rap afrique nord vincent - african development bank · the 2011 african development bank annual...

TRANSCRIPT

Concept

Note

s

Youth, Employment Creation and Shared Growth in AfricaPowering Africa: Financing Energy and Green Growth Private Sector Development and Domestic Resource Mobilization Africa – Innovation Hub for Growth

Agenda for Inclusive

Concept Notes

Growth in Africa

Towards an

Annual Meetings PORTUGAL 2011

African Development Bank Group The Chief Economist’s Office

Agenda for Inclusive

Concept Notes

Growth in Africa

Youth, Employment Creation and Shared Growth in AfricaPowering Africa: Financing Energy and Green Growth Private Sector Development and Domestic Resource Mobilization Africa – Innovation Hub for Growth

Towards an

3

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

Table of Content

5 Preface7 Introduction

11 HIGH LEVEL SEMINAR I Youth, Employment Creation and Shared Growth in Africa

13 1 Introduction14 2 Youth Unemployment in Africa: Nature and Causes19 3 Promoting Employment and Decent Jobs: Issues for Policy22 4 The Role of the African Development Bank23 5 Issues for Discussion

25 HIGH LEVEL SEMINAR II Powering Africa: Financing Energyand Green Growth

27 1 Introduction28 2 The Power Sector: Challenges and Opportunities30 3 Public and private finance sources33 4 The Role of the African Development Bank and other MDB’s35 5 Conclusion

37 HIGH LEVEL SEMINAR III Private Sector Development and Domestic Resource Mobilization

39 1 Introduction41 2 Strengthening Public Resource Mobilisation in Africa45 3 Developing Private Sector Resource Mobilization51 4 The Role of the African Development Bank53 5 Issues for Discussion

55 HIGH LEVEL SEMINAR IV Africa – Innovation Hub for Growth

57 1 Introduction58 2 Innovation as a Driver of Growth61 3 Innovation for Growth: Challenges in Africa64 4 Conclusion64 5 Issues for Discussion

5

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

Preface

This year, the Annual Meetings Seminars of the AfricanDevelopment Bank Group will once again be a unique

occasion to bring together policy makers and thoughtleaders from around the globe to interact on keydevelopment challenges and opportunities of thecontinent. Facilitating such exchanges is an importantaspect of the catalytic role the “Knowledge Bank” isplaying in assisting African countries sustain theireconomic growth and create stable environment fordevelopment. I am pleased to present to you the conceptnotes on the four High-Level Seminars to be held on 8June 2011, around the main theme: “Towards an Agendafor Inclusive Growth in Africa”.

The theme illustrates the fact that the economic growthof the past decade has not been shared widely in mostof countries across the continent. The recent wave ofsocial upheaval in North Africa calling for more inclusivegrowth, more accountability and better politicalgovernance has been partly the result of a growth processthat failed to generate adequate jobs and opportunitiesfor the large part of the countries’ labor force.

The topics of the four High-Level Seminars have beencarefully selected to capture the challenges facing Africain terms of setting an agenda that brings about inclusivegrowth capable of generating adequate jobs andopportunities for the large part of the country’s labor forceand to bite deeply into poverty.

The first seminar on “Youth, Employment Creation andShared Growth in Africa” will capture the fundamentalquestion of how to enhance growth and promoteemployment and decent jobs in Africa and will addressthe issues involved by examining the nature and causesof youth unemployment and highlights some policy areastowards addressing the problem.

The second seminar on “Powering Africa: FinancingEnergy, Green Growth and Climate Change” will explorethe challenges and opportunities of the Power Sector inAfrica. It will discuss innovative financing mechanismsdesigned to raise additional funds, and ways to optimizeboth private and public financing methods. Finally, it willexamine the role of multilateral development bank andother international financial institutions that, in addition toapplying their own financing mechanisms, can facilitatelarge-scale regional energy projects and help raise Africa’sinfluence and voice in the allocation, administration andabsorption of global climate-related resources.

The third seminar on “Private Sector Development andDomestic Resource Mobilization” will highlight the relevantissues involved in the mobilization of both domestic publicand private resources in Africa. The issues involved will beaddressed by examining the current state of domesticresource mobilization, the challenges and prospects.

The fourth seminar on “Africa – Innovation Hub for Growth”will aim at stimulating the debate and inspire thoughts onpractical strategies for implementing innovation policiesfor growth in Africa. It also will position innovation as acatalyst for developing African countries and offers insightsinto the opportunities for regional innovation strategies.

The unique opportunity offered by these High-LevelSeminars to engage with government officials, thoughtleaders, private sector entrepreneurs, civil society anddevelopment partners is valued and welcome by the Bank.

I look forward to welcoming you at the seminars.Thank you.

Prof. Mthuli NcubeChief Economist and Vice President, AfDB

6

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

7

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

7

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

Introduction

African economies have emerged from the crisis andeconomic expansion is expected to continue, albeit

at a somewhat lower speed than before the global crisis.Growth reached 4.8 percent in 2010, up from 3% in 2009and is likely to accelerate to more than 5% in 2011 and2012. In the four years before the global financial crisis,the continent´s growth was on average 6%.

The economic resurgence is most pronounced inresource-rich countries that benefit from the revival incommodity demand, oil and non-oilcommodity prices, and trade. Oil exportingcountries are expected to enjoy a robusteconomic expansion with GDP growth ofaround 7 percent in both 2011 and 2012.Non-oil but commodity exporters are alsolikely to show robust growth of above 6%in 2011 as gains from high export pricesand volumes offset losses from higher oiland food import bills. However, severalAfrican countries have to cope not only withhigher food and oil bills, but also withpolitical instability and social unrest and thisis bound to reduce their growth in 2011.

Thanks to economic reforms, improvedgovernance and prudent fiscal policies,inflation in Africa fell to 7 percent in 2010 –from an average of 10% in 2009– and isexpected to remain at around this level in2011 and 2012. The growth has beenstrong, and over the last decade, thecontinent was ranked the third fastestgrowing region after Asia and the Middle East. This trendmight, however, be reversed if food and fuel pricescontinue their recent hike.

Finally, it is worth mentioning that the continent has showna remarkable resilience to the global financial crisis. While

in many other regions growth levels have declinedfollowing the crisis, growth in Africa remained positiveand Africa has emerged from the crisis faster and morerobustly. However, the economic growth has not beeninclusive in most countries.

The recent wave of social upheaval sweeping North Africaand other parts of Africa, this year calling, for moreinclusive growth, more accountability and better politicalgovernance has been partly the result of a growth process

that failed to generate adequate jobs and opportunitiesfor the majority of the populations. It is also a clearmessage to the importance of a more equitable incomedistribution in the countries. Available evidence indicatesthat Africa is the second most unequal continent in theworld, after Latin America.

Further, while the continent has recorded growth, thenumber of poor has increased in many countries. Forpoverty to fall substantially, growth should be sustained,i.e., broad-based across sectors, inclusive, andaccompanied by mass job creation, in particular for theyouth. Thus, policies for inclusive growth should be animportant component of most African governmentstrategies for sustainable growth and poverty reduction. It is in this context that the African Development BankGroup will hold its 2011 Annual Meetings under thegeneral theme: “Towards an Agenda for inclusive Growthin Africa”. Four high-level will be organized, namely:

• High-Level Seminar 1: Youth, Employment Creationand Shared Growth in Africa;

• High-Level Seminar 2: Powering Africa: FinancingEnergy, Green Growth and Climate Change;

• High-Level Seminar 3: Private Sector Developmentand Domestic Resource Mobilization in Africa; and

• High-Level Seminar 4: Africa – Innovation Hub forGrowth.

8

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

9

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

High Level Seminar IYouth, Employment Creation and SharedGrowth in Africa

13

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

1 Introduction

Since the beginning of the 2000s, African countries haveexperienced a strong economic growth performance.Improving economic policy management, resulting fromyears of economic and structural reforms, positivedomestic private sector responses, and a generallyconducive international environment have combined tocreate opportunities for African countries to reverse thepoor economic performance experienced during the1980s and 1990s.

