purdue cooperative extension service ag outlook 2006

Post on 22-Dec-2015

217 views

TRANSCRIPT

PURDUE COOPERATIVE EXTENSION SERVICE

AG OUTLOOK 2006

2

U.S. Net Farm Income and Government82.5

71.8

13.3

21.4

0

10

20

30

40

50

60

70

80

90

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 0 1 2 3 4 5

Bill

ion

$

Net Farm Income

Government Payments

3

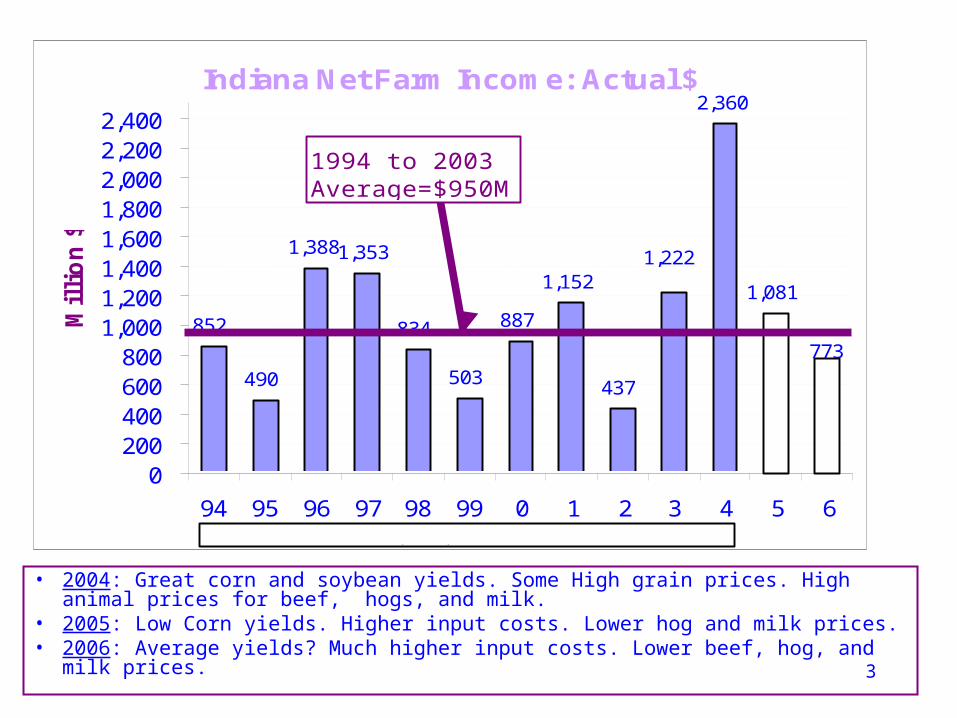

• 2004: Great corn and soybean yields. Some High grain prices. High animal prices for beef, hogs, and milk.

• 2005: Low Corn yields. Higher input costs. Lower hog and milk prices.• 2006: Average yields? Much higher input costs. Lower beef, hog, and milk prices.

Indiana Net Farm Income: Actual $

852

490

1,3881,353

834

503

887

1,152

437

2,360

1,081

773

1,222

0200400600800

1,0001,2001,4001,6001,8002,0002,2002,400

94 95 96 97 98 99 0 1 2 3 4 5 6

Mil

lio

n $

1994 to 2003 Average=$950M

Source 1994-2004 USDA; 2005, 2006 Estimates -P urdue

4

Forecast for 2006

Last 12 Months

Next 12 Months

GDP (Real) +3.6% +3.2% to 3.6%

CPI +3.0% (Jan-July 2005)

+2.5 to 3%

Unemployment 4.9% (August 05)

4.8%-5.0% (August 06)

3 Month Treasury 3.4% (Sept., 2005)

4.3% (August 06)

10 Year Treasury 4.2% (Sept., 2005)

5.3%(August 06)

