quest softech (india) limited

TRANSCRIPT

QUEST SOFTECH (INDIA) LIMITED

The Company was incorporated as Quest Softech (India) Private Limited on 27th March, 2000 under

the Companies Act, 1956 and was converted into a public limited company on 18th March 2008 vide

Certificate of Incorporation issued by the Registrar of Companies, Mumbai, Maharashtra.

Regd. Office: 27, Maker Bhavan II, 18, New Marine Lines, Mumbai – 400 020. INDIA.

Tel No.: 022 – 6615 7700 / 03; Fax No.: 022 – 6615 7704; Website: www.questsoftech.co.in

Contact Person: Mr. Siluvairajan, Compliance Officer; e-mail: [email protected]

INFORMATION MEMORANDUM FOR LISTING OF 1,00,00,000 EQUITY SHARES OF RS. 10/-

EACH FULLY PAID UP, PURSUANT TO THE SCHEME OF ARRANGEMENT BETWEEN THE

COMPANY AND CONTINENTAL CONTROLS LIMITED AND THEIR RESPECTIVE

SHAREHOLDERS AND CREDITORS.

GENERAL RISKS

Investment in equity and equity related securities involve a degree of risk and investors should not

invest any funds in the equity shares of Quest Softech (India) Limited unless they can afford to take

the risk of losing their investment. Investors are advised to read the risk factors carefully before taking

an investment decision in the shares of the Company. For taking an investment decision, investors

must rely on their own examination of the Company including the risks involved. The securities have

not been recommended or approved by Securities and Exchange Board of India (SEBI) nor does

SEBI guarantee the accuracy or adequacy of this document. Specific attention of investors is invited

to the statement of risk factors on page 5-6 of this Information Memorandum.

ABSOLUTE RESPONSIBILITY OF QUEST SOFTECH (INDIA) LIMITED

Quest Softech (India) Limited having made all reasonable inquiries, accepts responsibility for, and

confirms that this Information Memorandum contains all information with regard to the Company

which is material, that the information contained in this Information Memorandum is true and correct in

all material aspects and is not misleading in any material respect, that the opinions and intentions

expressed herein are honestly held and that there are no other facts, the omission of which makes

this document as a whole or any of such information or the expression of any such opinions or

intentions misleading in any material respect.

LISTING

The Equity Shares of Quest Softech (India) Limited are proposed to be listed on the Bombay Stock

Exchange Limited (BSE). The Company has submitted this Information Memorandum with BSE and

the same has been made available on the Company’s website viz. www.questsoftech.co.in. The

Information Memorandum would also be made available on the website of BSE viz.

www.bseindia.com.

REGISTRAR AND SHARE TRANSFER AGENT:

Purva Sharegistry (India) Pvt. Ltd.

33, Printing House, 28-D, Police Court Lane, Behind Old Handloom House, Fort, Mumbai 400 001.

Tel: 91-22-2262 6407 / 6634 8073;

Contact Person: Ms. Rajesh Shah;

e-mail: [email protected]

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

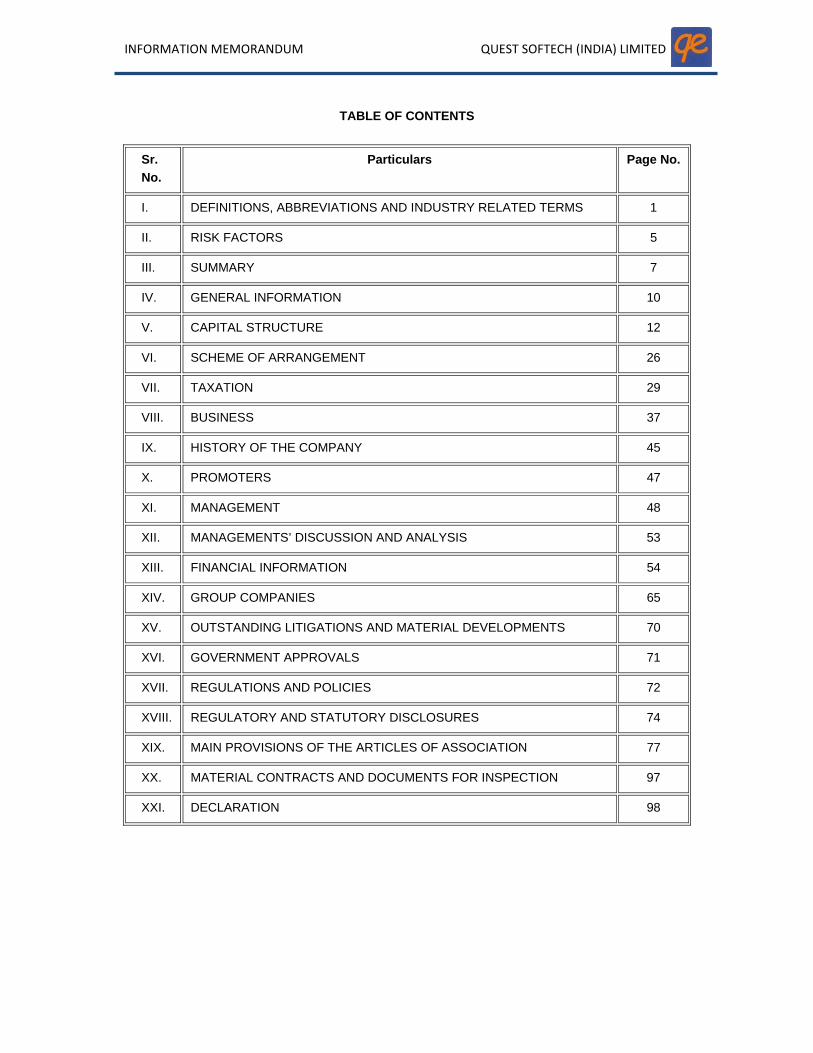

TABLE OF CONTENTS

Sr.

No.

Particulars Page No.

