public session agenda north carolina state … · 2018-08-08 · north carolina state board of cpa...

TRANSCRIPT

PUBLIC SESSION AGENDA NORTH CAROLINA STATE BOARD OF CPA EXAMINERS

AUGUST 20, 2018 10:00 A.M.

1101 OBERLIN ROAD RALEIGH, NC

I. Administrative ItemsA. Call to Order

In accordance with the State Government Ethics Act, it is the duty of every Board member to avoidboth conflicts of interest and appearances of conflict. Does any Board member have any knownconflict of interest or appearance of conflict with respect to any matters coming before the Boardtoday? If so, please identify the conflict or appearance of conflict and refrain from any undueparticipation in the particular matter involved.

B. Welcome and Introduction of GuestsC. Approval of Agenda (ACTION)D. Minutes (ACTION)E. Financial/Budgetary Items

1. Financial Statements for July 2018 (ACTION)

II. Legislative & Rule-Making Items

III. National Organization ItemsA. NASBA Update on Pathways and Regional Meetings (FYI)B. Draft NASBA Focus Questions (ACTION)

IV. State & Local Organization ItemsA. Joint Board/NCACPA CPE Task Force (ACTION)B. Record Retention and Disposal Schedule (ACTION)

V. Request for Declaratory Ruling

VI. Committee ReportsA. Professional Standards (ACTION)B. Professional Education and Applications (ACTION)

VII. Resolutions and Oaths of OfficeA. Resolutions for Outgoing Board Members (ACTION)B. Oaths for Incoming Board Members (ACTION)

VIII. Public Comments

IX. Executive Staff and Legal Counsel ReportA. Strategic Plan – Update (FYI)B. Operational Metrics (FYI)C. Executive Staff Report (FYI)

X. Closed Session

XI. Adjournment

PUBLIC SESSION MINUTES North Carolina State Board of CPA Examiners

July 23, 2018 1101 Oberlin Road Raleigh, NC 27605

MEMBERS ATTENDING: L. Samuel Williams, Jr., CPA; President; Jeffrey J. Truitt, Esq., Vice President; Arthur M. Winstead, Jr., CPA, Secretary-Treasurer; Cynthia B. Brown, CPA; Justin C. Burgess; Wm. Hunter Cook, CPA, and Michael H. Womble, CPA.

STAFF ATTENDING: Robert N. Brooks, Executive Director; David R. Nance, CPA, Deputy Director; Frank Trainor, Esq., Staff Attorney; Lisa R. Hearne, Communications Manager; Jean Marie Small, Professional Standards Specialist; Buck Winslow; Licensing Manager; and Noel L. Allen, Esq., Legal Counsel.

GUESTS: Mark Soticheck, CPA, COO, NCACPA; Nathan Standley, Esq., Allen & Pinnix, P.A.; and Sgt. J.A. Stokes, Raleigh Police Department.

CALL TO ORDER: President Williams called the meeting to order at 10:01 a.m.

MINUTES: The minutes of the June 22, 2018, meeting were approved as submitted.

FINANCIAL AND BUDGETARY ITEMS: The June 2018 financial statements were accepted as submitted.

Mr. Nance reported on a banking opportunity offered to the Board by one of its current banks, Pinnacle. The Cedars Program would allow the Board to place more than $250,000.00 on deposit and all funds would be covered under the FDIC program. The Board instructed Mr. Nance to proceed with the Cedars Program with Pinnacle.

LEGISLATIVE AND RULE-MAKING ITEMS: Mr. Brooks reported that Senate Bill 735, Reform Financial Reporting of Occupational Licensing Boards, failed to make it out of the Senate Rules Committee and was dead for the Session.

NATIONAL ORGANIZATION ITEMS: Mr. Brooks reported that Ken Bishop, President and Chief Executive Officer of NASBA, had expressed his lack of continued support for the “New Pathway to CPA” due to the overwhelming lack of support expressed by boards at the NASBA regional meetings.

President Williams announced that Mr. Womble was nominated by the NASBA Nominating Committee for Regional Director of the Middle Atlantic Region of NASBA. Mr. Womble will take office at the October 2018 NASBA Annual Meeting.

ITEM I-D

Public Session Minutes July 23, 2018

Page 2

STATE AND LOCAL ORGANIZATION ITEMS: President Williams announced that Mr. Winstead would receive the NCACPA’s Distinguished Public Service Award at the NCACPA Recognition dinner to be held in Raleigh on July 31, 2018.

REPORT OF THE PROFESSIONAL STANDARDS COMMITTEE: Ms. Brown moved and the Board approved the following recommendations of the Committee:

Case Nos. C2017201-1 and C2017201-2 - Gerrelene M. Walker, CPA, and Gerrelene M. Walker, CPA, CFE – Approve the signed Consent Order (Appendix I).

Case No. C2017205-2 Seiler, Singleton & Associates, PA - Approve the signed Consent Order (Appendix II).

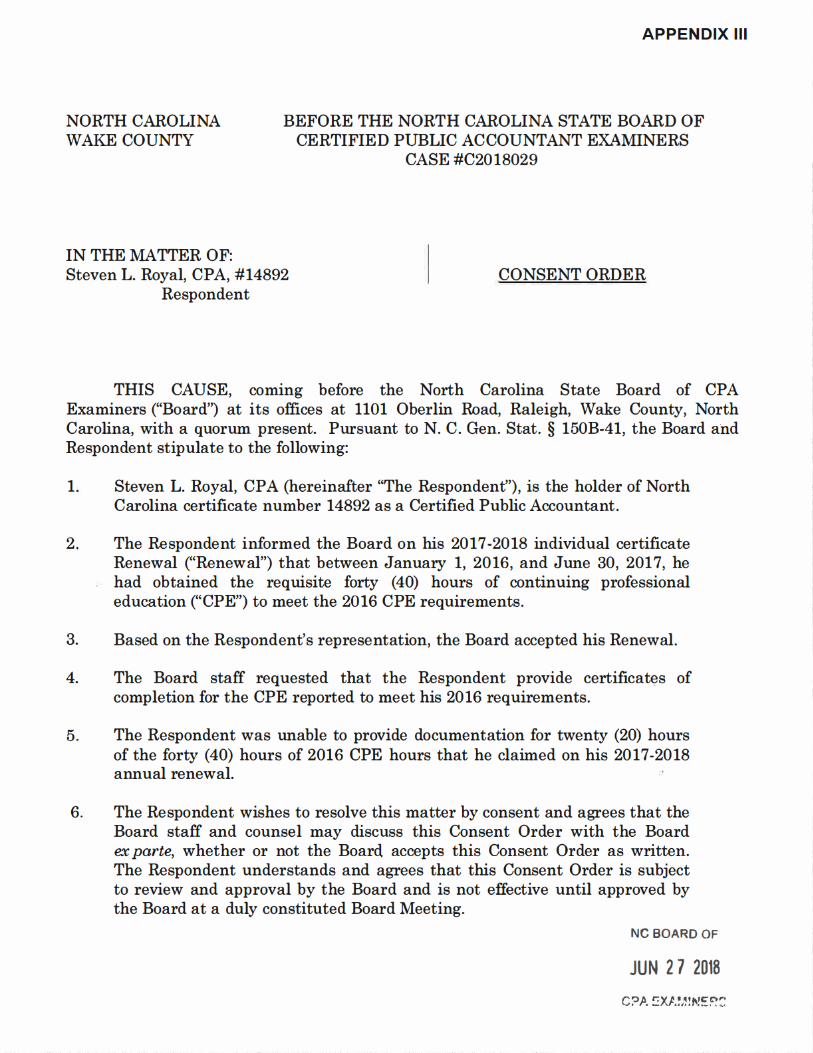

Case No. C2018029 - Steven L. Royal - Approve the signed Consent Order (Appendix III).

Case Nos. C2017121 and C2017122 – Close the cases without prejudice.

Case No. C2017252 - Close the case without prejudice.

Case No. C2017285 - Close the case without prejudice.

Case No. C2018055 – Close the case without prejudice with a Letter of Warning.

Case No. C2018058 – Close the case without prejudice.

REPORT OF THE PROFESSIONAL EDUCATION AND APPLICATIONS COMMITTEE: Mr. Burgess moved and the Board approved the following recommendations of the Committee:

Transfer of Grades Applications - The Committee recommended that the Board approve the following:

Nicholas Samuel Anderson Alicia Ann Ayers Stephen Clayton Beloin Leah Camille Bitetti

Paul Robert Ensminger Beverly Thomas Himes Taylor Thomas Rule ChaRon Chermaine Singleton

Original Certificate Applications - The Committee recommended that the Board approve the following:

Hyen Adrong Nicholas Samuel Anderson Seth William Anderson

Alicia Ann Ayers Elizabeth Kuchenmeister Bagwell Nicholas Alfred Barnas

Public Session Minutes July 23, 2018

Page 3

Stephen Clayton Beloin Thomas Joseph Bickes Leah Camille Bitetti Stefenie Howell Brinson Cassie Patricia Bumgarner John Thomas Burnett Chad Barton Chandler Mamie Gayle Duckworth Paul Robert Ensminger Sarah Kristine Exley Danielle Manierre Goldstein Michael Major Gore Heather Michelle Gray Turner Walton Haigwood Renee Rachel Halifax Monica Eve Hilburn Beverly Thomas Himes Jacqueline Beth Hobbs Joshua Thomas Holbrooks Kristen Elizabeth Jones Keith Joseph Keller Shareen Shelby Knapik David Matthew Komasara Kelly Ann Krebs Stefanie Liebhold Robin Ann Link

Eugene Francis McManus, III Tiffany Dixon McPherson Ian Lee Metcalf David Robert Padykula Camilla Anne Paramore Kristie Alise Ploetzke Mary Katherine Rawn Phillip Thomas Robbins Taylor Thomas Rule ChaRon Chermaine Singleton Kyle Andrew Stinman Bryan Daniel Stinson Everett Eugene Swimm Hannah Victoria Tennyson Austin Edward Tew Tamara Lynn Todi Onur Uman Cooper Joseph Wasil James Allen Watson, II Zachary Barrett Watts Kayla Hicks Willett Bradley Jay Williams John Patrick Willis Benjamin Ross Wood Yunhua Wu

