pwc’s insurance insights analysis of regulatory … · 0 1000 2000 3000 4000 5000 6000 7000 ......

TRANSCRIPT

PwC’s Insurance InsightsAnalysis of regulatory changes and impact assessment for May 2017

2 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017 Contacts

Updates on the insurance sector1

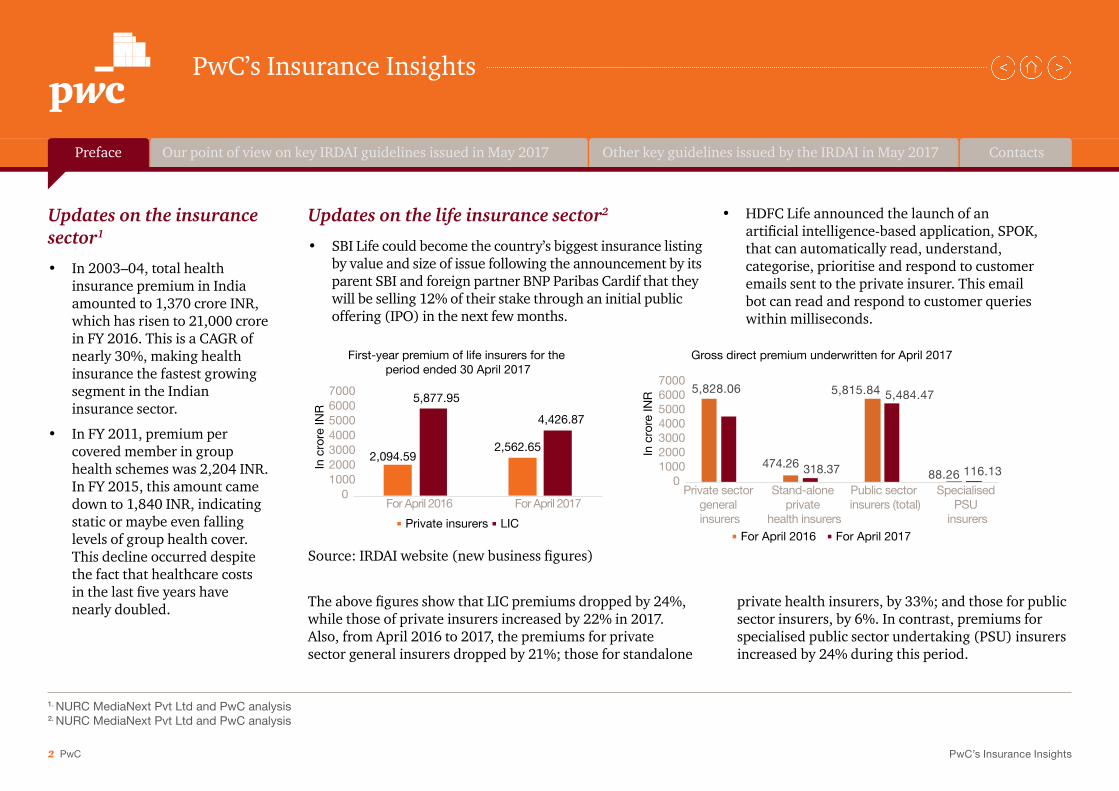

• In 2003–04, total health insurance premium in India amounted to 1,370 crore INR, which has risen to 21,000 crore in FY 2016. This is a CAGR of nearly 30%, making health insurance the fastest growing segment in the Indian insurance sector.

• In FY 2011, premium per covered member in group health schemes was 2,204 INR. In FY 2015, this amount came down to 1,840 INR, indicating static or maybe even falling levels of group health cover. This decline occurred despite the fact that healthcare costs in the last five years have nearly doubled. The above figures show that LIC premiums dropped by 24%,

while those of private insurers increased by 22% in 2017. Also, from April 2016 to 2017, the premiums for private sector general insurers dropped by 21%; those for standalone

Updates on the life insurance sector2

• SBI Life could become the country’s biggest insurance listing by value and size of issue following the announcement by its parent SBI and foreign partner BNP Paribas Cardif that they will be selling 12% of their stake through an initial public offering (IPO) in the next few months.

• HDFC Life announced the launch of an artificial intelligence-based application, SPOK, that can automatically read, understand, categorise, prioritise and respond to customer emails sent to the private insurer. This email bot can read and respond to customer queries within milliseconds.

