q&a target2-securities for · pdf fileq&a target2-securities for funds ... the...

TRANSCRIPT

Q&A TARGET2-Securities for FundsUpdated as of November 2016

Q&A

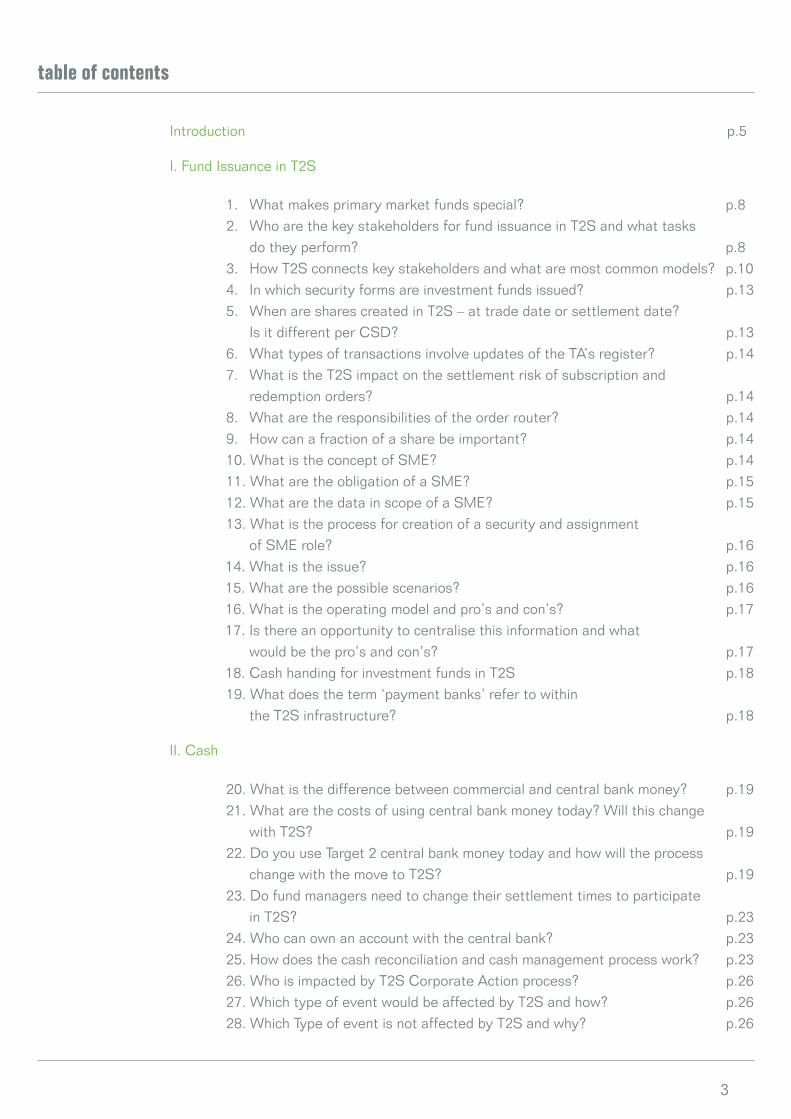

table of contents

3

Introduction p.5

I. Fund Issuance in T2S 1. What makes primary market funds special? p.8 2. Who are the key stakeholders for fund issuance in T2S and what tasks do they perform? p.8 3. How T2S connects key stakeholders and what are most common models? p.10 4. In which security forms are investment funds issued? p.13 5. When are shares created in T2S – at trade date or settlement date? Is it different per CSD? p.13 6. What types of transactions involve updates of the TA’s register? p.14 7. What is the T2S impact on the settlement risk of subscription and redemption orders? p.14 8. What are the responsibilities of the order router? p.14 9. How can a fraction of a share be important? p.14 10. What is the concept of SME? p.14 11. What are the obligation of a SME? p.15 12. What are the data in scope of a SME? p.15 13. What is the process for creation of a security and assignment of SME role? p.16 14. What is the issue? p.16 15. What are the possible scenarios? p.16 16. What is the operating model and pro’s and con’s? p.17 17. Is there an opportunity to centralise this information and what would be the pro’s and con’s? p.17 18. Cash handing for investment funds in T2S p.18 19. What does the term ‘payment banks’ refer to within the T2S infrastructure? p.18

II. Cash

20. What is the difference between commercial and central bank money? p.19 21. What are the costs of using central bank money today? Will this change with T2S? p.19 22. Do you use Target 2 central bank money today and how will the process change with the move to T2S? p.19 23. Do fund managers need to change their settlement times to participate in T2S? p.23 24. Who can own an account with the central bank? p.23 25. How does the cash reconciliation and cash management process work? p.23 26. Who is impacted by T2S Corporate Action process? p.26 27. Which type of event would be affected by T2S and how? p.26 28. Which Type of event is not affected by T2S and why? p.26

table of contents

4

29. What will T2S mean to market claims? p.26 30. How is the event notification of the TA reconciled with the CSD? p.26

III. Corporate actions in T2S

31. Does T2S change the way entitlement is calculated by the registrar? p.26 32. How is entitlement impacted by transfer? p.27 33. The impact of T2S on the transparency dilemma p.27 34. What are the challenges of T2S for the funds distribution? p.27 35. Why is transparency important? p.27 36. Did these challenges already exist pre T2S? p.28 37. Why are these challenges more important with T2S? p.28 38. What CSD models are currently used for Luxembourg funds? p.28 39. How is transparency managed in existing CSD models? p.29 40. What order-marking practices could be used? p.30 41. What position reporting practices could be used? p.30 42. How does each model respond to the challenges in the asset management industry? p.30 43. What is required to make these solutions work? p.31 44. Is there a need to review distribution agreements? p.31

Glossary p.33

5

introduction

Dear Reader,

TARGET2 -Securities (T2S) will have a significant impact on the fragmented European securities market, as domestic and cross-border settlement is taking place going forward on one centralised IT-platform. T2S is developed and operated by the Eurosystem, the monetary authority of the Eurozone, run by the European Central Bank and participating national central banks.

Will this commoditised securities settlement platform lead to a downstream harmonisation for equities, bonds or even primary market traded investment funds?

The answer will be yes, still, the big unknown is the size of the downstream harmonisation taking place and as well as the time it will take. The European authorities will carefully watch this development and nobody should be taken by surprise when future regulation will support a continued harmonisation across asset classes, leveraging on the T2S set-up.

T2S for investment funds will enable investors, distributors, asset managers and service providers alike to benefit from a secure and efficient way of cross border settlement across 21 European markets by using highly scalable and automated processes.

With this Q&A we will assist you in understanding the implications of T2S for investment funds and how you may benefit from the T2S opportunity.

Is a centralised platform still fit for purpose?

Yes, it is! The financial service industry should reap the gains which T2S brings for its clients. Block-chain might be the future backbone of the financial industry. There is considerable support and momentum for Distributed Ledger Technologies like Blockchain but it may take a long time until it becomes reality. Therefore acceleration needs to take place in adapting to T2S, to really make use of all benefits in time. The financial services industry cannot afford to stand still.

But where did T2S come from?

It all began with the interbank payment system for the real-time processing of cross-border money transfers throughout the European Union called TARGET. With time, TARGET was replaced by TARGET2 (T2) to support the euro real-time gross settlement payment system (RTGS).

The second key piece of the financial market infrastructure owned and managed by the Eurosystem is TARGET2-Securities, or T2S, which went live in June 2015. While TARGET2 had brought harmonisation to the cash side of settlement, the market infrastructure for securities settlement was still highly fragmented. T2S was therefore put forward as a way to improve the efficiency of securities settlement in Europe. It is an integrated, pan-European IT platform which processes the real-time settlement of securities transactions against central bank money across Europe will move their settlement activity to T2S in a number of migra-tion waves between June 2015 and September 2017.

It is fair to say that T2S is an unescapable feature in the future European securities settlement arena. Make use of it!

We wish you good and fruitful reading.

6

The primary areas for asset managers and their service providers to consider are:

• Requirement of the ability to perform trea-sury activities with money held in central banks. This will require discussion with the respective payment (commercial) bank to provide segregated Dedicated Cash Account (DCA) arrangements within T2S to allow direct access to these accounts by the asset manager.

• Rationalisation and consolidation of bank-ing and payment services linked to the CSD network for distributors and investors, where several cash positions are now held to support activity with multiple CSDs, ICSDs plus central and commercial bank accounts. This should provide opportunities to merge existing functions with fewer banking rela-tionships that offer compatible services and possibly allow for improved fee negotiations.

• Expanded distribution capabilities for domes-tic funds within the CSD network. This will be possible with the availability of CSD links supported by bilateral agreements between the participating CSDs. Asset managers should also consider the impact on marketing material and registration of fund in different countries.

• Depending on how the payment bank has structured their accounts with the NCB and using the RTGS account in T2 linked to DCA’s in T2S, there is the facility to obtain cash reporting activity if required by the cus-todian/ TA or asset manager, provided they are Directly Connected Parties (DCP) within the T2S system.

Impact of T2S on the shareholder transparency

Cross-border transactions and holding, in or outside T2S, are making the distribution oversight challenge even more complex. This is a challenge which offers the unique opportunity to work on the transparency dilemma of the fund industry, surpassing T2S.

To address this challenge, we need to combine transparency on orders and transparency on posi-tions and to have a joint approach supported by all market players. This implies:

Read it all in 60 seconds

When you as an asset manager already have invest-ment fund shares held through a national European CSD (or ICSDs) you are likely to be in scope of T2S.

In this instance it becomes important to know and understand T2S, and perhaps even formulate a prod-uct policy involving T2S. Should your investment funds not currently be eligible within a national European CSD you may still need to address the T2S question as you may have investors or distributors requesting T2S settlement going forward.