5

Commercial Ag Loan Rates: Chicago Fed District

5

6

7

8

9

10

11

12

13

90 91 92 93 94 95 96 97 98 99 0 1 2 3 4 5

Inte

rest

Rat

e

Operating

Feeder Cattle

Real Estate

6

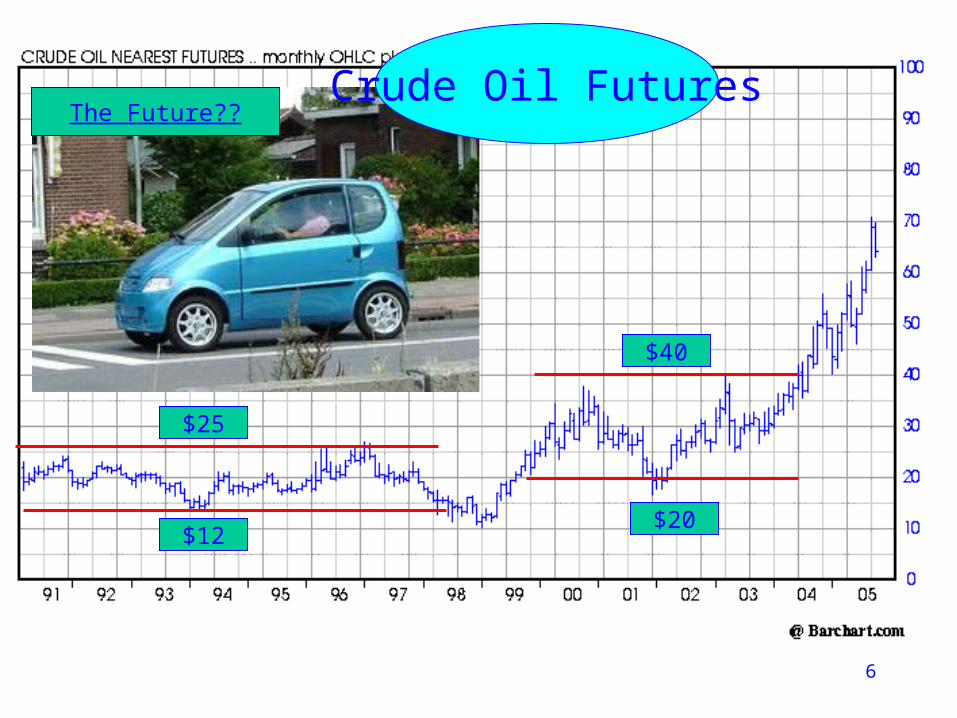

The Future??

$12

$40

$25

$20

Crude Oil Futures

7

17.3 FeetCurb Weight: 5,842

7.5 FeetCurb Weight: 1,388

Europe$5.00 Gasoline

U.S.$1.75 Gasoline

8

Government Provisions:

2005 to 2007 Crops ($/bu.)

Corn Soybeans Wheat

Target $2.63 (+.03) $5.80 3.92 (+.06)

Direct Payment $0.28 $0.44 $0.52

CCP Pivot $2.35 $5.36 $3.40

Maximum CCP $0.40 $0.36 $0.65

National Loan 1.95 (-.03) $5.00 2.75 (-.05)

9

Government Policy• Just two more years under current bill 2006 to 2007 crops.

• Review LDP rules for Corn:

– Today’s LDP is based on yesterday’s Posted County Price.

– 60-day MLG Lock-in rule (CCC-697).

• 2007 Farm Bill Driven By:– WTO: Cotton LDP’s are not legal. Impact soybeans, corn, and wheat as

well for 2007 Bill.

– Federal budget deficits. Will Congress cut payments to agriculture??

– Political Landscape: House Ag committee has changed leadership, Senate is more intact.

• Likely Implications for 2007 Farm Bill– Reduced spending for agriculture.

– Broad based programs like EQUIP and CSP. Less commodity based.

– Changes in the form and level of LDP payments.

10

Food Prices Lower than General Inflation!• Grocery store food prices up 1.4% in last year

much lower than the than 3.2% general inflation.

• Led by lower dairy and egg prices, and generally lower commodity prices after hurricanes, and BSE last year.

• Greater competition from food warehouses and super centers.

