qatalum site visit - norsk hydro · qatalum site visit (2) certain statements included within this...

TRANSCRIPT

(1)

January 25-26, 2010

Qatalum site visit

(2)

Certain statements included within this announcement contain forward-looking information, including, without limitation, those relating to (a) forecasts, projections and estimates, (b) statements of management’s plans, objectives and strategies for Hydro, such as planned expansions, investments or other projects, (c) targeted production volumes and costs, capacities or rates, start-up costs, cost reductions and profit objectives, (d) various expectations about future developments in Hydro’s markets, particularly prices, supply and demand and competition, (e) results of operations, (f) margins, (g) growth rates, (h) risk management, as well as (i) statements preceded by “expected”, “scheduled”, “targeted”, “planned”, “proposed”, “intended” or similar statements.

Although we believe that the expectations reflected in such forward-looking statements are reasonable, these forward-looking statements are based on a number of assumptions and forecasts that, by their nature, involve risk and uncertainty. Various factors could cause our actual results to differ materially from those projected in a forward-looking statement or affect the extent to which a particular projection is realized. Factors that could cause these differences include, but are not limited to: our continued ability to reposition and restructure our upstream and downstream aluminium business; changes in availability and cost of energy and raw materials; global supply and demand for aluminium and aluminium products; world economic growth, including rates of inflation and industrial production; changes in the relative value of currencies and the value of commodity contracts; trends in Hydro’s key markets and competition; and legislative, regulatory and political factors.

No assurance can be given that such expectations will prove to have been correct. Hydro disclaims any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Forward-looking statements

57Qatalum project – Tom Røtjer

97Qatalum operations – Jan Arve Haugan

3Hydro – Jørgen C. Arentz Rostrup

38Market update – Eigil Madsen

Table of contents

Jørgen C. Arentz Rostrup, Executive Vice President and CFO

Hydro

(4)

Hydro’s value proposition

• Leading integrated aluminium and energy company with global reach and attractive positions across the value chain

• Upstream cost position to be improved by the world-class Qatalum smelter

• Strong operational performance and cost focus

• Financial discipline

• Long-term prospects foraluminium remain encouraging

(5)

Business model

EnergyPrimary Metal

Rolled Products

Metal Markets

Extruded Products

• Revenue in NOK• Cost in NOK

• Long-term power supply

• 9.4 Twh of renewable energy production

• Revenue in USD• Cost in USD – alumina,

petroleum coke• Cost in local currency

– energy, labor, maintenance

• High LME and USD sensitivity

• Improving cost position

• Technology

• EUR and USD business

• Margin business

• Expertise in materials

• Flexible system• Strong marketing

organization

• Margin business• Regional business• Volumes-• 80% Europe, 5%

North-America and 15% other

• Close to customers• Innovation• Market leading in litho

and foil

• Margin business• Local business• Volumes: 75%

Europe, 20% North America and 5% other

• Close to customers• Innovation• Market leading in

Building Systems

Aluminium in productsPrimary aluminium production Midstream, recycling

(6)

1Market

(7)

Historic downturn in 2009

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

20%

24%

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Gross Domestic Product Aluminium Consumption Industrial Production

Source: Global Insight / CRU / Hydro

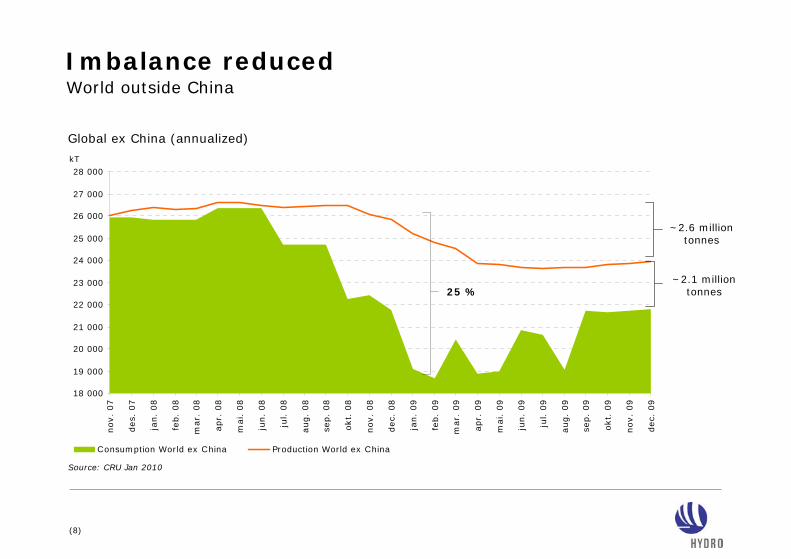

World outside China

% change YoY World ex China

(8)

Source: CRU Jan 2010

Imbalance reduced

Global ex China (annualized)

18 000

19 000

20 000

21 000

22 000

23 000

24 000

25 000

26 000

27 000

28 000

nov.

07

des.

07

jan.

08

feb.

08

mar.

08

apr.

08

mai. 0

8

jun.

08

jul. 0

8

aug.

08

sep.

08

okt.

08

nov.

08

dec.

08

jan.

09

feb.

09

mar.

09

apr.

09

mai. 0

9

jun.

09

jul. 0

9

aug.

09

sep.

09

okt.

09

nov.

09

dec.

09

Consumption World ex China Production World ex China

~2.1 million tonnes

~2.6 million tonnes

25 %

World outside China

kT

(9)

Hydro

Mixed signals in markets and economy

• LME inventories at record level

• Supply/demand imbalance

• Sales volumes increasing

• Margins stable

• Relatively strong LME-price in USD

• Risk of

w-shaped

recovery

• Strong NOK

• World GDP

and IP

growing

• Strong equity

markets

(10)

2Strategy

(11)

Solid measures executed in 2009

• Cash costs reduced by 30%• Primary aluminium production curtailed by 26%• Alumina production curtailed by 22%

• Utilized flexible remelt system to quickly respond to demand changes

• Significant cost savings and manning reductions• Agreement to divest Inasa rolling mill

• Operating capital reduced by NOK 5.8 billion• Capital expenditure plans cut by 50% from 2008-level• Permanent and temporary workers reduced by 4 500• Staff and support manning reduced by 30%, NOK 750 million

in reduced manning and external costs

• Significant cost savings and manning reductions• Agreement to divest Automotive Structures• Decision to close Adrian precision tubing plant

Primary Metal

Metal Markets

Rolled Products

Extruded Products

Hydro

(12)

Conversion cost31%

Power27%

Carbon13%

Alumina29%

2009*

* Includes only fully consolidated smelters

Target to reduce cash cost by 100 USD per tonne, representing 20% reductionin conversion cost

Focus on lean smelter operations and operational excellenceFurther upstream improvements necessary

(13)

Ambitious plan to cut cost by 100 USD/tonne

Calculation based on stable assumptions for LME, currencies, rawmaterial prices etc. Includes only fully consolidated smelters.

