putting the permian basin in perspective: tight oil & the ... · all prices in constant july...

TRANSCRIPT

Slide1LabyrinthConsul4ngServices,Inc. artberman.com

Putting the Permian Basin in Perspective: Tight Oil & the Long-Term Debt Cycle

West Texas Geological Society 2017 Fall Symposium

Art Berman Labyrinth Consulting Services, Inc.

Midland, Texas September 27, 2017

Slide2LabyrinthConsul4ngServices,Inc. artberman.com

Pu>ngtheShaleRevolu4oninPerspec4ve

• The1stBubble1974-1980:oilshocksandpriceincreasefrom$23to$117/barrelledtomassiveE&Pinvestments,over-produc4on,demanddestruc4on&oil-pricedefla4onun4l1998.

• SecondBubble:1999-2014:flatglobaloutput&growingAsiandemandledtoincreasingoilpricesfrom$17to$148/barrelby2008.

• ATerthe2008FinancialCollapse,OPECcutproduc4onthen,decliningOPECsparecapacity,fallingOECDinventories,&near-zerointerestrates—ledtothelongestperiodofhighoilpricesinhistoryfrom2011-2014.

• Over-investmentresultedinamassiveover-supply,muchofitfromtheUnitedStates.• Thebubbleburstin2014andpricescollapsed.

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

Jan-12

Mar-12

May-12

Jul-1

2

Sep-12

Nov-12

Jan-13

Mar-13

May-13

Jul-1

3

Sep-13

Nov-13

Jan-14

Mar-14

May-14

Jul-1

4

Sep-14

Nov-14

Jan-15

Mar-15

May-15

Jul-1

5

Sep-15

Nov-15

Jan-16

Mar-16

May-16

Jul-1

6

Sep-16

Nov-16

MillionsofIn

crem

entalBarrelsofCrudeOil&CondensatePerD

ay

U.S.IncrementalOuput:TheMajorCauseForLowOilPrices

Iraq

Iran

RussiaBrazil

SaudiArabia

U.S.

Canada

KuwaitUAE

AngolaVenezuelaMexicoAlgeriaNigeriaBase

Libya

Indonesia-Ecuador-Qatar-Gabon

Source:EIA & LabyrinthConsulting Services,Inc.

Canada, Iraq,Iran SaudiArabia andRussiaAlsoImportantContributors

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

$160

Jan-70

Jan-71

Jan-72

Jan-73

Jan-74

Jan-75

Jan-76

Jan-77

Jan-78

Jan-79

Jan-80

Jan-81

Jan-82

Jan-83

Jan-84

Jan-85

Jan-86

Jan-87

Jan-88

Jan-89

Jan-90

Jan-91

Jan-92

Jan-93

Jan-94

Jan-95

Jan-96

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

CPIA

djustedWTIPrice

s(Ja

nuary2017DollarsPe

rBarrel)

Oil Shocks-->

Massive E&PInvestment(North

Sea,Mexico,Siberia)

Over-Supply, DemandDestruction&PriceDeflation

Debt-FueledEconomicExpansion&Rapid

GrowthinChina&EastAsia

MassiveE&PInvestment(Shale, DeepWater,Heavy

Oil)

Over-Supply, DemandDestruction&Price

Deflation

Current$50OilPrice>40%HigherThanJan1986- Dec2004AverageinJuly2017Dollars

Source:EIA, U.S.Bureau ofLaborStatistics &LabyrinthConsulting Services,Inc.

Avg1986-2004 $36/barrel Avg2005-2014$91/barrel

All PricesinConstant July2017Dollars

Avg1974-1985 $71/barrel<$23/barrel

$50/barrel

1stBubble:1974-1980

2ndBubble:1999-2014

$48/barrel

Slide3LabyrinthConsul4ngServices,Inc. artberman.com

OilPrices&TheLong-TermDebtCycle

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$0

$5

$10

$15

$20

$25

$30

$35

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

WTIPricein2016Do

llarsPerBarrel

U.S.G

ovennm

ent+

Consumer+Non-FinancialCorporateDebt(Trillions)

OilPrices2.4timesHigherAfter2004Than1986-2004In2016Dollars

Debt

GDP

Source:U.S.FederalReserveBank,U.S.Bureauof Labor Statiistics, WorldBank,EIA&LabyrinthConsulting Services,Inc.

Oil Price

Oil Shocks$69AvgPrice

$86AvgPrice

$34AvgPrice

Debt>GDPAfter1974-1986OilShocks

$23AvgPrice

$48$45/barrel1950-2016AvgPrice

Debt >GDPAfter1986

3.5

2.7

3.5

4.1

3.4

2.2

2.9

1.1

1.2

1.7

1.4

1.8

1.1

0.4

0.5

0.6

0.1

1.0

1.5

1.7

1.3

0.5

1.8

1.8

0.8

0.6

1.6

3.1

1.4

1.0

1.5

3.1

0.9

1.1

1.0

1.2

1.9

1.3

1.5

1.4

-0.8

-0.4

-1.3

-1.9

-1.5

-0.4

-0.2

-0.6

-1.0

-2.25 -2 -1.75 -1.5 -1.25 -1 -0.75 -0.5 -0.25 0

0.25

0.5

0.75

1

1.25

1.5

1.75

2

2.25

2.5

2.75

3

3.25

3.5

3.75

4

4.25

4.5

$0

$20

$40

$60

$80

$100

$120

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017E

2018E

AnnualLiquidsDemandGrowth(mmb/d)

CPI-AdjustedBrentPrice(December2016$/barrel)

NoDemandDestructionDuringThe2012-2016Oil-PriceCollapse

Source:IEA,EIA,OPEC, BP,U.S.BureauofLabor Statistics&Labyrinth Consulting Services,Inc.

