rating agency analysis and perspective on mpl … leadership camp james auden, managing director,...

TRANSCRIPT

PIAA Leadership Camp

James Auden Managing Director Fitch Ratings

May 17 2017

Rating Agency Analysis and Perspective on MPL Insurance Reserve Adequacy

1

PropertyCasualty Insurer Ratings Approach

minus Fitch Rating Scale and Methodology Versus Other Agencies

minus Application of Rating Factors to MPLI Specialists

MPLI Loss Reserve Analysis

minus Key Loss Reserve Characteristics

minus Loss Reserve Analysis in Ratings Process

Agenda

2

PropertyCasualty Rating Approach1

3

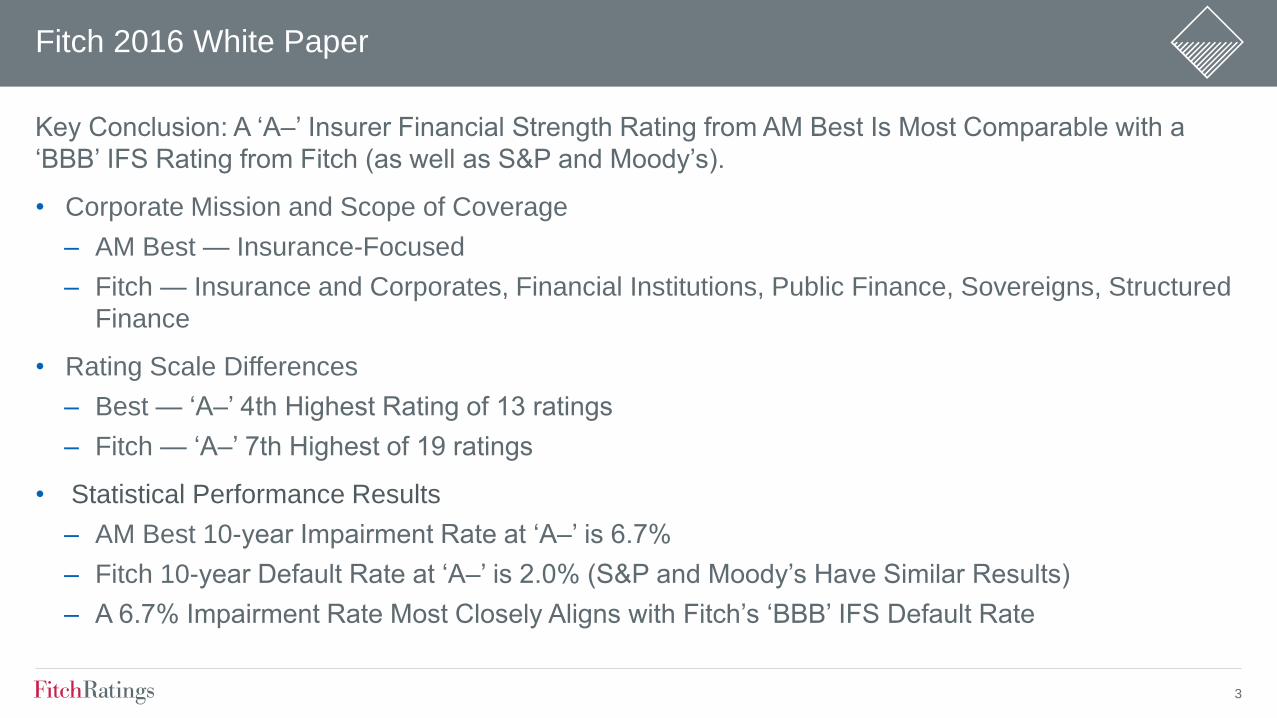

Fitch 2016 White Paper

Key Conclusion A lsquoAndashrsquo Insurer Financial Strength Rating from AM Best Is Most Comparable with a

lsquoBBBrsquo IFS Rating from Fitch (as well as SampP and Moodyrsquos)

bull Corporate Mission and Scope of Coverage

‒ AM Best mdash Insurance-Focused

‒ Fitch mdash Insurance and Corporates Financial Institutions Public Finance Sovereigns Structured

Finance

bull Rating Scale Differences

‒ Best mdash lsquoAndashrsquo 4th Highest Rating of 13 ratings

‒ Fitch mdash lsquoAndashrsquo 7th Highest of 19 ratings

bull Statistical Performance Results

‒ AM Best 10-year Impairment Rate at lsquoAndashrsquo is 67

‒ Fitch 10-year Default Rate at lsquoAndashrsquo is 20 (SampP and Moodyrsquos Have Similar Results)

‒ A 67 Impairment Rate Most Closely Aligns with Fitchrsquos lsquoBBBrsquo IFS Default Rate

4

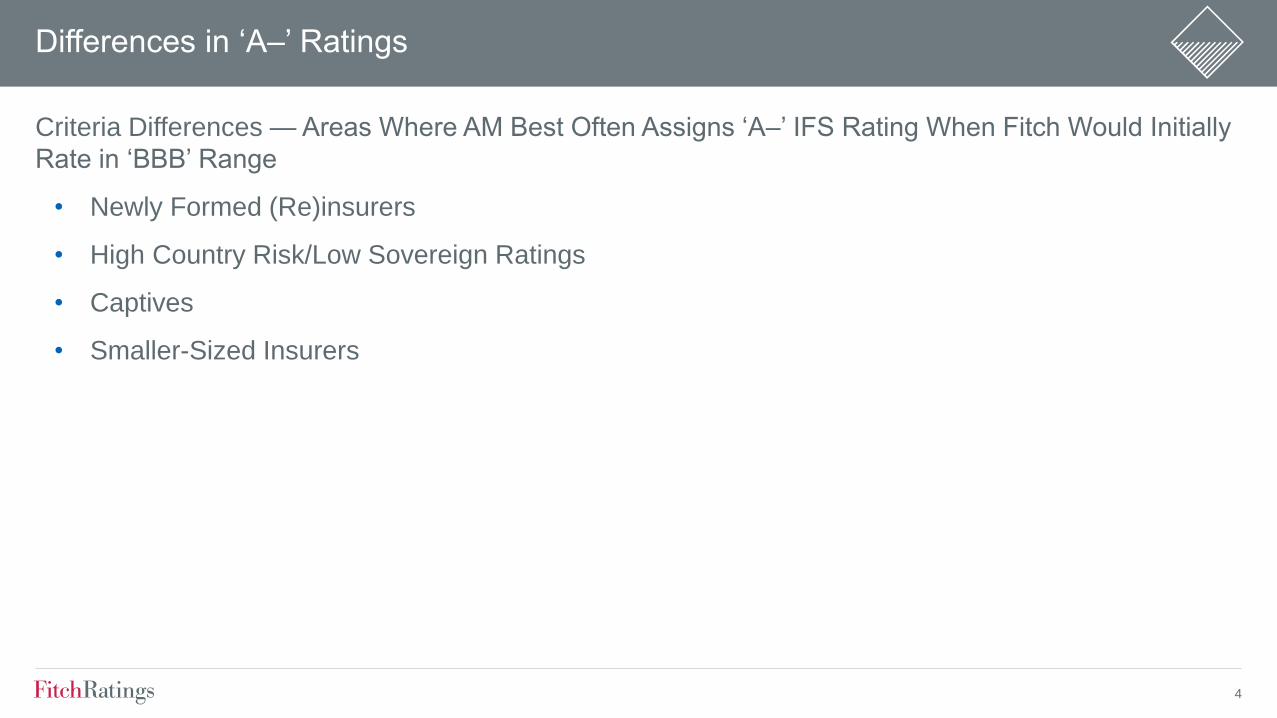

Criteria Differences mdash Areas Where AM Best Often Assigns lsquoAndashrsquo IFS Rating When Fitch Would Initially

Rate in lsquoBBBrsquo Range

bull Newly Formed (Re)insurers

bull High Country RiskLow Sovereign Ratings

bull Captives

bull Smaller-Sized Insurers

Differences in lsquoAndashrsquo Ratings

5

Qualitative Factors

bull Industry Profile and Operating Environment

bull Business Profile

bull Ownership

bull Corporate Governance

bull Management

Rating MPLI Specialists mdash Important Credit Factors

Quantitative Factors

bull Capitalization and Leverage

bull Debt Service Capabilities and Financial

Flexibility

bull Financial Performance and Earnings

bull Investment and Asset Risk

bull Reserve Adequacy

bull Reinsurance Risk Mitigation and Catastrophe

Risk

6

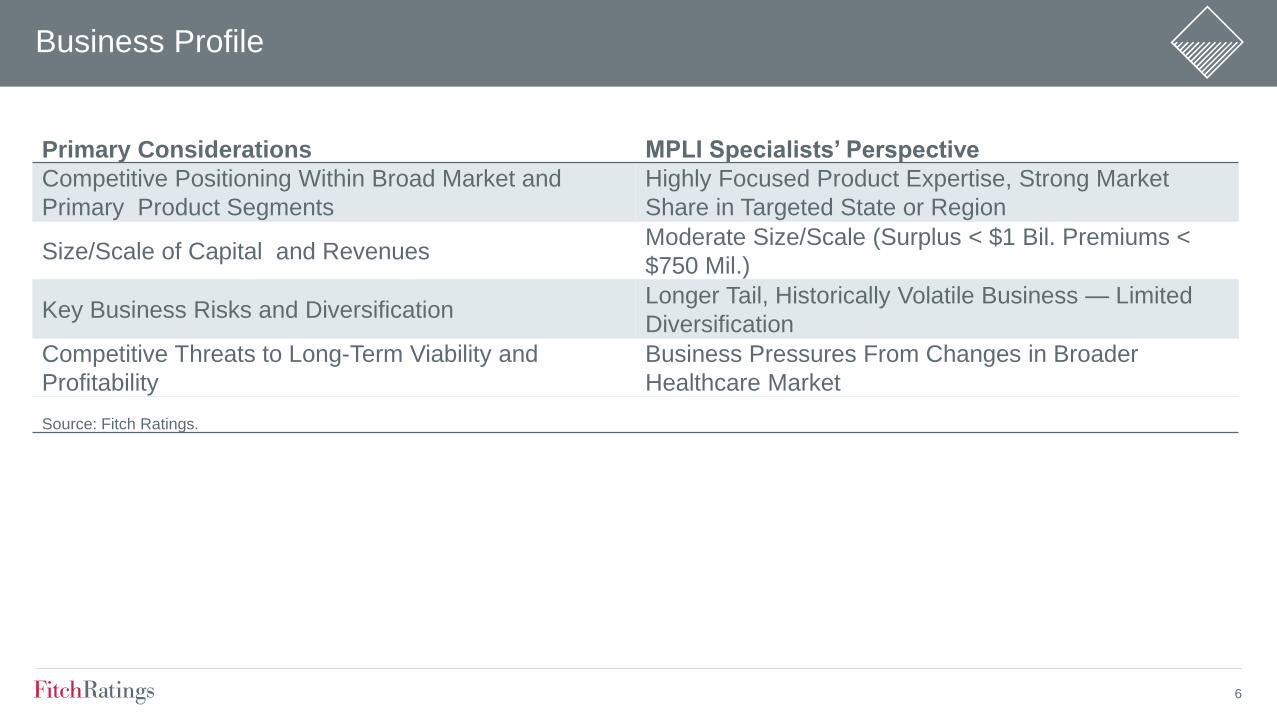

Business Profile

Primary Considerations MPLI Specialistsrsquo Perspective

Competitive Positioning Within Broad Market and

Primary Product Segments

Highly Focused Product Expertise Strong Market

Share in Targeted State or Region

SizeScale of Capital and Revenues Moderate SizeScale (Surplus lt $1 Bil Premiums lt

$750 Mil)

Key Business Risks and Diversification Longer Tail Historically Volatile Business mdash Limited

Diversification

Competitive Threats to Long-Term Viability and

Profitability

Business Pressures From Changes in Broader

Healthcare Market

Source Fitch Ratings

7

00

02

04

06

08

0

5

10

15

20

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

($ Bil)

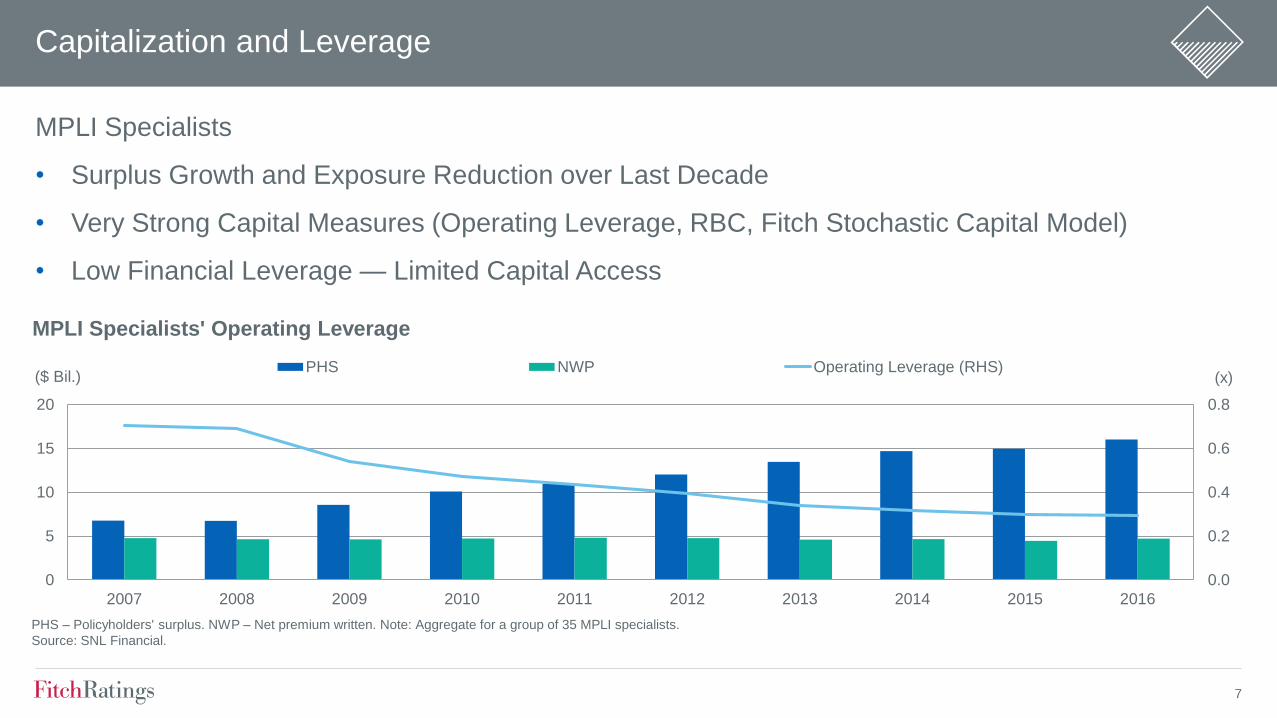

MPLI Specialists Operating Leverage

PHS NWP Operating Leverage (RHS)