90% to be realized by end-2011 compared to 2009

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010E 2011E 2012E

• Accelerated operational performance defined within Primary Metals production management system:• Improved current efficiency• Reduced power consumption• Reduced anode consumption

• Reduced fixed cost and lean operations

(14)

Primary Metal

• Implement stretch targets for cost savings and operational performance at existing assets

• Continued efforts on procurement initiatives

• Production curtailments• Additional curtailments – if needed• No restarts before it makes financial and industrial sense

• New growth projects only in first quartile on cost curve

• Qatalum start-up

Next steps in repositioning

(15)

Metal Markets

Primary production

3rd party primaryExtrusion ingot and Sheet ingot external

DownstreamRolled products

Extrusion

Ingot/scrapFoundry alloys/Wire rod/

Ingot external

Midstream casthouses& remelters

Strategy • Increased business volume through limited asset investments

• Optimized sourcing, casthouse operations and commercial marketing of metal products

• Primary casthouses to maximize capacity utilization by streamlining the production

• Gain leading position in scrap conversion

• Basis for strategic alliances

(16)

Extruded Products

• Leading positions in Extrusion Eurasia and Building Systems• Strong entrepreneurial spirit,

management culture and competence• Product quality and service excellence• Product innovation through strong

customer relations• Performance management – operational

excellence

• Strong position in the US and Brazil

• Strategy• Reinforce European extrusion base• Specialist in energy-neutral building

solutions• Selective acquisitions• Entry into new markets

222145

(1)10

459382

325 323380

456390

1 489

2007 2008

NOK millionUnderlying EBITDA*

1 237 367

2009

*Excluding Automotive Structures

(17)

• Strong multi-brand market penetration

• World wide sales organization

• High performing products

• Selective acquisitions

• Buildings of tomorrow

• Energy saving

• Energy gaining

• 100% recyclable

• Interactive with the user

Building SystemsOur way to energy neutral & surplus buildings

(18)

Rolled Products

• Strong position in foil, litho and automotive

• Underutilization and overcapacity is an industry challenge

• Strategy• Margin management and cash

generation• Focus production system on core

assets• High grading product portfolio

175

10079

92

242295

359

268267

383337

NOK millionUnderlying EBITDA

1 079

2007 2008

1 164 354

2009

(19)

Energy

Note: public ownership implies ownership by the state or municipalities

3.1

2.8

3.0 0.5

Røldal Suldal

Sogn

Telemark

TWh

2044-2049

2022

2051-2057

Strategy• Expand solid captive power position

• 0.5 – 1 TWh development potential• Utilizing existing concession areas and infrastructure• Investment NOK 1.2 – 2.5 billion from 2011 onwards• Normal production today 9.4 Twh

• Long-term power sourcing at predictable cost

Reversion• Effects for private companies• No renewal or new concessions

• Can own up to 1/3 of publicly owned plants• Everlasting concessions if sold to public companies

• Implications for Hydro• First large system to revert in 2022• Financial impact muted by:

• Public everlasting concession possibility• Hydro can maintain 1/3 indefinitely

Normal production capacity per region and terms

No reversion

(20)

Going forward

Upstream • Cost reduction

Midstream • Margin management

Downstream• Margin management • Capture possibilities • Cost control

Working capital management

Capital expenditures discipline

(21)

Attractive upstream growth pipeline

• Potential for expanding Qatalum up to 1.2 million mt

• Utilize next-generation smelting technology, HAL4e

• Development potential 0.5 – 1 TWh

• Utilizing existing concession areas and infrastructure

• Joint venture agreement between Vale (61%), Hydro (20%) and Dubal (19%)

• First stage 1.9 million mt of alumina, potential for expansions up to 7.4 million mt

Qatalum 2 – aluminium smelter, Qatar

CAP – alumina refinery, Brazil

Hydro power developments, Norway

(22)

3Qatalumexecution

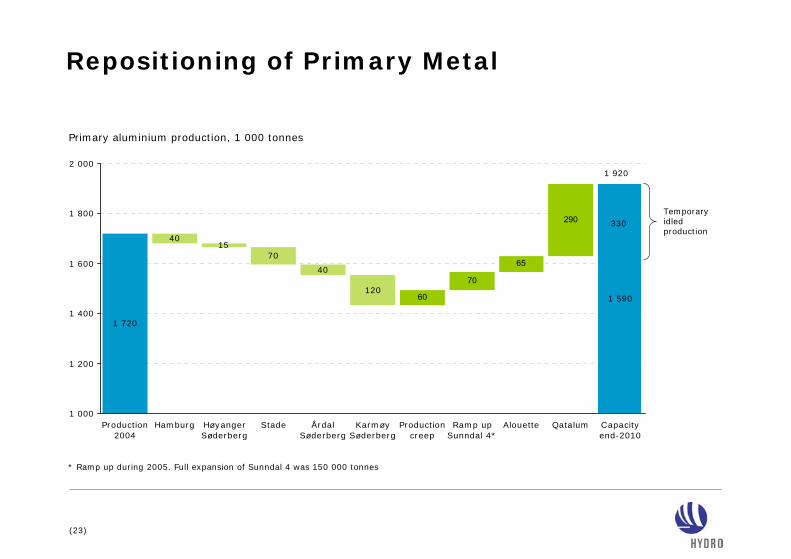

(23)

