ray martin *discounted cash flow (dcf) includes net present value (npv) and internal rate of return...

TRANSCRIPT

Ray MartinRay Martin

*Discounted Cash Flow (DCF) includes Net Present Value (NPV) and Internal Rate of Return (IRR).

*Discounted Cash Flow (DCF) includes Net Present Value (NPV) and Internal Rate of Return (IRR).

Discounted Cash Flow* Leads to Better

Financial Decisions Because . . .

IRR is Okay!

Discounted Cash Flow* Leads to Better

Financial Decisions Because . . .

IRR is Okay!

Ray MartinRay Martin

BackgroundBackground Mainstream corporate finance texts cite IRR as being inferior to IRR

for financial decision-making. One professor calls it “IRR bashing.” Framing NPV and IRR as either-or choices . . .

– overstates minor difficulties with IRR;– ignores coexistent difficulties with NPV; and– forces an unnecessary, unproductive choice between the two.

The two measures . . .– consider the time value of money;– are complementary;– are best used together; and– are reconcilable, each with the other and with discounted payback.

In short, IRR is Okay. This presentations compares . . .

– the mainstream view explained in Principles of Corporate Finance (Richard A. Brealey and Stewart C. Myers, 6th edition, Irwin-McGraw-Hill, 2000) to . . .

– an alternative view explained in Internal Rate of Return Revisited.

Mainstream corporate finance texts cite IRR as being inferior to IRR for financial decision-making. One professor calls it “IRR bashing.”

Framing NPV and IRR as either-or choices . . .– overstates minor difficulties with IRR;– ignores coexistent difficulties with NPV; and– forces an unnecessary, unproductive choice between the two.

The two measures . . .– consider the time value of money;– are complementary;– are best used together; and– are reconcilable, each with the other and with discounted payback.

In short, IRR is Okay. This presentations compares . . .

– the mainstream view explained in Principles of Corporate Finance (Richard A. Brealey and Stewart C. Myers, 6th edition, Irwin-McGraw-Hill, 2000) to . . .

– an alternative view explained in Internal Rate of Return Revisited.

Ray MartinRay Martin

Why Net Present Value Leads to Better Investment Decisions than Other Criteria

Principals of Corporate FinanceBrealey and Myers Sixth Edition

Slides by

Matthew Will Chapter 5

©The McGraw-Hill Companies, Inc., 2000The Irwin/McGraw Hill

Ray MartinRay Martin

©The McGraw-Hill Companies, Inc., 2000The Irwin/McGraw Hill

5- 2

Topics Covered

NPV and its Competitors

The Payback Period

The Book Rate of Return

Internal Rate of Return

Capital Rationing

Ray MartinRay Martin

Topics Covered(Brealey & Myers, Chapter 5 Only)

Topics Covered(Brealey & Myers, Chapter 5 Only)

The two measures of DCF are NPV and IRR.The two measures of DCF are NPV and IRR. Net Present Value (NPV) . . . Net Present Value (NPV) . . .

– is complementary to IRR, is complementary to IRR, – has difficulties that are ignored in the mainstream view, has difficulties that are ignored in the mainstream view,

which . . .which . . .– can lead to nonsensical decisions when used alone.can lead to nonsensical decisions when used alone.

Internal Rate of Return (IRR) . . . – is complementary to NPV, – always gives consistent rankings when properly viewed, and– highlights the minor difficulties using NPV only.

Discounted payback period . . .– is easily reconciled with DCF,– is easily incorporated and explained,– considers the time value of money, and– is different from undiscounted payback period which does not.

The two measures of DCF are NPV and IRR.The two measures of DCF are NPV and IRR. Net Present Value (NPV) . . . Net Present Value (NPV) . . .

– is complementary to IRR, is complementary to IRR, – has difficulties that are ignored in the mainstream view, has difficulties that are ignored in the mainstream view,

which . . .which . . .– can lead to nonsensical decisions when used alone.can lead to nonsensical decisions when used alone.

