q3 2013 final million q3 2013 q3 2012 diff ebitda excluding non-recurring items 9,419 9,283 136...

TRANSCRIPT

1

Interim ReportJanuary-September, 2013

Johan DennelindPresident and CEO

Third quarter summary

• Revenues impacted by modest economic growth and lower regulated interconnect

• Improved billed revenue trend in Mobility Services across Scandinavia supported by new pricing models

• Continued implementation and effects of efficiency measures

• Significant investments in internet experience - 4G and fiber

• Increased focus on governance and sustainability

• Initial observations as new CEO – a good company with untapped potential

2

2

Free cash flow

3,825

7,308

Q3 12 Q3 13

SEK million

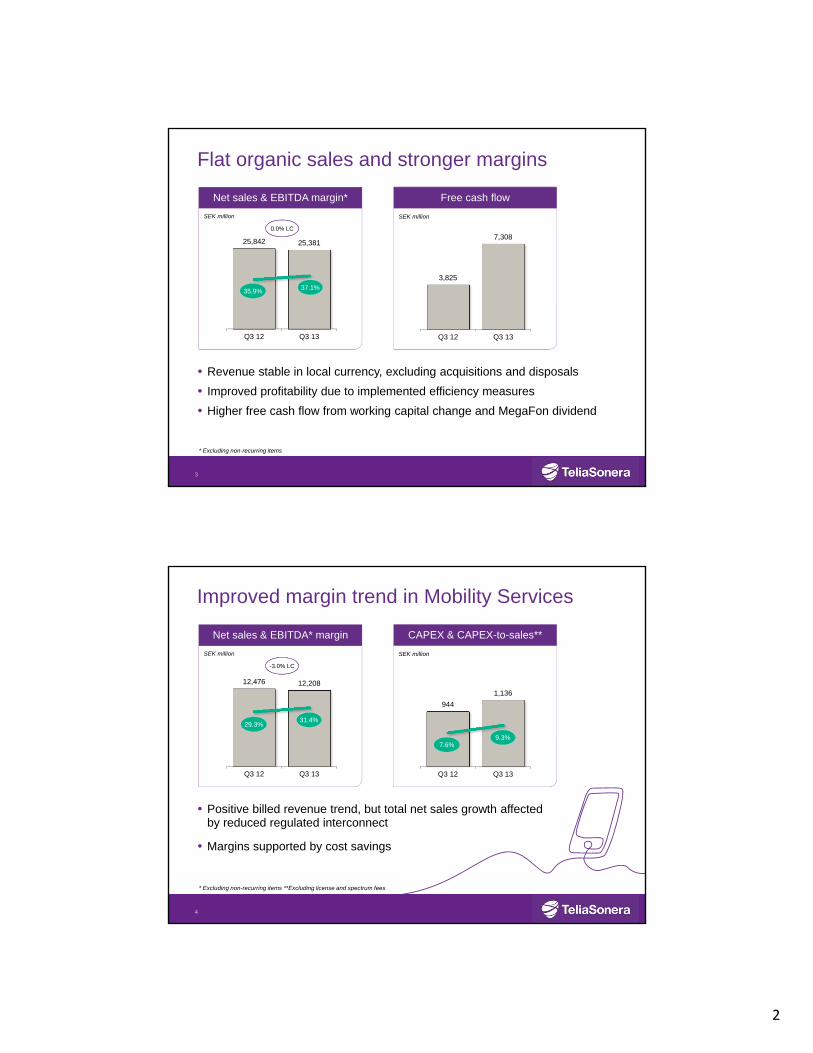

Flat organic sales and stronger margins

3

* Excluding non-recurring items

• Revenue stable in local currency, excluding acquisitions and disposals

• Improved profitability due to implemented efficiency measures

• Higher free cash flow from working capital change and MegaFon dividend

Net sales & EBITDA margin*

25,842 25,381

Q3 12 Q3 13

37.1%35.9%

SEK million

0.0% LC

Net sales & EBITDA* margin

12,476 12,208

Q3 12 Q3 13

31.4%29.3%

SEK million

-3.0% LC

CAPEX & CAPEX-to-sales**

SEK million

944

1,136

Q3 12 Q3 13

9.3%7.6%

Improved margin trend in Mobility Services

4

* Excluding non-recurring items **Excluding license and spectrum fees

• Positive billed revenue trend, but total net sales growth affected by reduced regulated interconnect