I. DEFINITIONS, ABBREVIATIONS AND INDUSTRY RELATED TERMS 1

II. RISK FACTORS 5

III. SUMMARY 7

IV. GENERAL INFORMATION 10

V. CAPITAL STRUCTURE 12

VI. SCHEME OF ARRANGEMENT 26

VII. TAXATION 29

VIII. BUSINESS 37

IX. HISTORY OF THE COMPANY 45

X. PROMOTERS 47

XI. MANAGEMENT 48

XII. MANAGEMENTS’ DISCUSSION AND ANALYSIS 53

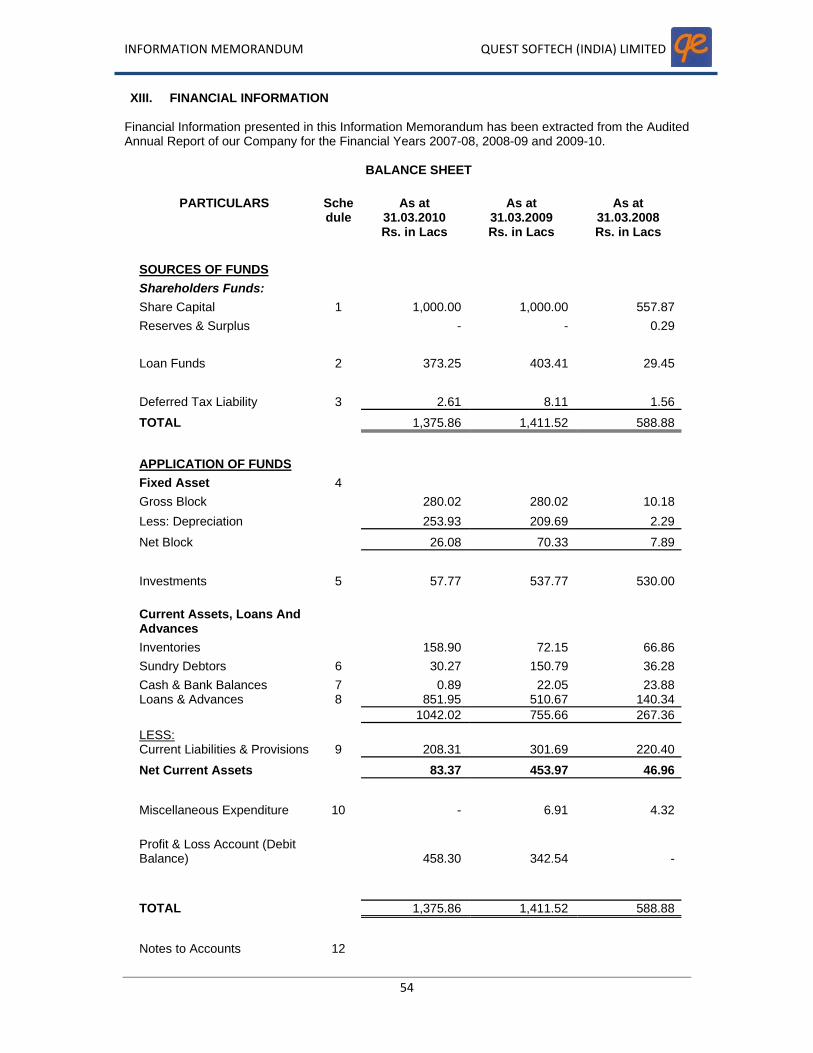

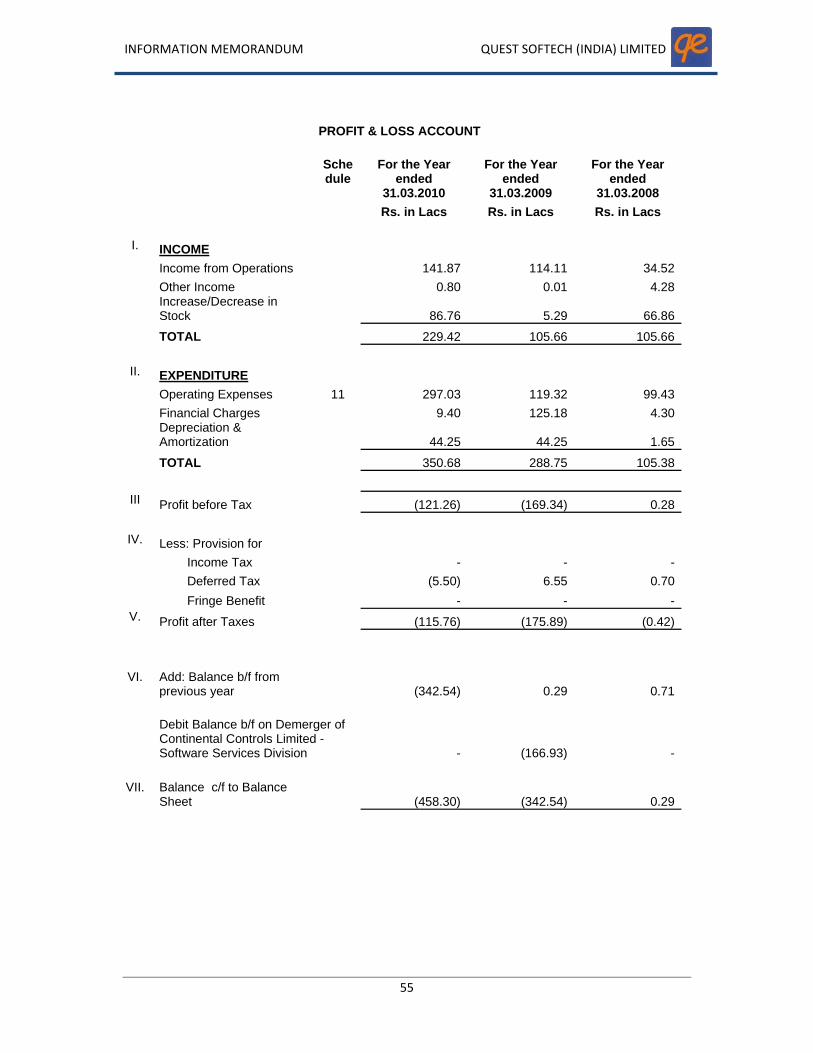

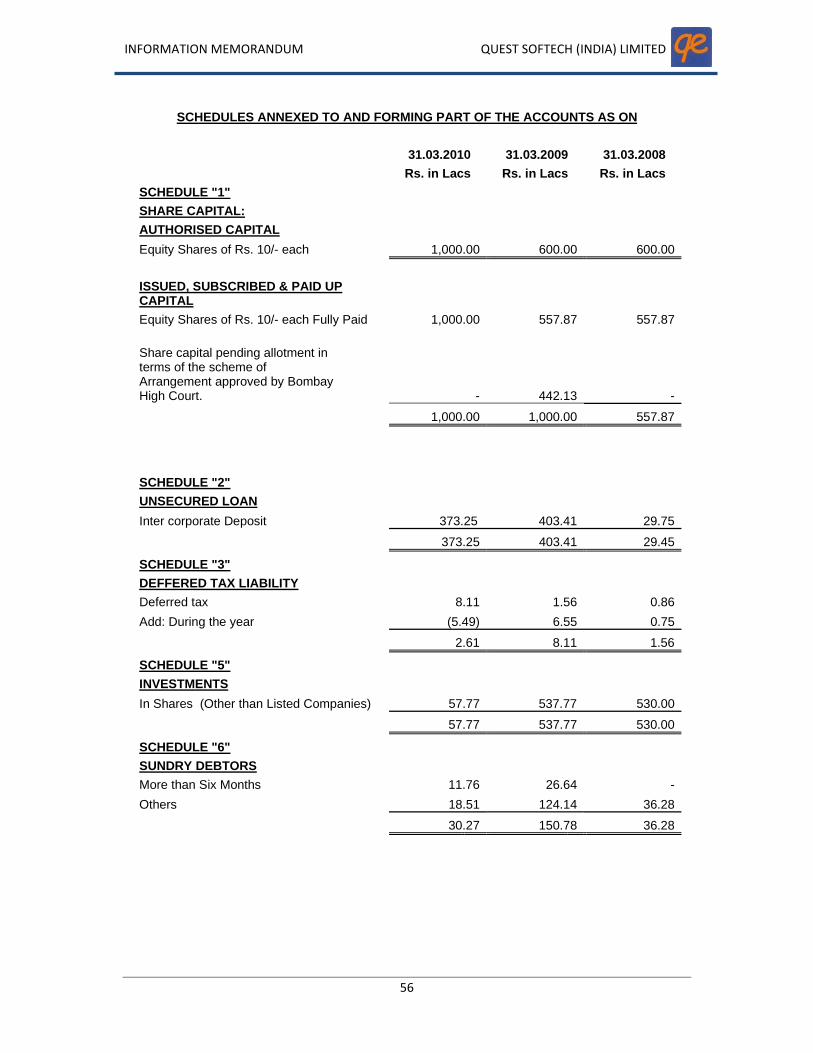

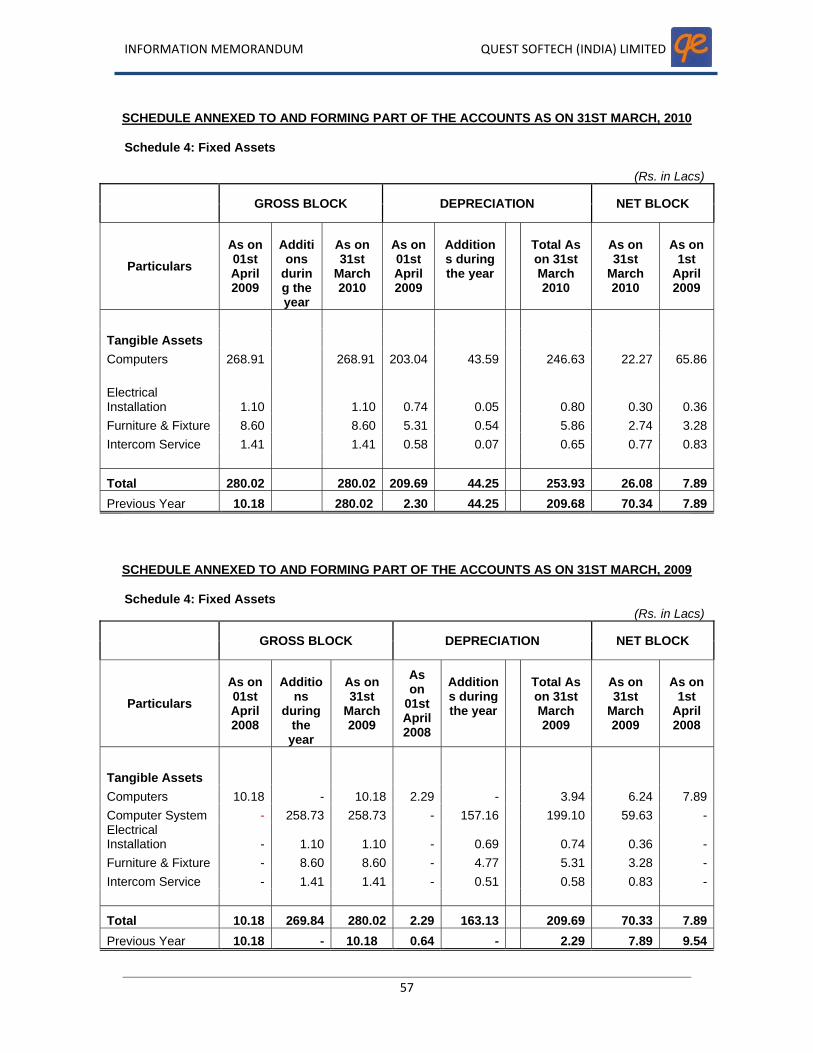

XIII. FINANCIAL INFORMATION 54

XIV. GROUP COMPANIES 65

XV. OUTSTANDING LITIGATIONS AND MATERIAL DEVELOPMENTS 70

XVI. GOVERNMENT APPROVALS 71

XVII. REGULATIONS AND POLICIES 72

XVIII. REGULATORY AND STATUTORY DISCLOSURES 74

XIX. MAIN PROVISIONS OF THE ARTICLES OF ASSOCIATION 77

XX. MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION 97

XXI. DECLARATION 98

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

1

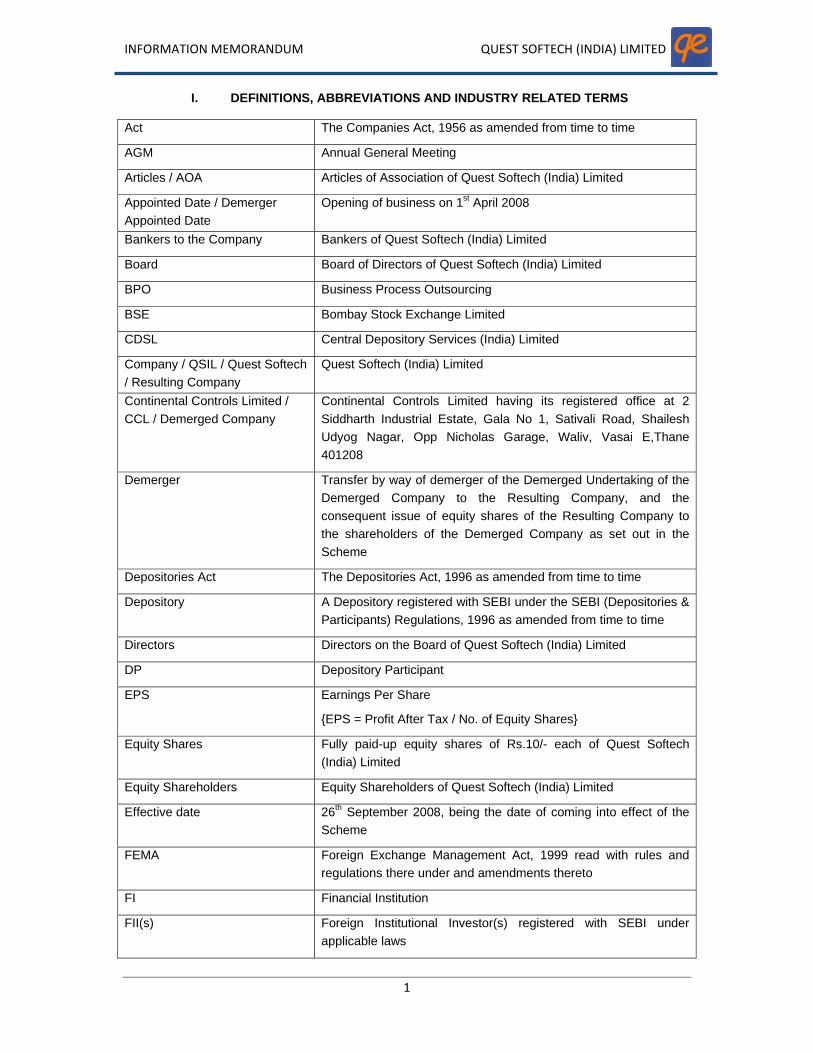

I. DEFINITIONS, ABBREVIATIONS AND INDUSTRY RELATED TERMS

Act The Companies Act, 1956 as amended from time to time

AGM Annual General Meeting

Articles / AOA Articles of Association of Quest Softech (India) Limited

Appointed Date / Demerger

Appointed Date

Opening of business on 1st April 2008

Bankers to the Company Bankers of Quest Softech (India) Limited

Board Board of Directors of Quest Softech (India) Limited

BPO Business Process Outsourcing

BSE Bombay Stock Exchange Limited

CDSL Central Depository Services (India) Limited

Company / QSIL / Quest Softech

/ Resulting Company

Quest Softech (India) Limited

Continental Controls Limited /

CCL / Demerged Company

Continental Controls Limited having its registered office at 2

Siddharth Industrial Estate, Gala No 1, Sativali Road, Shailesh

Udyog Nagar, Opp Nicholas Garage, Waliv, Vasai E,Thane

401208

Demerger Transfer by way of demerger of the Demerged Undertaking of the

Demerged Company to the Resulting Company, and the

consequent issue of equity shares of the Resulting Company to

the shareholders of the Demerged Company as set out in the

Scheme

Depositories Act The Depositories Act, 1996 as amended from time to time

Depository A Depository registered with SEBI under the SEBI (Depositories &

Participants) Regulations, 1996 as amended from time to time

Directors Directors on the Board of Quest Softech (India) Limited

DP Depository Participant

EPS Earnings Per Share

{EPS = Profit After Tax / No. of Equity Shares}

Equity Shares Fully paid-up equity shares of Rs.10/- each of Quest Softech

(India) Limited

Equity Shareholders Equity Shareholders of Quest Softech (India) Limited

Effective date 26th September 2008, being the date of coming into effect of the

Scheme

FEMA Foreign Exchange Management Act, 1999 read with rules and

regulations there under and amendments thereto

FI Financial Institution

FII(s) Foreign Institutional Investor(s) registered with SEBI under

applicable laws

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

2

FY Financial Year (the 12 month period starting on 1st April in a year

and ending on 31st March of subsequent year)

Information Memorandum This Information Memorandum

IT Information Technology

IT Act Income Tax Act, 1961 as amended

ITES Information Technology Enabled Services

KPO Knowledge Process Outsourcing

MOA Memorandum of Association of Quest Softech (India) Limited

NA Not Applicable

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

P/E Ratio Price/Earnings Ratio

PAT Profit After Tax

RBI Reserve Bank of India

Record Date 3rd July 2009, being the date fixed by the Board of Directors of

Quest Softech (India) Limited and Continental Controls Limited

pursuant to Part – I Clause A of the Scheme

Registrar and Share Transfer

Agent / Registrars / Sharepro

‘Purva Sharegistry India Private Limited’ having its Registered

Office at 33, Printing House, 28-D, Police Court Lane, B/H Old

Handloom House, Fort, Mumbai – 400001

Resulting Company See “Company” above

ROC Registrar of Companies, Maharashtra, Mumbai

Scheme / Scheme of

Arrangement

Scheme of Arrangement under Section 391 to 394 and other

applicable provisions of the Companies Act, 1956 between Quest

Softech (India) Limited and Continental Controls Limited and their

respective Shareholders and Creditors for the Demerger of the

Software Services Division Undertaking of Continental Controls

Limited into Quest Softech (India) Limited (with Appointed Date

being 1st April 2008) and Reduction of the Issued, Subscribed and

Paid up share capital of Continental Controls Limited, as

sanctioned by the Hon’ble High Court of Judicature at Bombay

vide its Order dated 5th September 2008, which was filed with the

Registrar of Companies, Maharashtra on 26th September 2008,

which is the Effective Date of the Scheme.

SEBI Securities and Exchange Board of India

SEBI Act Securities and Exchange Board of India Act, 1992

SEBI (ICDR) RGULATIONS Securities and Exchange Board of India (Issue of Capital and

Disclosure Requirements) Regulations, 2009, as amended,

including instructions and clarifications issued by SEBI from time

to time

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

3

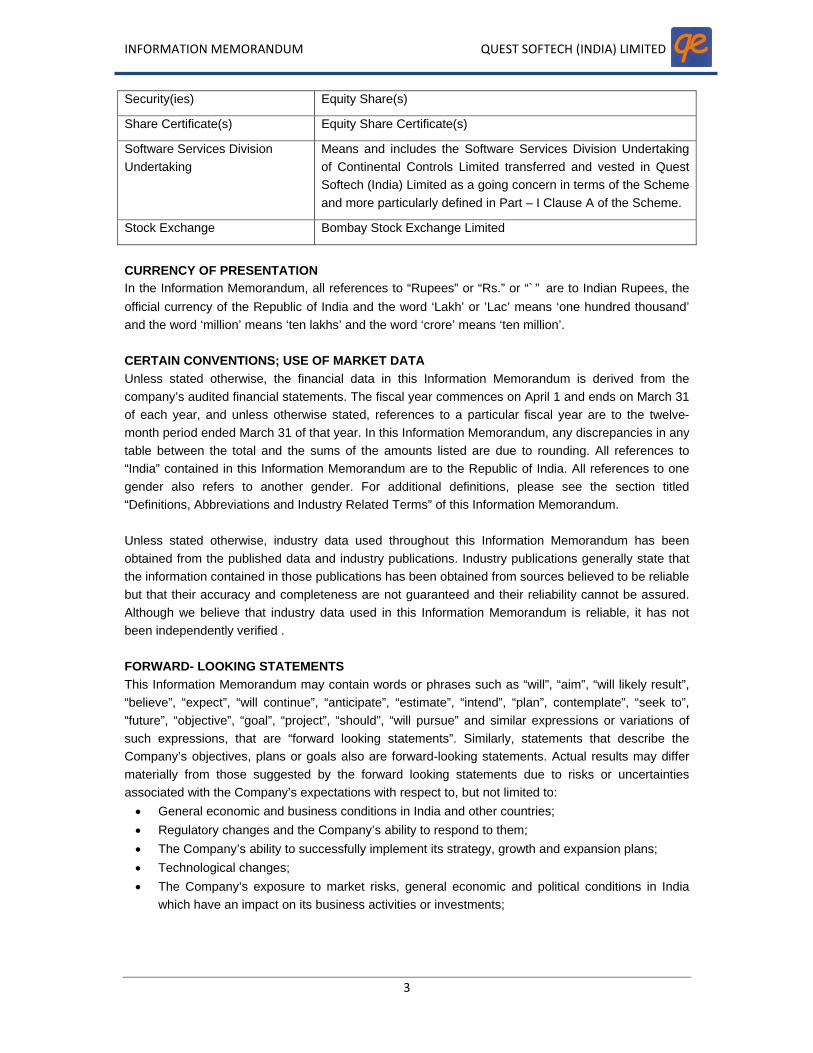

Security(ies) Equity Share(s)

Share Certificate(s) Equity Share Certificate(s)

Software Services Division

Undertaking

Means and includes the Software Services Division Undertaking

of Continental Controls Limited transferred and vested in Quest

Softech (India) Limited as a going concern in terms of the Scheme

and more particularly defined in Part – I Clause A of the Scheme.

Stock Exchange Bombay Stock Exchange Limited

CURRENCY OF PRESENTATION

In the Information Memorandum, all references to “Rupees” or “Rs.” or “`” are to Indian Rupees, the

official currency of the Republic of India and the word ‘Lakh’ or ’Lac’ means ‘one hundred thousand’

and the word ‘million’ means ‘ten lakhs’ and the word ‘crore’ means ‘ten million’.

CERTAIN CONVENTIONS; USE OF MARKET DATA

Unless stated otherwise, the financial data in this Information Memorandum is derived from the

company’s audited financial statements. The fiscal year commences on April 1 and ends on March 31

of each year, and unless otherwise stated, references to a particular fiscal year are to the twelve-

month period ended March 31 of that year. In this Information Memorandum, any discrepancies in any

table between the total and the sums of the amounts listed are due to rounding. All references to

“India” contained in this Information Memorandum are to the Republic of India. All references to one

gender also refers to another gender. For additional definitions, please see the section titled

“Definitions, Abbreviations and Industry Related Terms” of this Information Memorandum.

Unless stated otherwise, industry data used throughout this Information Memorandum has been

obtained from the published data and industry publications. Industry publications generally state that

the information contained in those publications has been obtained from sources believed to be reliable

but that their accuracy and completeness are not guaranteed and their reliability cannot be assured.

Although we believe that industry data used in this Information Memorandum is reliable, it has not

been independently verified .

FORWARD- LOOKING STATEMENTS

This Information Memorandum may contain words or phrases such as “will”, “aim”, “will likely result”,

“believe”, “expect”, “will continue”, “anticipate”, “estimate”, “intend”, “plan”, contemplate”, “seek to”,

“future”, “objective”, “goal”, “project”, “should”, “will pursue” and similar expressions or variations of

such expressions, that are “forward looking statements”. Similarly, statements that describe the

Company’s objectives, plans or goals also are forward-looking statements. Actual results may differ

materially from those suggested by the forward looking statements due to risks or uncertainties

associated with the Company’s expectations with respect to, but not limited to:

General economic and business conditions in India and other countries;

Regulatory changes and the Company’s ability to respond to them;

The Company’s ability to successfully implement its strategy, growth and expansion plans;

Technological changes;

The Company’s exposure to market risks, general economic and political conditions in India

which have an impact on its business activities or investments;

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

4

The monetary and fiscal policies of India, inflation, deflation, unanticipated turbulence in interest

rates, foreign exchange rates, equity prices or other rates or prices, the performance of the

financial markets in India and globally;

Changes in domestic and foreign laws, regulations and taxes and changes in competition in the

industry.

For further discussion of factors that could cause the actual results to differ, please see the section

titled “Risk Factors” of this Information Memorandum. By their nature, certain market risk disclosures

are only estimates and could be materially different from what actually occurs in the future. As a

result, actual future gains or losses could materially differ from those that have been estimated.

The Company does not have any obligation to, and does not intend to, update or otherwise revise any

statements reflecting circumstances arising after the date hereof or to reflect the occurrence of

underlying events, even if the underlying assumptions do not materialize.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

5

II. RISK FACTORS

An investment in equity shares involves a high degree of risk. You should carefully consider all of the

information in this Information Memorandum, including the risks of uncertainties described below. If

any of the following risks actually occur, our business, financial condition and results of the operations

could suffer, the trading price of our Equity Shares could decline, and you may lose all or part of your

investment. The business operations of the Issuer could also be affected by additional factors other

than those mentioned below and that are not presently known to the Company or the Management of

the Company or that are currently considered to be immaterial to the business and operations of the

Company.

