r pre budget analysis report construction - kotak … · kotak securities - private client research...

TRANSCRIPT

Service tax

Direct tax

Excise duty

Defenseexpenditure

Fiscal deficits

Subsidies

Government borrowings

Budget deficits

Indirec

t tax

Corporation tax

Income tax

Import duties

R

R

Expenditure

Good

s and

servi

ce ta

x

PRE BUDGET ANALYSIS REPORT CONSTRUCTION

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 19

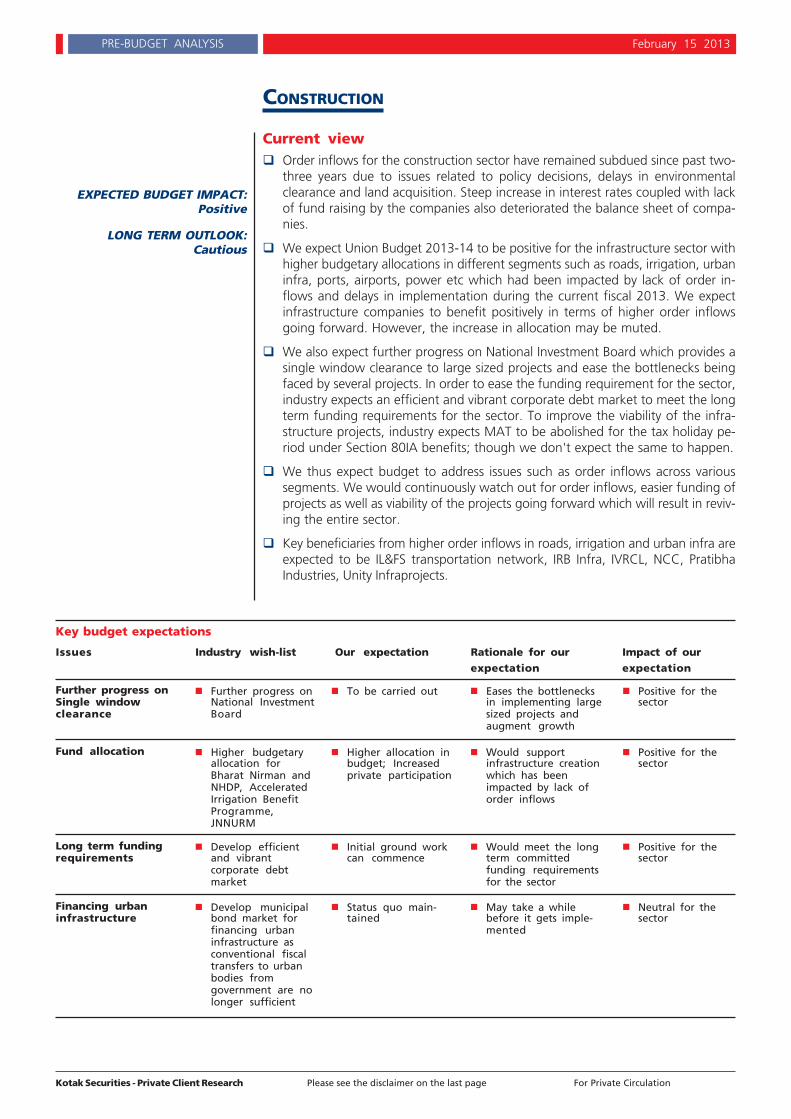

PRE-BUDGET ANALYSIS February 15 2013

CONSTRUCTION

Current view Order inflows for the construction sector have remained subdued since past two-

three years due to issues related to policy decisions, delays in environmentalclearance and land acquisition. Steep increase in interest rates coupled with lackof fund raising by the companies also deteriorated the balance sheet of compa-nies.

We expect Union Budget 2013-14 to be positive for the infrastructure sector withhigher budgetary allocations in different segments such as roads, irrigation, urbaninfra, ports, airports, power etc which had been impacted by lack of order in-flows and delays in implementation during the current fiscal 2013. We expectinfrastructure companies to benefit positively in terms of higher order inflowsgoing forward. However, the increase in allocation may be muted.