• Katrina: Higher coffee, bananas, chicken, seafood

• Over the next year:

– Restaurant prices +2% to 3%

– Food store prices +1% to 2%

11

U.S. Planted Acreage

40

50

60

70

80

90

80 82 84 86 88 90 92 94 96 98 00 2 4

Mill

ion

Acr

es

Corn Soybeans Wheat

2005:Corn + .9%Beans -2.8%Wheat -2.7%

12

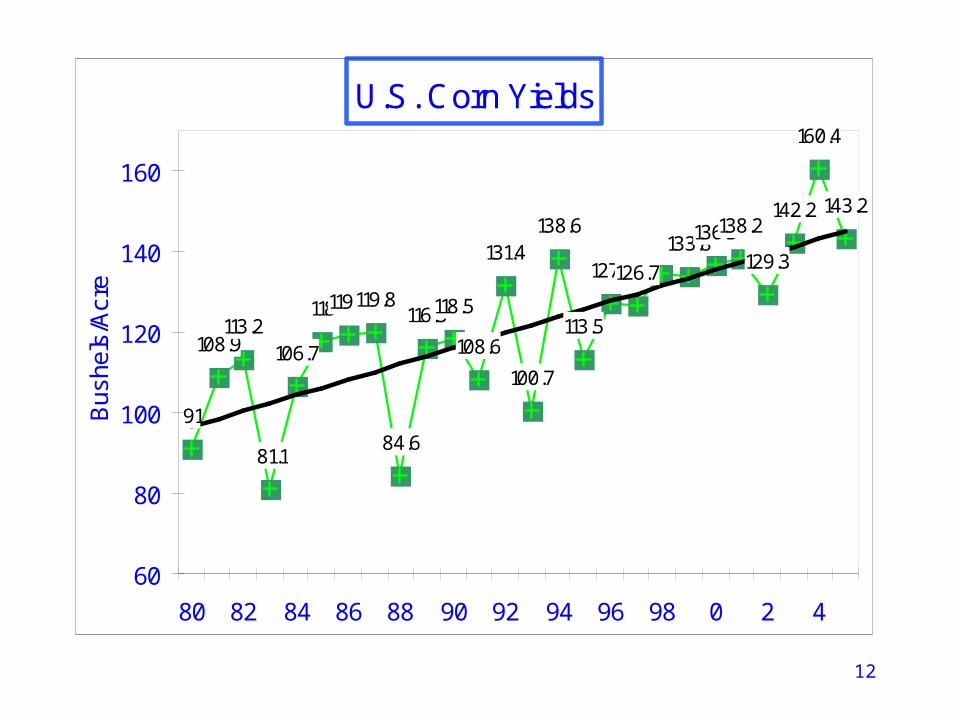

U.S. Corn Yields

91

108.9113.2

81.1

106.7

118119.3119.8

84.6

116.3118.5

108.6

131.4

100.7

138.6

113.5

127.1126.7133.8136.9138.2

129.3

142.2

160.4

143.2

60

80

100

120

140

160

80 82 84 86 88 90 92 94 96 98 0 2 4

Bus

hels

/Acr

e

13

U.S. Corn Production

6.64

8.128.24

4.17

7.67

8.88

8.23

7.13

4.93

7.537.93

7.48

9.48

6.34

10.05

7.40

9.239.21

9.769.43

9.929.51

8.97

10.09

11.81

10.64

3

4

5

6

7

8

9

10

11

80 82 84 86 88 90 92 94 96 98 0 2 4

Bill

ion

Bu

she

ls

14

15

Corn: USDA

9/12/2005

01/02 02/03 03/04 04/05 05/06

Carryin 1,899 1,596 1,087 958 2,125

Production 9,507 8,967 10,089 11,807 10,639

Total Supply 11,416 10,578 11,190 12,775 12,774

Feed & Residual 5,877 5,563 5,798 6,150 5,825

Food,Seed,&Ind 2,054 2,340 2,537 2,690 2,870

Export 1,889 1,588 1,897 1,810 2,000

Total Use 9,820 9,491 10,232 10,650 10,695

Ending Stocks 1,596 1,087 958 2,125 2,079

US Farm Price $1.97 $2.32 $2.42 $2.06 $1.70-$2.10

$1.90

16

Friday September 9, 2005

Corn Soybeans

Harvest to late-March

Harvest to June

Harvest to late-March

Harvest to June

Futures Premium $0.18 $0.24 $0.22 $0.26

Potential Basis Gain $0.15 $0.15 $0.15 $0.15

Expected Carry $0.33 $0.39 $0.37 $0.41

Interest -$0.04 -$0.06 -$0.14 -$0.22

Return After Interest: On-Farm $0.29 $0.33 $0.23 $0.19

Commercial Storage Charges* -0.22 -0.29 -0.22 -0.29

Returns to Commercial Storage $0.07 $0.04 $0.01 -$0.10

* Based on $.14 per bushel until December 31, and 2.5 cents per month after.

17

Corn Price Strategies• Harvest cash prices $1.65 to $1.80• LDP’s working-review FSA forms and mechanics

– Today’s LDP is on yesterday’s Posted County Price (PCP)– 60 day repayment lock-in provisions (CCC-697)

• Consider early LDP’s of $.35 to $.50 per bushel • Great returns to on-farm storage and some on Commercial:

