ratio analysis chapter 6 robinson, munter, grant

TRANSCRIPT

Ratio Analysis

Chapter 6

Robinson, Munter, Grant

Grant, Munter & Robinson

Chapter 6 2

Learning Objectives

• Identify situations in which ratio analysis is useful

• Understand the purpose of ratio analysis

• Calculate specific ratios

• Recognize limitations of accounting data in ratio analysis

Grant, Munter & Robinson

Chapter 6 3

Ratio Analysis

• Cross-sectional and time series analysis

• Controls for size differences

• Controls for currency differences

• Evaluate related components of different financial statements simultaneously

• Ratios are easily (and commonly) modified

Grant, Munter & Robinson

Chapter 6 4

Ratio Analysis Categories

• Activity (operations and asset management)

• Liquidity (meeting short-term obligations)

• Solvency (meeting long-term obligations)

• Profitability (earnings and cost coverage)

• Cash Flow (quality of earnings)

• Price Multiples (stock price)

Grant, Munter & Robinson

Chapter 6 5

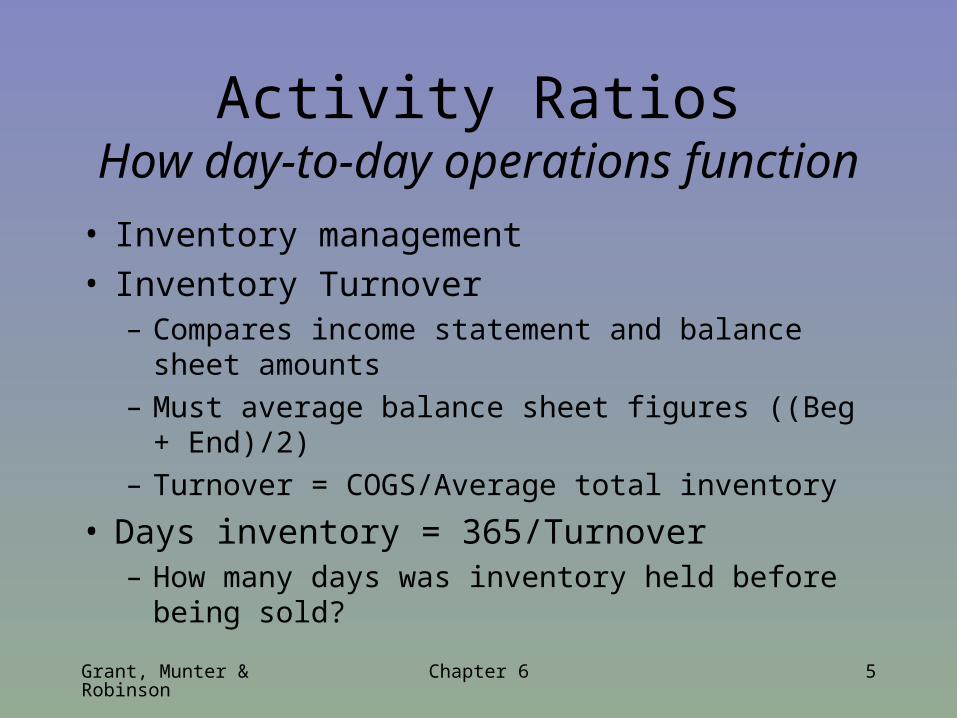

Activity RatiosHow day-to-day operations function

• Inventory management• Inventory Turnover

– Compares income statement and balance sheet amounts

– Must average balance sheet figures ((Beg + End)/2)

– Turnover = COGS/Average total inventory

• Days inventory = 365/Turnover– How many days was inventory held before being sold?

Grant, Munter & Robinson

Chapter 6 6

Activity RatiosCritical operating cash accounts

• Accounts receivable turnover– How many times a credit sale is made and subsequently

collected

– [credit sales/average accounts receivable]

– May have to use total sales rather than credit sales

– Consistency is important

• Days receivable– Number of days between the charge sale and collection

– [365/accounts receivable turnover]

Grant, Munter & Robinson

Chapter 6 7

Activity RatiosCritical operating cash accounts

• Accounts payable turnover– Number of times a credit purchase is made and

subsequently paid

– [credit purchases/average accounts payable]

– Often assume all purchases are on credit

– Purchases = [COGS + Ending Inv. - Beginning Inv.]