• Margins supported by cost savings

3

Data centric models gain traction in Mobility Services

5

* In local currencies

Data growth

0%

20%

40%

60%

80%

100%

120%

Q4 12 Q1 13 Q2 13 Q3 13

Volume Revenue

Billed revenues Q313 y-o-y*

6.0%

4.4%

3.2%

1.2%

0.2%

-4.3%

-7.3%

-7.9%

-8.9%

Denmark

Spain

Sweden

Mobility

Norway

Finland

Estonia

Latvia

Lithuania

CAPEX & CAPEX-to-sales**

SEK million

1,202 1,217

Q3 12 Q3 13

Revenue pressure in Broadband Services

6

* Excluding non-recurring items **Excluding license and spectrum fees

• Continued decline in traditional fixed telephony and heavy price pressure in B2B

• Profitability under pressure, but cost savings start to come through

Net sales and EBITDA* margin

8,644 8,252

Q3 12 Q3 13

31.5%33.2%

SEK million

-2.4% LC

14.7%13.9%

4

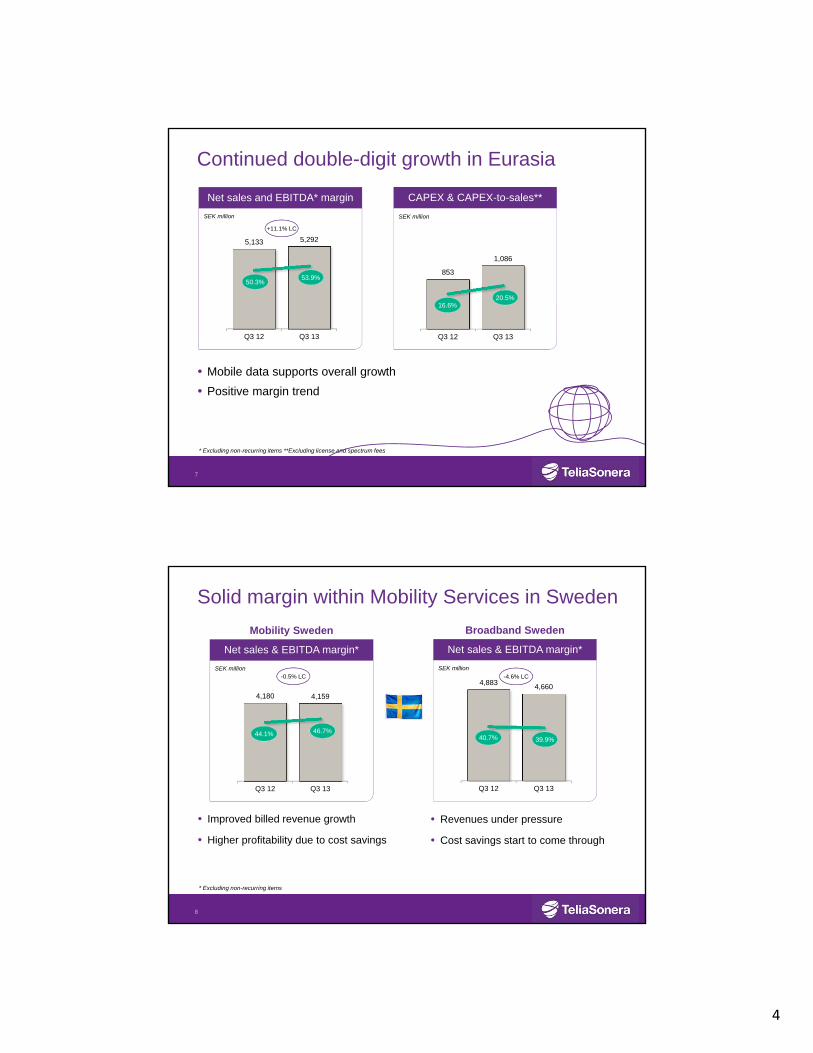

Continued double-digit growth in Eurasia

7

* Excluding non-recurring items **Excluding license and spectrum fees

SEK million

• Mobile data supports overall growth

• Positive margin trend

Net sales and EBITDA* margin

5,133 5,292

Q3 12 Q3 13

53.9%50.3%

SEK million

+11.1% LC

3.8257.308

Q3 12 Q3 13

CAPEX & CAPEX-to-sales**

SEK million

853

1,086

Q3 12 Q3 13

20.5%16.6%

Solid margin within Mobility Services in Sweden

8

* Excluding non-recurring items

46.7%

• Improved billed revenue growth

• Higher profitability due to cost savings

• Revenues under pressure

• Cost savings start to come through

Net sales & EBITDA margin*

4,8834,660

Q3 12 Q3 13

39.9%40.7%

SEK million

-4.6% LC

Broadband Sweden

Net sales & EBITDA margin*

4,180 4,159

Q3 12 Q3 13

44.1%

SEK million-0.5% LC

Mobility Sweden

46.7%

5

Challenging environment in Finland

9

* Excluding non-recurring items

46.7%

• Billed revenues under pressure

• EBITDA margin supportedby efficiency gains

• Weak sales and margin decline

Net sales & EBITDA margin*

1,335 1,273

Q3 12 Q3 13

25.6%28.6%

SEK million

-7.5% LC

Broadband Finland

Net sales & EBITDA margin*

1,938 1,856

Q3 12 Q3 13

30.3%

SEK million-7.2% LC

Mobility Finland

34.9%

Formalizing our sustainability agenda

• Three dimensions to secure ethical decision making– Compliance to legal frameworks– Adherence to ethical standards and values– Reinforcing a corporate culture and values that

embed sustainability in all things we do

• Actions taken/underway– New Compliance function– Establishment of CEO Office– Roll out of Code of Ethics and Conduct program