However, faster growth in the continent has not broughtabout improvements in the employment situation and,today, with the growing frequency of crises and greaterthreat of regional conflict, unemployment remains highin several African countries and has become a keychallenge for economic development.

Ironically, the reform process that created the improvinggrowth performance has had some countercyclical effectson unemployment. Civil and public service reformsresulted in the retrenchment of workers in the publicservice, the major sector of formal employment, drivingup unemployment rates in many countries. In addition,the small size and limited capacity of the private sectorto absorb job seekers has exacerbated theunemployment problem. Also, over the last two decades,the potentially dynamic and buoyant informal sector hasnot been effective in absorbing job seekers.

As a result, the labour market of many African countriesis characterized by an excess supply of unskilled labourand little effective demand for such labour in the formalsector. The unemployment trends in Africa show that thesituation has not changed much over the past two

14

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

decades. More importantly, the youth that constituteabout 35 per cent of the working-age population in Africahas the highest unemployment and underemploymentrates. Thus, youth unemployment has increasingly cometo be recognised as one of the most serious socio-economic problems currently confronting many Africancountries.

Increasingly, many African countries have shownawareness of the youth unemployment problem andbrought it to the fore of their development agenda. Somecountries in Northern and Southern Africa including

Algeria, Morocco, Tunisia and South Africa haveembedded clear strategies and actions in their nationalpolicies to enhance youth employment. Others have alsodeveloped social protection strategies that encompassclear objectives of the development of youth employment,in response to riots and social unrest.

Nonetheless, the challenge of unemployment in generaland youth unemployment in particular remains daunting.Therefore Africa’s policy makers are confronted with thefundamental question of how to enhance inclusive growthand promote employment and decent jobs. This briefaddresses the issues involved by examining the natureand causes of youth unemployment and highlights somepolicy areas towards addressing the problem.

2 Youth Unemployment in Africa: Nature and Causes

Nature of Youth Unemployment in Africa

Africa is often described as the youngest region in theworld given the fact that about 35 per cent of itspopulation is currently made up of people between theage of 15 and 34 (which according to the definition ofAfrican Union constitute the youth). Available projectionsindicate that by 2015, (see, figure 1) this category of thepopulation would increase to about 35.3 per cent andindeed, would double by 2045.

Characteristically, the youth in Africa are also increasinglybeing educated: the number of university graduatesalmost tripled between 1999 and 2009 in sub-SaharanAfrica, increasing from 1.6 million to 4.9 million. At thesame time, however, a very high proportion of these youngpeople are poor. On average 72 per cent of the youthpopulation in Africa live on less than $2 per day. Theincidence of poverty among young people in Nigeria,Ethiopia, Uganda, Zambia and Burundi is over 80 percent. With such demographic and socio-economictrends, the pressure to create new decent jobs will onlyincrease over time

Source : Nations Unies, « Perspectives de la population mondi-ale », cité dans le « Rapport mondial sur la jeunesse 2007 ».

Figure 1: Africa Population Trends

On the other hand, it is also a fact that the youthful natureof Africa’s population presents opportunities in additionto the challenges. If Africa can provide its young peoplewith the necessary education and skills, the future largeworkforce could be transformed into a highly productiveclass and result in a significant engine of growth anddevelopment.

The challenge, however, is how to create the jobs for themillions and ensure Africa benefits from this demographicdividend. Many African countries are now in a positionto reap this “demographic dividend” thereby increasingthe size and proportion of the working age populationand triggering high rates of economic growth.

Currently, the youth make up the bulk of the unemployedand underemployed in Africa. Unemployment among theyouth is higher than among adults. In Ghana, for example,youth unemployment reaches about 31.7 per cent ascompared to 8.7 per cent among adults. In Sierra Leone,the difference is even starker - youth unemployment is52.5 per cent compared to 10.2 per cent for adults.Recent estimates of the African Development Bank based

on household surveys for selected countries in Sub-Saharan Africa and data from ILO reveal that youthunemployment, including those who have stoppedactively searching for employment could be around 34per cent in several countries (see, Figure 2).

In fact, the share of unemployed youth among the totalunemployed can be as high as 83 per cent in Uganda,68 per cent in Zimbabwe, and 56 per cent in BurkinaFaso. Even for those employed, the earnings could beso low that significant percentages fall in the extremepoor population.

Furthermore, the youth unemployment situation is moresevere for females and rural youth. Female youth tend tobe the most disadvantaged in being able to enter thelabor markets. Around 50 per cent of females in Africaare married before the age of 24. Motherhood could starteven earlier and in Mozambique, Malawi, Niger, Chad,Uganda, and Gabon between 40-50 per cent of femaleyouth (15-24) had already given birth at least once.Participation of women in the labor market in North Africais severe. For example in Egypt, unemployment rates forfemales are close to 50 per cent as compared to lessthan 20 per cent for males.

15

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

Source : ILO Key Indicators of the Labor Market, version 6

Figure 2: High levels of unemployment amongyoung people in Africa

Source: World Bank African Development Indicators 2009

80

79

78

77

76

752002 2003 2004 2005 2006 2007

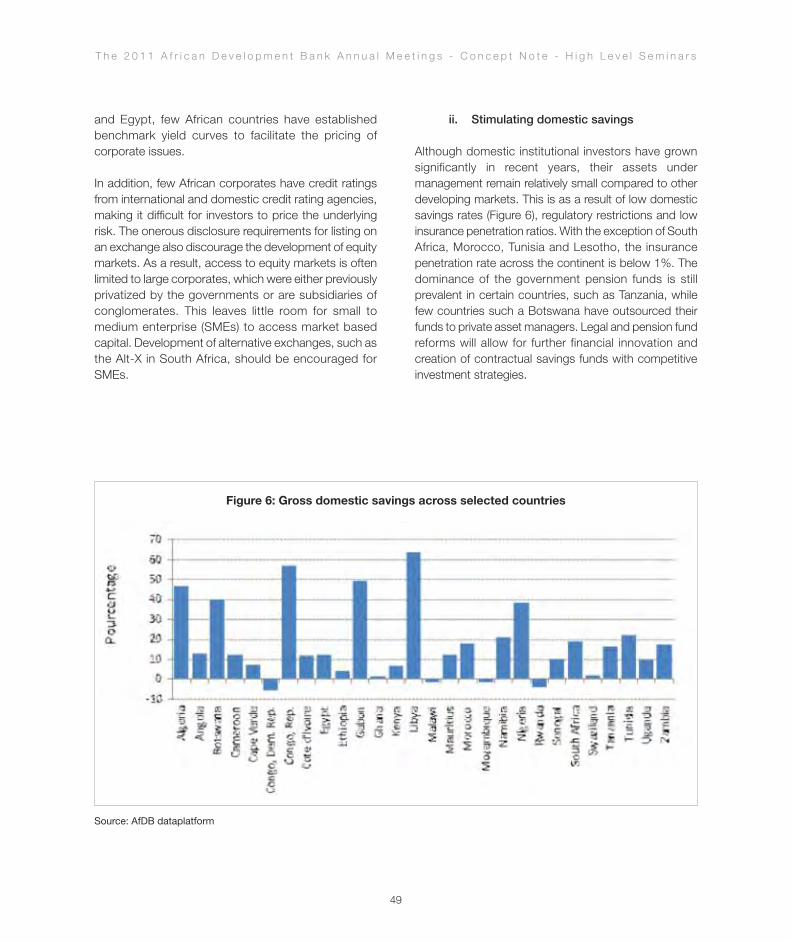

Figure 3: Africa: Share of vulnerable employment in total employment

16

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

Also, for most of the youth in Africa, the informal sectoris the main job provider leading to considerable ‘vulnerableemployment’. The youth are more likely than adults towork in the informal sector and less likely to be wage-employed or self-employed. It is clear from figure 3 that

there is a large share of ‘vulnerable employment’ in totalemployment in Africa. The significant proportion of thisis made of the youth. Engagement of youth in the informalsector becomes predominant during the time of conflictand there is evidence that such “vulnerable employment”which are also at times performing in illegal activitiescontinue to function even during the post conflict period,further challenging prospects to stability.