Reciprocal Certificate Applications - The Committee recommended that the Board approve the following:

Aradhana Aggarwal Daniel Joseph Albanese Denise Marie Anderson Richard Leroy Arnold, Jr. Timothy Edward Baisley Nancy Barker Beazley Katherine Marie Bierman Carolyn Beth Coonce Michael Francis Cosolito Grant Matthew Curry E’Meka Shirrell Davis Peter John Delvecchia Leah Henderson Dryden

Deborah Nyra Eason Sheila Marie Eichelberger Tracey Hazel Erbe Frederick Fulton Forbes, Jr. John Caldwell Gault Theresa Owusua Green Matthew Richard Grosh Pamela Denise Gunn Aleta Ann Habeeb Meredith Scott Harris Kari Lynn Hein Megan Claire Hicks Donna Emmett Hildebrand

Public Session Minutes July 23, 2018

Page 4

Juanjuan Huang Douglas Wayne Johnson Scot Eliot Justice Matthew Copeland Laney Suk Young Lee Jennifer Foppe Louis Amanda Leigh Lowry Alexandria Dandie Lyon Ishmael Anthony McKenzie Chad Bert Muhlestein Katherine Marlowe Nixon Ryan Peter Petrone David Michael Pickett Tony Lamar Rowland Erik Herman Ruppert Alison Thornal Santiago Eric Saxx

Melissa Van Acker Scanlon Anna Marie Schiltz Christopher Lee Schumacher Jeffry J. Sherwood Rhonda Graham Sommer Nicola Steele Jennifer Thompson Stephenson Musa Baba Sulayman Edward Paul Thill Ryan Patrick Trent Richard Earle Walck Laura Faye Ward Travis Alan Watson Nathan Joseph Wicker Ying Yu Limin Zhao

Temporary Permits - The Committee recommended that the Board approve the following temporary permits that were approved by the Executive Director:

Matthew Richard Grosh, T10511 Jennifer Foppe Louis, T10512 Eric Saxx, T10513 Ishmael Anthony McKenzie, T10514 Sheila Marie Eichelberger, T10515 Michele Marie Pratt, T10516 Sandra B. Carlson, T10517 Kennard S. Brackney, Jr., T10526 Scott Graykowski, T10527 Gema Catalina Colón-Albiñana, T10528 Elizabeth Anne Runser, T10529 Tracy June Dye, T10530 Ruth Marie Huster, T10531 Aaron Daniel Kees, T10532 Jessica Owens Brown, T10533

Wesley Walden Lyon, II, T10534 Michael James Hadden, T10535 Brendan Anthony Garay, T10536 Ann Wilson Woody, T10537 Kenton William Porter, T10538 Peter Jordan Zender, T10539 Charles Robert Zinn, T10540 Patrick James Collins, T10541 Jessica Lea Fine, T10542 Jordan John Sourwine, T10543 Manishkumar Thakkar, T10544 Mark Musheg Arakelyan, T10545 Anita Grace Doll, T10546 Rubing Chen, T10547

Reinstatements - The Committee recommended that the Board approve the following:

Mary Lucille Foy, #18786 Carla Gardner Marshall, #18304 Ashley Shavonne Middleton, #39475

Cheryl Brooks Plozizka, #22869 Shelly Renee Simmerman, #29631 Margaret Anna Szewczyk, #35966

Public Session Minutes July 23, 2018

Page 5

Reissuance of New Certificate - The Committee recommended that the Board approve the application for reissuance of new certificate submitted by Pamela Jean Strickland, #25225.

Reissuance of New Certificate and Consent Agreement - The Committee recommended that the Board approve the following application for reissuance of new certificate and consent agreement submitted by Jeffrey Robert Johnson, #38898.

Extension Requests - The Committee recommended that the Board approve the Joseph Monroe Giles, Jr., #7736 for extension for completion of CPE until June 30, 2018.

Letter of Warning - Staff reviewed the random CPE audit submitted by Andrew Wharton Blair, Sr., #34700 that listed 2016 CPE taken between January 1 and June 30, 2017, without an approved extension. Staff recommended a Letter of Warning for a first offense pursuant to 21 NCAC 08G .0406(b)(1). The Committee recommended that the Board approve staff recommendation.

The Committee recommended that the Board approve the requests to rescind the Letters of Warning issued to the following individuals:

April Elizabeth Audette, #40335 Cheyenne F. Folland, #28252 Philip Wiley Haigh, III, #7099

Joseph Gerald Pariseau, #40324 Britta Ashley Wakefield, #39533

Examinations –The Committee recommended that the Board approve the following staff-approved applicants to sit for the Uniform CPA Examination:

Robert Adams Alec Altman Deborah Anderson Christopher Aronis Tyler Augat Meghan Bailey Leizl Baker Derek Belza Alison Billman Brandon Bishopp Donald Blackwell Megan Blakley Meaghan Bleakley Lynn Bodine Joshua Bollinger Aaron Bonertz

Chase Branham Charles Brown Robert Callaghan Kyle Carmody Taylor Castle Felix Chang Nicholas Chilcutt Jonathan Clark Nicholas Clark Rashaad Clavon Melanie Clyburn Rodrigo Cohen Philip Colvard Grayson Compton Robert Connery Jake Connor

Public Session Minutes July 23, 2018

Page 6

Gavin Coyle Camille Cross Angel Dameron Alexandra Davis Miranda Davis Virginia Dawson Christianne De La Cruz Alena Degtereva Tammy Dixon Riley Dolan Brian Donaldson Alicia Driver Brice Edwards Rachel Eng Brooke English Matthew Epley Mohammad Eqteeshat Kimberly Ervin Parker Esoda Kate Etheridge Connie Everhart Dennis Farlow Sean Feeley Adam Filipponi Miguel Flores Chelsea Forman Jonathan Fountain Daniel Fox Meredith Freeman Stephen Frerichs Amanda Gadd Sean Gallagher Sarah Gasperson Anna Gates William Glidewell Isabel Golecruz Martha Goodman Andrew Gosnell Danez Green Leigh Gripman Cynthia Grose Justin Hall Michael Hamilton Xiaofeng Han Kevin Harris

Steve Harris Dustin Harrison David Hatfield Robert Hawley Daniel Hayes Hayley Henson Dwayne Herbert Logan Herring Paige Honeycutt Ryan Horgan Callie Houff Nicholas Howarth Staci Huffman Meganne Hurt Lilly Hutchinson Heather Isley Brynn Ivey Tonya Johnson Anna Jones Daniel Jones Cole Jordan Harpreet Kaur Erin Kim Maria Kim Charles King James King Katheryne King Meisha King Ashley Kirby Erin Kissling Christian Kohlmann Katherine Korol Hannah Lawson Ben Liboon Sarah Link Leah Lloyd Hayley Lower Rafael Loza Sean MacDevette Eric Mahaney Nicholas Mannon Kevin Marsh Hannah Massey Harrison Mathews Alexandria McCarrick

Public Session Minutes July 23, 2018

Page 7

Mary McCarthy Robert McCarthy Chase McConnachie Ricky McCoy Madison McDonald Alexander McLarnon Aiesha McLeod Michael Meglin Addis Melesse Marian Mercedes Diaz Erica Merriman Aubrey Middleton Amber Milby Melody Morgan Kelley Nichols Haley Nona Antoni Nowacki Evariste Ntirenganya Tara Null Stephen O'Gara Cheryl Oliver Amanda Ostrander Charlene Pacheco Nolan Pegg Stacey Phillips Charlotte Pielak Joshua Plafker Laura Pollin Rebekah Presson Kristen Pugliese Andra Radu Cyrus Rattler Mary Reed Jana Reeve Rebecca Reisberg Caroline Ricciarelli Richard Richards Tess Rollins Anastasia Rusakova Mona Sade Omar Sadou Anthony Sanguinetti

Landon Savino Reyna Sawyer Jennifer Schafer Franz Schmid Madison Schneider Lewis Schooler Vanessa Seiglie Jeanette Serena Alexander Sewell Jordan Sierra Deidra Simmons Brie Sisak Clinton Smith Elaina Smith Oluwademilade Soile Daniel Stack Caroline Starnes Jacob Stewart Shanique Sumter Brandon Tahamtan Jacob Thompson Julius Timberlake Kenny Tran Shawn Turk Sheryl Tyler Cody Underwood Matthew Vaden Tracy Van Duzen Veda Vang Vasukumar Vijayakumar Tessa Vinson Elizabeth Warren Jacklyn Weatherman Cameron Wegrzyn Angell Wescott Richard Whelan Robert Williams Miranda Wronecki Maheder Yohannes Austin Yount Deyu Zeng Yishan Zhao

The Committee recommended disapproval of a hypothetical request from an Exam candidate for an extension to the 18-month exam credit window. Because there had been

Public Session Minutes July 23, 2018

Page 8

no Exam issues that contributed to the request, the Committee recommended that the Board disapprove the hypothetical.

Rescind Form of Practice Statement –Tara Parker, #30398 signed a Form of Practice Statement due to her employment. However, due to rule changes staff recommended that the statement be rescinded. The Committee recommended that the Board approve the request.

REPORT OF THE AUDIT COMMITTEE: Mr. Cook provided the Board with the report of the Audit Committee and a draft of the 2017-2018 audit report. Mr. Cook moved and the Board approved the recommendation of the Committee to accept the audit report.

EXECUTIVE STAFF AND LEGAL COUNSEL REPORT: The monthly operational metrics and the Executive Staff report were provided.

ADJOURNMENT: Messrs. Burgess and Cook moved to adjourn the meeting at 10:32 a.m. Motion passed.

Respectfully submitted: Attested to by:

Robert N. Brooks L. Samuel Williams, Jr., CPAExecutive Director President

Gerrelene M. Walker, CPA Gerrelene M. Walker, CPA, CFE

9. In August 2017, the Board also received a referral from the LGC regarding the auditof the Town of Spring Hope. The audit contract was with Maxton C. McDowell,CPA.