PositiveDemandGrowth(RHS)

BrentPriceLHS(WTIbefore 1975)

NegativeDemandGrowth

(RHS)

1.2mmb/d30-YearAvg

• PetroleumAgeaTerWWIIproducedunprecedentedeconomicgrowth.• Oilshocksof1974-1986threatenedtoendthatparty.• Demanddestruc4on&oilproduc4onbubbleresultedin18yearsofcheapenergy.• Debtre-startedeconomicgrowth&debt-basedgrowthofChinachallengedoilsupplyaTer2004.• Secondoilshockmadeunconven4onaloilpossible.Zero-interestratesledto2ndoilbubble.• Longestperiodofhighoilpricesinhistory.• Thatbubbleburstin2014andoilpricescollapsedbutwithoutdemanddestruc4on.• Now,weareneartheendoflong-termdebtcyclebutdenyingthattheeconomicbasicshave

fundamentallychangedsincethepost-warera.

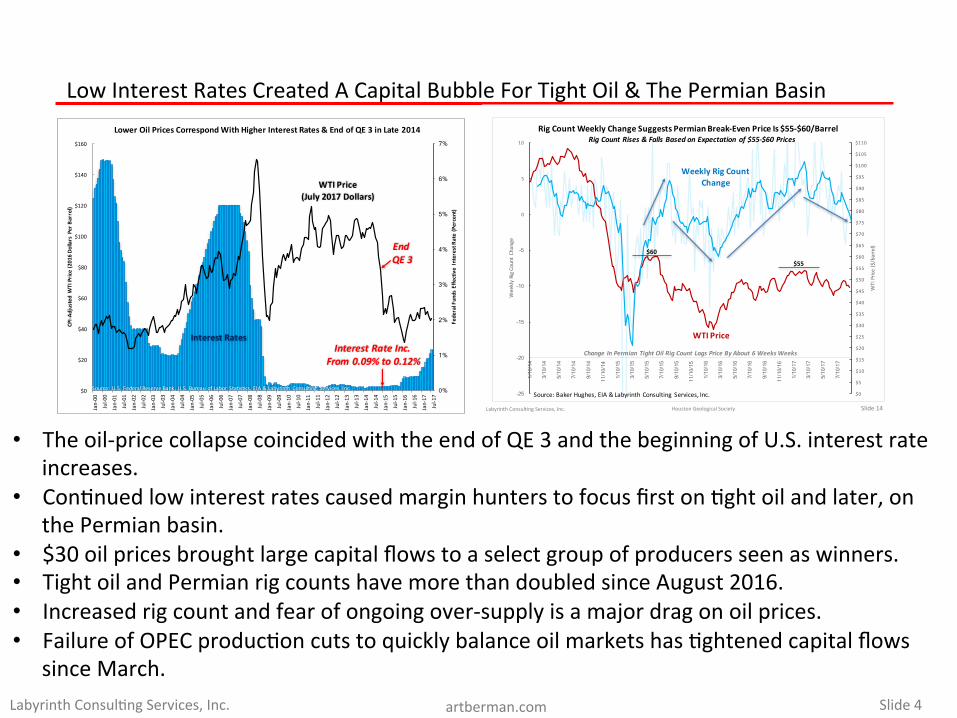

Slide4LabyrinthConsul4ngServices,Inc. artberman.com

LowInterestRatesCreatedACapitalBubbleForTightOil&ThePermianBasin

• Theoil-pricecollapsecoincidedwiththeendofQE3andthebeginningofU.S.interestrateincreases.

• Con4nuedlowinterestratescausedmarginhunterstofocusfirston4ghtoilandlater,onthePermianbasin.

• $30oilpricesbroughtlargecapitalflowstoaselectgroupofproducersseenaswinners.• TightoilandPermianrigcountshavemorethandoubledsinceAugust2016.• Increasedrigcountandfearofongoingover-supplyisamajordragonoilprices.• FailureofOPECproduc4oncutstoquicklybalanceoilmarketshas4ghtenedcapitalflows

sinceMarch.

0%

1%

2%

3%

4%

5%

6%

7%

$0

$20

$40

$60

$80

$100

$120

$140

$160

Jan-00

Jul-00

Jan-01

Jul-01

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Jan-14

Jul-14

Jan-15

Jul-15

Jan-16

Jul-16

Jan-17

Jul-17

FederalFundsEffe

ctiveInterestRate(Percent)

CPI-A

djustedWTIPrice(2016Do

llarsPerBarrel)

LowerOilPricesCorrespondWithHigherInterestRates&EndofQE3inLate2014

WTIPrice(July2017Dollars)

InterestRatesInterestRate Inc.

From0.09%to0.12%

EndQE3

Source:U.S.FederalReserve Bank,U.S.BureauofLabor Statistics,EIA&Labyrinth Consulting Services,Inc.