Ironically, higher levels of education do not protect againstunemployment among the youth. Youth unemploymentis actually higher among those with higher education.World Bank estimates suggest that on average,unemployment is three times higher among those withsecondary education or above as compared to thosewith no education. For example, in 2007, youthunemployment in Tunisia was 20 per cent among thosewithout diploma, 30 per cent with secondary diplomaand close to 50 per cent among those with advanceddegrees in economics, management and law.

More youth migrate to urban areas to find bettereducational and work opportunities as a way out ofpoverty. However, while the urban area continues toattract the rural poor it remains incapable of creating

the job opportunities. Young migrants from rural areasoften earn less than their counterparts in urban areas,and generally, youth unemployment is more prevalentin urban areas than in rural areas. Furthermore, youngpeople who migrate to the cities and fail to find jobs are

more prone to engage in criminal activity. Despite thisrural-urban migration, over 70 per cent of the youth stilllive in rural areas with high levels of poverty.

Causes of Youth Unemployment

• Development Policies: Until recently, employment ingeneral and youth employment in particular were notviewed as key concerns in development policies of mostAfrican countries. Currently, only a few countries like Tunisia,Morocco and Egypt have embedded job promotion in theirdevelopment strategies. For many sub-Saharan countries,either during the structural adjustment policy era or duringthe era of PRSP strategies, employment in general andyouth employment in particular has not been a key issuedespite laudable commitments.

Today, many African countries have adopted privatesector led development strategy. However, the privatesector promotion strategies being implemented are notnecessarily geared to the employment of highly skilledlabor. While strategies involving off-shore and outsourcingactivities being implemented in North African countriesas well as in some sub-Saharan countries, such asSenegal, Kenya, Ghana and South Africa are providing

17

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

job opportunities for unskilled and middle-skilled workers,few countries have implemented comprehensivestrategies to enable employment for university graduatesand others with high skills. As such, across the continentthere is now high level of unemployment of graduatesand highly skilled people. The experience of Moroccoand South Africa that have taken some actions in thisregard, now have more university graduates entering thelabor market.

• Structure of African Economies: Generally, thestructure of many African economies and the labourmarkets do not support the promotion of youthemployment.

The structure of many African economies and the labourmarkets do not support the promotion of youthemployment. The structure of many African economiesis unbalanced and unable to deliver labor intensive andinclusive growth. Most African economies arecharacterized by both excessive dependence on exportrevenues from a few commodities and external financialflows (FDI, aid and remittances) and a weak industrialbase and predominance of subsistence agriculture. Upto at least 19 countries in Africa are significant producersand exporters of oil and minerals, which often divertsresources away from “value-adding” sectors. This hasleft the economy vulnerable to commodity pricefluctuations and international vested interests, breedingcorruption and environmental problems and, last but notleast, condemning the majority of the people to economicexclusion and poverty. The lack of labor-intensive sectorsand the highly unequal distribution of resource rents have,in some cases, led to social unrest and violence.

Moreover, the larger part of the labour market in Africa isdominated by informal employment, which representsabout 72 per cent of non-agricultural employment in sub-Saharan Africa. Over the last 25 years, the potentiallydynamic and buoyant informal sector has not effectivelyabsorbed job seekers. Productivity has increased in theagriculture sector yet it remains relatively marginalized byvirtue of its prevalent rural aspects and the insufficientleverage of technology to enhance its functioning. Thiscontinues to affect its ability to attract educated schooldrop-outs and graduates. Even more of a concern is the

decrease of the average labor productivity of the non-agricultural informal sector in Low-Income Countries (LICs)in SSA over the last decades, from $US1,606 in 1985 toUS$986 in 2005.

However, available evidence suggests that unemploymentin and of itself may not be the main cause of violentconflict. Vulnerability resulting from unemployment is whatexacerbates conflict. In this sense, labor market policiesshould be geared to address vulnerability and deprivation

through relevant employment programs. This is alsoparticularly important for the creation of wage labouropportunities to broaden the tax revenue base, as oneof key elements to state building in fragile states.

• Education and Unemployment: The link betweeneducation and the high unemployment of Africa’s youthis also apparent. Sub-Saharan countries have some ofthe lowest primary education completion rate in the world.Even those who complete primary education often donot get the chance to progress to secondary or highereducation due to poor education quality or economicimpediments. Overall, more than a third of youth in theregion still remain illiterate. Failings in the education systemin terms of incomplete and low quality education hinderthe inclusive participation of African youth in the labor

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

markets causing them to be more likely stuck in lowpaying, low productivity jobs.

There is also a mismatch between higher educationsystems that are responding to the high social demandfor higher education and the labor market demands. Inthe last few years, in vocational and technical educationas well as tertiary education, the number of students hasrisen significantly in Africa. In Northern and South Africathere is an obvious and growing quantitativeoverproduction of higher education graduates. In low-income sub-Saharan countries between 1999 and 2009,the number of higher education graduates almost tripled(from 1.6 to 4.9 million). It is anticipated that this figurewill reach 9.6 million by 2020. This increase in numbershas often been at the expense of quality as expendituresper student have been decreasing throughout Africa.Hence, graduates are often ill-equipped with the requisiteskills. There is also a general pattern of disproportionateenrolments in the social science, humanities and businessmanagement courses, creating graduates with no jobsand jobs with few applicants.

The efficiency problem of the education sector in Africa isalso contributing to the unemployment problem. Moreinvestment in education is not always the answer and mayonly be a delaying strategy. Recent events in Egypt, Tunisiaand Libya have showed that despite the government’sheavy investments and the country’s rapid expansion of

primary, secondary and tertiary education, schools anduniversities are producing graduates lacking the skills theyneed to succeed in employment markets. In Sub-SaharanAfrica, large amounts of funding have been dedicated toinfrastructure inputs for schooling (e.g., school buildings)and much less to quality inputs (e.g., teacher training) andmore cost-efficient models of schooling such as e-learningand twinning. This has left the continent with a largelyunfunded traditional schooling model and poor educationpolicies producing large cohorts of graduating studentsand few skilled youth that can cater to the needs of Africa’s21st century labor market.

However, many sub-Saharan African governments haveundertaken reforms of TVET (Technical and VocationalEducation and Training) by adopting the dual approachthat allows the acquisition of relevant skills and somework experience during the training. In Kenya, Zambia,Botswana, Mauritius, Burundi, Benin, Ghana, Nigeria andTogo, these progammes have achieved some success,though the quality of training and the numbers enrolledhave been low. Besides, the impact on job creation forthe trainees is unknown. On the other hand, many TVETprograms in North Africa - Algeria, Egypt, Morocco andTunisia have received quality accreditation and theirgraduates can compete globally. In these countries,however, the number of graduates per year continues toexceed the real absorption capacity of the labor market.

• Socio-Political Environment: : The socio-politicalenvironment in Africa is also a significant factor in youthunemployment. Challenging socio-political environments,including the ineffective management of ethnic tensionsand hostilities – have contributed to youth unemployment.In these circumstances economic growth to generateemployment is hampered by weak and ineffective, andindeed fragile states. Africa has in the recent past madesignificant progress in reducing conflicts on the continent.However in some countries, including Sierra Leone,Liberia, Burundi, Uganda, and Democratic Republic ofCongo, violent ethnic wars have intensively engaged theyouth as foot soldiers and/or combatants. After suchwars, the youth have found that they are not onlyunemployed, but also without the requisite education andtechnical skills needed to compete for the available jobs,or to become productively engaged in the society.

18

19

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

3 Promoting Employment and Decent Jobs: Issues for Policy

The causes of youth unemployment in Africa clearlyindicate that the problem is complex andmultidimensional, requiring multiple strategies towardsfinding solutions. The important starting point is thatAfrican policy makers already recognize the youthunemployment problem and understand that achievinghigh rates of economic growth must be top priority increating wealth and employment that will take the millionsof Africans out of poverty. While high rates of economicgrowth are necessary, they may not be sufficient to containthe rising youth unemployment. Growth will need to beinclusive and translated into decent jobs that correspondto demand in the growing economy. The following arediscussed in this light.