Internal Rate of Return (IRR) . . . – is complementary to NPV, – always gives consistent rankings when properly viewed, and– highlights the minor difficulties using NPV only.

Discounted payback period . . .– is easily reconciled with DCF,– is easily incorporated and explained,– considers the time value of money, and– is different from undiscounted payback period which does not.

Ray MartinRay Martin

© T h e M c G r a w - H i l l C o m p a n i e s , I n c . , 2 0 0 0T h e I r w i n / M c G r a w H i l l

5 - 1 0

I n t e r n a l R a t e o f R e t u r n

E x a m p l e

Y o u c a n p u r c h a s e a t u r b o p o w e r e d m a c h i n e t o o l g a d g e t f o r $ 4 , 0 0 0 . T h ei n v e s t m e n t w i l l g e n e r a t e $ 2 , 0 0 0 a n d $ 4 , 0 0 0 i n c a s h f l o w s f o r t w o y e a r s ,r e s p e c t i v e l y . W h a t i s t h e I R R o n t h i s i n v e s t m e n t ?

0)1(

000,4

)1(

000,2000,4

21

IRRIRRNPV

%08.28IRR

Ray MartinRay Martin

Internal Rate of ReturnB&M Example: Purchase a gadget for $4,000. The investment should generate $2,000 and $4,000 in cash flows in years 1 and 2 respectively. What is the IRR on this investment?

Relevant IRR

Ray MartinRay Martin

© T h e M c G r a w - H i l l C o m p a n i e s , I n c . , 2 0 0 0T h e I r w i n / M c G r a w H i l l

5 - 1 2

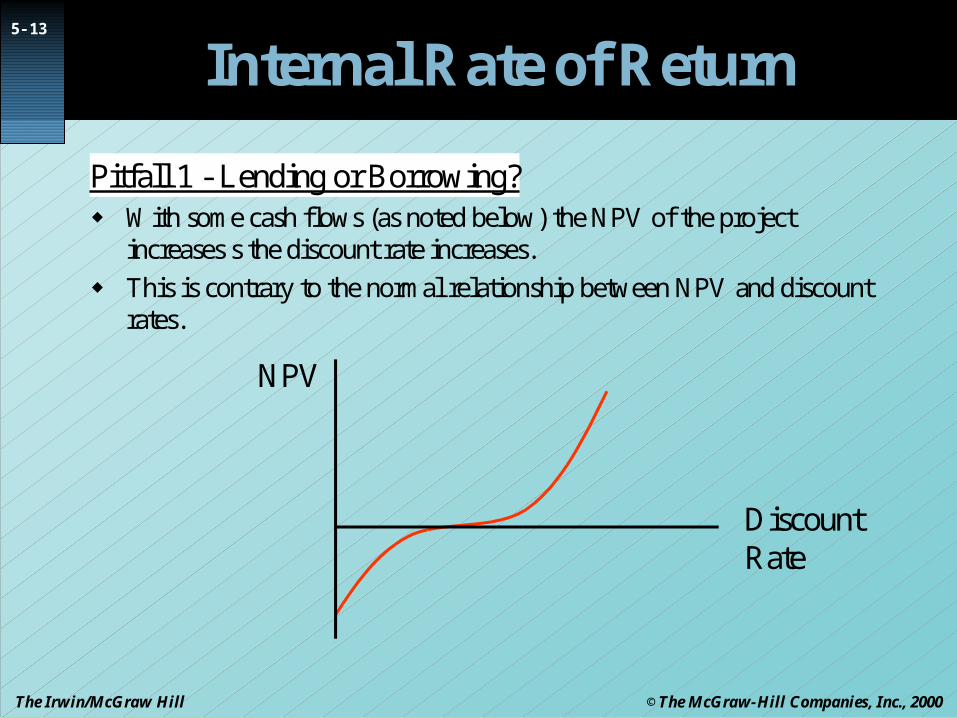

I n t e r n a l R a t e o f R e t u r n

P i t f a l l 1 - L e n d i n g o r B o r r o w i n g ? W i t h s o m e c a s h f l o w s ( a s n o t e d b e l o w ) t h e N P V o f

t h e p r o j e c t i n c r e a s e s s t h e d i s c o u n t r a t e i n c r e a s e s .