PHS ndash Policyholders surplus NWP ndash Net premium written Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

(x)

Capitalization and Leverage

MPLI Specialists

bull Surplus Growth and Exposure Reduction over Last Decade

bull Very Strong Capital Measures (Operating Leverage RBC Fitch Stochastic Capital Model)

bull Low Financial Leverage mdash Limited Capital Access

8

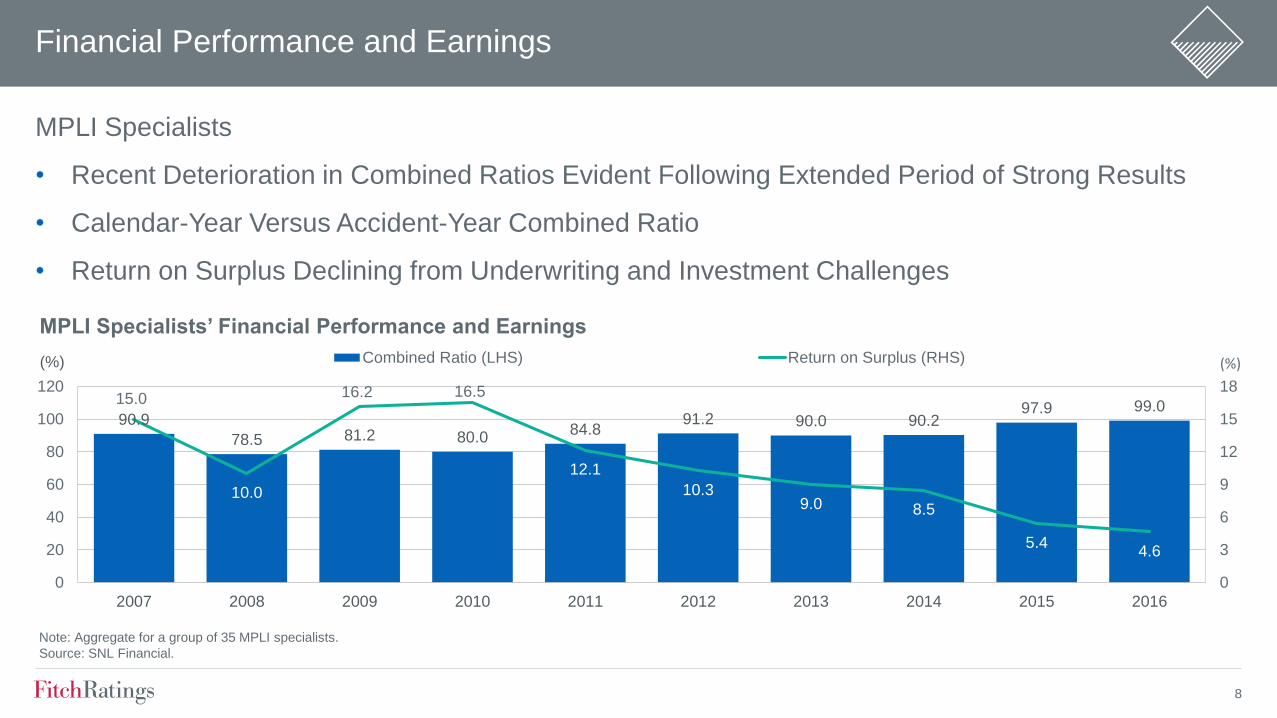

Financial Performance and Earnings

MPLI Specialists

bull Recent Deterioration in Combined Ratios Evident Following Extended Period of Strong Results

bull Calendar-Year Versus Accident-Year Combined Ratio

bull Return on Surplus Declining from Underwriting and Investment Challenges

909

785 812 800 848

912 900 902 979 990

150

100

162 165

121

103 90 85

54 46

0

3

6

9

12

15

18

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

MPLI Specialistsrsquo Financial Performance and Earnings

Combined Ratio (LHS) Return on Surplus (RHS)

Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

()

9

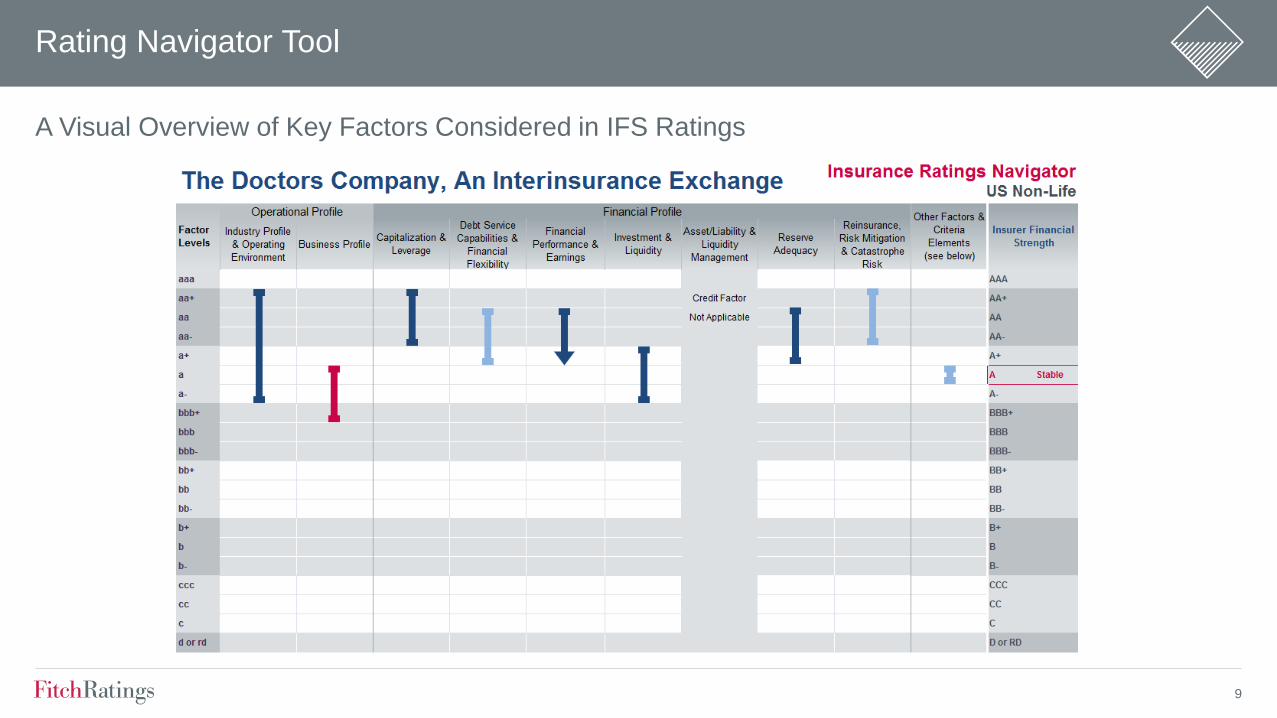

Rating Navigator Tool

A Visual Overview of Key Factors Considered in IFS Ratings

10

MPLI Reserve Analysis2

11

Workers Comp24

Other Liability22

Commercial Multiperil

6

Reinsurance6

MPLI4

Homeowners4

Special Property

2Other

Reserves3

Source SNL Financial

PropertyCasualty Industry Loss Reserves YE 2016(Total Industry Reserves = $621 Bil)

Private

Passenger Auto

20

Commercial Auto

5

Financial

Guaranty

Mortgage

Insurance

2Product Liability

2

MPLI mdash Reserve Characteristics

bull Represent 44 of Industry 2016 Loss

Reserves

bull More Volatile Segment Versus Other PC Lines

bull Longer-Tail Claims Liabilities

bull Large Defense Costs Component to Claims

12

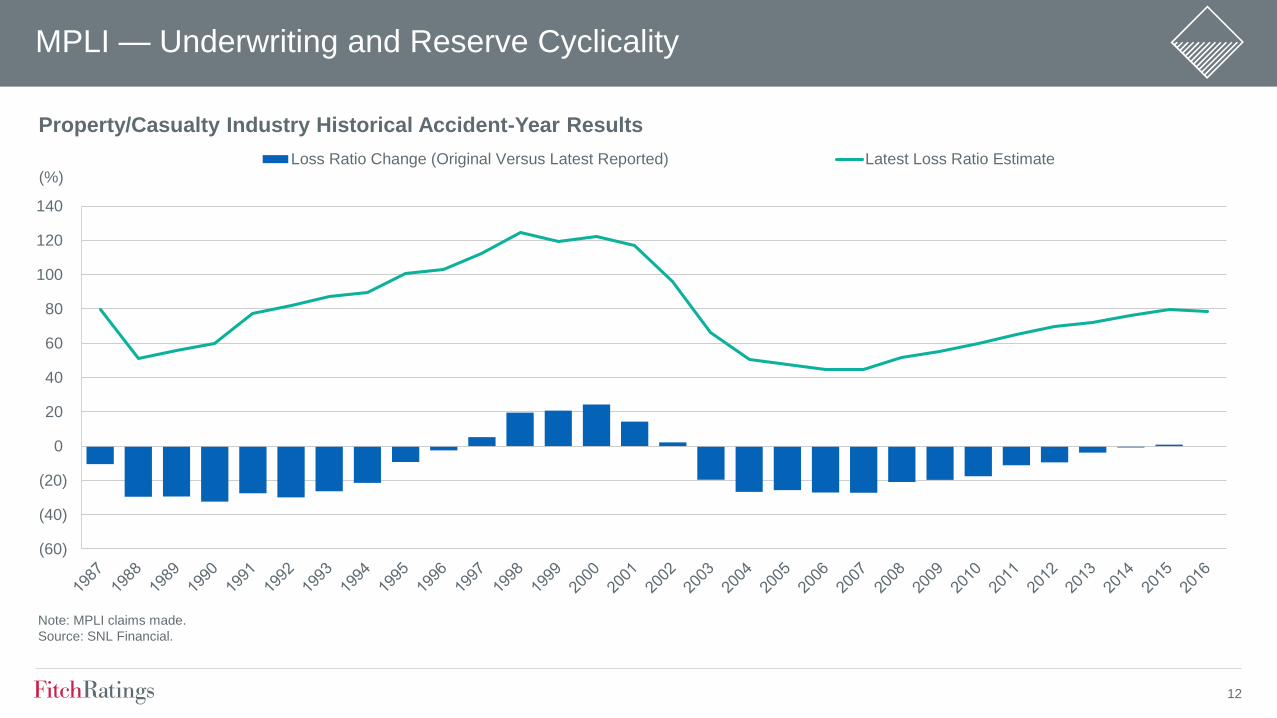

MPLI mdash Underwriting and Reserve Cyclicality

(60)

(40)

(20)

0

20

40

60

80

100

120

140

()

PropertyCasualty Industry Historical Accident-Year Results

Loss Ratio Change (Original Versus Latest Reported) Latest Loss Ratio Estimate

Note MPLI claims made

Source SNL Financial

13

Reserve Characteristics Volatility

MPLI Claims Made Has Higher Underwriting and Reserve Volatility than Nearly All Major PC Segments

Private Passenger Auto WCAll Lines

Commercial AutoCMP

HO

OL OCC

Specialty LiabilityMPLI CM

OL CM

Prod Liab Occ

0

5

10

15

20

25

30

0 5 10 15 20 25 30

(Average Loss Ratio Volatility )

Average Loss Ratio Volatility Versus Reserve Volatility by Segment

WC ndash Workers compensation CMP ndash Commercial multiperil HO ndash Homeowners OL OCC ndash Other liability ndash occurrence MPLI CM ndash Medical practice liability insurance claims made OL CM ndash Other

liability ndash claims made Liab OCC ndash Liability occurrence

Source SNL Financial Fitch

()

14

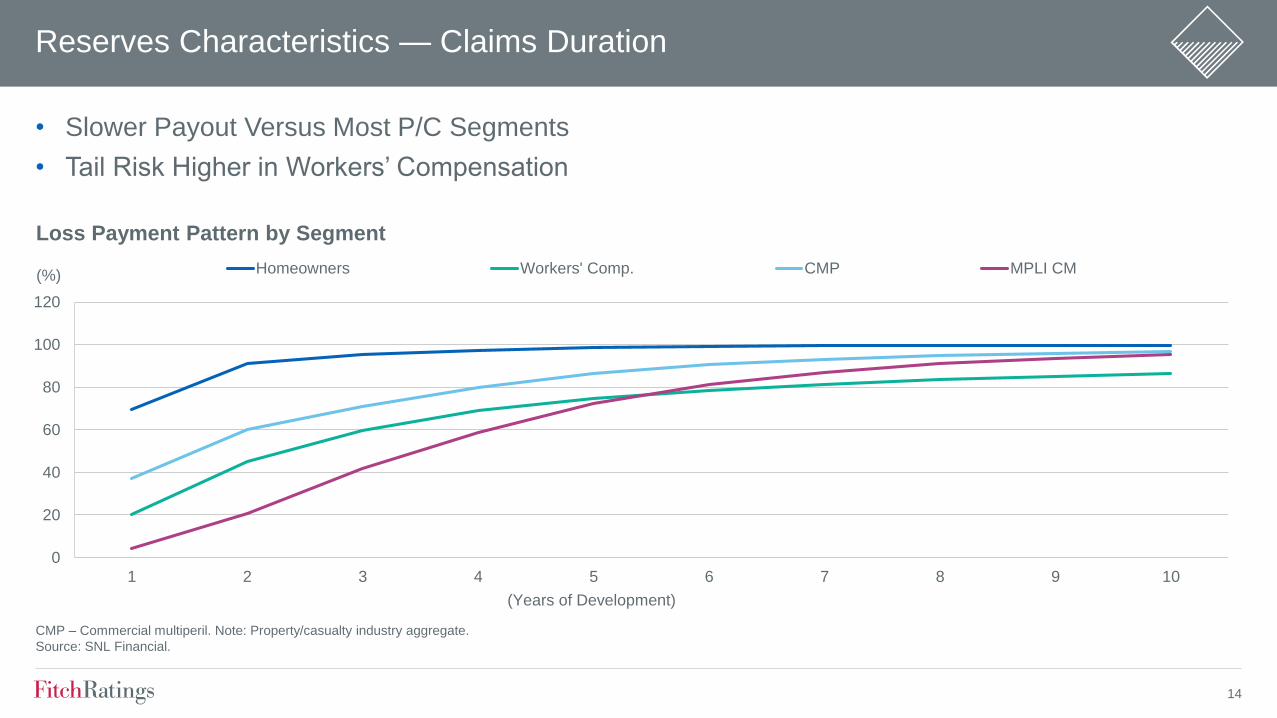

bull Slower Payout Versus Most PC Segments

bull Tail Risk Higher in Workersrsquo Compensation

Reserves Characteristics mdash Claims Duration

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10

()