1. Technological breakthroughs may render existing infrastructure redundant

The BPO industry is a rapidly evolving sector witnessing new technological breakthroughs

which may render the existing technology/infrastructure redundant. The future success of the

Company would depend on its ability to anticipate these changes and develop new product

and service offered.

2. Risks relating to intellectual property infringement

The Company relies on a combination of trade secrets, confidentiality procedures and

contractual provisions to protect its intellectual property. There are currently no pending or

threatened intellectual property claims against the Company. However if it becomes liable to

third parties for infringing their intellectual property rights then the Company could be required

to pay substantial damages and be forced to develop non – infringing technology or obtain a

license.

3. Disruptions in telecommunications and basic infrastructure could harm the service

delivery model, which could result in client dissatisfaction and a reduction in the

revenues of the Company

The services the Company provides are often critical to the clients business and any failure to

provide those services on a timely manner could result in a claim for substantial damages

against the Company. Any temporary or permanent loss of equipments or systems or any

disruptions to basic infrastructure such as power and telecommunication would impede the

Company’s ability to provide services to the clients, could expose the Company to a liability

claims and could have a material adverse effect on the reputation, results of operation,

financial conditions and cash flows

4. Low availability of skilled manpower may impact the business of the company

The IT/BPO Industry is human-resource intensive and is dependent on individual skill sets,

which may or may not be readily available or replaceable. Low availability of skilled

manpower and high rate of employee turnover in the industry will lead to additional cost of

investing in employee’s retention and training.

5. Stiff Competition

The Company faces competition from large established players in the industry. The industry

structure is skewed with major part of the business being captured by few large players who

can command a premium for the services rendered. This is opposed to the increasing

competition and massive price cutting faced by the smaller players. This has rendered small

businesses unviable and is responsible for a major shakeout in the industry.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

6

6. Exchange Rate Fluctuation

The Company reports its financial results in Rupees, but a significant portion of income in

future would be denominated in US Dollar. The appreciation of the Rupee against the US

Dollar would have a material adverse effect on the results of operations.

7. Political Risk

Political Risk is an inherent risk faced by all the businesses operating on a global scale. Bills

passed by various states in the USA opposing the outsourcing of government contracts to

firms of developing countries. This is a matter of concern for companies operating in the ITES

segment as their profitability may be impacted.

8. Sensitivity to the economy and extraneous factors

The Company’s performance is highly correlated to the performance of the economy and the

financial markets. The health of the economy and the financial markets in turn depends on the

domestic economic growth, state of the global economy and business and consumer

confidence, among other factors. Any event disturbing the dynamic balance of these diverse

factors may directly or indirectly affect the performance of the Company.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

7

III. SUMMARY

INDUSTRY SUMMARY

INDIAN ITeS AND BPO INDUSTRY

The Indian ITeS-BPO industry has been consistently growing over the past few years, in spite of rising

competition from countries such as Philippines, China, Brazil, Mexico and Ireland. Its contribution to

the service sector and to the country’s GDP has also been increasing over these years. The revenue

of the sector (IT-BPO) has manifolded during the last decade from merely US$8.3 bn in 2000 to

around US$71 bn in 2009 at a CAGR growth of 27%1.

The ITeS/BPO notably is the fastest-growing segment within the IT-BPO sector, and during the last

decade it grew at a CAGR of 42.8%; the IT services and software revenue grew at a CAGR of 26.8%.

In the last 10 years, the domestic IT services and software products and engineering services market

grew by 21% annually and reached US$10.5 bn in 2009.

Going ahead, the challenge for the industry players lies in maintaining the level of competency and

offering high level customer satisfaction at an affordable price.

INDIAN ITeS-BPO INDUSTRY AND ECONOMIC GROWTH

The Indian ITeS-BPO industry has revolutionized global sourcing and has emerged as one of the

sunrise sectors for the country.

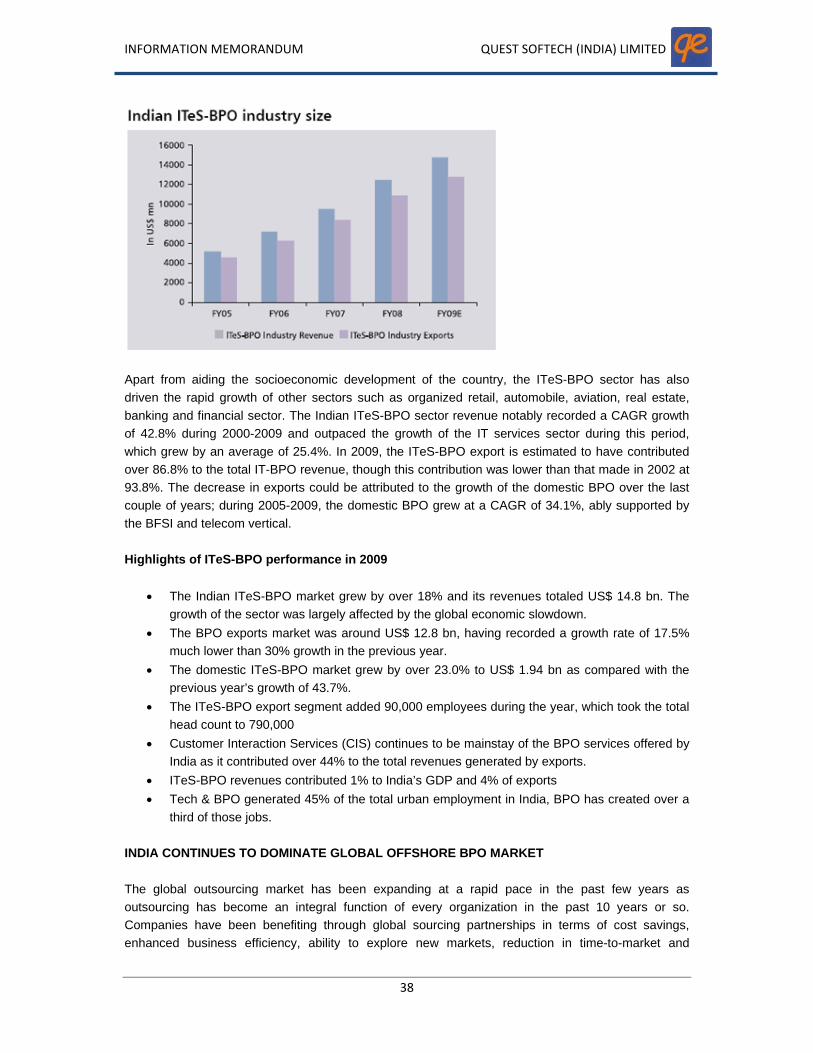

The Indian ITeS-BPO sector revenue notably recorded a CAGR growth of 42.8% during 2000-2009

and outpaced the growth of the IT services sector during this period, which grew by an average of

25.4%. In 2009, the ITeS-BPO export is estimated to have contributed over 86.8% to the total IT-BPO

revenue, though this contribution was lower than that made in 2002 at 93.8%. The decrease in

exports could be attributed to the growth of the domestic BPO over the last couple of years; during

2005-2009, the domestic BPO grew at a CAGR of 34.1%, ably supported by the BFSI and telecom

vertical.

INDIA CONTINUES TO DOMINATE GLOBAL OFFSHORE BPO MARKET

The global outsourcing market has been expanding at a rapid pace in the past few years as

outsourcing has become an integral function of every organization in the past 10 years or so.

Companies have been benefiting through global sourcing partnerships in terms of cost savings,

enhanced business efficiency, ability to explore new markets, reduction in time-to-market and

products and services among others.

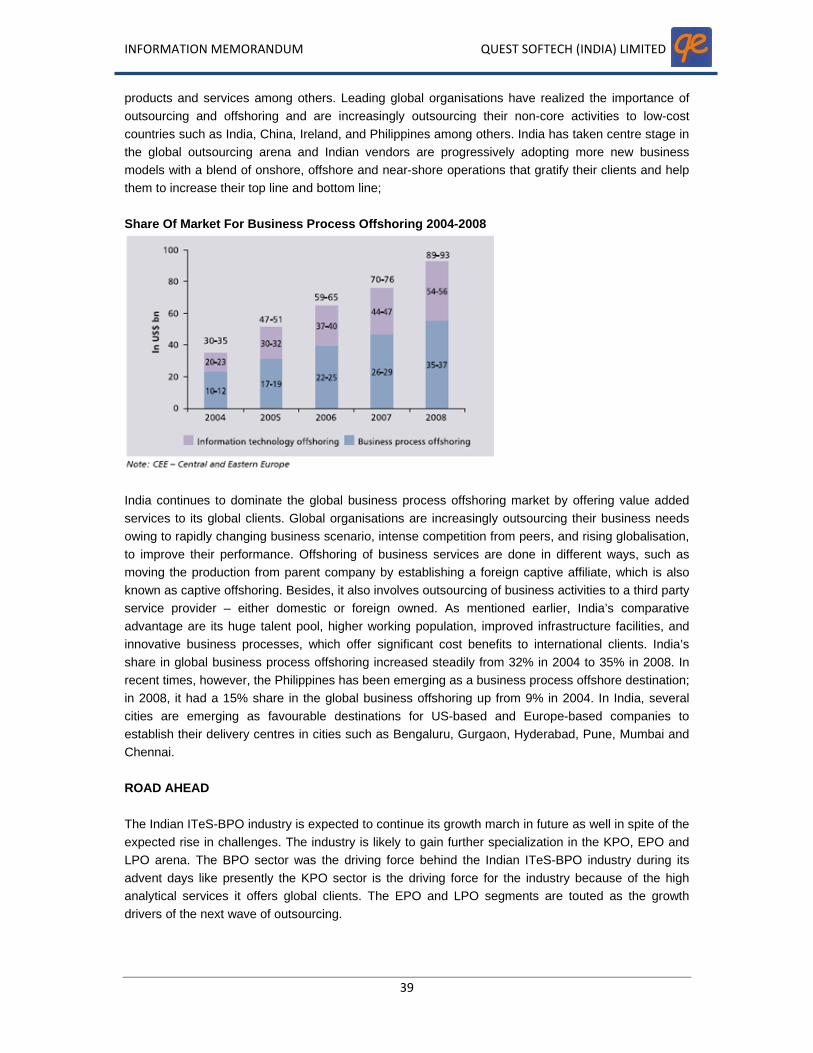

India continues to dominate the global business process offshoring market by offering value added

services to its global clients. Global organisations are increasingly outsourcing their business needs

owing to rapidly changing business scenario, intense competition from peers, and rising globalisation,

to improve their performance. As mentioned earlier, India’s comparative advantage are its huge talent

pool, higher working population, improved infrastructure facilities, and innovative business processes,

which offer significant cost benefits to international clients. India’s share in global business process

offshoring increased steadily from 32% in 2004 to 35% in 2008, according to data from UNCTAD-

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

8

Everest Research Institute. In India, several cities are emerging as favourable destinations for US-

based and Europe-based companies to establish their delivery centres in cities such as Bengaluru,

Gurgaon, Hyderabad, Pune, Mumbai and Chennai.

ROAD AHEAD

The Indian ITeS-BPO industry is expected to continue its growth march in future as well in spite of the

expected rise in challenges. The industry is likely to gain further specialization in the KPO, EPO and

LPO arena. The BPO sector was the driving force behind the Indian ITeS-BPO industry during its

advent days like presently the KPO sector is the driving force for the industry because of the high

analytical services it offers global clients. The EPO and LPO segments are touted as the growth

drivers of the next wave of outsourcing.

However, given the current global recession, the ITeS-BPO industry is registering lower growth rate

as compared with the previous years. For instance, during 2004 to 2008, the sector registered an

average growth of around 39%, while in 2009, the growth declined sharply to 18.2%. Consequently,

the BPO export revenue also recorded a much lower growth of 17.5% during 2009 as compared with

an average annual growth rate of 37% between 2004 to 2008. It is important to mention that the

sector’s share in overall services exports has gone up remarkably over the past few years from 5.5%

in 2001 to 12.8% in 2009. The Indian ITeS-BPO exports alone provided direct employment to around

0.8 mn people, not including the indirect employment. The sector has massively developed the overall

economic and social landscape of the country.

However, the economic slowdown has opened up opportunities for the Indian ITeS-BPO companies,

as it is expected that the global companies would adopt outsourcing as an initiative to reduce cost.

The Indian companies have to be proactive to grab the opportunities and should venture into newer

markets, verticals and service line. Besides, the Indian ITeS-BPO companies should further explore

domestic market, which offers immense opportunities.

BUSINESS SUMMARY

HISTORY

Quest Softech (India) Limited was incorporated as Quest Softech (India) Private Limited on 27th

March 2000 under the Companies Act, 1956 and was converted into a public limited company on 18th

March 2008, and engaged in the business of IT/BPO Consultancy services related to the preparation

and maintenance of accounting information and reports.

QSIL TODAY

Our unique business process outsourcing methodology and approach work to optimize operations

across the full range of finance and accounting functions. We serve as a single window outsourcing

solution for all Finance, Accounting and Tax Related services. Our unique approach ensures a highly

professional, friendly, value for money service.

QSIL is able to offer a complete range of services for businesses and individuals. From individual tax

planning services to complex corporate consulting engagements, we are ready and able to be full

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

9

service accounting firm. Our skilled professionals offer both knowledge of technical financial topics

and experience in process operations.

Our services and concern for client satisfaction are reasonably priced, helping clients manage costs

while obtaining the services they need.

VISION

“To be a leading provider of financial services and knowledge based services to a global clientele by

offering value through innovative use of technology and harnessing the highest potential of its

people”.

CAPABILITIES

Multi Medium – Phone, Web, E-Mail, Print, Fax and Face-to-Face

Multi Process – Data Collection, Processing, Analytics, Presentation

Multi Industry – IT & Telecom, Healthcare & Pharma, FMCG/Consumer Goods, BFSI, Retail &

Manufacturing, Media, Others.

SERVICES

Accounting and Financial Services

Our Professionals handles Bookkeeping Services, Write-Up Services, Accounts Payable

Services, Financial Reporting Services and Account Reconciliation Services. Our Accounting

personnel can act as the back-office operation staff on behalf for clients however situated in our

office. We have an experienced team of CA's and Accounting personnel to efficiently manage

the Accounting processes.

o General Accounting and bookkeeping processes

o Fixed Asset and capital accounting processes

o Cost and Inventory Accounting processes

Tax Preparation Services

We provide all kinds of taxation related services including tax preparation and tax consulting.

We are updated with the latest technology, software and workflow processes to enhance on-

the-job efficiency for tax processing.

Financial Analysis Services

Our Financial Analysis services can be utilized to create a complete picture of the financial

performance and streamlining operations. This will help in formulating strategic decisions

regarding your business organization's financial matters.

