q3 2013-14 investor presentation - lupin ltd. 2013-14 investor...safe harbor statement materials and...

TRANSCRIPT

LupinInvestor Presentation Q3FY14

Vision: To be an innovationled transnational company

Safe harbor statement

Materials and information provided during this presentation may contain ‘forward‐looking statements’.These statements are based on current expectations, forecasts and assumptions that are subject to risksand uncertainties which could cause actual outcomes and results to differ materially from thesestatements.

Risks and uncertainties include general industry and market conditions, and general domestic andinternational economic conditions such as interest rate and currency exchange fluctuations. Risks anduncertainties particularly apply with respect to product‐related forward‐looking statements. Productrisks and uncertainties include, but are not limited, to technological advances and patents attained bycompetitors, challenges inherent in new product development, including completion of clinical trials;claims and concerns about product safety and efficacy; obtaining regulatory approvals; domestic andforeign healthcare reforms; trends toward managed care and healthcare cost containment, andgovernmental laws and regulations affecting domestic and foreign operations.

Also, for products that are approved, there are manufacturing and marketing risks and uncertainties,which include, but are not limited, to inability to build production capacity to meet demand,unavailability of raw materials, and failure to gain market acceptance.

The Company disclaims any intention or obligation to update or revise any forward‐looking statementswhether as a result of new information, future events or otherwise.

Lupin today

Conversion rate: USD = INR 54.30

8th largest Market Cap amongst Global Generic Companies ~$5.7 billion

Revenues > $ 1.74 billion

Top 4 Pharmaceutical company in India

Secular growth across the geographies

Onshore presence in 10 countries (significant presence across 4 countries)

R&D expenditure @ 7.5% of net sales

Vertically integrated

12 manufacturing sites (5 US FDA approved) (2 sites in Japan)