– 32 to 35 cents to late-March– 36 to 40 cents into early-summer

• Late-spring or early-summer $1.95 to $2.10 • LDP, store, and earn the carry:

– LDP, store, and forward contract– LDP, store, and sell May or July futures (hedge)– LDP, store, and speculate on price rise – Do some of the first two on a sizable portion.

• Fewer corn acres in 2006, but better yields modest price improvement.

18

U.S. Soybean Yields

26.5

30.1

31.5

26.2

28.1

34.133.3

33.9

27.0

32.3

34.134.2

37.6

41.4

35.3

37.6

38.938.9

36.6

38.1

39.6

38.0

33.9

42.5

39.6

32.6

25

27

29

31

33

35

37

39

41

43

80 82 84 86 88 90 92 94 96 98 0 2 4

Bu

./acr

e

19

U.S.Soybean Production

2.45

3.14

2.86

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

80 82 84 86 88 90 92 94 96 98 0 2 4

Billi

on B

ushe

ls

20

21

Soybeans: USDA

9/12/2005

01/02 02/03 03/04 04/05 05/06

Carryin 248 208 178 112 295

Production 2,891 2,756 2,454 3,141 2,856

Total Supply 3,141 2,969 2,638 3,258 3,155

Seed & Residual 171 130 111 168 150

Crush 1,700 1,615 1,530 1,700 1,685

Exports 1,063 1,044 885 1,095 1,115

Total Use 2,933 2,791 2,526 2,963 2,950

Ending Stock 208 178 112 295 205

Farm Price $4.38 $5.40 $7.34 $5.75 $5.15-$6.05

$5.60

22

Soybean Pricing Strategies

• Harvest cash prices: $5.40 to $5.60• Post-harvest recovery back to $5.80 to $6.00 (by Thanksgiving)• Flat-to-modestly higher in Jan, Feb. March with normal South American

harvest?? Highs maybe $6.10 to $6.20 in late-spring• No LDP’s expected• Gross returns to storage: Store on-farm, maybe commercial

– 35 to 38 cents to late-March– 39 to 43 cents to late spring

• Strategies: - Store on-farm and speculate until December, then consider forward

pricing on hedging.- Consider commercial storage until Thanksgiving time.-Speculate for higher prices: Last four years cash increase has been:

- 2001 Crop = +$1.50/ bu. - 2002 Crop = +$1.25+ - 2003 Crop = +$3.00/bu. -2004 Crop = +$2.20/bu.

• With limited storage space, the Market favors corn storage over bean storage.

• More acres in 2006, higher yields, lower prices????