T h i s i s c o n t r a r y t o t h e n o r m a l r e l a t i o n s h i p b e t w e e nN P V a n d d i s c o u n t r a t e s .

75.%20728,1320,4600,3000,1

%10@3210

NPVIRRCCCC

Ray MartinRay Martin

Internal Rate of ReturnLending or Borrowing? (Criticism Number 1)*

With net-negative cash flows, project NPV nonsensically increases with the discount rate when expressed as a positive value.

This is obvious if you include the NPV at a zero discount rate, i.e., the total, in the calculations.

Express projects sensibly . . . – from the point of view of making money, – with positive values and rates, and – reject projects with net negative cash flows without discounting.

This is the same as both lender and borrower using the same mortgage loan amortization table.

Lending or Borrowing? (Criticism Number 1)*

With net-negative cash flows, project NPV nonsensically increases with the discount rate when expressed as a positive value.

This is obvious if you include the NPV at a zero discount rate, i.e., the total, in the calculations.

Express projects sensibly . . . – from the point of view of making money, – with positive values and rates, and – reject projects with net negative cash flows without discounting.

This is the same as both lender and borrower using the same mortgage loan amortization table.

.75 20% 8,648 1,728 4,320 3,600 1,000NPV@10% IRR Total C C C C3 2 1 0

* Refers to the criticism cited in the original paper, Internal Rate of Return Revisited.

Ray MartinRay Martin

©The McGraw-Hill Companies, Inc., 2000The Irwin/McGraw Hill

5- 13

Internal Rate of Return

Pitfall 1 - Lending or Borrowing? With some cash flows (as noted below) the NPV of the project

increases s the discount rate increases.

This is contrary to the normal relationship between NPV and discountrates.

DiscountRate

NPV

Ray MartinRay Martin

Internal Rate of ReturnCriticism Number 1 - Lending or Borrowing? With NPV expressed negatively it nonsensically increases as the

discount rate increases. This is correctable by viewing the project from the point of view

of making money--by inverting the cash flows. This expresses the relationship the same as the familiar yield

curve.

Criticism Number 1 - Lending or Borrowing? With NPV expressed negatively it nonsensically increases as the

discount rate increases. This is correctable by viewing the project from the point of view

of making money--by inverting the cash flows. This expresses the relationship the same as the familiar yield

curve.

