re-examining the modelling of yields in a volatile market by ben burston

DESCRIPTION

Re-examining the modelling of yields in a volatile market by Ben Burston DTZ, 125 Old Broad Street, London, EC2N 2BQ Tel: +44 (0)20 3296 3011 Email: [email protected] Kostis Papadopoulos DTZ, 125 Old Broad Street, London, EC2N 2BQ - PowerPoint PPT PresentationTRANSCRIPT

Page 1

Re-examining the modelling of yields in a volatile market by

Ben BurstonDTZ, 125 Old Broad Street, London, EC2N 2BQ

Tel: +44 (0)20 3296 3011 Email: [email protected]

Kostis PapadopoulosDTZ, 125 Old Broad Street, London, EC2N 2BQ

Tel: +44 (0)20 3296 2329 Email: [email protected]

& Tony McGough

DTZ, 125 Old Broad Street, London, EC2N 2BQTel: +44 (0)20 3296 2314 Email: [email protected]

Paper presented at the 17th European real Estate Society Conference,Milan, Italy – June 23rd 26th 2010.Draft paper: Not to be quoted without permission from the authors.

Page 2

Introduction

• Methodology

• Model

• Impact of global volatility

• Implications of modelling output

Page 3

Introduction

• Previous model (Hicks & McGough 2005) provided a framework for our yield analysis

• Previous equation looks at impact of• Rental expectations• Bond prices• Fixed risk premia via constant