Financial Budgeting & MIS Services

Our expertise in budgeting & MIS planning can protect from possible financial crises and help to

run the business smoothly. By utilizing a unique methodology, we assess the business risks

associated with the budget and forecast processes. We then analyze key performance

indicators through the data collection process and management review.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

10

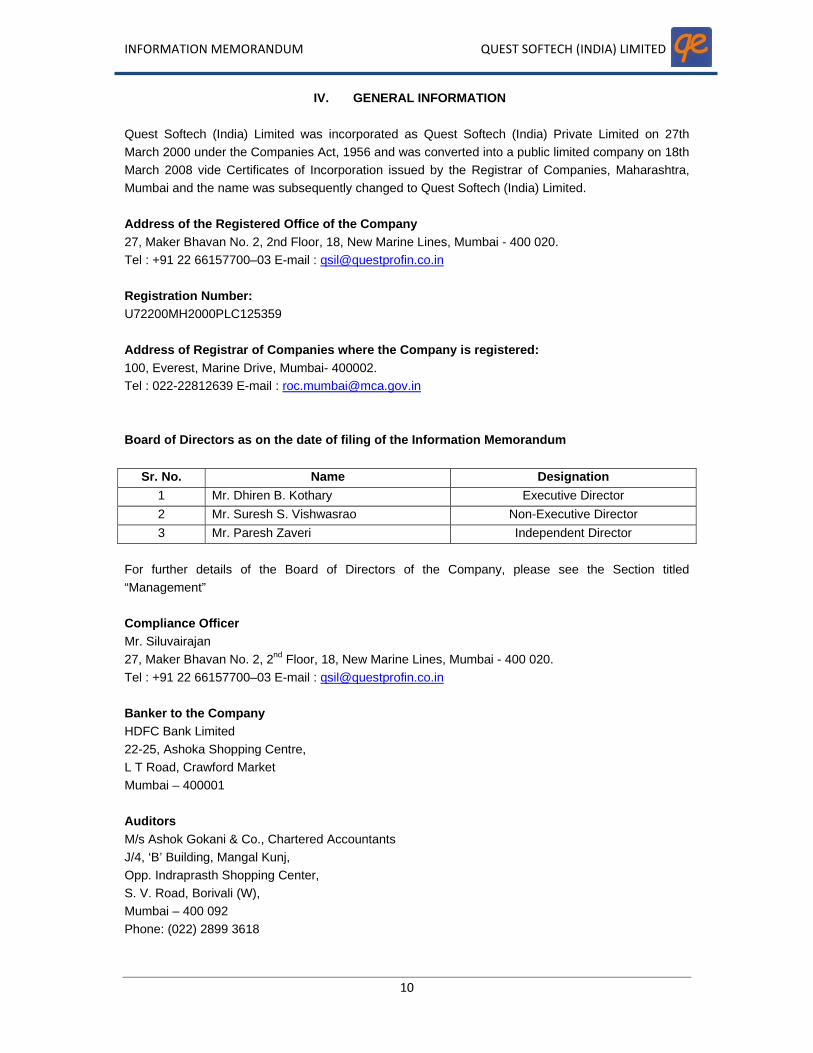

IV. GENERAL INFORMATION

Quest Softech (India) Limited was incorporated as Quest Softech (India) Private Limited on 27th

March 2000 under the Companies Act, 1956 and was converted into a public limited company on 18th

March 2008 vide Certificates of Incorporation issued by the Registrar of Companies, Maharashtra,

Mumbai and the name was subsequently changed to Quest Softech (India) Limited.

Address of the Registered Office of the Company

27, Maker Bhavan No. 2, 2nd Floor, 18, New Marine Lines, Mumbai - 400 020.

Tel : +91 22 66157700–03 E-mail : [email protected]

Registration Number:

U72200MH2000PLC125359

Address of Registrar of Companies where the Company is registered:

100, Everest, Marine Drive, Mumbai- 400002.

Tel : 022-22812639 E-mail : [email protected]

Board of Directors as on the date of filing of the Information Memorandum

Sr. No. Name Designation

1 Mr. Dhiren B. Kothary Executive Director

2 Mr. Suresh S. Vishwasrao Non-Executive Director

3 Mr. Paresh Zaveri Independent Director

For further details of the Board of Directors of the Company, please see the Section titled

“Management”

Compliance Officer

Mr. Siluvairajan

27, Maker Bhavan No. 2, 2nd Floor, 18, New Marine Lines, Mumbai - 400 020.

Tel : +91 22 66157700–03 E-mail : [email protected]

Banker to the Company

HDFC Bank Limited

22-25, Ashoka Shopping Centre,

L T Road, Crawford Market

Mumbai – 400001

Auditors

M/s Ashok Gokani & Co., Chartered Accountants

J/4, ‘B’ Building, Mangal Kunj,

Opp. Indraprasth Shopping Center,

S. V. Road, Borivali (W),

Mumbai – 400 092

Phone: (022) 2899 3618

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

11

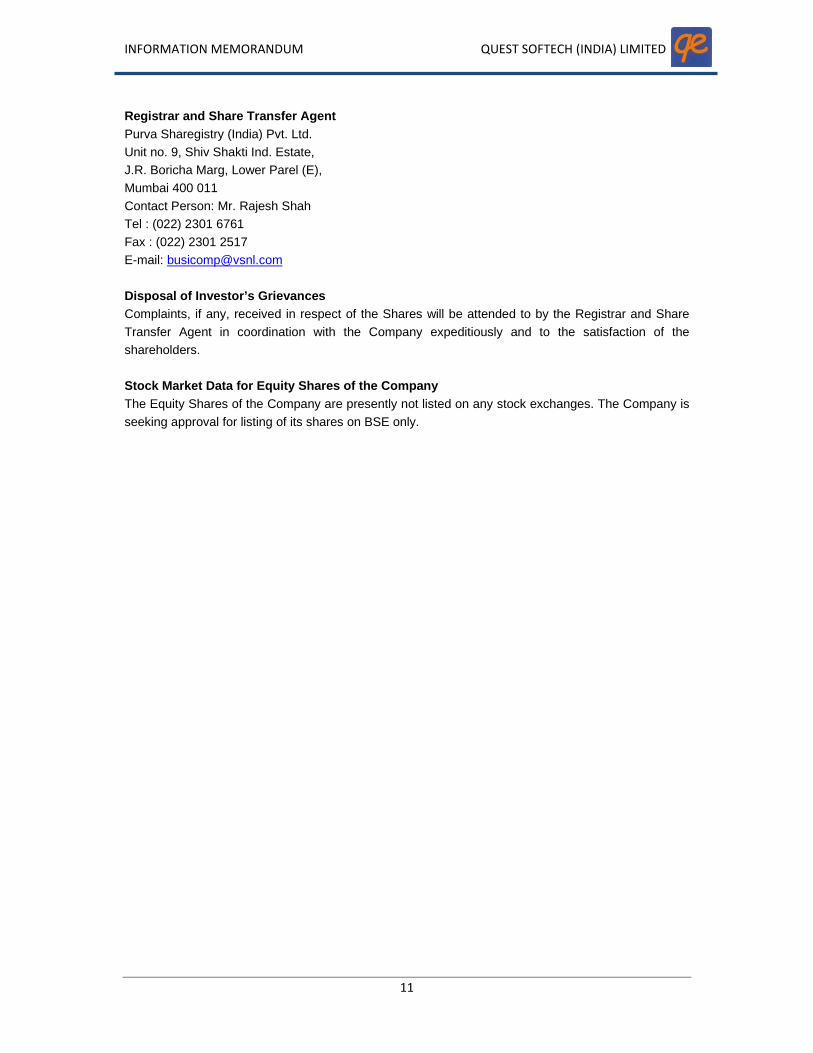

Registrar and Share Transfer Agent

Purva Sharegistry (India) Pvt. Ltd.

Unit no. 9, Shiv Shakti Ind. Estate,

J.R. Boricha Marg, Lower Parel (E),

Mumbai 400 011

Contact Person: Mr. Rajesh Shah

Tel : (022) 2301 6761

Fax : (022) 2301 2517

E-mail: [email protected]

Disposal of Investor’s Grievances

Complaints, if any, received in respect of the Shares will be attended to by the Registrar and Share

Transfer Agent in coordination with the Company expeditiously and to the satisfaction of the

shareholders.

Stock Market Data for Equity Shares of the Company

The Equity Shares of the Company are presently not listed on any stock exchanges. The Company is

seeking approval for listing of its shares on BSE only.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

12

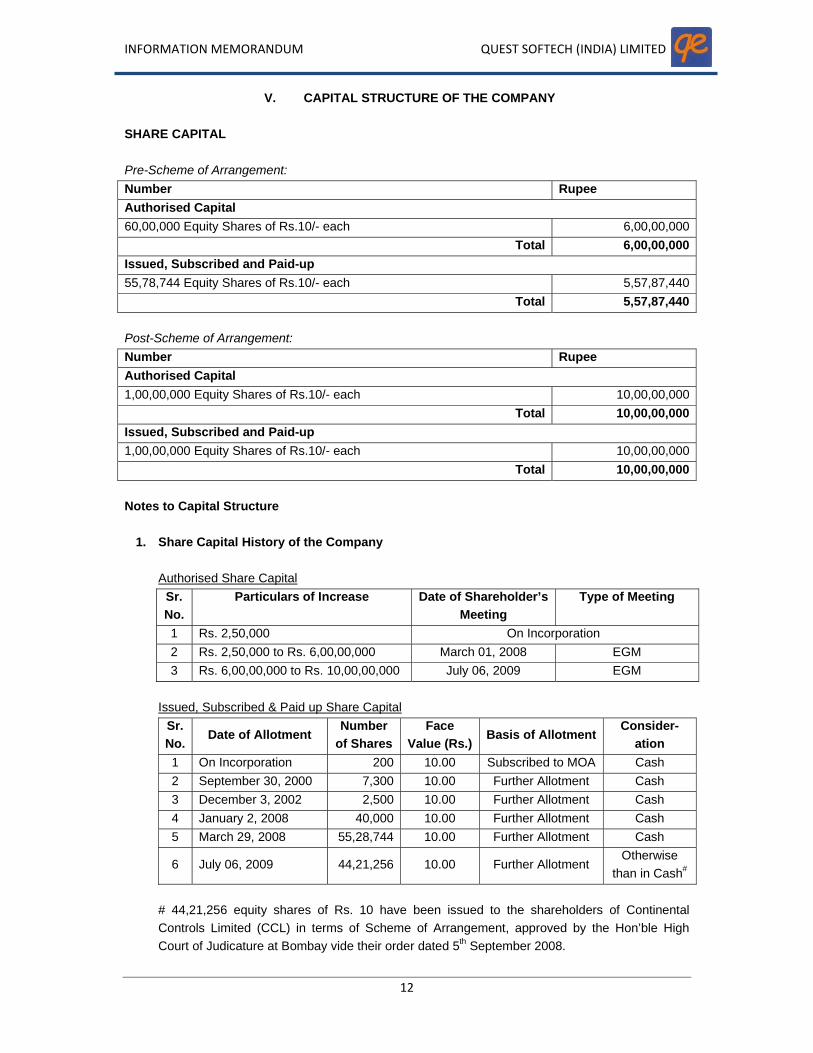

V. CAPITAL STRUCTURE OF THE COMPANY

SHARE CAPITAL

Pre-Scheme of Arrangement:

Number Rupee

Authorised Capital

60,00,000 Equity Shares of Rs.10/- each 6,00,00,000

Total 6,00,00,000

Issued, Subscribed and Paid-up

55,78,744 Equity Shares of Rs.10/- each 5,57,87,440

Total 5,57,87,440

Post-Scheme of Arrangement:

Number Rupee

Authorised Capital

1,00,00,000 Equity Shares of Rs.10/- each 10,00,00,000

Total 10,00,00,000

Issued, Subscribed and Paid-up

1,00,00,000 Equity Shares of Rs.10/- each 10,00,00,000

Total 10,00,00,000

Notes to Capital Structure

1. Share Capital History of the Company

Authorised Share Capital

Sr.

No.

Particulars of Increase Date of Shareholder’s

Meeting

Type of Meeting

1 Rs. 2,50,000 On Incorporation

2 Rs. 2,50,000 to Rs. 6,00,00,000 March 01, 2008 EGM

3 Rs. 6,00,00,000 to Rs. 10,00,00,000 July 06, 2009 EGM

Issued, Subscribed & Paid up Share Capital

Sr.

No. Date of Allotment

Number

of Shares

Face

Value (Rs.)Basis of Allotment

Consider-

ation

1 On Incorporation 200 10.00 Subscribed to MOA Cash

2 September 30, 2000 7,300 10.00 Further Allotment Cash

3 December 3, 2002 2,500 10.00 Further Allotment Cash

4 January 2, 2008 40,000 10.00 Further Allotment Cash

5 March 29, 2008 55,28,744 10.00 Further Allotment Cash

6 July 06, 2009 44,21,256 10.00 Further Allotment Otherwise

than in Cash#

# 44,21,256 equity shares of Rs. 10 have been issued to the shareholders of Continental

Controls Limited (CCL) in terms of Scheme of Arrangement, approved by the Hon’ble High

Court of Judicature at Bombay vide their order dated 5th September 2008.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

13

The said order was filed with the Registrar of Companies, Maharashtra on 26th September 2008

for both the Companies. Accordingly, the Demerger is effective from 26th September 2008.

Pursuant to Clause 7 of the Scheme, the Board of Directors of the Company on 6th July 2009

issued and allotted 44,21,256 Equity Shares of Rs. 10/- each to the shareholders of the

Demerged Company whose names appeared in the Register of Members of the Demerged

Company on the Record Date viz 3rd July 2009 in the Demerger Share Entitlement Ratio of 1

(One) new equity share of Rs. 10/- each credited as fully paid up of the Company for every 2

(Two) equity shares of Rs.10/- each held by such member in the Demerged Company.

On allotment of 44,21,256 Equity Shares by the Company, the issued, subscribed and paid up

share capital of the Company increased from Rs.5,57,87,440/- consisting of 55,78,744 equity

shares of Rs. 10/- each fully paid-up to Rs. 10,00,00,000/- consisting of 1,00,00,000 equity

shares of Rs.10/- each fully paid-up.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

14

2. Pre - Scheme of Arrangement Shareholding Pattern of the Company (As on 3rd July

2009, being the Record Date)

2(a).