• Days payable– Number of days between credit purchase and payment

– [365/accounts payable turnover]

Grant, Munter & Robinson

Chapter 6 8

Activity RatiosCash Cycle

• Also a measure of liquidity

• If low, small number of days in operating cycle to finance

[Days inventory + Days receivable - Days payable]

Grant, Munter & Robinson

Chapter 6 9

Activity RatiosAsset Turnover

• Long-term– Revenues generated by long-term assets– [Sales revenue/Average noncurrent assets]

• Total assets– Efficiency of generating revenues given total

assets– [Sales revenue/Average total assets]

Grant, Munter & Robinson

Chapter 6 10

Liquidity Ratios

• Current ratio– Ability to meet short-term obligations– [Current assets/current liabilities]

• Quick ratio– Remove less liquid assets– Keep cash, liquid investments, A/R– [(Current assets-inventory-ppd expenses-other)/current liabilities]

– [(Cash+short-term investments + A/R)/current liabilities]

Grant, Munter & Robinson

Chapter 6 11

Liquidity Ratios

• Defensive interval ratio– Compare 1 day’s costs to quick assets

– [((COGS+SGA+RD)/365)/(Cash+short-term investments + A/R)]

• For Motorola, defensive interval = .0075– COGS = 21,445– SG&A = 3,703– R&D = 4,318– Quick assets = 10,745 (6,082 + 80 + 4,583)

Grant, Munter & Robinson

Chapter 6 12

Solvency Ratios

• Debt to assets: Total liabilities/Total assets– Proportion of assets financed with debt

• Could include interest bearing debt only[(short term debt + noncurrent debt)/total assets]

• Be aware that assets are recorded at historical cost, which may be different from current market value

Grant, Munter & Robinson

Chapter 6 13

Solvency Ratios

• Debt to equity: Total liabilities/Total equity– A measure of how assets are financed

• Or… (current debt + noncurrent debt)/Total equity– Examine relative sizes of debt and equity

financing

• Capitalization ratio:[(current debt+noncurrent debt)/(current debt+noncurrent debt+total equity)]

Grant, Munter & Robinson

Chapter 6 14

Solvency RatiosCoverage Ratios

• Adequacy of resources for meeting firm’s contractual obligations

• Times interest earned– Can the firm cover its interest obligations?– (EBIT/Interest expense)

• Cash interest coverage– (Cash from ops + interest paid + tax paid)/Interest paid

Grant, Munter & Robinson

Chapter 6 15

Solvency RatiosCoverage Ratios

• Target a specific expense– [(EBIT+Rent expense)/(Interest expense+rent expense)]

• Target principal on debt that is about to be repaid– [EBIT/(interest expense + principal payments)]

Grant, Munter & Robinson

Chapter 6 16

Profitability RatiosCommon-size

• From chapter 5…

• Income statement– Divide item of interest by sales– ROS = Net income/Sales revenue– Gross margin = Gross profit/Sales revenue

• Balance sheet– Divide item of interest by total assets

Grant, Munter & Robinson

Chapter 6 17

Profitability RatiosReturn Ratios

• ROA = Net income/Average total assets

• Or, [(Net income + After-tax interest expense)/Average total assets]

• Also, [EBIT/Average total assets] reflects pre-tax, pre-interest return

Grant, Munter & Robinson

Chapter 6 18

Profitability RatiosReturn Ratios

• ROE = Net income/Average total equity– Return generated relative to the capital provided

by the owners over time

• Or, if firm has preferred stock[(Net income – Prfd dividends)/Average total common equity]

• ROMVE = Net income/Market value of equity

Grant, Munter & Robinson

Chapter 6 19

Cash Flow RatiosQuality of earnings

• Ability to pay obligations– CFO/Total liabilities– CFO = Cash flows from operations

• Profitability (cash flow relative to sales)– CFO/Sales revenue

• Cash return on assets– CFO/Average total assets

Grant, Munter & Robinson

Chapter 6 20

Cash Flow RatiosQuality of earnings

• Cash flow-earnings index– CFO/Net income

• Free cash flow ratio– CFO/Capital expenditures– If ratio>1, free cash flow exists

Grant, Munter & Robinson

Chapter 6 21

Price Multiple Ratios

• Market’s valuation of a firm’s common stock– P/E = Share price/Earnings per share

• Price/book ratio compares stock’s price to the recorded value of the net assets[Share price/(Book value of equity/Share outstanding)]

• Price/sales = Share price/Sales per share• Also, compare price to cash flow per share

Grant, Munter & Robinson

Chapter 6 22

Ratio Integration

DuPont analysis (decomposition)