Slide14LabyrinthConsultingServices,Inc. HoustonGeologicalSociety

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

$100

$105

$110

-25

-20

-15

-10

-5

0

5

10

1/10/1

4

3/10/1

4

5/10/1

4

7/10/1

4

9/10/1

4

11/10

/14

1/10/1

5

3/10/1

5

5/10/1

5

7/10/1

5

9/10/1

5

11/10

/15

1/10/1

6

3/10/1

6

5/10/1

6

7/10/1

6

9/10/1

6

11/10

/16

1/10/1

7

3/10/1

7

5/10/1

7

7/10/1

7

WTIPrice($/barrel)

WeeklyRigCountChange

RigCountWeeklyChangeSuggestsPermianBreak-EvenPriceIs$55-$60/Barrel

$55

$60

Source:BakerHughes,EIA&LabyrinthConsultingServices,Inc.

Weekly RigCountChange

WTIPrice

Change InPermianTightOilRigCountLagsPriceByAbout6WeeksWeeks

RigCountRises&FallsBasedonExpectationof$55-$60Prices

Slide5LabyrinthConsul4ngServices,Inc. artberman.com

TheFalsePremisethatTightOilPlaysAretheNewSwingProducer:the“CallonShale”

• WidespreadbeliefthatU.S.shaleproduc4oncontrolsworldproduc4onsurplus—resultsinover-emphasisonU.S.rigcountasaleadingindicator.

• The“callonshale”thesis:just-in-4menatureofshalesupplymeansthatproduc4oncanstart&stopquicklybasedonpriceandinventorysignals.

• ImpliesthatU.S.shaleisthenewswingproduceroftheworldeffec4velyreplacingOPEC.• Beingaswingproducermeansthatthereissufficientsparecapacitytoturnonandoffbasedonmarket

signals.• The“callonshale”isaridiculousidea:thevolumeofshaleproduc4onchangecannotbecorrelatedtooilprice

orinventoriesaspromotersclaim.• Shaleoutputreactstopricejustlikeallplays—slowly&inlong-periodcycles.• Shaleplayshavenosparecapacity—theyarejust-in-4me.• Shaleproducerscannotevencontroloutputbecausetheyareconstrainedbycomple4oncrewsandcapital.• DUCsarenotsparecapacitybecausetheyarenotreadytoproduce.

$0

$20

$40

$60

$80

$100

$120

$140

$160

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan-03

Jun-03

Nov-03

Apr-04

Sep-04

Feb-05

Jul-05

Dec-05

May-06

Oct-06

Mar-07

Aug-07

Jan-08

Jun-08

Nov-08

Apr-09

Sep-09

Feb-10

Jul-10

Dec-10

May-11

Oct-11

Mar-12

Aug-12

Jan-13

Jun-13

Nov-13

Apr-14

Sep-14

Feb-15

Jul-15

Dec-15

May-16

Oct-16

Mar-17

WTIPrice($2017/barrel)

CrudeOil+CondensateProduction(m

mb/d)

The"CallonShale"ThesisisNotSupportedByPriceData

Permian

Bakken

Niobrara

EagleFord

GraniteWash

Miss.Lime

WTI(RHS)

Source:Drilling Info,EIA,LabyrinthConsulting Services,Inc.&Crude OilPeak700

750

800

850

900

950

1,000

1,050

1,100

1,150

1,200

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan-03

Jun-03

Nov-03

Apr-04

Sep-04

Feb-05

Jul-0

5 Dec-05

May-06

Oct-06

Mar-07

Aug-07

Jan-08

Jun-08

Nov-08

Apr-09

Sep-09

Feb-10

Jul-1

0 Dec-10

May-11

Oct-11

Mar-12

Aug-12

Jan-13

Jun-13

Nov-13

Apr-14

Sep-14

Feb-15

Jul-1

5 Dec-15

May-16

Oct-16

Mar-17

CrudeOil+

RefinedProducts(m

mb)

CrudeOil+

CondensateProduction(m

mb/d)

The"CallonShale"ThesisisNotSupportedByInventoryData

Permian

Bakken

Niobrara

EagleFord

GraniteWash

Miss.Lime

Inventories(RHS)

Source:Drilling Info,EIA,LabyrinthConsulting Services,Inc.&Crude OilPeak

Slide6LabyrinthConsul4ngServices,Inc. artberman.com

Howisthe“CallonShale”ConsistentWithFlatU.S.OutputSincetheOPECCut?

• U.S.oiloutputhasbeenflatsincetheOPECproduc4oncutsandhigheroilprices.• 43%ofU.S.supplyis4ghtoil.• Whereisthesurgeinjust-in-4meproduc4onfromthecallonshale?

9.63

8.55

9.07 9.13

9.11 9.17

9.09 9.24

9.19 9.

69 10.09

$0

$20

$40

$60

$80

$100

$120

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Jul-14

Aug-14

Sep-14

Oct-14

Nov-14

Dec-14

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-15

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May-18

Jun-18

Jul-18

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

WTIPrice($/Barrel)

MillionsofB

arrelsofCrudeOilPerD

ay

U.S.OutputHasBeenFlatin2017

April

2015

Source: EIASTEOSept2017&Labyrinth Consulting Services,Inc.