1. NURC MediaNext Pvt Ltd and PwC analysis2. NURC MediaNext Pvt Ltd and PwC analysis

Source: IRDAI website (new business figures)

2,094.592,562.65

5,877.95

4,426.87

01000200030004000500060007000

For April 2016 For April 2017

In c

rore

INR

Private insurers LICFor April 2016 For April 2017

Private sector general insurers

Stand-alone private

health insurers

Public sector insurers (total)

Specialised PSU

insurers

5,828.06 5,815.84 5,484.47

88.26 116.13474.26 318.370

1000200030004000500060007000

In c

rore

INR

First-year premium of life insurers for the period ended 30 April 2017

Gross direct premium underwritten for April 2017

private health insurers, by 33%; and those for public sector insurers, by 6%. In contrast, premiums for specialised public sector undertaking (PSU) insurers increased by 24% during this period.

3 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017 Contacts

Updates on the general insurance sector3

• Travel insurance penetration in India is just 4–5%, which can go up to 70–80% once road transport is covered.

• Insurers are likely to increase their rates on property/fire insurance post-July, after the insurance regulator instructed them to peg the new rates to the Insurance Information Bureau’s (IIB) revised data.

• The new Motor Vehicle (Amendment) Bill, 2016, which has been passed by the Lok Sabha, will help the insurance industry cut its losses. The bill introduces specific timelines for faster processing of third-party insurance.

3. NURC MediaNext Pvt Ltd and PwC analysis

4 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017 Contacts

IRDAI circular reference:

Ref: F. No. IRDAI/Reg/5/142/2017 Date of notification: 6 May 2017

Preface Contacts

IRDAI (Outsourcing of activities by Indian Insurers) Regulations, 2017

Applicable entities: All insurers in India

Introduction:These regulations are applicable to outsourcing arrangements entered into by an insurer with an outsourcing service provider located in India or outside India.

Background and objective• To ensure that insurers follow

prudent practices on management of risks arising out of outsourcing with a view to preventing negative systemic impact and to protect the interests of the policyholders.

• To ensure sound and responsive management practices for effective oversight and adequate due diligence with regard to outsourcing of activities by Insurers.

Implications for insurersThe IRDAI has given a detailed classification of activities that can be outsourced.

• The Authority has defined core activities that are prohibited from being outsourced.

• Outsourcing activities that support policy servicing activities may be outsourced.

• Insurers can empanel only the entities defined in the guidelines as outsourcing service providers.

• Outsourcing arrangements shall be governed by written agreements that are legally binding for a specified period, subject to periodical renewals.

• The outsourcing service provider’s security policies, procedures and controls must enable the insurer to protect the confidentiality and security of policyholders’ information even after the contract terminates.

• Insurers shall establish and maintain adequate contingency plans with regard to disaster recovery plans and back-up facilities to support the continuation of an outsourced activity with minimal business disruption.

Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

5 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Contacts

Mandatory compliance by insurers• Board-approved outsourcing

policy: Insurers to have a board-approved outsourcing policy

• Outsourcing committee: Constitution of an outsourcing committee comprising key management persons

• Key risks: Evaluation of key risks by the outsourcing committee for any material outsourcing contract

• Implementation: Effective implementation of the outsourcing policy as approved by the board of directors

• Essential elements: The outsourcing policy to contain the essential elements as defined by the authority in the guidelines

• Conflict management: Conflict management policy to ensure adherence to the provisions on related party transactions as envisaged in the Companies Act,2013

• Annual review: Annual review of the summary of the outsourced activities of the insurer and approval of changes to the policy on the basis of the review report

• Annual review: Annual performance evaluation/due diligence of each of the outsourcing service providers and reporting of exceptions

• Periodic inspection: Periodic inspection or audit of the

outsourcing service providers either by internal auditors or a chartered accountant firm

• Legal and regulatory obligations: Compliance with these obligations as defined in the guidelines

• Related parties: Compliance with principles defined in the guidelines where outsourcing service providers are the related parties

• Record maintenance: Maintenance of records documentation for

five years from the end of the outsourcing contract

• Amendments to existing outsourcing agreements: Amendments to be made based on the applicability of these new regulations

• Annual filings: Reporting of annual payout if it is 1 crore INR or more every year within 45 days from the close of the financial year

Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

6 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

ContactsPreface

Sr. no. Guideline reference Particulars Impact

1 IRDA/INT/CIR/IMF/122/05/2017

Date of issue: 26 May 2017

Procedure to be followed to deal with resignation of insurance salespersons (ISPs) of insurance marketing firms (IMFs)

Background and objective

The IRDAI has issued the procedure that has to be followed to deal with the resignation of ISPs from IMFs.