Loss Payment Pattern by Segment

Homeowners Workers Comp CMP MPLI CM

CMP ndash Commercial multiperil Note Propertycasualty industry aggregate

Source SNL Financial

(Years of Development)

15

bull Approximately 73 of Industry MPLI Reserves Are in Latest Four Accident Years 2013ndash2016

MPLI Reserve Composition

201624

201521

201416

201312

20128

20116

20104

20092

20082

20071 2006 and Prior

4

Source SNL Financial

Industry MPLI Reserves by Accident Year(73 of Reserves Relate to Accident-Years 2013ndash2016)

16

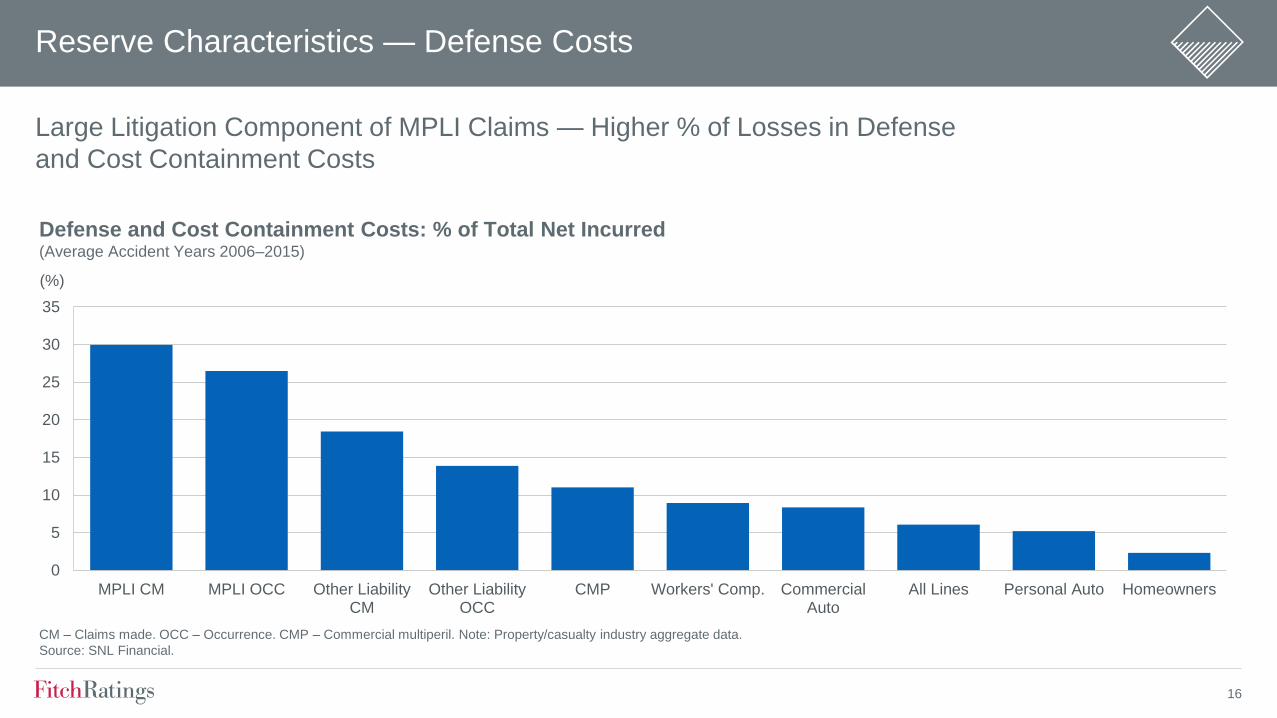

Large Litigation Component of MPLI Claims mdash Higher of Losses in Defense

and Cost Containment Costs

Reserve Characteristics mdash Defense Costs

0

5

10

15

20

25

30

35

MPLI CM MPLI OCC Other LiabilityCM

Other LiabilityOCC

CMP Workers Comp CommercialAuto

All Lines Personal Auto Homeowners

()

Defense and Cost Containment Costs of Total Net Incurred(Average Accident Years 2006ndash2015)

CM ndash Claims made OCC ndash Occurrence CMP ndash Commercial multiperil Note Propertycasualty industry aggregate data

Source SNL Financial

17

MPLI Reserve Analysis

bull Reserve Profile

bull Reserve Growth

bull Reserve Experience

bull Reserve Adequacy

18

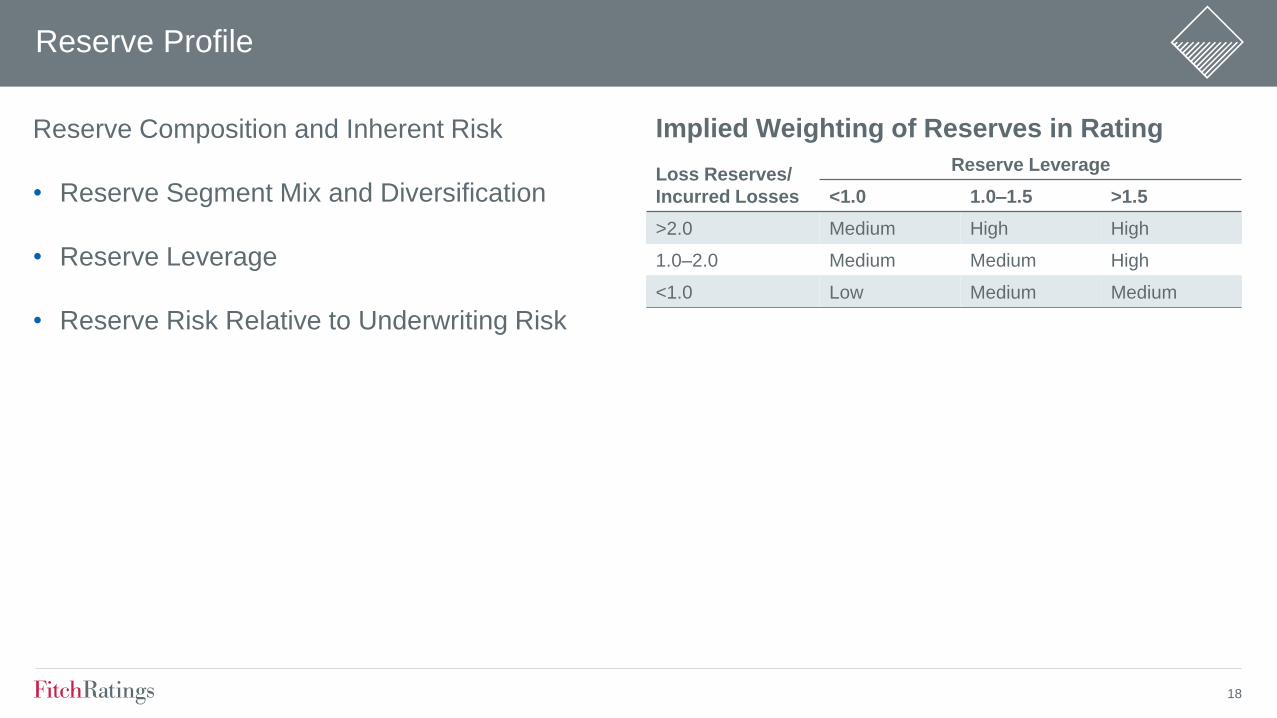

Reserve Profile

Reserve Composition and Inherent Risk

bull Reserve Segment Mix and Diversification

bull Reserve Leverage

bull Reserve Risk Relative to Underwriting Risk

Implied Weighting of Reserves in Rating

Loss Reserves

Incurred Losses

Reserve Leverage

lt10 10ndash15 gt15

gt20 Medium High High

10ndash20 Medium Medium High

lt10 Low Medium Medium

19

MPLI Specialists Reserve Leverage Declining over Time with Surplus Growth

ReservesIncurred Ratio Very High mdash Implies Greater Capital Sensitivity to Reserve Changes than

Current Underwriting Period

MPLI Reserve Profile

00

05

10

15

20

25

0

3

6

9

12

15

18

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

($ Bil)

MPLI Specialists Reserve Leverage

PHS Reserves Reserve Leverage

PHS ndash Policyholders surplus Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

(x)

00

10

20

30

40

50

60

70

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)ReservesCY Incurred Reserve Leverage

CY ndash Calendar year Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

MPLI Specialists Reserve Leverage Versus Reserves

CY Incurred

20

Over Long Term an Insurerrsquos Reserves Should Grow Commensurate with Exposures

Key Ratios

bull Calendar-Year PaidCalendar-Year Incurred Losses

bull ReservesEarned Premiums (Changes over Time)

MPLI Reserve Growth

00

02

04

06

08

10

12

14

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)

Note Aggregate for a group of 35 MPLI specialists Calendar-year paid and incurred losses

Source SNL Financial

Paid gt Incurred Loss Indicative of

Reserve Weakness but Incurred

Influence by Reserve Takedowns

MPLI Specialists Reserve Growth Indications(PaidIncurred Losses)

30

31

32

33

34

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)

Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

Stable Ratio = Reserve

Changes Keeping Pace

with Premium Changes

MPLI Specialists Reserve Growth Indications(ReservesEarned Premium)

21

Key Ratios

bull Calendar Year

‒ One Year Development Prior-Year Reserves

‒ One Year Development Prior-Year Surplus

‒ One Year Development Earned Premiums

bull Accident Year

‒ Current Loss Ratio Estimate Versus Original Estimate

‒ Accident-Year Development History and Trends

MPLI Reserve Experience

22

Reserve Experience mdash Favorable MPLI Development

bull Reserve Development Still Highly Favorable but Slowing Considerably

196

237228

266

221206

245

198

166

116

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

( of Earned Premiums)

MPLI Calendar-Year Reserve Development

Note Excludes MCIC Vermont Propertycasualty industry aggregate

Source SNL Financial

Favorable

Development

23

Reserve Experience mdash Calendar-Year Development

bull MPLI Development Greatly Exceeds Other Commercial Lines Segments over Last Decade

bull Magnitude of Favorable Development in MPLI Declining

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

Commercial Auto Other Liability mdash Claims Made Other Liability mdash Occurrence MPLI mdash Claims Made Workers Compensation

() 2012 2013 2014 2015 2016

Source SNL Financial

Segment Calendar-Year Development as a of Earned Premium mdash (Favorable)Unfavorable

24

Favorable Reserve Development Slowing

(5)

0

5

10

15

20

2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003

12ndash24 Months 24ndash36 Months 36ndash48 Months

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial

( Favorable[Unfavorable])

Favorable MPLI Accident-Year Development Slowing mdash Change in Loss Ratio

25

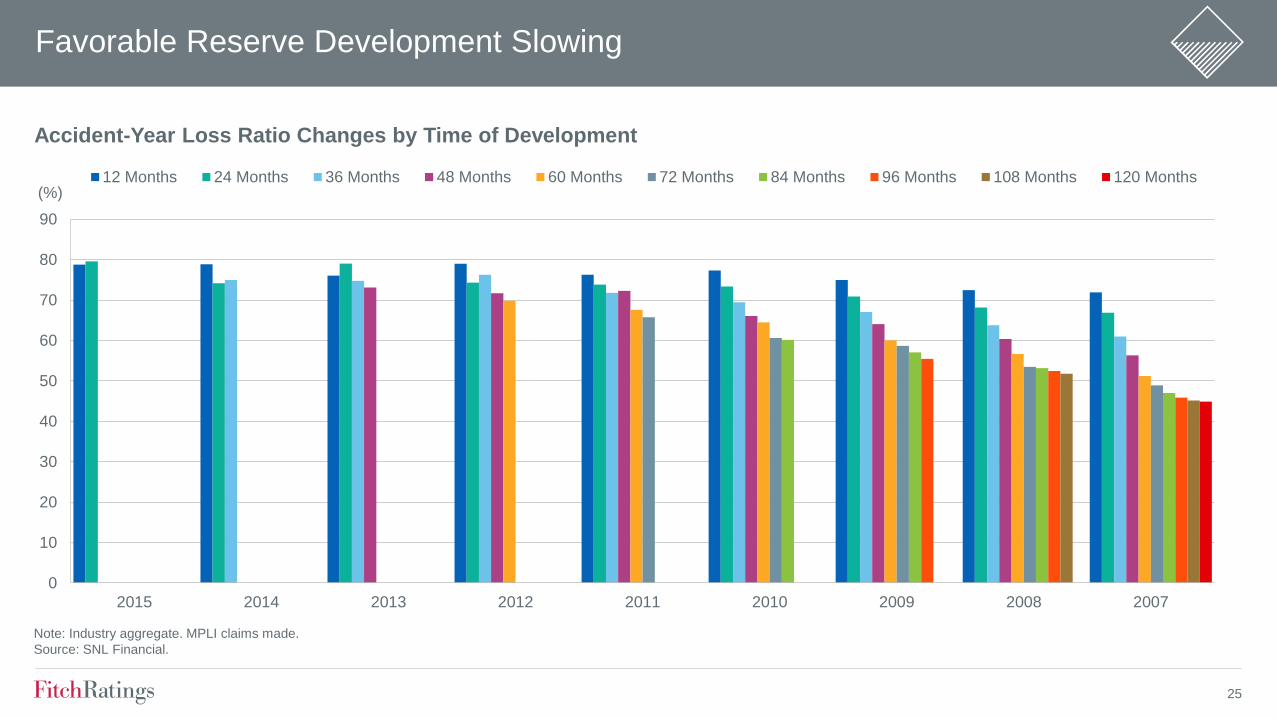

Favorable Reserve Development Slowing

0

10

20

30

40

50

60

70

80

90

2015 2014 2013 2012 2011 2010 2009 2008 2007

()