Category

code

Category of

shareholder

Number

of

sharehold

ers

Total

number of

shares

Number of

shares held

in

dematerializ

ed form

Total shareholding as a

percentage of total

number of shares

As a

percentage

of (A+B)1

As a

percentag

e of

(A+B+C)

(A) Shareholding of

Promoter and

Promoter Group2

(1) Indian

(a) Individuals/ Hindu

Undivided Family

003 43,51,944 Nil 78.01% 78.01%

(b) Central

Government/ State

Government(s)

--- --- --- --- ---

(c) Bodies Corporate --- --- --- --- ---

(d) Financial

Institutions/ Banks

--- --- --- --- ---

(e) Any Other

(specify)

--- --- --- --- ---

Sub-Total (A)(1) 003 43,51,944 Nil 78.01% 78.01%

(2) Foreign

(a) Individuals (Non-

Resident

Individuals/ Foreign

Individuals)

--- --- --- --- ---

(b) Bodies Corporate --- --- --- --- ---

(c) Institutions --- --- --- --- ---

(d) Any Other (specify) --- --- --- --- ---

Sub-Total (A)(2) --- --- --- --- ---

Total

Shareholding of

Promoter and

Promoter Group

(A)= (A)(1)+(A)(2)

003 43,51,944 Nil 78.01% 78.01%

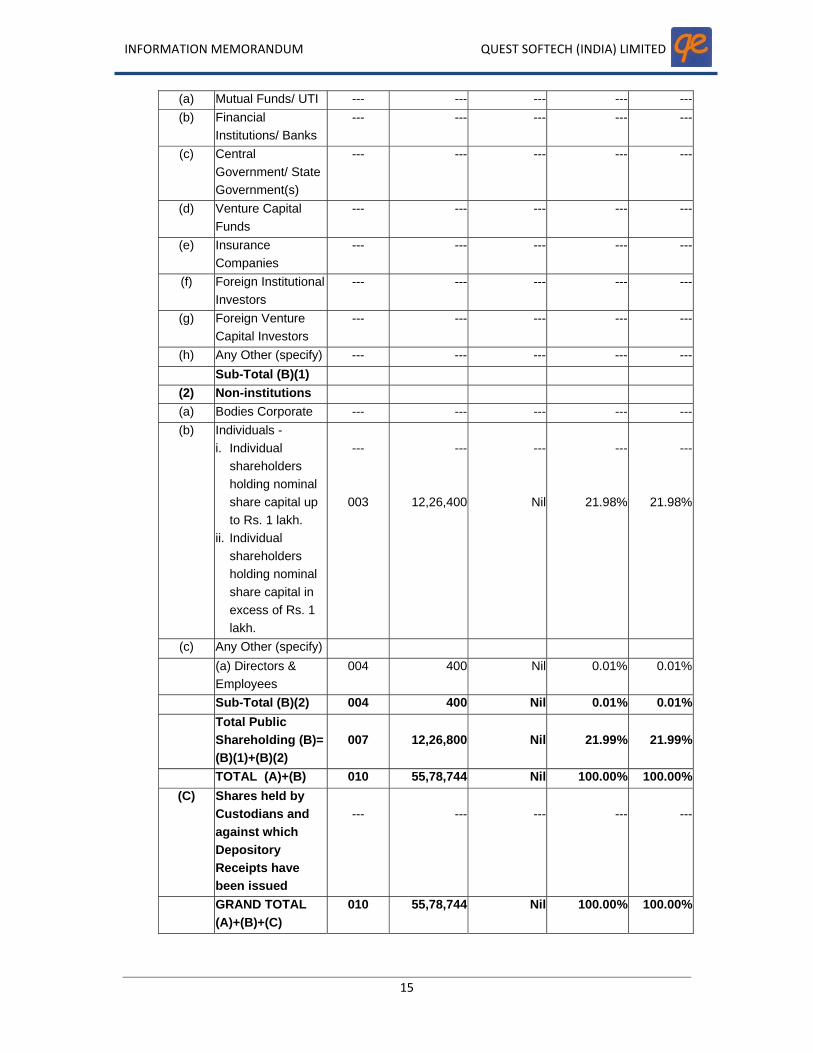

(B) Public

shareholding3

(1) Institutions

1 For determining public shareholding for the purpose of Clause 40A. 2 For definitions of “Promoter” and “Promoter Group", refer to Clause 40A. 3 For definitions of “Public Shareholding”, refer to Clause 40A.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

15

(a) Mutual Funds/ UTI --- --- --- --- ---

(b) Financial

Institutions/ Banks

--- --- --- --- ---

(c) Central

Government/ State

Government(s)

--- --- --- --- ---

(d) Venture Capital

Funds

--- --- --- --- ---

(e) Insurance

Companies

--- --- --- --- ---

(f) Foreign Institutional

Investors

--- --- --- --- ---

(g) Foreign Venture

Capital Investors

--- --- --- --- ---

(h) Any Other (specify) --- --- --- --- ---

Sub-Total (B)(1)

(2) Non-institutions

(a) Bodies Corporate --- --- --- --- ---

(b) Individuals -

i. Individual

shareholders

holding nominal

share capital up

to Rs. 1 lakh.

ii. Individual

shareholders

holding nominal

share capital in

excess of Rs. 1

lakh.

---

003

---

12,26,400

---

Nil

---

21.98%

---

21.98%

(c) Any Other (specify)

(a) Directors &

Employees

004 400 Nil 0.01% 0.01%

Sub-Total (B)(2) 004 400 Nil 0.01% 0.01%

Total Public

Shareholding (B)=

(B)(1)+(B)(2)

007 12,26,800 Nil

21.99% 21.99%

TOTAL (A)+(B) 010 55,78,744 Nil 100.00% 100.00%

(C) Shares held by

Custodians and

against which

Depository

Receipts have

been issued

--- --- ---

--- ---

GRAND TOTAL

(A)+(B)+(C)

010 55,78,744 Nil 100.00% 100.00%

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

16

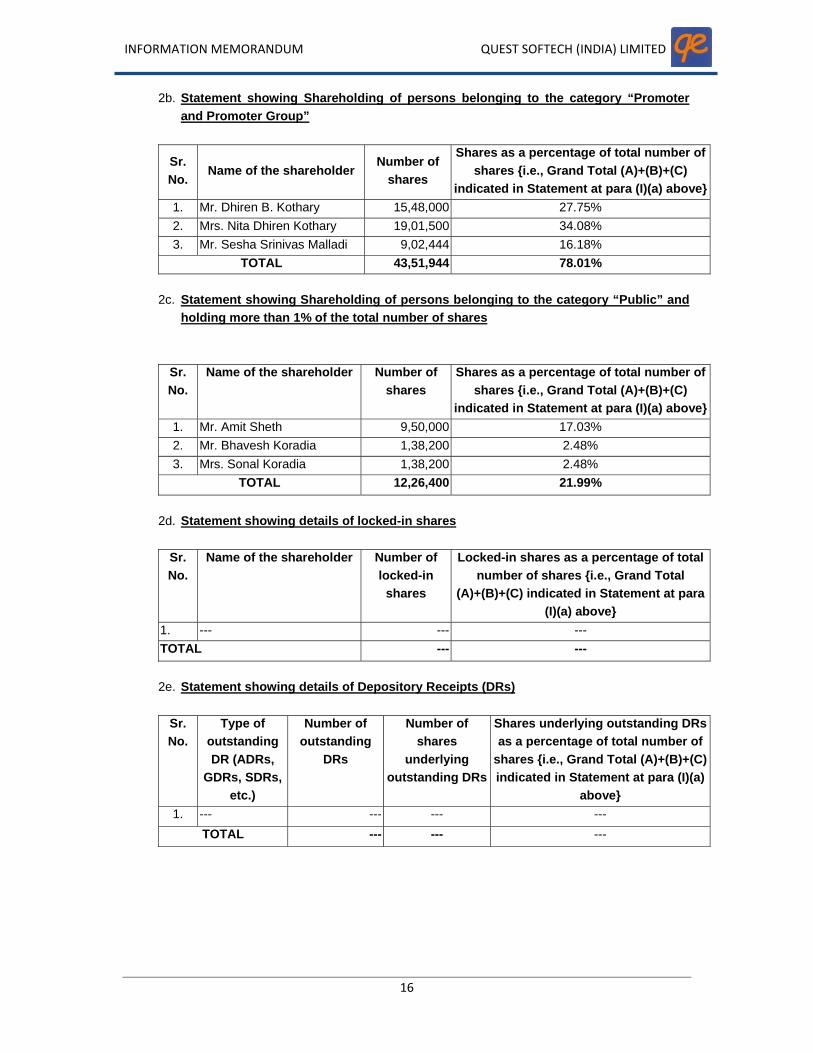

2b. Statement showing Shareholding of persons belonging to the category “Promoter

and Promoter Group”

Sr.

No. Name of the shareholder

Number of

shares

Shares as a percentage of total number of

shares {i.e., Grand Total (A)+(B)+(C)

indicated in Statement at para (I)(a) above}

1. Mr. Dhiren B. Kothary 15,48,000 27.75%

2. Mrs. Nita Dhiren Kothary 19,01,500 34.08%

3. Mr. Sesha Srinivas Malladi 9,02,444 16.18%

TOTAL 43,51,944 78.01%

2c. Statement showing Shareholding of persons belonging to the category “Public” and

holding more than 1% of the total number of shares

Sr.

No.

Name of the shareholder Number of

shares

Shares as a percentage of total number of

shares {i.e., Grand Total (A)+(B)+(C)

indicated in Statement at para (I)(a) above}

1. Mr. Amit Sheth 9,50,000 17.03%

2. Mr. Bhavesh Koradia 1,38,200 2.48%

3. Mrs. Sonal Koradia 1,38,200 2.48%

TOTAL 12,26,400 21.99%

2d. Statement showing details of locked-in shares

Sr.

No.

Name of the shareholder Number of

locked-in

shares

Locked-in shares as a percentage of total

number of shares {i.e., Grand Total

(A)+(B)+(C) indicated in Statement at para

(I)(a) above}

1. --- --- ---

TOTAL --- ---

2e. Statement showing details of Depository Receipts (DRs)

Sr.

No.

Type of

outstanding

DR (ADRs,

GDRs, SDRs,

etc.)

Number of

outstanding

DRs

Number of

shares

underlying

outstanding DRs

Shares underlying outstanding DRs

as a percentage of total number of

shares {i.e., Grand Total (A)+(B)+(C)

indicated in Statement at para (I)(a)

above}

1. --- --- --- ---

TOTAL --- --- ---

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

17

3. Post - Scheme of Arrangement Shareholding Pattern of the Company (As on 6th July

2009)

3(a).

Category

code

Category of

shareholder

Number of

shareholde

rs

Total number

of shares

Number of

shares held

in

demateriali

zed form

Total shareholding as a

percentage of total

number of shares

As a

percentage

of (A+B)4

As a

percentage

of (A+B+C)

(A) Shareholding of

Promoter and

Promoter Group5

(1) Indian

(a) Individuals/ Hindu

Undivided Family

003 44,09,752 57,768 44.10% 44.10%

(b) Central Government/

State Government(s)

--- --- --- --- ---

(c) Bodies Corporate --- --- --- --- ---

(d) Financial

Institutions/ Banks

--- --- --- --- ---

(e) Any Other

(specify)

--- --- --- --- ---

Sub-Total (A)(1) 003 44,09,752 57,768 44.10% 44.10%

(2) Foreign

(a) Individuals (Non-

Resident Individuals/

Foreign Individuals)

--- --- --- --- ---

(b) Bodies Corporate --- --- --- --- ---

(c) Institutions --- --- --- --- ---

(d) Any Other (specify) --- --- --- --- ---

Sub-Total (A)(2) --- --- --- --- ---

Total Shareholding

of Promoter and

Promoter Group

(A)= (A)(1)+(A)(2)

003 44,09,752 57,768 44.10% 44.10%

(B) Public

shareholding6

(1) Institutions

(a) Mutual Funds/ UTI --- --- --- --- ---

(b) Financial

Institutions/ Banks

001 13,926 13,926 0.14% 0.14%

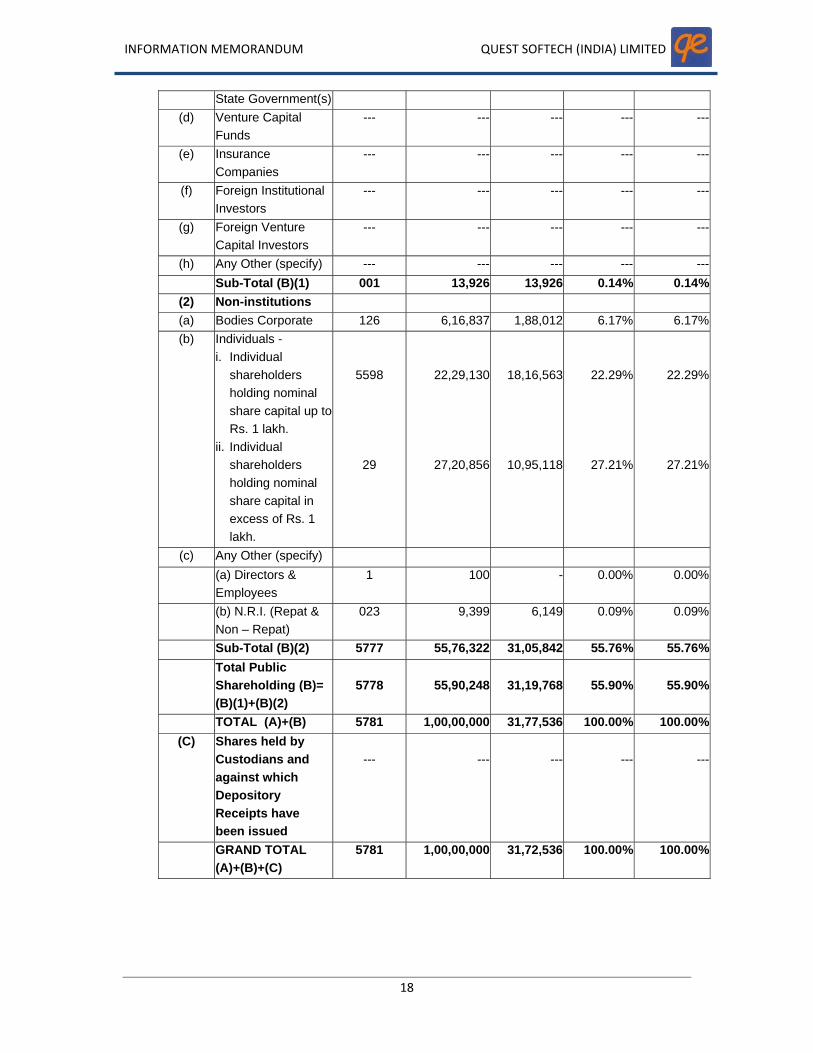

(c) Central Government/ --- --- --- --- ---

4 For determining public shareholding for the purpose of Clause 40A. 5 For definitions of “Promoter” and “Promoter Group", refer to Clause 40A. 6 For definitions of “Public Shareholding”, refer to Clause 40A.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

18

State Government(s)

(d) Venture Capital

Funds

--- --- --- --- ---

(e) Insurance

Companies

--- --- --- --- ---

(f) Foreign Institutional

Investors

--- --- --- --- ---

(g) Foreign Venture

Capital Investors

--- --- --- --- ---

(h) Any Other (specify) --- --- --- --- ---

Sub-Total (B)(1) 001 13,926 13,926 0.14% 0.14%

(2) Non-institutions

(a) Bodies Corporate 126 6,16,837 1,88,012 6.17% 6.17%

(b) Individuals -

i. Individual

shareholders

holding nominal

share capital up to

Rs. 1 lakh.

ii. Individual

shareholders

holding nominal

share capital in

excess of Rs. 1

lakh.