60

70

65

290

4015

70

40

120

1 720

1 590

1 000

1 200

1 400

1 600

1 800

2 000

Production2004

Hamburg HøyangerSøderberg

Stade ÅrdalSøderberg

KarmøySøderberg

Productioncreep

Ramp upSunndal 4*

Alouette Qatalum Capacityend-2010

Repositioning of Primary Metal

* Ramp up during 2005. Full expansion of Sunndal 4 was 150 000 tonnes

Primary aluminium production, 1 000 tonnes

Temporary idled production

330

1 920

(24)

Qatalum financing

Project economics• First decile position on cash cost

curve when in full operation

Qatalum financing - USD 5.7 billion (100%)• Equity from owners 54%• Project financed 46%

Project financing• Term of loan is 16.5 years from

August 2007• Installment profile adjusted for cash

flow profile• Competitive terms

(25)

Qatalum ramp-up schedule

Production in 1 000 tonnes on 100% basis, annualized

0

100

200

300

400

500

600

1 2 3 4 5 6 7 8 9 10 11 12

(26)

Qatalum earnings

• Build-up costs in 2009 and into 2010

• Depreciated over ~20 years• Marginal tax implications• At current forward prices -

• Earnings negative in 2010• No dividend expected short term

-16

-99 -91

-125

-62

-35

-16

Hydro’s share of underlying EBIT in NOK million 2008 2009

(27)

US South East

US MidwestSouthern Europe/ Mediterranean JapanSouth

Korea

Thailand

Malaysia/SEAsia

ChinaQatar

IstambulLivorno/ Gaeta

BarcelonaSouthern Europe/ MediterraneanLisboa

GCC

India

Planned routes

North America

Hydro‘s metalsourcing system

NorwegianSystem

FromAustralia

Izmir

Qatalum target markets

Taiwan

Total 340 000 tonnes: 75% products & 25% standard ingotGlobal metal sales from Qatalum in 2010

(28)

4Financial flexibility

(29)

Cash flow neutral first nine months 2009

• Significant reductions in operating capital ~NOK 5.8 billion realized in 2009

• Capital discipline – reduced investments

• No dividend payment in 2009

• Qatalum investments• Project financed in first half 2009• Equity contribution from partners

in second half 2009 and 2010

2.5

0.7

3.5

3.33.0

0

1

2

3

4

5

6

Cash endQ4 2008

Operations Investments Financing /currency

Cash endQ3 2009

YTD 2009 in NOK billion

(30)

Capital expenditures

2008 2009E 2010E

Debt-financed investments in joint ventures (upstream)Investments QatalumOtherSustaining capex

NOK billion

~5.3*

~10.2

12.2

* Excluding net operating capital in Qatalum

• ~80% of 2009-2010 investments upstream

• Sustaining capex ~NOK 2.5-3 billion annually

• Qatalum• Project financed in first half 2009• Equity contribution in Q3

– NOK 1.5 billion• Equity contributions from partners

and project financing in Q4• Equity contributions mainly from

partners in 2010

• Additional prospects not included• Holsbru power development• Selective growth in Extrusion and

Building Systems

(31)

Sustaining capital expenditures

Energy

Extruded Products

Rolled Products

Metal Markets

Primary Metal relining

Primary Metal

(32)

Financial position

2.43.03.5

8.7

10.8

Dec 31,2007

June 30,2008

Dec 31,2008

June 30,2009

Sep 30,2009

Cash less interest-bearing debt

(19.0)(19.2)

(15.4)

(2.1)(0.8)

Dec 31,2007

June 30,2008

Dec 31,2008

Jun 30,2009

Sep 30,2009

Adjusted net debt*

* Net interest-bearing debt in equity accounted investments, net pension liability, operating lease commitments and other

NOK billion

(33)

Liquidity well covered

Available long-term credit facilities• EUR 750 million in bank facility

maturing in 2012• USD 1.7 billion in multi-currency

revolving facility maturing in 2014• Currently ~NOK 16 billion undrawn

Qatalum investments• USD 5.7 billion project costs* (100%)

• USD 2.6 billion project financed• USD 0.1 billion outstanding end-Q3

• USD 3.1 billion in equity from owners• USD 1.2 billion remaining end-Q3

* Excluding net operating capital

(34)

Credit quality policy

Maintain investment-grade rating

• Currently: BBB- (S&P), Baa2 (Moody’s), both with negative outlook

• Competitive access to capital and important for Hydro’s business model (partnerships and counterparty risk)

Financial ratios over the business cycle – Hydro’s ambitions

• Funds from operations to net adjusted debt > 40%

• Net adjusted debt to equity < 0.55

Oct-07 Apr-08 Oct-08 Apr-09

Baa1/BBB+

Negative outlook

Baa3/BBB-

Baa2/BBB

Negative outlook

Moody’s

S&P

Ba1/BB+

Investment grade rating

(35)

Price and currency sensitivities

Aluminium price sensitivity +/- 100 USD per tonne NOK/USD sensitivity +/- 0.1 NOK

• Annual sensitivities• Aluminium price sensitivity is net of aluminium price indexed costs• NOK/USD sensitivity includes USD revenues and costs• Based on expected business volumes for 2010 and the following prices:

• Aluminium 1 900 USD/tonne• NOK/USD 5.50

• LME sensitivity excludes unrealized effects related to operational hedging

• USD sensitivity on financial items is based on financial positions end Q3 09

600

450

0

100

200

300

400

500

600

700

EBIT Net income

200

150

0

50

100

150

200

250

EBIT Net income

(36)

Shareholder policy

• Hydro aims to give shareholders competitive returns compared to alternative investments in peers

• Dividend payout ratio* will average 30% over the cycle

• Buyback of shares and extra-ordinary dividends

• When earnings, liquidity position and capital structure allow

• No dividend payout for 2008, but dividend policy maintained

* Dividend divided by net income

(37)

Hydro’s priorities

• Reposition upstream business

• Execute Qatalum

• Proactive corrective measures

• Financial flexibility

• Stay close to customers

• Solid operations

• Competitive shareholder returns

• Dividend policy: 30% of net income over the cycle

(38)

Aluminium market update

Eigil Madsen, Head of Portfolio Development Primary Metal

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

2 600

2 800

3 000

3 200

3 400

Jan.0

8

Feb.0

8

Mar.