-1.08mmb/d

OilProduction

(LHS)

WTIPrice(RHS)

Aug2

017

Dec2

017

Sept

2016

Dec2

018

+0.89mmb/dAug2017-Dec2018

mmb/d Apr-15 Sep-16 Jun-17 Jul-17 Aug-17 Dec-17 Dec-18Production 9.63 8.55 9.09 9.24 9.19 9.69 10.09Since Apr-15 0.00 -1.08 -0.53 -0.39 -0.43 0.07 0.46Since Sep-16 0.00 0.55 0.69 0.65 1.15 1.54Since Jun-17 0.00 0.15 0.10 0.60 1.00Since Jul-17 0.00 -0.04 0.45 0.85

0

1

2

3

4

5

6

7

8

9

10

Jan-00

Jun-00

Nov-00

Apr-01

Sep-01

Feb-02

Jul-0

2 Dec-02

May-03

Oct-03

Mar-04

Aug-04

Jan-05

Jun-05

Nov-05

Apr-06

Sep-06

Feb-07

Jul-0

7 Dec-07

May-08

Oct-08

Mar-09

Aug-09

Jan-10

Jun-10

Nov-10

Apr-11

Sep-11

Feb-12

Jul-1

2 Dec-12

May-13

Oct-13

Mar-14

Aug-14

Jan-15

Jun-15

Nov-15

Apr-16

Sep-16

Feb-17

OilP

roduction

(mmb/d)

43%ofU.S.ProductionisTightOil

ConventionalOil

TightOil

Source:Drilling Info,EIA,LabyrinthConsulting Services,Inc.&Crude OilPeak

Slide7LabyrinthConsul4ngServices,Inc. artberman.com

ShaleCostReduc4onsMostlyIndustryBust,ThresholdForGrowth>$50WTI

• Lowercostsofshaleproduc4onwidelyanributedtotechnologyandefficiency.• Costcostdefla4onwas90%becauseofadepressionintheoilindustry,10%technology.• Thatisoverfornowandpriceshaveincreased8%in2017.• Rigcountdataindicatesthatexpecta'onof$55-$60isnecessaryfordrillinggrowth.• Drillingdoesnottranslateintoproduc4onbecauseofOFSlimita4ons.• Shalegrowthhasmoretodowithinvestormoneythanbreak-evenprices.• Investorsneedtobelievethatsignificantlyhigherpricesarecoming.• WTIisnotthepricethatproducersget.Discountis$5to$15/barrel.• CurrentBakkenwellheadpriceis$35.83butWTIis$50.00.

0

0.2

0.4

0.6

0.8

1

Dec-85

Sep-86

Jun-87

Mar-88

Dec-88

Sep-89

Jun-90

Mar-91

Dec-91

Sep-92

Jun-93

Mar-94

Dec-94

Sep-95

Jun-96

Mar-97

Dec-97

Sep-98

Jun-99

Mar-00

Dec-00

Sep-01

Jun-02

Mar-03

Dec-03

Sep-04

Jun-05

Mar-06

Dec-06

Sep-07

Jun-08

Mar-09

Dec-09

Sep-10

Jun-11

Mar-12

Dec-12

Sep-13

Jun-14

Mar-15

Dec-15

Sep-16

Jun-17

Norm

alize

dWTI&ProducerPrice

Index

TheCostofDrillingOilandGasWellsFell45%AfterTheOil-PriceCollapse;CostsHaveIncreased8%SinceJanuary2017

Source:U.S.Federal ReserveBank,EIA&LabyrinthConsulting Services,Inc.

WTIPrice

OIl&GasWell DrillingProducer PriceIndex

Source:U.S.Federal ReserveBank,EIA&LabyrinthConsulting Services,Inc.

4-FoldIncreaseinO&GPPI Because of

UnconventionalOil&Gas2004-2014 45

%Decrease

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

$100

$105

$110

$115

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Jul-1

4 Au

g-14

Sep-14

Oct-14

Nov-14

Dec-14

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-1

5 Au

g-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-1

6 Au

g-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-1

7 Au

g-17

Sep-17

WTIPrice($/Barrel)

TightO

ilHR

ZRigCountC

hange

TightOilRigCountsFallWhenExpectationsof$55-$60OilPricesFade

TightOilRigCount4-weekmovingaverage(LHS)

WTIPrice12-weekmovingaverage(RHS)

Source:BakerHughes,EIA&LabyrinthConsultingServices,Inc.

$60

$54

Change InHorizontal TightOilRigCount LagsPriceByAbout 8Weeks

Slide8LabyrinthConsul4ngServices,Inc. artberman.com

Compara4veInventoryRemainsTheMostUsefulIndicatorofFuturePriceTrens

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

$100

$105

$110

$115

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160 170 180 190 200 210 220 230 240 250

MostLikelyDecember2017C.I.Range40-75mmb$50-$56/barrelC.I.Decreased-3.5mmbThisWeek

Comparative Inventory (C.I.)Millionsof Barrels

WTIPrice($/barrel)

Source:EIA&La

byrinthConsultingServices,Inc.

$40

$55

Mar-June 2015Optimism

2014-2017Data Mid-cycle

price

Late 2015-Early2016Pessimisim(Cushing >

80%Capacity)

OPEC ProductionCutOptimism

Last Week

Most-LikelyDec.2017C.I.Range40-75mmb

$50-$56/barrel

Mid-FebSept15

$0

$20

$40

$60

$80

$100

$120

800

850

900

950

1,000

1,050

1,100

1,150

1,200

1/1/10 1/1/11 1/1/12 1/1/13 1/1/14 1/1/15 1/1/16 1/1/17

WTIPrice($/barrel)

IvnetoriesofCrudeOil+Products(m

mb)

InventoriesHaveFallenFromRecordLevels--ComparativeInventory,TheDifferenceBetweenInventories&The5-YearAverage,RemainsNearRecordPre-2015Levels

Source:EIA &LabyrinthConsulting Services,Inc.