Impact of T2S on the fund issuance process

The implementation of T2S may require asset managers to review their current model with regards to issuance of fund shares in CSDs/ICSDs and the potential migration of this activity to T2S.

In particular, they will need to pay attention to:

• Whether they need to change their current fund issuance model or continue with the as is model. E.g. CSD settlement may have not been offered until now leading to a substan-tial change. The review needs to take into account all drivers and stakeholders in the fund issu-ance process (e.g. the service providers and distributors) before any decision should be taken. Depending on the asset manager distribution strategy and countries targeted, several options are possible with regards to fund issuance.

• The CSDs they interact with the participants in the T2S chain, being the Issuer CSDs and also in some cases with Investor CSDs (e.g. for transparency purposes) to achieve the most efficient operational outcome.

Impact of T2S on the cash process

T2S presents also opportunities in the cash man-agement arena, leading to more efficiencies through liquidity pooling. This pooling effect can be further leveraged once the current short-comings in Europe when it comes to local paying agent requirements is addressed. In turn, this improves fund distribution and allows a better liquidity management by utilis-ing pooled instead of segregated cash positions.

7

instruments that settle in T2S will have Corporate Action events where proceeds will be cash and/or securities (investment funds shares). The process will not be any different than for the other financial instruments settling in T2S3.

Conclusion

The Asset Manager will have various options related to CSD (and thus T2S) distribution.

1. If the Fund already is featured on a CSD the Fund needs to verify if its CSD will register the Funds in T2S, a prerequisite to subse-quently settle the Fund in T2S.

2. If a Fund today is issued on a CSD but wants to change CSD or wants not to be featured on T2S despite otherwise being eligible it will need to seek active dialogue with the CSD4.

3. If the Fund is currently not in a CSD5 but wants to render the Fund available in T2S it will need to seek out an T2S connected CSD and issuing agent (the current TA, or the desired CSD could be the first port of call for this).

• The definition of a central market-led data-base of order marking allowing distributors, in the T2S zone, but also outside, to be uniquely identified with all asset managers;

• The order marking of orders (e.g. subscrip-tions, redemptions, switches) and transfers;

• The implementation of incentives to ensure of gradual take-up of order marking practices throughout distribution chain, such as the application of front-end load fees for orders not being marked;

• The implementation of a position report-ing to the TA, as for example the new ISO 20022 transparency of holdings standard that should be adopted by all the intermediaries being in the custody chain.

The details of the issuance, cash, corporate actions as well as the order-routing and shareholder trans-parency are covered in all detail on the next pages. We hope you got interested.

Impact of T2S on the corporate actions

T2S is a settlement engine, but it supports the CSDs in their management of custody services by offering all the required functionalities. Investment funds

3 T2S CA standards: In line with CAJWG standards, T2S CA standards should apply to all securities used for direct investments (equities, fixed income instruments) deposited and settled in Book Entry form with an (I)CSD in Europe; investment funds list-ed and traded on a regulated trading venue should be processed, where possible, in accordance with the applicable standards. See: http://www.ecb.europa.eu/paym/t2s/progress/pdf/subcorpact/20130516-t2s-market-claim-standards-ag-approved-march.pdf?c9ff3488f7660466f76ce5001da27606

4 According to T2S Eligibility criterion 3: CSDs are eligible for access to T2S services provided that they make each security/In-ternational Securities Identification Number for which they are an issuer CSD, or technical issuer CSD, available to other CSDs in T2S upon request See: https://www.ecb.europa.eu/ecb/legal/pdf/l_31920111202en01170123.pdf

5 ICSDs do count in this respect, as at least one of them plan to allow seamless connections for fund issuance into T2S

8

An investor can be an Ultimate Beneficial Owner (UBO), intermediary to an UBO or intermediary to another intermediary. In case the investor is not the UBO every party in the chain holds Anti-Mon-ey-Laundering and Know-Your-Client (AML/KYC) responsibilities on their underlying clients. Every intermediary needs to ensure compliance with all AML/KYC regulations and give comfort to the enti-ty where it holds securities account.

b) CSD

The same CSD in T2S may act as Issuer or as inves-tor CSD, depending on the financial instrument in question.

Investors’ holdings are kept segregated or in pooled accounts6. The CSD7 opens securities accounts for institutional investors who have signed an agree-ment with them to provide a neutral and scalable infrastructure for settlement (primary and secondary markets). There may also be multiple ancillary ser-vices offered by the CSD that are tailored for invest-ment funds, such as order routing, asset servicing, reconciliation and reporting of trade dated holdings.

The investor may hold investment fund shares directly with the Issuer CSD. Alternatively, the in-vestor may also hold fund shares or via an Investor CSD (which connects to the Issuer CSD via a CSD link arrangement).

The CSD of the investor authorises and/or controls all orders and transfers issued by its participants, and reconciles its records with statements transmit-ted by the issuing agent (issuing agent set-up) or issuer CSD (issuer CSD set-up ).

AML/KYC checks on the investor CSDs are done by issuer CSD, issuing agent or by TA provided this is arranged for in the CSD link arrangement. For reasons of transparency the Investors CSD in most cases could provide disclosure reporting to the fund manager of underlying holdings and transactions, either directly or indirectly through the issuer CSD, provided this is agreed with the fund manager (i.e. the issuer for these securities).

The following section covers all questions the work-ing group identified as being relevant for the fund issuance in T2S. A side aspect is the order routing, which we did also capture to provide a holistic picture of the opportunities T2S will bring to the investment fund industry.

1. What makes primary market funds special?

Most of securities are issued in the primary market through an IPO, and then continue their existence mostly on the secondary market where settlement is relatively simple. The primary market for invest-ment funds remains open. Most funds have a “daily IPO” and the constantly changing number of issued shares leads to special requirements in transaction handling, record keeping and reconciliation when comparing with other securities.

2. Who are the key stakeholders for fund issuance in T2S and what tasks do they perform?

a) Investor

There are multiple type of investors in investment funds e.g.:

• A retail investor;• An institutional investor, e.g. a pension fund,

some other fund of funds, a distributor, an insurance company;

• A nominee, e.g. an investor’s custodian bank.

Those investors may settle directly or indirectly in T2S or with the TA appointed by the Fund. To settle in a CSD in T2S an institutional or a retail investor needs to open a securities account in a CSD in T2S (either in the issuer CSD for this security or in an Investor CSD for the respective security). Direct connectivity to T2S (e.g. for sending of instructions and receiving confirmations) is only available for investors, which have reached an agreement for this with their CSD and have the necessary technical capacity.

6 For further information on segregated vs pooled safekeeping, please see http://ecsda.eu/archives/47597 Issuer or Investor CSDs.

I. fund issuance in T2S

9

of shares in circulation sits with the TA. The issuing agent opens one or more issuance accounts in the issuer CSD on behalf of the investment fund. The notary function is performed by the CSD. Depend-ing on the future operating model of an asset man-ager there may be multiple issuer CSDs and issuing agents connected to multiple investor CSDs.

The issuing agent shall obtain timely information whenever the TA has updated a position on the TA register following the execution of orders, transfers and corporate actions. The issuing agent is required to transmit settlement instructions to the issuer CSD, reflecting all such register account updates, without undue delay.

The issuing agent is responsible for monitoring the successful settlement on its issuance account with the issuer CSD and reconciliation of shares with TA, and to help resolve any failures.Depending on the situation and preferences of the stakeholders, the issuing agent role can be assigned to a local agent, a paying agent or the TA, by the fund manager.

e) TA

For each investment fund, the fund manager must appoint a Transfer Agent (TA) to keep the register of all shareholders, within and outside of T2S. The TA shall validate and execute the subscriptions, re-demptions, switches, transfers and corporate actions on the register accounts that result in the mark-up/mark-down of shares owned by the account holder in fund register.In the context of T2S the account holder in the fund register may be either the issuing agent or issuer CSD depending on the chosen set-up. The TA must provide the owner with timely information of all relevant updates in the register.

Reports that the TA produces include sums of registered and issued shares for the fund manager and fund accountant, account statements for register account holders and distributors, and regulatory reporting.

The TA performs AML/KYC checks on the register account owner.

CSD, when acting in their Issuer CSD role provides a neutral and scalable infrastructure for primary market settlement (also known as issuance settle-ment) and ensures the integrity of the issued securi-ties. Like for the investor CSD role the issuer CSD will also offer multiple ancillary services tailored for investment funds, such as order routing, asset servicing, reconciliation and reporting of trade dated holdings.T2S CSDs maintain CSD omnibus (pooled) accounts of each investor CSD holding shares of the invest-ment fund and maintains the issuance account on behalf of the issuing agent.

The CSD which acts as Issuer CSD for a given fund share ISIN, obtains timely information (directly from TA or from issuing agent) whenever the TA has updated a position on the TA register following the execution of orders, transfers and corporate actions. Upon entry of issuing agent’s settlement instructions into the CSD, by the CSD will execute those instruc-tions into the CSD, without undue delay.Settlement related to corporate actions is processed by the CSD based on the confirmations of corporate actions that are transmitted by the TA.

The issuer CSD may also be the Securities Main-taining Entity (SME – covered under question 10), i.e. being responsible for creating and maintaining securities reference data in T2S. T2S system speci-fications demands that each ISIN has a single CSD fulfilling role of SME.

AML/KYC checks on the investor CSDs are per-formed by the issuer CSD. For reasons of trans-parency and disclosure the issuer CSD may offer a reporting of holdings and transactions to the fund manager. The reporting will either be on the level of the issuer CSD, or incorporate also the investor CSD’s level, depending on the individual arrange-ment of the issuer CSD with the linked investor CSDs.

d) Issuing agent

The issuing agent is an institution selected by the fund manager to manage issuance of shares and oversee settlement through T2S. The global amount

10

Therefore we developed within the group three pos-sible issuance models which can be seen as evolution over time of the below Model 1 (current model). It is already clear today that the competition in the CSD space will accelerate dramatically through T2S for the benefit of other market participants, as settle-ment rates will decrease and services increase.