Accident-Year Loss Ratio Changes by Time of Development

12 Months 24 Months 36 Months 48 Months 60 Months 72 Months 84 Months 96 Months 108 Months 120 Months

Note Industry aggregate MPLI claims made

Source SNL Financial

26

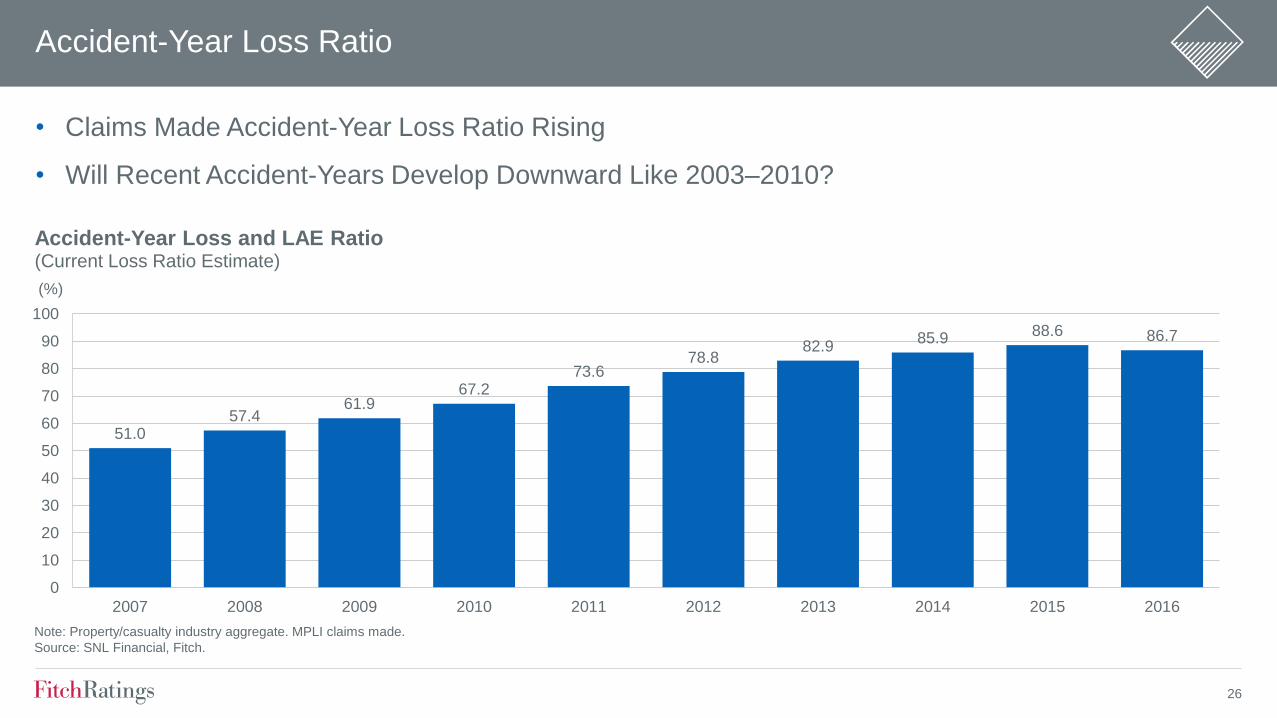

Accident-Year Loss Ratio

bull Claims Made Accident-Year Loss Ratio Rising

bull Will Recent Accident-Years Develop Downward Like 2003ndash2010

510 574

619 672

736 788

829 859 886 867

0

10

20

30

40

50

60

70

80

90

100

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

Accident-Year Loss and LAE Ratio(Current Loss Ratio Estimate)

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial Fitch

27

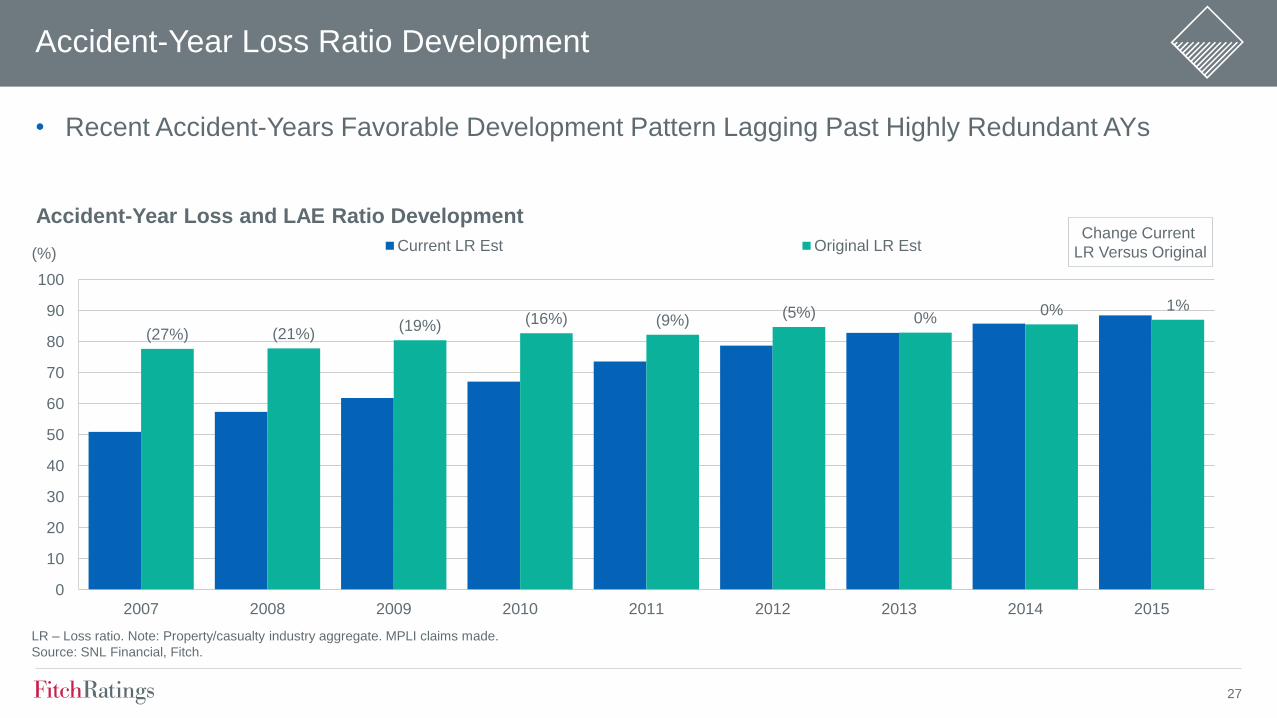

Accident-Year Loss Ratio Development

bull Recent Accident-Years Favorable Development Pattern Lagging Past Highly Redundant AYs

(27) (21)(19) (16) (9)

(5) 00 1

0

10

20

30

40

50

60

70

80

90

100

2007 2008 2009 2010 2011 2012 2013 2014 2015

()

Accident-Year Loss and LAE Ratio Development

Current LR Est Original LR Est

LR ndash Loss ratio Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial Fitch

Change Current

LR Versus Original

28

MPLI Reserve Adequacy

Key Considerations

bull Likelihood of Balance Sheet Reported Reserves to Develop HigherLower over Time

bull Stress Test Capital Impact of Potential Deficiencies

Analytical Tools

bull Project Reserve Adequacy Using Loss Development Methods (PaidCase Incurred)

bull Accident-Year Ratio Analysis

29

Reserve Adequacy mdash MPLI

bull Initial Analysis of Industry 2016 Reserves

bull MPLI Claims Made and Occurrence Reserves Still 5ndash7 Redundant ($14 Billionndash$20 Billion)

(09)

(09)(20)

(20) (34) (37) (20)

0

10

20

30

40

50

60

70

80

90

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

Estimated Reserve Adequacy mdash Paid Development Method

Reported Loss Ratio Projected Loss Ratio

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial

Accident-Year Loss

Ratio Redundant

30

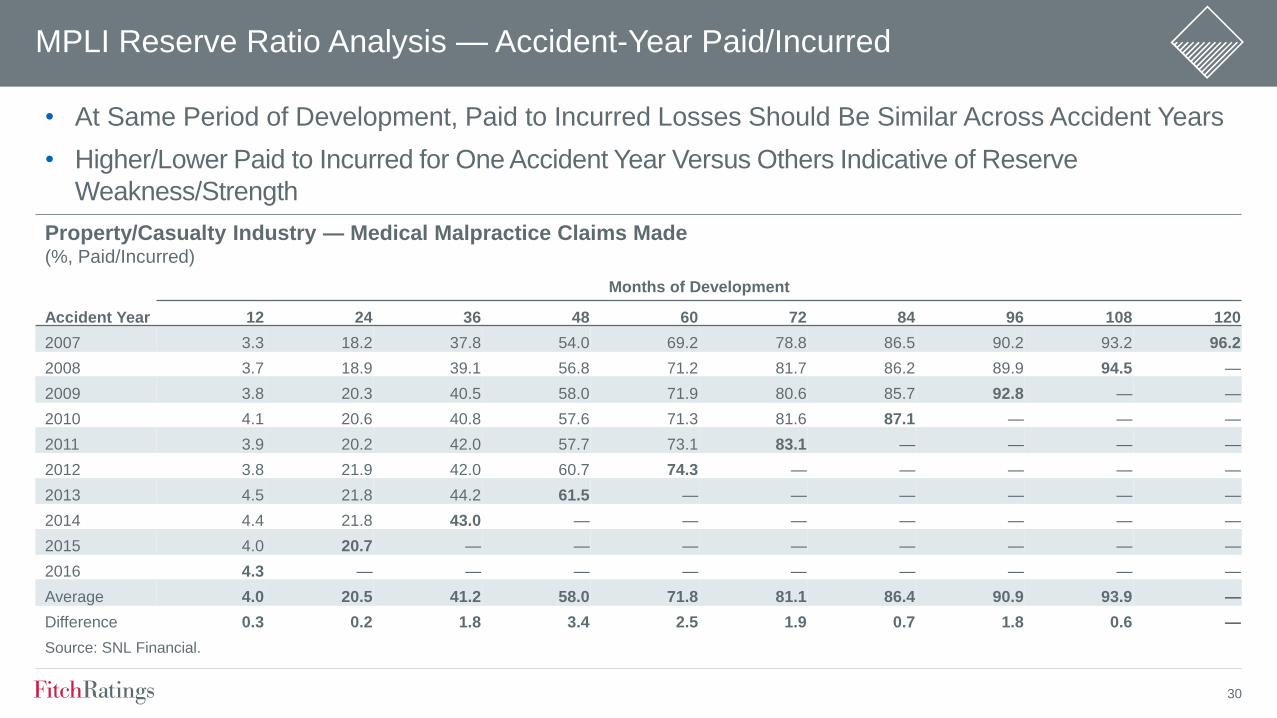

MPLI Reserve Ratio Analysis mdash Accident-Year PaidIncurred

bull At Same Period of Development Paid to Incurred Losses Should Be Similar Across Accident Years

bull HigherLower Paid to Incurred for One Accident Year Versus Others Indicative of Reserve

WeaknessStrength

PropertyCasualty Industry mdash Medical Malpractice Claims Made( PaidIncurred)

Months of Development

Accident Year 12 24 36 48 60 72 84 96 108 120

2007 33 182 378 540 692 788 865 902 932 962

2008 37 189 391 568 712 817 862 899 945 mdash

2009 38 203 405 580 719 806 857 928 mdash mdash

2010 41 206 408 576 713 816 871 mdash mdash mdash

2011 39 202 420 577 731 831 mdash mdash mdash mdash

2012 38 219 420 607 743 mdash mdash mdash mdash mdash

2013 45 218 442 615 mdash mdash mdash mdash mdash mdash

2014 44 218 430 mdash mdash mdash mdash mdash mdash mdash

2015 40 207 mdash mdash mdash mdash mdash mdash mdash mdash

2016 43 mdash mdash mdash mdash mdash mdash mdash mdash mdash

Average 40 205 412 580 718 811 864 909 939 mdash

Difference 03 02 18 34 25 19 07 18 06 mdash

Source SNL Financial

31

(50)

(40)

(30)

(20)

(10)

0

10

20

30

10 15 20 25 30 35

(PaidIncurred Losses at 24 Months )

