r&d tax incentive seminar

TRANSCRIPT

By Ben Youn

Copyright 2015 Quantum Business House

WELCOME to QUANTUM BUSINESS HOUSE

3 hours session

10 minutes tea time

Bathroom & Kitchen

Today’s Speaker

Please network each other

Future Plan

- Business Forum

- Networking Events

- Business Mentoring

Copyright 2015 Quantum Business House

Originally from R&D Tax Concession (change made on July 01, 2011)

45% refundable tax offset for businesses less than $20 million turnover

40% non-refundable tax offset for all other eligible entities.

Administered by AusIndustry (activity part) and the ATO (tax administration)

Copyright 2015 Quantum Business House

Legal authorities:

- Division 355 of Income Tax Assessment Act 1997

- Part III of the Industry Research & Development Act 1986

- The Tax Laws Amendment (Research and Development) Bill 2010 Explanatory Memorandum

Copyright 2015 Quantum Business House

Entities require to register eligible R&D activities with AusIndustry within 10 months after the end date of the financial year. (e.g. April 30 is the due for June 30 entities)

Once approved by the AusIndustry, a registration number will be given to the entity to claim the incentive for the R&D expenditure through tax return.

Copyright 2015 Quantum Business House

Must meet the definition of Core R&D activities

Supporting R&D activities

Self-Assessment and Record Keeping Requirements

Compliance review by AusIndustry

- Request of further evidences

- Monitoring visits

Copyright 2015 Quantum Business House

Core R&D Activities are experimental activities:

1. Whose outcome cannot be known or determined in advance on the basis of current knowledge, information or experience, but can only be determined by applying a systematic progression of work that:

a. is based on principles of established science; and

b. Proceeds from hypothesis to experiment, observation and evaluation, and leads to logical conclusions; and

Copyright 2015 Quantum Business House

2. that are conducted for the purpose of generating new knowledge that include new or improved materials, products, devices, processes and services.

Copyright 2015 Quantum Business House

1. Market research, market testing or market development, or sales promotion

2. Prospecting, exploring or drilling for minerals or petroleum

3. Management studies or efficiency surveys

4. Research in social sciences, arts or humanities

5. Commercial, legal and administrative aspects of patenting, licensing or other activities

Copyright 2015 Quantum Business House

6. Activities associated with complying with statutory requirements or standards.

7. Any activity related to the reproduction of a commercial product or process.

8. Developing, modifying or customising computer software for the dominant purpose of use by entities for their internal administration.

Copyright 2015 Quantum Business House

Activities directly related to core R&D activities:

a. is an activity referred to in the core R&D activities exclusion list; or

b. produces goods or services; orc. is directly related to producing goods or

services;

the activity is a supporting R&D activity only if it is undertaken for the dominant purpose of supporting core R&D activities.

Copyright 2015 Quantum Business House

The prevailing or most influence purpose for conducting an activity

a. the extent to which the activities also achieve commercial or production outcomes in addition to assisting the conduct of the core R&D activities; and

b. The importance of those non-R&D outcomes.

