q3 2013 investor presentation - norbord 2013 investor presentation november 2013 2 • all financial...

TRANSCRIPT

Q3 2013

Investor Presentation

November 2013

2

• All financial references are expressed in US$ unless otherwise noted.

• Financial numbers prior to 2010 were prepared in accordance with CGAAP, while numbers from 2010 onward have been prepared in accordance with IFRS.

• This presentation contains forward-looking statements and estimates.

• Actual company results could differ materially from a conclusion, forecast or projection in the forward-looking information.

• Certain material factors or assumptions were applied in drawing a conclusion or making a forecast or projection as reflected in the forward-looking information.

• Additional information can be found in the Company’s annual information form, annual MD&A, and on Norbord’s website (www.norbord.com) about the material factors that could cause actual results to differ materially from the conclusion, forecast or projection in the forward-looking information, and the material factors or assumptions that were applied in drawing a conclusion or making a forecast or projection as reflected in the forward-looking information.

• During the course of this presentation, certain non-IFRS financial information will be presented. Definitions and reconciliation of terms can be found in the Company’s annual and quarterly MD&A.

Forward-Looking Statements and

Non-IFRS Financial Information

3

Company Snapshot

• Norbord is a leading manufacturer of wood-based panel

products and one of the largest global producers of OSB

─ Installed OSB capacity of over 5 Bsf

─ 1,900 employees at 13 plants across the US, Europe

and Canada

• Listed on TSX (“NBD” and “NBD.WT”)

• Reports in US dollars and in accordance with IFRS

• As at September 28, 2013:

─ Total assets of $1,266 million

─ LTM sales of $1,363 million

─ LTM EBITDA of $328 million

I. COMPANY OVERVIEW

US

61%

Europe

27%

Canada

12%

6.1 Bsf

Panel Capacity by Region

4

Norbord’s Products

• New home construction

• Repair and remodel

• Light commercial construction

• Industrial applications

OSB – 84% of Capacity

Particleboard – 10% of Capacity

MDF – 6% of Capacity

• New home construction

• Repair and remodel

• Furniture

• Fixtures

• Furniture

• Fixtures

• Mill work

• Norbord’s operations include 11 OSB mills, two particleboard mills, one

medium density fibreboard (“MDF”) mill and one furniture plant

I. COMPANY OVERVIEW

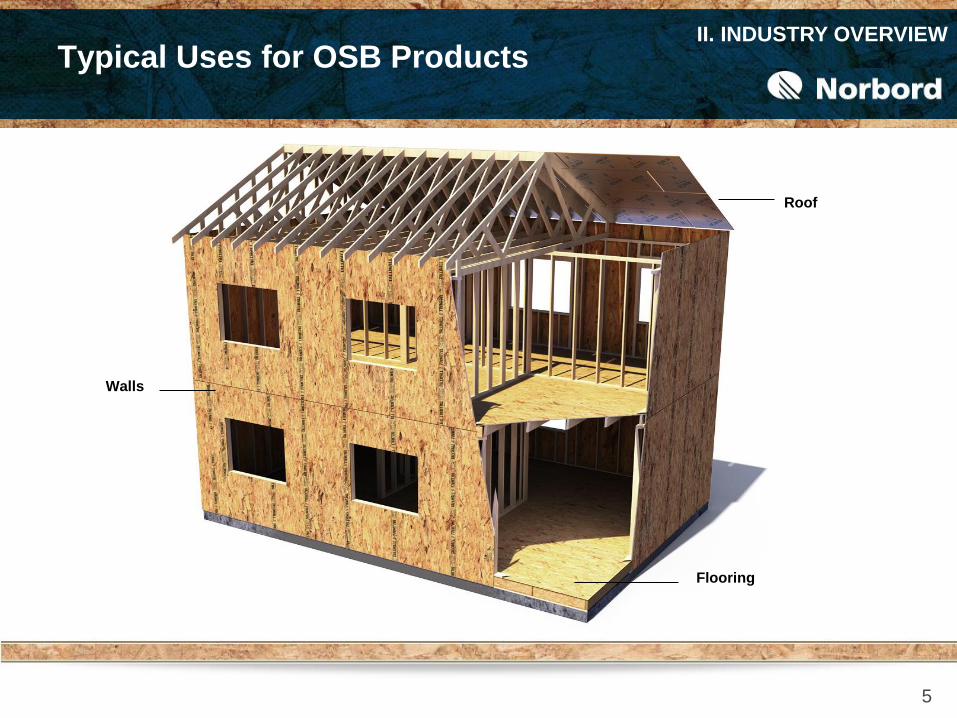

Typical Uses for OSB Products II. INDUSTRY OVERVIEW

5

Walls

Flooring

Roof

6

The OSB Market II. INDUSTRY OVERVIEW

• OSB is an innovative, affordable and environmentally “smart” structural panel

─ Serves many of the same uses as plywood, but produced at a lower cost

• Norbord expects that OSB will continue to capture market share from plywood

Sources: APA-The Engineered Wood Association (“APA”) and Forest Economic Advisors, LLC (“FEA”)

North American Structural Panels Market Share

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'80 '85 '90 '95 '00 '05 '10 '15F

% S

hare

of

No

rth

Am

eri

can

Str

uctu

ral

Pan

el P

rod

ucti

on

OSB

Plywood

7

US Housing Starts Recovery is Real

0.0

0.5

1.0

1.5

2.0

Housing Starts

Underlying Demand

US Housing Starts (millions)

Source: FEA

• Leverage to US housing recovery

• Favourable long-term OSB industry fundamentals

OVER

built

UNDER

built

II. INDUSTRY OVERVIEW

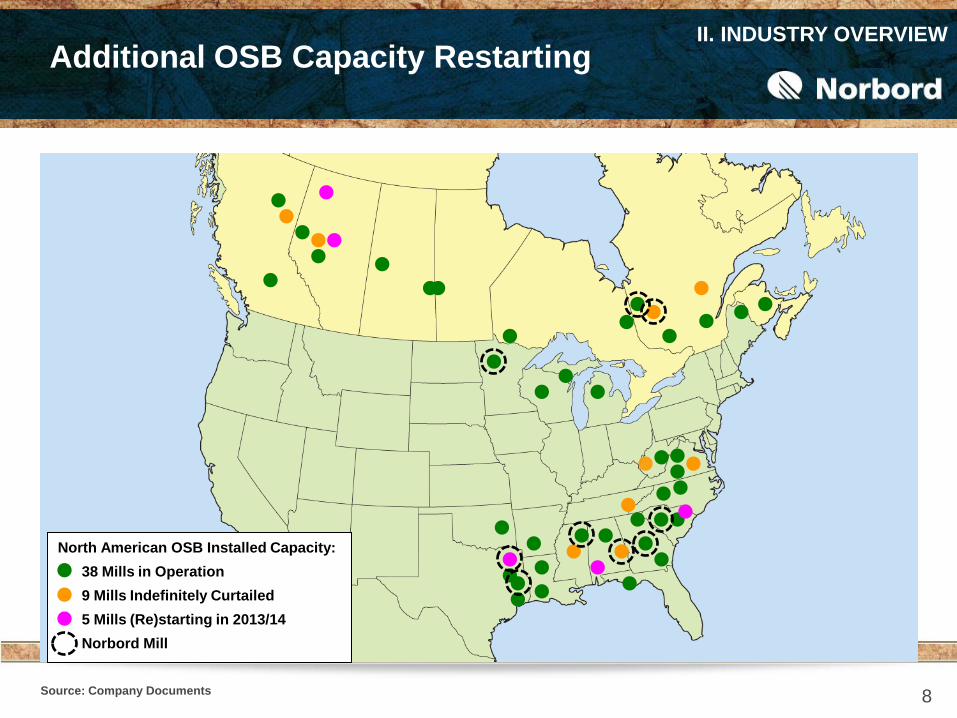

8 Source: Company Documents

II. INDUSTRY OVERVIEW

Additional OSB Capacity Restarting

38 Mills in Operation

9 Mills Indefinitely Curtailed

North American OSB Installed Capacity:

Norbord Mill

5 Mills (Re)starting in 2013/14

9 Source: FEA

II. INDUSTRY OVERVIEW High Demand/Capacity Ratio Supports

Robust Pricing Environment

0%

25%

50%

75%

100%

15

20

25

30

35

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Capacity (Bsf 3/8") Demand/Capacity %

Operating Capacity

Mothballed

Effective Demand/Capacity

10

Attractive OSB Outlook II. INDUSTRY OVERVIEW

Sources: Random Lengths and FEA

• OSB prices are tied to demand for building products, which is influenced by

the general economy, demographics and the need for housing

• With US housing recovering, OSB prices are projected to remain above trend

North Central Benchmark OSB Price

100

150

200

250

300

350

400

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E

An

nu

al A

vera

ge N

C P

rice

US

$ p

er

Msf

7/1

6"