• Next step - Establish KPIs to be reportedand monitored continuously

10

6

A strong foundation to build upon for the future

11

c

Growing and valuable associates

12

c

• Associated income of SEK 1,503 million (833)– of which Turkcell SEK 675 million (631)– of which MegaFon SEK 793 million (173)

• MegaFon dividend of SEK 1,940 million, net of taxes

7

Need to increase competitiveness

• Decreasing market shares in too many areas in recent years

• Unsatisfactory profitability trend in several units

• Focus areas– Understand customers– Reduce complexity– Shape culture

13

Summary and priorities

14

• Improved margin, stable revenue and strong cash flow in the quarter

• Data centric pricing models gaining traction across Scandinavia

• Essential to embed sustainability in all we do - several actions taken

• The journey ahead - need to strengthen competitiveness

8

Interim ReportJanuary-September, 2013

Per-Arne BlomquistExecutive Vice President and CFO

Summary first 9 months

• Net sales SEK 75,197 million (77,829)– Decline of 0.2 percent in local FX, excluding acquisitions

and disposals

• EBITDA* SEK 26,856 million (27,169)– Increase of 2.2 percent in local FX

• EBITDA margin* 35.7 percent (34.9)

• Earnings per share SEK 2.95 (3.00)

• Free cash flow SEK 12,244 million (9,080)

– Excluding dividends from MegaFon

* Excluding non-recurring items

16

9

Flat revenue development

17

* In local currencies, excluding acquisitions and disposals

Net sales split and Net sales growth* y-o-y

Q2 2012 Q2 2013 Q3 2012 Q3 2013

Mobility Broadband Eurasia

+14.3%+14.3%

-1.8%

-3.6%

+11.1%

-3.0%

+0.4% 0.0%

-2.4%

• Double-digit growth in Eurasia, but tougher comparable numbers in Uzbekistan

• Sequential improvement in Broadband related to International Carrier

• Mobility affected by lower growth in Spain

Sound balance between revenues and costs

* In local currencies, excluding acquisitions and disposals

Net sales and addressable cost base* change y-o-y

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2007 2008 2009 2010 2011 2012 Q113 Q213 Q313

Net sales Addressable cost base

18

10

Significant impact from interconnect in Mobility Services

19

Revenue growth* (%)

-3.0 0.7

-15 -10 -5 0 5 10 15

Lithuania

Norway

Finland

Estonia

Latvia

Total Mobility

Sweden

Denmark

Spain

Revenue growth exinterconnect impact

Total revenue growth

Billed revenues* change y/y (%)Billed revenues* change y/y (%)

