q1-q3 2012 conference call - gfk · q1-q3 2012 conference call matthias hartmann, ceo ... financial...

TRANSCRIPT

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 1

Q1-Q3 2012 CONFERENCE CALL

Matthias Hartmann, CEO

Pamela Knapp, CFO

Nine months results conference call, 14 November 2012

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 2

Disclaimer

This presentation constitutes neither an offer nor recommendation to subscribe or buy in any other way securities of GfK SE or any

of the companies that are members of the Group at present or in the future, nor does it form part of such an offer and it should not be

understood as such. The presentation or any part thereof should not form the basis for a contract for the purchase or subscription of

securities of GfK SE or any of the companies that are members of the Group or represent a guarantee in connection with such

contract.

All the information contained in this presentation has been established with care. Nevertheless, we cannot guarantee its reliability or

completeness and the information contained herein should not be deemed as a guarantee in this respect.

The information contained in this presentation may be supplemented, amended and updated. Certain statements made herein may

express future expectations, which are based on current opinions and assumptions of the management and are subject to

foreseeable and unforeseeable risks and uncertainties. Actual results, performance and events may differ considerably from the

statements expressed in the present information, partly due to changing business or market conditions and to the growth prospects

forecast by the management of GfK SE. These and other factors may have an unfavorable impact on the results and financial

consequences described in this presentation. GfK SE does not undertake to update or revise statements on future developments, on

the basis of new information, future events or for other reasons. You should not rely on statements made about future

developments, which simply express expectations as of the date of this presentation.

This document does not constitute an offer of sale of securities in the United States of America. Securities may not be

offered or sold in the United States of America without registration or exemption from registration in accordance with the

U.S. Securities‘ Act of 1933 in its currently valid form.

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 3

1. Highlights of the reporting period

Matthias Hartmann, CEO

2. Financial Results Q1-Q3 2012

Pamela Knapp, CFO

3. Guidance

Pamela Knapp, CFO

4. Q&A

Matthias Hartmann, CEO

Pamela Knapp, CFO

Agenda

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 4

Highlights of the reporting period

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 5

Q1-Q3 2012

Q1-Q3 2011

Financial Highlights for the first nine months 2012

Sales

Total sales growth

Organic growth

Adjusted operating income

Margin1)

EBIT

EBITDA

Cash flow from operating activity

Basic earnings per share

EUR 998.5m

7.1%

7.0%

EUR 130.9m

13.1%

EUR 121.4m

EUR 163.4m

EUR 125.2m

EUR 1.80

EUR 1,096.8m

9.8%

2.2%

EUR 125.8m

11.5%

EUR 104.7m

EUR 147.6m

EUR 73.4m

EUR 1.31

1) Adjusted operating income in relation to sales

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 6

51.0 45.1

≤ -3.0

Sales growth in % for Q1-Q3 2012

Nine month growth 2012 in comparison shows strongest organic

growth momentum among key competitors

0.7 0.9

3.3

Organic growth is

analyst estimate.

9.8

2.2

6.7

Nielsen does not report

organic growth.

0.9 n/a

4.1

1) Consumer Insight segment isolated. WPPs Consumer Insight segment comprises of Kantar, TNS, Millward Brown, and The Futures Company, amongst others.

Total Organic At constant

FX rates

Total Organic At constant

FX rates

Total Organic At constant

FX rates

Total Organic At constant

FX rates

1)

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 7

53.2 44.5

≤ -1.0

Sales growth in % for Q3 2012

Business returned to organic growth in Q3 2012

-0.4 0.8

3.5

Organic growth is

analyst estimate.

11.3

3.2

7.3

Nielsen does not report

organic growth.

0.7 n/a

4.6

1) Consumer Insight segment isolated. WPPs Consumer Insight segment comprises of Kantar, TNS, Millward Brown, and The Futures Company, amongst others.