Source SNL Financial

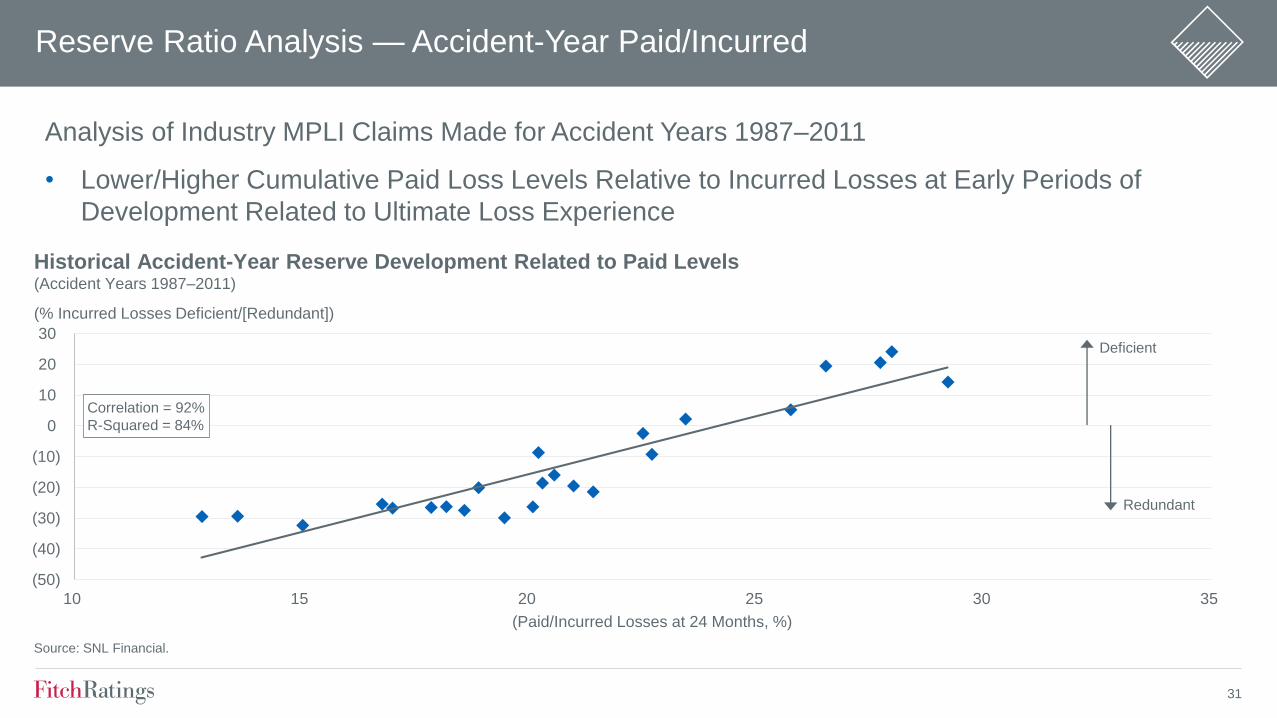

( Incurred Losses Deficient[Redundant])

Historical Accident-Year Reserve Development Related to Paid Levels(Accident Years 1987ndash2011)

Correlation = 92

R-Squared = 84

Reserve Ratio Analysis mdash Accident-Year PaidIncurred

Analysis of Industry MPLI Claims Made for Accident Years 1987ndash2011

bull LowerHigher Cumulative Paid Loss Levels Relative to Incurred Losses at Early Periods of

Development Related to Ultimate Loss Experience

Deficient

Redundant

32

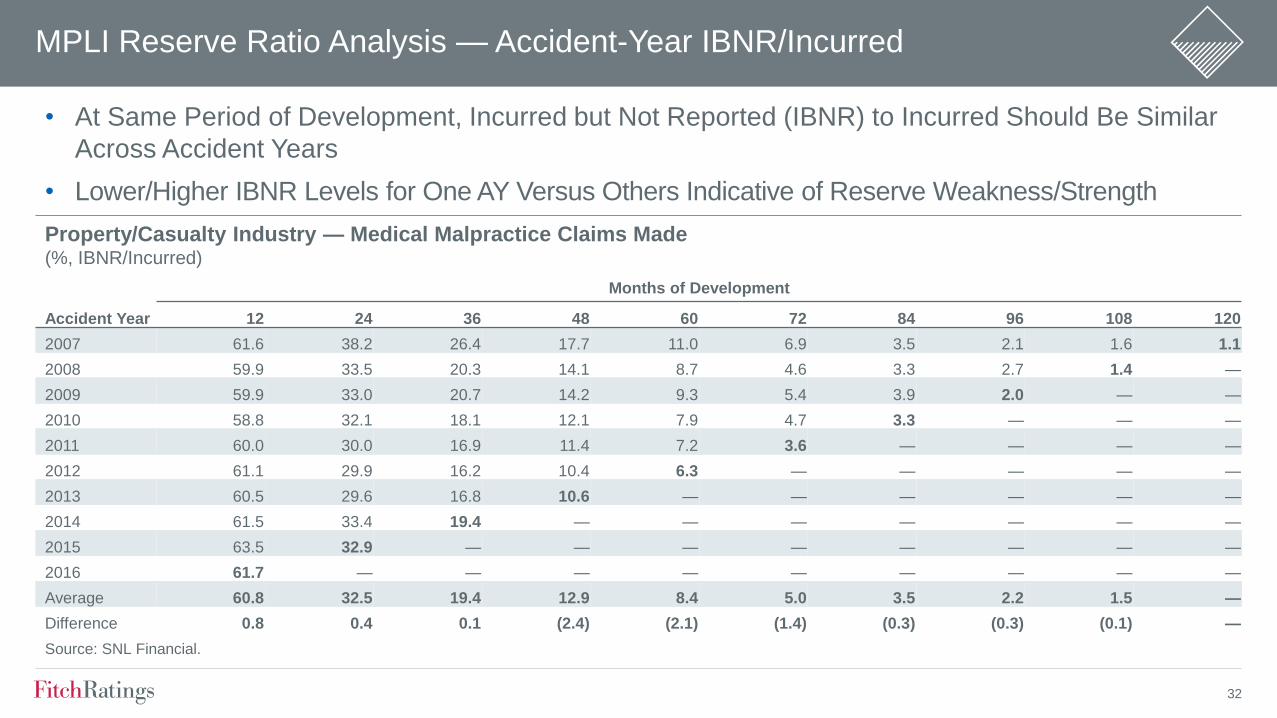

MPLI Reserve Ratio Analysis mdash Accident-Year IBNRIncurred

bull At Same Period of Development Incurred but Not Reported (IBNR) to Incurred Should Be Similar

Across Accident Years

bull LowerHigher IBNR Levels for One AY Versus Others Indicative of Reserve WeaknessStrength

PropertyCasualty Industry mdash Medical Malpractice Claims Made( IBNRIncurred)

Months of Development

Accident Year 12 24 36 48 60 72 84 96 108 120

2007 616 382 264 177 110 69 35 21 16 11

2008 599 335 203 141 87 46 33 27 14 mdash

2009 599 330 207 142 93 54 39 20 mdash mdash

2010 588 321 181 121 79 47 33 mdash mdash mdash

2011 600 300 169 114 72 36 mdash mdash mdash mdash

2012 611 299 162 104 63 mdash mdash mdash mdash mdash

2013 605 296 168 106 mdash mdash mdash mdash mdash mdash

2014 615 334 194 mdash mdash mdash mdash mdash mdash mdash

2015 635 329 mdash mdash mdash mdash mdash mdash mdash mdash

2016 617 mdash mdash mdash mdash mdash mdash mdash mdash mdash

Average 608 325 194 129 84 50 35 22 15 mdash

Difference 08 04 01 (24) (21) (14) (03) (03) (01) mdash

Source SNL Financial

33

Reserve Adequacy mdash Ratio Analysis

(40)

(30)

(20)

(10)

0

10

20

30

0 5 10 15 20 25 30 35 40 45

(IBNRIncurred Losses at 24 Months )IBNR ndash Incurred but not reported

Source SNL Financial

( Incurred Losses Deficient[Redundant])

Historical Accident-Year Reserve Development Related to IBNR Levels(Accident Years 1987ndash2011)

Correlation = (78)

R-Squared = 74

Deficient

Redundant

Analysis of Industry MPLI Claims Made for Accident Years 1987ndash2011

bull HigherLower IBNR Levels Relative to Incurred Losses at Early Periods of Development Related

to Ultimate Loss Experience

34

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS

PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK

HTTPSFITCHRATINGSCOMUNDERSTANDINGCREDITRATINGS IN ADDITION RATING

DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE

AGENCYS PUBLIC WEB SITE

AT WWWFITCHRATINGSCOM PUBLISHED RATINGS CRITERIA AND METHODOLOGIES ARE

AVAILABLE FROM THIS SITE AT ALL TIMES FITCHS CODE OF CONDUCT CONFIDENTIALITY

CONFLICTS OF INTEREST AFFILIATE FIREWALL COMPLIANCE AND OTHER RELEVANT

POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE CODE OF CONDUCT

SECTION OF THIS SITE FITCH MAY HAVE PROVIDED ANOTHER PERMISSIBLE SERVICE TO

THE RATED ENTITY OR ITS RELATED THIRD PARTIES DETAILS OF THIS SERVICE FOR

RATINGS FOR WHICH THE LEAD ANALYST IS BASED IN AN EU-REGISTERED ENTITY CAN BE

FOUND ON THE ENTITY SUMMARY PAGE FOR THIS ISSUER ON THE FITCH WEBSITE

Copyright copy 2017 by Fitch Ratings Inc Fitch Ratings Ltd and its subsidiaries 33 Whitehall Street

NY NY 10004 Telephone 1-800-753-4824 (212) 908-0500 Fax (212) 480-4435 Reproduction or

retransmission in whole or in part is prohibited except by permission All rights reserved In issuing

and maintaining its ratings and in making other reports (including forecast information) Fitch relies on

factual information it receives from issuers and underwriters and from other sources Fitch believes to

be credible Fitch conducts a reasonable investigation of the factual information relied upon by it in

accordance with its ratings methodology and obtains reasonable verification of that information from

independent sources to the extent such sources are available for a given security or in a given

jurisdiction The manner of Fitchrsquos factual investigation and the scope of the third-party verification it

obtains will vary depending on the nature of the rated security and its issuer the requirements and

practices in the jurisdiction in which the rated security is offered and sold andor the issuer is located

the availability and nature of relevant public information access to the management of the issuer and

its advisers the availability of pre-existing third-party verifications such as audit reports agreed-upon

procedures letters appraisals actuarial reports engineering reports legal opinions and other reports

provided by third parties the availability of independent and competent third-party verification sources

with respect to the particular security or in the particular jurisdiction of the issuer and a variety of

other factors Users of Fitchrsquos ratings and reports should understand that neither an enhanced factual

investigation nor any third-party verification can ensure that all of the information Fitch relies on in

connection with a rating or a report will be accurate and complete Ultimately the issuer and its

advisers are responsible for the accuracy of the information they provide to Fitch and to the market in

offering documents and other reports In issuing its ratings and its reports Fitch must rely on the work

of experts including independent auditors with respect to financial statements and attorneys with

respect to legal and tax matters Further ratings and forecasts of financial and other information are

inherently forward-looking and embody assumptions and predictions about future events that by their

nature cannot be verified as facts As a result despite any verification of current facts ratings and

forecasts can be affected by future events or conditions that were not anticipated at the time a rating

or forecast was issued or affirmed

The information in this report is provided ldquoas isrdquo without any representation or warranty of any kind

and Fitch does not represent or warrant that the report or any of its contents will meet any of the

requirements of a recipient of the report A Fitch rating is an opinion as to the creditworthiness of a

security This opinion and reports made by Fitch are based on established criteria and methodologies

that Fitch is continuously evaluating and updating Therefore ratings and reports are the collective

work product of Fitch and no individual or group of individuals is solely responsible for a rating or a

report The rating does not address the risk of loss due to risks other than credit risk unless such risk

is specifically mentioned Fitch is not engaged in the offer or sale of any security All Fitch reports

have shared authorship Individuals identified in a Fitch report were involved in but are not solely

responsible for the opinions stated therein The individuals are named for contact purposes only A

report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled

verified and presented to investors by the issuer and its agents in connection with the sale of the

securities Ratings may be changed or withdrawn at any time for any reason in the sole discretion of

Fitch Fitch does not provide investment advice of any sort Ratings are not a recommendation to buy

sell or hold any security Ratings do not comment on the adequacy of market price the suitability of

any security for a particular investor or the tax-exempt nature or taxability of payments made in

respect to any security Fitch receives fees from issuers insurers guarantors other obligors and

underwriters for rating securities Such fees generally vary from US$1000 to US$750000 (or the

applicable currency equivalent) per issue In certain cases Fitch will rate all or a number of issues

issued by a particular issuer or insured or guaranteed by a particular insurer or guarantor for a single

annual fee Such fees are expected to vary from US$10000 to US$1500000 (or the applicable

currency equivalent) The assignment publication or dissemination of a rating by Fitch shall not

constitute a consent by Fitch to use its name as an expert in connection with any registration

statement filed under the United States securities laws the Financial Services and Markets Act of

2000 of the United Kingdom or the securities laws of any particular jurisdiction Due to the relative

efficiency of electronic publishing and distribution Fitch research may be available to electronic

subscribers up to three days earlier than to print subscribers

For Australia New Zealand Taiwan and South Korea only Fitch Australia Pty Ltd holds an Australian

financial services license (AFS license no 337123) which authorizes it to provide credit ratings to

wholesale clients only Credit ratings information published by Fitch is not intended to be used by

persons who are retail clients within the meaning of the Corporations Act 2001

fitchratings

fitchratingscom

New York London33 Whitehall Street

New York NY 10004

30 North Colonnade

Canary Wharf

London E14 5GN

1

PropertyCasualty Insurer Ratings Approach

minus Fitch Rating Scale and Methodology Versus Other Agencies

minus Application of Rating Factors to MPLI Specialists

MPLI Loss Reserve Analysis

minus Key Loss Reserve Characteristics

minus Loss Reserve Analysis in Ratings Process

Agenda

2

PropertyCasualty Rating Approach1

3

Fitch 2016 White Paper

Key Conclusion A lsquoAndashrsquo Insurer Financial Strength Rating from AM Best Is Most Comparable with a

lsquoBBBrsquo IFS Rating from Fitch (as well as SampP and Moodyrsquos)

bull Corporate Mission and Scope of Coverage

‒ AM Best mdash Insurance-Focused

‒ Fitch mdash Insurance and Corporates Financial Institutions Public Finance Sovereigns Structured

Finance

bull Rating Scale Differences

‒ Best mdash lsquoAndashrsquo 4th Highest Rating of 13 ratings

‒ Fitch mdash lsquoAndashrsquo 7th Highest of 19 ratings

bull Statistical Performance Results

‒ AM Best 10-year Impairment Rate at lsquoAndashrsquo is 67

‒ Fitch 10-year Default Rate at lsquoAndashrsquo is 20 (SampP and Moodyrsquos Have Similar Results)

‒ A 67 Impairment Rate Most Closely Aligns with Fitchrsquos lsquoBBBrsquo IFS Default Rate

4

Criteria Differences mdash Areas Where AM Best Often Assigns lsquoAndashrsquo IFS Rating When Fitch Would Initially