Discount Rate

NPVRelevant Range

+

-

Nonsensical

+

Ray MartinRay Martin

Internal Rate of Return

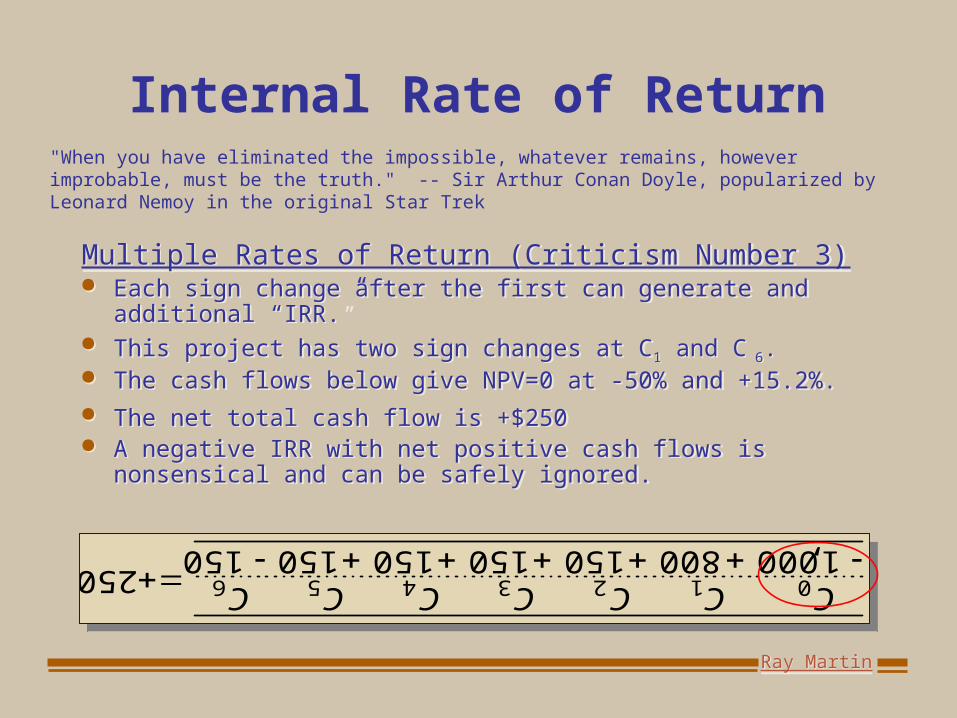

Multiple Rates of Return (Criticism Number 3) Each sign change after the first can generate and

additional “IRR.” This project has two sign changes at C1 and C 6. The cash flows below give NPV=0 at -50% and +15.2%. The net total cash flow is +$250 A negative IRR with net positive cash flows is

nonsensical and can be safely ignored.

Multiple Rates of Return (Criticism Number 3) Each sign change after the first can generate and

additional “IRR.” This project has two sign changes at C1 and C 6. The cash flows below give NPV=0 at -50% and +15.2%. The net total cash flow is +$250 A negative IRR with net positive cash flows is

nonsensical and can be safely ignored.

"When you have eliminated the impossible, whatever remains, however improbable, must be the truth." -- Sir Arthur Conan Doyle, popularized by Leonard Nemoy in the original Star Trek

250150 150 150 150 150 800 000 , 1

6 5 4 3 2 1 0 C C C C C C C

250150 150 150 150 150 800 000 , 1

6 5 4 3 2 1 0 C C C C C C C

Ray MartinRay Martin

©The McGraw-Hill Companies, Inc., 2000The Irwin/McGraw Hill

5- 15

Internal Rate of Return

Pitfall 2 - Multiple Rates of Return Certain cash flows can generate NPV=0 at two different discount rates.

The following cash flow generates NPV=0 at both (-50%) and 15.2%.

1000NPV

500

0

-500

-1000

DiscountRate

IRR=15.2%

IRR=-50%

Ray MartinRay Martin

Internal Rate of ReturnMultiple Rates of Return (Criticism Number 3) Each sign change over the first can generate and

additional “IRR.” A negative IRR with net positive cash flows is

nonsensical and can be safely ignored.

Multiple Rates of Return (Criticism Number 3) Each sign change over the first can generate and

additional “IRR.” A negative IRR with net positive cash flows is

nonsensical and can be safely ignored.

Discount Rate0

Relevant IRR=15.2%

“IRR”=-50%

NPV

1000

500

-500

-1000

Ray MartinRay Martin

© T h e M c G r a w - H i l l C o m p a n i e s , I n c . , 2 0 0 0T h e I r w i n / M c G r a w H i l l

5 - 1 6

I n t e r n a l R a t e o f R e t u r n

P i t f a l l 3 - M u t u a l l y E x c l u s i v e P r o j e c t s

I R R s o m e t i m e s i g n o r e s t h e m a g n i t u d e o f t h ep r o j e c t .

T h e f o l l o w i n g t w o p r o j e c t s i l l u s t r a t e t h a tp r o b l e m .

818,1175000,35000,20

182.8100000,20000,10

%10@Project 0

F

E

NPVIRRCC t

Ray MartinRay Martin

Internal Rate of Return

Mutually Exclusive Projects (Criticism Number 2) IRR says nothing about project scale (relative size). NPV says nothing about project risk (relative rates of return). Larger projects should give a larger NPV, ceteris paribus.