Macroeconomic and Structural Measures

Africa’s recent economic recovery has been achieved,in part, as a result of the far-reaching macroeconomic andstructural reforms undertaken onthe continent in the past threedecades. The growth expansionhas occurred in a stablemacroeconomic environment.Most African countries haveimplemented soundmacroeconomic policies andstrengthened the managementof their economies. In addition tothe introduction of growth-oriented macroeconomicreforms, many countries havetaken steps to create goodconditions for business. Forsome time now, clear effortshave been exerted to liberalizemarkets, increase legalprotection for investors, andreduce the cost of doingbusiness by simplifyingprocedures and removingimpediments to businessenterprise development. Indeed,recent World Bank Doing

Business Reports place several Africa countries near toppositions in the regional rankings for reforms thatencourage new enterprises, formal sector jobs andgrowth. In 2010, Rwanda was the world champion indoing business reforms and countries like Ghana andTanzania have been among recent top reformers in theworld.

The challenge now is how to deepen these reforms andundertake those remaining to enhance job creation.Reforms that are achieving macroeconomic stability nowneed to be complemented with labour market policiesthat address labour market distortions. Fiscal policiesneed to support labour intensive public works thatemploys large numbers of skilled and unskilled people.

20

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

• Labour Market Laws: In order to help reduce barriersto job creation and promote decent work for Africa’syouth, up-to-date and suitable labour laws are needed.

African countries need labour market regulation to preventexploitation, discrimination, forced labour, low wages andintolerable conditions of work. Available information onat least nine African countries - Botswana, Lesotho,Malawi, Mozambique, Namibia, South Africa, Swaziland,Zambia and Zimbabwe – suggest that lack of systematic,comprehensive and up-to-date market information is astumbling block to the decent work agenda in Africa thatinvolves employment and productive work, workers’rights, social protection and social dialogue. In the contextof fragile states, short term measures such as labourintensive public works programs go a long way to stabilisethe state but this must be accompanied by well-designedmedium to long term measures for job creation built onprivate sector development.

• Decentralization of Public Spending: Economically,decentralization is justified by the need for efficient useof public resources. Local authorities, closer to the areaadministered, provide services needed more closely andaccurately target beneficiaries. Proximity also producesadministrations better suited to managing localdevelopment, including local employment. Althoughseveral African countries have tried to devolve power tolocal authorities –Nigeria has 774 local government areas;Ghana has 110 district assemblies with a Common Fund,Uganda has devolved several powers and functions tothe local level; and, Ethiopia has devolved decentralizedauthorities to regions and lower tier government –generally, these have not been effective. The mainchallenges include manpower and financial resourceconstraints, lack of political autonomy, real power andthe capacity to raise revenue.

• Enabling Entrepreneurship Initiatives:Entrepreneurship talents and skills exist in Africa’s joblessyouth. However, these are rarely channelled towardsefficient business activity. The youth with such skills needto be supported in developing projects through businessincubators and seed-capital programmes. Nearly allAfrican countries have put in place measures toencourage entrepreneurial development and self-employment of the youth. Some successes have beenachieved in Egypt, Mauritius, South Africa, Nigeria, andZambia. Most importantly, these programmes requireactive public and private support to be successful. Agood example is the scheme developed by the AfricanDevelopment Bank in Tanzania linking business incubatorswith technical schools. An important feature ofentrepreneurship development support in fragile stateswill be the access to suitable financing in addition to skills.This will require appropriate incentives for risk guaranteeschemes and a more comprehensive approach tobanking sector reforms.

Sectoral Approaches

Global experiences suggest that major obstacles topromoting employment for the youth are sector specific.Sectoral approaches to job creation must be multi-sectoral and in order to maximize impact, linkages amongsectors are important. Africa needs policies that focus

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

on sectors that offer most opportunities for growth anddecent work. Such sectoral policies and approachesshould involve special training in skills related to the sector,improving access to finance, enhancing productivityknowledge and development.

• Enhancing Agricultural Productivity: In Africa, growthof the agricultural sector can stimulate employmentgrowth in other areas of the economy because of itsstrong links with other sectors. Indeed, available estimatessuggest that in sub-Saharan Africa there is high multipliereffect of 1.5 associated with agricultural growth, whichimplies that every $1.00 increase in agricultural incomegenerates an additional $0.50, primarily amongstsuppliers of non-farm goods and services. Thus, broadbased economic growth and employment creation inAfrica requires a focus on agricultural. Also, since Africanpoverty and unemployment is predominantly a ruralphenomenon. Policy interventions to combat rural povertyshould include promoting agro-business and processingrelating to value adding.

The basic problem with Africa’s agriculture is lowproductivity. Agriculture in Africa suffers by virtue of itsprevalent rural aspects and the insufficient leverage oftechnology to enhance its functioning. This is a bottleneckto the sector’s ability to attract educated school dropouts and graduates. The basic challenge is to enhanceagricultural productivity and the sector’s attraction to theyouth. Provision of support to small farm holders whoconstitute the majority of Africa’s farmers is essential.

Support in terms of finance, technical advice, and farmequipment will enhance productivity. Also, existingtechnologies that are known to have worked elsewhereneed to be adopted and new ones developed alongsidethe improvement of agricultural infrastructure. It isnecessary that policies support private sector initiativesto develop value chains and promote labor-intensivemanufacturing, especially in areas such as agricultureand agro-processing.

• Engaging the Informal Sector in Job creation: TheAfrican Union has asked the question “whether theinformal sector should really be seen as a marginalized,survival sector, which mops up excess or entrenchedworkers or as a vibrant entrepreneurial part of theeconomy, which can stimulate economic growth and jobcreation”. It is now obvious in Africa that employment inthe informal sector is a reality. Thus, the aim to createjobs must include the informal sector. This will comethrough government recognition of the importance of theinformal sector. Alongside strengthening the formal sectorin job creation through the removal of barriers to enhanceincreased participation, governments need to extendbenefits to the informal sector. Several avenues are opento African governments to encourage job creation in theinformal sector. These include, provision of enablingenvironment and supportive regulatory framework;provision of appropriate training and equipment;improvement of basic facilities, amenities andinfrastructure; and enhancing access to credit andproperty titles.

22

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

• Promoting Social Inclusion: Social inclusion, voiceand accountability are pre-requisites without which nocountry can truly aspire to broad-based, shared andsustainable economic growth needed to create decentjobs. Indeed, a vacuum in voice and accountabilitymechanisms has been one of the major triggers of therecent events in North Africa and the Arab world.Following decades of top-down rule, corruption and lackof transparency there is also a remarkable deficit in socialinclusion, voice and accountability and participatorymechanisms contributing to an overall sense ofdisempowerment of the population – especially amongthe educated youth. People in North Africa as well as inthe whole continent are aspiring for greater transparencyand accountability as well as public participation atnational and regional levels, through the activeparticipation of civil society.

4 The Role of the African Development Bank

Since 1990, the African Development Bank has beenchanneling resources to 37 countries mainly throughprojects aiming at providing employable skills to vulnerablegroups including youth and projects promoting self-employment. A focus on youth employment falls squarelywithin the Bank’s Medium Term Strategy (MTS). TheBank’s overall aim is to assist in the development of Africaand the reduction of poverty, in particular by promotingequitable growth and economic integration, and throughthem, wider opportunities for Africa’s poor. The proposedactions respond to the Bank’s MTS broad developmentgoal of ensuring sustained and equitable growth.

Governance • Labour market reforms• Setting key indicators on job creation• Enabling environment for SMEs

Infrastructure • Using infrastructure projects as a vehicle for youth employment• Introducing skills development and technical training packages with infrastructure projects

Private Sector • Involving multi-nationals and private operators in skills upgrading and transfer• Promotion of SMEs • Microfinance

Higher Education Addressing the mismatch between the skills produced by the education system and those re-quired by the labor market

Regional Integration Integrating markets: Increasing market size and developing value chains

23

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

The areas of the Bank’s interventions in YouthEmployment within the MTS’s Pillars are set out below:

Specifically, the Bank has also been actively involved inskills development through Technical and VocationalEducation and Training (TVET) projects and ruraldevelopment projects. The Bank has assisted indeveloping a scheme in Tanzania linking businessincubators with technical schools. This initiative was aimedat helping entrepreneurs to produce proper accountingdocuments and to put bankable projects together in orderto facilitate their access to finance. There is nocomprehensive assessment of Bank’s projects on jobcreation for youth. However, for the social sector projects,preliminary studies show that skills developmentoperations and microfinance schemes have yielded goodresults in terms of job creation.

