beginning with July 2007 data, with the exception of a few very

small units. The cost per renewable energy credit for small facilities, or facilities where Otter

Tail receives only a fraction of the energy produced, can be as much as 100 times the cost for a

large facility. Otter Tail is working with the M-RETS system to find a solution for the small

generators.

Table VII shows Otter Tail’s expected renewable energy availability and requirements over the

2007 – 2020 time period.

Table VII

2007 – 2020 Renewable Energy Objective/Standard Compliance

Year 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Wind 68 272 612 612 612 612 952 952 952 952 952 1021 1021 1021

Hydro 25 25 25 25 25 25 25 25 25 25 25 25 25 25

Tot

al A

nnua

l R

enew

able

E

nerg

y (G

Wh)

Biomass 2 2 2 2 2 2 2 2 2 2 2 2 2 2

REO Requirement 0 0 0 0 0 0 0 0 222 223 224 225 226 228

Wind Energy Used for

Compliance 0 0 0 0 0 0 0 0 220 222 222 223 224 226

Nor

th D

akot

a (G

Wh)

Biomass Energy Used

for Compliance

0 0 0 0 0 0 0 0 2 2 2 2 2 2

REO/RES Requirement 21 22 23 159 159 275 276 277 279 398 398 401 403 478

Wind Energy Used for

Compliance 0 0 0 134 135 251 251 252 254 373 374 376 378 453

Min

neso

ta (G

Wh)

Hydro Energy Used for

Compliance 21 22 23 25 25 25 25 25 25 25 25 25 25 25

Wind 68 272 612 478 477 362 701 700 478 358 357 422 419 342

Hydro 4 3 2 0 0 0 0 0 0 0 0 0 0 0

Biomass 2 2 2 2 2 2 2 2 0 0 0 0 0 0

Surp

lus R

enew

able

Ene

rgy

afte

r R

EO

/RE

S C

ompl

ianc

e (G

Wh)

Total 73 277 616 480 479 363 703 702 478 358 357 422 419 342

1 Biomass is ND eligible only. 2 OTP-owned hydro is MN eligible only. 3 MN REO is 1% through 2009. MN RES is 7% in 2010, 12% in 2012, 17% in 2016, 20% in 2020 and 25% in 2025. 4 ND REO is 10% in 2015.

Process Going Forward

Otter Tail originally filed its request for resource plan approval on June 30, 2005. Since that

initial filing, this is the third resource plan update the Company has filed. The updates have been

filed for a variety of reasons, including (1) to address modeling concerns by the Department, (2)

to address cost revisions of the Big Stone Unit II estimate, and now (3) to address new legislation

regarding renewable resources and conservation, and a possible change in the Big Stone Unit II

project size and participants.

Some of the parties to this docket have expressed concern that if the Commission should approve

the Company’s resource plan in the instant docket, somehow the Commission will have set

precedence or prejudged the Big Stone Unit II project transmission Certificate of Need docket

(E017 et al/CN-05-619). Accordingly, the Commission made a previous determination that the

Otter Tail resource plan decision would be rendered the same day as the decision in the

Certificate of Need docket. The Certificate of Need docket is now expected to be decided in

April 2008. Otter Tail recommends the Commission continue with its previous decision to decide

on the Otter Tail resource plan at the same hearing.

There is a timing conflict, as the Company’s next resource plan filing is expected to be filed April

1, 2008 in accordance with the Commission’s ORDER dated February 20, 2007. It would be

illogical and a waste of valuable resources of all parties involved having two Otter Tail resource

planning dockets open simultaneously. Further, Otter Tail cannot begin analysis on the next

resource plan filing until the Commission has rendered a decision in the current docket. Otter

Tail therefore requests the Commission to extend the date of the Company’s next resource plan

filing to September 2, 2008. Over the course of the past year, including this updated filing, the

Company has provided updated load forecast information, REO/RES compliance status and

plans, incorporated the new conservation requirements in Minnesota and conservation plans in

North Dakota and South Dakota, and incorporated a $9/ton CO2 tax in its latest analysis. Even

though the current docket has been open for 2 ½ years, the updated information has kept current

with the new legislative requirements for renewable energy and conservation. The Commission

can comfortably render a decision in the current docket because of the updated information.

Finally, Otter Tail is in the process of migrating to new Strategist long-term planning software.

The latest software version will allow the modeling of Otter Tail as two separate jurisdictions, a

Minnesota jurisdiction and a non-Minnesota jurisdiction. Each jurisdiction will be able to have

its own renewable energy requirements, consideration of environmental externalities, potential

future carbon taxes, and other issues. Currently Otter Tail is in the situation of having Minnesota

and North Dakota laws that are in direct conflict with each other. The new Strategist model will

allow the Company to simultaneously develop resource plans that comply with the requirements

of both areas without violating the laws of any state. A September 2, 2008 filing date will

provide the time necessary to develop and benchmark the new database and ensure the

development of robust plans.

Summary

Otter Tail has conducted updated analysis due to the recent changes in Big Stone Unit II proposal

sizing and ownership, updated cost and load forecast information, and new legislative

requirements in Minnesota. The Company’s resource plan has been modified accordingly,

reflecting an increase in the amount of renewable energy and conservation, and a reduction in the

amount of baseload generation.

Otter Tail respectfully requests the Commission:

• Approve the Company’s updated resource plan filing at the same time a decision is

rendered in the Big Stone Unit II proposal transmission Certificate of Need, Docket No.

E017 et al/CN-05-619; and

• Extend the filing date of the Company’s next resource plan filing to September 2, 2008.

Any questions regarding this submittal can be directed to me by telephone at 218-739-8269 or via

email at [email protected].

Sincerely,

/s/ Bryan D. Morlock

Bryan D. Morlock, P.E.

Manager, Resource Planning