pwc m&a 2014 review and 2015 outlook · pwc key messages – china m&a in 2014 (2 of 3) 6...

TRANSCRIPT

PwC M&A 2014 Review and 2015 Outlook

27 January 2015 David Brown, PwC China and Hong Kong Transaction Services Leader Christopher Chan, PwC China and Hong Kong Advisory Partner

PwC

Foreword – explanation of data shown in this presentation (1 of 2)

2

• The data presented is based on information compiled by ThomsonReuters, ChinaVenture and PwC analysis unless stated otherwise

• Thomson Reuters and ChinaVenture record announced deals. Some announced deals will not go on to complete

• The deal volume figures presented in this report refer to the number of deals announced, whether or not a value is disclosed for the deal

• The deal value figures presented in this report refers only to those deals where a value has been disclosed (referred to in this presentation as “disclosed value”)

• “Domestic” means China including Hong Kong and Macau

• “Outbound” relates to mainland China company acquisitions abroad

• “Inbound” relates to overseas company acquisitions of Domestic companies,

• “Private Equity deals” or “PE deals” refer to financial buyer deals with deal value over US$10mn and/or with undisclosed deal value, mainly invested by private equity GPs but also including direct investments by financial institutions and conglomerates which are of the nature of private equity type investing

PwC

Foreword – explanation of data shown in this presentation (2 of 2)

3

• “VC deals” refer to financial buyer deals with deal value less than US$10mn and/or with undisclosed deal, but invested by venture capital funds

• “Strategic buyer” refers to corporate buyers (as opposed to financial buyers) that acquire companies with the objective of integrating the acquisition in their existing business

• “Financial buyer” refers to investors that acquire companies with the objective of realizing a return on their investment by selling the business at a profit at a future date and mainly, but not entirely, comprise PE and VC funds

• In order to exclude foreign exchange impact, deal values from 2008 to 2012 were adjusted based on 2014 average Rmb/US$ exchange rate

PwC

Key messages

4

PwC

Key messages – China M&A in 2014 (1 of 3)

5

Overall

• China M&A surged by 55% in both volume and value terms to reach record levels in 2014

• Nearly all sub-sectors achieved new volume records - led by domestic strategic M&A which increased by nearly two thirds compared to the prior year

• Deals sizes were also bigger in nearly all sub-sectors – 2014 China M&A at US$407bn was more than half as much again as the previous high set in 2013

Domestic and Foreign-Inbound Strategic

• Strategic M&A surged 52% by volume and 63% by value to reach record highs; ongoing consolidation in China’s maturing domestic economy and firms seeking equity capital through reverse takeovers of listed shells were key drivers

• Technology, consumer-related and financial services deals were important industry sectors, reflecting to some extent the development of the broader economy, but real estate continued to attract the biggest dollar numbers with developers seeking new sources of capital

• Foreign-inbound strategic M&A also hit a record high in value terms with some sizable deals in banking and FS in particular

PwC

Key messages – China M&A in 2014 (2 of 3)

6

Private Equity

• Fundraising by PEs remained healthy, with the strongest US$ fundraise since 2008 and a slight uptick in Renminbi fundraising despite some disintermediation of domestic GPs

• 2014 was a banner year for new investments by PEs and financial-buyers with record volumes (up 51%) and values (up 101%); participation in SOE reforms and - for the first time at scale - outbound deals involving Chinese GPs and financial buyers underpinned this performance

• PE deals in technology and consumer-related sectors accounted for more than half the total reflecting investment plans intended to align with the strategic direction of the wider economy; a similar trend was seen in deal values: in total there were 15 PE / financial-buyer deals valued at more than US$1bn in 2014, another record

• Outbound investment by local PEs and financial buyers almost doubled in volume terms and outbound deal values also reached a record high; PEs typically look for overseas businesses which have a strong China-angle in their growth strategies

• As expected, there was a rebound in the number of PE exits; trade sale exits by M&A hit a record high, but IPO activity – although at a three year best - remains well below the levels seen in 2010/11

• A-share listings, although rebounding, nevertheless remain somewhat challenging and overseas listings in Hong Kong and New York are important exit routes

• The longer term overhang of new investments compared to exits continues to present a challenge to the PE industry

PwC

Key messages – China M&A in 2014 (3 of 3)

7

China Outbound

• The number of China outbound deals surged by more than a third to reach a record high; at US$56.9bn, outbound transaction values have been exceeded only once (in 2012) despite a lack of mega-deals

• There was strong outbound investment activity in all three sub-sectors, but M&A activity from privately owned enterprises continues to lead the way in terms of deal numbers with financial buyers and PEs making a meaningful contribution to the numbers for the first time

• SOEs continue to do deals in the industrials, resources and energy sectors; POEs are looking for technologies and brands to bring back to the China market; PEs and financial buyers have backed some of these strategic deals as well as investing on their own account

• Chinese buyers in particular tend to favour developed markets where advanced technologies and brands can be found

PwC

Overview

PwC

Volume Value Volume Value Volume Value Volume Value Volume Value Volume Value Volume Value

Strategic buyers (US$bn) (US$bn) (US$bn) (US$bn) (US$bn) (US$bn) (US$bn)

Domestic 3,006 150.4 2,774 101.9 2,947 143.9 3,262 120.8 2,667 90.3 2,704 149.2 4,180 243.6 55% 63%

Foreign 614 19.3 409 11.5 539 18.5 482 17.7 286 9.3 275 15.2 354 24.0 29% 58%

Total Strategic buyers 3,620 169.7 3,183 113.4 3,486 162.3 3,744 138.5 2,953 99.6 2,979 164.4 4,534 267.6 52% 63%

Financial buyers

Private Equity 369 22.0 264 22.8 434 27.0 529 41.0 358 34.3 392 36.4 593 73.2 51% 101%