Copyright 2015 Quantum Business House

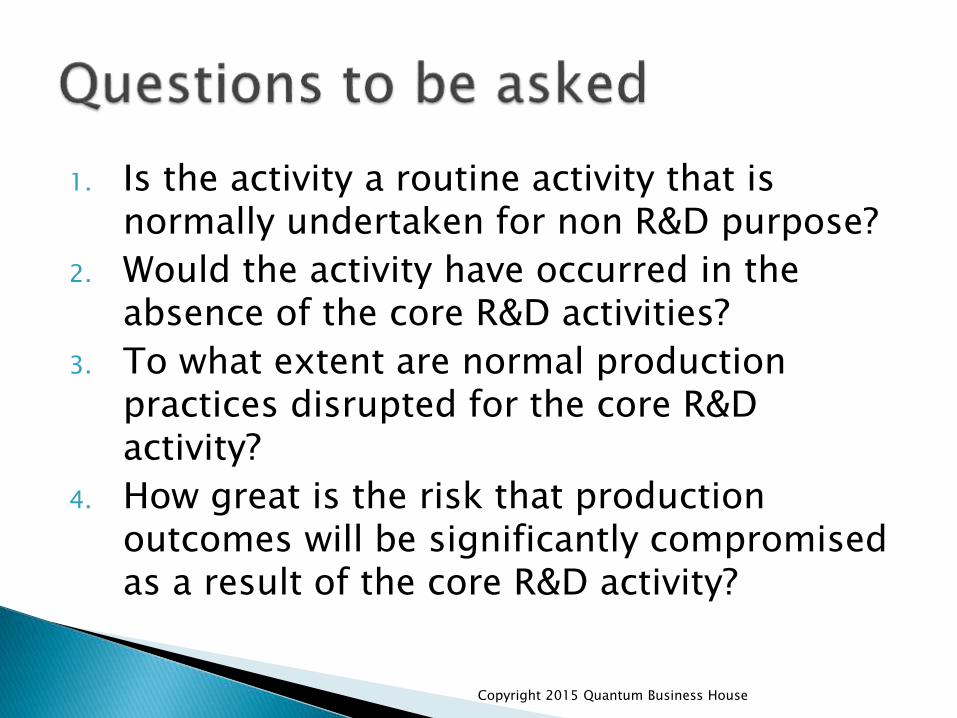

1. Is the activity a routine activity that is normally undertaken for non R&D purpose?

2. Would the activity have occurred in the absence of the core R&D activities?

3. To what extent are normal production practices disrupted for the core R&D activity?

4. How great is the risk that production outcomes will be significantly compromised as a result of the core R&D activity?