23

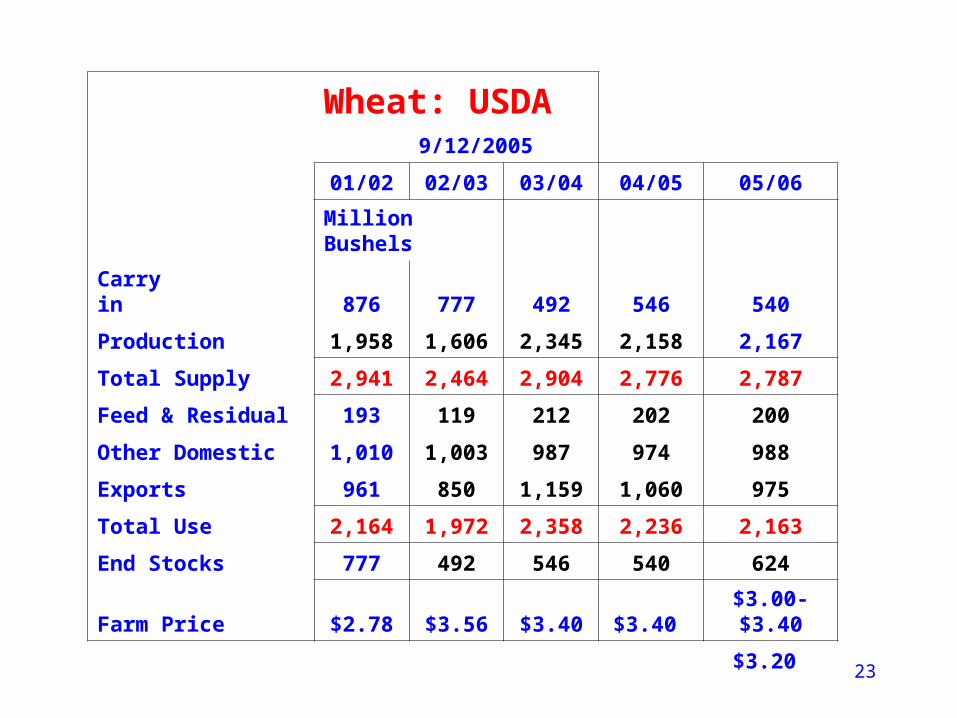

Wheat: USDA

9/12/2005

01/02 02/03 03/04 04/05 05/06

Million Bushels

Carryin 876 777 492 546 540

Production 1,958 1,606 2,345 2,158 2,167

Total Supply 2,941 2,464 2,904 2,776 2,787

Feed & Residual 193 119 212 202 200

Other Domestic 1,010 1,003 987 974 988

Exports 961 850 1,159 1,060 975

Total Use 2,164 1,972 2,358 2,236 2,163

End Stocks 777 492 546 540 624

Farm Price $2.78 $3.56 $3.40 $3.40 $3.00-$3.40

$3.20

24

Estimated Production CostsEstimated Variable Expenses Per Acre: 04, 05, 2006

$88$96

$191

$171

$106$114

$184

$207

128

226

205

105

$0

$25

$50

$75

$100

$125

$150

$175

$200

$225

$250

Cont. Corn Rot. Corn Rot. Beans Wheat

$/A

cre

2004

2005

2006

+ 12% + 8%

+ 11% + 9%

25

Annual Prices 2003 - 2006

86

100

71

46

74

62

105

49

736669

98100

81

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

ChoiceSteers

FeederSteers

Lambs Barrow&Gilts

Broilers Turkey Eggs

$/cw

t o

r ce

nts

/do

z

3 4 5 6

26

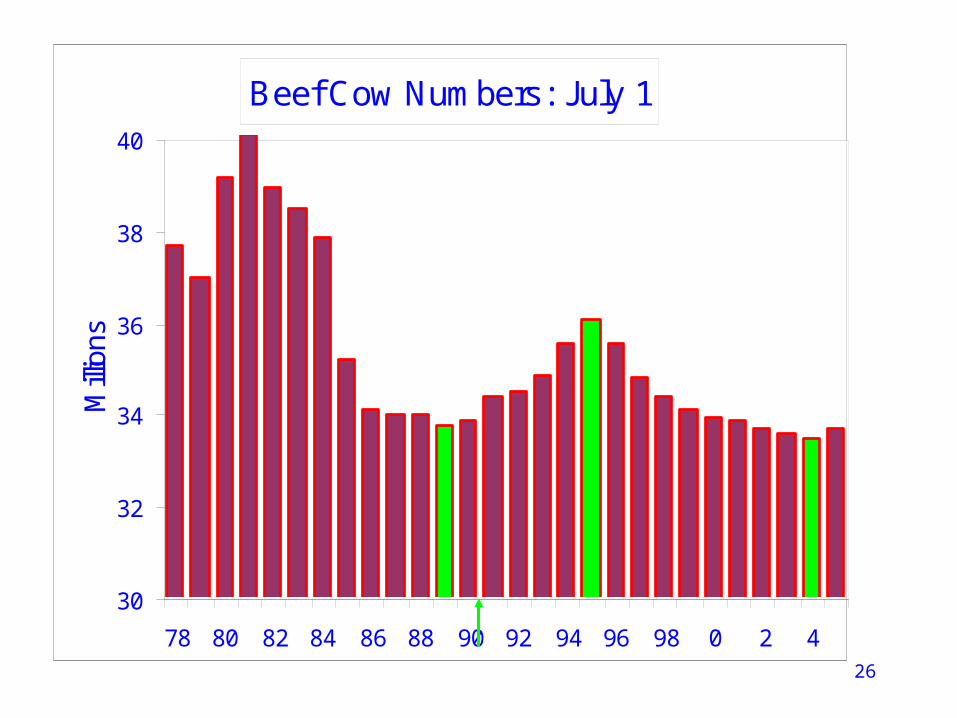

Beef Cow Numbers: July 1

30

32

34

36

38

40

78 80 82 84 86 88 90 92 94 96 98 0 2 4

Milli

ons

27

2004 I 5,838 -7.1% $82.16 $103.57 $111.50 $87.98

II 6,253 -9.4% $88.15 $116.47 $122.45 $104.58

III 6,360 -10.2% $83.58 $123.51 $129.12 $116.27

