re-designing the onboarding customer journey of a retail bank

TRANSCRIPT

- Research project & methodology -

Re-designing the Onboarding Customer Journey

of a Retail Bank

2

Background

0

3

The Onboarding challenge

Onboarding is definitely one of the biggest challenges for a bank within the customer

lifecycle:

at the outset of the relationship, insight on the new customer is still to be built up

almost entirely

switching is still quite easy: "strings" entailed by owning products yet to come and

relationship still "shallow"

Making customers tick even before getting to know them, is not the easiest of the tasks.

Yet, as they say, you never get a second chance to make a good first impression: Onboarding shapes customers’ first impression of a bank and has the potential to influence the long-term

success of the relationship

4

Opportunities and pitfalls of Onboarding

Together with trouble shooting, the onboarding phase (account opening and the 3 up to 6

months that follow) is the moment-of-truth with the greatest impact on advocacy, share

of wallet and ultimately on loyalty:

onboarding can turn to be a sort of "grace" period, a moment when cross-

selling potential is at its highest: it has been estimated that 75% of all cross-

selling takes place in the first few months of new customer acquisition

but unfortunately attrition rate is as well: new customers are the least satisfied

and the most likely to leave; indeed, studies show that customers are three times

more likely to show attrition during the first ninety days of opening a new account*

*Source: J.D. Power & Associates 2013 U.S. Retail Banking Satisfaction StudySM

5

Beyond Acquisition

Provided that churn is avoided, the challenge of avoiding the "great decoupling"

between acquisition and cross-selling is at stake.

Plenty of evidence is available that

"fully engaged" customers – as opposed as merely "satisfied" – show much

higher repurchase rates

the lack of a consistent and meaningful value proposition through all the

relevant touchpoints highly hinders the likability of customers to convert their

purchasing intentions into actual purchases

The challenge is twofold then:

- What makes customers tick? What has the power of making a new customer "engaged"? - What is the experience to be delivered through all the relevant touchpoints during the

onboarding phase?

6

Our approach

2

7

The bank certainly know the % of prospects dropping out after the first contact, of customers becoming inactive or leaving the bank after opening the account, and even

the touchpoints involved and consulted before deciding not to go ahead with a purchase.

What the bank doesn't know is WHY, i.e. - what the customers' expectations were at any given touchpoint

- and how the experience provided by the bank failed to deliver vs. these expectations

In-depth qualitative research is therefore needed to map an ideal onboarding customer journey, in order to make sure for the bank to deliver a consistently relevant experience

through all touchpoints and moments of truth, by tapping into the customers' needs, expectations and pain points

Our approach In-depth qualitative research

8

Ethnography - more than group discussions - certainty is the most promising approach:

research in behavioural economics has shown how relying on respondents'

recollections often leads to misleading results

not only because memories deteriorate over time and become less reliable

but above all because whereas we make our decisions mostly driven by Kahneman's

"System 1" – emotions and feelings, we tend to justify our behaviours in terms of

"System 2" – rationality.

Our approach Beware of recollections!/1

9

Therefore it is crucial to

gather customers' feelings and feedback as close as possible to the actual

individual experience they have had

get real: no vague tales but slices of life full of details regarding touchpoints and

processes the customer was involved into

o whenever possible (when it doesn't cause interferences with the customers'

experience), direct observation by Episteme researchers is granted

o in other cases, self-ethnography by respondents is required

Our approach Beware of recollections!/2

What form of observation is to be preferred depends on the touchpoint(s) especially investigated in each interview

10

Due to practical considerations, it is not feasible to shadow a panel of customers

during their whole onboarding period and strictly monitor what happens, however, the

methodology is inspired exactly by this philosophy.

The ideal customer journey is an abstraction rooted in the actual experience of a

number of customers, each of whom

1. is interviewed on their overall expectations and approach to banking, in order to

attribute each individual to the relevant archetypes and persona

2. is especially selected to provide their story and point of view on a specific

moment and experience within the onboarding process, in order to avoid getting

generic recollections devoid of actionability

Our approach Shadowing different people in different touchpoints

In other terms, instead of shadowing a group of people for the whole onboarding period, we get the same accuracy and actionability by shadowing a well varied sample of individuals, each on a

specific moment/touchpoint/experience within the onboarding period.