08

Apr.

08

May.0

8

Jun.0

8

Jul.08

Aug.0

8

Sep.0

8

Oct

.08

Nov.0

8

Dec.

08

Jan.0

9

Feb.0

9

Mar.

09

Apr.

09

May.0

9

Jun.0

9

Jul.09

Aug.0

9

Sep.0

9

Oct

.09

Nov.0

9

Dec.

09

Jan.1

0

US

D/t

onne

8 000

9 000

10 000

11 000

12 000

13 000

14 000

15 000

16 000

17 000

18 000

19 000

20 000

21 000

22 000

23 000

24 000

25 000

26 000

27 000

NO

K/t

onne

LME 3m USD LME 3m NOK

Aluminium price

-60%

+80%

-48%

+50%

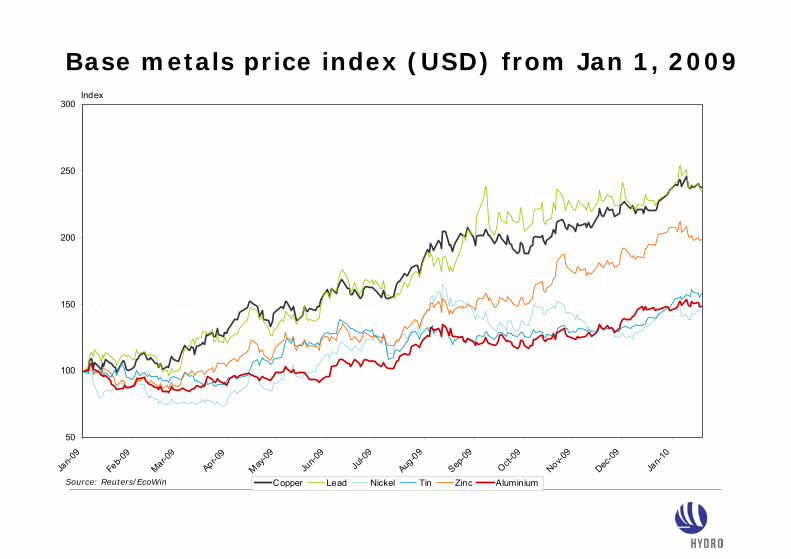

Base metals price index (USD) from Jan 1, 2009

Source: Reuters/EcoWin

50

100

150

200

250

300

Jan-0

9

Feb-0

9

Mar-09

Apr-09

May-09

Jun-0

9

Jul-0

9

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-1

0

Index

Copper Lead Nickel Tin Zinc Aluminium

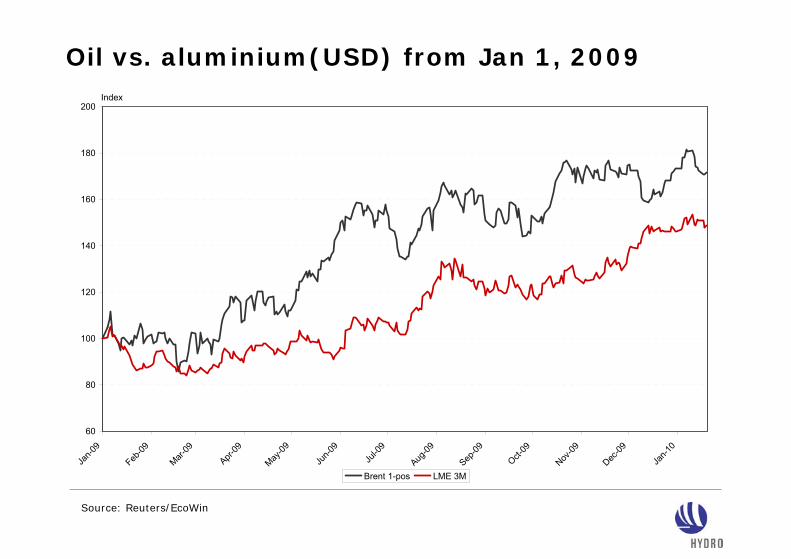

Oil vs. aluminium(USD) from Jan 1, 2009

Source: Reuters/EcoWin

60

80

100

120

140

160

180

200

Jan-0

9

Feb-09

Mar-09

Apr-09

May-09

Jun-0

9

Jul-0

9

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-1

0

Index

Brent 1-pos LME 3M

2 000

2 050

2 100

2 150

2 200

2 250

2 300

2 350

2 400

1.D

ec.

09

3.D

ec.

09

5.D

ec.

09

7.D

ec.

09

9.D

ec.

09

11.D

ec.

09

13.D

ec.

09

15.D

ec.

09

17.D

ec.

09

19.D

ec.

09

21.D

ec.

09

23.D

ec.

09

25.D

ec.

09

27.D

ec.

09

29.D

ec.

09

31.D

ec.