5-YearInventoryAverage(LHS)

WTIPrice(RHS)

Inventories(LHS)

99mmbGap

97mmbGap

RecordInventoryLevel

• Compara4veinventory(C.I.)isthekeytounderstandingoilpricesandpoten4alfuturetrends.• TheoilpricecollapseresultedinthelargestincreaseininventoriesandC.I.onrecord.• C.I.hasfallen116mmbsincemid-Februarybutthegapbetweeninventories&the5-yearaverageis

s4llverylarge.• FlatyieldcurveofWTIvsC.I.—largedecreasesinC.I.donotcreatemeaningfulpriceincreases.• Most-likelyrangeofC.I.indicatespossibleyear-endWTIpricerangeof$50to$56/barrel.• ThisassumesthatC.I.willfall3.75mmb/week,theaverageforthelast30weeks.• Obviously,thismustbemonitoredforchangesthatwouldpoten4allyresultinhigherorloweryear-

endprices.

Slide9LabyrinthConsul4ngServices,Inc. artberman.com

StrongRefinedProductDemand&LowerNetImportsDriveInventoryReduc4ons

-100

-50

0

50

100

150

200

250

300

18.0

18.5

19.0

19.5

20.0

20.5

21.0

21.5

22.0

22.5

1/3/14

3/3/14

5/3/14

7/3/14

9/3/14

11/3/

14

1/3/15

3/3/15

5/3/15

7/3/15

9/3/15

11/3/

15

1/3/16

3/3/16

5/3/16

7/3/16

9/3/16

11/3/

16

1/3/17

3/3/17

5/3/17

7/3/17

9/3/17

CrudeOil+

RefinedProductsComparativeInventory(m

mb)

Csonum

ption(ProductSupplied)(m

mb/d)

2017AverageConsumptionAtRecordLevelsFellAfterGulfHurricanesButRecoveredAboveYTDAvgThisWeek

Consumption(LHS)

ComparativeInventory(RHS)

Source:EIA &LabyrinthConsulting Services,Inc.

4-WeekAvg

AnnualAvg

0

50

100

150

200

250

300

-4.5

-4

-3.5

-3

-2.5

-2

-1.5

-1

-0.5

0

1/1/16

1/1

5/16

1/29/1

6 2/1

2/16

2/26/1

6 3/1

1/16

3/25/1

6 4/8

/16

4/22/1

6 5/6

/16

5/20/1

6 6/3

/16

6/17/1

6 7/1

/16

7/15/1

6 7/2

9/16

8/12/1

6 8/2

6/16

9/9/16

9/2

3/16

10/7/

16

10/21

/16

11/4/

16

11/18

/16

12/2/

16

12/16

/16

12/30

/16

1/13/1

7 1/2

7/17

2/10/1

7 2/2

4/17

3/10/1

7 3/2

4/17

4/7/17

4/2

1/17

5/5/17

5/1

9/17

6/2/17

6/1

6/17

6/30/1

7 7/1

4/17

7/28/1

7 8/1

1/17

8/25/1

7 9/8

/17

CrudeOIl+ProductsCom

parativeInventories(m

mb)

NetP

etroleum

ProductImports(m

mb/d)

~4.2mmb/week(600kb/d)DecreaseinNetPetroleumProductImportsAccountForMostInventoryReductionsin2017

ComparativeInventory-113mmb

(RHS)

NetImportsAnnual Avg(LHS)

NetProductImports&Trendline

(LHS)

-2.0mmb/d

-2.5mmb/d

Source:EIA &LabyrinthConsulting Services,Inc.

ComparativeInventoriesHaveFallen116mmbSinceMid-February

FEB10

SEPT8

Netimportsincreased1.7mmb/dbecauseofHurricaneHarvey

NetimportsdecreasedtoYTD avg3rdweekafterHarvey

• Strongrefinedproductdemandandreducednetproductimportsaredrivinginventoryreduc4on.• 2017YTDconsump4onisatrecordlevels.• ItfellaTerthehurricanesbuthasrecoveredtoabovetheYTDaveragethisweek.• Netrefinedproductimportshavefallen600kbpd(4.2mmb/week)in2017.• Lowernetcrudeimports,andfallinggasolineanddis4llatestocksarethekeycomponents.

Slide10LabyrinthConsul4ngServices,Inc. artberman.com

HowEffec4veisOPEC-NOPECComplianceWithProduc4onCuts?

• LibyaandNigeriaarechiefOPECover-producers.• SaudiArabiahasalsoincreasedproduc4onsinceQ12017.• MaximumOPEC-NOPECproduc4oncutswereinMarchandApril2017.• Augustoutputwas1.3mmb/dlessthaninNovember2016vs.sanc4onedcutsof1.8mmb/d.

51

51.5

52

52.5

53

53.5

54

Nov-16 Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17

Increm

entalLiquidsProduction(m

mb/d)

MostRecentOPEC-NOPECIncreasesFromNigeria,Libya&SaudiArabia

Angola,Gabon,Algeria,Ecuador

Libya

Nigeria

UAE SaudiArabia

Kuwait

Base

Russia

Mexico

Source:EIASeptSTEO,EIAInternationalData&LabyrinthConsulting Services,Inc.

IraqVenezuela

Qatar

Iran

0.00

-0.27

-1.56

-1.72

-2.25 -2.21

-1.72

-1.41

-1.07

-1.28

50

50.5

51

51.5

52

52.5

53

53.5

54

54.5

-2.6

-2.4

-2.2

-2

-1.8

-1.6

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-1

7

Aug-17

LiquidsProduction(m

mb/d)

LiquidsProductionComparedWithNovem

ber2

016(m

mb/d)

OPEC-NOPECOnlyinComplianceWithProductionCutsInMarch&April2017

Source:EIASeptSTEO,EIAInternationalData&Labyrinth Consulting Services,Inc.