Total Organic At constant

FX rates

Total Organic At constant

FX rates

Total Organic At constant

FX rates

Total Organic At constant

FX rates

1)

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 8

Revenue growth of +11.3% in Q3

Organic growth of 18.5% in APAC, 9.4% in LATAM and 5.3% in

Southern & Western Europe and 5.7% in North America

o Flat organic growth in CEE

o Northern Europe is only region in decline, but reduced negative

development

Strong revenue growth momentum of 11.3%, of which

3.2% are organic growth

Strong

double digit

revenue growth

in Q3

User Centric acquisition complements SirValUse, creating global

coverage and Leadership in User Experience Consulting & Tracking Strengthening

Digital

Expanding in APAC through organic investment

• South Korea practice ramp & significant first wins

• Strong Leadership addition in China, Greater China, Singapore

and South East Asia

Expanding in Africa through GlobalEDGE acquisition

(FMGC data from 33 countries)

Expanding in

growth markets

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 9

Positive order intake Q3 momentum in Consumer Electronics

Good growth in IT and Stationery

Strong growth within Home & Lifestyle

Q3 wins and global product launches in Consumer Choices confirm

traction and logic of ‘Own the Future’ strategy

Retail Tracking

First NIS data available by year end from global framework contract

with major provider previously announced (two countries) Network

Intelligence

Solution (NIS)

Smart Steps/ Telefonica:

• Global framework contract signed with Telefonica

• Local contracts for product launch being finalized in the UK and

Brazil (for launch Q1 2013)

Successful LPS trial completed with a major US operator –

discussions in progress for commercialization in 2013

Live Population

Services (LPS)

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 10

Network Intelligence Solutions: GfK’s competitive advantages

Extraction Processing Reporting Enrichment Anonymisation Sales

GfK Network Intelligence Solutions transform Telco network data to deliver essential insights on

consumer behavior. This requires deep knowledge of end-to-end network systems and

communications platforms

• Network Intelligence Solution (NIS): IP traffic delivers insights on internet and mobile app

usage

• Live Population Services (LPS): mobile network data delivers location/ consumer journey

information

GfK is uniquely positioned versus other

market research companies through

deep understanding of network data and

the ability to offer our own network

“probes” for NIS.

GfK is uniquely positioned versus big data

analytical companies (incl. operators) by

our marketing science expertise, data

assets (e.g., panels) and trusted reputation

for delivering valuable consumer insights.

Our services will be

promoted across all

GfK vertical customer

sectors

Note: GfK may deliver different elements of this value chain within different operator partnerships

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 11

Microsoft Partnership:

• Double digit million order intake

• Global scale campaign tracking and cross media optimization for important

new product launch campaigns

• Complemented by a Brand Tracker in more than 40 markets

Global Tracker (86 countries/ 20 languages):

• Worldwide b2b satisfaction tracking program of a global telecommunications

equipment company out of the Emerging Asian markets

• Strong central management as well as local specialized field capacities were

crucial to win contract

Latin America: contract with a leading Telecom operator

• 3 year contract includes various types of research programs around the full

cycle of customer experience

Global contract wins in Consumer Experiences confirm GfK’s

strategic direction

Technology

China:

• One of the world leading healthcare companies, extending our relationship

with this client into China

• Investment strategy in Asia and healthcare crucial in winning contract from

competition

Healthcare

New global Brand and Customer Experience (BaCE) product launched: CBR

(Customer Brand Relationship)

• First wins from China Southern Airlines and Coca-Cola

Rollout of

BaCE offerings

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 12

Financial Results Q1-Q3 2012

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 13

Detailed group and sector figures for Q1-Q3 2012

In EUR m Sales Growth rate in % Operating Income Margin in %

Q1-Q3

2011 Q1-Q3

2012 Total Organic

Q1-Q3

2011 Q1-Q3

2012 Q1-Q3

2011 Q1-Q3

2012

Consumer

Choices 396.8 423.6 6.7 3.5 99.7 97.3 25.1 23.0

Consumer

Experiences 598.1 669.5 11.9 1.4 37.4 35.0 6.3 5.2

Other 3.6 3.7 2.8 1.3 -6.2 -6.6

Total 998.5 1,096.8 9.8 2.2 130.9 125.8 13.1 11.5

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 14

Main influences for operating margin development

Price/cost

(CH, S, NL,

F, POR,

CEE)