VC 694 1.8 712 1.8 1,011 2.6 903 1.9 473 1.0 738 0.9 1,334 1.4 81% 63%

Total Financial buyers 1,063 23.8 976 24.6 1,445 29.5 1,432 42.9 831 35.3 1,130 37.2 1,927 74.6 71% 101%

China mainland Outbound

SOE 27 6.8 37 23.3 60 34.1 40 29.1 40 36.7 57 39.4 78 27.9 37% -29%

POE 95 2.0 97 6.3 119 6.8 139 6.2 125 19.9 118 11.4 145 14.7 23% 29%

Financial buyers 4 1.7 10 3.7 9 1.4 27 8.2 26 10.3 25 1.1 49 14.3 96% 1200%

Total China mainland Outbound 126 10.4 144 33.3 188 42.1 206 43.5 191 66.9 200 51.9 272 56.9 36% 10%

HK Outbound 156 6.7 152 6.3 171 19.4 183 8.5 166 13.1 164 9.7 215 22.4 31% 131%

Total 4,961 208.9 4,445 173.9 5,281 251.9 5,538 225.1 4,115 204.6 4,448 262.1 6,899 407.2 55% 55%

2010 2011 2012 2013 2014% Diff

volume

2014 vs.

2013

% Diff

value

2014 vs.

2013

20092008

9

Source: ThomsonReuters, ChinaVenture and PwC analysis

Total deal volume and value, from 2008 to 2014

China M&A surged by 55% in both volume and value terms to reach

record levels in 2014

*

*

* Some financial buyer backed outbound deals are also recorded in private equity deals, but they are not double counted in the total deal volume and deal value in the table above

PwC

3,006 2,774 2,947

3,262

2,667 2,704

4,180

614

409 539

482

286 275

354

369

264

434

529

358 392

593*

126

144

188

206

191 200

272*

-500

500

1,500

2,500

3,500

4,500

5,500

2008 2009 2010 2011 2012 2013 2014

Deal volume by main category

Domestic Strategic Buyers Foreign Strategic Buyers Private Equity Deals China Mainland Outbound

Nearly all sub-sectors achieved new volume records - led by domestic strategic M&A which increased by nearly two thirds compared to the prior year

10

Source: ThomsonReuters, ChinaVenture and PwC analysis

No.

* 49 financial buyer backed outbound deals are also recorded in private equity deals

PwC

Deals sizes were also bigger in nearly all sub-sectors – 2014 China M&A at US$407bn was more than half as much again as the previous high set in 2013

150.4

101.9 143.9

120.8 90.3

149.2

243.6

19.3

11.5

18.5

17.7

9.3

15.2

24.0

22.0

22.8

27.0 41.0

34.3

36.4

73.2*

10.4

33.3

42.1 43.5

66.9

51.9

56.9*

0

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011 2012 2013 2014

Deal value by main category

Domestic Strategic Buyers Foreign Strategic Buyers Private Equity Deals China Mainland Outbound

US$ billion

11

Source: ThomsonReuters, ChinaVenture and PwC analysis * US$14.3bn of financial buyer backed outbound deals are also recorded in private equity deals

PwC

Strategic buyers

12

PwC

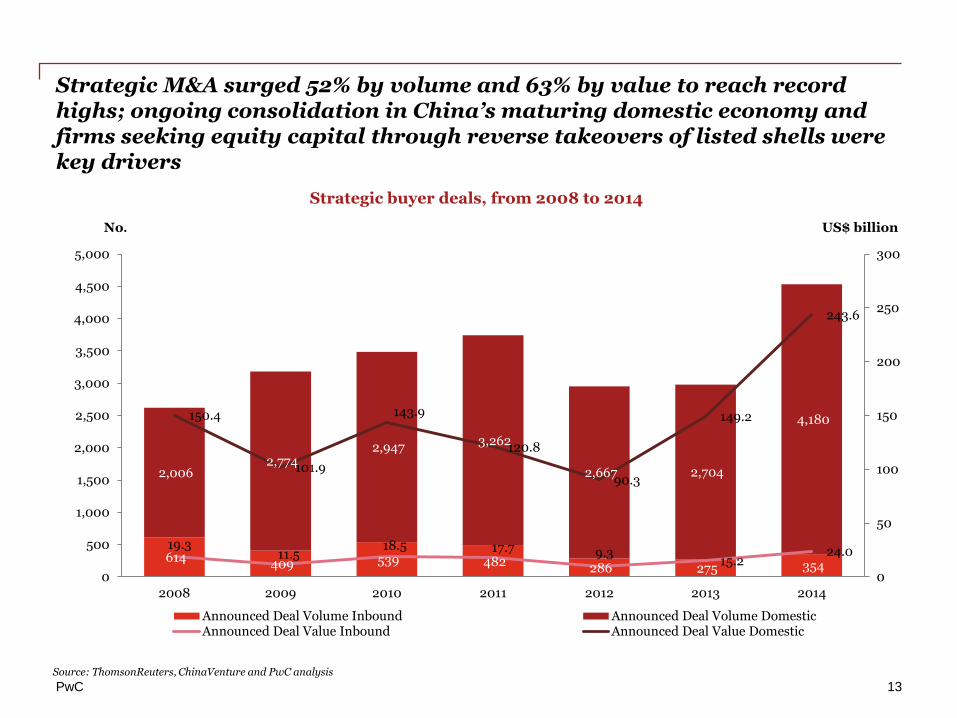

Strategic M&A surged 52% by volume and 63% by value to reach record highs; ongoing consolidation in China’s maturing domestic economy and firms seeking equity capital through reverse takeovers of listed shells were key drivers