09

2.J

an.1

0

4.J

an.1

0

6.J

an.1

0

8.J

an.1

0

10.J

an.1

0

12.J

an.1

0

14.J

an.1

0

16.J

an.1

0

18.J

an.1

0

20.J

an.1

0

US

D/t

onne

11 500

11 700

11 900

12 100

12 300

12 500

12 700

12 900

13 100

13 300

13 500

13 700

NO

K/t

onne

LME 3m USD LME 3m NOK

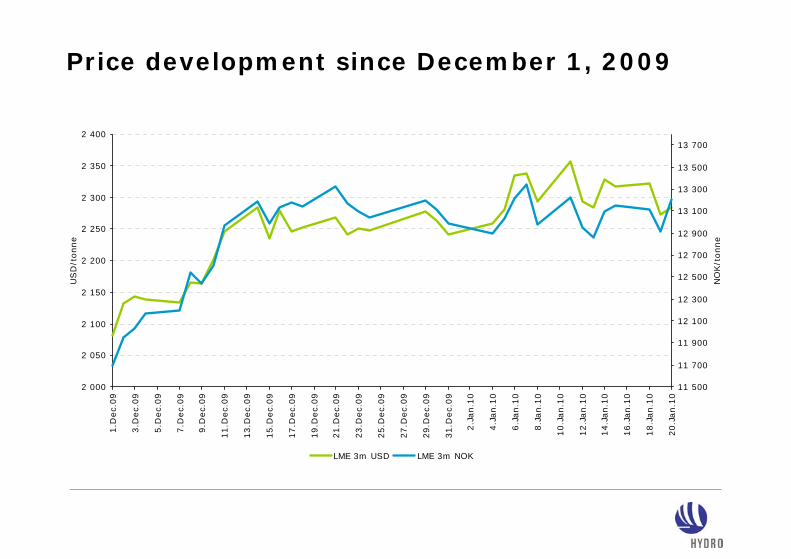

Price development since December 1, 2009

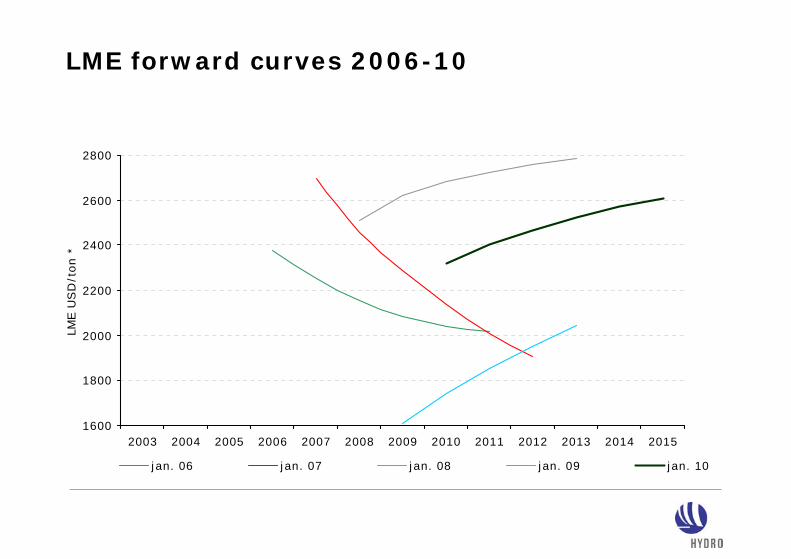

LME forward curves 2006-10

1600

1800

2000

2200

2400

2600

2800

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

LME U

SD

/ton *

jan. 06 jan. 07 jan. 08 jan. 09 jan. 10

18 000

19 000

20 000

21 000

22 000

23 000

24 000

25 000

26 000

27 000

28 000

nov.

07

des

. 07

jan.

08

feb.

08

mar

. 08

apr.

08

mai

. 08

jun.

08

jul. 0

8

aug.

08

sep.

08

okt

. 08

nov.

08

dec

. 08

jan.

09

feb.

09

mar

. 09

apr.

09

mai

. 09

jun.

09

jul. 0

9

aug.

09

sep.

09

okt

. 09

nov.

09

dec

. 09

jan.

10

kT

Consumption World ex China Production World ex China

Still unbalance, but at a reduced level

Source: CRU

~2.1 mill tons

~2.7 mill tons

Global ex China (annualized)

Source: Reuters/EcoWin

1 000 tonnes

Stock development

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

Jan.0

8

Feb.0

8

Mar.

08

Apr.

08

May.0

8

Jun.0

8

Jul.08

Aug.0

8

Sep.0

8

Oct

.08

Nov.0

8

Dec.

08

Jan.0

9

Feb.0

9

Mar.

09

Apr.

09

May.0

9

Jun.0

9

Jul.09

Aug.0

9

Sep.0

9

Oct

.09

Nov.0

9

Dec.

09

Jan.1

0

IAI inventories LME inventories

(300)

(200)

(100)

0

100

200

300

400

500

600

700

800

Jan Feb Mar April May June July Aug Sep Oct Nov Dec

LME stocks IAI stocks Japanese Port stocks

Net primary export to China Est. Unreported stocks (CRU) Balance

1 000 tonnes

Sto

ck r

educt

ion/

Net

im

port

Apparent (un)balance demand/production outside China

Sto

ck incr

ease

/

Net

exp

ort

9 000

10 000

11 000

12 000

13 000

14 000

15 000

16 000

17 000

18 000

nov.

07

des

. 07

jan.

08

feb.

08

mar

. 08

apr.

08

mai

. 08

jun.

08

jul. 0

8

aug.

08

sep.

08

okt

. 08

nov.

08

dec

. 08

jan.

09

feb.

09

mar

. 09

apr.

09

mai

. 09

jun.

09

jul. 0

9

aug.

09

sep.

09

okt

. 09

nov.

09

dec

. 09

annualis

ed k

T p

er

month

China Consumption China Production

Chinese production at all-time high

China (annualised per month)

Source: CRU

…and increasing

LME and Shanghai* aluminium price

1 000

1 500

2 000

2 500

3 000

3 500Ja

n.0

7

Mar.

07

May.0

7

Jul.07

Sep.0

7

Nov.0

7

Jan.0

8

Mar.

08

May.0

8

Jul.08

Sep.0

8

Nov.0

8

Jan.0

9

Mar.

09

May.0

9

Jul.09

Sep.0

9

Nov.0

9

Jan.1

0

USD/t

SHFE 3M (*incl VAT) LME 3M

Arbitrage LME vs Shanghai aluminium price

Source: Reuters/EcoWin

3 M Prices

0

100

200

300

400

500

600

700

800

Jan-0

9

Feb-09

Mar-09

Apr-09

May-09

Jun-0

9

Jul-0

9

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-1

0

USD/mt

Difference SHFE - LME 17% VAT (LME) Freight (30 USD/t)

(350)(300)(250)(200)(150)(100)(50)

050

100

150200250300350400450500550600

Primary / alloyed Semis Fabricated Scrap Total

China: swift response to market conditions and prices Limited imports of primary metal likely in 2010

• Production curtailments

• Strategic government purchases –lifted inland prices, import became profitable

• Government incentives increased demand in 2009

• Production increase in 2009/2010• Restart of curtailed capacity• New capacity being built

• Imports of primary aluminium expected to stay low, but also primary exports to be limited

Source: Hydro / Antaike Jaunary 2010

1 000 tonnes

Net

im

port

Net

exp

ort

2006 2007 2008 2009

New production from green and brownfieldprojects under construction is coming on stream