– This is another way of saying more money is better than less, even when discounted.

– Project E has lower risk in that less money is at risk.– Return and risk are inseparable for decision-making.

NPV and IRR together provide information on both relative size (return) and relative rates of return (risk) .

Mutually Exclusive Projects (Criticism Number 2) IRR says nothing about project scale (relative size). NPV says nothing about project risk (relative rates of return). Larger projects should give a larger NPV, ceteris paribus.

– This is another way of saying more money is better than less, even when discounted.

– Project E has lower risk in that less money is at risk.– Return and risk are inseparable for decision-making.

NPV and IRR together provide information on both relative size (return) and relative rates of return (risk) .

Ray MartinRay Martin

Internal Rate of ReturnInternal Rate of Return

Calculating IRR manually can be laborious. Financial calculators and spreadsheets calculate

– IRR assumes reinvestment at the IRR.– XIRR assumes reinvestment at the discount rate.

Some caution is needed with both NPV and IRR.– Both can give nonsensical answers at extremes.– IRR can be incalculable making NPV is suspect as well.– Nonsensical answers are . . .

• obvious with IRR, but • not obvious with NPV.

The DCF program calculates the relevant IRR.

Calculating IRR manually can be laborious. Financial calculators and spreadsheets calculate

– IRR assumes reinvestment at the IRR.– XIRR assumes reinvestment at the discount rate.

Some caution is needed with both NPV and IRR.– Both can give nonsensical answers at extremes.– IRR can be incalculable making NPV is suspect as well.– Nonsensical answers are . . .

• obvious with IRR, but • not obvious with NPV.

The DCF program calculates the relevant IRR.

Ray MartinRay Martin

©The McGraw-Hill Companies, Inc., 2000The Irwin/McGraw Hill

5- 17

Internal Rate of Return

Pitfall 4 - Term Structure Assumption

We assume that discount rates are stableduring the term of the project.

This assumption implies that all funds arereinvested at the IRR.

This is a false assumption.

Ray MartinRay Martin

Internal Rate of ReturnTerm Structure Assumption (Criticism Number 5) The usual assumption is that discount rates are constant

during the term of the project. Without adjustment, IRR assumes that positive cash

flows generated are reinvested at the IRR, which is inconsistent with the reinvestment assumption above.

If reinvestment at the IRR is a poor assumption, simply use a better one, e.g., . . .– either assume positive cash flows are reinvested at the

discount rate by using the XIRR function in Excel®, Lotus 1-2-3® and many financial calculators, or

– include what is done with the cash flows in the project itself when using the DCF program or a custom spreadsheet.

Term Structure Assumption (Criticism Number 5) The usual assumption is that discount rates are constant

during the term of the project. Without adjustment, IRR assumes that positive cash

flows generated are reinvested at the IRR, which is inconsistent with the reinvestment assumption above.

If reinvestment at the IRR is a poor assumption, simply use a better one, e.g., . . .– either assume positive cash flows are reinvested at the

discount rate by using the XIRR function in Excel®, Lotus 1-2-3® and many financial calculators, or

– include what is done with the cash flows in the project itself when using the DCF program or a custom spreadsheet.

Ray MartinRay Martin

Internal Rate of Return and Discounted Payback

“The perfect is the enemy of the good.” -- Author unknown It is generally better to calculate all relevant financial measures, then

reconcile and explain any apparent differences than it is to . . . hang on to one, and explain all others as flawed or ignore them.

NPV

Discounted Payback

Relevant IRR

Ray MartinRay Martin

©The McGraw-Hill Companies, Inc., 2000The Irwin/McGraw Hill

5- 4

Payback

The payback period of a project is the numberof years it takes before the cumulativeforecasted cash flow equals the initial outlay.

The payback rule says only accept projectsthat “payback” in the desired time frame.