614 409 539 482 286 275 354

2,006 2,774

2,947 3,262

2,667 2,704

4,180

19.3 11.5

18.5 17.7 9.3 15.2

24.0

150.4

101.9

143.9

120.8

90.3

149.2

243.6

0

50

100

150

200

250

300

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2008 2009 2010 2011 2012 2013 2014

Strategic buyer deals, from 2008 to 2014

Announced Deal Volume Inbound Announced Deal Volume DomesticAnnounced Deal Value Inbound Announced Deal Value Domestic

No. US$ billion

13

Source: ThomsonReuters, ChinaVenture and PwC analysis

PwC

Technology, consumer-related and financial services deals were important industry sectors, reflecting to some extent the development of the broader economy …

372 310 320 395 352 404 766

529 428 475

575 439 434

659 522 381 446

500 402 400

568 664

539 614

668

570 429

550 358

106 137

252

264 300

501 432

404 369

384

273 315

372 241

253 248

272

203 235

353

194

120 179

190

176 167

296

308

642

698

508

274 295

469

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2008 2009 2010 2011 2012 2013 2014

Strategic buyer deal volume by industry sector

High Technology Industrials Consumer Related Raw Materials Financial Services

Real Estate Energy and Power Healthcare Others

No.

14

Source: ThomsonReuters, ChinaVenture and PwC analysis

PwC

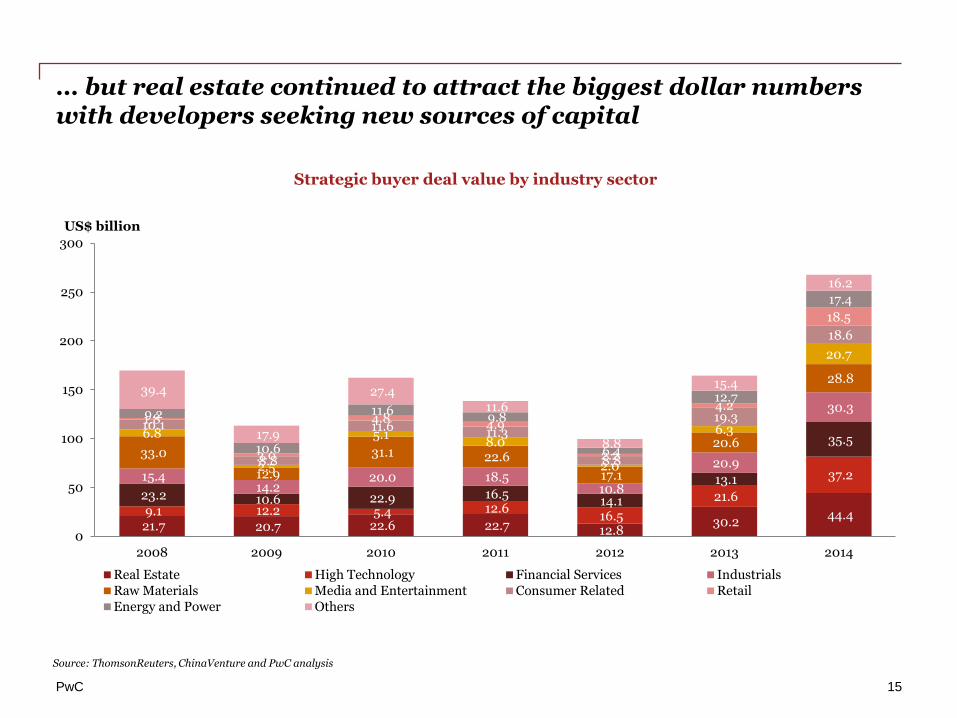

… but real estate continued to attract the biggest dollar numbers with developers seeking new sources of capital

21.7 20.7 22.6 22.7 12.8 30.2

44.4 9.1 12.2 5.4 12.6 16.5

21.6

37.2

23.2 10.6 22.9 16.5 14.1

13.1

35.5

15.4 14.2

20.0 18.5 10.8

20.9

30.3

33.0

12.9

31.1 22.6

17.1

20.6

28.8

6.8

2.5

5.1 8.0

2.0

6.3

20.7

10.1

8.8

11.6 11.3

8.8

19.3

18.6

1.8

3.0

4.8 4.9

2.2

4.2

18.5

9.2

10.6

11.6 9.8

6.4

12.7

17.4

39.4

17.9

27.4 11.6

8.8

15.4

16.2

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014

Strategic buyer deal value by industry sector

Real Estate High Technology Financial Services IndustrialsRaw Materials Media and Entertainment Consumer Related RetailEnergy and Power Others