10. The LGC alleged that the Town of Spring Hope audit was late and that the clienthas signed two extensions. The LGC also indicated that it had received a thirdextension request, but the Town of Spring Hope officials provided attestations thatthey had not signed or authorized the third extension request.

11. When asked by the Board about the potentially forged extension request, MaxtonMcDowell replied that he did not have any knowledge regarding the audit and thatit had been performed by the Respondent. He did, however, point out that theextension request had been faxed. from the Respondent's fax machine.

12. The Respondent did not provide any explanation of how the extension request hadthe signature of a town official.

13. Further, the Town of Spring Hope audit was submitted without having first beensubjected to pre-issuance review.

14. The Respondents wish to resolve this matter by consent and agree that the Boardstaff and counsel may discuss this Consent Order with the Board ex parte, whetheror not the Board accepts this Consent Order as written. The Respondentsunderstand and agree that this Consent Order is subject to review and approval bythe Board and is not effective until approved by the Board at a duly constitutedBoard Meeting.

BASED upon the foregoing, the Board makes the following Conclusions of Law:

1. The Respondents are subject to the provisions of Chapter 93 of the North CarolinaGeneral Statutes and Title 21, Chapter 08 of the North Carolina AdministrativeCode, including the Rules of Professional Ethics and Conduct promulgated andadopted therein by the Board.

2. The Respondent Firm's failure to perform audit services in a timely manner is aviolation of 21 NCAC 08N .0403.

3. The Respondent's issuance of an audit report without first subjecting that report topre-issuance review is a violation of 21 NCAC 08N .0203(a) and .0203(b)(3).

4. If proven at hearing, the allegations that the Respondent had forged the signaturesof town officials on an extension request would constitute a violation of 21 NCAC08N .0201, .0202 and .0203.

5. Per N.C. Gen. Stat. § 93-12(9), 93-lO(b) and also by virtue of the Respondents'consent to this order, the Respondents are subject to the discipline set forth below.

NC BOARD OF

JUN 2 5 2018

CPA EXAMINERS

Consent Order - 2 Steven L. Royal, CPA

BASED upon the foregoing, the Board makes the following Conclusions of Law:

1. The Respondent is subject to the provisions of Chapter 93 of the NorthCarolina General Statutes and Title 21, Chapter 08 of the North CarolinaAdministrative Code, including the Rules of Professional Ethics and Conductpromulgated and adopted therein by the Board.

2. The Respondent's actions as set out above constitute violations of 21 NCAC08N .0202(a), .0202(b)(3), and .0202(b)(4).

3. Per N.C. Gen. Stat. § 93-12(9), 93-l0(b) and also by virtue of theRespondent's consent to this order, the Respondent is subject to the

discipline set forth below.

BASED on the foregoing and in lieu of further proceedings, the Board and theRespondent agree to the following Order:

1. The Respondent's failure to provide adequate documentation of CPE rendersthe Renewal insufficient and untimely. The Respondent's failure toadequately renew his certificate results in a forfeiture pursuant to N.C. Gen.Stat. § 93-12(15).

2. The Respondent must return his certificate to the Board within fifteen (15)days of his receipt of the Board's notification of its approval of this ConsentOrder.

3. The Respondent may apply for the reissuance of his certificate after one (1)year from the date the Board approves this Consent Order as long as the civil

penalty required in number five (5) of this Order has been timely received bythe Board.

4. The Respondent may apply to return his certificate to active status by

submission and approval of a reissuance application which includes:

a. Application form,

b. Payment of the application fee,

c. Three (3) moral character affidavits, andd. Sixty (60) hours of CPE in the twelve (12) months preceding the application

including an eight (8) hour accountancy law course as offered by the North

Carolina Association of CP As.NC BOARD OF

JUN 2 7 2018

C?A EXP.�,1!N!::R�:

Total Revenue

Financial Highlights

For the Four Month Period Ended July 31, 2018 Compared to the Four Month Period Ended July 31, 2017

II Budget Var. I Jul-18 Jul-17

II$ 29,889.61 I $ 1,802,656.53 $ 1,707,912.91

Item I-E-1

Inc. (Dec.)

$ 94,743.62 ■Total Operating Revenue $ 29,387.3311 $ 1,777,245.61 $ 1,681,809.75 $ 95,435.861 ❖Total Net Non Operating Revenue $ 502.28 I $ 25,410.92 $ 26,103.16 $ (692.24)1 OTotal Expenses $ 25,837.21 $ 961,509.83 $ 833,871.39 $ 127,638.441

IIncrease(Dec.) Net Assets for Period I $ 841,146.10 I$ 874,041.52 $ (32,894.82)1 !Total Checking and Savings $ 1,093,354.1011 $ 1,904,143.01 $ (8 I 0,788.3 I )I!Total Assets $ 4,541,764.55 11 $ 4,352,447.09 $ 189,317.461

II !Full-Time/Part-time Employees II 13/1 II 13/1 0/0

Budget: ■ Operating revenue was $29,000 over budget. Certificate fees decreased ($4k), primarily due to

a slight dip in new applications. Exam fee revenue was up by $33,000.

❖ Non-Operating revenue was within budget expectations.

0 Expenses were over budget by $26,000. Key variances individually were increased exam costs ($62k), offset by reduced operational expenses that are mainly due to the timing of their payment.

Actual: ■ Total operating revenue increased from prior year by $95,000. Increase related to the

increase in exam fee revenue ($78k) and certificate fees ($17k).

❖ Total net non-operating revenue decreased this period compared to prior by $700 primarily dueincreased interest income as Board offset by reduced gift card revenue.

0 Total expenses increased from prior period by $128,000. The majority of the increase can be explained by the increased costs related to the exam fees ($103k).

I I

08/02 /18

NC Board of CPA Examiners

Statement of Net Position As of July 31, 2018

ASSETS Current Assets

Checking/Savings 1077 · Fidelity Bank - MMA 1076 · Pinnacle - MMA 1075 · Union - Money Market 1074 · First Tennessee Bank - MMA 1023 · BB&T Disciplinary Clearing Acct 1020 · BB&T Checking Acct 1021 · BB&T Savings Account 1030 · BB&T Payroll Acct

Total Checking/Savings

Other Current Assets 111 O · Accrued CD Interest 1050 · CD Investments - Current 1165 · Deferred Lease Commissions 1126 · Accts Rec Admin Cost 1125 · Accts Rec Civil Penalties 1120 · Accounts Receivable

Total Other Current Assets

Total Current Assets

Fixed Assets 1330 · Land Improvement 1300 · Building 1305 · Land 1310 · Furniture 1320 · Equipment 1325 · Data Base Software 1390 · Accumulated Depreciation

Total Fixed Assets

Other Assets 1250 · CD Investments Non-Current

Total Other Assets

TOT AL ASSETS

LIABILITIES & NET ASSETS

Liabilities Current Liabilities

Other Current Liabilities 2040 · Accounts Payable Civil Penal ... 2005 · Due to Exam Vendors

JuI31,18

0.00

511,959.34

251,121.73

0.00

500.00

219,203.35

110,470.28

100.00

Jul31,17

249,373.02

507,296.00

249,943.55

245,874.74

3,600.00

177,570.21

470,385.49

100.00

1,093,354.70 1,904,143.01

8,732.55

1,503,751.00

2,266.22

1,000.00

1,000.00

-15.00

1,516,734.77

6,769.85

503,943.24

4,358.12

500.00

0.00

215.96

515,787.17

2,610,089.47 2,419,930.18

14,640.90

1,024,414.94

300,000.00

112,387.24

144,539.95

180,336.18

-859,627.73

916,691.48

1,014,983.60

1,014,983.60

14,640.90

1,022,767.10

300,000.00

112,387.24

182,776.27

180,336.18

-876,802.30

936,105.39

996,411.52

996,411.52

4,541,764.55 4,352,447.09

900.00

504,828.68

0.00

469,139.63

Page 1

NC Board of CPA Examiners

08/02/18 Statement of Net Position As of July 31, 2018

Jul31,18 Jul31,17

2011 · Accounts Payable Other 2,500.00 2,500.00

2015 · Accrued Vacation Current 5,992.17 817.62

Total Other Current Liabilities 514,220.85 472,457.25

Total Current Liabilities 514,220.85 472,457.25

Long Term Liabilities 2020 · Accrued Vacation 80,350.27 83,473.44

Total Long Term Liabilities 80,350.27 83,473.44

Total Liabilities 594,571.12 555,930.69

N�tA.ssets 3010 · Net Assets Invest in Cap Assets 916,691.48 936,105.39

3020 · Designated for Capital Assets 100,000.00 100,000.00

3031 · Designated-Operating Expenses 300,000.00 300,000.00

3040 · Designated for Litigation 1,000,000.00 1,000,000.00

3900 · Net Assets Undesignated 789,355.25 586,369.49

Change in Net Assets 841,146.70 874,041.52

Total Net Assets 3,947,193.43 3,796,516.40

TOTAL LIABILITIES & NET ASSETS 4,541,764. 5 5 4,3 52,447.09

Page 2

NC Board of CPA Examiners

08/02/18 Statement of Revenues & Expense - Budget v. Actual April 2018 through July 2018

Apr-Jul 18 Budget $ Over B ...