IV 6,097 2.1% $85.09 $112.94 $125.13 $110.19

Year 24,548 -6.4% $84.75 $114.12 $122.05 $104.76

2005 I 5,727 -1.9% $89.09 $122.70 $129.75 $104.09

II 6,195 -0.9% $87.96 $124.70 $136.05 $113.36

III 6,953 9.3% $79.54 $112.42 $120.40 $107.94

IV 6,392 4.8% $82.55 $111.74 $121.13 $109.62

Year 25,267 2.9% $84.79 $117.89 $126.83 $108.75

2006 I 6,134 7.1% $84.84 $120.09 $128.77 $103.89

II 6,686 7.9% $80.73 $109.14 $117.75 $106.06

28

U.S. All Milk Price 16.05

14.05

13.35

$11

$12

$13

$14

$15

$16

90 92 94 96 98 0 2 4 6

$/C

wt.

For 2006: Cow numbers + .5%Milk per cow +1.8%Production +2.3%

Milk prices lower, feed similar prices

29

The Numbers: June 1

Total Inventory +0.2%

Breeding +0.7%

Market +0.1%

Spring farrowings = 0 %

Summer farrowings - 0.1%

Fall farrowings - 0.3%

30

PRODUCTION

PRICES

Prod.%Chg

vs. Live Price

% Chg Vs.

Year Qtr Mill.#sYear-

ago Year Qtr $/cwt.Year-

ago

2004 Year 20,508 2.8% 2004 Year $52.51 33.1%

2005 I 5,136 0.1% 2005 I $51.92 17.5%

II 5,033 2.8% II $52.45 -4.5%

III 5,089 0.8% III $47.27 -16.5%

IV 5,501 1.2% IV $44.33 -18.4%

Year 20,758 1.2% Year $48.99 -6.7%

2006 I 5,190 1.1% 2006 I $46.75 -10.0%

II 5,045 0.2% II $50.42 -3.9%

Year 21,055 1.4% Year $45.62 -6.9%

31

Estimated Hog Returns ($/LiveCwt.)