-1.8mmb/dThreshold

Slide11LabyrinthConsul4ngServices,Inc. artberman.com

OilFuturesHaveMovedIntoBackwarda4oninSeptember

• WTIhasmovedintofullbackwarda4onasoflastweek.• Brenthasalsomovedintobackwarda4on.• Thissignalsapercep4onofsupply4ghteningthatfavorssellingoilratherthanstoringit.

$44

$45

$46

$47

$48

$49

$50

$51

$52

$53

$54

Oct-17

Dec-17

Feb-18

Ap

r-18

Jun-18

Au

g-18

Oct-18

Dec-18

Feb-19

Ap

r-19

Jun-19

Au

g-19

Oct-19

Dec-19

Feb-20

Ap

r-20

Jun-20

Au

g-20

Oct-20

Dec-20

Feb-21

Ap

r-21

Jun-21

Au

g-21

Oct-21

Dec-21

Feb-22

Ap

r-22

Jun-22

Au

g-22

Oct-22

Dec-22

WTIFuturesPrice($/barrel)

WTIFuturesHaveMovedToBackwardationinSeptemberSignalingIncreasedSupplyTightening

Source:CME& LabyrinthConsultingServices,Inc.

Sept15

Sept20

Sept5

Sept26

$49

$50

$51

$52

$53

$54

$55

$56

$57

$58

$59

$60

Nov-17

Jan-18

Mar-18

May-18

Jul-1

8 Sep-18

Nov-18

Jan-19

Mar-19

May-19

Jul-1

9 Sep-19

Nov-19

Jan-20

Mar-20

May-20

Jul-2

0 Sep-20

Nov-20

Jan-21

Mar-21

May-21

Jul-2

1 Sep-21

Nov-21

Jan-22

Mar-22

May-22

Jul-2

2 Sep-22

Nov-22

Jan-23

Mar-23

May-23

Jul-2

3 Sep-23

Nov-23

Jan-24

Mar-24

May-24

Jul-2

4 Sep-24

Nov-24

BrentFuturesPrice

($/barrel)

BrentFuturesHaveAlsoMovedIntoBackwardation

Sept15

Sept20

Sept5

Source:CME& LabyrinthConsultingServices,Inc.

Sept26

Slide12LabyrinthConsul4ngServices,Inc. artberman.com

ReserveEs4mateUsing201610-KSECFilings(AnnualReports)

• EIA2015provedreserves:5billionbarrelsBakken,4.3bbEagleFord,0.8bbPermian.• Permianseemslow.• Es4mated~3.7billionbarrelsofprovedPermian4ghtoilreservesusing201610-KSECfilings

ofleadingoperatorsintheplays.• Allthecompaniesinthetabledifferen4atedPermianreservesfromothercompanyreserves.• Thosecompaniesaccountedfor47%ofall4ghtoilproduc4onin2016.Usedthatasascaling

factortoes4matethecontribu4onofcompanieslikeAnadarko,Apache,EOGandOXYthatdidnotseparatePermianfromothercompanyreservesintheir10-Kfilings.

• Thees4mateisfoundedonareliablebaseof1.7billionbarrelsfromcompanyfilings.Theassump4onthatundifferen4atedcompanyreserveswillfollow2016produc4onra4osisreasonablebutuncertain.

Permian2016ProvedOilReserves(kbo)

2016TightOilProduction(kbo)

PCTOFTotal2016Production

CONCHO 321,026 37,315 9.3%PIONEER 283,647 45,538 11.3%ENERGEN 199,575 10,468 2.6%LAREDO 167,100 9,146 2.3%RSPPERMIAN 164,700 11,040 2.7%DIAMONDBACK 139,174 14,892 3.7%PARSLEY 136,536 11,763 2.9%EP 81,800 3,973 1.0%DEVON 81,000 16,211 4.0%CIMAREX 74,300 17,920 4.5%CALLON 71,145 8,509 2.1%SUBTOTAL 1,720,003 186,776 47%TOTAL 3,696,999 401,459 100%

millionbarrels2014 2014 2015 2015

Production Reserves Production ReservesWilliston Bakken ND,MT,SD 387 5,972 421 5,030WesternGulf EagleFord TX 497 5,172 565 4,295Permian BoneSpring,Wolfcamp NM,TX 53 722 66 782Denver Niobrara* CO,KS,NE,WY 42 512 58 460Appalachian Marcellus* PA,WV 13 232 16 143FortWorth Barnett TX 9 47 5 33Sub-total 1,001 12,657 1,131 10,743Othertight 56 708 83 859U.S.tightoil 1,057 13,365 1,214 11,602

Basin Play State(s)

Table2.CrudeoilproductionandprovedreservesfromselectedU.S.tightplays,2014-15

Slide13LabyrinthConsul4ngServices,Inc. artberman.com

ShalePlays&SweetSpots($40CommercialAreas)

• Allthreeplayshaveconsiderablecommercialareasat$40wellheadprices.• BoneSpringcommercialareaisalmosttwiceaslargeasBakkenorEagleFord.• BoneSpringhas1/3thewelldensityoftheBakkenorEagleFord.• BoneSpringandEagleFordhavelowerbreak-evenEURthanBakken.• HigherearlyratesandlowerwellcostslargelyaccountforadvantagestoBoneSpringandEagleFord.