• Present model• Incorporates transaction volumes• Money supply

Methodology

Page 4

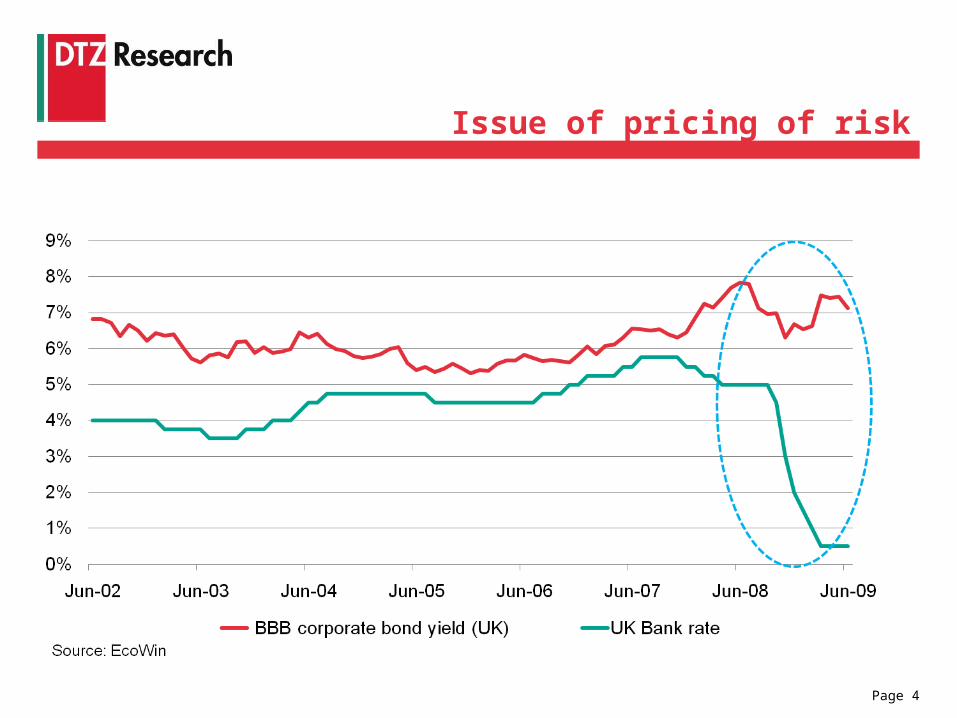

Issue of pricing of risk

Page 5

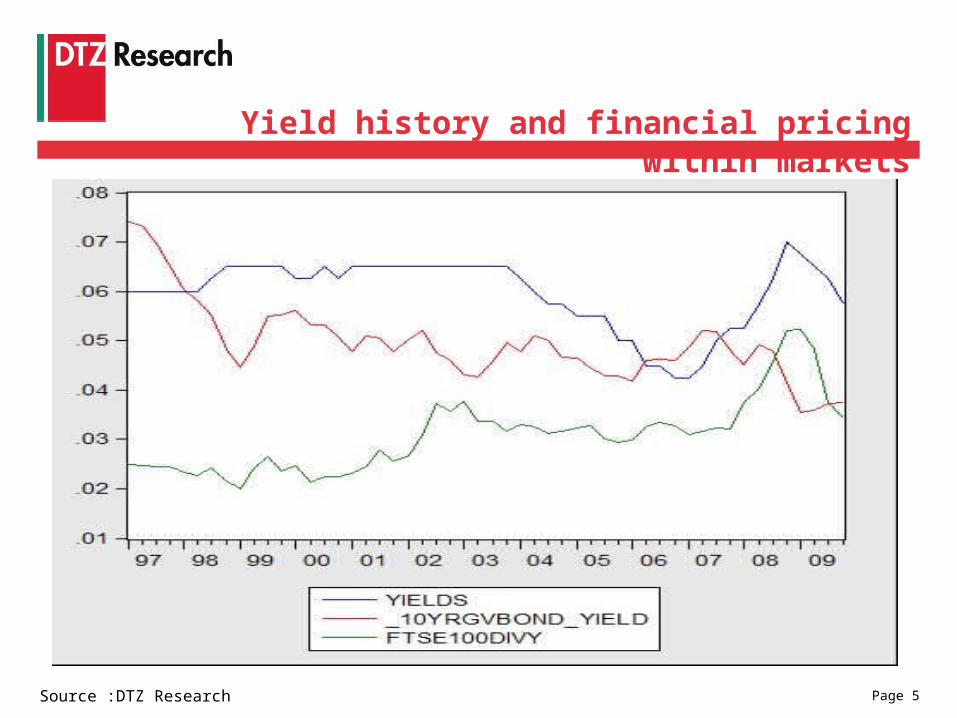

Yield history and financial pricing within markets

Source :DTZ Research

Page 6Source :DTZ Research

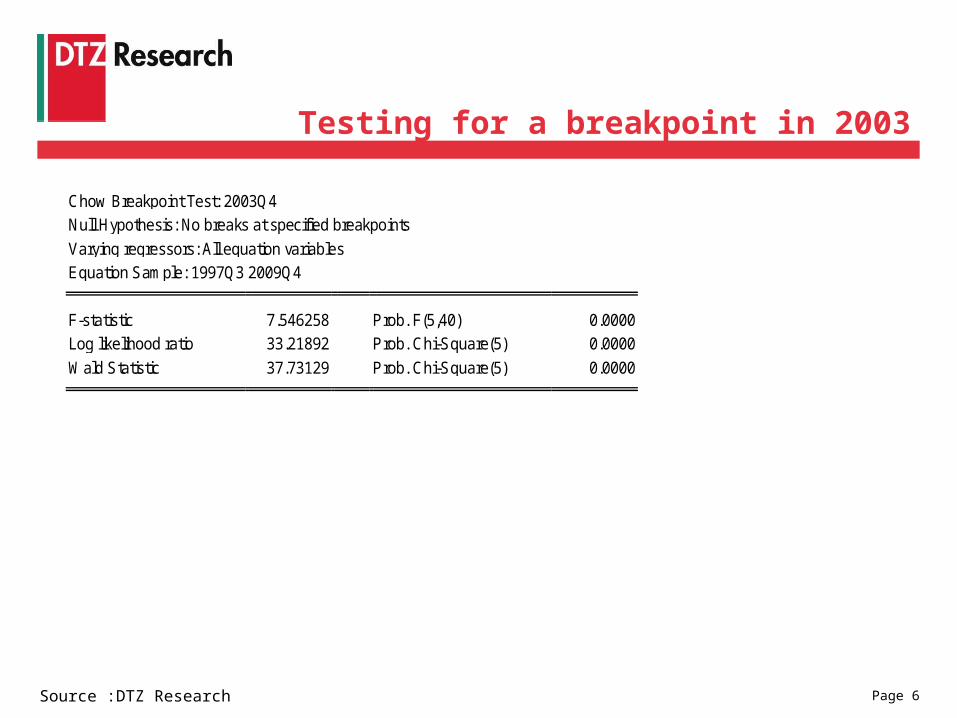

Testing for a breakpoint in 2003

Chow Breakpoint Test: 2003Q4

Null Hypothesis: No breaks at specified breakpoints

Varying regressors: All equation variables

Equation Sample: 1997Q3 2009Q4

F-statistic 7.546258 Prob. F(5,40) 0.0000

Log likelihood ratio 33.21892 Prob. Chi-Square(5) 0.0000

Wald Statistic 37.73129 Prob. Chi-Square(5) 0.0000

Page 7

Data used

• Variables

RR = real rentsBond = 10 year government bondDivy = Dividend YieldTrvn = transaction volume numbersRMoney = Real money supply