Ordinary Income/ Expense Income

Certificate Fees 4110 · Certificates -Initial 15,400.00 20,000.00 -4,600.00

4120 · Certificates -Reciprocal 12,000.00 10,666.68 1,333.32

4121 · Certificates -Recip/Temp 0.00 0.00 0.00

4130 · Certificates -Temporary 0.00 0.00 0.00

4131 ·Certificates-Temp Renewal 0.00 0.00 0.00

4140 · Certificates -Renewal Fees 1,272,480.00 1,272,000.00 480.00

4150 · Certificates -Reinst/Revoked 700.00 0.00 700.00

4151 · Certificates -Reinst/Surr 1,600.00 3,333.32 -1,733.32

4152 · Certificates -Reinst/lnactive 0.00 0.00 0.00

4160 · Certificates -Notification 0.00 0.00 0.00

4161 · Certificate -Notification Rnwl 0.00 0.00 0.00

Total Certificate Fees 1,302,180.00 1,306,000.00 -3,820.00

Exam Fee Revenue 4001 · Initial Adm Fees 63,480.00 61,333.32 2,146.68

4002 · Re-Exam Adm Fees 54,450.00 55,000.00 -550.00

4004 · Exam Fees Revenue 364,284.93 333,333.32 30,951.61

4060 · Equivalency Exam Fees 0.00 0.00 0.00

4070 · Transfer Exam Grade Credit 0.00 0.00 0.00

4071 · Exam Review Fees 0.00 0.00 0.00

4072 · Exam Scholarship Coupon -9,387.20 -10,241.68 854.48

Total Exam Fee Revenue 472,827.73 439,424.96 33,402.77

Misc 4993 · Revenue Suspense 0.00 0.00 0.00

4999 · Board Training 63.75 0.00 63.75

4910 · Educational Program Fees 0.00 0.00 0.00

4970 · Duplicate Certificates 125.00 0.00 125.00

4980 · Copies 0.00 0.00 0.00

4990 · Miscellaneous 379.13 500.00 -120.87

Total Misc 567.88 500.00 67.88

Partnership Fees 4260 · Partnership Registration Fees 570.00 0.00 570.00

4261 · Partnership Renewal Fees 0.00 0.00 0.00

Total Partnership Fees 570.00 0.00 570.00

Professional Corporation Fees 4250 · PC Registration Fees 1,100.00 1,933.32 -833.32

4251 · PC Renewal Fees 0.00 0.00 0.00

4252 · PC Renewal Fees W/Penalties 0.00 0.00 0.00

Total Professional Corporation Fees 1,100.00 1,933.32 -833.32

Total Income 1,777,245.61 1,747,858.28 29,387.33

Expense 6900 · Bad Debit Expense 0.00 0.00 0.00

6690 · Over & Short -1.01 0.00 -1.01

Page 1

NC Board of CPA Examiners

08/02/18 Statement of Revenues & Expense - Budget v. Actual April 2018 through July 2018

Apr-Jul 18 Budget $ Over B ...

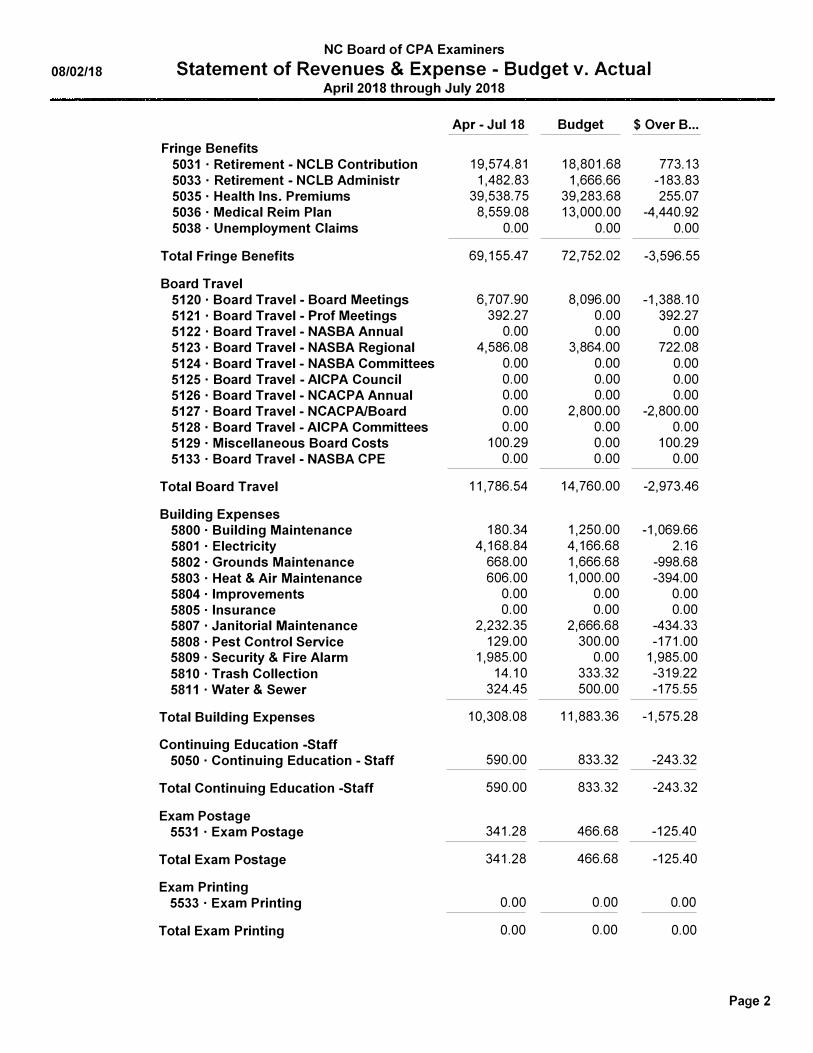

Fringe Benefits 5031 · Retirement - NCLB Contribution 19,574.81 18,801.68 773.13

5033 · Retirement - NCLB Administr 1,482.83 1,666.66 -183.83

5035 · Health Ins. Premiums 39,538.75 39,283.68 255.07

5036 · Medical Reim Plan 8,559.08 13,000.00 -4,440.92

5038 · Unemployment Claims 0.00 0.00 0.00

Total Fringe Benefits 69,155.47 72,752.02 -3,596.55

Board Travel 5120 · Board Travel - Board Meetings 6,707.90 8,096.00 -1,388.10

5121 · Board Travel - Prof Meetings 392.27 0.00 392.27

5122 · Board Travel - NASBA Annual 0.00 0.00 0.00

5123 · Board Travel - NASBA Regional 4,586.08 3,864.00 722.08

5124 · Board Travel- NASBA Committees 0.00 0.00 0.00

5125 · Board Travel -AICPA Council 0.00 0.00 0.00

5126 · Board Travel - NCACPA Annual 0.00 0.00 0.00

5127 · Board Travel - NCACPA/Board 0.00 2,800.00 -2,800.00

5128 · Board Travel -AICPA Committees 0.00 0.00 0.00

5129 · Miscellaneous Board Costs 100.29 0.00 100.29

5133 · Board Travel - NASBA CPE 0.00 0.00 0.00

Total Board Travel 11,786.54 14,760.00 -2,973.46

Building Expenses 5800 · Building Maintenance 180.34 1,250.00 -1,069.66

5801 · Electricity 4,168.84 4,166.68 2.16

5802 · Grounds Maintenance 668.00 1,666.68 -998.68

5803 · Heat & Air Maintenance 606.00 1,000.00 -394.00

5804 · Improvements 0.00 0.00 0.00

5805 · Insurance 0.00 0.00 0.00

5807 · Janitorial Maintenance 2,232.35 2,666.68 -434.33

5808 · Pest Control Service 129.00 300.00 -171.00

5809 · Security & Fire Alarm 1,985.00 0.00 1,985.00

5810 · Trash Collection 14.10 333.32 -319.22

5811 · Water & Sewer 324.45 500.00 -175.55

Total Building Expenses 10,308.08 11,883.36 -1,575.28

Continuing Education -Staff 5050 · Continuing Education - Staff 590.00 833.32 -243.32

Total Continuing Education -Staff 590.00 833.32 -243.32

Exam Postage 5531 · Exam Postage 341.28 466.68 -125.40

Total Exam Postage 341.28 466.68 -125.40

Exam Printing 5533 · Exam Printing 0.00 0.00 0.00

Total Exam Printing 0.00 0.00 0.00

Page 2

NC Board of CPA Examiners

08/02/18 Statement of Revenues & Expense - Budget v. Actual April 2018 through July 2018

Apr -Jul 18 Budget $ Over B ...

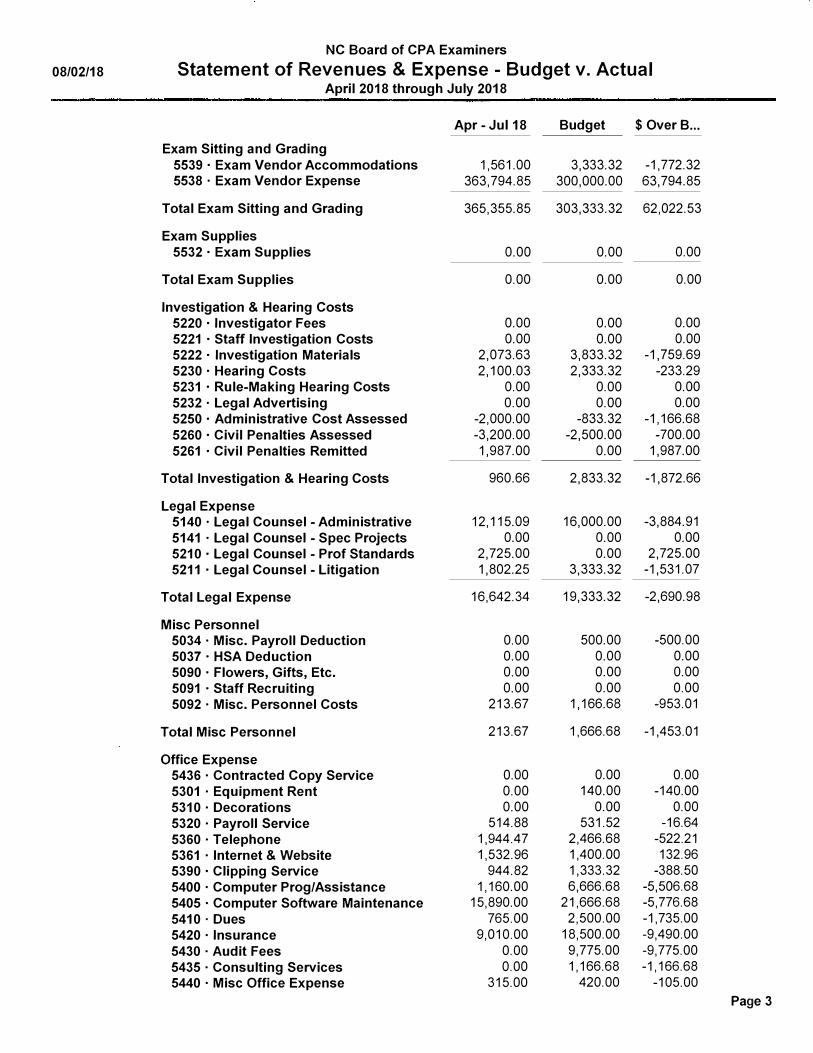

Exam Sitting and Grading 5539 · Exam Vendor Accommodations 1,561.00 3,333.32 -1,772.32