Slide14LabyrinthConsul4ngServices,Inc. artberman.com

TightOilProduc4onForecast

• Permianproduc4onshouldcon4nuetoincreaseintothemid-2020s.• EagleFordandBakkenwillprobablynotreach2015peakproduc4onlevels.• BakkenshoulddeclinemorethanEagleFord.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2

2.1

2.2

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

CrudeOil+

CondensateProduction(m

mb/d)

TightOilProductionForecast

Permian

EagleFord

Source:EIA&LabyrinthConsultingServices,Inc.

Bakken

Slide15LabyrinthConsul4ngServices,Inc. artberman.com

BakkenEUR,Gas-OilRa4os&WaterCutTrends

0

100

200

300

400

500

600

1 2 3 4 5 6 7 8 9 101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

OilP

roduction

(BarrelsofOilP

erDay)

MonthsofProduction

OilProductionDeclineRatesForRecentYearsAreGreaterThanForPreviousYearsForTop8BakkenProducers

2016

20152014

2013 2012

2016Declining FasterThanAllPreviousYearsDespiteHigherInitialRates

2015Declining FasterThanPreviousYears2014Declining FasterThanPreviousYears

Source:DrillingInfo& LabyrinthConsultingServices,Inc.

20%

25%

30%

35%

40%

45%

50%

55%

60%

1 2 3 4 5 6 7 8 9 10111213141516171819202122232425262728293031323334353637383940414243444546474849505152535455565758

PercentWater

MonthsofProduction

WaterCutIncreasedInTheLast3YearsForTop8BakkenProducers

2016 2015 2014

2013

2012

Source:DrillingInfo& LabyrinthConsultingServices,Inc.0

500

1,000

1,500

2,000

2,500

1 2 3 4 5 6 7 8 9 101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

Gas-OilRatio(CubicFeetPerBarrel)

MonthsofProduction

Gas-OilRatioIncreasesEveryYearForTop8BakkenProducers

2016

2015

2014 2013

2012

Source:DrillingInfo& LabyrinthConsultingServices,Inc.

• EURdecreased&declineratesincreasedforwellswith1stproduc4onaTer2013.• Gas-oilra4osincreased&thendecreased.• Watercutsincreasedforallwellswith1stproduc4onaTer2013.• Thesetrendssuggestdeple4onandthattheplayhasbeenover-drilled—notconclusivewithoutpressuredata.• Pioneer’sPermianbasinGORhasincreased28%sinceNovember2016.

0

500

1,000

1,500

2,000

2,500

1/1/12

3/1

/12

5/1/12

7/1

/12

9/1/12

11

/1/12

1/1

/13

3/1/13

5/1

/13

7/1/13

9/1

/13

11/1/

13

1/1/14

3/1

/14

5/1/14

7/1

/14

9/1/14

11

/1/14

1/1

/15

3/1/15

5/1

/15

7/1/15

9/1

/15

11/1/

15

1/1/16

3/1

/16

5/1/16

7/1

/16

9/1/16

11

/1/16

1/1

/17

3/1/17

5/1

/17

7/1/17

Gas-OilRatio(cubicfeet/barrel)

Pioneer'sPermianBasinGas-OilRatioHasIncreased28%SinceNovember2016

Source:DrillingInfo &LabyrinthConsultingServices,Inc.

Slide16LabyrinthConsul4ngServices,Inc. artberman.com

TightOilIsAMarginalBusinessAtBest

6.5

3.6

2.4

1.8 1.7 1.6 1.5 1.5 1.5 1.51.2 1.1 1.1 1.0 1.0 1.0

0.8 0.7 0.7 0.7 0.70.6 0.5

0

1

2

3

4

5

6

7

Parsley

Sanchez

Energen

Whitin

g

Hess

Carrizo

Laredo

Callon

Pion

eer

EPE

Oasis

New

field

Concho

EOG

Continental

Apache

Diamon

dback

Oxy

Chevron

Murph

y

Maratho

n

Cono

co

Statoil

FirstH

alf2

017RatioofC

apitalExpenditurestoCashFrom

Operations

TightOilIsaMarginalBusinessAtBestMostCompanies LoseMoneyorBreakEven

OnlyIntegratedCompanies&DiamondbackMadeMoneyin2017

MakeMoneyBreakEven

Lose Money

Source:GoogleFinance&LabyrinthConsultingServices,Inc.

• Despiteclaimsofever-decreasingcostsandbreak-evenprices,companybalancesheetsandincomestatementsdonotreflectprofitabilityformostpure4ghtoilplayers.

• Amongkey4ghtoil-weightedcompanies,mostlosemoney.• Afewbreakeven.• Onlyintegratedcompanieswithdiversifiedporwoliosoutsideof4ghtoilplays(e.g.,Chevron,ConocoPhilips,

Statoil,Oxy)makemoney.• Diamondbackistheonlypure4ghtoilplayerthatmademoneyin2017.• Thedisparitybetweenbreak-evenandIRRclaims,andcorporatefinancialdata:

Ø Selec4vedatainclaimsvs.averagewellEURandcosts.Ø Exclusionofmanycostsinclaimsthatarepartofthecostofdoingbusiness.Ø Misleadingemphasisonproduc4oncostsvsfullcosts.