Awards & accolades

NDTV Business Leadership Awards ‐ Pharma Company of the Year 2012

Lupin was ranked amongst top 2 pharma companies in the Great Place to

Work survey ‘Best Companies to work for 2013, India’ and amongst the

Top 50 companies overall

NSE included Lupin in the S&P CNX NIFTY index

Ernst & Young Entrepreneur of the Year 2011, for Life Sciences and Health

Care: Dr Desh Bandhu Gupta

Ernst & Young Family Business Award 2012: Ms. Vinita Gupta

CVS Caremark Supplier Partner Award winner ‐ Pharmacy Category for 2012

6,423 7,4399,981

12,00014,590

22,978

FY08 FY09 FY10 FY11 FY12 FY13

28,34137,950

47,73657,068

69,597

94,616

FY08 FY09 FY10 FY11 FY12 FY13

Evolved into a multinational company with >70 % of turnover from outside India

► 4th largest pharma company in India

► 5th largest and fastest growing generic player in the US by prescriptions

► 7th largest and the fastest growing generic player in Japan

Net Sales ‐ CAGR 27% EBITDA ‐ CAGR 29%

Consistent track record of growth

Figures in Rs. m

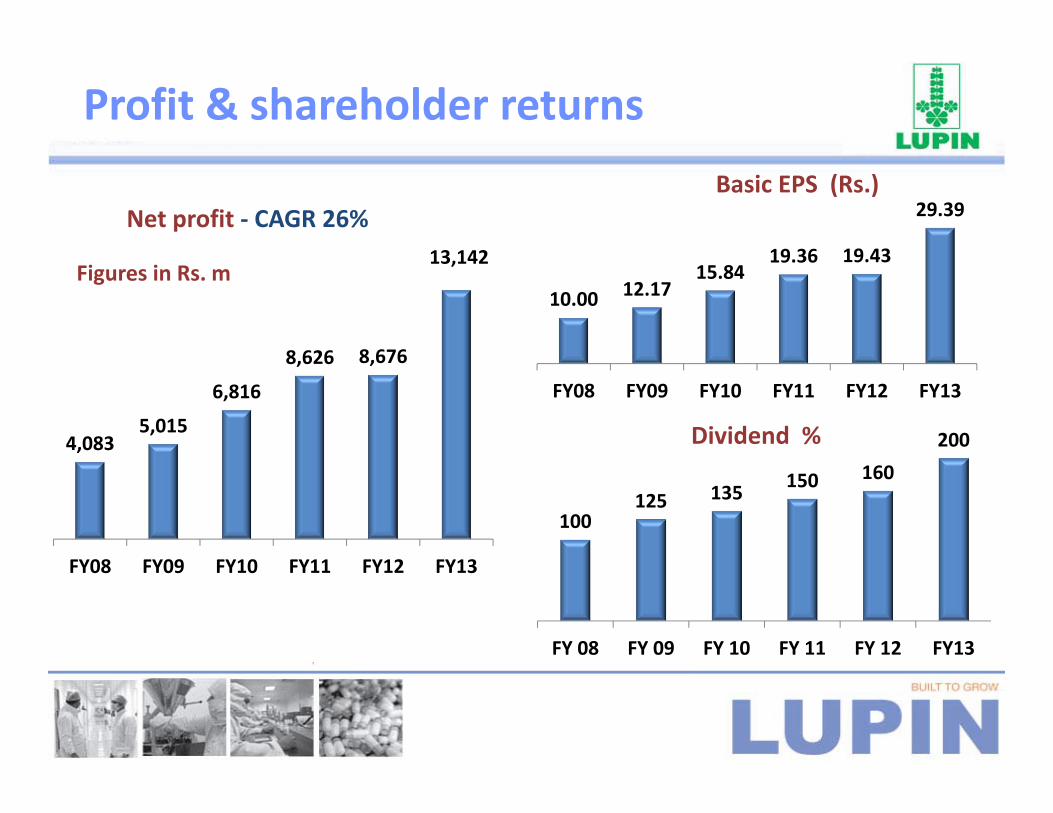

10.00 12.1715.84

19.36 19.43

29.39

FY08 FY09 FY10 FY11 FY12 FY13

Basic EPS (Rs.)

100125 135 150 160

200

FY 08 FY 09 FY 10 FY 11 FY 12 FY13

Dividend %

Profit & shareholder returns

4,0835,015

6,816

8,626 8,676

13,142

FY08 FY09 FY10 FY11 FY12 FY13

Net profit ‐ CAGR 26%

Figures in Rs. m

Major markets (Net sales)

Geographical breakup

Sales break up

US sales split

Business Mix – FY13

India 28%Outside

India 72%

API10%

Formulations90%

Brand21%

Generic79%

40%

2%25%

14%

3%

6% 10% US (including IP)

Europe

India

Japan

South Africa

Rest of world

API

69,243

80,351

9MFY13 9MFY14

Net Sales Rs. m

Corporate Highlights 9MFY14

Continued investment for growth

Capital expenditure at Rs. 3,639 m

Revenue expenditure on R&D 8.5% of net sales at Rs. 6,838 m

Filed 12 ANDA & received 19 approvals

Consistent performance:

Net sales grew by 16% to Rs. 80,351 m during9MFY14

PBT grew by 45% to Rs. 20,360 m during 9MFY14

US & Europe business (including IP) grew by 30%

South Africa grew by 19%

16,329

22,371

9MFY13 9MFY14

EBITDA Rs. m

9,061

12,834

9MFY13 9MFY14

Net Profit Rs. m

Q3FY14 performance

24,659

29,830

Q3FY13 Q3FY14

Net Sales Rs. m

Corporate Highlights Q3FY14

Continued investment for growth

Acquired Nanomi B.V. in Netherlands

Capex at Rs. 1,041 m

Revenue expenditure on R&D 9.1% of net sales at Rs. 2,710 m

Consistent performance:

Net sales grew by 21% to Rs. 29,830 m duringQ3FY14

PBT grew by 33% to Rs. 7,379 m during Q3FY14

US & Europe business (including IP) grew by 29%

South Africa grew by 18%

6,314

8,057

Q3FY13 Q3FY14

EBITDA Rs. m

3,352

4,761

Q3FY13 Q3FY14

Net Profit Rs. m

Major markets (Net sales)

Geographical breakup

Sales break up

US sales split

Business Mix – Q3FY14

25%

75%

India

Outside India

10%

90%

API

Formulations

11%

89%

Brand

Generic

45%

2%22%

13%

3%5%

10% US (incl. IP)

Europe

India

Japan

South Africa

ROW

API

Business update

10,988

14,228

Q3FY13 Q3FY14

Net sales (Rs. m)

United States & Europe

US business grew 31% to Rs. 13,567 m in Q3FY14 from Rs. 10,390 in Q3FY13 & contributed 45% to overall revenues

Brand business contributed 11% to US sales, while generics contributed 89%

5 products launched during the quarter

Current product portfolio of 62 products

No. 1 market share in 26 products & Top 3 market share in 44 products

Europe business grew 11% to Rs. 661 m in Q3FY14 from Rs. 598 m in Q3FY13 & contributed 2% to overall sales

Acquired Nanomi B.V. in Netherlands. Nanomi has patented technology platforms to develop complex injectable products.

Filed 5 ANDAs & received 5 approvals during the quarter

India

India formulations sales grew by 14% to Rs. 6,504 m during Q3FY14

9th largest Indian company in domestic market**

Launched 8 new products during the quarter

Field force strength +5,000 no.’s

Entered into strategic partnership with MSD to co –market MSD’s PPV in India

** Source : (AICOD AWACS MAT Dec 13)

23%

8%

10%

14%

15%

8%

4%

4%

14%

Therapy Mix CVS

Anti‐TB

Anti ‐ Asthama

Anti Biotics +Ceph Oral & Inj.

Anti Diabetic

GastroIntestinal (GI)

CNS

Gynaecology

Others

5,497

6,046

Q3FY13 Q3FY14

Net Sales (JPY m)

Japan & ROW

Q3FY14 Japan sales stands at Rs. 3,720 m

Strong presence in CNS, CVS, GI & Respiratory segments

Focus on improving I’rom overall business quality

Commercialization for products developed in India

Kyowa field force size increased from 95 to 114

Azithromycin, TS 1, Pitavastatin & Valacyclovir launched during the quarter

South Africa

4th largest Generic Pharma company

# 1 CVS player in South Africa

5 products registered during the quarter

Philippines

Ranked 28th as per IMS MAT Nov 2013

Growth of 23% vs. industry growth at 3%

Oncology division & 2 products launched

during the quarter

Australia

Launched Terbinafine during the quarter

Cost, quality and reliability are the cornerstones of our API

strategy

Strategic input into formulations business

Global leadership in chosen therapies

►Cephs

►Ceph‐intermediates

►Anti‐TB range

Achieved global cost, capacity and market share leadership in

most products

API and intermediates

Globally Integrated Research & Manufacturing network

Nagpur

R&D

1,359 1,546 2,318

3,570 4,834 5,228

FY07 FY08 FY09 FY10 FY11 FY12 FY13

R&D spends (Rs. m)

R&D expenditure Q3FY14 stands at Rs. 2,710 m, 9.1% of net sales

Talent pool of 1200+ scientists 186 ANDA filings, of which 96 have been

approved by the USFDA Filed 5 ANDA & received 5 approvals

during the quarter Increased focus on F2F

NDDD:►Pipeline of 10 programs in various phases of drug discovery

Bio‐similars:► Approval received for GCSF

(Filgrastim)► Pipeline of 10 drugs in various

phases of development

7,098

Highlights

Capex of Rs. 1,041 m during Q3FY14

Successful inspections of plants by various regulatory

agencies without critical observations:

USFDA : Tarapur, Dabhasa, Indore & Aurangabad

(Zero 483 in all inspections)