ERP

CC

business

ramp up

CE

business

ramp up

CC

depreciation

AM assets

Evogenius

impairment

Other

effects

-0,1% -0,7%

-0,2% -0,2% +0,4%

13,1%

-0,9%

11,5%

+0,1%

Q3

Ye

ar

To

Da

te

-0,4%

11,8%

-0,2% -1,1%

-0,1% -1,0%

-0,5% +1,2%

13,9%

Q3

Is

ola

ted

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 15

Regional growth

42.0 45.6

2011 2012

Latin America

146.9

196.8

2011 2012

North America

203.8 208.5

2011 2012

Southern and Western Europe

85.9 86.6

2011 2012

CEE and META

85.6

113.5

2011 2012

Asia and the Pacific

2011 2012

Northern Europe

+34.0%

Sales in EUR million for Q1-Q3 year on year

+2.4%

Total

Growth

Organic

Growth

+2.6%

-1.1%

0.9%

+1.0%

+8.7%

+10.1%

+2.3%

+2.3%

+32.5%

+16.0%

445.8 434.4

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 16

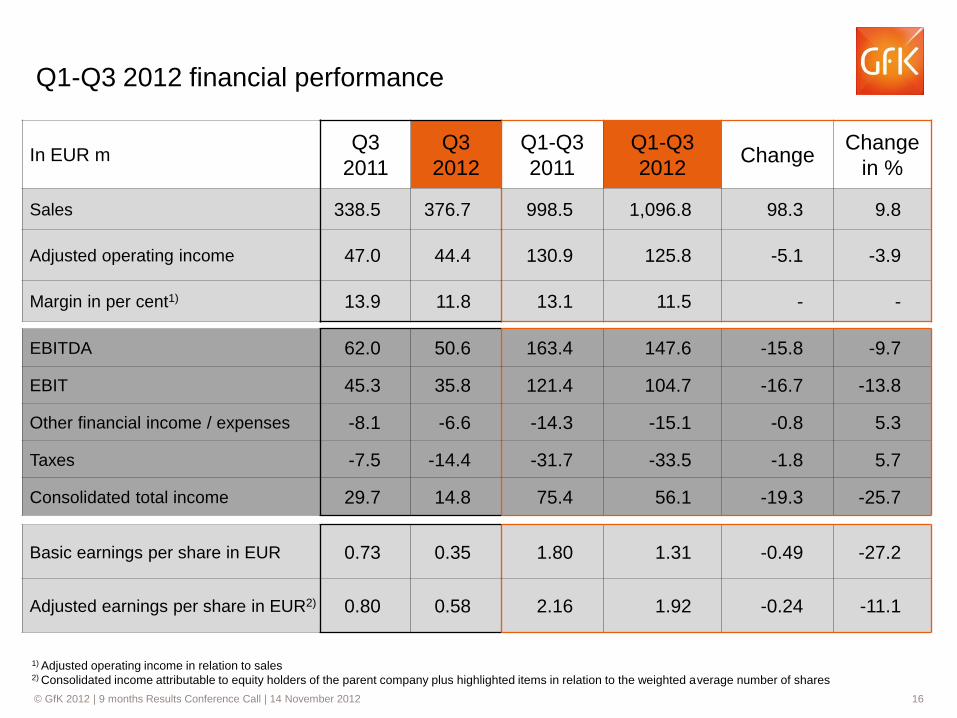

Q1-Q3 2012 financial performance

In EUR m Q3

2011

Q3

2012

Q1-Q3

2011

Q1-Q3

2012 Change

Change

in %

Sales 338.5 376.7 998.5 1,096.8 98.3 9.8

Adjusted operating income 47.0 44.4 130.9 125.8 -5.1 -3.9

Margin in per cent1) 13.9 11.8 13.1 11.5 - -

1) Adjusted operating income in relation to sales 2) Consolidated income attributable to equity holders of the parent company plus highlighted items in relation to the weighted average number of shares