5538 · Exam Vendor Expense 363,794.85 300,000.00 63,794.85

Total Exam Sitting and Grading 365,355.85 303,333.32 62,022.53

Exam Supplies 5532 · Exam Supplies 0.00 0.00 0.00

Total Exam Supplies 0.00 0.00 0.00

Investigation & Hearing Costs 5220 · Investigator Fees 0.00 0.00 0.00

5221 · Staff Investigation Costs 0.00 0.00 0.00

5222 · Investigation Materials 2,073.63 3,833.32 -1,759.69

5230 · Hearing Costs 2,100.03 2,333.32 -233.29

5231 · Rule-Making Hearing Costs 0.00 0.00 0.00

5232 · Legal Advertising 0.00 0.00 0.00

5250 · Administrative Cost Assessed -2,000.00 -833.32 -1,166.68

5260 · Civil Penalties Assessed -3,200.00 -2,500.00 -700.00

5261 · Civil Penalties Remitted 1,987.00 0.00 1,987.00

Total Investigation & Hearing Costs 960.66 2,833.32 -1,872.66

Legal Expense 5140 · Legal Counsel - Administrative 12,115.09 16,000.00 -3,884.91

5141 · Legal Counsel - Spec Projects 0.00 0.00 0.00

5210 · Legal Counsel - Prof Standards 2,725.00 0.00 2,725.00

5211 · Legal Counsel - Litigation 1,802.25 3,333.32 -1,531.07

Total Legal Expense 16,642.34 19,333.32 -2,690.98

Misc Personnel 5034 · Misc. Payroll Deduction 0.00 500.00 -500.00

5037 • HSA Deduction 0.00 0.00 0.00

5090 • Flowers, Gifts, Etc. 0.00 0.00 0.00

5091 • Staff Recruiting 0.00 0.00 0.00

5092 · Misc. Personnel Costs 213.67 1,166.68 -953.01

Total Misc Personnel 213.67 1,666.68 -1,453.01

Office Expense 5436 · Contracted Copy Service 0.00 0.00 0.00

5301 · Equipment Rent 0.00 140.00 -140.00

5310 · Decorations 0.00 0.00 0.00

5320 · Payroll Service 514.88 531.52 -16.64

5360 · Telephone 1,944.47 2,466.68 -522.21

5361 · Internet & Website 1,532.96 1,400.00 132.96

5390 · Clipping Service 944.82 1,333.32 -388.50

5400 · Computer Prog/Assistance 1,160.00 6,666.68 -5,506.68

5405 · Computer Software Maintenance 15,890.00 21,666.68 -5,776.68

5410 · Dues 765.00 2,500.00 -1,735.00

5420 · Insurance 9,010.00 18,500.00 -9,490.00

5430 · Audit Fees 0.00 9,775.00 -9,775.00

5435 · Consulting Services 0.00 1,166.68 -1,166.68

5440 · Misc Office Expense 315.00 420.00 -105.00

Page 3

NC Board of CPA Examiners

08/02/18 Statement of Revenues & Expense - Budget v. Actual April 2018 through July 2018

Apr -Jul 18 Budget $ Over B ...

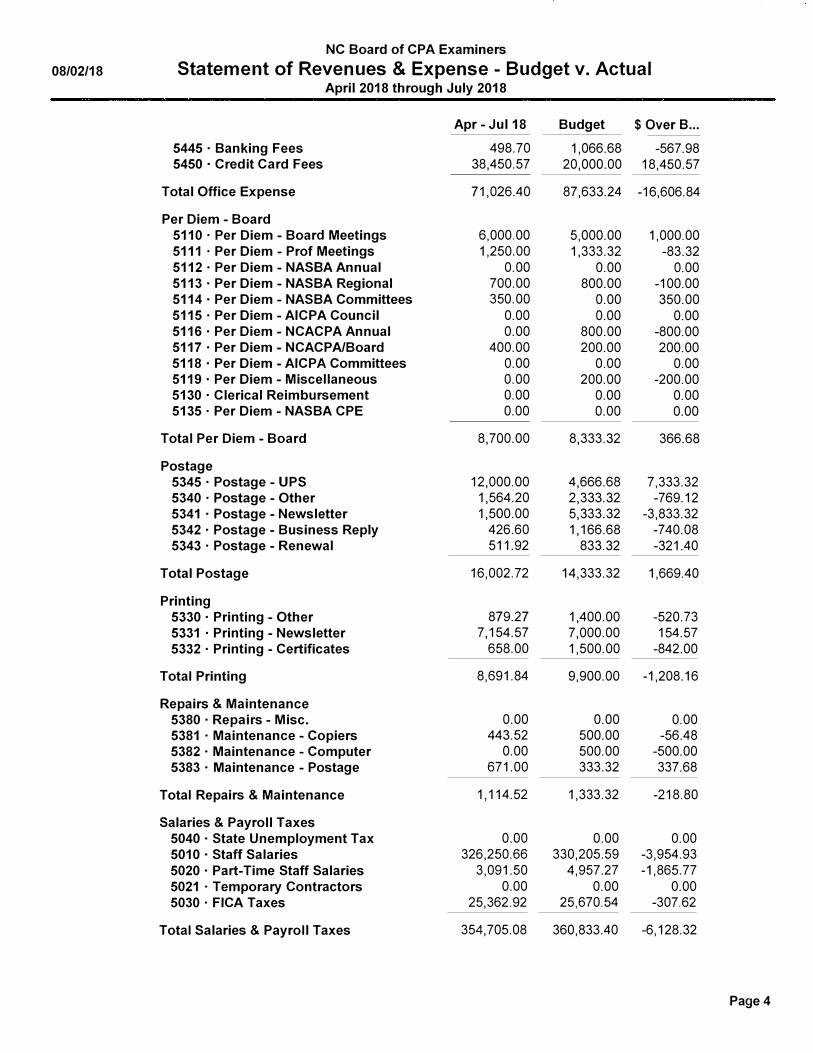

5445 · Banking Fees 498.70 1,066.68 -567.98

5450 · Credit Card Fees 38,450.57 20,000.00 18,450.57

Total Office Expense 71,026.40 87,633.24 -16,606.84

Per Diem -Board 5110 · Per Diem -Board Meetings 6,000.00 5,000.00 1,000.00

5111 · Per Diem -Prof Meetings 1,250.00 1,333.32 -83.32

5112 · Per Diem -NASBA Annual 0.00 0.00 0.00

5113 · Per Diem -NASBA Regional 700.00 800.00 -100.00

5114 · Per Diem -NASBA Committees 350.00 0.00 350.00

5115 · Per Diem -AICPA Council 0.00 0.00 0.00

5116 · Per Diem -NCACPA Annual 0.00 800.00 -800.00

5117 · Per Diem -NCACPA/Board 400.00 200.00 200.00

5118 · Per Diem -AICPA Committees 0.00 0.00 0.00

5119 · Per Diem -Miscellaneous 0.00 200.00 -200.00

5130 · Clerical Reimbursement 0.00 0.00 0.00

5135 · Per Diem -NASBA CPE 0.00 0.00 0.00

Total Per Diem -Board 8,700.00 8,333.32 366.68

Postage 5345 · Postage -UPS 12,000.00 4,666.68 7,333.32

5340 · Postage -Other 1,564.20 2,333.32 -769.12

5341 · Postage -Newsletter 1,500.00 5,333.32 -3,833.32

5342 · Postage -Business Reply 426.60 1,166.68 -740.08

5343 · Postage -Renewal 511.92 833.32 -321.40

Total Postage 16,002.72 14,333.32 1,669.40

Printing 5330 · Printing -Other 879.27 1,400.00 -520.73

5331 · Printing -Newsletter 7,154.57 7,000.00 154.57

5332 · Printing -Certificates 658.00 1,500.00 -842.00

Total Printing 8,691.84 9,900.00 -1,208.16

Repairs & Maintenance 5380 · Repairs -Misc. 0.00 0.00 0.00

5381 · Maintenance -Copiers 443.52 500.00 -56.48

5382 · Maintenance -Computer 0.00 500.00 -500.00

5383 · Maintenance -Postage 671.00 333.32 337.68

Total Repairs & Maintenance 1,114.52 1,333.32 -218.80

Salaries & Payroll Taxes 5040 · State Unemployment Tax 0.00 0.00 0.00

5010 · Staff Salaries 326,250.66 330,205.59 -3,954.93

5020 · Part-Time Staff Salaries 3,091.50 4,957.27 -1,865.77

5021 · Temporary Contractors 0.00 0.00 0.00

5030 · FICA Taxes 25,362.92 25,670.54 -307.62

Total Salaries & Payroll Taxes 354,705.08 360,833.40 -6, 128.32

Page4

NC Board of CPA Examiners

08/02/18 Statement of Revenues & Expense - Budget v. Actual April 2018 through July 2018

Apr -Jul 18 Budget $ Over B ...