Implications for IMFs

• The resignation of ISPs of IMFs shall be approved by a committee constituting of members nominated by the Life Insurance Council or General Insurance Council.

• The Authority has allotted states/UTs to the Life Insurance Council and General Insurance Council for receiving resignation requests from IMFs (Annexure A of the circular).

• The IMF, on receipt of a resignation, must forward it with the copy of its registration certificate either to the Life Insurance Council or General Insurance Council (as per the allocation defined in the circular).

• The Council will then forward the requests of ISPs to the committee, and the decision of the committee shall be communicated to the IMF under intimation to the Authority.

Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

7 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Contacts

Sr. no. Guideline reference Particulars Impact

2 F. No. IRDAI/Reg/7/144/2017

Date of issue: 22 May 2017

IRDAI (Insurance Surveyors and Loss Assessors) (First Amendment) Regulations

The IRDAI released an amendment to its regulations on insurance surveyors and loss assessors.Under this amendment, the Authority has emended various sections of the earlier master regulations.

Implication for insurers

Every insurer appointing surveyors/loss assessors shall ensure that the applicant has:

• Secured a degree or diploma from a recognised institute after attending a full-time course as a regular student or a part-time course with an equivalency certificate issued by the respective institute/university;

• Obtained a technical degree/diploma from

- All India Council for Technical Education (AICTE) approved institutions or - Universities recognised by the University Grants Commission or - Institutions of national importance recognised by the Ministry of Human Resources

Development (MHRD).

Mandatory compliance by insurers

Half-yearly report as per Form-IRDAI-19 to be submitted within 45 days from the end of the half year

3 IRDA/ACT/CIR/ULIP/113/05/2017

Date of issue: 5 May 2017

Revival option under discontinued unit-linked policies

For all life insurers

The Authority has provided a clarification on the revival option under discontinued unit-linked policies issued by life insurers.

Implications for insurers

When policyholders opt for complete withdrawal during the lock-in period or do not opt for revival within the lock-in period, the fund value should be payable to the policyholders at the end of the lock-in-period as per the provisions of the IRDAI (Treatment of Discontinued Linked Insurance Policies) Regulations, 2010, and clarifications issued thereon.

Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

8 PwC PwC’s Insurance Insights

Sr. no. Guideline reference Particulars Impact

4 IRDA/NL/GDL/F&U/109/05/2017

Date of issue: 3 May 2017

Classification of products

For all general insurance companies

The Authority mandates that all general insurers classify all existing products under two buckets—retail and commercial products.

Implications for insurers

• Classification of all products whether under the File and Use or Use and File procedures

• Products classified as both retail and commercial need to have a suitable name change, prefix or suffix, as the case may be, and need to have a separate unique identification number (UIN)

• Add-on covers to follow the basic product, its classification, and filing and approval procedures

• Add-on covers developed exclusively for commercial customers with a policy sum insured of above 5 crore INR under the products currently classified as retail products may be filed as per the Use and File procedure

Mandatory compliance

All insurers will resubmit the list of existing products being sold both as retail and commercial on or before 1 October 2017.

PwC’s Insurance Insights

ContactsPreface Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

9 PwC PwC’s Insurance Insights

Sr. no. Guideline reference Particulars Impact

5 IRDA/NL/MISC/PRO/115/05/2017

Date of issue: 9 May 2017

Guiding principles for pricing of risk

Fall all general insurance companies

The IRDAI advises the Product Management Committee (PMC) of insurers to put in place a mechanism to follow the prescribed process for fire/property risks before pricing a risk under commercial products under the Use and File procedure.

Implications for insurers

Based on the publication of the loss costs by the Insurance Information Bureau of India (IIBI), the IRDAI advises insurers to adopt the guiding principles.