3. How T2S connects key stakeholders and what are most common models?

As T2S is one central settlement platform the next possible downstream harmonisation level hits the CSDs. Considering there are more then 20 nation-al CSDs in Europe there is a lot of potential for harmonisation. It is unlikely that this harmonisation happens quickly.

Model 1 - Pre T2S CSD model (no change after migration onto T2S)

• All investor CSDs are also issuer CSDs for the ISINs issued in their books

• Current operating model is maintained whereby CSD continue to operate in silos.

• No cross border links between the different CSDs.

• Multiple issuer CSDs need to be maintained by the fund managers

• This model is expected to prevail until both Euroclear France and Clearstream Frankfurt joined T2S

Investor CSD/ Issuer CSD 1

(EuroclearFrance)

Investor CSD/ Issuer CSD 2 (Clearstream

Frankfurt)

TA Account 1 TA Account 2

Order routing & Settlement Instructions Order routing & Settlement Instructions

No Link

I. fund issuance in T2S

11

• Investor CSDs will hold their positions with the issuer CSD

• Only one issuer CSD needs to be maintained by the fund managers

T2S

TA Account 1 TA Account 2

Order routing & Settlement Instructions

Investor CSD 1(Euroclear France)

Investor CSD 2(ClearstreamFrankfurt)

Issuer CSD 1(Euroclear France)

Issuer CSD 2 (Clearstream

Frankfurt)

Order routing & Settlement Instructions

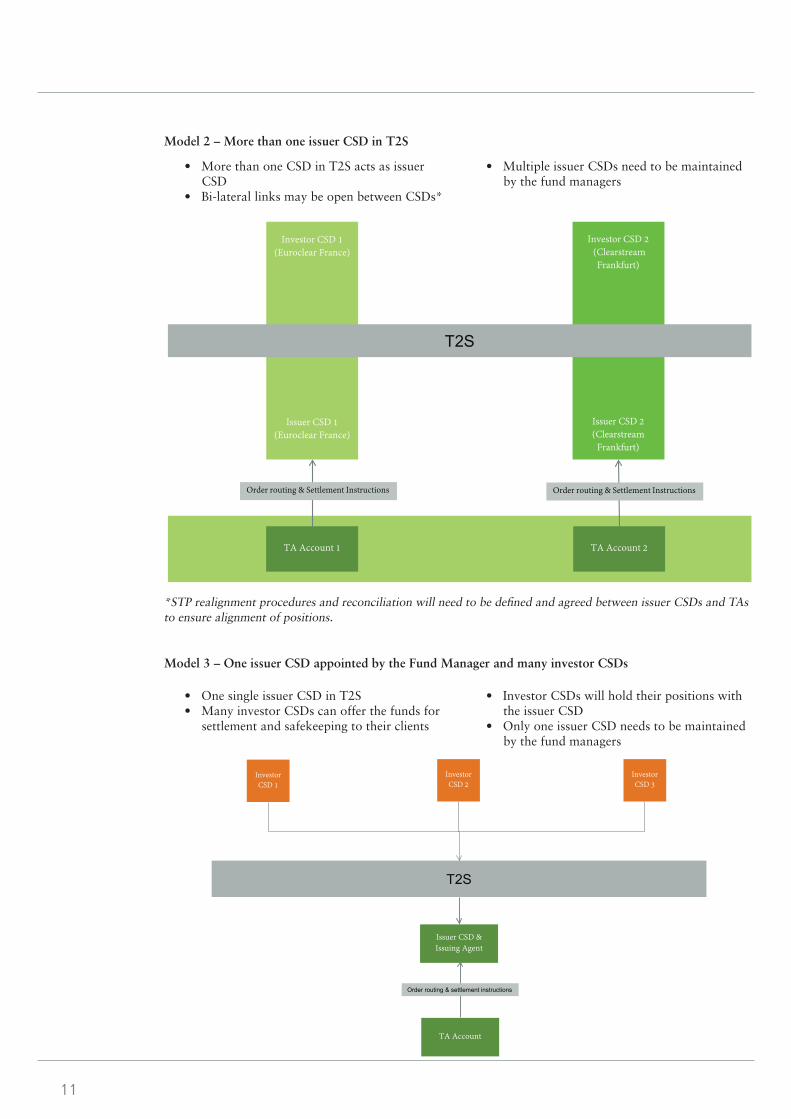

Model 2 – More than one issuer CSD in T2S

• More than one CSD in T2S acts as issuer CSD

• Bi-lateral links may be open between CSDs*

• Multiple issuer CSDs need to be maintained by the fund managers

*STP realignment procedures and reconciliation will need to be defined and agreed between issuer CSDs and TAs to ensure alignment of positions.

Model 3 – One issuer CSD appointed by the Fund Manager and many investor CSDs

• One single issuer CSD in T2S• Many investor CSDs can offer the funds for

settlement and safekeeping to their clients

T2S

TA Account

Issuer CSD & Issuing Agent

Order routing & settlement instructions

InvestorCSD 1

InvestorCSD 3

InvestorCSD 2

12

Hence the single final model is not possible to pre-dict. Nevertheless the two most commonly discussed future T2S set-ups for investment funds, which can be operated as Model 2 or Model 3 are as follow and they evolved from the current models operated in France and Germany.

Issuing agent set-up

Models 2 and 3 allow for flexibility in terms of set-up depending if:

1. Account segregation takes place or if the assets will be pooled;

2. An issuing agent will be used, which does not belong to the CSD;

3. The ordering is done via the proprietary CSD solution or via a third party, be it the issuing agent or another vendor.

In this set-up8:

• The fund manager appoints the issuing agent • The order (subscription, redemption) is sent

by the investor, either directly or through the chosen investor CSD, to the issuing agent

• The issuing agent holds an account at the TA • Is the register of all fund shareholders for

shares issued/to be issued through T2SThe issuing agent open a settlement account with the issuer CSD also appointed by the fund manager.

I. fund issuance in T2S

Delivery vs Payment (DVP) Settlement

instruction

Delivery vs Payment (DVP) Settlement

instruction

Order marking

Issuing Agent / Fund Sub-Issuing Account

Issuing Agent register

Order Routing/ExecutionInvestor1

Investor2

Investor1 Acct Investor CSD 1

Issuer CSD

Issuing Agent

TA

Investor2’s Bank Acct Investor CSD 2

Investor2’s Bank

Investor CSD 1 Account

Investor CSD 2 Account

Investor3 Acct Investor CSD 3 Investor CSD 3 Account

Investor3 Investor CSD 3

Issuance/Settlement

8 An Issuing agent can receive an order also from the participants in the issuer CSD. Issuance of securities can happen also directly on accounts of participants of the issuer CSD (does not have to be only on investor CSD accounts at the issuer CSD).

13

Issuer CSD set-up

In this set-up9:

• The Fund appoints the issuer CSD • The order (subscriptions, redemptions) is sent

by the investor, either directly or through the chosen investor CSD, to the issuer CSD

• The issuer CSD holds an account at the TA • The issuer CSD is the register of all fund

shareholders for shares issued/to be issued through T2S

• The issuer CSD opens a settlement account with the TA also appointed by the fund manager

4. In which security forms are invest-ment funds issued?

Investment funds are generally issued in units of shares, unlike debt instruments that are issued in nominal amounts. Luxembourg domiciled funds are mostly issued in registered form. Each Fund requires a TA that maintains a register of shareholders and their individual holdings.

Some CSDs who opened an pooled account with the TA would also keep the registered form of fund shares issued to its participants. However, when issued in domestic CSDs the shares may have to change form depending on national legislation.

Notable examples are the dematerialised bearer shares in France, and the global certificates for col-lective safe custody in Germany. It is still the TA that confirms validity of shares, whether in bearer or registered form.

Luxembourg’s Law of Dematerialisation (6 April 2013) presents an option for the form of issuance of shares. The law changes the place of available balances of shares from the TA to a securities set-tlement system (e.g. a CSD or ICSD), but it doesn’t change the date of entitlement: the trade date, which is normally the date when a price per share (NAV) is applied to an order. This form is also suitable for T2S settlement.

5. When are shares created in T2S – at trade date or settlement date? Is it different per CSD?

Under Luxembourg Law, changes in the entitlement of fund shares are established by the TA whenever the register of shareholders is updated. It is com-monly referred to as the trade date. Such updates are then followed by the creation/cancellation of shares in the issuer CSD on a contractual settlement date.

Delivery vs Payment (DVP) Settlement

instruction

Issuing Agent/Fund Sub-Issuing Account

Issuer CSD register

Investor1 Acct Investor CSD 1

Issuer CSD

TA

Investor2’s Bank Acct Investor CSD 2

Investor CSD 1 Account

Investor CSD 2 Account

Investor3 Acct Investor CSD 3 Investor CSD 3 Account

Issuer CSD

Investor1 Acct Investor CSD 1

Investor2’s Bank Acct Investor CSD 2

Investor3 Acct Investor CSD 3

Order marking

Order Routing/Execution

Issuance/Settlement

Delivery vs Payment (DVP) Settlement

instruction

9 An Issuer CSD can receive an order also directly from the banks of an investor if they are participants in that issuer CSD.Issuance of securities can happen also directly on accounts of participants of the Issuer CSD (does not have to be only on Inves-tor CSD accounts at the issuer CSD).