Scholarships 5535 · Scholarship 0.00 0.00 0.00

Total Scholarships 0.00 0.00 0.00

Staff Travel 5060 · Staff Travel -Local 74.50 425.00 -350.50

5061 · Staff Travel -Prof Mtgs 453.84 658.32 -204.48

5062 · Staff Travel -NASBA CPE 0.00 0.00 0.00

5063 · Staff Travel -NASBA Ethics 0.00 0.00 0.00

5070 · Staff Travel -NASBA Annual 0.00 0.00 0.00

5071 · Staff Travel -NASBA Regional 4,168.76 3,864.00 304.76

5072 · Staff Travel -NASBA ED/Legal 0.00 0.00 0.00

5073 · Staff Travel -NASBA Committee 0.00 0.00 0.00

5074 · Staff Travel -AICPA 0.00 0.00 0.00

5075 · Staff Travel -NCACPA Meetings 0.00 333.32 -333.32

5076 · Staff Travel -NCACPA/Board 195.87 250.00 -54.13

5077 · Staff Travel -Clear/FARB Conf 0.00 0.00 0.00

Total Staff Travel 4,892.97 5,530.64 -637.67

Subscriptions/References 5370 · Subscriptions/References 1,549.72 1,166.68 383.04

Total Subscriptions/References 1,549.72 1,166.68 383.04

Supplies 5350 · Supplies -Office 3,626.20 1,246.68 2,379.52

5351 · Supplies -Copier 0.00 1,416.68 -1,416.68

5352 · Supplies -Computer 847.50 1,083.32 -235.82

5353 · Supplies -Special Projects 0.00 0.00 0.00

Total Supplies 4,473.70 3,746.68 727.02

5920 · Funded Depreciation 15,000.00 15,000.00 0.00

6999 · Uncategorized Expenses 0.00 0.00 0.00

9999 · Suspense 0.00 0.00 0.00

Total Expense 961,509.83 935,672.62 25,837.21 -- -

Net Ordinary Income 815,735.78 812,185.66 3,550.12

Other Income/Expense Other Income

8250 · Gift Card Revenue 0.00 1,250.00 -1,250.00

Interest Income 8500 · Interest Income -MMAs 2,044.72 1,000.00 1,044.72

8510 · Interest Income -CDs 9,110.60 8,333.32 777.28 �

Total Interest Income 11,155.32 9,333.32 1,822.00

8200 · Rental Income 14,255.60 14,325.32 -69.72

8920 · Gain on Sale of Fixed Assets 0.00 0.00 0.00

8921 · Loss on Sale of Fixed Assets 0.00 0.00 0.00

Total Other Income 25,410.92 24,908.64 502.28

Page 5

08/02/18

NC Board of CPA Examiners

Statement of Revenues & Expense - Budget v. Actual April 2018 through July 2018

Apr - Jul 18 Budget $ Over B ... -

Other Expense 7000 · Leasing Commission 0.00 0.00 0.00

Total Other Expense 0.00 0.00 0.00

Net Other Income 25,410.92 24,908.64 502.28

Change in Net Assets 841,146.70 837,094.30 4,052.40

Page6

08/02/18

NC Board of CPA Examiners

Statement of Revenues & Expenses Year-to-Date Comparison

Ordinary Income/Expense Income

Certificate Fees 4110 • Certificates - Initial 4120 · Certificates - Reciprocal 4140 · Certificates - Renewal Fees 4150 · Certificates - Reinst/Revoked 4151 · Certificates - Reinst/Surr

Total Certificate Fees

Exam Fee Revenue 4001 · Initial Adm Fees 4002 · Re-Exam Adm Fees 4004 · Exam Fees Revenue 4072 · Exam Scholarship Coupon

Total Exam Fee Revenue

Misc 4999 · Board Training 4970 · Duplicate Certificates 4990 · Miscellaneous

Total Misc

Partnership Fees 4260 · Partnership Registration Fees

Total Partnership Fees

Professional Corporation Fees 4250 · PC Registration Fees

Total Professional Corporation Fees

Total Income

Expense 6690 · Over & Short Fringe Benefits

5031 · Retirement - NCLB Contribution 5033 · Retirement - NCLB Administr 5035 · Health Ins. Premiums 5036 · Medical Reim Plan

Total Fringe Benefits

Apr - Jul 18 Apr - Jul 17

15,400.00

12,000.00

1,272,480.00

700.00

1,600.00

15,200.00

8,800.00

1,257,240.00

900.00

2,200.00

1,302,180.00 1,284,340.00

63,480.00

54,450.00

364,284.93

-9,387.20

472,827.73

63.75

125.00

379.13

567.88

570.00

570.00

1,100.00

1,100.00

1,777,245.61

-1.01

19,574.81

1,482.83

39,538.75

8,559.08

69,155.47

47,840.00

49,725.00

305,477.90

-7,973.15

395,069.75

0.00

350.00

150.00

500.00

0.00

0.00

1,900.00

1,900.00

1,681,809.75

0.80

18,072.65

666.33

36,805.28

4,512.85

60,057.11

Page 1

08/02/18

NC Board of CPA Examiners

Statement of Revenues & Expenses Year-to-Date Comparison

Board Travel 5120 · Board Travel - Board Meetings 5121 · Board Travel - Prof Meetings 5122 · Board Travel - NASBA Annual 5123 · Board Travel - NASBA Regional 5127 · Board Travel - NCACPA/Board 5129 · Miscellaneous Board Costs

Total Board Travel

Building Expenses 5800 · Building Maintenance 5801 · Electricity 5802 · Grounds Maintenance 5803 · Heat & Air Maintenance 5807 · Janitorial Maintenance

5808 · Pest Control Service 5809 · Security & Fire Alarm 5810 · Trash Collection 5811 · Water & Sewer

Total Building Expenses

Continuing Education -Staff 5050 · Continuing Education - Staff

Total Continuing Education -Staff

Exam Postage 5531 · Exam Postage

Total Exam Postage

Exam Sitting and Grading 5539 · Exam Vendor Accommodations 5538 · Exam Vendor Expense

Total Exam Sitting and Grading

Investigation & Hearing Costs 5222 · Investigation Materials 5230 · Hearing Costs 5250 · Administrative Cost Assessed 5260 · Civil Penalties Assessed 5261 · Civil Penalties Remitted

Total Investigation & Hearing Costs

Legal Expense 5140 · Legal Counsel - Administrative 5210 · Legal Counsel - Prof Standards 5211 · Legal Counsel - Litigation

Total Legal Expense

Apr -Jul18

6,707.90

392.27

0.00

4,586.08

0.00

100.29

11,786.54

180.34

4,168.84

668.00

606.00

2,232.35

129.00

1,985.00

14.10

324.45

10,308.08

590.00

590.00

341.28

341.28

1,561.00

363,794.85

365,355.85

2,073.63

2,100.03

-2,000.00

-3,200.00

1,987.00

960.66

12,115.09

2,725.00

1,802.25

16,642.34

Apr - Jul 17

5,972.36

280.32

554.80

9,568.67

1,102.68

178.26

17,657.09

163.50

3,696.99

6,005.00

606.00

2,050.10

150.00

1,800.00

-337.42

326.98

14,461.15

749.41

749.41

120.00

120.00

0.00

262,158.40

262,158.40

1,982.73

504.01

-2,600.00

-6,300.00

1,139.62

-5,273.64

9,008.00

0.00

2,350.00

11,358.00

Page 2

08/02/18

NC Board of CPA Examiners

Statement of Revenues & Expenses Year-to-Date Comparison

Apr - Jul 18 Apr - Jul 17

Misc Personnel 5034 · Misc. Payroll Deduction 5037 · HSA Deduction 5091 · Staff Recruiting 5092 · Misc. Personnel Costs

Total Misc Personnel

Office Expense 5320 · Payroll Service 5360 · Telephone 5361 · Internet & Website 5390 · Clipping Service 5400 · Computer Prog/Assistance 5405 · Computer Software Maintenance 5410 · Dues 5420 · Insurance 5435 · Consulting Services 5440 · Misc Office Expense 5445 · Banking Fees 5450 · Credit Card Fees

Total Office Expense

Per Diem - Board 5110 · Per Diem - Board Meetings 5111 · Per Diem - Prof Meetings 5113 · Per Diem - NASBA Regional 5114 · Per Diem - NASBA Committees 5117 · Per Diem - NCACPA/Board

Total Per Diem - Board

Postage 5345 · Postage - UPS 5340 · Postage - Other 5341 · Postage - Newsletter 5342 · Postage - Business Reply 5343 · Postage - Renewal

Total Postage

Printing 5330 · Printing - Other 5331 · Printing - Newsletter 5332 · Printing - Certificates

Total Printing

Repairs & Maintenance 5380 · Repairs - Misc. 5381 · Maintenance - Copiers 5383 · Maintenance - Postage

Total Repairs & Maintenance

0.00

0.00

0.00

213.67

213.67

514.88

1,944.47

1,532.96

944.82

1,160.00

15,890.00

765.00

9,010.00

0.00

315.00

498.70

38,450.57

71,026.40

6,000.00

1,250.00

700.00

350.00

400.00

8,700.00

12,000.00

1,564.20

1,500.00

426.60

511.92

16,002.72

879.27

7,154.57

658.00

8,691.84

0.00

443.52

671.00

1,114.52

0.00

0.00

299.00

226.52

525.52

429.52

2,067.58

1,304.96

899.00

5,385.00

14,766.96

920.00

9,020.00

2,250.00

315.00

935.63

37,733.28

76,026.93

4,800.00

200.00

1,500.00

400.00

600.00

7,500.00

4,000.00

566.50

13,400.00

150.00

180.00

18,296.50

330.88

13,660.75

758.50

14,750.13

281.70

240.54

646.00

1,168.24

Page 3

NC Board of CPA Examiners

08 /02 /18 Statement of Revenues & Expenses Year-to-Date Comparison

Apr -Jul18 Apr -Jul 17

Salaries & Payroll Taxes 5010 · Staff Salaries 326,250.66 301,215.66

5020 · Part-Time Staff Salaries 3,091.50 3,803.13

5030 · FICA Taxes 25,362.92 23,490.79

Total Salaries & Payroll Taxes 354,705.08 328,509.58

Staff Travel 5060 · Staff Travel -Local 74.50 104.26

5061 · Staff Travel - Prof Mtgs 453.84 429.01

5070 · Staff Travel - NASBA Annual 0.00 207.40

5071 · Staff Travel - NASBA Regional 4,168.76 6,741.13

5072 · Staff Travel - NASBA ED/Legal 0.00 22.62

5075 · Staff Travel - NCACPA Meetings 0.00 93.63

5076 · Staff Travel - NCACPA/ Board 195.87 326.30

Total Staff Travel 4,892.97 7,924.35

Subscriptions/References 5370 · Subscriptions/References 1,549.72 482.47

Total Subscriptions/References 1,549.72 482.47

Supplies 5350 · Supplies - Office 3,626.20 1,036.66

5351 · Supplies - Copier 0.00 816.69

5352 · Supplies - Computer 847.50 546.00

Total Supplies 4,473.70 2,399.35

5920 · Funded Depreciation 15,000.00 15,000.00

9999 · Suspense 0.00 0.00

Total Expense 961,509.83 833,871.39

Net Ordinary Income 815,735.78 847,938.36

Other Income/Expense Other Income

8250 · Gift Card Revenue 0.00 4,500.00

Interest Income 8500 · Interest Income - MMAs 2,044.72 2,209.49

8510 · Interest Income - CDs 9,110.60 5,433.27

Total Interest Income 11,155.32 7,642.76

8200 · Rental Income 14,255.60 13,840.40

8920 · Gain on Sale of Fixed Assets 0.00 120.00

Total Other Income 25,410.92 26,103.16

Net Other Income 25,410.92 26,103.16

Change in Net Assets 841,146.70 874,041.52

Page4

Bob Brooks

From:

Sent:

To:

Cc:

Subject:

All,

Randy Ross < [email protected]>

Tuesday, July 31, 2018 11:27 AM

ITEM III A

Abigail Gaskins; Ana Garcia; Andy L. Wright; Brenda Turley; Catherine M. Carroll; Charles

Satterlund; Cheryl Pezon; Clifford Cooks; Cori Hondolero; D. Boyd Busby; Dan

Sweetwood; Darla M. Saux; David Sanford; Dennis L. Gring; Doreen Frost; Doris Cubitt;

Edwin Ramos; Erin Karow; Grace Berger; James Corley; James Koehl; Jeanette Contreras;

Jennifer Winters; Jim Abbott; John E. Patterson; Jovanna Edwards; Kent Absec; Kimberly

Gaedeke; Laureen M Kai; Linda Capuchino; Luis Barreto; Michela Ross; Monica L.

Petersen; Nathalie Hodge; Nicole Kasin; Pamela Ivey; Patti Bowers; Paul Ziga; Richard C.

Carroll; Richard M. Hurlburt; Robert E. Lampe; Bob Brooks; Robyn Barkdull; Russ

Friedewald; Sara Fox; Susan L. Somers; Thomas DeGroodt; Veloria Kelly; Viki A.

Windfeldt; Wade A. Jewell; Wendy S. Garvin; William Treacy

[email protected]; Patricia Hartman

ED update

At the Board of Directors meeting it was decided to not to have a single regional conference at this time. We will

continue to have an Eastern and Western regional. There was a lot of good conversation with pros and cons but

ultimately this was the decision. Additionally, Ken announced that there was not support to move forward with the

alternate pathway proposal as discussed at our previous meetings. He wrote an article in the state board report that all

of you should have received by now. It is titled "That dog wont hunt". All recognized that we need to address the

changing work environment in our profession as it relates to IT and data analytics. There will be more discussion about

this in the future.

I will attend the summit with the AICPA and NABA leadership later this week. It will be an interesting meeting.

Also, it is my understanding that the CPE program that was moved to the Association is being moved back to the

Institute soon. Certificates will be changed to clearly denote that it is from the American Institute. The Institute is

continuing to work on the rebranding effort as Sue Coffey explained at the regionals to clearly denote that the guidance

areas that we depend on authoritative information is coming from the American Institute.

Just a note to keep everyone up to date.

That is all

Randall A. Ross MBA CPA

Executive Director

Oklahoma Accountancy Board

405-522-4464

1

"That Dog Ain't Gonna Hunt!" For many months we have been discussing the impact of technology on the accounting profession

and, specifically, considering a new"technology pathway"to become a CPA. The culmination of

that process for NASBA took place at the Regional Meetings, where thoughtful and passionate

discussions occurred. Saying that there was a "lack of support" for the two-path concept would

be an understatement: In fact, there was strong and consistent opposition to the concept. As my

old grandpa used to say: "That dog ain't gonna hunt!" After listening to and reflecting upon your

feedback, by the end of the Western Regional Meeting I had advised NASBA's governance leadership

that I no longer supported pursuing the two-pathway concept and suggested we consider a new

approach. Chair Ted Long has placed this as a major item on the agenda for the NASBA Board of

Directors' meeting in July.

So where does that leave us? First, let me state that leadership was very pleased with the robust

debate that occurred at the Regional breakouts and in other forums across the country. While it

Ken L. Bishop

President & CEO

became obvious that the proposal, admittedly a somewhat radical idea, was unacceptable to most of our Boards, there

was a clear consensus that we need to do something. The comments we heard most frequently were: "We are glad NASBA

and AICPA are focusing on this issue" and, "The current pathway needs to be modified to address the use and reliance on

technology:' The responses from the Boards were not inconsistent with the feedback from recent AICPA Council meetings.

Similarly, from the discussions that I have had with individuals, large firms, state societies and several other stakeholder

groups, the support for evolving the current pathway to become a CPA is prevalent.

It was clear to me that many of our volunteers came to the meetings well prepared to discuss this initiative. The

insightful comments we received included suggestions and recommendations to be considered in lieu of the proposed

technology pathway. NASBA staff have been consolidating and categorizing those comments as we prepare for leadership

meetings with the AICPA to consider next steps. I am hopeful that we can refocus our efforts without losing the momentum

resultant from the work to this point.

We have already b1

egun discussions with our AICPA counterparts, both volunteers and staff, about the ideas and

opportunities that developed during the exposure process. Those discussions will be formalized at the upcoming AICPA/

NASBA Summit in August and in senior staff preparation meetings for the Summit. I am optimistic that we can quickly pivot

to a new course of action that addresses the need for change with as little disruption to the current pipeline and marketplace

as possible. Hopefully, we will have a new approach fleshed out by the NASBA Annual Meeting in late October.

I am writing this President's Memo near the end of our fiscal year -- and what a year it has been! Beyond the technology

discussions, this has been a year of development and implementation of several major IT projects, the completion of the

NASBA buildout at our Nashville offices, the opening of our new Guam testing and call centers, and a restructuring of several

of our business and service operations.

For most of us at NASBA, the pinnacle measurement of a successful year is our relationship with you, our member

Boards. This year we had a record 54 states and territories represented at the NASBA Annual Meeting and 51 participated

in this year's Regional Meetings. Other records include the number of requests for assistance by State Boards, the amount

(nearly $10 million) of mission spending in support of State Boards, the number of Student Chapters (now 40) in our Center

for the Public Trust subsidiary and, finally, we have continued to grow NASBA's net assets to a record amount, assuring we

can continue to fulfill our mission to support Boards of Accountancy. This is my opportunity to say "thank you" to the many

NASBA volunteers who helped make all of this possible, and for the support and trust given me again this year.

Mark your calendars for what is going to be an informative and truly memorable 111 th NASBA Annual Meeting in

Scottsdale, AZ, on October 28-31.

Semper ad mefiora (Always toward better things).

President& CEO

Page 1 of 3

REGIONAL DIRECTORS' FOCUS QUESTIONS ITEM Ill B

To State Board Chairs/Presidents, Members and Executive Directors:

The input received from our Focus Questions is reviewed by all members of NASBA 's Board of Directors, committee chairs and executive staff and used to guide their actions. Please

submit your Board's responses by October 16, 2018.

,... GENERAL INFORMATION -------------------.

Name of person submitting form:* rtiobert N Brooks

Board of Accountancy: * �--------------------·, Please select...

Ai Alab ama State Board of Public Accountancy Alaska Board of Public Accountancy v 1

1

�A _ri _zo_n_a_S_t_a _te_B_ o_ a_rd_of_A_ c_co_u _nt_a_nc�:y ________ __

Email:* �[email protected]

QUESTIONS -----------------------1. Has legislation that seeks to deregulate professions been introduced in your state? If so,please give details.

@ No legislation proposed in my state. 0 Yes.

Please explain below: egislation introduced to increase financial oversight of occupational boards but it died

·n committee.

2. It has been mentioned that many colleges are bringing IT courses into their accountingprograms. (a) Can you identify any schools in your jurisdiction which have doneso?IM2ost of the 16 A

j{JNc system v

https://nasba.tfaforms.net/327355 8/3/2018

Page 2 of 3

(b) Does your Board permit IT courses to be counted as accounting or business courses?Accounting - YesAccounting - No

(!) Business - Yes Business - No

( c) If so, are there additional criteria those courses must meet?

3. (a) As your rules are currently written, could your candidates take the Uniform CPAExamination continuously throughout the year?

Yes. (!) No. Changes would be required.

(b) Can they only take sections once per window?(tt) Yes

No

4. What is happening in your jurisdiction that is important for other State Boards andNASBA to know about?µoint Task Force with State CPA Association to review all CPE rules

5. Can NASBA be of any assistance to your Board at this time?C!)No

Yes. Please explain below.

6. NASBA's Board of Directors would appreciate as much input on the above questionsas possible. How were the responses shown above compiled? Please check all that apply.

Input only from Board Chair. Input only from Executive Director. Input only from Board Chair and Executive Director.

Fil Input from all Board Members and Executive Director. Input from some Board Members and Executive Director. Input from all Board Members. Input from some Board Members. Other (please explain).

https ://nasba. tfaforms.net/3 2 73 5 5 8/3/2018

ITEM IV B

DEPARTMENT OF NATURAL AND CULTURAL RESOURCES

DIVISION OF ARCHIVES AND RECORDS

GOVERNMENT RECORDS SECTION

Memorandum

Date: 7/24/2018

Initials Date

TO: Bob Brooks

Samuel Williams

Please return to Emily Sweitzer, Government Records, 4615 Mail Service Center, Raleigh NC 27699-4615.

FROM:

SUBJECT:

Emily Sweitzer Government Records

Records Retention and Disposition Schedule

Attached for approval and signature is the signature page for the 2018 Functional Schedule for North Carolina State Agencies. The functional schedules listed on the signature page have been identified as representative of your agency's function and records, and may be found at the following URL: https: / /archives. ncdcr.gov I documents/functionalschedule-state-agencies

Signatures of approval within your department are required by Chapter 121-S(c) of the General Statutes of North Carolina.