-6%

-4%

-2%

0%

2%

4%

6%

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

* In local currencies

Further margin improvement

* Excluding non-recurring items

EBITDA margin*, 4 quarters rollingEBITDA margin*, 4 quarters rolling

32%

33%

34%

35%

36%

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

35.1%

EBITDA margin*, change Y/YEBITDA margin*, change Y/Y

-2

-1

0

1

2

3

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Percentage point

20

* Excluding non-recurring items

11

Balance between sales and OPEX growth

• All business areas reduced costs in the quarter

Net sales in local currencies, excluding acquisitions and disposals

BroadbandBroadband

-15%

-10%

-5%

0%

5%

Q112 Q212 Q312 Q412 Q113 Q213 Q313

Change in Net Sales (y-o-y)Change in Opex (y-o-y)

MobilityMobility

-15%

-10%

-5%

0%

5%

10%

Q112 Q212 Q312 Q412 Q113 Q213 Q313

Change in Net Sales (y-o-y)Change in Opex (y-o-y)

EurasiaEurasia

-10%

-5%

0%

5%

10%

15%

20%

25%

Q112 Q212 Q312 Q412 Q113 Q213 Q313

Change in Net Sales (y-o-y)Change in Opex (y-o-y)

21

• Revenue remains under pressure, but cost savings start to come through

Stronger margins in Mobility and Eurasia

• Higher margins in 5 out of 8 business due to positive impact from efficiency measures

• Positive margin change due to solid sales growth and reduced costs

* Excluding non-recurring items

Mobility Services

9M 12 9M 13

EBITDA* margin

29.3% 30.7%

Broadband Services

9M 12 9M 13

EBITDA* margin

31.7% 30.1%

Eurasia

EBITDA* margin

9M 12 9M 13

52.9%50.5%

22

12

Addressable cost base target*

Lowering the cost base by SEK 2 billion

• Savings of SEK 0.2 billion recorded in Q4 2012 and around SEK 0.6 billion in 9M 2013

• In total, 1,800 employees will be affected

• 1,460 employees noticed y-t-d

• Restructuring costs of SEK 1.7 billion, of which SEK 1.4 billion expected in 2013. SEK 1.0 billion has been recorded y-t-d