14

However, T2S allows the investment funds to benefit from the security of DVP settlement and the credit facilities provided with the National Central Banks (NCBs). When there are extended intermediary chains including linked CSDs, the added risk has to do with transparency. The parties involved in invest-ment funds orders with settlement in T2S need to manage the risk of settlement failures based on their own contractual obligations.

8. What are the responsibilities of the order router?

Any stakeholder involved in the order routing chain may need to ensure that any relevant related party information, also known as order marking, is pre-served throughout the order chain and reaches the TA.

Some parties in the order routing chain (investor, in-vestor CSD, any intermediary between those parties, issuer CSD, issuing agent etc.) may have to perform provision checking (e.g. positioning of shares (in case of redemptions), check of minimum subscrip-tion amounts, computation of the expected settle-ment date) before forwarding an order downstream to the TA. Without provision checking there is the risk of settlement failure which needs to be avoided to have an efficient order flow.

9. How can a fraction of a share be important?

Investment funds are often issued in quantities that have one or more decimal digits, e.g. so the TA can fill cash amount orders as accurately as possible. The maximum decimal precision of shares is commonly set between 0 and 6 digits, as defined in the prospec-tus. A prerequisite for any investor CSD to accept an investment fund is that it has systems and processes in place to manage the required decimal precision of fractional units, so that that it can reconcile its books with the omnibus account at the linked CSD, for example the issuer CSD.

10. What is the concept of SME?

Luxembourg funds issued in a CSD will have had to provide the CSD with some static data, such as ISIN, name and so forth. With T2S a list of Securities.

Maintenance Data is to be maintained by the CSD bringing the (Luxembourg) fund into T2S.

In case the settlement date is one or more days after the trade date, the payer (investor for subscriptions, fund manager for redemptions) is effectively given credit by the receiver (fund manager for subscrip-tions, investor for redemptions). All parties involved in a transaction are contractually bound (by the prospectus and governing principles of each account servicer) to finalise its settlement.

6. What types of transactions involve updates of the TA’s register?

• Subscription – the investor pays into the fund and new shares are issued;

• Redemption – the investor delivers shares to be cancelled and receives cash in return;

• Switch – the investor delivers shares to be cancelled and receives newly issued shares of a different class;

• Transfer – a movement in the custody chains between two registered owners;

• Reinvestment – income distributed as units of shares;

• Corporate actions – any action that affect holdings, e.g. distribution payments, mergers, liquidations, splits.

7. What is the T2S impact on the settlement risk of subscription and redemption orders?

An investor enters into a contract with the fund manager or one of its intermediaries (e.g. investor CSD) to execute and settle the order once it has been executed. The fund manager shall receive payment for subscriptions and the TA will perform reconcili-ation on the bank accounts designated for collection of subscription money (those accounts typically will be opened with any bank or credit institution in the name of the TA or the fund). Redemptions will be paid to Investor by the fund, through its TA, usually being the party to initiate payments on the accounts opened with the same bank as the subscription ac-counts. In case of T2S subscription money would hit the fund collection accounts via the issuer CSD and redemption payments would be paid by the fund also via the issuer CSD.

The risk of settlement failure in a CSD has not fundamentally changed with T2S. For the payment chains, there is a risk with the solvency of all stake-holders including the intermediaries to perform the settlement of subscriptions and redemptions.

I. fund issuance in T2S

15

Finally, the Eurosystem may accept to act as SME for a given security upon request by all participating CSDs. This exceptional role assignment shall only be applied in abnormal situations and the Eurosystem will not accept any liability in connection with its function as SME. In a nutshell, a SME ensures timely creation and maintenance of reference data for securities in T2S whilst mitigating costs and risks for all CSDs and with a high control level.

11. What are the obligation of a SME?

The SME role entails various obligations for a CSD against the Eurosystem and other participating CSDs. A summary of obligations according to the Framework Agreement has been collated in the following table for easy reference.

The ‘Securities Maintaining Entity (SME)’ is defined as an entity, typically an issuer CSD, which has been assigned the responsibility for maintaining the refer-ence data for a security in T2S.

In general the CSD issuing a security is obliged to act in the SME role. Therefore, each participating CSD will be expected to maintain reference data in T2S for securities issued in its own market similar to the current procedures.Additionally, a participating CSD may be assigned the SME role for a particular security for which it is not the issuer CSD. All participating CSDs will need to have mandated it to take over the SME role for this security. This scenario would apply frequently if the actual issuer CSD is not part of T2S. For ex-ample, a T2S investor CSD will need to be the SME for a security issued in the US but will be eligible for settlement in T2S.

Obligations Description

Creation Timeliness The SME is responsible to create reference data in a timely manner once a security is required for settlement

Maintenance Continuation The SME is responsible for the continuous maintenance of securities ref-erence data once it has created a security [until the security is deleted or it has been agreed with other participating CSDs that the SME role is to be transferred to another CSD]

Correction Timeliness The SME is responsible for correction of any errors or omissions within two hours once aware of this fact

Securities Reference Data Rights

The SME is responsible for obtaining all authorisations, permits and licences to make available securities reference data in T2S

Infringement of Third Party Rights

The SME is responsible for reimbursement of all payments that the Eurosys-tem has to make to a third party due to an enforceable judgement related to the securities reference data introduced by the SME into T2S

SME Role Reassignment The SME is responsible to agree with another participating CSD to take over the SME role for a security and to inform Eurosystem in writing about the envisage change in case that T2S shall reassign the responsibility on an exceptional basis

Liability The SME is liable for any errors or omissions in the reference data and responsible for settling any potential claims between the participating CSDs without involvement of the Eurosystem

12. What are the data in scope of a SME ?

The SME is exclusively responsible for the creation

and maintenance of four out of eleven data entities within the securities data management domain.

Securities Data Management

SME CSDs (incl. SME) NCBs and Payment Banks

• Securities• Securities Code• Securities Name• Deviating Settlement Unit

• Market-Specific • Security Attribute Value• Security CSD Link• Security Restriction

• Close Link• Securities Valuation• Securities Valuation Party• Security Auto-collateralisa-

tion Eligibility

16

2. Security CSD link creation (via A2A message or T2S GUI) where the CSD A:

- Defines the type of link. Here it will be ‘Issuer’ type

- Defines whether the CSD A is the SME for this ISIN, e.g. set the SME flag to ‘True’

- Optionally assigns Issuance account(s) to the ISIN

14. What is the issue?

T2S can only assign a single SME per securities whereas multiples CSDs may have a holding and ac-cess to information (and updates). T2S favors setting a single SME per market, yet T2S can set SME per ISIN.

The T2S application is not in a position to check that a CSD is allowed to create a given security and that it should be the SME for that security, i.e. it is technically not possible for T2S to validate whether the CSD who is attempting to assign itself the SME role in T2S, is the actual issuer of the security which may create issues in terms of allocation and mainte-nance of existing security and new security.

15. What are the possible scenarios?

1. The Fund can be issued onto any CSD

The Fund can decide to be issued onto a CSD. Such decision will necessitate the delivery of one set of in-formation the CSD will require is the Static Data set laid out by the T2S-CSD relation. This is the Secu-rities Maintenance Data and the CSD is responsible for the correctness of that information is the SME.

The CSD chosen by the Fund can now be the Issuing CSD and Securities Maintenance Entity, it can enter the Fund in T2S and it can facilitate settling the Fund in another T2S connected CSD. This SME CSD has the ultimate responsibility on the Securities Maintenance Data vis-à-vis the T2S system.

Since the Fund, through its Issuing CSD can aliment all T2S connected CSDs there would be little reason to issue again, in parallel through another CSD. Such reasons might however, emerge and may have to do with features CSD will compete on.

2. The Fund was issued onto a single CSD

When this CSD migrates onto T2S it will become the Issuing CSD for the Fund, and SME. The CSD in question will thus become responsible for the SME relevant data. Wrong SME data may cause errors in the T2S Settlement process.

The four data entities to be maintained encompass attributes per security in total. These data attributes are elementary for processing of settlement instruc-tions in T2S.

• Mandatory attributes - ISIN - CFI codes (classification of financial

instruments) - Short name - Long name - Issue date - Settlement type - Minimum settlement unit - Settlement unit multiple - Country of issuance - Currency

• Optional attributes - Maturity/expiry date - Deviating settlement units

• Market specific attributes - CSDs can independently set up market

specific attributes for any ISIN to steer T2S settlement-processing for their own specific validations. Furthermore, neither an Issuer CSD nor Investor CSD can view MSAs created by the other one

- Market specific attributes are not reported to T2S CSD participants via the T2S platform

- In case customer impact is expected CSDs will publish details regarding MSA

13. What is the process for creation of a security and assignment of SME role?

The SME is not defined at the creation of the secu-rity in T2S, but when a CSD creates a security CSD link record for itself and flags that it is the SME.For example, CSD A (in T2S) which the issuer CSD for ISIN A, will perform the following activities to create the security and assigns itself as SME for the security:

1. Security Creation where the CSD A: - Creates master reference data attri-

butes - Optionally assigns Intra-day restric-

tion(s) and Market Specific At-tribute(s) for its market

I. fund issuance in T2S

17

When Euroclear France migrates to T2S as well as Clearstream Germany a number of fund managers will be faced with the scenario that they have two entry points in T2S, as their two Issuing CSDs will have entered the investment funds on T2S. The current working assumption is that the CSD first migrating to T2S and pulling the investment funds in issue with it will be the SME CSD.

16. What is the operating model and pro’s and con’s?

Each issuer will be responsible to deliver the relevant data to the issuer CSD(s) and each issuer CSD will be responsible to deliver this information to T2S as per the diagram below.

As under point 1 when the Fund migrates onto T2S together with its CSD it will be able to aliment the other CSDs through settlement over the T2S plat-form. We in effect will have Model 3.