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2010 2011 2012 2013

Accumulated new capacity World ex China, 1 000 tonnes

Source: Hydro S&BD , Analysis 2009

Qatalum

• 600 kT

Emal

• 700 kT

India

• ~ 1500 kT

• In addition we assume 300 ktunspecified creep by 2010, and 400 kt in 2011

Industry cost came down from 2008 to 2009, currently the cost curve is moving up

Curtailed capacity

Source: CRU, BOC 2008: LME 2834 USD/tonne, USDNOK 5,16BOC 2009: LME 1940 USD/tonne, USDNOK 5,64

0

400

800

1 200

1 600

2 000

2 400

2 800

3 200

3 600

0 4000 8000 12000 16000 20000 24000 28000Accumulated capacity World ex China (1000 t)

Bus

ines

s O

pera

ting

cost

(US

D/t)

BOC 2008 BOC 2009

Cost curve is currently moving up from 2009 levels as LME drives alumina price up. Energy and other raw materials may follow

18 000

19 000

20 000

21 000

22 000

23 000

24 000

25 000

26 000

27 000

28 000

2006 2007 2008 2009 2010 2011

Production New capacity Demand

2010 balance – same view as shown at CMD World outside China

Source: CRU / Hydro

8%

8%

Primary export

Stock increase

Net curtailments

1 000 tonnes

2009 imbalance handled by:

2010 imbalance “handling” options:

• Consumption upside (GDP, pipeline)• Increased primary demand due to

increased scrap export to China• Stock increase• New curtailments

Demand estimates world excluding China

5 %22.521.4Alcoa – 4Q presentation

9 %22.320.4CRU – January Quarterly

%Demand 2010 million tonnes

Demand 2009 million tonnes

World outside China

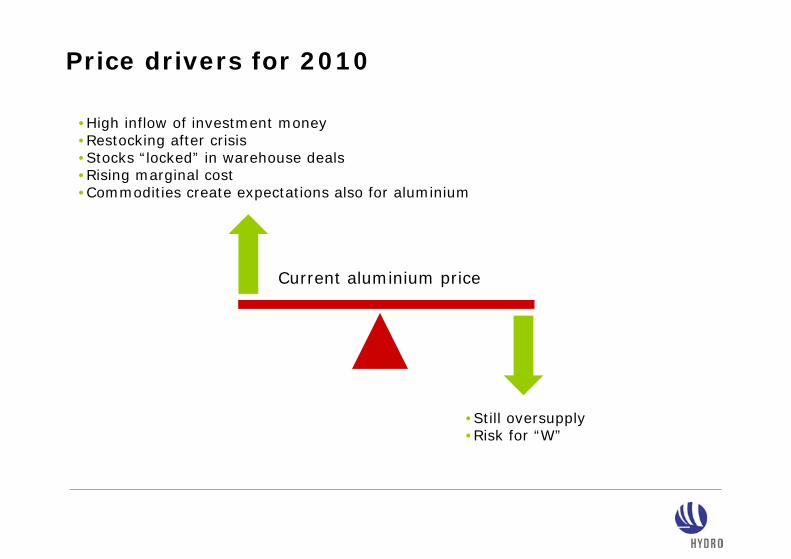

Strong LME price in spite of sustained over production

• High inventory levels • Availability of capital at low interest rates• A stable contango has financed stocks that are “locked in” until Q2/Q3 2010

• Strong inflow of investment money – No producers selling

• Physical ingot premiums still elevated – Rusal continuing warehousing deals

Price drivers for 2010

Current aluminium price

•Still oversupply•Risk for “W”

•High inflow of investment money•Restocking after crisis•Stocks “locked” in warehouse deals •Rising marginal cost•Commodities create expectations also for aluminium

Qatalum project

Tom Røtjer, Executive Vice President and Head of Projetcs

Qatalum location

Mesaieed Industrial City

● Qafco 1 in 1973 ● Qafco 2 in 1979● Qafco 3 in 1997● Qafco 4 in 2004

Hydro history in Qatar

● Qatar Vinyl Company in 2001

Qatalum a 50/50 joint-venture company

Power plant and smelter

Joint venture agreement

Technology and competence

Metal marketing & off-take

Project management

50% 50%

Gas supply

Industrial climate

Site

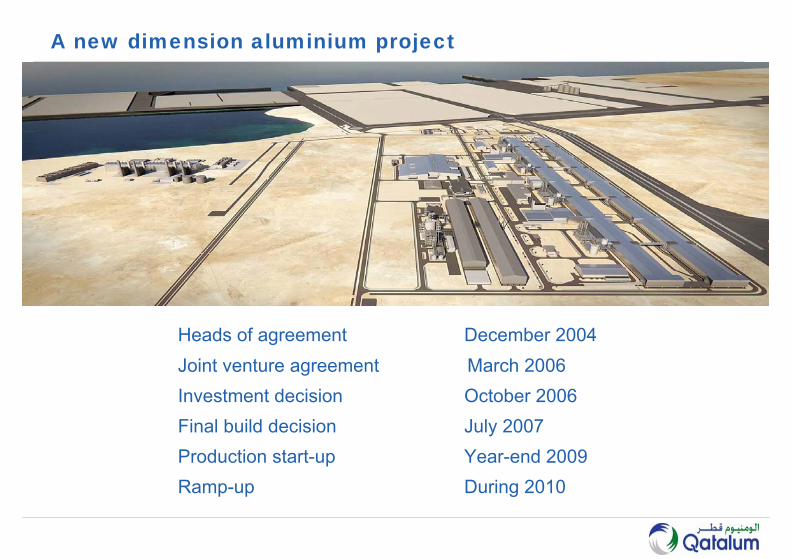

Heads of agreement December 2004Joint venture agreement March 2006Investment decision October 2006Final build decision July 2007Production start-up Year-end 2009Ramp-up During 2010

A new dimension aluminium project

• Hydro technology used in Sunndal, further developed for Qatalum• Project execution, start-up and operations experience implemented

in Qatalum • Personnel with experience from Sunndal key in Qatalum project

Key reference project - Sunndal 4

Power Plant

Cast house

Anode plant

Pot rooms

Port

Qatalum project scope

Silos

Construction Village

10.000 people

Anode Service PlantKempe

Power PlantGeneral Electrics

Service Areas & Potroom BuildingSNC - Lavalin

Construction CampSaudi Arabian Trading & Construction Co.