Rate in lsquoBBBrsquo Range

bull Newly Formed (Re)insurers

bull High Country RiskLow Sovereign Ratings

bull Captives

bull Smaller-Sized Insurers

Differences in lsquoAndashrsquo Ratings

5

Qualitative Factors

bull Industry Profile and Operating Environment

bull Business Profile

bull Ownership

bull Corporate Governance

bull Management

Rating MPLI Specialists mdash Important Credit Factors

Quantitative Factors

bull Capitalization and Leverage

bull Debt Service Capabilities and Financial

Flexibility

bull Financial Performance and Earnings

bull Investment and Asset Risk

bull Reserve Adequacy

bull Reinsurance Risk Mitigation and Catastrophe

Risk

6

Business Profile

Primary Considerations MPLI Specialistsrsquo Perspective

Competitive Positioning Within Broad Market and

Primary Product Segments

Highly Focused Product Expertise Strong Market

Share in Targeted State or Region

SizeScale of Capital and Revenues Moderate SizeScale (Surplus lt $1 Bil Premiums lt

$750 Mil)

Key Business Risks and Diversification Longer Tail Historically Volatile Business mdash Limited

Diversification

Competitive Threats to Long-Term Viability and

Profitability

Business Pressures From Changes in Broader

Healthcare Market

Source Fitch Ratings

7

00

02

04

06

08

0

5

10

15

20

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

($ Bil)

MPLI Specialists Operating Leverage

PHS NWP Operating Leverage (RHS)

PHS ndash Policyholders surplus NWP ndash Net premium written Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

(x)

Capitalization and Leverage

MPLI Specialists

bull Surplus Growth and Exposure Reduction over Last Decade

bull Very Strong Capital Measures (Operating Leverage RBC Fitch Stochastic Capital Model)

bull Low Financial Leverage mdash Limited Capital Access

8

Financial Performance and Earnings

MPLI Specialists

bull Recent Deterioration in Combined Ratios Evident Following Extended Period of Strong Results

bull Calendar-Year Versus Accident-Year Combined Ratio

bull Return on Surplus Declining from Underwriting and Investment Challenges

909

785 812 800 848

912 900 902 979 990

150

100

162 165

121

103 90 85

54 46

0

3

6

9

12

15

18

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

MPLI Specialistsrsquo Financial Performance and Earnings

Combined Ratio (LHS) Return on Surplus (RHS)

Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

()

9

Rating Navigator Tool

A Visual Overview of Key Factors Considered in IFS Ratings

10

MPLI Reserve Analysis2

11

Workers Comp24

Other Liability22

Commercial Multiperil

6

Reinsurance6

MPLI4

Homeowners4

Special Property

2Other

Reserves3

Source SNL Financial

PropertyCasualty Industry Loss Reserves YE 2016(Total Industry Reserves = $621 Bil)

Private

Passenger Auto

20

Commercial Auto

5

Financial

Guaranty

Mortgage

Insurance

2Product Liability

2

MPLI mdash Reserve Characteristics

bull Represent 44 of Industry 2016 Loss

Reserves

bull More Volatile Segment Versus Other PC Lines

bull Longer-Tail Claims Liabilities

bull Large Defense Costs Component to Claims

12

MPLI mdash Underwriting and Reserve Cyclicality

(60)

(40)

(20)

0

20

40

60

80

100

120

140

()

PropertyCasualty Industry Historical Accident-Year Results

Loss Ratio Change (Original Versus Latest Reported) Latest Loss Ratio Estimate

Note MPLI claims made

Source SNL Financial

13

Reserve Characteristics Volatility

MPLI Claims Made Has Higher Underwriting and Reserve Volatility than Nearly All Major PC Segments

Private Passenger Auto WCAll Lines

Commercial AutoCMP

HO

OL OCC

Specialty LiabilityMPLI CM

OL CM

Prod Liab Occ

0

5

10

15

20

25

30

0 5 10 15 20 25 30

(Average Loss Ratio Volatility )

Average Loss Ratio Volatility Versus Reserve Volatility by Segment

WC ndash Workers compensation CMP ndash Commercial multiperil HO ndash Homeowners OL OCC ndash Other liability ndash occurrence MPLI CM ndash Medical practice liability insurance claims made OL CM ndash Other

liability ndash claims made Liab OCC ndash Liability occurrence

Source SNL Financial Fitch

()

14

bull Slower Payout Versus Most PC Segments

bull Tail Risk Higher in Workersrsquo Compensation

Reserves Characteristics mdash Claims Duration

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10

()

Loss Payment Pattern by Segment

Homeowners Workers Comp CMP MPLI CM

CMP ndash Commercial multiperil Note Propertycasualty industry aggregate

Source SNL Financial

(Years of Development)

15

bull Approximately 73 of Industry MPLI Reserves Are in Latest Four Accident Years 2013ndash2016

MPLI Reserve Composition

201624

201521

201416

201312

20128

20116

20104

20092

20082

20071 2006 and Prior

4

Source SNL Financial

Industry MPLI Reserves by Accident Year(73 of Reserves Relate to Accident-Years 2013ndash2016)

16

Large Litigation Component of MPLI Claims mdash Higher of Losses in Defense

and Cost Containment Costs

Reserve Characteristics mdash Defense Costs

0

5

10

15

20

25

30

35

MPLI CM MPLI OCC Other LiabilityCM

Other LiabilityOCC

CMP Workers Comp CommercialAuto

All Lines Personal Auto Homeowners

()

Defense and Cost Containment Costs of Total Net Incurred(Average Accident Years 2006ndash2015)

CM ndash Claims made OCC ndash Occurrence CMP ndash Commercial multiperil Note Propertycasualty industry aggregate data

Source SNL Financial

17

MPLI Reserve Analysis

bull Reserve Profile

bull Reserve Growth

bull Reserve Experience

bull Reserve Adequacy

18

Reserve Profile

Reserve Composition and Inherent Risk

bull Reserve Segment Mix and Diversification

bull Reserve Leverage

bull Reserve Risk Relative to Underwriting Risk

Implied Weighting of Reserves in Rating

Loss Reserves

Incurred Losses

Reserve Leverage

lt10 10ndash15 gt15

gt20 Medium High High

10ndash20 Medium Medium High

lt10 Low Medium Medium

19

MPLI Specialists Reserve Leverage Declining over Time with Surplus Growth

ReservesIncurred Ratio Very High mdash Implies Greater Capital Sensitivity to Reserve Changes than

Current Underwriting Period

MPLI Reserve Profile

00

05

10

15

20

25

0

3

6

9

12

15

18

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

($ Bil)

MPLI Specialists Reserve Leverage

PHS Reserves Reserve Leverage

PHS ndash Policyholders surplus Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

(x)

00

10

20

30

40

50

60

70

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)ReservesCY Incurred Reserve Leverage

CY ndash Calendar year Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

MPLI Specialists Reserve Leverage Versus Reserves

CY Incurred

20

Over Long Term an Insurerrsquos Reserves Should Grow Commensurate with Exposures

Key Ratios

bull Calendar-Year PaidCalendar-Year Incurred Losses

bull ReservesEarned Premiums (Changes over Time)

MPLI Reserve Growth

00

02

04

06

08

10

12

14

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)

Note Aggregate for a group of 35 MPLI specialists Calendar-year paid and incurred losses

Source SNL Financial

Paid gt Incurred Loss Indicative of

Reserve Weakness but Incurred

Influence by Reserve Takedowns

MPLI Specialists Reserve Growth Indications(PaidIncurred Losses)

30

31

32

33

34

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)

Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

Stable Ratio = Reserve

Changes Keeping Pace

with Premium Changes

MPLI Specialists Reserve Growth Indications(ReservesEarned Premium)

21

Key Ratios

bull Calendar Year

‒ One Year Development Prior-Year Reserves

‒ One Year Development Prior-Year Surplus

‒ One Year Development Earned Premiums

bull Accident Year

‒ Current Loss Ratio Estimate Versus Original Estimate

‒ Accident-Year Development History and Trends

MPLI Reserve Experience

22

Reserve Experience mdash Favorable MPLI Development

bull Reserve Development Still Highly Favorable but Slowing Considerably

196

237228

266

221206

245

198

166

116

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

( of Earned Premiums)

MPLI Calendar-Year Reserve Development

Note Excludes MCIC Vermont Propertycasualty industry aggregate

Source SNL Financial

Favorable

Development

23

Reserve Experience mdash Calendar-Year Development

bull MPLI Development Greatly Exceeds Other Commercial Lines Segments over Last Decade

bull Magnitude of Favorable Development in MPLI Declining

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

Commercial Auto Other Liability mdash Claims Made Other Liability mdash Occurrence MPLI mdash Claims Made Workers Compensation

() 2012 2013 2014 2015 2016

Source SNL Financial

Segment Calendar-Year Development as a of Earned Premium mdash (Favorable)Unfavorable

24

Favorable Reserve Development Slowing

(5)

0

5

10

15

20

2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003

12ndash24 Months 24ndash36 Months 36ndash48 Months

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial

( Favorable[Unfavorable])

Favorable MPLI Accident-Year Development Slowing mdash Change in Loss Ratio

25

Favorable Reserve Development Slowing

0

10

20

30

40

50

60

70

80

90

2015 2014 2013 2012 2011 2010 2009 2008 2007

()

Accident-Year Loss Ratio Changes by Time of Development

12 Months 24 Months 36 Months 48 Months 60 Months 72 Months 84 Months 96 Months 108 Months 120 Months

Note Industry aggregate MPLI claims made

Source SNL Financial

26

Accident-Year Loss Ratio

bull Claims Made Accident-Year Loss Ratio Rising

bull Will Recent Accident-Years Develop Downward Like 2003ndash2010

510 574

619 672

736 788

829 859 886 867

0

10

20

30

40

50

60

70

80

90

100

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

Accident-Year Loss and LAE Ratio(Current Loss Ratio Estimate)

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial Fitch

27

Accident-Year Loss Ratio Development

bull Recent Accident-Years Favorable Development Pattern Lagging Past Highly Redundant AYs

(27) (21)(19) (16) (9)

(5) 00 1

0

10

20

30

40

50

60

70

80

90

100

2007 2008 2009 2010 2011 2012 2013 2014 2015

()

Accident-Year Loss and LAE Ratio Development

Current LR Est Original LR Est

LR ndash Loss ratio Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial Fitch

Change Current

LR Versus Original

28

MPLI Reserve Adequacy

Key Considerations

bull Likelihood of Balance Sheet Reported Reserves to Develop HigherLower over Time

bull Stress Test Capital Impact of Potential Deficiencies

Analytical Tools

bull Project Reserve Adequacy Using Loss Development Methods (PaidCase Incurred)

bull Accident-Year Ratio Analysis

29

Reserve Adequacy mdash MPLI

bull Initial Analysis of Industry 2016 Reserves

bull MPLI Claims Made and Occurrence Reserves Still 5ndash7 Redundant ($14 Billionndash$20 Billion)

(09)

(09)(20)

(20) (34) (37) (20)

0

10

20

30

40

50

60

70

80

90

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

Estimated Reserve Adequacy mdash Paid Development Method

Reported Loss Ratio Projected Loss Ratio

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial

Accident-Year Loss

Ratio Redundant

30

MPLI Reserve Ratio Analysis mdash Accident-Year PaidIncurred

bull At Same Period of Development Paid to Incurred Losses Should Be Similar Across Accident Years

bull HigherLower Paid to Incurred for One Accident Year Versus Others Indicative of Reserve

WeaknessStrength

PropertyCasualty Industry mdash Medical Malpractice Claims Made( PaidIncurred)

Months of Development

Accident Year 12 24 36 48 60 72 84 96 108 120

2007 33 182 378 540 692 788 865 902 932 962

2008 37 189 391 568 712 817 862 899 945 mdash

2009 38 203 405 580 719 806 857 928 mdash mdash

2010 41 206 408 576 713 816 871 mdash mdash mdash

2011 39 202 420 577 731 831 mdash mdash mdash mdash

2012 38 219 420 607 743 mdash mdash mdash mdash mdash

2013 45 218 442 615 mdash mdash mdash mdash mdash mdash

2014 44 218 430 mdash mdash mdash mdash mdash mdash mdash

2015 40 207 mdash mdash mdash mdash mdash mdash mdash mdash

2016 43 mdash mdash mdash mdash mdash mdash mdash mdash mdash

Average 40 205 412 580 718 811 864 909 939 mdash

Difference 03 02 18 34 25 19 07 18 06 mdash

Source SNL Financial

31

(50)

(40)

(30)

(20)

(10)

0

10

20

30

10 15 20 25 30 35

(PaidIncurred Losses at 24 Months )

Source SNL Financial

( Incurred Losses Deficient[Redundant])

Historical Accident-Year Reserve Development Related to Paid Levels(Accident Years 1987ndash2011)

Correlation = 92

R-Squared = 84

Reserve Ratio Analysis mdash Accident-Year PaidIncurred

Analysis of Industry MPLI Claims Made for Accident Years 1987ndash2011

bull LowerHigher Cumulative Paid Loss Levels Relative to Incurred Losses at Early Periods of

Development Related to Ultimate Loss Experience

Deficient

Redundant

32

MPLI Reserve Ratio Analysis mdash Accident-Year IBNRIncurred

bull At Same Period of Development Incurred but Not Reported (IBNR) to Incurred Should Be Similar

Across Accident Years

bull LowerHigher IBNR Levels for One AY Versus Others Indicative of Reserve WeaknessStrength

PropertyCasualty Industry mdash Medical Malpractice Claims Made( IBNRIncurred)

Months of Development

Accident Year 12 24 36 48 60 72 84 96 108 120

2007 616 382 264 177 110 69 35 21 16 11

2008 599 335 203 141 87 46 33 27 14 mdash

2009 599 330 207 142 93 54 39 20 mdash mdash

2010 588 321 181 121 79 47 33 mdash mdash mdash

2011 600 300 169 114 72 36 mdash mdash mdash mdash

2012 611 299 162 104 63 mdash mdash mdash mdash mdash

2013 605 296 168 106 mdash mdash mdash mdash mdash mdash

2014 615 334 194 mdash mdash mdash mdash mdash mdash mdash

2015 635 329 mdash mdash mdash mdash mdash mdash mdash mdash

2016 617 mdash mdash mdash mdash mdash mdash mdash mdash mdash

Average 608 325 194 129 84 50 35 22 15 mdash

Difference 08 04 01 (24) (21) (14) (03) (03) (01) mdash

Source SNL Financial

33

Reserve Adequacy mdash Ratio Analysis

(40)