• Premium rates to be determined based on the loss costs for fire line of business published by the IIBI

• Appropriate pricing to be set for natural catastrophe perils such as STFI (i.e. storm, tempest, flood, inundation and earthquake), if offered

• Insurer’s own experience on procurement, management cost and other relevant cost inputs to be factored in before arriving at the basic rate

• Technical justification to be offered in case the board allows the adoption of a loss cost lower than that published by the IIBI

Mandatory compliance by insurers

Insurers are required to arrive at the basic rate (which will be effective from 1 July 2017) that they would like to adopt for the various occupancies listed in IIBI’s report and maintain the information at their end in the format provided by the Authority.

PwC’s Insurance Insights

ContactsPreface Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

10 PwC PwC’s Insurance Insights

Sr. no. Guidelines reference Particulars Impact

6 IRDA/HLT/CIR/CSC/ 097/05/2017

Date of issue: 3 May 2017

Circular on offering existing health insurance products that are in compliance with IRDAI (Insurance Services by Common Service Centres) Regulations, 2015

For all general and health insurers

The Authority permits all general and health insurers to adopt the existing health insurance products by complying with the following conditions mentioned in the circular.

Mandatory compliance by insurers

• Filing of certificates in compliance with the product parameters of Common Service Centres (CSC) Regulations, 2015, as health CSC insurance products. The format has been prescribed in Annexure I of the circular.

• Insurers to incorporate the proposed CSC product along with the systems in place to service customers in the PMC

• Apart from the norms specified in the guidelines, the PMC will also examine other parameters defined in the circular before sign-off

• Changes to existing health products offered as health CSC products to be separately filed as per the regulation

PwC’s Insurance Insights

ContactsPreface Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

11 PwC PwC’s Insurance Insights

Sr. no. Guidelines reference Particulars Impact

7 Date of issue: 3 May 2017

Investments - Master Circular - IRDAI (Investment) Regulations, 2016

To enforce the IRDAI (Investment) Regulations, 2016, the Authority issued various circulars and guidelines at different times. This Master Circular covers all the circulars and guidelines that are effective to date and will serve as a one-stop reference guide for all investment-related activities.

Mandatory compliance by insurers

• Compliance to nature/categories of investments as defined by the IRDAI

• Certification by a chartered accountant firm for implementing investment risk management systems

• Concurrent audit of investment transactions on a quarterly basis

• Compliance with the valuation guidelines

• Reporting of repo transactions to the Investment Committee and board at least quarterly

• No part of investment function to be outsourced, investment being a core function

• Life insurers to obtain clearance for all new funds from the Investment Department of the IRDAI

• Compliance to reporting and disclosure norms as per the regulations

• Portfolio disclosure as defined by the IRDAI on a monthly basis before the 5th of the succeeding month

PwC’s Insurance Insights

ContactsPreface Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

12 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Contacts

Vivek Iyer Partner [email protected] Mobile: +91 9167745318

Dnyanesh Pandit Director [email protected] Mobile: +91 9819446928

Joydeep K Roy Partner [email protected] Mobile: +91 9821611173

Yugal Mehta Manager [email protected] Mobile: +91 9970163293

Our point of view on key IRDAI guidelines issued in May 2017 Other key guidelines issued by the IRDAI in May 2017

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 157 countries with more than 2,23,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com

In India, PwC has offices in these cities: Ahmedabad, Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata, Mumbai and Pune. For more information about PwC India’s service offerings, visit www.pwc.com/in

PwC refers to the PwC International network and/or one or more of its member firms, each of which is a separate, independent and distinct legal entity in separate lines of service. Please see www.pwc.com/structure for further details.

©2017 PwC. All rights reserved.

About PwC

pwc.inData Classification: DC0

This document does not constitute professional advice. The information in this document has been obtained or derived from sources believed by PricewaterhouseCoopers Private Limited (PwCPL) to be reliable but PwCPL does not represent that this information is accurate or complete. Any opinions or estimates contained in this document represent the judgment of PwCPL at this time and are subject to change without notice. Readers of this publication are advised to seek their own professional advice before taking any course of action or decision, for which they are entirely responsible, based on the contents of this publication. PwCPL neither accepts or assumes any responsibility or liability to any reader of this publication in respect of the information contained within it or for any decisions readers may take or decide not to or fail to take.

© 2017 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Private Limited (a limited liability company in India having Corporate Identity Number or CIN : U74140WB1983PTC036093), which is a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of which is a separate legal entity.

SUB/June2017-9861