Building on this the Bank is proposing a new initiativeon youth employment. In light of the recent lessonslearned from Northern Africa and the potential of SSAcountries to join in benefiting from the demographicdividend, the Bank proposes to support RMCs to scaleup their support to youth employment policies andprograms. The proposed initiative is a response toaddress the urgent needs of countries that faceexcessively high levels of youth unemployment as wellas social unrest. In addition, it also tackles structuralissues over a longer time frame, to mitigate the risksof economic and social threats on the continent.

The Bank is being increasingly involved in supportingestablishment of voice and accountabily mechanisms inthe RMCs through increased citizen participation and controlover public management, and strengthening the civil societyorganisations and local governments as a response to thecrisis in North African countries. The example of Tunisia hasshown that all the machinery in place for supportingemployment creation and increased employability of theyouth is not effective because of lack of transparency, goodgovernance, participation and accountability.

5 Issues for Discussion

1. Why are most of the policies, reforms andprogrammes focusing on reducing youthunemployment in Africa not succeeded?

2. What policy interventions needs to be taken toensure that employment is given a more central rolein macroeconomic policy, poverty reductionstrategies and as an integral part of nationaldevelopment strategies.?

3. What is the most appropriate policy mix forpromoting meaningful youth employment in reducingvulnerabilities in fragile states?

4. Are there internationally successful strategies andpolicies for addressing the problem of youthunemployment to be applied in Africa? How canAfrica domesticate such promising strategies thathave been implemented elsewhere?

5. To what extent is the political environment in Africancountries blamed for youth unemployment?

High Level Seminar IIPowering Africa: Financing Energy and Green Growth

27

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

1 Introduction

The strong economicperformance of Africa during

the last ten years, as well as itsestimated economic growth, willlead to an ever-increasing energydemand across the continent.Unfortunately, the growth inpower supply has not beensufficient. Consequently, it hasbecome crucial to implementconcrete measures to endenergy insecurity and to setAfrica on a sustainable energypath. Africa has now thepossibility to use its abundantnatural resources coupled withan expanding number ofinnovative environment-relatedfinancing instruments, tosignificantly decrease its energygap and do it, growing under alow-carbon, clean energy paththat will attract more than everthe interest and participation ofdonors and private investors insupport of strong growth, jobcreation, and poverty reduction on the continent.

Currently, the main challenges facing Africa’s power sectorare: (i) inadequate generation capacity; (ii) limitedelectrification; (iii) low power consumption; (iv) unreliableservices; (v) high average generation costs; and (vi) afinancing gap of approximately USD23 billion per year.To fight the aforementioned challenges, Africa will requirea paradigmatic shift in the development of the powersector in order to tap into its vast renewable resources,including hydro-potential (estimated around 1,750 TWh),geothermal (estimated at 9,000 MW), wind, and solar.These sustainable sources of energy are in the frontline

to respond to the needs of Africa’s large rural and oftengeographically dispersed population, which will best andin some cases only be reached in the long term by off-grid technologies. Furthermore, they can provide thenecessary scale to avoid dependence on costly small-scale national power systems, which are heavily relianton expensive fossil fuel-based generation.

A shift towards clean energy solutions will allow Africa totap into existing concessionary resources that reducethe costs and risks of such investments while providingan extremely valuable leverage of private sector resources.An example is the USD4.3 billion Clean Technology Fund,

28

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

which is expected to leverage at least four times this valuein clean energy solutions, including energy efficiency,renewable energy, and sustainable transport investments.

Nevertheless, given the high costs of clean energysolutions and the existing financing gap, a portfolio offinancing sources will have to be considered andsustained to meet current and future demand. This papersummarizes the challenges and opportunities of thePower Sector in Africa. It also builds in the public andprivate finance sources, emphasizing the measures

needed to attract private investments to the sectorincluding a write-up on Public-Private Partnerships. Itdraws on innovative financing mechanisms designed toraise additional funds, and ways to optimize both privateand public financing methods. Finally, it examines the roleof multilateral development bank and other internationalfinancial institutions that, in addition to applying their ownfinancing mechanisms, can facilitate large-scale regionalenergy projects and help raise Africa’s influence and voicein the allocation, administration and absorption of globalclimate-related resources.

2 The Power Sector: Challenges and Opportunities

Power Deficits and Investment Opportunities. It isestimated that 80% of the World’s 1.5 billion peoplewithout electricity live in Sub-Saharan countries, mostlyin rural areas. Residential electricity consumption in Sub-Saharan Africa, excluding South Africa, is roughlyequivalent to consumption in New York. In other words,the 19.5 million inhabitants of New York consume in a

year roughly the same quantity of electricity, 40 TWh, asthe 791 million inhabitants of Sub-Saharan Africa1.

Source: Briceno-Garmendia, QFC, 2008

Figure 1: Average Cost of Grid and Backup Power in Sub-Saharan Africa

1 International Energy Agency. “Energy Poverty: How to make

modern energy access universal?”, September 2010

.

29

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

Given that rural areas account forabout two-thirds of the populationand only 15 percent of the ruralpopulation lives within 10 km ofan existing substation, only asmall proportion of ruralpopulation can be added to theelectricity grid at relatively lowcost. As much as 41 percent ofthe rural population is currentlyliving in areas considered isolatedor remote, and therefore distantfrom the grid.

The lack of robust infrastructurehas been identified as a factorlimiting the economic performanceof a number of African countries.In particular, costly and unreliablepower supply coupled with weaktransportation networks increasethe cost of doing business, reduce overall productivity andcompetitiveness (by 40%)2, and diminish social progress.

Power Generation Costs. The average total cost ofproducing power in Africa is extremely high: USD0.18per KWh with an average effective tariff of USD0.14 perKWh when compared with tariffs of USD0.04 per KWhin South Asia and USD0.07 in East Asia. Theseexceptionally high costs are mostly due to the small scaleof most national power systems and the widespreadreliance on expensive diesel-based generation. Highproduction cost is just one of numerous inefficiencies;others include less than full implementation of the fiscalbudgets allocated for investment in energy, insufficientmaintenance, inefficiencies and losses during thedistribution phase, and pricing of electricity below thecost as is done is South Africa, which encourageswasteful consumption.

The average operating cost of predominantly diesel-based power systems is as much as USD0.20 per kWh,well above the cost associated with hydro-based

2 Escribano, J. L; Pena, J. “Impact of Infrastructure Constraints on Firm Productivity in Africa”. 2008.

systems. Moreover, countries with small national powersystems (below 200 MW of installed capacity) face anoperating cost penalty of as much as USD 0.15 per kWhrelative to countries with large national power systems(above 500 MW of installed capacity). Landlockedcountries and island states face an even higher costpenalty due to higher transportation costs of fossil fuels.

Nowadays, the swiftest way to recover costs is to reducethe inefficiency of Sub-Saharan utilities, combined withthe widespread practice of charging tariffs below theaverage generation cost. These hidden costs, amountto at least 1.8% of Sub-Saharan GDP. In many cases,the dividend accruing from improving utility performancecould be extremely high and would allow utilities’ abilityto attract external funding, either public or private. Fullcost-recovery tariffs could be affordable already incountries with efficient large-scale hydropower or coal-based systems, but not in those relying on small-scalediesel-based plants. If regional power trade becomes areality, generation costs will fall, and full cost-recoverytariffs could be affordable across Africa.

30

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

Financing Gap. The national targets under a stagnationof power trade are to add 7,000MW per year, or 70,00MWbetween 2005 and 2015. The trend for the past decadehas been a 4% generation increase per yearcorresponding to 3,500MW. The financing needs underthe above scenario equals USD 50,3 billion per year. Thisamount is equally split between capital costs andoperating costs. Two thirds of this amount shall targetincrease in generating capacity while the remaining thirdwill target transmission and distribution.