• Time Series Quarterly 1997 2009• London Office rents

Page 8

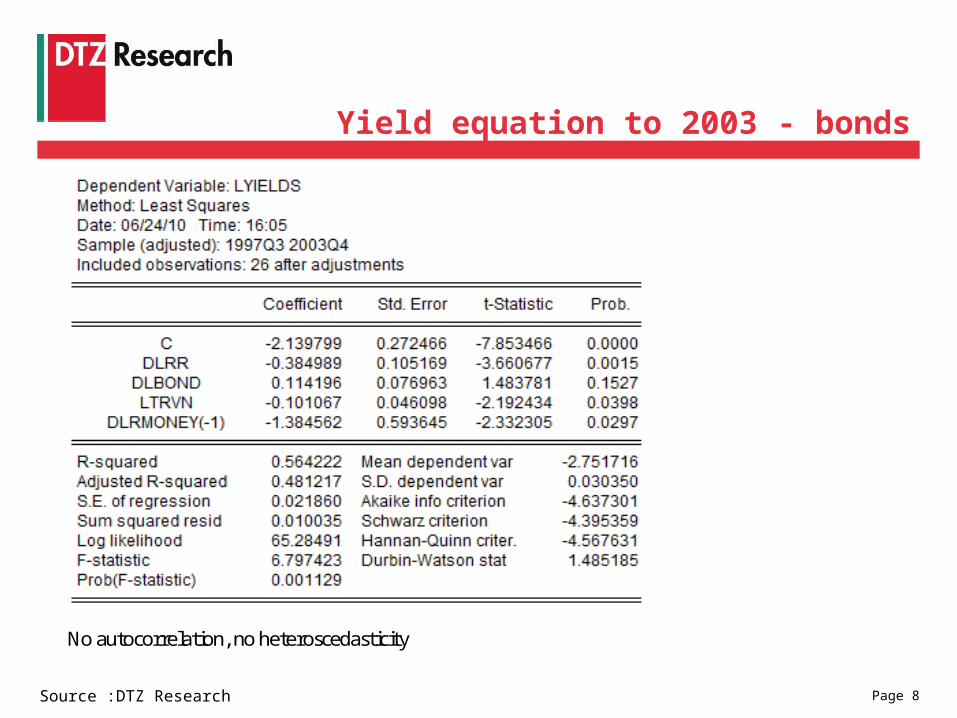

Yield equation to 2003 - bonds

Source :DTZ Research

No autocorrelation, no heteroscedasticity

Page 9Source :DTZ Research

Yield equation to 2003 - bonds

Page 10Source :DTZ Research

No autocorrelation, no heteroscedasticity

Yield equation to 2003 – dividend yields

Page 11Source :DTZ Research

Full model to 2009 Q4 - bonds

Page 12Source :DTZ Research

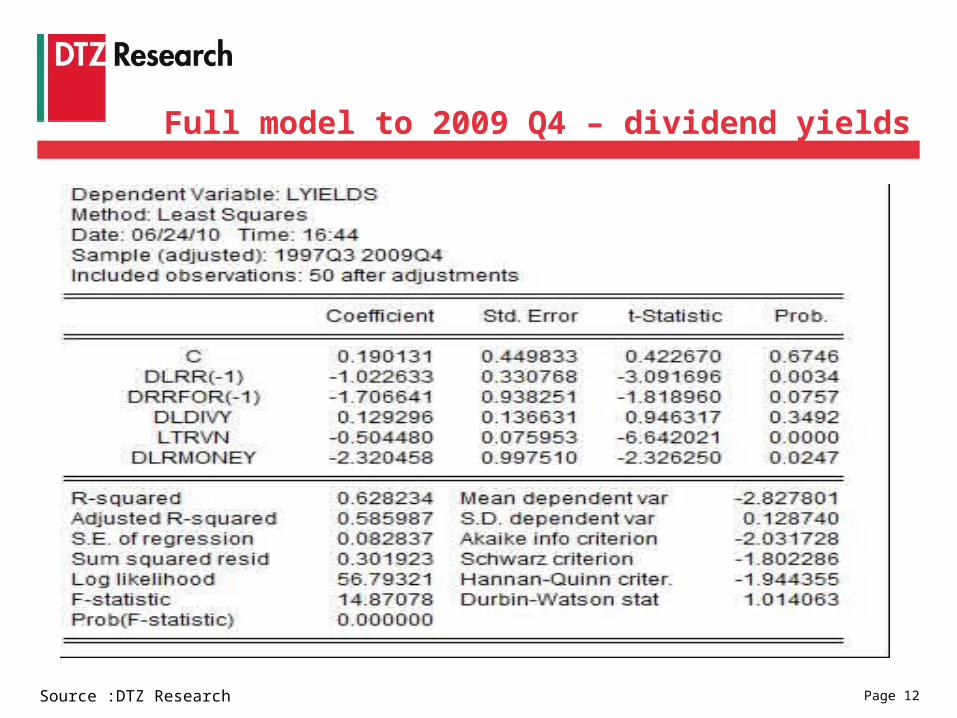

Full model to 2009 Q4 – dividend yields

Page 13Source :DTZ Research

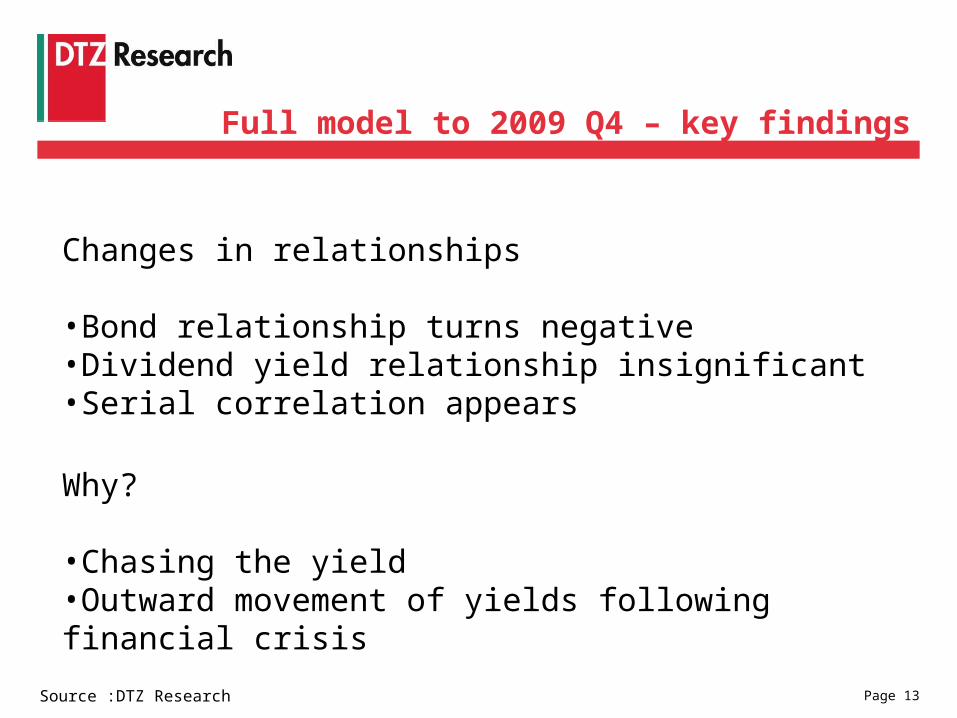

Full model to 2009 Q4 – key findings

Changes in relationships

•Bond relationship turns negative •Dividend yield relationship insignificant•Serial correlation appears

Why?

•Chasing the yield•Outward movement of yields following financial crisis

Page 14Source :DTZ Research

Full model to 2009 Q4 – solutions

Need to incorporate other variables into this analysis

•In particular risk measures and time varying premia

Page 15

Risk pricing from near zero to 400 bps

0%

1%

2%

3%

4%

5%

Jan-03 Oct-03 Jul-04 Apr-05 Jan-06 Oct-06 Jul-07 Apr-08 Jan-09 Oct-09

A AA AAA BBB

UK corporate benchmarks - 10 year yield spread over 10 year gilts

Source: DTZ Research, EcoWin

Page 16Source :DTZ Research

Full model to 2009 Q4

Page 17Source :DTZ Research

Full model to 2009 Q4

Page 18

Conclusions

Source: DTZ Research

London (City)

London (West End)MadridParis

Sydney

FrankfurtNew YorkShanghai

Tokyo

•Structural break found in yield relationships using old methodology

•Previous relationships have changed in the current environment

•More sophisticated modelling of risk needed to take into account more volatile risk markets