5598

29

22,29,130

27,20,856

18,16,563

10,95,118

22.29%

27.21%

22.29%

27.21%

(c) Any Other (specify)

(a) Directors &

Employees

1 100 - 0.00% 0.00%

(b) N.R.I. (Repat &

Non – Repat)

023 9,399 6,149 0.09% 0.09%

Sub-Total (B)(2) 5777 55,76,322 31,05,842 55.76% 55.76%

Total Public

Shareholding (B)=

(B)(1)+(B)(2)

5778 55,90,248 31,19,768 55.90% 55.90%

TOTAL (A)+(B) 5781 1,00,00,000 31,77,536 100.00% 100.00%

(C) Shares held by

Custodians and

against which

Depository

Receipts have

been issued

--- --- ---

--- ---

GRAND TOTAL

(A)+(B)+(C)

5781 1,00,00,000 31,72,536 100.00% 100.00%

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

19

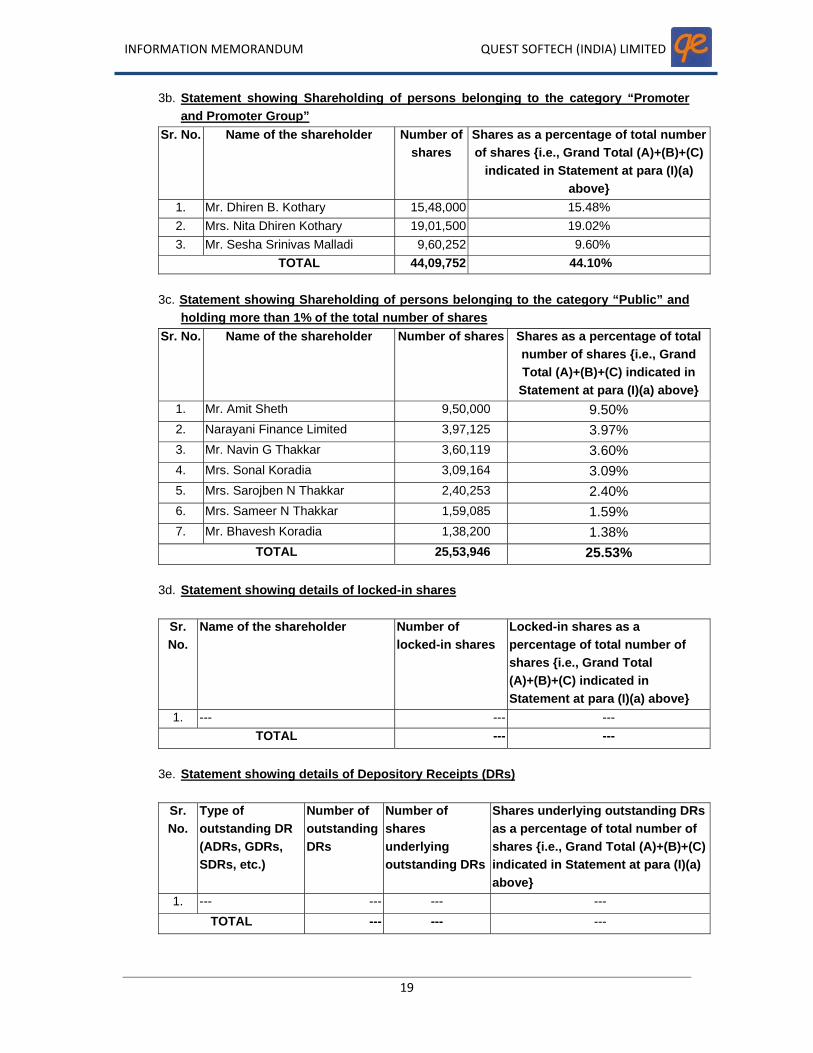

3b. Statement showing Shareholding of persons belonging to the category “Promoter

and Promoter Group”

Sr. No. Name of the shareholder Number of

shares

Shares as a percentage of total number

of shares {i.e., Grand Total (A)+(B)+(C)

indicated in Statement at para (I)(a)

above}

1. Mr. Dhiren B. Kothary 15,48,000 15.48%

2. Mrs. Nita Dhiren Kothary 19,01,500 19.02%

3. Mr. Sesha Srinivas Malladi 9,60,252 9.60%

TOTAL 44,09,752 44.10%

3c. Statement showing Shareholding of persons belonging to the category “Public” and

holding more than 1% of the total number of shares

Sr. No. Name of the shareholder Number of shares Shares as a percentage of total

number of shares {i.e., Grand

Total (A)+(B)+(C) indicated in

Statement at para (I)(a) above}

1. Mr. Amit Sheth 9,50,000 9.50% 2. Narayani Finance Limited 3,97,125 3.97%

3. Mr. Navin G Thakkar 3,60,119 3.60%

4. Mrs. Sonal Koradia 3,09,164 3.09%

5. Mrs. Sarojben N Thakkar 2,40,253 2.40%

6. Mrs. Sameer N Thakkar 1,59,085 1.59%

7. Mr. Bhavesh Koradia 1,38,200 1.38% TOTAL 25,53,946 25.53%

3d. Statement showing details of locked-in shares

Sr.

No.

Name of the shareholder Number of

locked-in shares

Locked-in shares as a

percentage of total number of

shares {i.e., Grand Total

(A)+(B)+(C) indicated in

Statement at para (I)(a) above}

1. --- --- ---

TOTAL --- ---

3e. Statement showing details of Depository Receipts (DRs)

Sr.

No.

Type of

outstanding DR

(ADRs, GDRs,

SDRs, etc.)

Number of

outstanding

DRs

Number of

shares

underlying

outstanding DRs

Shares underlying outstanding DRs

as a percentage of total number of

shares {i.e., Grand Total (A)+(B)+(C)

indicated in Statement at para (I)(a)

above}

1. --- --- --- ---

TOTAL --- --- ---

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

20

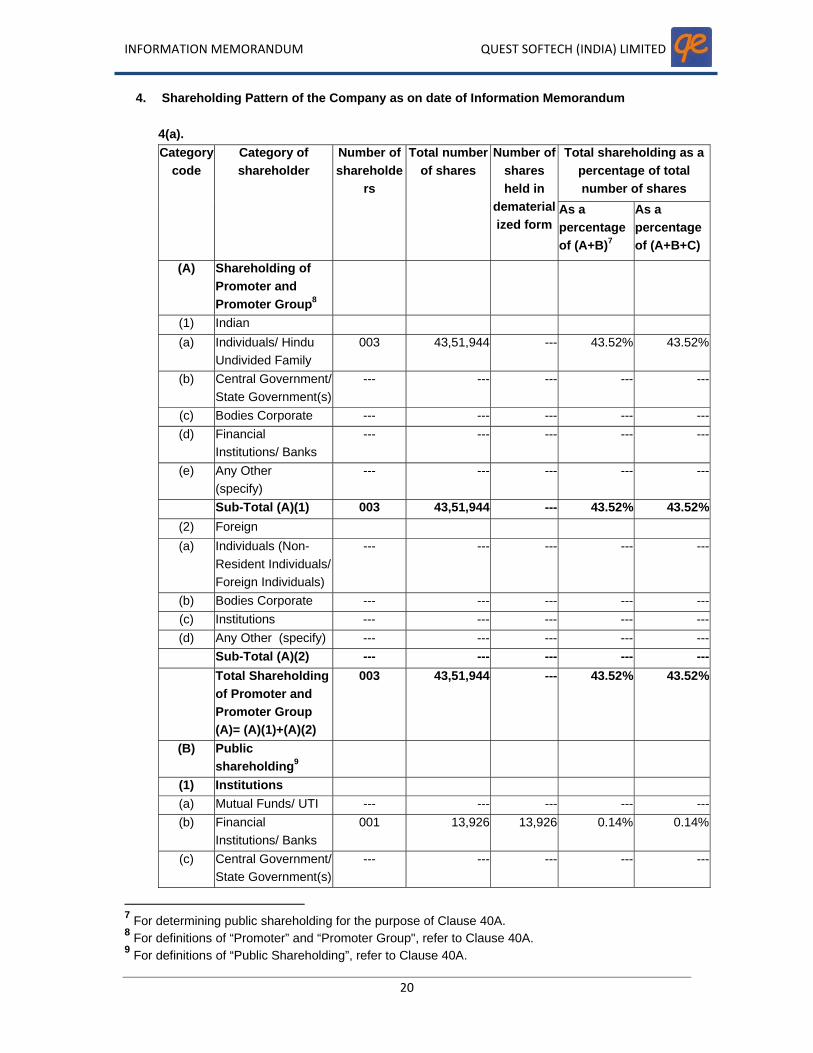

4. Shareholding Pattern of the Company as on date of Information Memorandum

4(a).

Category

code

Category of

shareholder

Number of

shareholde

rs

Total number

of shares

Number of

shares

held in

dematerial

ized form

Total shareholding as a

percentage of total

number of shares

As a

percentage

of (A+B)7

As a

percentage

of (A+B+C)

(A) Shareholding of

Promoter and

Promoter Group8

(1) Indian

(a) Individuals/ Hindu

Undivided Family

003 43,51,944 --- 43.52% 43.52%

(b) Central Government/

State Government(s)

--- --- --- --- ---

(c) Bodies Corporate --- --- --- --- ---

(d) Financial

Institutions/ Banks

--- --- --- --- ---

(e) Any Other

(specify)

--- --- --- --- ---

Sub-Total (A)(1) 003 43,51,944 --- 43.52% 43.52%

(2) Foreign

(a) Individuals (Non-

Resident Individuals/

Foreign Individuals)

--- --- --- --- ---

(b) Bodies Corporate --- --- --- --- ---

(c) Institutions --- --- --- --- ---

(d) Any Other (specify) --- --- --- --- ---

Sub-Total (A)(2) --- --- --- --- ---

Total Shareholding

of Promoter and

Promoter Group

(A)= (A)(1)+(A)(2)

003 43,51,944 --- 43.52% 43.52%

(B) Public

shareholding9

(1) Institutions

(a) Mutual Funds/ UTI --- --- --- --- ---

(b) Financial

Institutions/ Banks

001 13,926 13,926 0.14% 0.14%

(c) Central Government/

State Government(s)

--- --- --- --- ---

7 For determining public shareholding for the purpose of Clause 40A. 8 For definitions of “Promoter” and “Promoter Group", refer to Clause 40A. 9 For definitions of “Public Shareholding”, refer to Clause 40A.

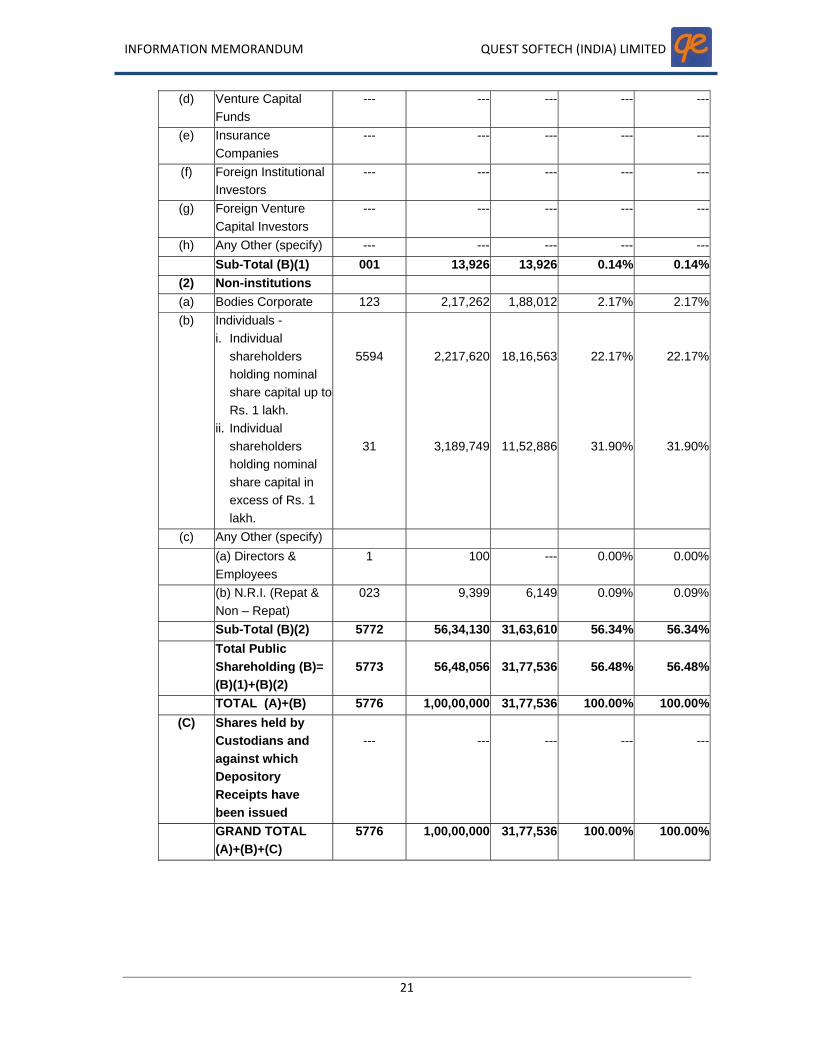

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

21

(d) Venture Capital

Funds

--- --- --- --- ---

(e) Insurance

Companies

--- --- --- --- ---

(f) Foreign Institutional

Investors

--- --- --- --- ---

(g) Foreign Venture

Capital Investors

--- --- --- --- ---

(h) Any Other (specify) --- --- --- --- ---

Sub-Total (B)(1) 001 13,926 13,926 0.14% 0.14%

(2) Non-institutions

(a) Bodies Corporate 123 2,17,262 1,88,012 2.17% 2.17%

(b) Individuals -

i. Individual

shareholders

holding nominal

share capital up to

Rs. 1 lakh.

ii. Individual

shareholders

holding nominal

share capital in

excess of Rs. 1

lakh.

5594

31

2,217,620

3,189,749

18,16,563

11,52,886

22.17%

31.90%

22.17%

31.90%

(c) Any Other (specify)

(a) Directors &

Employees

1 100 --- 0.00% 0.00%

(b) N.R.I. (Repat &

Non – Repat)

023 9,399 6,149 0.09% 0.09%

Sub-Total (B)(2) 5772 56,34,130 31,63,610 56.34% 56.34%

Total Public

Shareholding (B)=

(B)(1)+(B)(2)

5773 56,48,056 31,77,536 56.48% 56.48%

TOTAL (A)+(B) 5776 1,00,00,000 31,77,536 100.00% 100.00%

(C) Shares held by

Custodians and

against which

Depository

Receipts have

been issued

--- --- ---

--- ---

GRAND TOTAL

(A)+(B)+(C)

5776 1,00,00,000 31,77,536 100.00% 100.00%

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

22

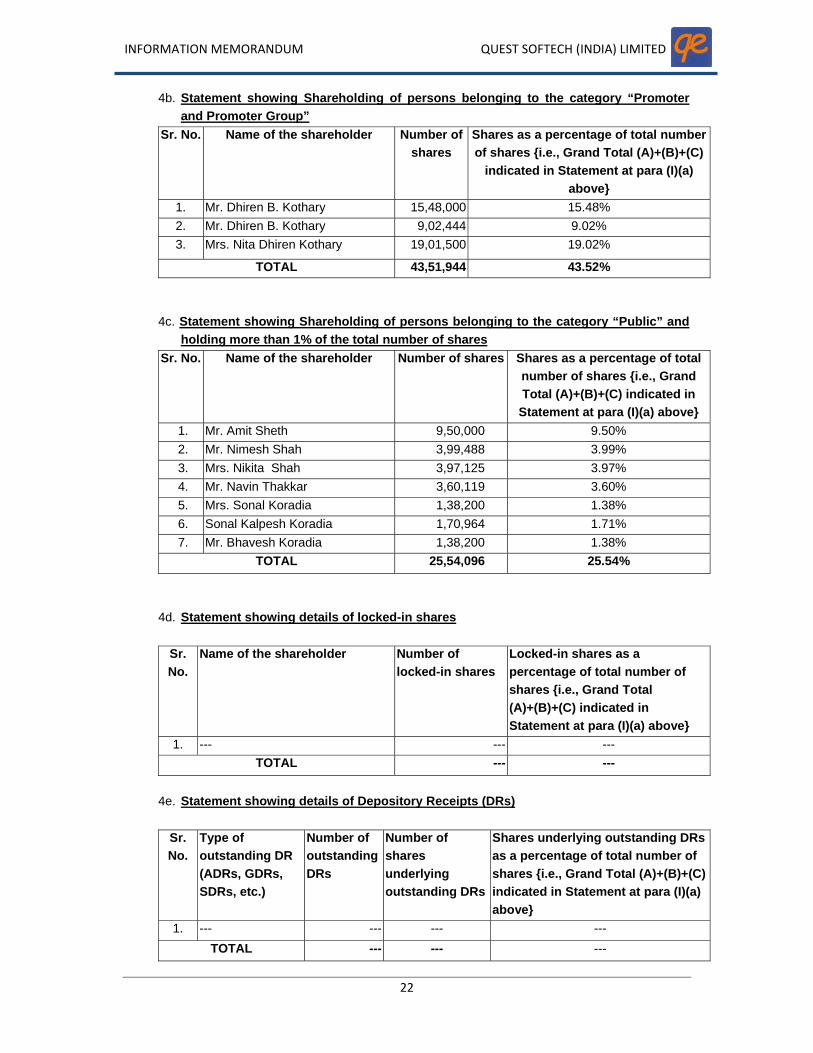

4b. Statement showing Shareholding of persons belonging to the category “Promoter

and Promoter Group”

Sr. No. Name of the shareholder Number of

shares

Shares as a percentage of total number

of shares {i.e., Grand Total (A)+(B)+(C)

indicated in Statement at para (I)(a)

above}

1. Mr. Dhiren B. Kothary 15,48,000 15.48%

2. Mr. Dhiren B. Kothary 9,02,444 9.02%

3. Mrs. Nita Dhiren Kothary 19,01,500 19.02%

TOTAL 43,51,944 43.52%

4c. Statement showing Shareholding of persons belonging to the category “Public” and

holding more than 1% of the total number of shares

Sr. No. Name of the shareholder Number of shares Shares as a percentage of total

number of shares {i.e., Grand

Total (A)+(B)+(C) indicated in

Statement at para (I)(a) above}

1. Mr. Amit Sheth 9,50,000 9.50%

2. Mr. Nimesh Shah 3,99,488 3.99%

3. Mrs. Nikita Shah 3,97,125 3.97%

4. Mr. Navin Thakkar 3,60,119 3.60%

5. Mrs. Sonal Koradia 1,38,200 1.38%

6. Sonal Kalpesh Koradia 1,70,964 1.71%

7. Mr. Bhavesh Koradia 1,38,200 1.38%

TOTAL 25,54,096 25.54%

4d. Statement showing details of locked-in shares

Sr.