US$ billion

15

Source: ThomsonReuters, ChinaVenture and PwC analysis

PwC

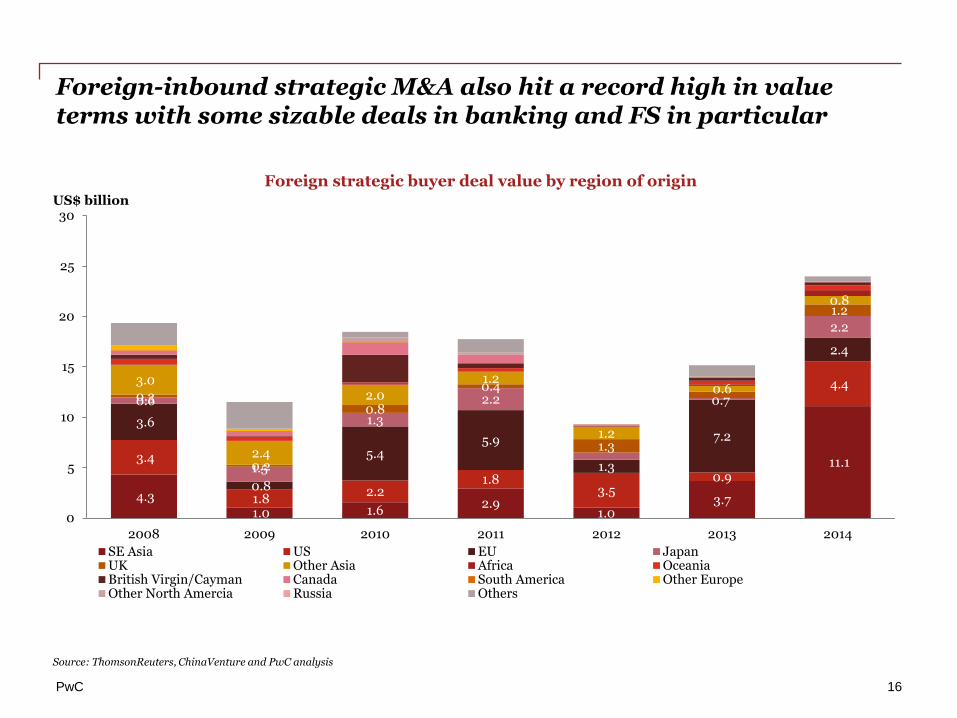

Foreign-inbound strategic M&A also hit a record high in value terms with some sizable deals in banking and FS in particular

4.3

1.0 1.6 2.9

1.0 3.7

11.1 3.4

1.8 2.2

1.8 3.5

0.9

4.4

3.6

0.8

5.4 5.9

1.3

7.2

2.4

0.6

1.5

1.3

2.2

2.2

0.3

0.2

0.8

0.4

1.3

0.7

1.2

3.0

2.4

2.0

1.2

1.2

0.6

0.8

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014

Foreign strategic buyer deal value by region of origin

SE Asia US EU JapanUK Other Asia Africa OceaniaBritish Virgin/Cayman Canada South America Other EuropeOther North Amercia Russia Others

16

Source: ThomsonReuters, ChinaVenture and PwC analysis

US$ billion

PwC

PE/VC deals and financial buyer deals

17

PwC

4.9 6.8

20.3

30.7

20.8

13.3 15.6

50.0

9.7

15.6

17.6

21.6

19.8

28.4

172

165

249

277

123 130

96

0

10

20

30

40

50

60

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014

PE/VC fund raising for China investment*

Renminbi Fund Size Non-renminbi Fund Size Fund Volume

No. US$ billion

Fundraising by PEs remained healthy, with the strongest US$ fundraise since 2008 and a slight uptick in renminbi fundraising despite some disintermediation of domestic GPs

18

Source: AVCJ and PwC analysis

* Excludes PEs investing in China from non-region specific funds

PwC

2014 was a banner year for new investments by PEs and financial-buyers with record volumes (up 51%) and values (up 101%); participation in SOE reforms and - for the first time at scale - outbound deals involving Chinese GPs and financial buyers underpinned this performance

369

264

434

529

358 392

593

22.0 22.8

27.0

41.0

34.3 36.4

73.2

0

10

20

30

40

50

60

70

80

0

50

100

150

200

250

300

350

400

450

500

550

2008 2009 2010 2011 2012 2013 2014

Private Equity deals, from 2008 to 2014

Announced Deal Volume Announced Deal Value

No. US$ billion

19

Source: ThomsonReuters, ChinaVenture and PwC analysis

PwC

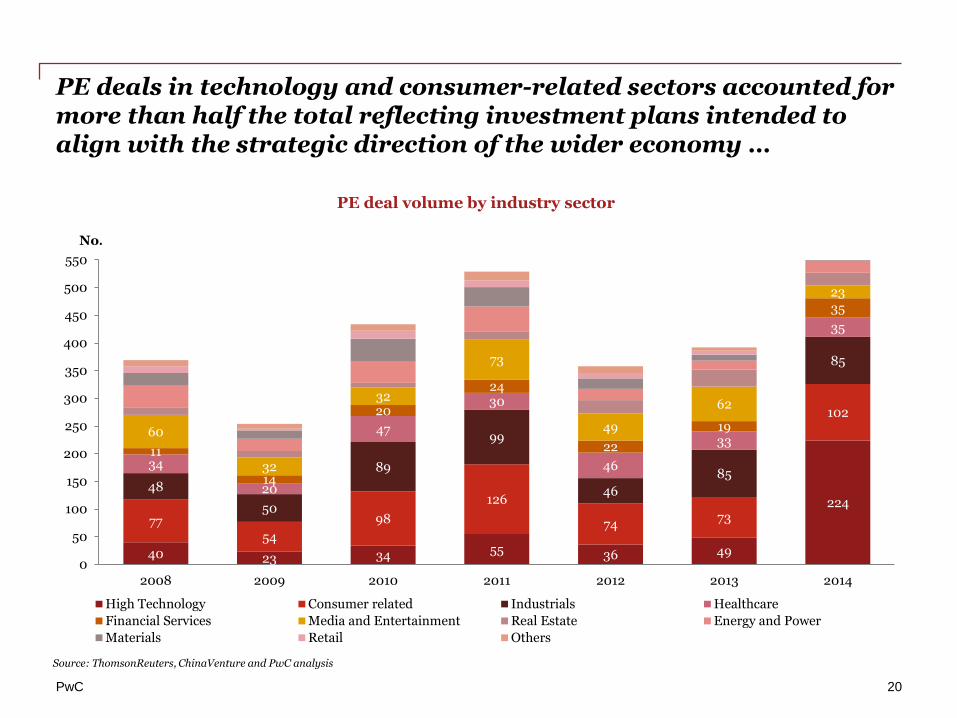

PE deals in technology and consumer-related sectors accounted for more than half the total reflecting investment plans intended to align with the strategic direction of the wider economy …

40 23 34 55 36 49

224

77 54

98

126

74 73

102

48

50

89

99

46

85

85

34

20

47

30

46

33

35

11

14

20

24

22

19

35

60

32

32

73

49

62

23

0

50

100

150

200

250

300

350

400

450

500

550

2008 2009 2010 2011 2012 2013 2014

PE deal volume by industry sector

High Technology Consumer related Industrials Healthcare

Financial Services Media and Entertainment Real Estate Energy and Power

Materials Retail Others

No.