11

In particular, the sample should include customers

who have just opened the account

who have considered opening the account at the bank's but have eventually decided not to

who have opened the account for a month or so

that are considering a purchasing decision or have just made it or have decided not to

proceed further

customers at the end of what is typically considered as the standard duration of the

onboarding period who have or have not been fully activated

customers at risk of churn (e.g. have filed a complaint) or who have just left the bank

before the end of the standard onboarding period

Our approach Building the sample/1

Customers will be both from the bank's and other players' customer base, in order to discover best practices also coming from the competitive environment

12

Journey mapping has to be done also from the organisational point of view, in several

ways

1. Current onboarding customer journey as delivered by the bank must be used

as a constant reference

2. All relevant quantitative data available from different internal sources (CRM,

contact center, complaint logs, online behaviour) must be analysed

3. The point of view of the sale force must be also integrated to get a precise picture

of how the bank concretely deals with prospects and newly acquired customers

Our approach Integrating the bank's point of view

13

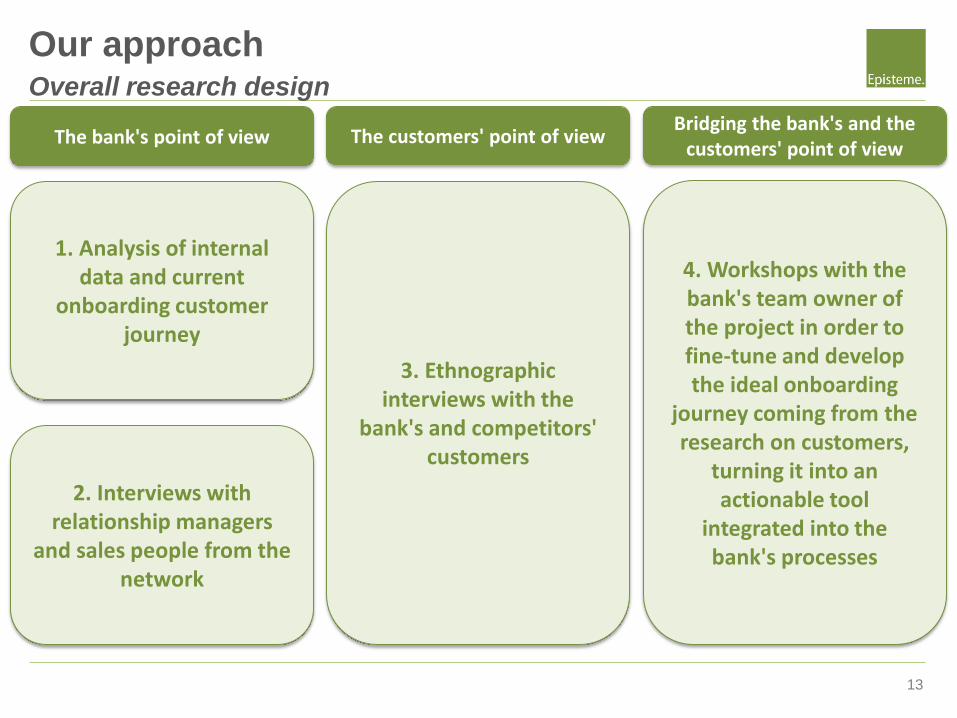

Our approach Overall research design

1. Analysis of internal data and current

onboarding customer journey

The bank's point of view

2. Interviews with relationship managers

and sales people from the network

The customers' point of view

3. Ethnographic interviews with the

bank's and competitors' customers

Bridging the bank's and the customers' point of view

4. Workshops with the bank's team owner of the project in order to fine-tune and develop the ideal onboarding

journey coming from the research on customers,

turning it into an actionable tool

integrated into the bank's processes