PotshellAhmed Mansoor Anode Superstructure

Great Wall China

Power PlantDoosan

Pot Tending MachineNKM Noell

BusbarsSalztburger Al.

CasthouseFATA/ K-HomeAnode Baking PlantFATA/ K-Home

HAL3000 Pot Control SystemABB

Paste PlantSolios

FTP & Dist. SystemsSolios

Recitifier PlantABB

Installation Reduction Celland Potroom EquipmentDutco McConnell Dowell

Global procurement

21 Contracts

9 GCC, 2 North America, 7 Europe, 2 Asia, 1 Australia

2007-2008 ”Crunch time”

for project execution in the Gulf area

First site office February 07 Hail storm March 07

Qatalum site September 2007

10 million tonnes of landfill=200.000 truckloadsTotal driving distance ~20 million km1500 truck loads pr day

June 2008 - piling

June 2008 - 7200 people on site and INCREASING

17 000 workers on site – January 2009

Construction village

Construction Village for 10 000 people

Health, Safety & Environment – December 2009

Qatalum HSE statistics Construction hours

0,0

1,0

2,0

3,0

4,0

5,0

HRI rate 1,4 1,2 1,0 1,1 0,9 1,2 1,0 0,8 1,0 1,0 1,0 1,0 1,0 1,0 1,1 1,0 1,0 0,9 1,0 1,1 1,0 1,0 1,1 1,1 1,2

TRI rate 3,2 4,0 3,3 3,1 2,7 2,4 2,9 2,7 3,4 3,2 3,0 2,9 2,9 2,9 3,0 3,1 3,1 3,0 3,0 3,0 3,0 3,0 2,9 3,0 3,0

LTI rate 1,4 2,4 2,0 1,9 1,5 1,4 1,1 1,0 0,8 0,7 0,6 0,6 0,5 0,5 0,5 0,5 0,5 0,4 0,5 0,4 0,4 0,4 0,4 0,4 0,4

LTI-KPI 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

des-07

jan-08

feb-08

mar-08

apr-08

mai-08

jun-08

jul-08

aug-08

sep-08

okt-08

nov-08

des-08

jan-09

feb-09

mar-09

apr-09

mai-09

jun-09

jul-09

aug-09

sep-09

okt-09

nov-09

des-09

Total Project Number of LTI Medical Treatment * Working hours LTI-rate* TRI-rate* High Risk Total No. Cases RWC (Constr. hours) Incidents of HSE

NH Contr. NH Contr. NH Contr. NH Contr. Total NH Contr. Total ObservationsPeriod 0 1 0 5 1 18 912 3 216 293 0 0,3 0,3 0 2,2 2,2 4 4161Accum 0 32 0 139 64 390 042 79 057 222 0 0,4 0,4 0 3,0 3,0 84 66688

Last 12 months Number of LTI Medical Treatment * Working hours LTI-rate* TRI-rate* High Risk Total No. Cases RWC (Constr. hours) Incidents of HSE

NH Contr. NH Contr. NH Contr. NH Contr. Total NH Contr. Total ObservationsPeriod 0 1 0 5 1 18 912 3 216 293 0 0,3 0,3 0 2,2 2,2 4 4161Accum 0 19 0 89 52 241 672 52 972 847 0 0,4 0,4 0 3,0 3,0 61 52713

*Man-hours from NKM Noell and Solios Carbone have not been included as the report has not yet been submitted

No. of cranes related to no. of observations

215 14

33 28

61

37

61 6449

2639

3138

47

30 36

19 187 36

20

82

148

215 216

235

266

248233 230

215

182

0

50

100

150

200

250

300

2008 0

1200

8 0220

08 03

2008 0

420

08 05

2008 0

6200

8 07

2008

0820

08 09

2008 1

020

08 11

2008 1

2200

9 0120

09 02

2009 0

320

09 04

2009 0

5200

9 06

2009

0720

09 08

2009 0

9Number ofMajor/Critical orMedium/Seriouscrane related obs.

No of cranes

December 7, 2009 Halfway there... Pot room installation

Overall progress by end December 2009: 95%

Qatalum completion : some 400.000 tags

THE HYDRO WAY !!!!!!!!!!

Qatalum completion : some 400.000 tags

THE HYDRO WAY !!!!!!!!!!

2009-10-26

2009-10-13 potroom building and fume treatment plant

2009-10-26

Carbon - Baking Furnace Tending Assembly

Anode Baking furnace production:

340 000 anodes per year.

Paste Plant capacity 60 tonnes/hour of green anodes

2009-10-26

2009-12-14 Silos with conveyor belt

2009-09-27

Start-up Potline 2 - December 16, 2009

Qatalum power plant

EPC- Contractor: GE / DoosanEPC value: appr. 900 musdPower production Cap: 1350 MWGrid Connection: 250 MWSite: 252.000 m2

Fuel Gas

Aluminium Plant 220kV GIS

Rectifiers220kV Distribution

Qatalum Power Plant Open Cycle OperationQP

GTGen ~

GTGen ~

GTGen ~

GTGen ~ 219 MW

219 MW

219 MW

219 MW

400kV Grid Connection

250 MW

QP

Fuel Gas

Aluminium Plant 220kV GIS

Rectifiers220kV Distribution

Combined Cycle Operation

GTGen ~

GTGen ~

GTGen ~

GTGen ~

400kV Grid Connection

250 MW

HRSG

HRSG

HRSG

~HP LP Gen

Condr

Steam Turbine 1

~HP LP Gen

Condr

Fume Treatment(6165 m3/hr)

SW Make-Up (8025 m3/hr)

Steam Turbine 2

Cooling Water System

Power Plant OutputMax Power: ~ 1350 MWPower in (n-1) ~ 1100 MWPower in (n-2) ~ 800 MW

HRSG

SW Circ(88 000 m3/hr)

Power plant 2009-10-26

Power plant

Power plant

Qatar newspapers October 5, 2009

Key project success factors

● Well-defined concept at time of decision● Successful contract strategy and selection of contractors● Interface management● Sound risk management● Active stakeholder management● Strong HSE ambitions● Project completion – “The Hydro Way”