20

Source: ThomsonReuters, ChinaVenture and PwC analysis

PwC

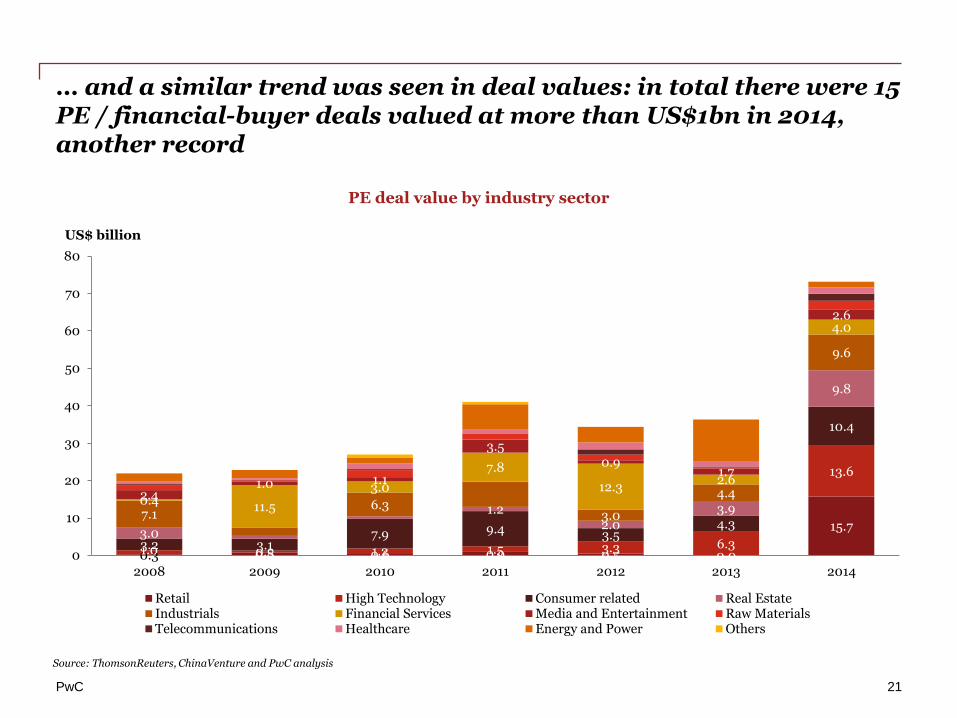

… and a similar trend was seen in deal values: in total there were 15 PE / financial-buyer deals valued at more than US$1bn in 2014, another record

0.3 0.8 0.6 0.9 0.5 0.0

15.7

1.0 0.5 1.2 1.5 3.3 6.3

13.6

3.2 3.1 7.9 9.4 3.5

4.3

10.4

3.0

1.2 2.0

3.9

9.8

7.1 6.3

3.0

4.4

9.6

0.4 11.5

3.0

7.8

12.3 2.6

4.0

2.4 1.0 1.1

3.5 0.9

1.7

2.6

0

10

20

30

40

50

60

70

80

2008 2009 2010 2011 2012 2013 2014

PE deal value by industry sector

Retail High Technology Consumer related Real EstateIndustrials Financial Services Media and Entertainment Raw MaterialsTelecommunications Healthcare Energy and Power Others

US$ billion

21

Source: ThomsonReuters, ChinaVenture and PwC analysis

PwC

Outbound investment by local PEs and financial buyers almost doubled in volume terms …

4 10 9

27 26 25

49

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014

China mainland PE/Financial buyer backed outbound deal volume

Financial buyers

22

Source: ThomsonReuters, ChinaVenture and PwC analysis

No.

PwC

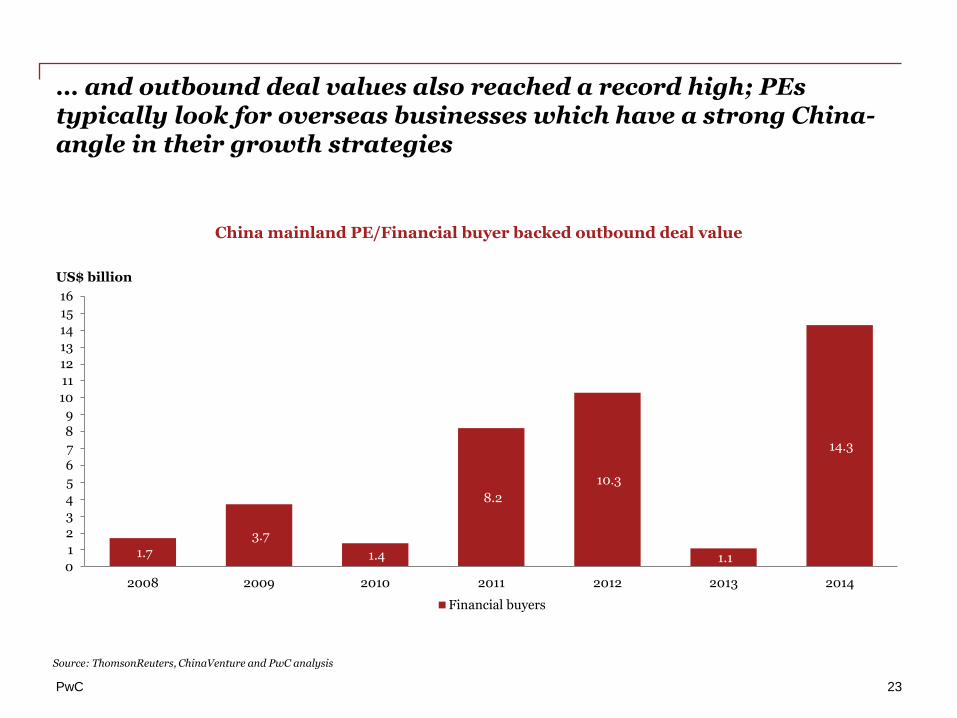

… and outbound deal values also reached a record high; PEs typically look for overseas businesses which have a strong China-angle in their growth strategies