As in some cases the Fund automatically migrates onto T2S (depending on the policy of the CSD in question there will be an explicit request) there is a potential for discord in case the Fund actively decides to want to use another issuance CSD.

3. The Fund was issued onto more than one CSD

Since Germany and France have been much favored target countries for many cross border distributing Funds in Luxembourg, such Funds will likely have landed in the French and German CSD.

• Pro’s - SME model in line with issuance

process - Oblige issuer to provide accurate static

data - Contractual framework already in

place - Interface already or currently being

developed

• Con’s: - Spaghetti model may lead to confusion

on who is doing what in the context of a multiple issuer CSD model

- No centralisation and standardisation of fund static data

- Multiple flows to be setup between issuer and CSDs, and between CSD and T2S

- Revenue model: no specific remunera-tion for CSD

- Limited scope of data

17. Is there an opportunity to cen-tralise this information and what would be the pro’s and con’s?

There is certainly opportunities to gain efficiencies by appointing central data repositories to manage the transmission of static data from the issuers to the CSDs but also from the CSDs to T2S as per the below chart.

Issuer CSD 2 T2SIssuer 1

Issuer CSD 1 – SME for issuer 1

Issuer CSD 3 – SME for issuer 2Issuer 2

Static data 1

Static data 2

Static data 1

Static data 2

Issuer CSD 2 T2S

Issuer 1

Issuer CSD 1 – SME for issuer 1

Issuer CSD 3 – SME for issuer 2

Issuer 2

Static data 1

Static data 2

Static data 1

Static data 2

Provider

18

There are no obligation today to follow this model and will be based on commercial decision from the issuer and the CSD to adopt this model.

18. Cash handing for investment funds in T2S

The T2S framework requires settlement of trans-actions be performed using central bank money. Clearstream Germany, Euroclear France, Lux CSD and VP LUX, for Luxembourg domiciled fund share trading activities, are all using central bank money today.

Within the T2S infrastructure, ‘payment banks’ is the term used to define entities which hold cash ac-counts with the country specific NCB. By definition these will be entities which meet the European Sys-tem Central Bank (ESCB) requirements. The ESCB has agreed fixed fees that will be applied in each NCB for the management of T2 cash accounts and settlement of trades within T2S. In addition there are separate fees for the liquidity transfers between T2 and T2S.

Asset managers, TAs, distributors and other non NCB account holders will continue to deal in com-mercial bank money and may experience changes in their payment cut-off times, plus credit facilities, linked to Euro settlement of fund shares traded within T2S. Some of these changes would have already happened as a consequence of the dealing in existing Euro denominated securities within the CSDs.

With the expanded use of CSDs to support fund share distribution and associated cash settlement processes, this should trigger a review of existing central bank account rationalisation by payment banks. The new T2S framework should provide the ability to improve cash management from the payment bank perspective, one dedicated cash ac-count (DCA) with one NCB is sufficient to cover all security accounts in T2S.

Fund managers, investors and distributors should also review their commercial bank arrangements to determine if it is possible to transition to a single Euro cash account to settle all euro denominated trades within T2S.

CSDs will only have a direct cash account rela-tionship with NCBs to support corporate actions activity.

The T2S harmonisation focused efforts lead to a convention of settling on a T+2 cycle which took effect in October 2014 as a precursor to the imple-mentation of T2S. This will not be mandatory for the fund investor share dealing with the exception of Exchange Traded Funds (ETF). Where a fund predominantly holds Euro denominated assets which will settle on a T+2 cycle and the asset manager elects to retain the investor trades on a T+3 or longer settlement period, the asset manager will be responsible for effective cash management to meet country specific liquidity regulations based on the fund structure.

All these topics will be reviewed in more detail in the following Q and A section.

19. What does the term ‘payment banks’ refer to within the T2S infra-structure?

The term is used to define entities which hold cash accounts with the country specific National Central Bank (NCB). By definition these will be entities which meet the European System Central Bank (ESCB) requirements. The ESCB has agreed fixed fees that will be applied in each NCB for the man-agement of cash accounts and settlement of trades within T2S.

I. fund issuance in T2S

19

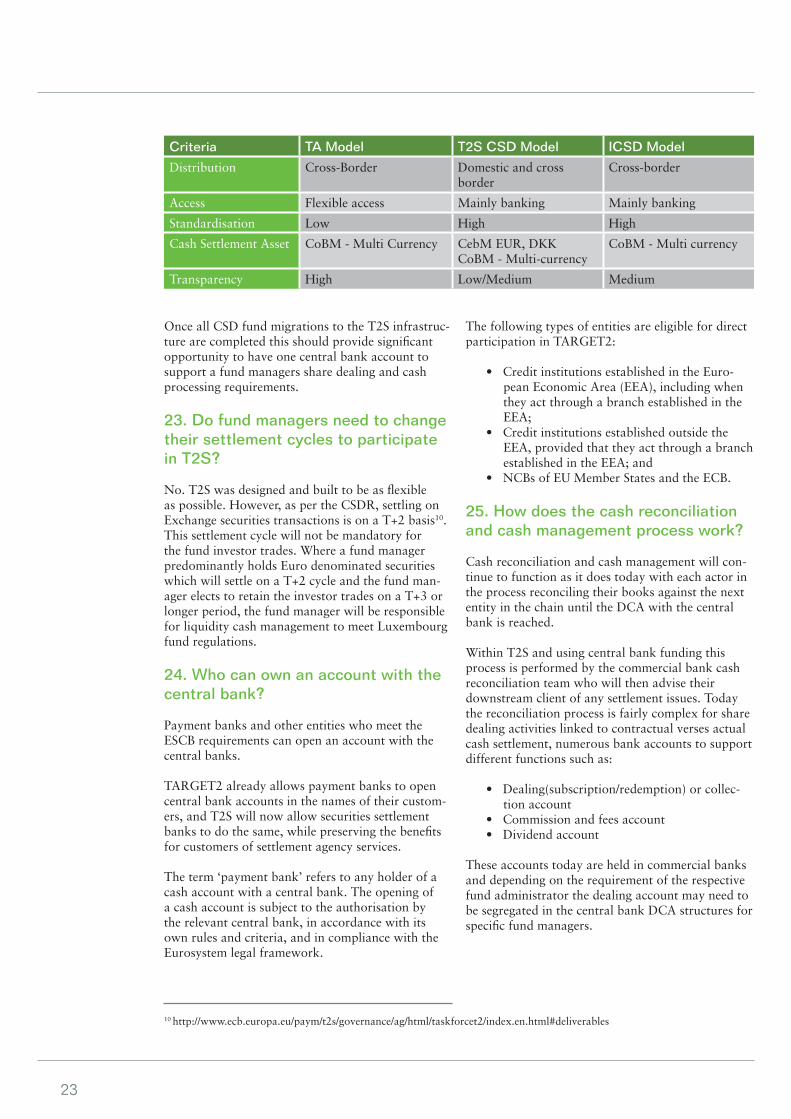

The fee will be the same for all central banks partici-pating in T2 and T2S.It is up to each payment bank that has a relationship with one or more central banks to determine what segregation level is required, based on the level of access and reporting needed by respective clients and open the applicable number of DCAs. A single DCA is sufficient to support the delivery verses payment process across multiple securities accounts with multiple CSDs.

Another key benefit from T2S will be a significant reduction of securities settlement fees in Europe, in particular for cross-border transactions. With the existing fragmentation of settlement over a multi-tude of platforms run by different CSDs, settling across borders today still costs many times more than settling within the same country.Cross-border and domestic transactions will be processed in the same way and therefore at the same price within T2S.

With the economies of scale that come from con-solidating cash and share settlement volumes from many platforms onto a single platform, T2S will allow substantial reduction of the settlement fee in Europe. This represents a significant potential bene-fit for investment funds.

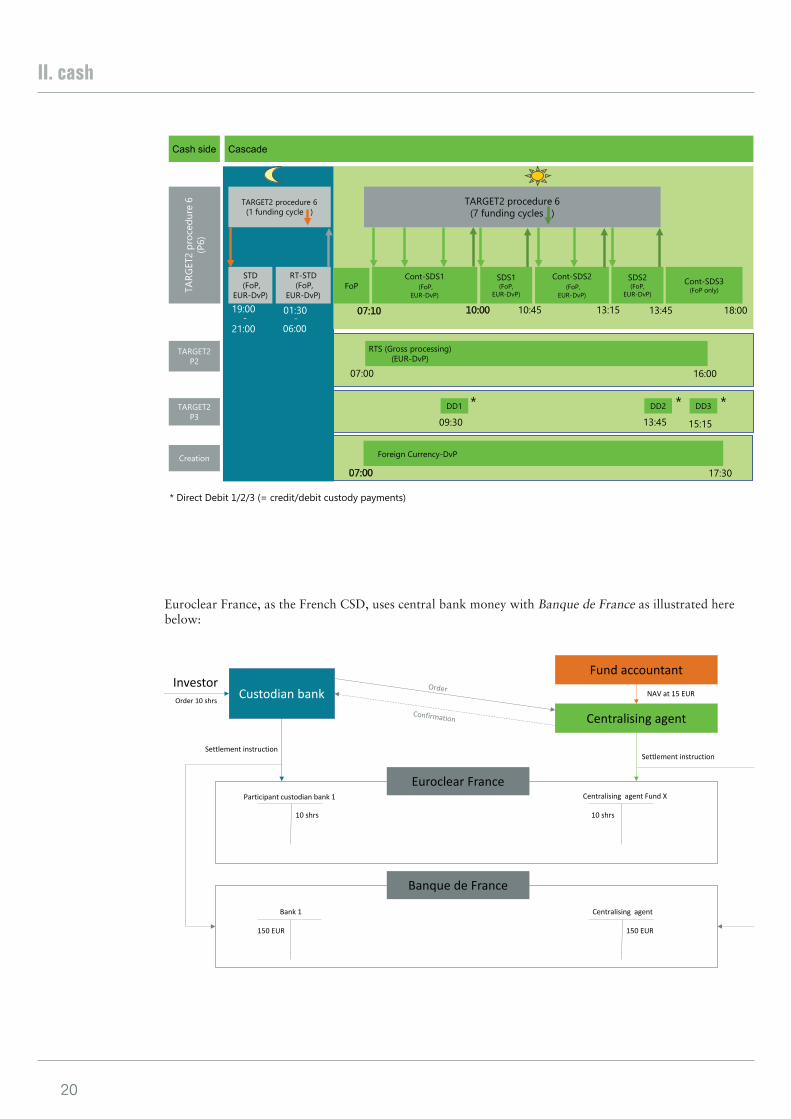

22. Do you use Target 2 central bank money today and how will the process change with the move to T2S?

Where Luxembourg domiciled funds are eligible in Clearstream Germany, Euroclear France, LuxCSD and VP LUX, these platforms all use central bank money today for settling Euro denominated trans-actions. Below are the current models adopted by the respective CSDs to support the cash settlement activities with the respective NCB.