1.43

-3.25

-7.03

-8.70

-5.05

1.532.38

-4.90

-0.87

6.34

14.3615.72

12.4712.38

5.885.00

6.767.20

-$10

-$6

-$2

$2

$6

$10

$14

$18

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2

2 3 4 5 6

$/liv

eCw

t.

32

Indiana Land Values and Cash Rents

$500

$750

$1,000

$1,250

$1,500

$1,750

$2,000

$2,250

$2,500

$2,750

$3,000

75 77 79 81 83 85 87 89 91 93 95 97 99 1 3 5

$40

$60

$80

$100

$120

$140

$160

Average Land: $2,945 up 9.4%

Cash Rent: $126Up 3.3%

Outlook 2006:Land….up 4% to 6%Rents…up .5% to 1%

33

Indiana Avg. LandPrice/Earnings Ratio

10

12

14

16

18

20

22

24

75 77 79 81 83 85 87 89 91 93 95 97 99 1 3 5

Ra

tio

Value/Rent Ratio

Mean = 17.0

+1 & +2 Std Dev

34

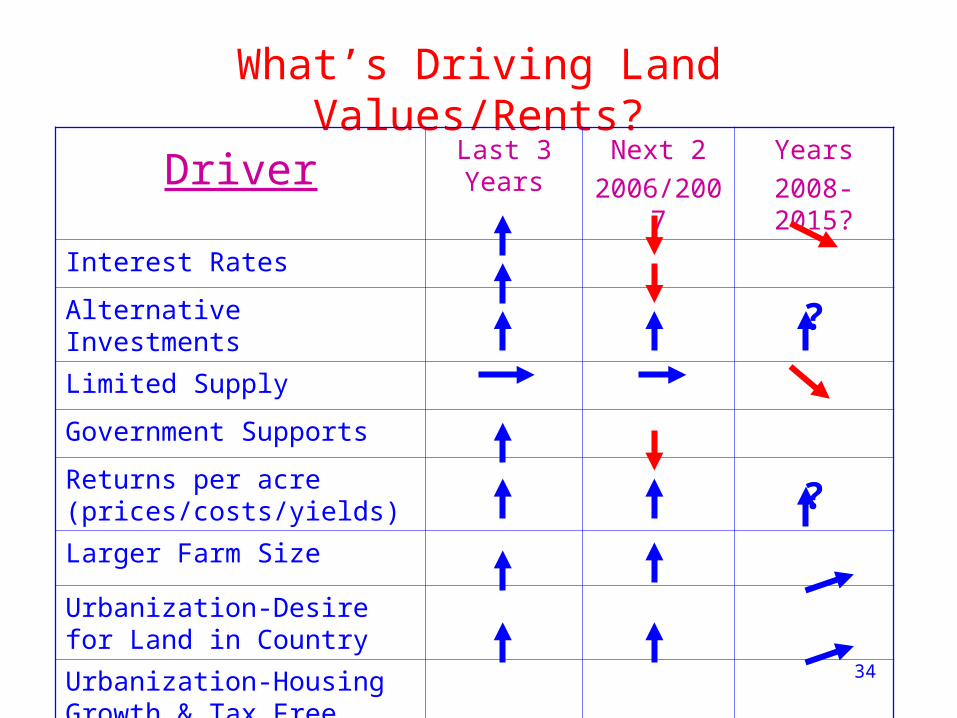

What’s Driving Land Values/Rents?

DriverLast 3 Years Next 2

2006/2007

Years

2008-2015?

Interest Rates

Alternative Investments ?Limited Supply

Government Supports

Returns per acre (prices/costs/yields) ?

Larger Farm Size

Urbanization-Desire for Land in Country

Urbanization-Housing Growth & Tax Free Exchanges (1031s)

35

Monday-Katrina

Tuesday-Flooding

Impact on Ohio River Corn Basis:-20 to -25 cents/bushel

36

Kokomo Corn Basis Impact:-4 to -6 cents/bushel

37

N.E. Indiana Corn Basis Impact:-2 to -3 cents/bushel