1.7

3.7

1.4

8.2

10.3

1.1

14.3

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

2008 2009 2010 2011 2012 2013 2014

China mainland PE/Financial buyer backed outbound deal value

Financial buyers

US$ billion

23

Source: ThomsonReuters, ChinaVenture and PwC analysis

PwC

As expected, there was a rebound in the number of PE exits; trade sale exits by M&A hit a record high, but IPO activity – although at a three year best - remains well below the levels seen in 2010/11

46

88

212

171

98

35

114 44

84

83

91

92

85

111

7

5

8

6

8

6

7

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013 2014

PE/VC backed deal exit volume by type

IPO M&A - trade M&A - PE

24

No.

Source: AVCJ and PwC analysis

PwC

A-share listings, although rebounding, nevertheless remain somewhat challenging and overseas listings in Hong Kong and New York are important exit routes

21

48

118 106

70

-

45 12

27

39

26

11

29

38

2

-

11

18

11

-

17

4

7

30

11

2

6

13

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014

PE/VC backed IPO exit volume by bourse

Shenzhen Hong Kong Shanghai A NYSE/ NASDAQ Others

25

No.

Source: AVCJ and PwC analysis

PwC

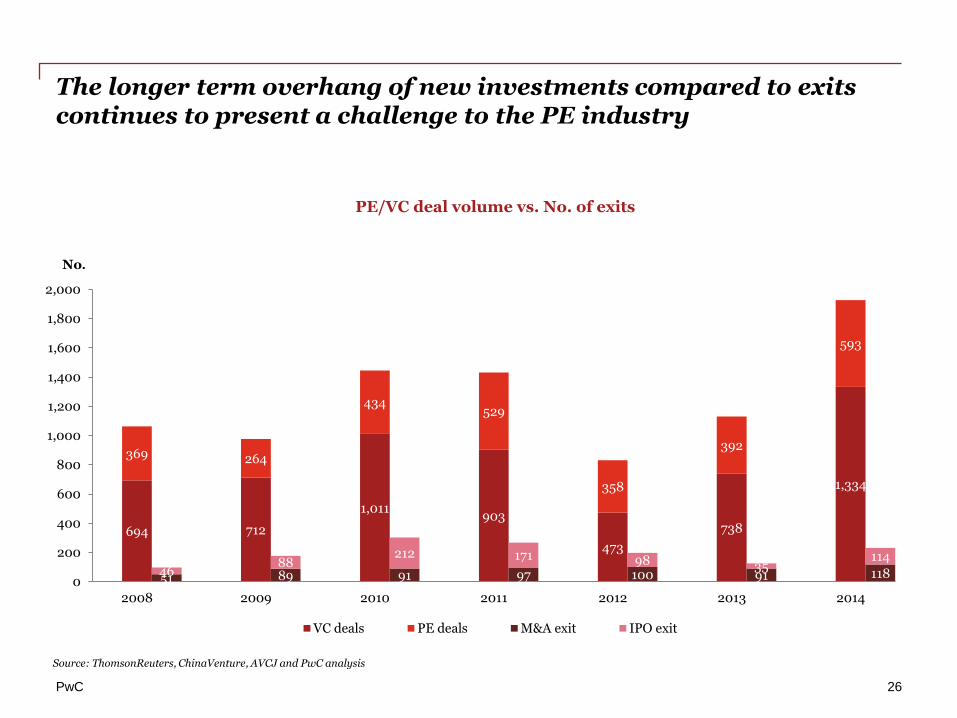

The longer term overhang of new investments compared to exits continues to present a challenge to the PE industry

26

694 712

1,011 903

473

738

1,334

369 264

434 529

358

392

593

51 89 91 97 100 91 118 46 88

212 171 98 35 114

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2008 2009 2010 2011 2012 2013 2014

PE/VC deal volume vs. No. of exits

VC deals PE deals M&A exit IPO exit

Source: ThomsonReuters, ChinaVenture, AVCJ and PwC analysis

No.

PwC

Mainland China outbound

27

PwC

The number of China outbound deals surged by more than a third to reach a record high; at US$56.9bn, outbound transaction values have been exceeded only once (in 2012) despite a lack of mega-deals