MHRA : Indore, Mandideep

TGA : Mandideep

ANVISA: Ankleshwar, Tarapur

MCC: Aurangabad

Frost & Sullivan in association with The Economic Times

conferred “Manufacturing Excellence Award”

Supply chain initiative rolled out to efficiently meet

global scale up & complexity challenges

Capabilities

10 manufacturing locations (2 in Japan)

housing 12 sites

► 5 API sites

► 7 formulation sites

5 FDA inspected sites

Manufacturing capabilities across tablets,

capsules, liquids, injectables and MDIs

Combined capacity of ~ 20b dosage units

Mihan formulation site for US commissioned

Sep’13

OCs launched in U.S. market from Indore

Investments in ‐ ophthalmology, derma and

inhalers

Globally integrated supply chain

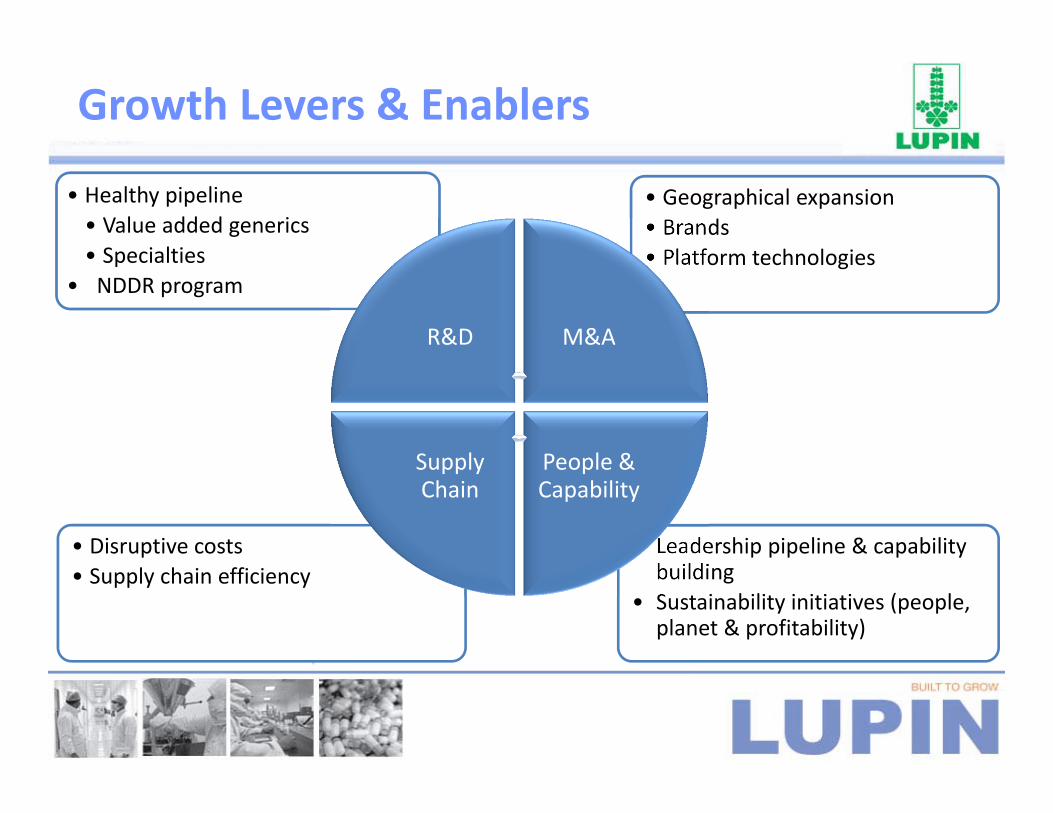

• Disruptive costs• Supply chain efficiency

• Geographical expansion• Brands• Platform technologies

• Leadership pipeline & capability building

• Sustainability initiatives (people, planet & profitability)

Growth Levers & Enablers

R&D M&A

People & Capability

Supply Chain

• Healthy pipeline• Value added generics• Specialties

• NDDR program

Thank You