No.

Name of the shareholder Number of

locked-in shares

Locked-in shares as a

percentage of total number of

shares {i.e., Grand Total

(A)+(B)+(C) indicated in

Statement at para (I)(a) above}

1. --- --- ---

TOTAL --- ---

4e. Statement showing details of Depository Receipts (DRs)

Sr.

No.

Type of

outstanding DR

(ADRs, GDRs,

SDRs, etc.)

Number of

outstanding

DRs

Number of

shares

underlying

outstanding DRs

Shares underlying outstanding DRs

as a percentage of total number of

shares {i.e., Grand Total (A)+(B)+(C)

indicated in Statement at para (I)(a)

above}

1. --- --- --- ---

TOTAL --- --- ---

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

23

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

24

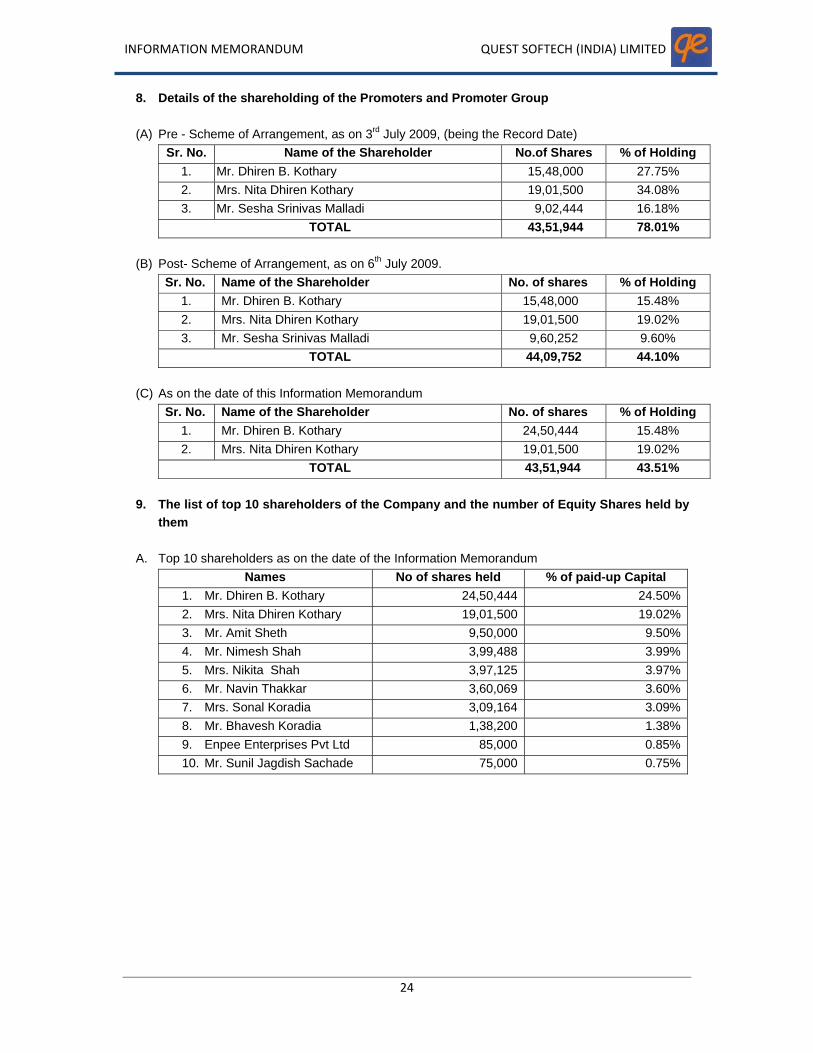

8. Details of the shareholding of the Promoters and Promoter Group

(A) Pre - Scheme of Arrangement, as on 3rd July 2009, (being the Record Date)

Sr. No. Name of the Shareholder No.of Shares % of Holding

1. Mr. Dhiren B. Kothary 15,48,000 27.75%

2. Mrs. Nita Dhiren Kothary 19,01,500 34.08%

3. Mr. Sesha Srinivas Malladi 9,02,444 16.18%

TOTAL 43,51,944 78.01%

(B) Post- Scheme of Arrangement, as on 6th July 2009.

Sr. No. Name of the Shareholder No. of shares % of Holding

1. Mr. Dhiren B. Kothary 15,48,000 15.48%

2. Mrs. Nita Dhiren Kothary 19,01,500 19.02%

3. Mr. Sesha Srinivas Malladi 9,60,252 9.60%

TOTAL 44,09,752 44.10%

(C) As on the date of this Information Memorandum

Sr. No. Name of the Shareholder No. of shares % of Holding

1. Mr. Dhiren B. Kothary 24,50,444 15.48%

2. Mrs. Nita Dhiren Kothary 19,01,500 19.02%

TOTAL 43,51,944 43.51%

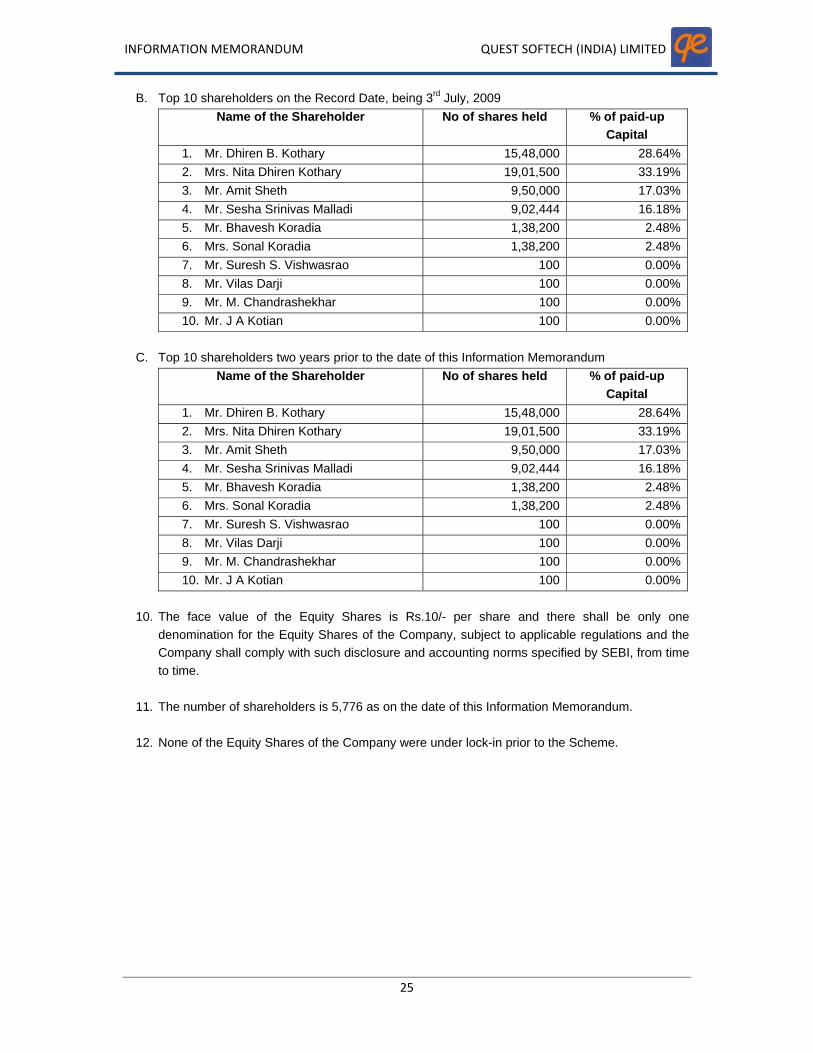

9. The list of top 10 shareholders of the Company and the number of Equity Shares held by

them

A. Top 10 shareholders as on the date of the Information Memorandum

Names No of shares held % of paid-up Capital

1. Mr. Dhiren B. Kothary 24,50,444 24.50%

2. Mrs. Nita Dhiren Kothary 19,01,500 19.02%

3. Mr. Amit Sheth 9,50,000 9.50%

4. Mr. Nimesh Shah 3,99,488 3.99%

5. Mrs. Nikita Shah 3,97,125 3.97%

6. Mr. Navin Thakkar 3,60,069 3.60%

7. Mrs. Sonal Koradia 3,09,164 3.09%

8. Mr. Bhavesh Koradia 1,38,200 1.38%

9. Enpee Enterprises Pvt Ltd 85,000 0.85%

10. Mr. Sunil Jagdish Sachade 75,000 0.75%

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

25

B. Top 10 shareholders on the Record Date, being 3rd July, 2009

Name of the Shareholder No of shares held % of paid-up

Capital

1. Mr. Dhiren B. Kothary 15,48,000 28.64%

2. Mrs. Nita Dhiren Kothary 19,01,500 33.19%

3. Mr. Amit Sheth 9,50,000 17.03%

4. Mr. Sesha Srinivas Malladi 9,02,444 16.18%

5. Mr. Bhavesh Koradia 1,38,200 2.48%

6. Mrs. Sonal Koradia 1,38,200 2.48%

7. Mr. Suresh S. Vishwasrao 100 0.00%

8. Mr. Vilas Darji 100 0.00%

9. Mr. M. Chandrashekhar 100 0.00%

10. Mr. J A Kotian 100 0.00%

C. Top 10 shareholders two years prior to the date of this Information Memorandum

Name of the Shareholder No of shares held % of paid-up

Capital

1. Mr. Dhiren B. Kothary 15,48,000 28.64%

2. Mrs. Nita Dhiren Kothary 19,01,500 33.19%

3. Mr. Amit Sheth 9,50,000 17.03%

4. Mr. Sesha Srinivas Malladi 9,02,444 16.18%

5. Mr. Bhavesh Koradia 1,38,200 2.48%

6. Mrs. Sonal Koradia 1,38,200 2.48%

7. Mr. Suresh S. Vishwasrao 100 0.00%

8. Mr. Vilas Darji 100 0.00%

9. Mr. M. Chandrashekhar 100 0.00%

10. Mr. J A Kotian 100 0.00%

10. The face value of the Equity Shares is Rs.10/- per share and there shall be only one

denomination for the Equity Shares of the Company, subject to applicable regulations and the

Company shall comply with such disclosure and accounting norms specified by SEBI, from time

to time.

11. The number of shareholders is 5,776 as on the date of this Information Memorandum.

12. None of the Equity Shares of the Company were under lock-in prior to the Scheme.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

26

VI. SCHEME OF ARRANGEMENT

Background and Rationale of the Scheme of Arrangement

CCL was incorporated on March 02, 1995 with the Registrar of Companies, Maharashtra, Mumbai.

CCL was engaged in the business of Electrical Controls and Software Services each of which were

being carried out as two separate business divisions. Both the divisions of CCL were being run

independently with different characteristics, distinct fixed assets, non-overlapping revenue streams

and separately identifiable customers. The nature of risks and competition involved in the business of

Electrical Division Undertaking is different from that of the business Software Services Division.

The software services business of the Company was started in the year 2000 and in the year 2003,

Continental Softech Limited, a Group Company engaged in the business of Software Services was

amalgamated with CCL to strengthen the Software Services business. However, due to increased

competition this Division was passing through a tough phase and the management was unable to

spare sufficient time and effort to put the Software Services Division Undertaking on the path of

efficiency and growth. Thus, infrastructure created for the Software Services Division was not being

utilized to its fullest potential and proving to be a drag on the overall working of the Company.

QSIL was incorporated on 27th day of March 2000 with the Registrar of Companies, Maharashtra,

Mumbai. QSIL is engaged in the business of providing software and BPO Services to both domestic

and international clients. However, its growth is constrained due to lack of infrastructure and

resources commensurate with the business development potential the management has. The

infrastructure and resources transferred from CCL by the demerger would enable QSIL to expand its

business substantially, the fruits whereof can be enjoyed by the shareholders of the Company.

The restructuring has resulted in segregation of the Software Services Division Undertaking from

CCL, leading to operational efficiencies and synergies and enable exploitation of growth opportunities

of both the CCL and the QSIL. Since the shares of both companies are proposed to be listed, the

entire investment of all the shareholders will continue to remain tradeable on the Stock Exchanges,

thereby not jeopardizing their interests in any manner.