126 144

188 206

191 200

272

10.4

33.3

42.1 43.5

66.9

51.9 56.9

0

10

20

30

40

50

60

70

80

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014

China mainland outbound deals, from 2008 to 2014

Announced Deal Volume Announce Deal Value

No. US$ billion

28

Source: ThomsonReuters, ChinaVenture and PwC analysis

PwC

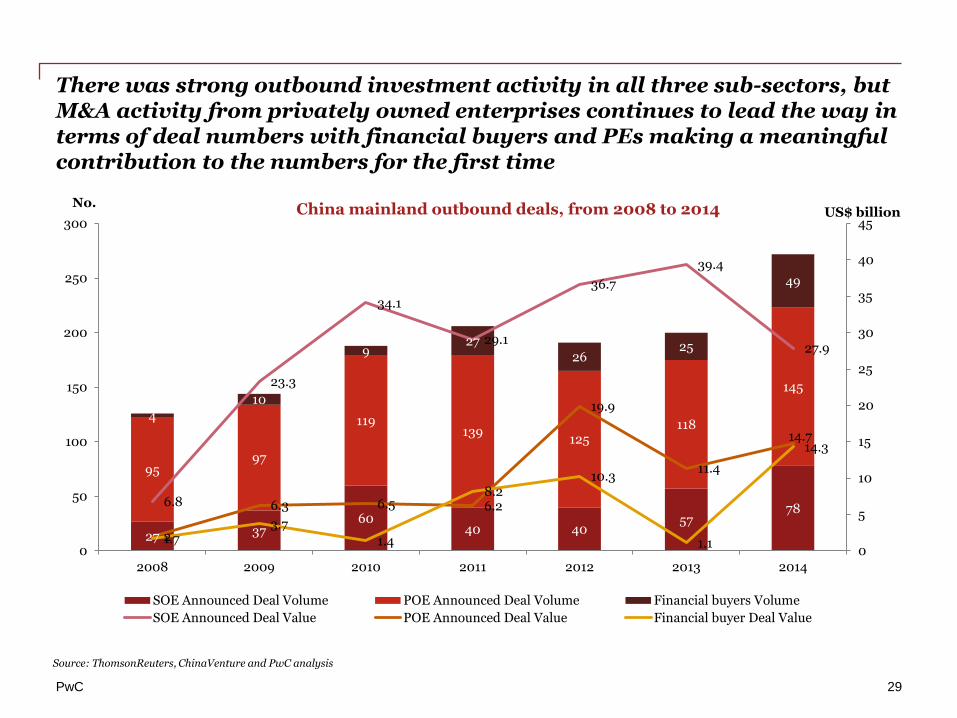

There was strong outbound investment activity in all three sub-sectors, but M&A activity from privately owned enterprises continues to lead the way in terms of deal numbers with financial buyers and PEs making a meaningful contribution to the numbers for the first time

29

Source: ThomsonReuters, ChinaVenture and PwC analysis

27 37 60

40 40 57

78

95 97

119 139

125 118

145

4

10

9 27

26 25

49

6.8

23.3

34.1

29.1

36.7

39.4

27.9

2

6.3 6.5 6.2

19.9

11.4

14.7

1.7 3.7

1.4

8.2 10.3

1.1

14.3

0

5

10

15

20

25

30

35

40

45

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014

SOE Announced Deal Volume POE Announced Deal Volume Financial buyers Volume

SOE Announced Deal Value POE Announced Deal Value Financial buyer Deal Value

China mainland outbound deals, from 2008 to 2014 No. US$ billion

PwC

SOEs continue to do deals in the industrials, resources and energy sectors; POEs are looking for technologies and brands to bring back to the China market; PEs and financial buyers have backed some of these strategic deals as well as investing on their own account

30

19 14

10 10 6 5

14

21

13

13 12 24

30

32

6

2

1 3

7

17

13

15 18

11 5 5

1 2

27 14

17

4

20

10

26

3

3

1

1

6

5

6

0

10

20

30

40

50

60

70

Industrials Energy and Power Raw Materials Financial Services Consumer related High Technology Others

2014 SOE 2014 POE 2014 Financial buyers 2013 SOE 2013 POE 2013 Financial buyers

China mainland outbound deals by industry sector

–By number of deals, 2014 vs. 2013

Source: ThomsonReuters, ChinaVenture and PwC analysis

No.

PwC

POEs and financial buyers in particular tend to favour developed markets where advanced technologies and brands can be found

Outbound M&A deal volume by region of destination 2014 vs. 2013

Source: ThomsonReuters and PwC analysis

31

33

North America

51 63

South America

Europe

Africa

Asia

Oceania

11 29 8

64

7

82 96

5 17

5

Russia

2014 2013

1

PwC

Outlook

32

PwC

Outlook for 2015 (1 of 5)

Overall

• The healthy trends in China M&A will continue into 2015

• Drivers for M&A activity include:

─ Growth in domestic M&A with SOE reform a key source of larger transactions

─ POE-led outbound M&A, with increasing involvement of PE and financial buyers

─ An active PE market, including exit-related activity

Key industry sectors

Technology, especially internet:

- The BAT group will continue to lead deal activities both domestically and outbound

- Hot sub-sectors include internet, eCommerce, media and semi-conductors

- M&A activity will be increasingly centred around mobile, location-based services and social networks, as well as opportunities around O2O

- We expect TMT to continue to be a hot sector in 2015

33

PwC

Outlook for 2015 (2 of 5)

Key industry sectors (continued)

Financial services:

- We anticipate inbound interest in P&C insurance (especially specialty insurance) and money lenders (leasing, micro-finance, guarantee companies) which are driven by the expected rapid growth in the SME and retail lending sectors

- With the fast evolving electronic media channel providing efficiencies in market coverage and customer analytics, we expect significant inbound and domestic interest in third party payment platforms and internet banking platforms

34

Retail and consumer:

- R&C generally is expected to be an active sector for M&A in 2015

- Active sub-sectors tend to be changeable, but we expect activity in the following areas

◦ Education

◦ Healthcare

◦ Restaurants

◦ Food related sectors including agriculture and businesses related to food quality and safety

◦ Technology, electrical, home appliance products

◦ Consumer targeted e-commerce

PwC

Outlook for 2015 (3 of 5)

35

Key industry sectors (continued)

Real estate:

- We expect M&A activity in real estate to be driven by a number of factors including group restructurings, back door listings to access capital, funding requirements, growth, etc

- Liquidity of developers will become more challenging

- We think more distressed assets will become available in 2015, especially in tier-2 and tier-3 cities

Healthcare:

- Healthcare sector is attracting investment from SOEs, POEs and PE, but less so from MNCs at this stage

- We expect investment interest in the full industry value chain of “Big Healthcare” with special focus on public and enterprise owned hospital