Slide17LabyrinthConsul4ngServices,Inc. artberman.com

30

35

40

45

50

55

60

100105110115120125130135140145150

12-Sep-16

12-Oct-16

12-Nov-16

12-Dec-16

12-Jan-17

12-Feb-17

12-M

ar-17

12-Apr-17

12-M

ay-17

12-Jun

-17

12-Jul-17

12-Aug-17

Concho

Close WTI

30

35

40

45

50

55

60

120130140150160170180190200210

12-Sep-16

12-Oct-16

12-Nov-16

12-Dec-16

12-Ja

n-17

12-Feb-17

12-M

ar-17

12-Apr-17

12-M

ay-17

12-Ju

n-17

12-Ju

l-17

12-Aug-17

Pioneer

Close WTI

9/9/17, 6(51 PMEnergy Shares Set for Worst Month Since 2015 - WSJ

Page 2 of 4https://www.wsj.com/articles/energy-shares-set-for-worst-month-since-2015-1503846001?mg=prod/accounts-wsj

rise, bolstered by an agreement by the Organization of the PetroleumExporting Countries and other major producers to curb output.

But such shares lost much of their appeal this year when oil pricesstarted to fall again, even as earnings have generally improved off

a low base. U.S. crude prices are down 11% this year and arelanguishing below $50 a barrel.

About $2.7 billion has flowed out of energy-focused stock funds for theyear through July, according to data from Morningstar, after roughly$5.8 billion flowed in last year.

Analysts and investors pointed to quarterly reports from companiesincluding Pioneer Natural Resources Co. as key contributors to thesector’s sagging stock prices this month.

Some companies talked about not hitting production levels, which“spooked a lot of investors,” said Terry Simpson, a multiassetinvestment strategist at BlackRock.

Pioneer cut its production-growth guidance after running into drillingproblems that caused delays. Shares of Pioneer fell 11% Aug. 2, eventhough it reported a higher profit that beat analysts’ expectations.Pioneer is down 28% for the year, with most of that decline coming inAugust.

Investors are yanking money from energy funds after three years of inflows.Estimated net flows into and out of U.S. energy stock funds

THE WALL STREET JOURNALSource: MorningstarNote: All data are full-year except 2017, which is through July.

.billion

2012 ’13 ’14 ’15 ’16 ’17

-4

-2

0

2

4

6

8

$10

30

35

40

45

50

55

60

80

85

90

95

100

105

110

12-Sep-16

12-Oct-16

12-Nov-16

12-Dec-16

12-Jan-17

12-Feb-17

12-M

ar-17

12-Apr-17

12-M

ay-17

12-Jun

-17

12-Jul-17

12-Aug-17

Vanguard

Close WTI

EnergyStocksHaveSufferedin2017,PermianStocksMoreRecently

• Capitalflowsto4ghtoilhaveslowedin2017.• Sharepriceshavedeclinedasmarkets4reofmediocrefinancialreturns.• Con4nuedcapitalflowisthechieffactorin4ghtoilgrowth,notreservesoreconomics.

Slide18LabyrinthConsul4ngServices,Inc. artberman.com

TightOilandTheLong-TermDebtCycle

4835

0

50

100

150

200

250

300

350

Venezuela

Saud

iArabia

Canada Iran

Iraq

Russia

Kuwait

UAE

Libya

US

Nigeria

Kazakhstan

China

Qatar

Brazil

Algeria

Angola

Ecuado

r

Mexico

Norway

Azerbaijan

Oman

India

Vietnam

Australia

Malaysia

SouthSudan

Egypt

Perm

ian

BillionsofBarrelsofLiquids

TheU.S.MustDoubleReservesToBecomeanOil-DominantProducerEvenDoublingorTriplingPermianReservesNotNearlyEnough

BP EIA

UnitedStates So

urce:BP,EIA&LabyrinthConsultingServices,Inc.

PermianBasin

0%

20%

40%

60%

80%

100%

120%

$0

$20

$40

$60

$80

$100

$120

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

U.S.PublicDebt-To-GDP

Percent

OilPriceinOctober2016Do

llars

HighOilPrices2005-2014PlusMassiveDebt&LowInterestRatesAfter2008

WTIPrice$2016(LHS)

Debt/GDP(RHS)

Source:U.S.FederalReserve Bank,U.S.Bureauof LaborStatiistics,WorldBank,EIA&LabyrinthConsultingServices,Inc.

LowOilPrices

HighOilPrices

HighOilPrices

IncreasingDebt-To-GDP

FallingOilPrices

CreditBubble

LedToMajorCreditBubble&TheShaleRevolution

• Shalerevolu4onmustbeputinperspec4ve.• Highoilprices2005-2104plusmassivedebt&lowinterestratesaTer2008createdacapitalbubblethatdrove

4ghtoildevelopmentandgrowth—muchofituneconomic!• Con4nuedavailabilityofexternalcapitalisthemostcri4calfactorforproduc4ongrowth&maintenance.• Thetruebreak-evenpricefor4ghtoilisnot<$50butiscloserto$60wellheadprice.• Tightoilplaysarenotthenewswingproduceroftheworld(i.e.,the“callonshale”).• Compara4veinventoryremainsthebestindicatoroffutureoilprices.• C.I.has4ghtenedinspiteofOPEC’smodestcompliancebutwillthiscon4nue?• Year-end2017WTIpricescouldbe$55butforwardcurvesareinbackwarda4on.• Permianplaysaregoodbutwillprobablycon4nuetodeliverlowreturnsandlowerproduc4ongrowththan

manyanalystspredict.• Enthusiasmfor4ghtoilinnova4onmustbebalancedbythedesirabilityofyearsofdepressedoilprices.