11

Kronospan

37%

Kronoswiss

21%

Norbord

14%

Sonae

13%

Egger

8%

Smartply

6%

Norbord a Significant Player in

OSB Industry

Louisiana-

Pacific*20%

Georgia-

Pacific17%

Norbord

16%

Weyer-

haeuser14%

Ainsworth*

10%

Huber

7%

Tolko

5%

Other

11%

Source: Company Documents - Installed Capacity

*Louisiana-Pacific announced plans to acquire Ainsworth in September 2013

Industry

Capacity

28 Bsf

Industry

Capacity

5 Bsf

II. INDUSTRY OVERVIEW

North American OSB Industry European OSB Industry

12

Norbord’s Strategy is Well Defined

• Pursue growth in OSB

• Own highest-quality assets with

lowest cost position

• Maintain a margin-focused operating

culture

• Focus on growth customers through

best-in-class service and product

development

• Allocate capital with discipline

III. BUSINESS STRATEGY

13

Norbord’s Growth Focused on OSB

0

1

2

3

4

5

6

'92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Norbord OSB Capacity (Billion Square Feet 3/8”)

III. BUSINESS STRATEGY

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

2005 2006 2007 2008 2009 2010 2011 2012 LTM

Norbord North American peer (1)

14

-30%-20%-10%0%10%20%30%40%50%

2005 2006 2007 2008 2009 2010 2011 2012

Norbord North American peer (1)

Low Cost Margin-Focused

Operating Platform

• Low cost operating platform providing superior margins versus peers

Source: Company Documents

(1) North American peer = Louisiana-Pacific

III. BUSINESS STRATEGY

North American OSB EBITDA Margin %

15

35 37

28

56

914

29

16

25 23

$0

$10

$20

$30

$40

$50

$60

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Margin Improvement is an

Operational Priority

• Margin Improvement Program

(MIP) gains help offset impact of

industry-wide rising input costs,

without capex investment:

─ Increased productivity

─ Reduced overhead costs

─ Reduced raw material usage

─ Improved product mix

III. BUSINESS STRATEGY

MIP Gains (US$ millions)

16

Customer Strategy Sets Norbord Apart

• New housing sales volume growing as US housing starts recover

• Pro-dealer shipments now represent 50% of Norbord sales volume

50%

30%

20%

35%

35%

30%New Home

Construction

(Pro-dealers)

Repair & Remodel

(Big Box)

Industrial

NA

Shipments

2.9 Bsf

NA

Shipments

3.5 Bsf

III. BUSINESS STRATEGY

2011 Q3 2013 (annualized)

17

Disciplined Capital Allocation

• Track record of disciplined capital

allocation

─ Accretive acquisitions

─ Low cost capacity additions

─ Divestment of non-core assets

─ Deleverage on cyclical upturns

─ Dividends

─ Share buybacks

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013F

Capex Greenfield Expansion

III. BUSINESS STRATEGY

Capex Investment (US$ millions)

18

Strong Operating Cash Flow

Through Cycle

365

631

495

247

42

(60)

0

107

45

188

328

($100)

$0

$100

$200

$300

$400

$500

$600

$700

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 LTM

10yr Average

$206 million

North Central

Benchmark OSB Price 293 369 320 217 161 172 163 219 186 271 337

Norbord Sensitivity to North American

OSB Price Changes:

+$10/Msf 7/16” = +$36 million EBITDA

(at full capacity)

Total EBITDA (US$ millions)

IV. FINANCIAL OVERVIEW

19

Stable Results Continue from

European Operations

• Norbord’s European operations provide greater sales and earnings

diversification than other North American-based competitors

29

58

32 35

81

4

17

3744

3943

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 LTM

IV. FINANCIAL OVERVIEW

European EBITDA (US$ millions)

20

245

200

240

0

50

100

150

200

250

300

2014 2015 2016 2017

Pri

nc

ipa

l V

alu

e -

US

$ m

illio

ns

6.25%

Bonds

Revolving

Bank Lines

(Undrawn) 7.70%

Bonds

Strong Liquidity

US$ millions Q3 2013

Cash 239

Bank Lines 241

A/R Sec. (1) 100

Liquidity

580

(1) In addition, the Company has an undrawn $100 million 1-year evergreen A/R securitization program.