This method is very flawed, primarilybecause it ignores later year cash flows andthe the present value of future cash flows.

Ray MartinRay Martin

Payback (Undiscounted)Payback (Undiscounted)

The payback period of a project is the amount of time it takes before the cumulative forecasted cash flow equals the initial outlay.

This method is flawed for other than short-term projects because . . .– it ignores the time value of money, and . . .

– if used without caution, it will miss downstream cash flow reversals.

Solution: Present discounted payback along with undiscounted payback and explain any apparent discrepancies between it and the DCF solution (incorporating NPV and IRR together).

The payback period of a project is the amount of time it takes before the cumulative forecasted cash flow equals the initial outlay.

This method is flawed for other than short-term projects because . . .– it ignores the time value of money, and . . .

– if used without caution, it will miss downstream cash flow reversals.

Solution: Present discounted payback along with undiscounted payback and explain any apparent discrepancies between it and the DCF solution (incorporating NPV and IRR together).

Ray MartinRay Martin

Discounted PaybackDiscounted Payback The discounted payback period of a project is the amount

of time it takes before the discounted cumulative forecasted cash flow equals the initial outlay.

This discounted payback guideline evaluates projects in terms of how long it takes to recoup the initial investment.

Discounted payback . . .– accommodates a decision-maker preference for payback;– is easily reconciled with the NPV and IRR measures of DCF;– gives an indication of risk along with IRR;– considers the time value of money; and therefore . . .– overcomes the major difficulty with undiscounted payback;

however . . .– it retains the shortcoming of no insight into possible

downstream cash flow reversals; and therefore . . .– should be used in conjunction with DCF.

The discounted payback period of a project is the amount of time it takes before the discounted cumulative forecasted cash flow equals the initial outlay.

This discounted payback guideline evaluates projects in terms of how long it takes to recoup the initial investment.

Discounted payback . . .– accommodates a decision-maker preference for payback;– is easily reconciled with the NPV and IRR measures of DCF;– gives an indication of risk along with IRR;– considers the time value of money; and therefore . . .– overcomes the major difficulty with undiscounted payback;

however . . .– it retains the shortcoming of no insight into possible

downstream cash flow reversals; and therefore . . .– should be used in conjunction with DCF.

Ray MartinRay Martin

© T h e M c G r a w - H i l l C o m p a n i e s , I n c . , 2 0 0 0T h e I r w i n / M c G r a w H i l l