Clearstream Bank Germany performs settlement in central bank money through the ASI procedures which allows the use of accounts in TARGET2 held with any Eurozone central bank.

20. What is the difference between central bank and commercial bank money?

Central bank money is a claim on a central bank whereas commercial bank money is a claim on a commercial bank.

Central bank money is generally completely safe in its jurisdiction as it is normally connected to the government of a country, whereby commercial bank money is only connected to the financial health of the respective commercial bank. A central bank can e.g. always cover their obligations by issuing their own currency.

The settlement in commercial bank money is often considered as permitting more flexibility than the settlement in central bank money.

Both central bank and commercial bank money play an important part in facilitating economic activity. The most effective and efficient financial system is one in which there is competition among banks and in which central bank money is used where its particular features are most important.

Central bank money can be perceived as an added value in terms of security and safety for financial transactions. However, some institutions argue that the use of central bank money or commercial bank money does not make a big difference for their own business.

21. What are the costs of using central bank money today? Will this change with T2S?

T2S requires the usage of a DCA (dedicated cash account) for settlement in central bank money. The monthly fee to hold a DCA is EUR 250 and is charged to the main PM account holder who may be a different entity from the DCA account owner. This fee will be adjusted over time in order to ensure the cost recovery for the Eurosystem.

II. cash

20

19:00 01:30

07:00

13:1510:00

STD(FoP,

EUR-DvP)

RT-STD(FoP,

EUR-DvP)

TARGET2 procedure 6(1 funding cycle )

Cont-SDS1(FoP,

EUR-DvP)

TARG

ET2

proc

edur

e 6

(P6)

Cont-SDS2(FoP,

EUR-DvP)

TARGET2 procedure 6 (7 funding cycles )

09:30

16:00

18:00

DD2DD1

SDS1(FoP,

EUR-DvP)

SDS2(FoP,

EUR-DvP)

TARGET2 P2

TARGET2P3

Cont-SDS3(FoP only)FoP

RTS (Gross processing) (EUR-DvP)

17:30

Cash side Cascade

21:00-

Foreign Currency-DvPCreation

07:10

07:00

-06:00

10:45 13:45

* *

* Direct Debit 1/2/3 (= credit/debit custody payments)

13:45DD3

15:15

*

Custodian bank

Fund accountant

Centralising agent

Euroclear France

Banque de France

InvestorOrder 10 shrs

Settlement instructionSettlement instruction

Participant custodian bank 1 Centralising agent Fund X

10 shrs 10 shrs

NAV at 15 EUR

Bank 1 Centralising agent

150 EUR 150 EUR

Euroclear France, as the French CSD, uses central bank money with Banque de France as illustrated here below:

II. cash

21

VP LUX performs settlement in central bank money as described below:

Custodian BankInvestor

Order 10 SHS

Issuing Agent (is or appointed by /Fund) TA

Fund Accountant

VP LUX

Investor

order

confirmation

Custodian Bank’s nostro in Central Bank Issuing Agent’s Bank’s nostro in Central Bank

NAV 15 EUR

Settlement instructionSettlement instruction

Participating Custodian Bank

10 SHS

Issuing Agent

10 SHS

150 EUR150 EUR

CENTRAL BANK

Settlement instruction

Current

LuxCSD performs settlement in central bank money through the ASI procedure 6 which allows the use of accounts in TARGET2 held with any Eurozone central bank.

Source: LuxCSD Customer Handbook

End of Day Reports

End of Day Processing

Instruction Pre-Matching and Settlement Information

00:00 6:00 07:15 8:00 12:00 17:00 18:00 20:00 20:35

Creation* Continuous Settlement Processing

Customers

21:30 9:00 10:00 11:00 13:00 14:00 15:00 16:00

TARGET2 / BCL

DVP/ RVP/FOP

LuxCSD

*operated by CBL

Mandatory & Optional Settlement Period (13:40/14:50/14:55 provisioning end times)

Optional Settlement Period(16:40 / 17:50 / 20:35 provisioning end times)

19:00

ASI Night-time / Daylight Procedure 6 Interface for EUR CeBM settlements (last cash provisioning cycle for CeBM settlement is triggered at 16:00)

22

Custodian BankInvestor

Order 10 SHS

Issuing Agent (is or appointed by /Fund) TA

Fund Accountant

VP LUXVP SECURITIES or otherconnected T2S CSD

Central Bank Account available to CUSTODIAN BANK

Central Bank Account available to ISSUING AGENT

Investor

order

confirmation

Custodian Bank’s dedicated cash account with T2SVia transfer from TARGET2 RTGS account

Issuing Agent’s Bank’s dedicated cash account with T2STo be transfered back to TARGET2 RTGS account

NAV 15 EUR

Settlement instructionSettlement instruction

Participating Custodian Bank

10 SHS

Issuing Agent

10 SHS

150 EUR150 EUR

T2S

The future holistic model for fund share dealing and the associated cash processing could be represented as in the below diagrams:

Local Bank Transfer Agent

TA/Fund PM accountOrder Originator CSD PM

accountDirect or indirect

Register

Account 1Local agent

…

Order confirmation

Order

Recording

DVPRVP

Local Fund Agent CSD securities account

Order originator CSD securities account

DVP Settlement

CSD

NCB

Local Fund agent

Order confirmation

Order

Issuance

Investors

OrderOrder

confirmation

Order originatorCash correspondent bank

TA/Fund cash correspondent bank

Cash payment

Funding Credit confirmation

Cash reporting

II. cash

23

The following types of entities are eligible for direct participation in TARGET2:

• Credit institutions established in the Euro-pean Economic Area (EEA), including when they act through a branch established in the EEA;

• Credit institutions established outside the EEA, provided that they act through a branch established in the EEA; and

• NCBs of EU Member States and the ECB.

25. How does the cash reconciliation and cash management process work?

Cash reconciliation and cash management will con-tinue to function as it does today with each actor in the process reconciling their books against the next entity in the chain until the DCA with the central bank is reached.

Within T2S and using central bank funding this process is performed by the commercial bank cash reconciliation team who will then advise their downstream client of any settlement issues. Today the reconciliation process is fairly complex for share dealing activities linked to contractual verses actual cash settlement, numerous bank accounts to support different functions such as:

• Dealing(subscription/redemption) or collec-tion account

• Commission and fees account• Dividend account

These accounts today are held in commercial banks and depending on the requirement of the respective fund administrator the dealing account may need to be segregated in the central bank DCA structures for specific fund managers.

Criteria TA Model T2S CSD Model ICSD Model

Distribution Cross-Border Domestic and cross border

Cross-border

Access Flexible access Mainly banking Mainly banking

Standardisation Low High High

Cash Settlement Asset CoBM - Multi Currency CebM EUR, DKKCoBM - Multi-currency

CoBM - Multi currency

Transparency High Low/Medium Medium

Once all CSD fund migrations to the T2S infrastruc-ture are completed this should provide significant opportunity to have one central bank account to support a fund managers share dealing and cash processing requirements.

23. Do fund managers need to change their settlement cycles to participate in T2S?

No. T2S was designed and built to be as flexible as possible. However, as per the CSDR, settling on Exchange securities transactions is on a T+2 basis10. This settlement cycle will not be mandatory for the fund investor trades. Where a fund manager predominantly holds Euro denominated securities which will settle on a T+2 cycle and the fund man-ager elects to retain the investor trades on a T+3 or longer period, the fund manager will be responsible for liquidity cash management to meet Luxembourg fund regulations.

24. Who can own an account with the central bank?

Payment banks and other entities who meet the ESCB requirements can open an account with the central banks.

TARGET2 already allows payment banks to open central bank accounts in the names of their custom-ers, and T2S will now allow securities settlement banks to do the same, while preserving the benefits for customers of settlement agency services.

The term ‘payment bank’ refers to any holder of a cash account with a central bank. The opening of a cash account is subject to the authorisation by the relevant central bank, in accordance with its own rules and criteria, and in compliance with the Eurosystem legal framework.