EBITDA 62.0 50.6 163.4 147.6 -15.8 -9.7

EBIT 45.3 35.8 121.4 104.7 -16.7 -13.8

Other financial income / expenses -8.1 -6.6 -14.3 -15.1 -0.8 5.3

Taxes -7.5 -14.4 -31.7 -33.5 -1.8 5.7

Consolidated total income 29.7 14.8 75.4 56.1 -19.3 -25.7

Basic earnings per share in EUR 0.73 0.35 1.80 1.31 -0.49 -27.2

Adjusted earnings per share in EUR2) 0.80 0.58 2.16 1.92 -0.24 -11.1

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 17

Highlighted items for Q1-Q3 2012

In EUR m Q1-Q3

2011

Q1-Q3

2012 Change

Write-downs/write-ups of additional assets

identified on acquisitions -7.6 -8.6 -1.0

Income and expenses in connection with

share and asset deals 1.9 -1.0 -2.9

Income and expenses in connection with

reorganization and improvement projects -3.4 -6.8 -3.4

Personnel expenses for share-based incentive

payments -4.3 -3.2 1.1

Currency conversion differences 1.2 -2.1 -3.3

Income and expenses related to one-off

effects and other exceptional circumstances -0.8 -0.4 0.4

Highlighted items -12.9 -22.1 -9.2

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 18

Cash flow for the first nine months 2012

Free cash flow before acquisitions, other

investments and asset disposals 89.1 18.9 -70.2

In EUR m Q1-Q3

2011 Q1-Q3

2012 Change

Cash flow from operating activity 125.2 73.4 -51.8

Capital expenditure -36.1 -54.5 -18.4

Free cash flow after acquisitions, other

investments and asset disposals 82.4 -76.2 -158.6

Acquisitions -10.3 -95.9 -85.6

Other financial investments/ Asset disposals 3.6 0.8 -2.8

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 19

Capital Expenditure increase in Q1-Q3 2012

In EUR m Q1-Q3 2011 Q1-Q3 2012 Change

Intangible assets 21.3 23.8 2.5

including

-Software 16.8 19.3 2.5

-Panel 2.4 3.7 1.3

Tangible assets 14.8 30.7 15.9

including

-Real estate 0.0 7.8 7.8

-Other plant and equipment 14.5 19.5 5.0

Capital Expenditure 36.1 54.5 18.4

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 20

375 376

309

237

256

347

187

166

189

210 215

196

2008 2009 2010 2011 Q3 2011 Q3 2012

Net Debt in EURm (covenantdefinition)

EBITDA in EURm (covenantdefinition)

Net debt development

1) EBITDA and Net Debt are calculated according to bank covenant definition on rolling four quarter basis

2008 2009 2010 2011 Q3 2011 Q3 2012

Net debt headroom

in EUR m

233 162 305 446 442 290

Net debt/EBITDA 1)

covenant definition

2.01 2.27 1.63 1.13 1.19 1.77

Net debt/EBITDA

IFRS

2.51 3.14 2.19 1.63 1.65 2.23

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 21

Guidance

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 22

Guidance

Under the assumption that the FX ratios remain on a similar level as YTD, GfK expects for 2012

• EUR 1.5bn in sales which represents a total growth of around 9% year-on-year

• to achieve a margin (AOI to sales) between 12.2 and 12.7%

For 2015 we aim to achieve around EUR 2.0bn in sales and an AOI margin of 16.0%

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 23

Q&A

© GfK 2012 | 9 months Results Conference Call | 14 November 2012 24

THANK YOU