5 - 6

P a y b a c k

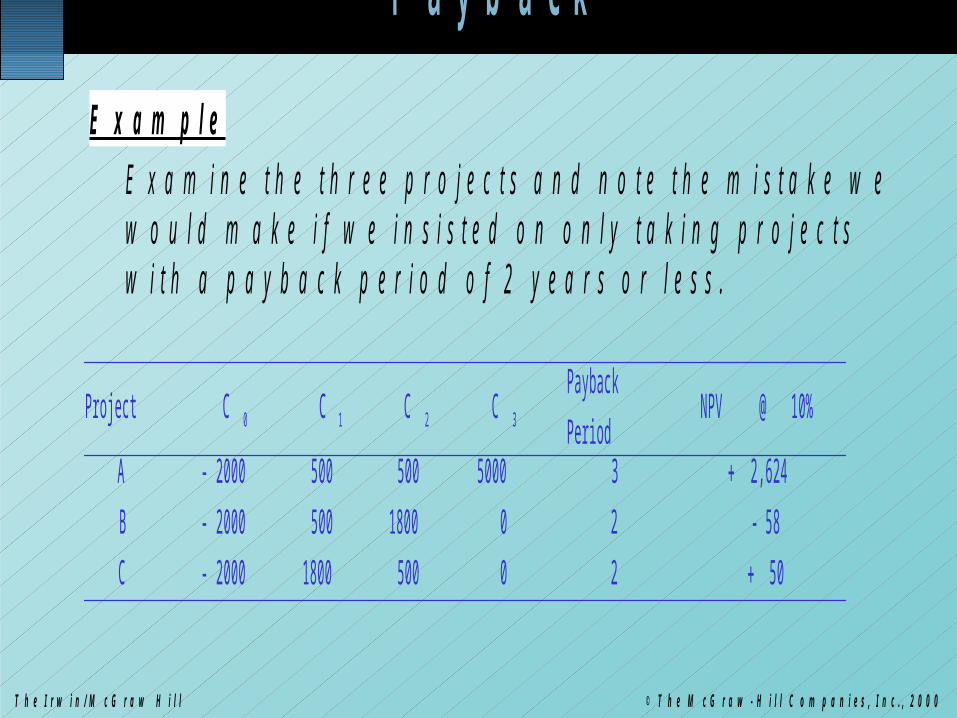

E x a m p l e

E x a m i n e t h e t h r e e p r o j e c t s a n d n o t e t h e m i s t a k e w ew o u l d m a k e i f w e i n s i s t e d o n o n l y t a k i n g p r o j e c t sw i t h a p a y b a c k p e r i o d o f 2 y e a r s o r l e s s .

502050018002000-C

58-2018005002000-B

2,624350005005002000-A

10% @NPVPeriod

PaybackCCCCProject 3210

Ray MartinRay Martin

Discounted Payback ADiscounted Payback A

Discounted Payback A

Ray MartinRay Martin

Discounted Payback BDiscounted Payback B

Compares a 3-year project to a 2-year project:– Neither NPV nor discounted payback are reliable for comparison.

– Can use uniform annual inflow instead. Reject the project on all grounds: NPV, IRR below discount rate,

no discounted payback period, negative uniform annual inflow.

Compares a 3-year project to a 2-year project:– Neither NPV nor discounted payback are reliable for comparison.

– Can use uniform annual inflow instead. Reject the project on all grounds: NPV, IRR below discount rate,

no discounted payback period, negative uniform annual inflow.

Discounted Payback

B

Uniform annual inflow

Ray MartinRay Martin

Discounted Payback CDiscounted Payback C Compares a 3-year project A to 2-year project C. Excluding risk, Project A is more attractive on all grounds except discounted payback (misses $3,756.34

discounted revenue in Year 3). Risk deserves special attention with Projects A and C because . . .

– Example A has a larger IRR, suggesting lower relative risk for A.– Example A has a longer discounted payback, suggesting lower relative risk for C.

Compares a 3-year project A to 2-year project C. Excluding risk, Project A is more attractive on all grounds except discounted payback (misses $3,756.34

discounted revenue in Year 3). Risk deserves special attention with Projects A and C because . . .

– Example A has a larger IRR, suggesting lower relative risk for A.– Example A has a longer discounted payback, suggesting lower relative risk for C.

Discounted Payback

C

Ray MartinRay Martin

ConclusionConclusion

This presentation . . .– addresses disagreement over the treatment of IRR only.

– is not a critique of any other aspects of the Principles text. Little has changed between the 6th and prior editions of

Principles of Corporate Finance as far as treatment of IRR is concerned.

The differences were discussed in the papers at:– http://members.tripod.com/~Ray_Martin/DCF/nr7aa003.html

– http://members.tripod.com/~Ray_Martin/DCF/B-MFAQs.html

– http://members.tripod.com/~Ray_Martin/NSF9914/RejctRev.html

Thank you for your review. Click for a >>> Home Page Menu.

This presentation . . .– addresses disagreement over the treatment of IRR only.

– is not a critique of any other aspects of the Principles text. Little has changed between the 6th and prior editions of

Principles of Corporate Finance as far as treatment of IRR is concerned.

The differences were discussed in the papers at:– http://members.tripod.com/~Ray_Martin/DCF/nr7aa003.html

– http://members.tripod.com/~Ray_Martin/DCF/B-MFAQs.html

– http://members.tripod.com/~Ray_Martin/NSF9914/RejctRev.html

Thank you for your review. Click for a >>> Home Page Menu.