10 http://www.ecb.europa.eu/paym/t2s/governance/ag/html/taskforcet2/index.en.html#deliverables

24

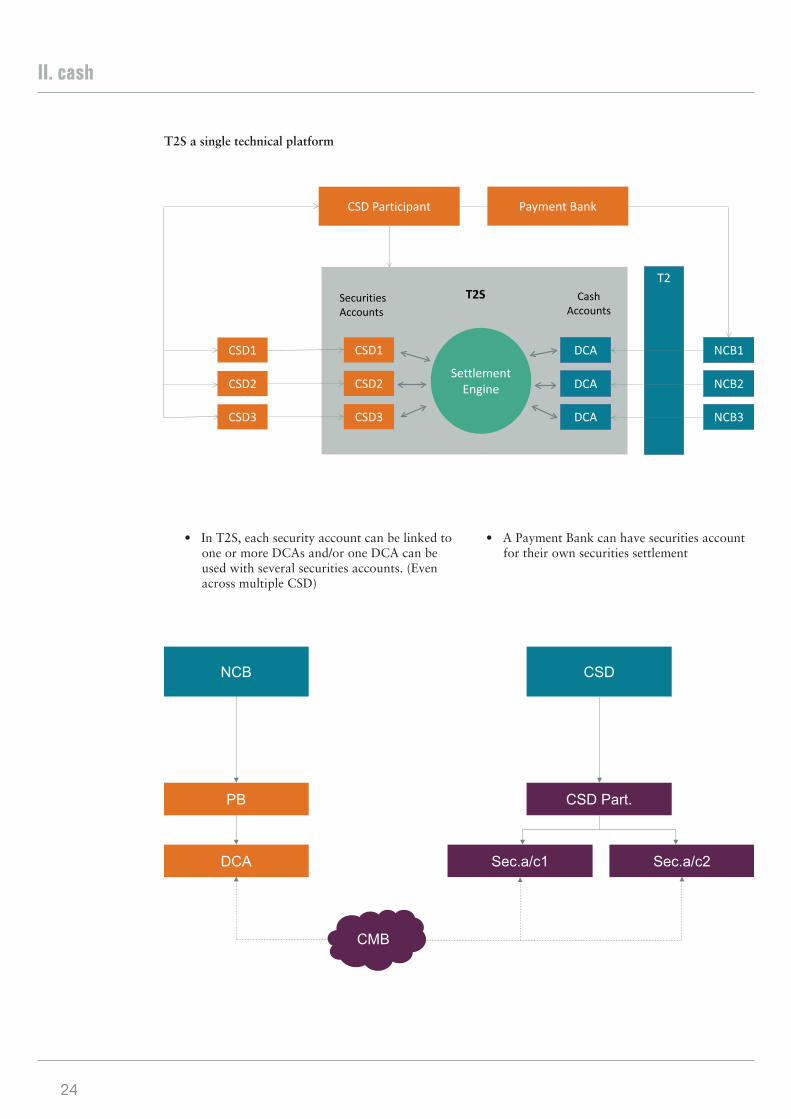

• A Payment Bank can have securities account for their own securities settlement

sCSD1

CSD3

CSD2

DCA

DCA

DCA

CSD1

CSD3

CSD2

NCB1

NCB3

NCB2Settlement

Engine

T2

CSD Participant Payment Bank

Securities Accounts

T2S CashAccounts

T2S a single technical platform

• In T2S, each security account can be linked to one or more DCAs and/or one DCA can be used with several securities accounts. (Even across multiple CSD)

NCB CSD

PB

DCA

CSD Part.

Sec.a/c1 Sec.a/c2

CMB

II. cash

25

Having segregated DCA accounts linked to a specific fund administrator/manager would depend on the level of detailed reporting and online access required to support the cash management and reconciliation process performed by the entity reconciling the funds cash accounts.

NCB CSD

PB

DCA

CSD Part.1

Sec.a/c1 Sec.a/c2

CMB

PB as CSD Part.

CMB

While the central bank allows payment banks to maintain single or multiple DCA structures the requirements and associated fees linked to these structures would need to be discussed between the fund administrator/manager and their commercial bank to determine the most effective and cost effi-cient model to adopt.

26

It should be mentioned that according to the CA market standards and the T2S CA Standards, cash entitlements resulting from corporate actions should be paid using the same payment mechanism used for settlement of the underlying instruments. This means that cash entitlements resulting from CAs on securi-ties on securities accounts of CSDs on T2S, should be paid using DCAs on T2S.

28. Which Type of event is not taking place in T2S and why?

Proxy voting per se does not take place in T2S, However the potential settlement outcome of proxy voting takes place in T2S.

29. What will T2S mean to market claims?

For transactions in investment funds, listed and traded on a regulated trading venue, the T2S Advi-sory Group has endorsed harmonised standards for market claims to be used where possible, including primary market transactions

30. How is the event notification of the TA reconciled with the CSD?

Where the TA is the ultimate recordkeeper (except for fund shares issued as per the Dematerialisation Law of 2013), the TA may send event notifications of traded holdings to the CSD. The CSD then has to reconcile this with its own books. Where the CSD is the ultimate recordkeeper, the CSD provides a state-ment of holding to its client via local agent and/or is-suance agent, as applicable. It is the TA’s responsibil-ity to reconcile this with the shareholder register. For actively traded funds with many pending primary market transactions, this can be a very challenging task because the CSD records settled holdings and the register records traded holdings.

31. Does T2S change the way entitle-ment is calculated by the registrar?

No.

III. corporate actions in T2S

The core of T2S is settlement. Asset servicing, e.g. corporate actions processing, do not fall within the remit of T2S. Nevertheless, T2S supports CSDs in their management of custody services by offering all the necessary functionalities to ensure their effective and efficient processing. T2S has forced the industry to address the lack of corporate action harmonisa-tion in order to ensure efficient cross border settle-ment. Two main initiatives were taken in Europe to address this:

1. The private sector EU initiative: the CA mar-ket standards11

2. Initiative of the T2S Community: the T2S CA standards12

The first initiative led to the creation of the Corpo-rate Action Joint Working Group (CAJWG) that worked to streamline the process to reduce costs and operational risks for market participants. They issued market standards for corporate action pro-cessing in Europe.

The second initiative was led by some T2S stake-holders who recognised the need for common T2S practicing for processing corporation action with securities proceeds in the context of T2S.

26. Who is impacted by T2S Corporate Action process?

Corporate actions are managed by the CSDs partic-ipating into T2S. T2S as such does not manage the corporate action process; the settlement process of the CAs, i.e. instructing cash and securities balances as a result of CAs, takes place in T2S.

27. Which type of event would be settled in T2S and how?

All events that affect the unit quantity of holdings, such as mergers, splits and liquidations as well as events, where there is distribution of cash entitle-ments to the owners of the funds, are managed by CSDs and settled in T2S. The CSDs will generate the relevant instructions for T2S settlement in accor-dance with the corporate action confirmations. The direct impact is on the CSD.

11 The Market Standards for Corporate Actions Processing, developed by the Corporate Actions Joint Working Group (CA-JWG), are available on the website of the European Banking Federation at http://www.ebf-fbe.eu by clicking on European Industry Standards

12 For more information about the CASG and the T2S CA standards, please visit the T2S website at http://www.ecb.europa.eu/paym/t2s and click on Governance, then Advisory Group, then Sub-Group on Corporate Actions.

27

• Distribution oversight:

- Sales monitoring; - Due diligence and on-going monitor-

ing of distribution; - Mis-Selling prevention/suitability/

appropriateness of investment; - KYD/Distributor Selection/Distribu-

tion Agreements; - Trailer fees/Rebates or service fees

management; - Local distribution rules; - Compliance with AML/KYC.

• Product Investment restriction monitoring;

The main challenge for asset managers is to define the framework around T2S which will allow asset manager to benefit from the efficiency brought by the T2S infrastructure while managing these specific processes.

A key feature is the identification of the order giver (e.g. investor/distributor/intermediary) for orders and transfers, which is at the heart of investor pro-tection and distribution oversight.

35. Why is transparency important?

A management company has to ensure that any investment in its fund is:

• Compliant with regulation (e.g. AML/KYC checks);

• Eligible (e.g. client acceptance, investment restriction, compliance with local sales and marketing rules);

• Suitable and appropriate (e.g. information on investors, suitability and appropriateness checks).

Such controls should ideally be performed ex-ante to avoid mis-selling and that a non-eligible transaction is booked in the fund.

The management company also needs to monitor the performance of the sales team, the distribution agreements, and receive information on the trends and habits of their clients.

32. How is entitlement impacted by transfer?

T2S enables transfers to be settled between par-ticipants of different CSDs without requiring any update of the TA’s register (i.e. ‘Model 3’) – this might create transparency issues further detailed in the next paragraph. For the processing of corporate actions when transactions are pending settlement on or around the record date, the CSDs must either follow agreed standards by default or follow the optional indicators used by the participants in their settlement instructions, i.e. no market claim, and cum-dividend or ex-dividend.

Specific note related to investment funds:According to the market (CAJWG) standards, the scope of instruments whose corporate actions has to be processed according to the CA standards is: ‘all securities used for direct investments (equities, fixed income instruments) deposited and settled in Book Entry form with an (I)CSD in Europe; investment funds listed and traded on a regulated trading venue should be processed, where possible, in accordance with the applicable standards hereof’

Exchanged traded funds are not considered in this paper.

33. The impact of T2S on the transpar-ency dilemma

Asset management firms are already struggling with the ever-increasing amount of data and reports in-termediaries are providing, and how to make those useful in their oversight and compliance activities.Cross-border settlement via CSDs, (in or outsideT2S) will make this challenge even more complex to address at a time when asset managers are reinforc-ing their distribution oversight duties.

In this context, we will highlight how transparency should be dealt with when reporting on distribution activities to asset managers on the one hand and the distribution chain on the other.

34. What are the challenges of T2S for the funds distribution?

Unlike other securities, funds are following specific processes which will not be accommodated by T2S infrastructure itself:

28

The opening of bilateral links between CSDs can mean that shares will circulate across the various CSDs without the asset manager being informed. This puts more emphasis on reconciliation and realignment procedures involving the CSDs.In this situation, identifying the point of sales behind this CSD omnibus account will be even more chal-lenging, and the existing risk even higher.