(30)

(20)

(10)

0

10

20

30

0 5 10 15 20 25 30 35 40 45

(IBNRIncurred Losses at 24 Months )IBNR ndash Incurred but not reported

Source SNL Financial

( Incurred Losses Deficient[Redundant])

Historical Accident-Year Reserve Development Related to IBNR Levels(Accident Years 1987ndash2011)

Correlation = (78)

R-Squared = 74

Deficient

Redundant

Analysis of Industry MPLI Claims Made for Accident Years 1987ndash2011

bull HigherLower IBNR Levels Relative to Incurred Losses at Early Periods of Development Related

to Ultimate Loss Experience

34

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS

PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK

HTTPSFITCHRATINGSCOMUNDERSTANDINGCREDITRATINGS IN ADDITION RATING

DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE

AGENCYS PUBLIC WEB SITE

AT WWWFITCHRATINGSCOM PUBLISHED RATINGS CRITERIA AND METHODOLOGIES ARE

AVAILABLE FROM THIS SITE AT ALL TIMES FITCHS CODE OF CONDUCT CONFIDENTIALITY

CONFLICTS OF INTEREST AFFILIATE FIREWALL COMPLIANCE AND OTHER RELEVANT

POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE CODE OF CONDUCT

SECTION OF THIS SITE FITCH MAY HAVE PROVIDED ANOTHER PERMISSIBLE SERVICE TO

THE RATED ENTITY OR ITS RELATED THIRD PARTIES DETAILS OF THIS SERVICE FOR

RATINGS FOR WHICH THE LEAD ANALYST IS BASED IN AN EU-REGISTERED ENTITY CAN BE

FOUND ON THE ENTITY SUMMARY PAGE FOR THIS ISSUER ON THE FITCH WEBSITE

Copyright copy 2017 by Fitch Ratings Inc Fitch Ratings Ltd and its subsidiaries 33 Whitehall Street

NY NY 10004 Telephone 1-800-753-4824 (212) 908-0500 Fax (212) 480-4435 Reproduction or

retransmission in whole or in part is prohibited except by permission All rights reserved In issuing

and maintaining its ratings and in making other reports (including forecast information) Fitch relies on

factual information it receives from issuers and underwriters and from other sources Fitch believes to

be credible Fitch conducts a reasonable investigation of the factual information relied upon by it in

accordance with its ratings methodology and obtains reasonable verification of that information from

independent sources to the extent such sources are available for a given security or in a given

jurisdiction The manner of Fitchrsquos factual investigation and the scope of the third-party verification it

obtains will vary depending on the nature of the rated security and its issuer the requirements and

practices in the jurisdiction in which the rated security is offered and sold andor the issuer is located

the availability and nature of relevant public information access to the management of the issuer and

its advisers the availability of pre-existing third-party verifications such as audit reports agreed-upon

procedures letters appraisals actuarial reports engineering reports legal opinions and other reports

provided by third parties the availability of independent and competent third-party verification sources

with respect to the particular security or in the particular jurisdiction of the issuer and a variety of

other factors Users of Fitchrsquos ratings and reports should understand that neither an enhanced factual

investigation nor any third-party verification can ensure that all of the information Fitch relies on in

connection with a rating or a report will be accurate and complete Ultimately the issuer and its

advisers are responsible for the accuracy of the information they provide to Fitch and to the market in

offering documents and other reports In issuing its ratings and its reports Fitch must rely on the work

of experts including independent auditors with respect to financial statements and attorneys with

respect to legal and tax matters Further ratings and forecasts of financial and other information are

inherently forward-looking and embody assumptions and predictions about future events that by their

nature cannot be verified as facts As a result despite any verification of current facts ratings and

forecasts can be affected by future events or conditions that were not anticipated at the time a rating

or forecast was issued or affirmed

The information in this report is provided ldquoas isrdquo without any representation or warranty of any kind

and Fitch does not represent or warrant that the report or any of its contents will meet any of the

requirements of a recipient of the report A Fitch rating is an opinion as to the creditworthiness of a

security This opinion and reports made by Fitch are based on established criteria and methodologies

that Fitch is continuously evaluating and updating Therefore ratings and reports are the collective

work product of Fitch and no individual or group of individuals is solely responsible for a rating or a

report The rating does not address the risk of loss due to risks other than credit risk unless such risk

is specifically mentioned Fitch is not engaged in the offer or sale of any security All Fitch reports

have shared authorship Individuals identified in a Fitch report were involved in but are not solely

responsible for the opinions stated therein The individuals are named for contact purposes only A

report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled

verified and presented to investors by the issuer and its agents in connection with the sale of the

securities Ratings may be changed or withdrawn at any time for any reason in the sole discretion of

Fitch Fitch does not provide investment advice of any sort Ratings are not a recommendation to buy

sell or hold any security Ratings do not comment on the adequacy of market price the suitability of

any security for a particular investor or the tax-exempt nature or taxability of payments made in

respect to any security Fitch receives fees from issuers insurers guarantors other obligors and

underwriters for rating securities Such fees generally vary from US$1000 to US$750000 (or the

applicable currency equivalent) per issue In certain cases Fitch will rate all or a number of issues

issued by a particular issuer or insured or guaranteed by a particular insurer or guarantor for a single

annual fee Such fees are expected to vary from US$10000 to US$1500000 (or the applicable

currency equivalent) The assignment publication or dissemination of a rating by Fitch shall not

constitute a consent by Fitch to use its name as an expert in connection with any registration

statement filed under the United States securities laws the Financial Services and Markets Act of

2000 of the United Kingdom or the securities laws of any particular jurisdiction Due to the relative

efficiency of electronic publishing and distribution Fitch research may be available to electronic

subscribers up to three days earlier than to print subscribers

For Australia New Zealand Taiwan and South Korea only Fitch Australia Pty Ltd holds an Australian

financial services license (AFS license no 337123) which authorizes it to provide credit ratings to

wholesale clients only Credit ratings information published by Fitch is not intended to be used by

persons who are retail clients within the meaning of the Corporations Act 2001

fitchratings

fitchratingscom

New York London33 Whitehall Street

New York NY 10004

30 North Colonnade

Canary Wharf

London E14 5GN

2

PropertyCasualty Rating Approach1

3

Fitch 2016 White Paper

Key Conclusion A lsquoAndashrsquo Insurer Financial Strength Rating from AM Best Is Most Comparable with a

lsquoBBBrsquo IFS Rating from Fitch (as well as SampP and Moodyrsquos)

bull Corporate Mission and Scope of Coverage

‒ AM Best mdash Insurance-Focused

‒ Fitch mdash Insurance and Corporates Financial Institutions Public Finance Sovereigns Structured

Finance

bull Rating Scale Differences

‒ Best mdash lsquoAndashrsquo 4th Highest Rating of 13 ratings

‒ Fitch mdash lsquoAndashrsquo 7th Highest of 19 ratings

bull Statistical Performance Results

‒ AM Best 10-year Impairment Rate at lsquoAndashrsquo is 67

‒ Fitch 10-year Default Rate at lsquoAndashrsquo is 20 (SampP and Moodyrsquos Have Similar Results)

‒ A 67 Impairment Rate Most Closely Aligns with Fitchrsquos lsquoBBBrsquo IFS Default Rate

4

Criteria Differences mdash Areas Where AM Best Often Assigns lsquoAndashrsquo IFS Rating When Fitch Would Initially

Rate in lsquoBBBrsquo Range

bull Newly Formed (Re)insurers

bull High Country RiskLow Sovereign Ratings

bull Captives

bull Smaller-Sized Insurers

Differences in lsquoAndashrsquo Ratings

5

Qualitative Factors

bull Industry Profile and Operating Environment

bull Business Profile

bull Ownership

bull Corporate Governance

bull Management

Rating MPLI Specialists mdash Important Credit Factors

Quantitative Factors

bull Capitalization and Leverage

bull Debt Service Capabilities and Financial

Flexibility

bull Financial Performance and Earnings

bull Investment and Asset Risk

bull Reserve Adequacy

bull Reinsurance Risk Mitigation and Catastrophe

Risk

6

Business Profile

Primary Considerations MPLI Specialistsrsquo Perspective

Competitive Positioning Within Broad Market and

Primary Product Segments

Highly Focused Product Expertise Strong Market

Share in Targeted State or Region

SizeScale of Capital and Revenues Moderate SizeScale (Surplus lt $1 Bil Premiums lt

$750 Mil)

Key Business Risks and Diversification Longer Tail Historically Volatile Business mdash Limited

Diversification

Competitive Threats to Long-Term Viability and

Profitability

Business Pressures From Changes in Broader

Healthcare Market

Source Fitch Ratings

7

00

02

04

06

08

0

5

10

15

20

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

($ Bil)

MPLI Specialists Operating Leverage

PHS NWP Operating Leverage (RHS)

PHS ndash Policyholders surplus NWP ndash Net premium written Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

(x)

Capitalization and Leverage

MPLI Specialists

bull Surplus Growth and Exposure Reduction over Last Decade

bull Very Strong Capital Measures (Operating Leverage RBC Fitch Stochastic Capital Model)

bull Low Financial Leverage mdash Limited Capital Access

8

Financial Performance and Earnings

MPLI Specialists

bull Recent Deterioration in Combined Ratios Evident Following Extended Period of Strong Results

bull Calendar-Year Versus Accident-Year Combined Ratio

bull Return on Surplus Declining from Underwriting and Investment Challenges

909

785 812 800 848

912 900 902 979 990

150

100

162 165

121

103 90 85

54 46

0

3

6

9

12

15

18

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

MPLI Specialistsrsquo Financial Performance and Earnings

Combined Ratio (LHS) Return on Surplus (RHS)

Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

()

9

Rating Navigator Tool

A Visual Overview of Key Factors Considered in IFS Ratings

10

MPLI Reserve Analysis2

11

Workers Comp24

Other Liability22

Commercial Multiperil

6

Reinsurance6

MPLI4

Homeowners4

Special Property

2Other

Reserves3

Source SNL Financial

PropertyCasualty Industry Loss Reserves YE 2016(Total Industry Reserves = $621 Bil)

Private

Passenger Auto

20

Commercial Auto

5

Financial

Guaranty

Mortgage

Insurance

2Product Liability

2

MPLI mdash Reserve Characteristics

bull Represent 44 of Industry 2016 Loss

Reserves

bull More Volatile Segment Versus Other PC Lines

bull Longer-Tail Claims Liabilities

bull Large Defense Costs Component to Claims

12

MPLI mdash Underwriting and Reserve Cyclicality

(60)

(40)

(20)

0

20

40

60

80

100

120

140

()

PropertyCasualty Industry Historical Accident-Year Results

Loss Ratio Change (Original Versus Latest Reported) Latest Loss Ratio Estimate

Note MPLI claims made

Source SNL Financial

13

Reserve Characteristics Volatility

MPLI Claims Made Has Higher Underwriting and Reserve Volatility than Nearly All Major PC Segments

Private Passenger Auto WCAll Lines

Commercial AutoCMP

HO

OL OCC

Specialty LiabilityMPLI CM

OL CM

Prod Liab Occ

0

5

10

15

20

25

30

0 5 10 15 20 25 30

(Average Loss Ratio Volatility )

Average Loss Ratio Volatility Versus Reserve Volatility by Segment

WC ndash Workers compensation CMP ndash Commercial multiperil HO ndash Homeowners OL OCC ndash Other liability ndash occurrence MPLI CM ndash Medical practice liability insurance claims made OL CM ndash Other

liability ndash claims made Liab OCC ndash Liability occurrence

Source SNL Financial Fitch

()

14

bull Slower Payout Versus Most PC Segments

bull Tail Risk Higher in Workersrsquo Compensation

Reserves Characteristics mdash Claims Duration

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10

()

Loss Payment Pattern by Segment

Homeowners Workers Comp CMP MPLI CM

CMP ndash Commercial multiperil Note Propertycasualty industry aggregate

Source SNL Financial

(Years of Development)

15

bull Approximately 73 of Industry MPLI Reserves Are in Latest Four Accident Years 2013ndash2016

MPLI Reserve Composition

201624

201521

201416

201312

20128

20116

20104

20092

20082

20071 2006 and Prior

4

Source SNL Financial

Industry MPLI Reserves by Accident Year(73 of Reserves Relate to Accident-Years 2013ndash2016)

16

Large Litigation Component of MPLI Claims mdash Higher of Losses in Defense

and Cost Containment Costs

Reserve Characteristics mdash Defense Costs

0

5

10

15

20

25

30

35

MPLI CM MPLI OCC Other LiabilityCM

Other LiabilityOCC

CMP Workers Comp CommercialAuto

All Lines Personal Auto Homeowners

()

Defense and Cost Containment Costs of Total Net Incurred(Average Accident Years 2006ndash2015)

CM ndash Claims made OCC ndash Occurrence CMP ndash Commercial multiperil Note Propertycasualty industry aggregate data

Source SNL Financial

17

MPLI Reserve Analysis

bull Reserve Profile

bull Reserve Growth

bull Reserve Experience

bull Reserve Adequacy

18

Reserve Profile

Reserve Composition and Inherent Risk

bull Reserve Segment Mix and Diversification

bull Reserve Leverage

bull Reserve Risk Relative to Underwriting Risk

Implied Weighting of Reserves in Rating

Loss Reserves

Incurred Losses

Reserve Leverage

lt10 10ndash15 gt15

gt20 Medium High High

10ndash20 Medium Medium High

lt10 Low Medium Medium

19

MPLI Specialists Reserve Leverage Declining over Time with Surplus Growth

ReservesIncurred Ratio Very High mdash Implies Greater Capital Sensitivity to Reserve Changes than

Current Underwriting Period

MPLI Reserve Profile

00

05

10

15

20

25

0

3

6

9

12

15

18

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

($ Bil)

MPLI Specialists Reserve Leverage

PHS Reserves Reserve Leverage

PHS ndash Policyholders surplus Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

(x)

00

10

20

30

40

50

60

70

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)ReservesCY Incurred Reserve Leverage