Regarding power trade, it is important to mention thatits expansion is a logical path to reduce carbon emission,protect countries from rises in oil prices, and diversifysources of energy both in terms of source and in termsof geographical location. It is estimated that power tradecould promote savings of around USD2.7 billion per yearin Sub-Saharan Africa, or 5.3% of the annual cost ofmeeting power needs.

3 Public and private finance sources

Potential Public Finance Sources. While it is expectedthat private sector will assume a key role in implementingand financing clean energy projects, the associated lowreturns so far imply that a substantial portion ofexpenditures will need to be covered from publicsources. Potential public sources include domestic andinternational taxation; official development assistance;emerging donors; and innovative forms of financingfrom carbon markets. These sources can and shouldbe assessed according to their revenue raising potential,additionality, efficiency, practicality and reliability.

On the long run, domestic revenue mobilization, viaimproved tax policies and tax administration, is the mostviable financing basis to raise and channel money intothe energy sector. African countries could also mobilize

Source: AICD Report, 2008

Installed capacity in 2005 (MW) Additional capacity by 2015 (MW)

IslandStates

Figure 2: Current and additional capacity needed by Region in 2015 in MW

31

establish an enabling environment for private sectorinvestment need to take the following intoconsiderations: (i) creating or strengthening theregulatory frameworks that facilitate businessregistration; (ii) ensuring contract enforcement; (iii)simplifying tax codes; (iv) guaranteeing propertyownership; (v) supplying trained local labor; and (vi)reforming the financial sector in order to allowconvertibility and repatriation of earnings.

Governments with Public-Private-Partnership (PPP)units are prone to attract more private sector investment.Successful partnerships between state and privateactors that go beyond business reforms tend to createenvironments conducive to investment. The best PPPunits have established programs of prioritizedinvestment opportunities with features including: (i) clearpolitical support; (ii) a proper legal and regulatorystructure; (iii) a transparent procurement framework;and (iv) support services to facilitate implementingproject timetables. These features reduce uncertainty,

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

further resources by developing their banking sectorsand with the right incentives they can capitalize on futureflows such as remittances and initiate innovative waysto make “unbanked projects, bankable”.

Nonetheless, a variety of sources, public and private,bilateral and multilateral, including some innovativeforms, will be needed to generate sufficient funding andmaximize strengths of each, while offsettingweaknesses.

Private Sector Role. Private financiers and projectdevelopers look beyond project-technical and financialcharacteristics when making an investment decision.In selecting projects, private developers have to considerthe wider political, legal, and economic contexts whichwill likely affect a certain project. Targeted public sectorand donor support that address market failures andstructural deficits can build on market forces andeliminate constraints which otherwise would crowd-outprivate sector involvement. Policy-makers seeking to

32

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

lower the risk profile of the project and increase itsviability.

As a result, governments should invest resources to buildcapacity within government entities to engage onnegotiations of contractual agreements which reflectappropriate risk allocation and reward sharing betweenstakeholders. For renewable energy in particular, technicalcapacity is required to properly price and reflect theeconomic and financial value of environmental and naturalresources. Bankable project documentation that suitablyallocates costs and risks to appropriate parties is essentialto boost private investor confidence. This can only beachieved when concessions and off-take agreementsare negotiated within a transparent framework governedby an independent regulatory authority.

Public-Private Partnerships. The rationale for using aPPP arrangement instead of conventional publicprocurement rests on the proposition that optimal risksharing with the private partner delivers better value-for-money for the public sector. The downside of thisarrangement is its complexity since they require detailedproject preparation and planning, and propermanagement of the procurement phase to incentivizecompetition among bidders. They also require carefulcontract design to set service standards, allocate risksand reach an acceptable balance between commercialrisks and returns. These features usually require skills inthe public sector, which unfortunately, most of the timesare not available.

Achieving value-for-money that justifies the PPP optionalso depends on the ability to identify, analyze and allocaterisks adequately. Failure to do so will result into financialcosts to the Government.

Mitigating Risks. There a number of factors that limitprivate financiers’ appetite for long term exposure torenewable energy projects in emerging and frontiermarkets, including political risk, refinancing risk, andcommercial risk introduced by the poor creditworthinessof state-owned utilities that have the payment obligationsto buy generated power under power purchaseagreements.

Some state-owned utilities perform reasonably well, butthe majority of them lack government support in orderto remain financially viable. Ordinary problems affectingprofitability include: (i) poor billing and payment collectionsystems; (ii) limited innovation; and (iii) prices which reflectneither costs nor demand. In many African countrieswhere electrification rates are low, governments preferto enforce average prices which are lower than averagecosts in order to increase accessibility. Eventually thiscauses the utility to experience financial distress andcut back on maintenance or investment. In systemswhere the public sector still has the responsibility forproviding transmission and distribution infrastructure,this can inhibit private participation if the ancillaryinfrastructure to evacuate and distribute power isunavailable or overloaded. Technical losses are higherwhen ancillary infrastructure is improperly maintained,resulting in less revenue collection while the utility muststill fulfill payment obligations for undistributed butgenerated power.

In case of utilities exposure to commercial risks causedby weak financial and technical performance, lenders willseek credit enhancement from other sources to backstopthe utility’s payment obligations. There are a number ofavailable instruments to the Government, which canrange from an open-ended government guarantee of

33

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

the utility’s debt obligations, to having three to six monthsof utility payment obligations under the off-takeagreement backstopped by a letter of credit issued bycommercial banks. In the case of the governmentguarantee, lenders consider the government’screditworthiness. Government guarantees, however,create contingent liabilities for governments and willultimately impact the sovereign debt sustainability.

Multilateral Development Institutions, such as AfDB, offera number of instruments to mitigate political andcommercial risk in order to stimulate private investmentand improve the terms of the commercial debt. Forinstance, the use of partial risk guarantees will coverspecified political risk events, including covering lossesincurred by commercial lenders caused by a governmentor government-owned entity failing to perform itsobligations under a certain contract. Partial creditguarantees support sovereign borrowing from membercountries, and can be used to facilitate commercial bankissuance of letters of credit to backstop a pre-specifiedamount of the utility’s payment obligations with respectto a particular project. Political risk insurance coveringprivate investors’ equity, quasi-equity, and non-equitydirect investments can also be sought, covering anycombination of transfer restriction, expropriation, warand civil disturbance, and breach of contract.

Optimizing Financing Strategies. Usually, renewableenergy projects are greenfield investments. Both capitalexpenditure cost associated with operation andmaintenance of a given renewable energy project, shallbe reflected in the tariff negotiated upfront in the off-takeagreement. The tariff impacts the revenue the project isexpected to earn during the concession period, andmust be sufficient to service debt and provide a minimumand acceptable return for equity investors. Whileelectricity generated from renewable energy sources istypically more expensive than electricity generated fromconventional sources since the technology is moreexpensive and lacks economies of scale, thermal powerhas lower capital expenditures compared to renewableenergy but higher operating costs due to dependenceon external fossil fuel sources. Despite the fact that volatilecommodity prices can be hedged with long term fuelsupply agreements and derivatives, so long as the fuelsource is finite, there can never be a sustainable solution.In contrast, renewable energy has the advantage ofproviding a stable fuel source for power generation, butthe associated technologies are generally at an earlierstage of market development.

A combination of financing options is required to offsetthe high cost of generation associated with new oruntested technologies and ensure the sale ofcompetitively-priced power. A mixture of concessionalfinancing with commercial financing can play a key rolein subsidizing generation tariffs which would otherwisebe too high and make the green energy too expensivefor off-takers to purchase.

4 The Role of the African Development Bank and otherMDB’s

MDBs have the experience and capacity to catalyze fundsacross the private and public sector to deploy financefor clean energy projects. In addition to their mandate,MDBs have the capacity to (i) mobilize additionalconcessional and innovative finance; (ii) facilitate thedevelopment and utilization of market-based financingmechanisms; (iii) leverage available resources; (iv) supportaccelerated development; (v) deployment of new

34

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

technologies; and (vi) support policy research, knowledgeand capacity building. Their comparative advantage reliesin the capacity to use a wide range of instruments tosupport simultaneously the development andstrengthening of institutional and regulatory capacity, aswell as finance for investments. MDBs need to play a keyrole in addressing the Africa’s energy deficit in facilitatinglarge-scale national and regional projects.