DBRS BB

Moody’s Ba3

S&P BB-

Norbord’s Financial House Is In Order IV. FINANCIAL OVERVIEW

Manageable Debt Maturities (1) Strong Liquidity

Stable Issuer Credit Ratings

21

Attractive Investment Opportunity

• Leverage to accelerating US housing recovery

─ Every +$10 in OSB price = +$36 million in EBITDA at full capacity

• Low-cost operating platform

• Superior margins versus peers

• Track record of disciplined capital allocation

• Well positioned for recovery

─ Strong customer partnerships

─ Diversification from European operations

─ Strong financial liquidity and comfortable debt maturities

─ Improving OSB demand requires more North American capacity

V. SUMMARY

22

Appendices

Ticker Symbol TSX: NBD, NBD.WT

Common Shares 53.3 million outstanding

Warrants 1.2 million outstanding; expire December 24, 2013 (to purchase 0.1 million Common Shares, on a cash exercise basis)

Cash Exercise:

(10 Warrants + CAD $13.60) = 1 Common Share

OR Cashless Exercise:

(# Warrants / 10 * (Market Price(1) – Exercise Price)) /

Market Price(1) = # Common Shares

Quarterly Dividend CAD $0.60 per share (payable on Dec. 21, 2013 to shareholders of record on Dec. 1, 2013)

Majority Shareholder Brookfield Asset Management – 53%

Capital Structure (as at October 31, 2013)

(1) Market Price = volume weighted average trading price (“VWAP”) on the TSX for the five trading days immediately preceding the Exercise Date 23

24

0

50

100

150

200

250

300

350

400

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

An

nu

al A

vera

ge N

C P

rice

US

$ p

er

Msf

7/1

6"

Source: Random Lengths

Q1 157 217 261 132 163 175 423 364 285 145 137 154 212 198 203 417

Q2 195 291 240 190 159 215 443 297 238 156 179 146 295 173 235 347

Q3 287 301 171 180 159 381 351 303 181 177 201 178 180 184 313 252

Q4 178 230 155 140 156 401 264 317 166 165 170 172 191 190 332

Average 204 260 207 160 159 293 369 320 217 161 172 163 219 186 271

15 year Average

OSB Prices Strong Over the Cycle

Historical North Central Benchmark OSB Price

25

(1) Assumes operation at full capacity levels

Before the impact of any cash flow currency hedges

Tax operating loss carry-forwards (gross) as at Dec. 31, 2012 – US $145 million, Canada C$85 million,

Belgium €38 million

Exposure Change

EBITDA

Impact (1)

($ millions)

North American OSB $10 per Msf 7/16” + $36

European OSB €10 per m3 + $7

Canadian dollar $0.01 per Cdn$ + $1

Pound sterling £0.01 per € + $2

Financial Sensitivities

26

Analyst Analyst Name Contact

BMO Capital Markets Stephen Atkinson (514) 286-7309 [email protected]

CIBC Mark Kennedy (403) 221-4133 [email protected]

Credit Suisse Andrew Kuske (416) 352-4561 [email protected]

Desjardins Securities Pierre Lacroix (514) 281-4231 [email protected]

ERA Forest Products

Research Claire Huxtable (604) 886-5741 [email protected]

John Tumazos Very

Independent Research John Tumazos (732) 444-1083 [email protected]

Raymond James Daryl Swetlishoff (604) 659-8246 [email protected]

RBC Capital Markets Paul Quinn (604) 257-7048 [email protected]

Salman Partners Rajiv Mukhi (604) 622-5289 [email protected]

Scotia Capital Benoit Laprade (514) 287-3627 [email protected]

TD Securities Sean Steuart (416) 308-3399 [email protected]

Vertical Research Partners James Armstrong (212) 256-6157 [email protected]

Analyst Coverage of Norbord

27

• Norbord does not provide guidance regarding its expectations of future OSB prices. The following is a

sample of price forecasts by analysts as at November 7, 2013. It is not exhaustive.

Annual Average

North Central Benchmark OSB Price US$ per Msf 7/16” 2013 2014

BMO 320 255

CIBC 324 325

Desjardins Securities 319 278

ERA Forest Products Research 349 246

Raymond James 320 300

RBC Capital Markets 320 300

Salman Partners 325 300

Scotia Capital 322 300

TD Securities 320 290

Vertical Research Partners 340 365

Average $326 $296

Forecast OSB Pricing – North Central 7/16”