* Excluding Mobility Spain and NextGenTel, stable FX

2012 9M 2013 2013e 2014e

SEK billion

26.0

25.0

26.8

26.1

23

CAPEX-to-sales

* Excluding license and spectrum fees

CAPEX-to-sales ratio*CAPEX-to-sales ratio*

Q3 12 Q3 13 2012 2013 9M 2013e

14.0%14.6%

12.7%

14.3%

12.5%

• Increased CAPEX following relatively low activity in H113

• Focus on high speed internet access through 4G and fiber

24

CAPEX-to-sales ratio*CAPEX-to-sales ratio*

Mobility Services Broadband Services Eurasia

14.7%

20.5%

9.3%

Q3 12 Q3 12 Q3 12Q3 13 Q3 13 Q3 13

13

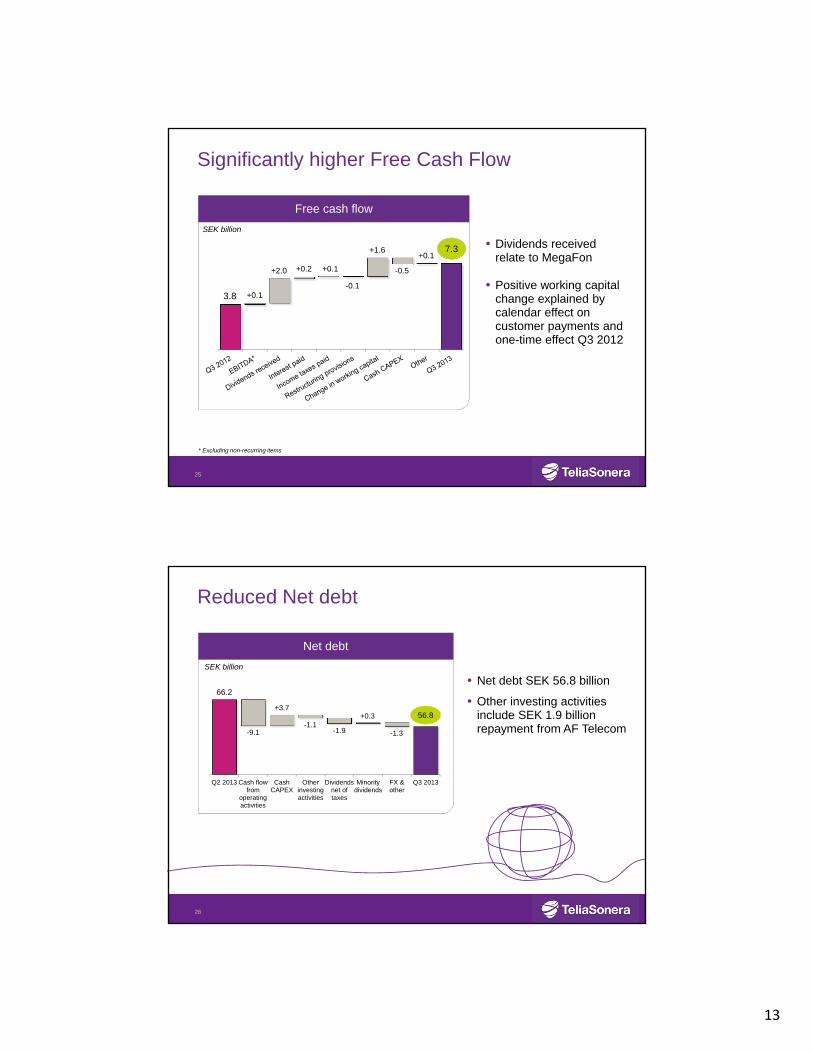

Significantly higher Free Cash Flow

25

* Excluding non-recurring items

Free cash flow

7.3

3.83.8

SEK billionSEK billion

+1.6+1.6+0.1+0.1

+2.0+2.0

+0.1+0.1

-0.5-0.5

Free cash flow

7.3

3.8

SEK billion

+1.6+0.1

+2.0

+0.1

-0.5+0.2

-0.1

+0.1

• Dividends received relate to MegaFon

• Positive working capital change explained by calendar effect on customer payments and one-time effect Q3 2012

Net debt Net debt

Reduced Net debt

Q2 2013 Cash flowfrom

operatingactivities

CashCAPEX

Otherinvestingactivities

Dividendsnet oftaxes

Minoritydividends

FX &other

Q3 2013

56.8

66.2

SEK billion

+0.3

-1.3-9.1-1.1

-1.9

• Net debt SEK 56.8 billion

• Other investing activities include SEK 1.9 billion repayment from AF Telecom

+3.7

26

14

Net debt and Net debt / EBITDA*Net debt and Net debt / EBITDA*

Net debt to EBITDA within our target range

* 4 quarters rolling

0.0

0.5

1.0

1.5

2.0

2.5

0

15

30

45

60

75

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

SEK billion

• Gross debt of SEK 86.6 billion and Net debt of SEK 56.8 billion

• Net debt to EBITDA of 1.58x

• Target range between 1.5-2.0x

1.58

27

Outlook for 2013 – Unchanged

* In local currencies, excluding acquisitions and disposals** Excluding non-recurring items *** Excluding license and spectrum fees