Over the past five years, MDBs demand-side energyefficiency financing has more than doubled, reaching

USD3 billion in 2009. Supply-side energy efficiencyfinancing has trebled, reaching USD1.9 billion, whilerenewable energy financing has close to quadrupled fromUSD1.1 billion in 2006 to USD4.2 billion. The leverageratio of total project cost to MDB financing rangedbetween 3.3 and 3.8 with an average leverage ratio overthe period 2006 to 2009 of 3.4. Nearly half of the MDBfinancing was targeted to the private sector.

These efforts have been supported through themobilization and deployment of global climate financinginstruments, in particular the Climate Investment Fundsand the Global Environment Facility. Recent conservative

estimates indicate a significant expected growth in MDBrenewable energy financing, which can increase fromUSD4.2 billion in 2009 to USD5.9 billion in 2012. Still,MDB clean energy financing results over this period willdepend to a significant extent on the sustained availabilityof concessional funding, either in the form of grants tosupport technical assistance and capacity building or inthe form of concessional loans to address marketdistortions. Different forms of guarantees can also playan important role.

The African Development Bank is proposing to establisha special fund, the Africa Green Fund as a financingmechanism for addressing Africa’s low carbon growthneeds, including the development of its clean energypotential. The fund would predominantly be financed fromthe resources allocated to Africa from the pledges underthe Copenhagen Accord. The location of this fundingmechanism in Africa has the potential to enhance Africancountries’ resource ownership, African participation inthe decision-making processes regarding fund usage,and the principle of equity and fairness in the allocationof resources.

Policy Recommendations. A number of recommendationsfollow from the foregoing analysis of the challenges andopportunities associated with financing sustainable cleanenergy in Africa. They include the following:

- Combine instruments. Significant scale andtransformational impacts can be achieved by linkingproject interventions to policy in a programmatic way.Combining resources across climate financinginstruments not only supports scaling up but canstimulate transformational processes.

- Promote new and additional concessional funds for cleanenergy projects. This will be a key determinant to furtherscale up clean energy financing activity particularly in theabsence of a significant strengthening of the climateframework, including the carbon markets. Currentcommitted donor finance, plus projected CDM fundingthrough 2012, amount to less than USD8 billion per year.

- Mitigate regulatory risk. This remains a key priority in anumber of countries, particularly with respect to

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

renewable energy. Guaranteeing grid access, implementadequate tariff levels, and put in place clear rules topass through the incremental costs of renewable energyare key to increase market penetration, particularly forindependent power producers.

- Consideration for feed-in tariffs. Feed-in tariffs aremandated by legislation and ensure that IndependentPower Producers cover the cost of generation plus areasonable return for equity investors to incentivizedevelopers to invest. The Kenyan government, forexample, introduced feed-in tariffs for wind, biomass,and small hydropower generation in March 2008, withguaranteed prices for 15 years. South Africa, Algeria andMauritius also have feed-in tariffs, while many others aremaking plans to introduce them. In the South-Africancase, the national energy regulator of South Africa,NERSA, introduced separate feed-in tariffs for wind, solar,and small hydro in March 2009 following a consultationpaper, public hearings, and deliberations with majorstakeholders. The tariffs are set at above-market ratesand are guaranteed for a period of 20 years.

- Create incentives for new technologies. Africangovernments should promote the development of localgreen technology industries and encourage the transferand diffusion of technologies and knowledge from otherparts of the world. For example, Ghana ceasedsubsidizing petroleum products in 2005 and divertedthose resources to developing clean technology. Otheroptions include relaxing import barriers, such as highimport duties on products used in renewable energyproduction and promoting the domestic production ofrenewable energy components, like solar panels or windturbines, to ensure sustainable development of greentechnology domestically.

5 Conclusion

Africa’s natural resources together with its energy gapshould be looked as an opportunity for (i) private sectorinvestment; (ii) accelerating growth and poverty reduction;and (iii) embarking on green growth.

The magnitude of financing needs linked to the energysector in Africa will require a mixture of financialinstruments and different sources of funds. The publicsector will be pivotal not only in terms of raising neededfinance that can for the time being compensate for thelow returns of clean energy projects but also for crowdingin the private sector.

The African Development Bank is highly committed tothe development of the renewable energy sector andmarkets using the whole variety of instruments that is hasat its disposal and new tailored instruments that isestablishing to cater for the specific constraints andopportunities of Africa, including the Africa Green Fund.

Discussion Questions.

- What are the challenges that a country needs to addressto engage in sustainable and clean energy solutions(e.g. regulatory framework, access to financing, markets,policies like feed-in tariffs)?

- How can AfDB best provide practical support to Africancountries to face such challenges and tap into existingand future opportunities?

- Given Africa’s financing gap in the energy sector and thehigh costs of sustainable and clean energy solutions, whichportfolio of financial instruments should be considered?

High Level Seminar IIIPrivate Sector Development and DomesticResource Mobilization

39

1 Introduction

Africa’s near term economic outlook remains very positive,despite the recent adverse effects of the global economiccrises. Over the last decade, productive internal structuralreforms, progress in regional integration, improved politicalclimate and reduced conflicts have combined with alargely favourable external environment – in terms ofhigher commodity prices and increased resource inflows- to spur economic activity. Moreover, the considerableimprovement that has taken place in the business climatehas enabled private sector activity to generally respondpositively to government programmes.

However, the global economic crisis has shown howuncertain external flows are for African governments.Several countries faced reduced export revenues;considerable uncertainty was experienced with regardto future foreign investment and aid inflows, while highlevels of indebtedness remained a concern. In fact theglobal economic crisis has given a new impetus todialogue on domestic resource mobilization in Africa toeffectively and sustainably bridge the persistentdevelopment-financing gap. The recent global uncertaintyposes important challenges to fiscal policies in Africa andmore so in the most vulnerable African countries. Publicfinances are under additional strain in Africa as aid-

providers are facing at home significant fiscal shortfallsand are forced to take severe fiscal adjustment measures.

Over the past 10 years only oil rich countries in Africahave achieved a fiscal surplus of about 2 per cent of GDPwithout grants. Middle income countries have been ableto contain their deficit at around 2 per cent of GDP, whilein low income countries and fragile states the deficit isabout 8 per cent of GDP. Indeed, the overall fiscal deficitof some low income countries such as Burkina Faso,Ethiopia Ghana, Malawi, Mozambique Rwanda and somefragile countries such as Burundi, Eritrea and Sao Toméand Principe is so large that it often accounts for about40 to 100 per cent of total government domestic revenuesof some specific countries.

These factors have combined to raise the importance ofincreasing domestic resources in Africa, not necessarilyby increasing taxes but by improving the efficiency of thetax administration and the broadening of the tax basethrough a vibrant private sector. Indeed, as the UnitedNations’ Monterrey Consensus on financing forDevelopment acknowledged earlier in 2002, externalfinancial resources for development are inadequatetowards meeting the MDGs. The Monterrey Consensusstressed the necessity to develop new strategies bymobilizing domestic resources.

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

40

The attractiveness of Domestic Resource Mobilization(DRM) is quite apparent. DRM avoids the restrictionsand conditionality often present in financing from externalsources and is also likely to support increased domesticownership of the development agenda. DRM also hedgesagainst the potential volatility of access to externalresources such as FDI and export earnings. Increased

DRM through a well-functioning financial system willcontribute significantly to private sector expansion.Indeed, global development success stories indicate thatbetter mobilization of a country’s own resources and lessdependence on aid and other foreign finance, are key forsustained, strong and shared growth.

There are two sides to generating domestic savings andtheir allocation to socially productive investments within

a country. The private side concerns private domesticsavings, encompassing household savings and privatefirms, through banks and non-bank financial institutionsand capital markets that channel these resources tocommercially productive investments. The other side ispublic resource mobilization, which involves resourcemobilization through fiscal regimes for investment in social

services and infrastructure that support private sectoractivity.