Site canteen

Jan Arve Haugan, CEO Qatalum

Qatalum operations

Qatalum

Committed to deliver…

Qatalum Operations- January 26, 2010

Background

Organization development

Start up of Operations

Ramp up plan

Qatalum going forward

Qatalum - Background

Qatalum- A 50/50 Joint Venture

Heads of agreement December 2004Joint venture agreement March 2006Investment decision October 2006Final build decision July 2007Production start-up Year- end 2009Ramp-up During 2010

A new dimension aluminium project

Qatalum

Qatalum

Qatalum

Power Plant

Cast house

Anode plant

Pot rooms

Port

Qatalum project scope

Silos

Construction Camp

10.000 people

Qatalum organization

Deputy CEOHassan Al-Rashid

HR & AdmAhmed Al-Kuwari

Internal Auditor

HSE Manager

CFOOlaf Meissner

CarbonAndrew Robbins

ReductionRoald Holten

CasthousePål Vigeland

TechnicalKurt Nilsson

PowerSteve Davison

CEOJan Arve Haugan

Anode Service PlantKempe

Power PlantGeneral Electrics

Service Areas & Potroom BuildingSNC - Lavalin

Construction CampSaudi Arabian Trading & Construction Co.

PotshellAhmed Mansoor Anode Superstructure

Great Wall China

Power PlantDoosan

Pot Tending MachineNKM Noell

BusbarsSalztburger Al.

CasthouseFATA/ K-HomeAnode Baking PlantFATA/ K-Home

HAL3000 Pot Control SystemABB

Paste PlantSolios

FTP & Dist. SystemsSolios

Recitifier PlantABB

Installation Reduction Celland Potroom EquipmentDutco McConnell Dowell

Global Procurement

21 Contracts9 GCC, 2 North America, 7 Europe, 2 Asia, 1 Australia

1

18

1

1

1

1

1

1

26

5

69

6

61

21

1

1

1

3

1

92

1

201

328

45

5

8

74

1

12

4

2

9

Qatalum’s Global Family

Mobilization Progress

Recruitment Plan Vs Actual

0

200

400

600

800

1000

1200

1400

May-07

Jul-0

7Sep

-07Nov

-07Ja

n-08

Mar-08

May-08

Jul-0

8Sep

-08Nov

-08Ja

n-09

Mar-09

May-09

Jul-0

9Sep

-09Nov

-09Ja

n-10

Mar-10

May-10

Jul-1

0Sep

-10Nov

-10

Date of Employment

No

of E

mpl

oyee

s Recruitment in Progress

Employees Identified

Planned

Our governing documents

Qatalum directives• Code of conduct• Corporate social

responsibility• Etc.

Qatalum policies• Duty visits• Accounting• Etc.

Our Strategic

focus areas

Operational excellence• Entire value chain• Continuous improvement

Environmental integrity• Life-cycle view• Operating philosophy• Communications

Value for Qatar• People development• Industrial relations

Mission, Values, Strategies and Governing Documents

The Qatalum Way

Mission

Values

Strategies

Governing documents

Work processes, roles and relations

Value based management

Qatalum principles

The Qatalum Values Our performance criteria

Beliefs that differentiate and

focus our performance

Our Values

EthicsRelationships, Teamwork, Communication

RespectWe work in an open, cooperative way.

DriveEfficiency, Innovation

ProactiveWe are driven to meet optimum standard while always seeking improvement.

AbilityCompetence, Reliability

TrustworthyWe always keep our word and ensure the job gets done right.

AttitudeMotivation, Seeing big picture

EnthusiasticWe have a positive attitude toward our jobs and each other.

TechnicalBasic Course

Cast houseBasic Course

ReductionBasic Course

CarbonBasic Course

Power PlantBasic Course

Employee training according to role descriptionThe period covers Process training, Supplier training and Special courses

2 days

1-3 days

3-6 weeks

4 days

Special coursesEnglish HSE Energy control Work permit Car certificate SAP-MM

Truck certificate SOP alignment APICS Train the trainer

Vehicle certif. Crane certificate SAP PM SAP-HR SAP FICO1-5 days

Qatalum Basic Course(Introduction, Qatalum Way, HSE, SOPs, Aluminium, Qatalum Plant)

Leadership Course (Supervisors/experts)(Leadership, HSE, communication, cultural understanding, Qatalum Way

Process training – alignment to Q SOPs)

= Operator training

= Supervisor/staff training

A Comprehensive Training Program

Growing international media interest with high level visits

October 2009

October 26, 2009, the first pitch vessel arrived at Qatalum’s inbound dock

Anode Handling and Storage

Rodding Anodes

Dry out of Anode Baking Furnace at December 31, 2009

Qatalum Project and Management

Potline -1 Team ready for Start up

PTM Cranes at Potline 1

CasthouseCast house – Furnace

First Foundry Alloy December 04, 2009

Foundry Alloy ready for market

First Export of Foundry Alloys – December 18, 2009First Export of Foundry AlloysQatar National Day, December 18, 2009

First Extrusion Ingot January 22, 2010

Raw Material storage at Harbour Area

Critical period ahead

Qatalum – competitive cost position

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

3,600

0 4000 8000 12000 16000 20000 24000 28000

BOC 2008 BOC 2009

Curtailed capacity

Accumulated capacity World ex China (1000 t)

Business Operating cost (USD/t)

2009 2010 2011 2012 2013

Source: CRU, BOC 2008: LME 2834 USD/ton, USDNOK 5,16BOC 2009: LME 1594 USD/ton, USDNOK 6,53

Qatarisation

Established 5 years intake plan

Agreement with Qatar University

Professorship at QU"Aluminum Production Technology"

Relationship with the high schools in Al-Wakrah

Recruit 35 technicians from different disciplines through QP’s corporate training center

Direct recruitment and training of 10 tapping vehicle operators/drivers for the Reduction Dept.

Intake of Technicians/Operators through QP Training Center

Head of Qatarization

Training & Development Supervisor

Recruitment Supervisor(Qatarization)

Qatalum

Deliver as committed

www.hydro.com