Copyright 2015 Quantum Business House

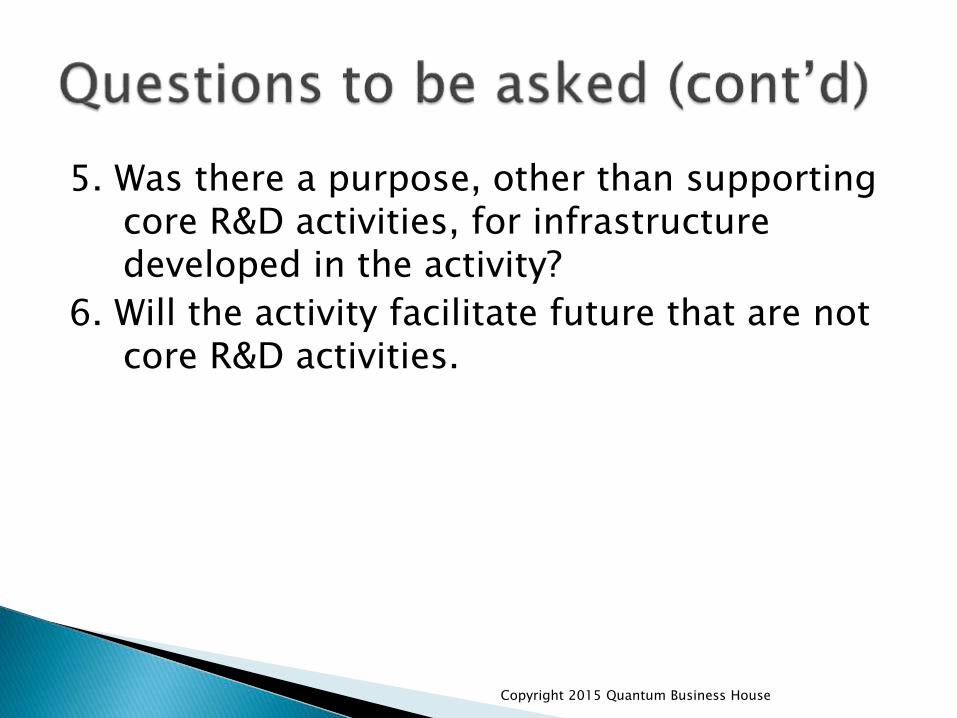

5. Was there a purpose, other than supporting core R&D activities, for infrastructure developed in the activity?

6. Will the activity facilitate future that are not core R&D activities.

Copyright 2015 Quantum Business House

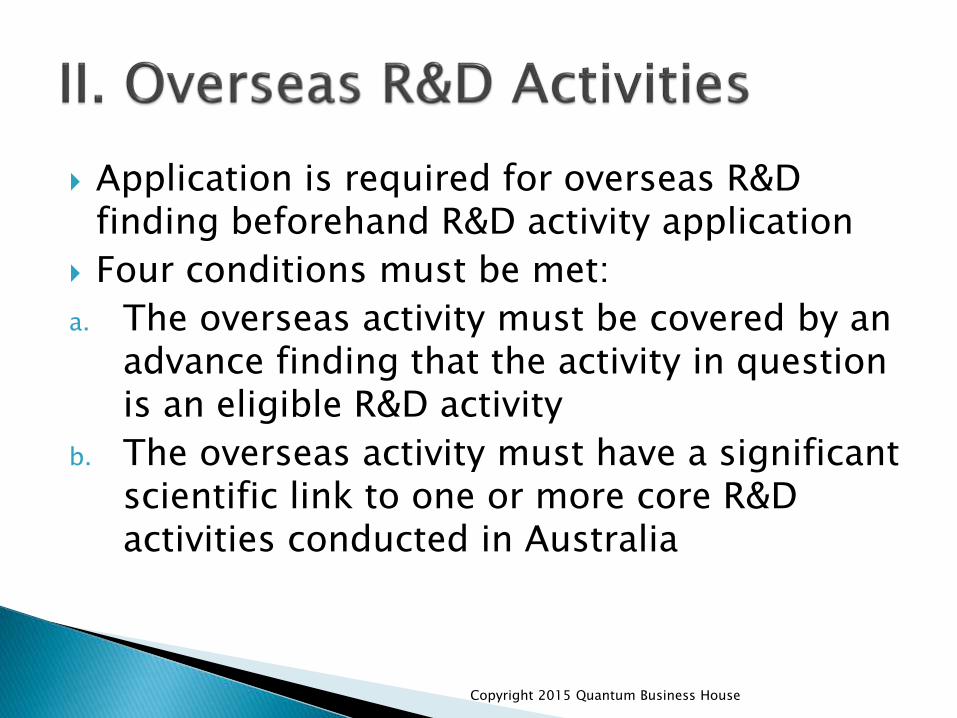

Application is required for overseas R&D finding beforehand R&D activity application

Four conditions must be met:

a. The overseas activity must be covered by an advance finding that the activity in question is an eligible R&D activity

b. The overseas activity must have a significant scientific link to one or more core R&D activities conducted in Australia

Copyright 2015 Quantum Business House

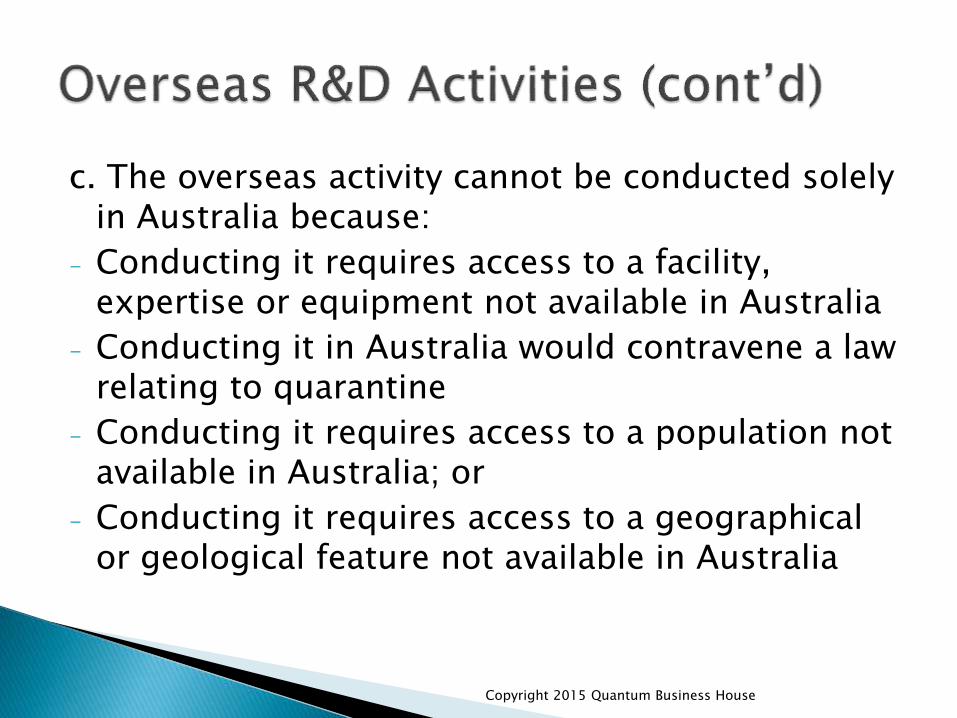

c. The overseas activity cannot be conducted solely in Australia because:

- Conducting it requires access to a facility, expertise or equipment not available in Australia

- Conducting it in Australia would contravene a law relating to quarantine

- Conducting it requires access to a population not available in Australia; or

- Conducting it requires access to a geographical or geological feature not available in Australia

Copyright 2015 Quantum Business House

d. The total amount to be spent in all income years by the company and any other entities on:

- The overseas activities that meet the four conditions; and

- Each other activity conducted wholly or partly outside Australia that has a significant scientific link to Australian core activities.

is less than the total amount to be spent in all income year on:

Copyright 2015 Quantum Business House

- The Australian core activities; and

- The activities conducted within Australia that are supporting R&D activities in relation to the Australian core activities.

Copyright 2015 Quantum Business House

1. Background of the project

2. Preliminary Works

3. Technical Objectives & Risks

4. Commercialisation and Implementation

5. Scope and timeframe

6. Resource allocation

Copyright 2015 Quantum Business House

1. Medical Equipments Manufacturer

2. Software Development Company

Copyright 2015 Quantum Business House

Any Questions?

Copyright 2015 Quantum Business House

Ben Youn: Business Grant Consultant

Address: Level 8, 280 Pitt Street SYDNEY NSW 2000

Phone: (02) 8268 0388

Fax: (02) 8268 0378

www.quantumhouse.com.au

www.australiantaxexperts.com.au

Copyright 2015 Quantum Business House