Outlook 9M 2013

Net sales* Flat -0.2%

EBITDA margin**Increase slightly

(34.5% 2012)35.7%

CAPEX-to-sales ratio***

Around 14% 12.7%

28

15

29

30

16

Organic revenue growth Q3 2013

Revenue growth (%)Q3 2013

Reportedgrowth

of whichcurrency

of whichacquisitions

and disposals

of which organic

Mobility Services -2.1 0.9 - -3.0

Broadband Services -4.5 0.9 -3.0 -2.4

Eurasia 3.1 -8.3 0.3 11.1

The Group -1.8 -0.9 -0.9 0.0

31

Statement of cash flows Q3 2013

SEK million Q3 2013 Q3 2012 Diff

EBITDA excluding non-recurring items 9,419 9,283 136

Dividends received from ass companies 2,043 0 2,043

Interest paid (net) -109 -259 150

Income taxes paid -836 -922 86

Payment of restructuring provisions -220 -157 -63

Diff between paid/recorded pensions 24 -26 50

Changes in working cap and other items 741 -854 1,595

Cash flow from operating activities 11,062 7,065 3,997

Cash CAPEX -3,754 -3,240 -514

Free cash flow 7,308 3,825 3,483

32

17

Financial key ratios

Sep 30, 2013 Dec 31, 2012

Return on equity* 21.5% 20.5%

Return on capital employed* 16.2% 14.9%

Equity/assets ratio 40.9% 38.2%

Net debt/equity ratio 57.3% 61.4%

Net debt/EBITDA rate* multiple 1.58 1.64

Net debt/assets ratio 23.4% 23.5%

* Rolling 12 months

33

Higher earnings per share

EPS, SEK EPS, SEK

Q32012

Operat. Asscomp

Non-rec

items

FX Net fin Taxes Min int Q32013

1.07

0.93

+0.07

+0.16

-0.11-0.03

+0.05+0.04

-0.04

34

18

Debt Maturing next 12 months – Sept 30, 2013

Debt Portfolio Maturity Schedule – 2013 and onwards

Debt maturity scheduleMMO

0

1

2

3

4

5

6

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Jul-14

Aug-14

Sep-14

0

2

4

6

8

10

12

14

16

18

2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037 2039 2041 2043

SEK billion

SEK billion

Debt per Q3 2013• Gross debt SEK 86.6 bn

• Net debt SEK 56.8 bn

• Net debt/EBITDA 1.58

35

Liquidity position TeliaSonera Group

Committed bank lines Maturity Size Amount undrawn

Syndicated revolving credit facility

Dec 2017 EUR 1 billion EUR 1 billion

Cash and cash equivalents, less blocked funds approx. SEK 23.7 billion

September 30, 2013

36

19

TeliaSonera AB long-term ratings migration history 2002-to-today

TeliaSonera AB credit ratings (A3/A-)

0

1

2

3

4

5

Q1 02 Q4 04 Q4 07 Q4 08 Q4 09 Q4 10 Q4 11 Q4 12

AAAA-A+AA-

Moody’s (A3/P-2)

• January 8, 2003, lowered long-termdebt rating to A2

• November 1, 2006, outlook changed to Negative

• October 30, 2007, lowered long- and short-term debt rating to A3 and P-2respectively

• May 4, 2012, Outlook changed from Negative to Stable

• January 8, 2003, lowered long-termdebt rating to A2

• November 1, 2006, outlook changed to Negative

• October 30, 2007, lowered long- and short-term debt rating to A3 and P-2respectively

• May 4, 2012, Outlook changed from Negative to Stable

Moody’s (A3/P-2)

• January 8, 2003, lowered long-termdebt rating to A2

• November 1, 2006, outlook changed to Negative

• October 30, 2007, lowered long- and short-term debt rating to A3 and P-2respectively

• May 4, 2012, Outlook changed from Negative to Stable

Standard & Poor’s (A-/A-2)

• February 5, 2003, lowered long-term debt rating to A

• October 28, 2005, lowered long-term debt rating to A- and short-term debt rating to A-2

• July 2012, debt ratings confirmedOutlook: Stable

• February 5, 2003, lowered long-term debt rating to A

• October 28, 2005, lowered long-term debt rating to A- and short-term debt rating to A-2

• July 2012, debt ratings confirmedOutlook: Stable

Standard & Poor’s (A-/A-2)

• February 5, 2003, lowered long-term debt rating to A

• October 28, 2005, lowered long-term debt rating to A- and short-term debt rating to A-2

• July 2012, debt ratings confirmedOutlook: Stable

37

Dividend policy

• The company shall target a solid investment grade long-term credit rating (A- to BBB+) to secure the company’s strategically important financial flexibility for investments in future growth, both organically and by acquisitions

• The ordinary dividend shall be at least 50% of net income attributable to owners of the parent company

• Excess capital shall be returned to shareholders, after the Board of Directors has taken into consideration the company’s cash at hand, cash flow projections and investment plans in a medium term perspective, as well as capital market conditions

38

20

39

Forward-looking statements

Statements made in this document relating to future status or circumstances, including future performance and other trend projections are forward-looking statements. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There can be no assurance that actual results will not differ materially from those expressed or implied by these forward-looking statements due to many factors, many of which are outside the control of TeliaSonera.