We also expect further progress on National Investment Board which provides asingle window clearance to large sized projects and ease the bottlenecks beingfaced by several projects. In order to ease the funding requirement for the sector,industry expects an efficient and vibrant corporate debt market to meet the longterm funding requirements for the sector. To improve the viability of the infra-structure projects, industry expects MAT to be abolished for the tax holiday pe-riod under Section 80IA benefits; though we don't expect the same to happen.

We thus expect budget to address issues such as order inflows across varioussegments. We would continuously watch out for order inflows, easier funding ofprojects as well as viability of the projects going forward which will result in reviv-ing the entire sector.

Key beneficiaries from higher order inflows in roads, irrigation and urban infra areexpected to be IL&FS transportation network, IRB Infra, IVRCL, NCC, PratibhaIndustries, Unity Infraprojects.

EXPECTED BUDGET IMPACT:Positive

LONG TERM OUTLOOK:Cautious

Further progress onNational InvestmentBoard

Further progress onSingle windowclearance

To be carried out Eases the bottlenecksin implementing largesized projects andaugment growth

Positive for thesector

Key budget expectations

Issues Industry wish-list Our expectation Rationale for our Impact of ourexpectation expectation

Higher budgetaryallocation forBharat Nirman andNHDP, AcceleratedIrrigation BenefitProgramme,JNNURM

Fund allocation Higher allocation inbudget; Increasedprivate participation

Would supportinfrastructure creationwhich has beenimpacted by lack oforder inflows

Positive for thesector

Develop efficientand vibrantcorporate debtmarket

Long term fundingrequirements

Initial ground workcan commence

Would meet the longterm committedfunding requirementsfor the sector

Positive for thesector

Develop municipalbond market forfinancing urbaninfrastructure asconventional fiscaltransfers to urbanbodies fromgovernment are nolonger sufficient

Financing urbaninfrastructure

Status quo main-tained

May take a whilebefore it gets imple-mented

Neutral for thesector

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 20

PRE-BUDGET ANALYSIS February 15, 2013

Top picks

Company Price EPS (Rs) PE (x) Recommendation(Rs) FY13E FY14E FY13E FY14E as per our last

report

IL&FS TRANSPORTATION NETWORKS 190 27.9 27.5 6.8 6.9 BUY

IRB INFRASTRUCTURE 114 15.5 8.7 7.4 13.1 BUY

UNITY INFRAPROJECTS 37 13.2 14.9 2.8 2.5 BUY

PRATIBHA INDUSTRIES 42 9.5 11.6 4.4 3.6 BUY

Source: Kotak Securities - Private Client Research

Key budget expectations

Issues Industry wish-list Our expectation Rationale for our Impact of ourexpectation expectation

Construction (contd...)

MAT should beabolished for the taxholiday period underSection 80IA toimprove viability ofprojects

MAT during theperiod of availmentof Section 80IA

Status quomaintained

Tax collection forgovernment may getimpacted

Neutral for thesector

Players havingmultiple SPVs shouldbe allowed to set offthe losses incurred inone SPV againstprofits earned inother SPVs

Tax offsets to lossmaking SPVs

Status quomaintained

Tax collection forgovernment may getimpacted

Neutral for thesector

Full pass through ofDDT for infrastruc-ture SPVs

Dividend distributiontax for SPVs

Likely to beallowed

DDT exemption is likelyto benefit many compa-nies since most of themhave multi layer holdingstructure

Positive forplayers carryingout projects inseparate SPVstructures

Source: Kotak Securities - Private Client Research, Industry

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 38

PRE-BUDGET ANALYSIS February 15, 2013

DisclaimerThis document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any otherperson. Persons into whose possession this document may come are required to observe these restrictions.

This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report is not to be construedas an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It is for thegeneral information of clients of Kotak Securities Ltd. It does not constitute a personal recommendation or take into account the particular investment ob-jectives, financial situations, or needs of individual clients.