The Salient Features of the Scheme are:-

i. The Scheme envisages the demerger of the Software Services Division Undertaking of the

Applicant Company to the QSIL pursuant to Sections 391 to 394 and other relevant provisions

of the Act in the manner provided for in the Scheme, and the consequent issue of equity shares

by the QSIL to the shareholders of the Applicant Company in the Share Entitlement Ratio (as

defined hereinafter).

ii. The Scheme provides that the "Appointed Date" shall be April 1, 2008.

iii. The "Effective Date" for the Scheme means the last of the dates on which the conditions and

matters referred to in Clause 12 of the Scheme occur or have been fulfilled or waived.

iv. "Software Services Division Undertaking " as described in Clause A of Part I of the Scheme

means the software services business carried on by the Applicant Company, which shall

include the following:

a. All the properties and assets, investments, stocks, debtors, receivables, loans, advances,

all rights, powers, interests, authorities, privileges and liberties, whether or not recorded in

the books of account and/or appearing in the balance sheet of the Applicant Company

pertaining, or relating, to the Software Services Business.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

27

b. All liabilities, including all the financial commitments / obligation present and future,

contingent or otherwise, whether or not recorded in the books of account and/or

appearing in the balance sheet of the Applicant Company pertaining, or relating to the

Software Services Business.

c. Such of the general or multi-purpose borrowings of the Software Services Business as

identified by the Board of Directors of the Applicant Company.

d. All books of account, registers, records, files, papers and all other documents of whatever

nature relating to the above assets, properties and liabilities.

e. Without prejudice to the generality of sub-clauses (a) and (b) hereinabove, the Software

Services Division Undertaking shall include all the assets and properties of the Applicant

Company pertaining or relating to its Software Services Business, whether real corporeal

and incorporeal, in possession or reversion, present and contingent, all other assets

(whether tangible or intangible) and liabilities of whatsoever nature, and wheresoever

situate, investments, stocks, other rights, powers, authorities, allotments, approvals,

consents, exemptions, letters of intent, licences, permits, registrations, contracts,

engagements, arrangements, agreements with clients, rights, titles, interests, benefits,

and advantages of any nature whatsoever and wheresoever situate of, belonging to, or in

the ownership, power or possession and in the control of, or vested in, or granted in

favour of, or enjoyed by, the Software Services Business of the Applicant Company,

including all intellectual properties and rights of any nature whatsoever and licences,

assignments, grants in respect thereof, privileges, liberties, easements, contracts,

advantages, benefits, goodwill, , approvals, authorisations, right to use and avail of

telephones, facsimile and other communication facilities, connections, equipments and

installations, utilities, electricity and electronic connections and all other services, of every

kind, nature and descriptions whatsoever, benefits of all agreements, contracts,

arrangements, deposits, advances, recoverables and receivables whether from

government, semi-government, local authorities or any other customers, etc., and all

other rights, interests, claims and powers of every kind, nature and description of, and

arising to, Software Services Business of the Applicant Company and cash and bank

balances, all earnest moneys or deposits including security deposits, if any, paid by the

Software Services Business of the Applicant Company.

f. All permanent employees of the Software Services of the Applicant Company

substantially engaged in the Software Services Business and those permanent

employees that are determined by the Board of Directors of the Applicant Company to be

substantially engaged in, or in relation to, the Software Services Division Undertaking.

v. "Electrical Division Undertaking" means all the businesses, activities and operations of the

Applicant Company other than Software Services Division Undertaking.

vi. The Scheme of Arrangement provides that though it shall become effective from the Effective

Date, the provisions of the Scheme of Arrangement shall be applicable and come into operation

from the Appointed Date.

vii. The Scheme also provides for:

a. the manner of vesting and transfer of the assets of the Applicant Company relating to the

Software Services Division Undertaking in the QSIL;

b. the transfer of contracts, deeds, bonds, agreements, schemes, arrangements and other

instruments of whatsoever nature relating to the Software Services Division Undertaking

from the Applicant Company to the QSIL;

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

28

c. the transfer of all consents, permissions, licenses, certificates, clearances, authorities,

powers of attorney given by, issued to or executed in favour of the Software Services

Division Undertaking from the Applicant Company to the QSIL;

d. the transfer of all debts, liabilities, duties, and obligations of the Software Services

Division Undertaking from the Applicant Company to the QSIL;

e. the transfer of all suits, actions and proceedings by or against the Applicant Company

relating to the Software Services Division Undertaking to the QSIL;

f. the manner in which the Applicant Company shall be deemed to have been carrying on

all business and activities relating to the Software Services Division Undertaking for and

on account of, and in trust for, the QSIL;

g. the transfer of employees engaged in the Software Services Division Undertaking of the

Applicant Company to the QSIL on terms and conditions not less favourable than those

on which they are engaged in the Applicant Company;

h. provisions for the Software Services Division Undertaking to continue in the Applicant

Company;

i. the issuance of 1 (One) share of face value of Rs. 10/- by the QSIL to the shareholders of

the CCL whose names are recorded in the Register of Members of the Applicant

Company on the Record Date for every 2 (Two) share of face value of Rs. 10/- credited

as fully paid-up held by such shareholder and matters related thereto;

j. the reduction of paid-up capital of the Applicant Company by half, consequent to the

transfer of Software Services Undertaking to QSIL and the allotment of shares by QSIL in

lieu thereof and the matters related thereto.

k. The treatment of fractional entitlements in view of (i) and (j) above.

l. that the QSIL shall apply for the listing of the shares issued by the QSIL pursuant to the

Scheme to the Bombay Stock Exchange Limited (BSE), on which the equity shares of the

Applicant Company are listed;

m. that the shares allotted and issued pursuant to this Scheme of Arrangement shall remain

frozen in the depositories system till listing/trading permission is given by the Bombay

Stock Exchange;

n. the accounting treatment for the arrangement in the books of the Applicant Company and

the QSIL respectively.

viii. The Scheme is conditional upon and subject to:

a. the Scheme being agreed to by the respective requisite majorities of the Shareholders

and creditors (where applicable) of the Applicant Company and the QSIL as required

under the Act and the requisite orders of the High Court being obtained;

b. such other sanctions and approvals including but not limited to in-principle approvals,

sanctions of any Governmental Authority or any stock exchanges as may be required by

law in respect of the Scheme being obtained; and

c. the certified copies of the orders of the High Court referred to in the Scheme being filed

with the Registrar of Companies, Mumbai.

The Shareholders of the Transferor Company have accorded their approval for the Scheme of

Arrangement at the Court Convened meeting on 24th May, 2008. Subsequently, Scheme of

Arrangement has been approved by the Honourable High Court of Judicature at Bombay on

September 5, 2008. The Copy of order of High court along with the Scheme of Demerger is available

at the registered office of the Company.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

29

VII. Taxation

The information provided below sets out the possible tax benefits available to the shareholders of

an Indian company in a summary manner only and is not a complete analysis or listing of all potential

tax consequences of the subscription, ownership and disposal of the Equity Shares, under the

current tax laws presently in force in India. Several of these benefits are dependent on our

shareholders fulfilling the conditions prescribed under the relevant tax laws. Hence the ability of any

shareholder to derive the tax benefits is dependent upon fulfilling such conditions, which based on

business imperatives it faces in the future, it may not choose to fulfill. The following overview is not

exhaustive or comprehensive and is not intended to be a substitute for professional advice. You are

advised to consult your own tax consultant and advisors with respect to the tax implications of an

investment in the Equity Shares, particularly in view of certain recently enacted legislation which may

not have a direct legal precedent or may have a different interpretation on the benefits which you can

avail.

STATEMENT OF POSSIBLE TAX BENEFITS AVAILABLE TO OUR SHAREHOLDERS UNDER

THE INCOME TAX ACT, 1961 (“IT ACT”) AND OTHER DIRECT TAX LAWS PRESENTLY IN

FORCE IN INDIA TAX BENEFITS AVAILABLE TO OUR SHAREHOLDERS

• This statement sets out below the possible tax benefits available to our shareholders under

the current tax laws presently in force in India. Several of these benefits are dependent on

such shareholders fulfilling the conditions prescribed under the relevant tax laws. Hence, the

ability of our shareholders to derive the tax benefits is dependent upon fulfilling such

conditions, which based on the business imperatives, the shareholders may or may not

choose to fulfil;

• This statement sets out below the provisions of law in a summary manner only and is not

a complete analysis or listing of all potential tax consequences of the subscription,

ownership and disposal of Equity Shares. This statement is only intended to provide

general information to the investors and is neither designed nor intended to be a substitute

for a professional tax advice. In view of the individual nature of tax consequences and the

changing tax laws, each investor is advised to consult his or her or their own tax consultant

with respect to the specific tax implications arising out of their participation in the issue;

• In respect of non-residents, the tax rates and the consequent taxation, mentioned in this

section shall be further subject to any benefits available under the Double Taxation

Avoidance Agreement, if any, between India and the country in which the non-resident has

fiscal domicile; and

• The stated benefits will be available only to the sole/first-named holder in case the Equity

Shares are held by joint shareholders.

I. Benefits under the IT Act

A. Resident Shareholders

1. Under Section 10(32) of the IT Act, any income of minor children clubbed in the total income of the

parent under Section 64(1 A) of the IT Act, will be exempt from tax to the extent of Rs. 1,500

per minor child whose income is so included.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

30

2. As per Section 10(34), read with Section 115-O(6) of the IT A, any income by way of dividends

referred to in Section 115-O (i.e. dividends declared, distributed or paid on or after 1 April

2003 by the domestic companies) received on the Equity Shares is exempt from tax. However it

is pertinent to note that Section 14A of the IT Act restricts claims for deduction of expenses

incurred in relation to exempt income. Thus, any expense incurred to earn the dividend income is

not an allowable expenditure.

3. As per Section 2(29A), read with Section 2(42A), Equity Shares held in a company are treated as

long term capital asset if the same are held by the assessee for more than twelve months

period immediately preceding the date of its transfer. Accordingly, the benefits enumerated

below in respect of long term capital assets would be available if the Equity Shares are held for

more than twelve months.

4. As per Section 10(38) of the IT A, long term capital gains arising from the transfer of a long term

capital asset being an Equity Share, where such transaction is chargeable to securities

transaction tax, will be exempt in the hands of the shareholder.

5. As per Section 54EC of the IT A and subject to the conditions and to the extent specified therein,

long-term capital gains (in cases not covered under Section 10(38) of the ITA) arising on the

transfer of a long-term capital asset will be exempt from capital gains tax to the extent such

capital gains are invested in a “long term specified asset” within a period of 6 months after the

date of such transfer. It may be noted that investment made on or after April 1, 2007 in the

long term specified asset by an assessee during any financial year cannot exceed Rs. 50 Lacs.

However, if the assessee transfers or converts the long term specified asset into money within a

period of three years from the date of its acquisition, the amount of capital gains exempted

earlier would become chargeable to tax as long-term capital gains in the year in which the long

term specified asset is transferred or converted into money.

A “long term specified asset” means any bond, redeemable after three years and issued on or

after the 1st day of April 2007 by the:

• National Highways Authority of India constituted under Section 3 of the National

Highways

Authority of India Act, 1988; or

• Rural Electrification Corporation Limited, a company formed and registered under the

Companies

Act, 1956.

6. As per Section 54F of the ITA, long term capital gains (in cases not covered under Section

10(38)) arising on the transfer of the Equity Shares held by an individual or Hindu Undivided

Family (HUF) will be exempt from capital gains tax if the net consideration is utilised, within a

period of one year before, or two years after the date of transfer, in the purchase of a residential

house, or for construction of a residential house within three years. Such benefit will not be

available:

if the individual or Hindu Undivided Family -

• owns more than one residential house, other than the new residential house, on the date

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

31

of transfer of the Equity Shares; or

• purchases another residential house within a period of one year after the date of

transfer of the Equity Shares; or

• constructs another residential house within a period of three years after the date of

transfer of the Equity Shares; and

the income from such residential house, other than the one residential house owned on the date

of transfer of the original asset, is chargeable under the head “Income from house property”.

If only a part of the net consideration is so invested, so much of the capital gain as bears to the

whole of the capital gain, the same proportion as the cost of the new residential house bears to the

net consideration, will be exempt.

If the new residential house is transferred within a period of three years from the date of

purchase or construction, the amount of capital gains on which tax was not charged earlier, will

be deemed to be income chargeable under the head “Capital Gains” of the year in which the

residential house is transferred.

7. As per Section 74 Short-term capital loss suffered during the year is allowed to be set-off against

short-term as well as long-term capital gains of the said year. Balance loss, if any, could be

carried forward for eight years for claiming set-off against subsequent years' short term as well as

long-term capital gains. Long-term capital loss suffered during the year is allowed to be set-off

against long-term capital gains. Balance loss, if any, could be carried forward for eight years for

claiming set-off against subsequent years' long-term capital gains.

8. As per Section 111A of the IT A, short term capital gains arising from the sale of Equity Shares

transacted through a recognised stock exchange in India, where such transaction is chargeable to

securities transaction tax, will be taxable at the rate of 15% (plus applicable surcharge and

education cess).

9. As per Section 112 of the IT A, taxable long-term capital gains, if any, on sale of listed securities

will be charged to tax at the rate of 20% (plus applicable surcharge and education cess) after

considering indexation benefits or at 10% (plus applicable surcharge and education cess) without

indexation benefits, whichever is less. Under Section 48 of the IT A, the long term capital gains

arising out of sale of capital assets excluding bonds and debentures (except Capital Indexed

Bonds issued by the Government) will be computed after indexing the cost of acquisition/

improvement.

B.1 Non-Resident Shareholders - Other Than Foreign Institutional Investors

1. Under Section 10(32) of the IT Act, any income of minor children clubbed with the total income

of the parent under Section 64(1A) of the IT Act, will be exempt from tax to the extent of Rs.

1,500 per minor child whose income is so included.

2. As per Section 10(34) read with Section 115-O(6) of the ITA, any income by way of dividends

referred to in Section 115-O (i.e. dividends declared, distributed or paid on or after 1 April 2003

by the domestic companies) received on the Equity Shares is exempt from tax.

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

32

3. As per Section 2(29A) read with Section 2(42A), Equity Shares held in a company are treated

as long term capital asset if the same are held by the assessee for more than twelve months

period immediately preceding the date of its transfer. Accordingly, the benefits enumerated

below in respect of long term capital assets would be available if the Equity Shares are held

for more than twelve months.

4. As per Section 10(38) of the ITA, long term capital gains arising from the transfer of long term

capital asset being an Equity Share, where such transaction is chargeable to securities

transaction tax, will be exempt in the hands of the shareholder.

5. As per first proviso to Section 48 of the ITA, in case of a non-resident shareholder, the capital

gain/loss arising from transfer of Equity Share, acquired in convertible foreign exchange, is to

be computed by converting the cost of acquisition, sales consideration and expenditure

incurred wholly and exclusively incurred in connection with such transfer, into the same foreign

currency which was initially utilized in the purchase of Equity Shares. Cost Indexation benefit

will not be available in such a case. As per Section 112 of the ITA, taxable long-term capital

gains, if any, on sale of Equity Shares is chargeable to tax at the rate of 20% (plus applicable

surcharge and education cess).

6. As per Section 54EC of the ITA and subject to the conditions and to the extent specified

therein, long-term capital gains (in cases not covered under Section 10(38) of the ITA) arising

on the transfer of a long-term capital asset will be exempt from capital gains tax to the extent

such capital gains are invested in a “long term specified asset” within a period of 6 months

after the date of such transfer. It may be noted that investment made on or after April 1, 2007

in the long term specified asset by an assessee during any financial year cannot exceed Rs.

50 Lacs.

However, if the assessee transfers or converts the long term specified asset into money within a

period of three years from the date of its acquisition, the amount of capital gains exempted

earlier would become chargeable to tax as long-term capital gains in the year in which the long

term specified asset is transferred or converted into money.

A “long term specified asset” for making investment under this Section on or after 1st April 2007

means any bond, redeemable after three years and issued on or after the 1st April 2007 by:

• National Highways Authority of India constituted under Section 3 of the National

Highways Authority of India Act, 1988; or

• Rural Electrification Corporation Limited, a company formed and registered under the

Companies Act.

7. As per Section 54F of the IT A, long term capital gains (in cases not covered under Section

10(38)) arising on the transfer of the Equity Shares held by an individual or Hindu Undivided

Family (HUF) will be exempt from capital gains tax if the net consideration is utilised, within a

period of one year before, or two years after the date of transfer, in the purchase of a residential

house, or for construction of a residential house within three years. Such benefit will not be

available:

if the individual or Hindu Undivided Family -

INFORMATION MEMORANDUM QUEST SOFTECH (INDIA) LIMITED

33

• owns more than one residential house, other than the new residential house, on the date

of transfer of the Equity Shares; or

• purchases another residential house within a period of one year after the date of

transfer of the Equity Shares; or

• constructs another residential house within a period of three years after the date of

transfer of the Equity Shares; and

the income from such residential house, other than the one residential house owned on the date

of transfer of the original asset, is chargeable under the head “Income from house property”.

If only a part of the net consideration is so invested, so much of the capital gain as bears to the

whole of the capital gain, the same proportion as the cost of the new residential house bears to the

net consideration, will be exempt.