38. What CSD models are currently used for Luxembourg funds?

Luxembourg funds are distributed on a cross-border basis in CSD markets such as France or Germany.If an asset manager wants to effectively sell in these market, it has to comply with the local market prac-tices and to be technically issued in the respective CSDs.

Asset managers therefore appoint an issuing agent to centralise and collect orders from the CSD partic-ipants, to execute them at the TA, to manage the sub-issuing account in the CSD and to perform the settlement in the CSD for the fund.

Currently, the investor CSD is the same as the issuer CSD. For example the Luxembourg funds available in Euroclear France or Clearstream Frankfurt are only available to participants in the respective CSD. All transactions are booked in the issuer’s CSD om-nibus account opened at the TA.

Tomorrow, with T2S, a fund could appoint mul-tiple Technical Issuer CSDs and will face multiple investor CSDs. This will increase issues in terms of transparency. It might be best to appoint one Techni-cal Issuer CSD and aliment the other CSDs through T2S.

Current account structure:

36. Did these challenges already exist pre T2S?

In order to reach more investors, while simplifying the operating model, the fund industry has seen the increasing importance of intermediaries, such as platforms, custodians or ICSD, who collect orders, and centralise these in an omnibus account opened at the TA.

Already today the identification of the real investor/distributor behind these intermediaries is challeng-ing.

Even if solutions to improve transparency have been implemented, they are not widely used. Therefore introducing common standards will be beneficial for the entire fund industry.

Example: A TA could receive a redemption order from an investor for settlement in the omnibus account of its intermediary. Should the TA accepts such order, and the intermediary accepts its clients to instruct on its account, the TA is only able to check the omnibus position of the intermediary, but not the position of the investor. Therefore, it creates a risk to execute this transaction and to redeem shares that are actually not owned by the investor.

37. Why are these challenges more important with T2S?

When a fund is distributed in a CSD market, the fund manages a sub-issuing account, either directly or through a third party, in the CSD and creates an omnibus account in its register.

With the introduction of T2S, some investors may progressively use the T2S setup for dealing in secu-rities, including funds. At that stage their positions would be transferred from their registered account to the CSD omnibus account which in most cases prevail in the CSD environment.

Investor CSD = Issuer CSD

Investor Account 1

Investor Account 2

Investor Account 3

TA

Fund Sub-Issuing Issuing Agent / Issuer CSD Account

III. corporate actions in T2S

29

• There are also markets where these practices are combined.

What are the operating models of each option?

1. Order-marking

Order-marking is a model where only one omnibus account is opened in the fund register per issuer CSD, and the order giver places the order to the fund with a code identifying the point of sale. This code will be used by the same entity placing the or-ders for transfers and reported back by the CSDs to the market participants (e.g. TA and asset manager).

The model would work as follows:

39. How is transparency managed in existing CSD models?

Each CSD has different standards to address trans-parency hence these are different per market. The methods used include:

• Order-marking: In France for example all transactions recorded in the fund register are marked by the order giver with an identifica-tion code, the BIC1 of the investor.

• Position reporting whereby the position of ac-count holder in the investor CSD is provided on a periodic basis.

• Account segregation, for example Denmark, whereby all accounts at the investor CSD are disclosed and segregated in the register of the fund.

Investor 1

Order marking

TA

Issuing Agent / TechnicalIssuer CSD

Asset Manager

Transaction Reporting

Investor 1

Investor 2

Investor 3

Investor 2

Investor 3

Distribution Oversight

2. Position reporting

The principle of position reporting involves both the investor and issuer CSD to report all positions to the asset manager.

3. Account segregation

In T2S, the investor CSD will hold an account with each individual Technical Issuer CSD.

These investor CSDs could potentially share the de-tails of the investor in its books with the issuer CSD in order to provide transparency.

The issuer CSD in turn could open as many accounts in its books as is necessary to achieve transparency, including the ones for which the investor CSDs has provided details on. Full transparency would only be achieved if all CSDs share this information together with transfers between participants.

The model would then work as in the following example:

30

The usage of one common database for order-mark-ing would be a clear benefit for the fund industry in order to standardise the identification of an order giver; e.g. order giver/investor/distributor, and which is fundamental for an efficient transparency model.

41. What position reporting practices could be used?

An ISO standard that can be used by the industry participants to report the positions. It supports a custodian chain with up to 10 levels.

42. How does each model respond to the challenges in the asset manage-ment industry?

TA

Investor CSD = Issuer CSD

Investor Acct A

Investor Acct B

Investor Acct C

Issuing Agent / CSD accounts

c/o Investor acct A

c/o Investor acct B

c/o Investor acct C

Fund Sub-Issuing

Account

40. What order-marking practices could be used?

There is an ISO-standard and is recommended by EFAMA, called BIC1, and this standard is adopted by the French market, and proven to work in a CSD environment.

There are approximately 2,000 BIC1 codes, stored in a centralised database.

These BIC1 codes are BIC 8 or BIC 11, allowing BIC1 to go beyond the entity of the order giver to identify the nature of its underlying activities (e.g. primary dealing, third-party dealing, insurance, etc.). The Legal Entity Identifier (LEI) could also be used to mark orders. The LEI will identify the legal entity placing the order, but will not identify the underly-ing activity.

Challenge Segregation Order-marking Position Reporting

Distribution oversight YesEx-ante

YesEx-ante

YesEx-post

Local distribution rules compliance YesEx-ante

YesEx-ante

YesEx-post

Sales monitoring YesEx-ante

YesEx-ante

YesEx-post

Trailer fees or service fees calculation YesEx-ante

YesEx-ante

YesEx-post

‘Real time’ position tracking (this would include transfers)

YesEx-post

YesEx-ante

No

Product Investment restriction monitoring YesEx-ante

YesEx-ante

YesEx-post

Suitability/appropriateness of investment

YesEx-ante

YesEx-ante

YesEx-post

III. corporate actions in T2S

31

An example is the adoption of the ISO transparency of holding report which implies the following:

• Those CSD participants that use one account for holdings representing more than one commercial relationship with a fund shall re-port the breakdown of such holdings to their respective investor CSD.

• Investor CSDs compile any received reports of participant account breakdowns with the holdings recorded at the CSD participant level, and report this to their issuer CSD. Issuer CSDs compile the reports received from their investor CSDs, and disseminate the information to the respective TAs and/or asset managers;

• Whenever relevant, the stated holdings are marked with the same identification as is used for order marking; and

• The TAs and/or asset managers use the position files for reconciliation and ex-post distribution monitoring purposes.

3. Account segregation

Account segregation is market practice for most of the Scandinavian CSDs but not all CSD may support account segregation. It would require a total change of most models outside of Scandinavia, and may in the end not be supported by T2S.

This model will require:

• Cooperation between CSDs to provide detailed information about their clients and accounts;

• Non-cooperating CSD will have to follow option 2 or 3 detailed below if they still wish to be transparent .

44. Is there a need to review distribu-tion agreements?

There is no obligation to review distribution agree-ments in the context of T2S nor, more specifically, when it comes to transparency. That being said, we would highly recommend asset managers to amend their distribution agreement if they want to achieve a good level of transparency perspective; i.e. they may want to impose certain obligations (e.g. order-marking obligation, position reporting obliga-tion to the CSD to increase the visibility of account holders,…).

43. What is required to make these solutions work?

For all models, it is key to reconcile with the posi-tion in the CSDs.

Efficiency will come from the amounts and level of reconciliation required and the ability to have a real-time allocation of orders.

1. Order-marking

This model provides transparency on orders, and allows a calculation of the positions based on the orders received. This model will need to capture all orders and transfers to avoid reconciliation breaks between the calculated positions and the actual positions.

This model will require:

• The fund industry (asset managers, asset servicers, distributors/investors) to define and adopt order-marking industry standards such as BIC1 or LEI.

• A central database of order-marking for the industry to create and manage order mark-ing codes for identifying uniquely a business counterparty (e.g. institutional investor, distributor) across fund managers and across markets.

• Transfers between investors’ CSD accounts to be reported to the fund with the applicable order-marking to allow monitoring of distri-bution and to avoid reconciliation issues.

• The asset managers or their asset servicers will have to calculate their clients positions based on transactions received, and to rec-oncile these positions with the CSDs investor accounts.

• This reconciliation should be limited to ex-ceptions if all transactions are order marked and reported to the asset manager.

2. Position reporting

The fund market participants will need to cooper-ate for the position reporting to meet the require-ments of transparency and to define the framework allowing the disclosure of information about their respective clients.

33

BIC Business Identifier Code, defined in ISO 9362. A BIC is either 8 or 11 characters’ long (called BIC8 and BIC11 respectively). The main purpose of a BIC is to identify a business entity in the payload of an electronic message, and it is different to the elec-tronic addresses (senders and receivers, always 12 characters long) of SWIFT messages. Registration is maintained globally by SWIFT.

BIC1 This is the BIC of a business entity that is not a member of SWIFT, traditionally characterised by the number 1 as the 8th character. Unlike SWIFT membership, a BIC1 is free of charge. Like a BIC, a BIC1 can be either a BIC8 or a BIC11.

BIC8 The BIC of a business entity without branch code is 8 characters long and called a BIC8.

BIC11 The BIC of a business entity with branch code is 11 characters long and called a BIC11. A BIC8 becomes a BIC11 by specifying ‘XXX’ as the branch code.

T2S requires settlement parties to be identified by BIC11 or LEI.

CCB A Cash Correspondent Bank is a financial institution that makes and receives payments on behalf of others (clients and clients of clients). The quality of cash held at a CCB is CoBM.

CeBM Central Bank Money is the quality of cash held on accounts serviced by NCBs.

CoBM Commercial Bank Money is the quality of cash held on ac-counts that are serviced by private sector banks, i.e. all banks except NCBs.