We have reviewed the report, and in so far as it includes current or historical information, it is believed to be reliable though its accuracy or completenesscannot be guaranteed. Neither Kotak Securities Limited, nor any person connected with it, accepts any liability arising from the use of this document. Therecipients of this material should rely on their own investigations and take their own professional advice. Price and value of the investments referred to inthis material may go up or down. Past performance is not a guide for future performance. Certain transactions -including those involving futures, optionsand other derivatives as well as non-investment grade securities - involve substantial risk and are not suitable for all investors. Reports based on technicalanalysis centers on studying charts of a stock’s price movement and trading volume, as opposed to focusing on a company’s fundamentals and as such, maynot match with a report on a company’s fundamentals.

We do not have any information other than information available to general public with regard to budget proposals. The industry expecta-tions are based on information got from sources like respective industry associations, FICCI, CII, companies, media and other public sources.This report contains budget expectations of our experts and its impact on specific sectors and companies, which may or may not come true.

Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavor to update on a reasonable basis the informa-tion discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. Prospective investors and others arecautioned that any forward-looking statements are not predictions and may be subject to change without notice. Our proprietary trading and investmentbusinesses may make investment decisions that are inconsistent with the recommendations expressed herein.

Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report has been prepared by thePrivate Client Group . The views and opinions expressed in this document may or may not match or may be contrary with the views, estimates, rating, targetprice of the Institutional Equities Research Group of Kotak Securities Limited.

We and our affiliates, officers, directors, and employees world wide may: (a) from time to time, have long or short positions in, and buy or sell the securitiesthereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensationor act as a market maker in the financial instruments of the company (ies) discussed herein or act as advisor or lender / borrower to such company (ies) orhave other potential conflict of interest with respect to any recommendation and related information and opinions. "Kotak Securities Limited (KSL) may haveproprietary long/short position in the above mentioned scrips and therefore should be considered as interested."

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company orcompanies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations orviews expressed in this report.

No part of this material may be duplicated in any form and/or redistributed without Kotak Securities’ prior written consent.

Kotak Securities Limited. Regd. Office: Bakhtawar, 1st Floor, 229, Nariman Point, Mumbai - 400021.Tel No 022-66341100.Correspondence Address: Infinity IT Park, Bldg. No 21, Opp Film City Road, A K Vaidya Marg, Malad (East), Mumbai 400097. Tel no: 66056825.SEBI Reg No: NSE INB/INF/INE 230808130, BSE INB 010808153/INF 011133230, OTC INB 200808136, MCXSX INE 260808130.Investments in securities are subject to market risk; please read the SEBI prescribed Combined Risk Disclosure Document prior to investing.Compliance Officer Details: Mr. Sandeep Chordia. Call: 022 6605 6825, or Email: [email protected]

Fundamental Research TeamDipen [email protected]+91 22 6621 6301

Sanjeev ZarbadeCapital Goods, [email protected]+91 22 6621 6305

Teena VirmaniConstruction, [email protected]+91 22 6621 6302

Saurabh AgrawalMetals, [email protected]+91 22 6621 6309

Saday SinhaBanking, NBFC, [email protected]+91 22 6621 6312

Arun [email protected]+91 22 6621 6143

Ruchir KhareCapital Goods, [email protected]+91 22 6621 6448

Ritwik RaiFMCG, [email protected]+91 22 6621 6310

Sumit PokharnaOil and [email protected]+91 22 6621 6313

Amit AgarwalLogistics, [email protected]+91 22 6621 6222

Jayesh [email protected]+91 22 6652 9172

K. [email protected]+91 22 6621 6311

Technical Research Team

Shrikant [email protected]+91 22 6621 6360

Amol [email protected]+91 20 6620 3350

Premshankar [email protected]+91 22 6621 6261

Derivatives Research TeamSahaj [email protected]+91 22 6621 6343

Rahul [email protected]+91 22 6621 6198

Malay [email protected]+91 22 6621 6350

Prashanth [email protected]+91 22 6621 6110