CY ndash Calendar year Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

MPLI Specialists Reserve Leverage Versus Reserves

CY Incurred

20

Over Long Term an Insurerrsquos Reserves Should Grow Commensurate with Exposures

Key Ratios

bull Calendar-Year PaidCalendar-Year Incurred Losses

bull ReservesEarned Premiums (Changes over Time)

MPLI Reserve Growth

00

02

04

06

08

10

12

14

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)

Note Aggregate for a group of 35 MPLI specialists Calendar-year paid and incurred losses

Source SNL Financial

Paid gt Incurred Loss Indicative of

Reserve Weakness but Incurred

Influence by Reserve Takedowns

MPLI Specialists Reserve Growth Indications(PaidIncurred Losses)

30

31

32

33

34

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(x)

Note Aggregate for a group of 35 MPLI specialists

Source SNL Financial

Stable Ratio = Reserve

Changes Keeping Pace

with Premium Changes

MPLI Specialists Reserve Growth Indications(ReservesEarned Premium)

21

Key Ratios

bull Calendar Year

‒ One Year Development Prior-Year Reserves

‒ One Year Development Prior-Year Surplus

‒ One Year Development Earned Premiums

bull Accident Year

‒ Current Loss Ratio Estimate Versus Original Estimate

‒ Accident-Year Development History and Trends

MPLI Reserve Experience

22

Reserve Experience mdash Favorable MPLI Development

bull Reserve Development Still Highly Favorable but Slowing Considerably

196

237228

266

221206

245

198

166

116

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

( of Earned Premiums)

MPLI Calendar-Year Reserve Development

Note Excludes MCIC Vermont Propertycasualty industry aggregate

Source SNL Financial

Favorable

Development

23

Reserve Experience mdash Calendar-Year Development

bull MPLI Development Greatly Exceeds Other Commercial Lines Segments over Last Decade

bull Magnitude of Favorable Development in MPLI Declining

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

Commercial Auto Other Liability mdash Claims Made Other Liability mdash Occurrence MPLI mdash Claims Made Workers Compensation

() 2012 2013 2014 2015 2016

Source SNL Financial

Segment Calendar-Year Development as a of Earned Premium mdash (Favorable)Unfavorable

24

Favorable Reserve Development Slowing

(5)

0

5

10

15

20

2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003

12ndash24 Months 24ndash36 Months 36ndash48 Months

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial

( Favorable[Unfavorable])

Favorable MPLI Accident-Year Development Slowing mdash Change in Loss Ratio

25

Favorable Reserve Development Slowing

0

10

20

30

40

50

60

70

80

90

2015 2014 2013 2012 2011 2010 2009 2008 2007

()

Accident-Year Loss Ratio Changes by Time of Development

12 Months 24 Months 36 Months 48 Months 60 Months 72 Months 84 Months 96 Months 108 Months 120 Months

Note Industry aggregate MPLI claims made

Source SNL Financial

26

Accident-Year Loss Ratio

bull Claims Made Accident-Year Loss Ratio Rising

bull Will Recent Accident-Years Develop Downward Like 2003ndash2010

510 574

619 672

736 788

829 859 886 867

0

10

20

30

40

50

60

70

80

90

100

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

Accident-Year Loss and LAE Ratio(Current Loss Ratio Estimate)

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial Fitch

27

Accident-Year Loss Ratio Development

bull Recent Accident-Years Favorable Development Pattern Lagging Past Highly Redundant AYs

(27) (21)(19) (16) (9)

(5) 00 1

0

10

20

30

40

50

60

70

80

90

100

2007 2008 2009 2010 2011 2012 2013 2014 2015

()

Accident-Year Loss and LAE Ratio Development

Current LR Est Original LR Est

LR ndash Loss ratio Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial Fitch

Change Current

LR Versus Original

28

MPLI Reserve Adequacy

Key Considerations

bull Likelihood of Balance Sheet Reported Reserves to Develop HigherLower over Time

bull Stress Test Capital Impact of Potential Deficiencies

Analytical Tools

bull Project Reserve Adequacy Using Loss Development Methods (PaidCase Incurred)

bull Accident-Year Ratio Analysis

29

Reserve Adequacy mdash MPLI

bull Initial Analysis of Industry 2016 Reserves

bull MPLI Claims Made and Occurrence Reserves Still 5ndash7 Redundant ($14 Billionndash$20 Billion)

(09)

(09)(20)

(20) (34) (37) (20)

0

10

20

30

40

50

60

70

80

90

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

()

Estimated Reserve Adequacy mdash Paid Development Method

Reported Loss Ratio Projected Loss Ratio

Note Propertycasualty industry aggregate MPLI claims made

Source SNL Financial

Accident-Year Loss

Ratio Redundant

30

MPLI Reserve Ratio Analysis mdash Accident-Year PaidIncurred

bull At Same Period of Development Paid to Incurred Losses Should Be Similar Across Accident Years

bull HigherLower Paid to Incurred for One Accident Year Versus Others Indicative of Reserve

WeaknessStrength

PropertyCasualty Industry mdash Medical Malpractice Claims Made( PaidIncurred)

Months of Development

Accident Year 12 24 36 48 60 72 84 96 108 120

2007 33 182 378 540 692 788 865 902 932 962

2008 37 189 391 568 712 817 862 899 945 mdash

2009 38 203 405 580 719 806 857 928 mdash mdash

2010 41 206 408 576 713 816 871 mdash mdash mdash

2011 39 202 420 577 731 831 mdash mdash mdash mdash

2012 38 219 420 607 743 mdash mdash mdash mdash mdash

2013 45 218 442 615 mdash mdash mdash mdash mdash mdash

2014 44 218 430 mdash mdash mdash mdash mdash mdash mdash

2015 40 207 mdash mdash mdash mdash mdash mdash mdash mdash

2016 43 mdash mdash mdash mdash mdash mdash mdash mdash mdash

Average 40 205 412 580 718 811 864 909 939 mdash

Difference 03 02 18 34 25 19 07 18 06 mdash

Source SNL Financial

31

(50)

(40)

(30)

(20)

(10)

0

10

20

30

10 15 20 25 30 35

(PaidIncurred Losses at 24 Months )

Source SNL Financial

( Incurred Losses Deficient[Redundant])

Historical Accident-Year Reserve Development Related to Paid Levels(Accident Years 1987ndash2011)

Correlation = 92

R-Squared = 84

Reserve Ratio Analysis mdash Accident-Year PaidIncurred

Analysis of Industry MPLI Claims Made for Accident Years 1987ndash2011

bull LowerHigher Cumulative Paid Loss Levels Relative to Incurred Losses at Early Periods of

Development Related to Ultimate Loss Experience

Deficient

Redundant

32

MPLI Reserve Ratio Analysis mdash Accident-Year IBNRIncurred

bull At Same Period of Development Incurred but Not Reported (IBNR) to Incurred Should Be Similar

Across Accident Years

bull LowerHigher IBNR Levels for One AY Versus Others Indicative of Reserve WeaknessStrength

PropertyCasualty Industry mdash Medical Malpractice Claims Made( IBNRIncurred)

Months of Development

Accident Year 12 24 36 48 60 72 84 96 108 120

2007 616 382 264 177 110 69 35 21 16 11

2008 599 335 203 141 87 46 33 27 14 mdash

2009 599 330 207 142 93 54 39 20 mdash mdash

2010 588 321 181 121 79 47 33 mdash mdash mdash

2011 600 300 169 114 72 36 mdash mdash mdash mdash

2012 611 299 162 104 63 mdash mdash mdash mdash mdash

2013 605 296 168 106 mdash mdash mdash mdash mdash mdash

2014 615 334 194 mdash mdash mdash mdash mdash mdash mdash

2015 635 329 mdash mdash mdash mdash mdash mdash mdash mdash

2016 617 mdash mdash mdash mdash mdash mdash mdash mdash mdash

Average 608 325 194 129 84 50 35 22 15 mdash

Difference 08 04 01 (24) (21) (14) (03) (03) (01) mdash

Source SNL Financial

33

Reserve Adequacy mdash Ratio Analysis

(40)

(30)

(20)

(10)

0

10

20

30

0 5 10 15 20 25 30 35 40 45

(IBNRIncurred Losses at 24 Months )IBNR ndash Incurred but not reported

Source SNL Financial

( Incurred Losses Deficient[Redundant])

Historical Accident-Year Reserve Development Related to IBNR Levels(Accident Years 1987ndash2011)

Correlation = (78)

R-Squared = 74

Deficient

Redundant

Analysis of Industry MPLI Claims Made for Accident Years 1987ndash2011

bull HigherLower IBNR Levels Relative to Incurred Losses at Early Periods of Development Related

to Ultimate Loss Experience

34

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS

PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK

HTTPSFITCHRATINGSCOMUNDERSTANDINGCREDITRATINGS IN ADDITION RATING

DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE

AGENCYS PUBLIC WEB SITE

AT WWWFITCHRATINGSCOM PUBLISHED RATINGS CRITERIA AND METHODOLOGIES ARE

AVAILABLE FROM THIS SITE AT ALL TIMES FITCHS CODE OF CONDUCT CONFIDENTIALITY

CONFLICTS OF INTEREST AFFILIATE FIREWALL COMPLIANCE AND OTHER RELEVANT

POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE CODE OF CONDUCT

SECTION OF THIS SITE FITCH MAY HAVE PROVIDED ANOTHER PERMISSIBLE SERVICE TO

THE RATED ENTITY OR ITS RELATED THIRD PARTIES DETAILS OF THIS SERVICE FOR

RATINGS FOR WHICH THE LEAD ANALYST IS BASED IN AN EU-REGISTERED ENTITY CAN BE

FOUND ON THE ENTITY SUMMARY PAGE FOR THIS ISSUER ON THE FITCH WEBSITE

Copyright copy 2017 by Fitch Ratings Inc Fitch Ratings Ltd and its subsidiaries 33 Whitehall Street

NY NY 10004 Telephone 1-800-753-4824 (212) 908-0500 Fax (212) 480-4435 Reproduction or

retransmission in whole or in part is prohibited except by permission All rights reserved In issuing

and maintaining its ratings and in making other reports (including forecast information) Fitch relies on

factual information it receives from issuers and underwriters and from other sources Fitch believes to

be credible Fitch conducts a reasonable investigation of the factual information relied upon by it in

accordance with its ratings methodology and obtains reasonable verification of that information from

independent sources to the extent such sources are available for a given security or in a given

jurisdiction The manner of Fitchrsquos factual investigation and the scope of the third-party verification it

obtains will vary depending on the nature of the rated security and its issuer the requirements and

practices in the jurisdiction in which the rated security is offered and sold andor the issuer is located

the availability and nature of relevant public information access to the management of the issuer and

its advisers the availability of pre-existing third-party verifications such as audit reports agreed-upon

procedures letters appraisals actuarial reports engineering reports legal opinions and other reports

provided by third parties the availability of independent and competent third-party verification sources

with respect to the particular security or in the particular jurisdiction of the issuer and a variety of

other factors Users of Fitchrsquos ratings and reports should understand that neither an enhanced factual

investigation nor any third-party verification can ensure that all of the information Fitch relies on in

connection with a rating or a report will be accurate and complete Ultimately the issuer and its

advisers are responsible for the accuracy of the information they provide to Fitch and to the market in

offering documents and other reports In issuing its ratings and its reports Fitch must rely on the work

of experts including independent auditors with respect to financial statements and attorneys with

respect to legal and tax matters Further ratings and forecasts of financial and other information are

inherently forward-looking and embody assumptions and predictions about future events that by their

nature cannot be verified as facts As a result despite any verification of current facts ratings and

forecasts can be affected by future events or conditions that were not anticipated at the time a rating

or forecast was issued or affirmed

The information in this report is provided ldquoas isrdquo without any representation or warranty of any kind

and Fitch does not represent or warrant that the report or any of its contents will meet any of the

requirements of a recipient of the report A Fitch rating is an opinion as to the creditworthiness of a

security This opinion and reports made by Fitch are based on established criteria and methodologies

that Fitch is continuously evaluating and updating Therefore ratings and reports are the collective

work product of Fitch and no individual or group of individuals is solely responsible for a rating or a

report The rating does not address the risk of loss due to risks other than credit risk unless such risk

is specifically mentioned Fitch is not engaged in the offer or sale of any security All Fitch reports

have shared authorship Individuals identified in a Fitch report were involved in but are not solely

responsible for the opinions stated therein The individuals are named for contact purposes only A

report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled

verified and presented to investors by the issuer and its agents in connection with the sale of the

securities Ratings may be changed or withdrawn at any time for any reason in the sole discretion of

Fitch Fitch does not provide investment advice of any sort Ratings are not a recommendation to buy

sell or hold any security Ratings do not comment on the adequacy of market price the suitability of

any security for a particular investor or the tax-exempt nature or taxability of payments made in

respect to any security Fitch receives fees from issuers insurers guarantors other obligors and

underwriters for rating securities Such fees generally vary from US$1000 to US$750000 (or the

applicable currency equivalent) per issue In certain cases Fitch will rate all or a number of issues

issued by a particular issuer or insured or guaranteed by a particular insurer or guarantor for a single

annual fee Such fees are expected to vary from US$10000 to US$1500000 (or the applicable

currency equivalent) The assignment publication or dissemination of a rating by Fitch shall not

constitute a consent by Fitch to use its name as an expert in connection with any registration

statement filed under the United States securities laws the Financial Services and Markets Act of

2000 of the United Kingdom or the securities laws of any particular jurisdiction Due to the relative

efficiency of electronic publishing and distribution Fitch research may be available to electronic

subscribers up to three days earlier than to print subscribers

For Australia New Zealand Taiwan and South Korea only Fitch Australia Pty Ltd holds an Australian

financial services license (AFS license no 337123) which authorizes it to provide credit ratings to

wholesale clients only Credit ratings information published by Fitch is not intended to be used by

persons who are retail clients within the meaning of the Corporations Act 2001

fitchratings

fitchratingscom

New York London33 Whitehall Street

New York NY 10004

30 North Colonnade

Canary Wharf

London E14 5GN

3

Fitch 2016 White Paper

Key Conclusion A lsquoAndashrsquo Insurer Financial Strength Rating from AM Best Is Most Comparable with a