ROE = ROA x Leverage

And more…

equity totalAverage

assets totalAverage

assets totalAverage

incomeNet

equity totalAverage

incomeNet

equity totalAverage

assets totalAverage

assets totalAverage

Sales

Sales

incomeNet

equity totalAverage

incomeNet

Grant, Munter & Robinson

Chapter 6 23

Ratio Integration

ROA = Profitability x Turnover

assets totalAverage

Sales

Sales

incomeNet

assets totalAverage

incomeNet

Grant, Munter & Robinson

Chapter 6 24

Analysis

• Generally compare 3-5 years• Requires 4-6 years of data

– Balance sheet numbers may be averaged

• Compare Motorola and Nokia– Activity– Liquidity– Solvency– Profitability

Grant, Munter & Robinson

Chapter 6 25

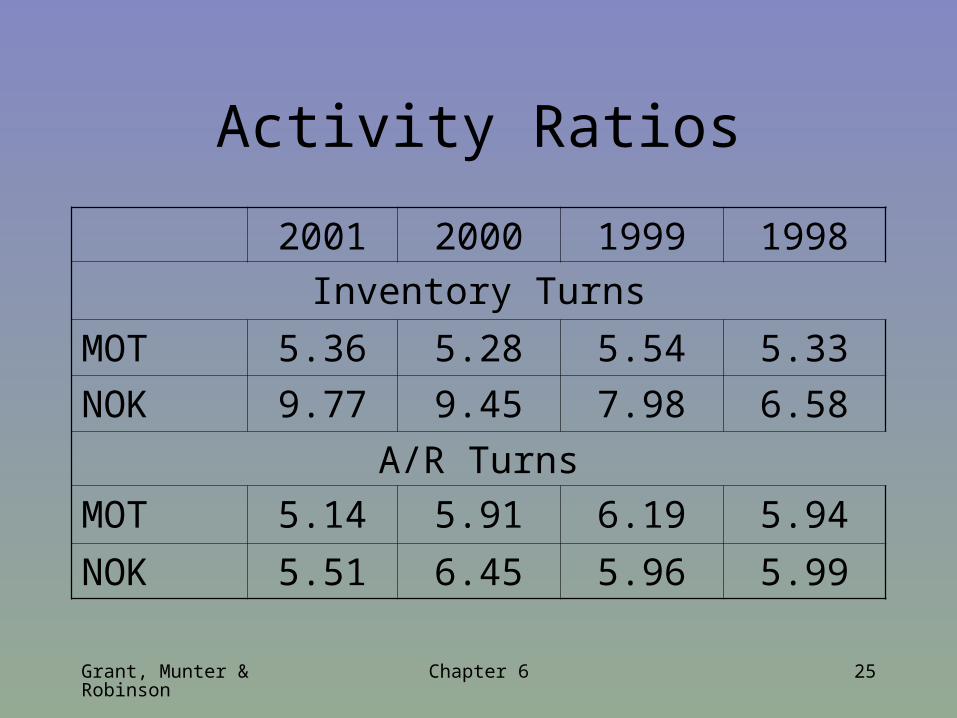

Activity Ratios

2001 2000 1999 1998

Inventory Turns

MOT 5.36 5.28 5.54 5.33

NOK 9.77 9.45 7.98 6.58

A/R Turns

MOT 5.14 5.91 6.19 5.94

NOK 5.51 6.45 5.96 5.99

Grant, Munter & Robinson

Chapter 6 26

Liquidity Ratios

2001 2000 1999 1998

Current ratio

MOT 1.77 1.22 1.36 1.18

NOK 1.62 1.57 1.69 1.75

Quick ratio

MOT 1.11 0.66 0.76 0.58

NOK 1.24 1.14 1.25 1.28

Grant, Munter & Robinson

Chapter 6 27

Solvency Ratios

2001 2000 1999 1998

Debt-to-assets

MOT 57.6% 54.9% 52.6% 57.5%

NOK 44.7% 44.8% 47.5% 48.5%

Times interest earned

MOT -7.54 6.05 5.65 -3.56

NOK 43.38 51.97 16.14 13.40

Grant, Munter & Robinson

Chapter 6 28

Profitability Ratios

2001 2000 1999 1998

ROA

MOT -10.4% 3.2% 2.6% -3.4%

NOK 10.4% 23.1% 21.2% 20.5%

ROE

MOT -23.7% 6.9% 5.7% -7.6%

NOK 18.8% 42.6% 40.7% 40.7%

Grant, Munter & Robinson

Chapter 6 29

Limitations to consider

• Historical cost of balance sheet items

• GAAP vs. IAS rules

• Accounting method differences– LIFO vs. FIFO inventory valuation

Grant, Munter & Robinson

Chapter 6 30

Summary

• Calculate ratios

• Decompose and interpret results

• Understand limitations of ratio analysis