- There are some challenges, however, including:

◦ Longer investment return periods

◦ Defining sustainable business models

◦ Post deal management and exit

◦ The sensitive nature of the sector (policymakers must consider how to monitor and manage investments activities in order to balance economic interests with social responsibility and the interests of various stakeholders involved)

- We also expect to see some outbound activity around healthcare

PwC

Outlook for 2015 (4 of 5)

Domestic and Foreign-Inbound Strategic

• Domestic M&A will show steady single digit or low double digit growth driven by:

─ Continuing consolidation in many industries to remove excess or competitive capacity

─ SOE reforms – which will lead to some large transactions

─ A-share listed companies looking for inorganic growth

─ Back-door listings in response to difficulties in achieving new IPOs

• Technology (especially internet), FS, retail and consumer, and real estate are hot sectors; healthcare is also a focus, albeit smaller

China Outbound

• POEs will continue to lead double digit growth in China outbound chasing:

─ New markets for growth

─ Technologies, brands and know-how to bring back to China market

─ Diversified investments

• SOE outbound should also be strong as domestic reform plans work through

• SOEs in particular are increasingly building presence in Hong Kong as a platform for future outbound activity

• Financial investors and PEs will also drive growth in outbound M&A as a means to diversify investment portfolios, whilst usually seeking foreign companies with a China angle in their growth strategies

36

PwC

Outlook for 2015 (5 of 5)

Private equity

• PE activity will remain robust in 2015

• Trends in the market will include:

─ More larger sized deals and buyouts

─ PE involvement in outbound transactions

─ PE participation in SOE reforms as a source of diversified capital

─ Deals involving A-share listed companies, both as targets and as buyers of PE held assets (trade sale exit)

─ More exit activity from IPOs, strategic trade sales and – eventually – secondary PE sales

37

PwC

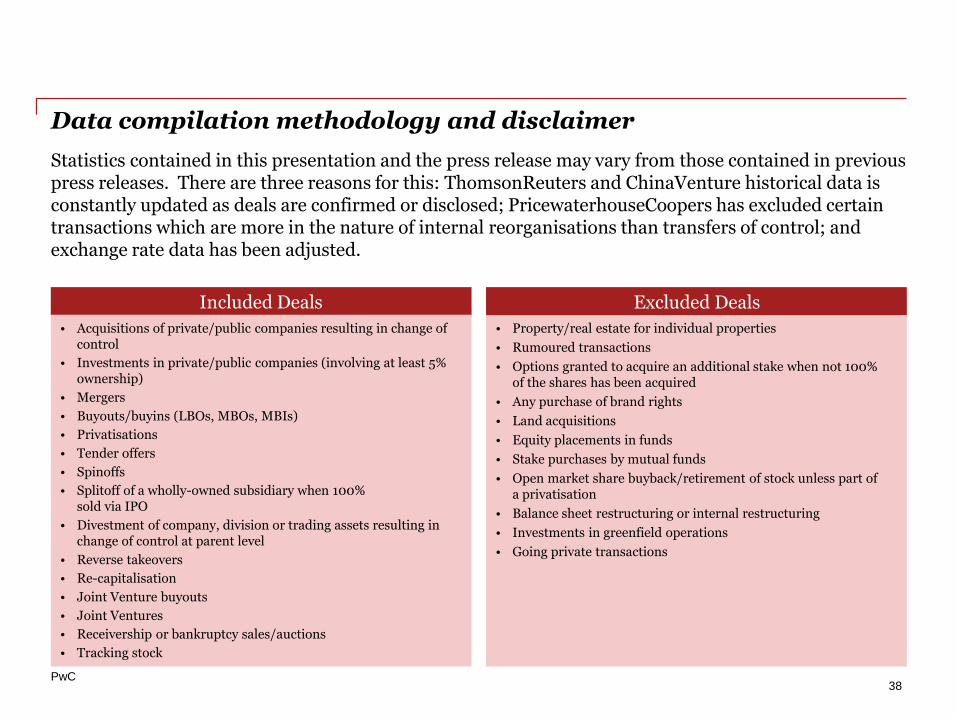

Data compilation methodology and disclaimer

Statistics contained in this presentation and the press release may vary from those contained in previous press releases. There are three reasons for this: ThomsonReuters and ChinaVenture historical data is constantly updated as deals are confirmed or disclosed; PricewaterhouseCoopers has excluded certain transactions which are more in the nature of internal reorganisations than transfers of control; and exchange rate data has been adjusted.

• Acquisitions of private/public companies resulting in change of control

• Investments in private/public companies (involving at least 5% ownership)

• Mergers

• Buyouts/buyins (LBOs, MBOs, MBIs)

• Privatisations

• Tender offers

• Spinoffs

• Splitoff of a wholly-owned subsidiary when 100% sold via IPO

• Divestment of company, division or trading assets resulting in change of control at parent level

• Reverse takeovers

• Re-capitalisation

• Joint Venture buyouts

• Joint Ventures

• Receivership or bankruptcy sales/auctions

• Tracking stock

• Property/real estate for individual properties

• Rumoured transactions

• Options granted to acquire an additional stake when not 100% of the shares has been acquired

• Any purchase of brand rights

• Land acquisitions

• Equity placements in funds

• Stake purchases by mutual funds

• Open market share buyback/retirement of stock unless part of a privatisation

• Balance sheet restructuring or internal restructuring

• Investments in greenfield operations

• Going private transactions

Included Deals Excluded Deals

38

Thank you

© 2015 PricewaterhouseCoopers. All rights reserved. "PricewaterhouseCoopers" refers to the Hong Kong firm of

PricewaterhouseCoopers or, as the context requires, the network of member firms of PricewaterhouseCoopers

International Limited, each of which is a separate and independent legal entity.