Therefore, increasing DRM in Africa requires a two-pronged approach. First, strengthening the fiscaleffectiveness of governments and their capacity. This isessential towards improving the social rate of return ofpublic investment. Second, deepening and reforming thefinancial sector, which despite progress in diversification

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

41

and employment of market based banking systems stillface vital challenges in broadening access to financialservices and the availability of long-term resources.

This main purpose of this note is to highlight the relevantissues involved in the mobilization of both domestic publicand private resources. The issues involved are addressedby examining the current state of domestic resourcemobilization, the challenges and prospects.

2 Strengthening Public Resource Mobilisation in Africa

Current Situation and Challenges

Africa needs better mobilization of domestic publicresources for development. The imperative ofstrengthening domestic resource mobilization is quiteapparent. It is evident from Figure 1, that in many African

countries, Official Development Assistance (ODA) percapita exceeds tax revenue per capita. Thus, for self-sustaining growth, it is essential to enhance domesticresource mobilization.

The continent’s heavy dependence on ODA and its lowpublic resource mobilization is in spite of recent significantprogress in tax mobilization. Indeed, many countries haveover the last decade seen an upward trend in the shareof tax in total GDP. Figure 2, which classifies Africancountries into three income groups show that for ‘uppermiddle income countries’ (those with per capita incomebetween $3856 and $11905 in 2008)), tax share in totalGDP is around 35 per cent, which is similar to the OECDcountries. In ‘lower middle income countries’ (per capitaincome between $976 and $3855 in 2008), the tax shareis about 22 per cent of GDP. This share is similar to otherdeveloping countries in the same income group.However, for lower income African countries (per capitaincome of $975 or less in 2008), the tax ratio is muchlower at below 15 per cent.

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

Source: African Economic Outlook, 2010

Figure 1: Public Resource Mobilization in Africa

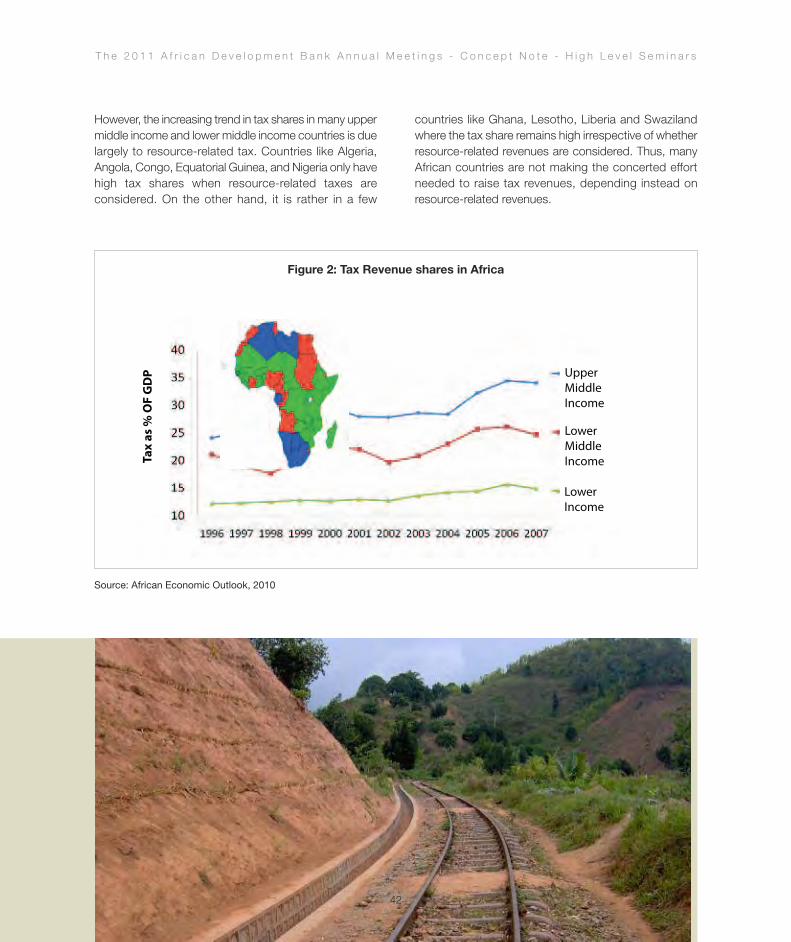

However, the increasing trend in tax shares in many uppermiddle income and lower middle income countries is duelargely to resource-related tax. Countries like Algeria,Angola, Congo, Equatorial Guinea, and Nigeria only havehigh tax shares when resource-related taxes areconsidered. On the other hand, it is rather in a few

countries like Ghana, Lesotho, Liberia and Swazilandwhere the tax share remains high irrespective of whetherresource-related revenues are considered. Thus, manyAfrican countries are not making the concerted effortneeded to raise tax revenues, depending instead onresource-related revenues.

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

42

Source: African Economic Outlook, 2010

Figure 2: Tax Revenue shares in Africa

43

Nonetheless, increasing tax revenue to enhance publicresource in Africa faces daunting challenges. Many Africaneconomies are characterised by large informal sectorsthat make it difficult to enhance tax revenues by eitherbroadening the tax base and/or increasing direct taxation.Also, the narrow tax base in many countries is oftenconstricted further by excessive granting of taxpreferences, inefficient taxation of extractive activities andan inability to fight abuses of transfer pricing bymultinational enterprises. Further, several countries areconstrained by an unbalanced tax mix that reliesexcessively on a narrow set of taxes.

Strengthening Public Resource Mobilization: Issues for Policy

How African countries address the challenges withoutover-taxing their economies will determine the extent to

which public resources drive investment in social servicesand infrastructural activity needed for private sectorexpansion. In this quest, simply increasing taxes may notbe the required response. Tax increase could harm theprivate sector and hamper economic growth but maynot necessarily improve the efficiency of the tax system.

In the long run the most effective way that domesticpublic resources can be increased is through policiesthat increase the tax-base through sustained economicgrowth. In the short to medium term, Africangovernments have to address the efficiency issues andadapt strategies to deepen the tax base in administrativefeasible ways. A focus on deepening the tax base givesmore stability through a diversified set of taxes, with amild burden on each type of taxpayer and each type ofeconomic activity. Also, a deepened tax base will engagea bigger range of stakeholders in the nationaldevelopment process. The following issues must be atthe forefront of attempts to deepen the tax base tostrengthen public resource mobilization.

i. Bringing the Informal Sector into the tax net

There are a number of challenges in any attempt towiden the tax net to informal activities. Firstly, the increasein tax revenue that formalized informal firms could yieldmay be small, as these firms are often too small and toopoor. Hence, there is need for innovative ways to ensurepositive net tax returns. A number of approaches havebeen adapted in some African countries that couldprovide a way forward. For example, the Ghana InternalRevenue Service has negotiated with the Ghana PrivateRoad Transport Union to use the union as a tax collectionagent under the Identifiable Grouping Taxation (IGT)scheme. The IDT levies small and affordable taxes thatare collected daily or weekly from both the formal andinformal union members. Algeria is using a presumptivetax for the mainly informal entrepreneurs. In Zambia, aflat-rate ‘base tax’ for rural areas has been introducedalong with ‘presumptive taxation’ of 3 per cent on grossincome for urban areas. Additionally, a ‘peddler’s licence’has been issued for street sellers.

T h e 2 0 1 1 A f r i c a n D e v e l o p m e n t B a n k A n n u a l M e e t i n g s - C o n c e p t N o t e - H i g h L e v e l S e m i n a r s

44

ii. Reducing improper transfer pricing

Improper transfer pricing is an international problem thataffects developed and developing countries alike.Multinational enterprises operating in African countriesmight take advantage through different tax regimes,including tax havens, under-invoice or over-invoice forgoods and services, and financial transactions tomaximize after-tax profit at the expense of the hostcountry. The general consensus towards reducing transferpricing abuse requires countries to develop specificlegislative measures that are adapted to their legal system