*After approval and comments, please route back to EmilySweitzer.

NC BOARD OF

JUL 3 0 2018

CPA EXAMINERS

4615 Mail Service Center

Raleigh, NC 27699-4615

Phone:

Fax:

919-807-7358919-715-3627

Courier: 51-81-20

emily. [email protected]

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANT EXAMINERS

RECORDS RETENTION AND DISPOSITION SCHEDULE

The retention periods governing the records series found on the following functional records schedules are hereby approved. In accordance with the provisions of Chapters 121 and 132 of the North Carolina

General Statutes, it is agreed that the records of the

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANT EXAMINERS

do not and will not have further official use or value for administrative, research, or reference purposes after the respective retention periods specified herein. The Department of Natural and Cultural Resources (DNCR) consents to the destruction or other disposition of these records in accordance with the retention and disposition instructions specified in the following schedules:

1. Agency Management2. Asset Management5. Financial Management6. Governance8. Human Resources9. Information Technology12. Legal13. Monitoring and Compliance15. Public Relations16. Risk Management

Public records including electronic records not listed on an approved functional schedule are not authorized to be destroyed. The retention periods established in these functional schedules should be interpreted as minimums. If an agency chooses to retain records longer than required in the disposition instructions, this practice should be documented in internal agency procedures. In all cases, agencies must maintain logs documenting destructions. The presence of a records series on one of these schedules does not obligate an agency to create that record; however, if a record is not represented on any of these schedules, an agency may not destroy it without explicit authorization from DNCR.

References to confidentiality throughout the standards of the functional schedule are not meant to be exhaustive. Consult your legal counsel for questions concerning the disclosure of records. No claim of confidentiality of records can be made without specific regard to a state or federal authority.

DESTRUCTIONS

G.S. § 121-5 authorizes the Department of Natural and Cultural Resources to regulate the destruction of public records. Furthermore, Rule 04M .0510 of Title 7 of the North Carolina Administrative Code states:

"(a) Paper records which have met their required retention requirements and are not subject to legal or other audit holds should be destroyed in one of the following ways:

1. burned, unless prohibited by local ordinance;2. shredded, or torn up so as to destroy the record content of the documents or material

concerned;3. placed in acid vats so as to reduce the paper to pulp and to terminate the existence of the

documents or materials concerned; or4. sold as waste paper, provided that the purchaser agrees in writing that the documents or

materials concerned will not be resold without pulverizing or shredding the documents sothat the information contained within cannot be practicably read or reconstructed.

(b) When used in an approved records retention and disposition schedule, the provision thatelectronic records are to be destroyed means that the data and metadata are to be overwritten,deleted, and unlinked so the data and metadata may not be practicably reconstructed.(c) When used in an approved records retention and disposition schedule, the provision thatconfidential records of any format are to be destroyed means the data, metadata, and physical

July 1, 2018

Page 1 of 4

media are to be destroyed in such a manner that the information cannot be read or reconstructed under any means."

For all records with a specified retention period, State agencies must maintain a destructions log as part of the Records Management File.

Public records, including electronic records, not listed in this schedule are not authorized to be

destroyed.

AUDITS AND LITIGATION ACTIONS

Records subject to audit or those legally required for ongoing official proceedings must be retained until released from such audits or official proceedings.

ELECTRONIC RECORDS

State agencies should consider retention requirements and disposition authorities when designing and implementing electronic records management systems. Any type of electronically-created or electronically-stored information falls under the North Carolina General Assembly's definition of public records cited above. For example, e-mail, text messages, blog posts, voicemails, websites, word processing documents, spreadsheets, databases, and PDFs all fall within this definition of public records. In addition, G.S. § 132-6.1 (a) specifies:

"Databases purchased, leased, created, or otherwise acquired by every public agency containing public records shall be designed and maintained in a manner that does not impair or impede the public agency's ability to permit the public inspection and examination of public records and provides a means of obtaining copies of such records. Nothing in this subsection shall be construed to require the retention by the public agency of obsolete hardware or software."

State agencies may scan any paper record and retain it electronically for ease of retrieval. If an agency wishes to destroy the original paper records before their assigned retention periods have been met, the agency must establish an electronic records policy, including putting into place internal procedures for quality assurance and documentation of authorization for records destructions. This electronic records policy must be approved by the Government Records Section. Agencies should be aware that for the purpose of any audit, litigation, or public records request, they are considered the records custodian obligated to produce requested records, even if said records are being maintained electronically by an outside vendor. Therefore, contracts regarding electronically stored information should be carefully negotiated to specify how records can be exported in case a vendor goes out of business or the agency decides to award the contract to a different vendor.

RECORD COPY

A record copy is defined as "The single copy of a document, often the original, that is designated as the official copy for reference and preservation." 1 The record copy is the one whose retention and disposition is mandated by these functional schedules; all additional copies are considered reference or access copies and can be destroyed when their usefulness expires. In some cases, postings to social media may be unofficial copies of information that is captured elsewhere as a record copy (e.g., a press release about an upcoming agency event that is copied to various social media platforms). Appropriately retaining record copies and disposing of reference copies requires agencies to designate clearly what position or office is required to maintain an official record for the duration of its designated retention period. In identified cases where records overlap between state agencies, the State Archives specifies on the schedules which agency is considered the record owner.

TRANSITORY RECORDS

Transitory records are defined as "record[s] that [have] little or no documentary or evidential value and that need not be set aside for future use."2

North Carolina has a broad definition of public records. However, the Department of Natural and Cultural Resources recognizes that some records may have little or no long-term documentary or evidential value

1 Richard Pearce-Moses, A Glossary of Archival and Records Terminology {2005) 2 Ibid.

July 1, 2018

Page 2 of 4

to the creating agency. These records are often called transitory records. They may be disposed of according to the guidance below. However, all public employees should be familiar with the Functional Schedules for North Carolina State Agencies and any other applicable guidelines for their office. If there is a required retention period for these records, that requirement must be followed. When in doubt about whether a record is transitory or whether it has special significance or importance, retain the record in question and seek guidance from the DNCR records analyst assigned to your agency.

Routing slips and transmittal sheets adding no information to that contained in the transmitted material have minimal value after the material has been successfully transmitted. These records may be destroyed or otherwise disposed of after receipt of the material has been confirmed. Similarly, "while you were out" slips, memory aids, and other records requesting follow-up actions (including voicemails and calendar invites) have minimal value once the official action these records are supporting has been completed and documented. These records may be destroyed or otherwise disposed of once the action

has been resolved.

Drafts and working papers, including notes and calculations, are materials gathered or created to assist in the creation of another record. All drafts and working papers are public records subject to all provisions of Chapter 132 of the General Statutes, but many of them have minimal value after the final version of the record has been approved, and may be destroyed after final approval, if they are no longer necessary to support the analysis or conclusions of the official record. Drafts and working documents that may be destroyed after final approval include:

• Drafts and working papers for internal administrative reports, such as daily and monthly activity

reports;

• Drafts and working papers for internal, non-policy-level documents, such as informal workflows

and manuals; and

• Drafts and working papers for presentations, workshops, and other explanations of agency policy

that is already formally documented.

Forms used solely to create, update, or modify records in an electronic medium may be destroyed in office after completion of data entry and after all verification and quality control procedures, so long as these records are not required for audit or legal purposes. However, if the forms contain any analog components that are necessary to validate the information contained on them (e.g., a signature or notary's seal), they must be retained according to the disposition instructions for the records series encompassing the forms' function.

HISTORICAL VALUE

The term historical value is used interchangeably with archival value. The SAA Glossary of Archival and

Records Terminology defines it as "the importance or usefulness of records that justifies their continued preservation because of the enduring administrative, legal, fiscal, or evidential information they contain."3

There are certain record types on these schedules about which the Government Records Section is giving the creating agency the discretion to determine historical value. These items are indicated with a disposition of Permanent but also have a companion item that allows for the destruction of routine items when their reference value ends. Advertisements and press releases are two good examples - there will be some ads and press releases associated with agency events or initiatives that have historical value and should be retained permanently, while there will be many more of a rather mundane nature that can be destroyed when they have no further value to the creating agency. Two criteria for determining historical value are inherent interest and extraordinary documentation:

• Inherent interest is created by non-routine events, by the involvement of famous parties, and by

compelling contexts. For instance, foreclosure proceedings from the 1930s have high historical

value because they date from the era of the Great Depression.

• Extraordinary documentation is found in records that shed light on political, public, or social

history. For instance, the records from the replevin case that returned the Bill of Rights to North

3 Ibid.

July 1, 2018

Page 3 of 4

Carolina hold more historical value than most property case files because of the political history

intertwined with this case.

Records with historical value are identified with one of three designations in the Disposition Instructions: • PERMANENT: These records will be retained in office permanently.

• PERMANENT (appraisal required): When these records no longer have administrative value in

office, the agency will contact the Government Records Section so the records can be appraised

by a records analyst and an appraisal archivist. These individuals will determine whether the

records should be retained in office permanently or transferred to the custody of the State

Archives of North Carolina.

of administrative value in office

/'\ I Records

/ Mdl�tand

contact Reeords Appraisal 1---_..., Analyst at the State 1-----, Archivist

Arhives \ appraii;e \historical value

\ of reco(ds

:.'m:hival matei�ls are transferred to the rustod·,. of the

State Arthlves

Remaining mateials are

retained permanently in

offic:e

• PERMANENT (archival): These records will transfer to the State Records Center so they can betransferred to the custody of the State Archives of North Carolina.

As with any situation in which a state agency has questions about the records it produces and maintains, the records analyst assigned to the agency is available for consultation on decisions about historical value.

The State Board of Certified Public Accountant Examiners agrees to destroy, transfer or dispose of records as specified herein. This schedule is to remain in effect until superseded. If the required functions of the agency change, the agency must contact a records analyst to have this agreement amended.

APPROVAL RECOMMENDED

Robert N. Brooks Executive Director

L. Samuel Williams, Jr., PresidentState Board of Certified Public Accountant

Examiners

July 1, 2018

APPROVED

Page 4 of 4

Sarah E. Koonts, Director Division of Archives and Records

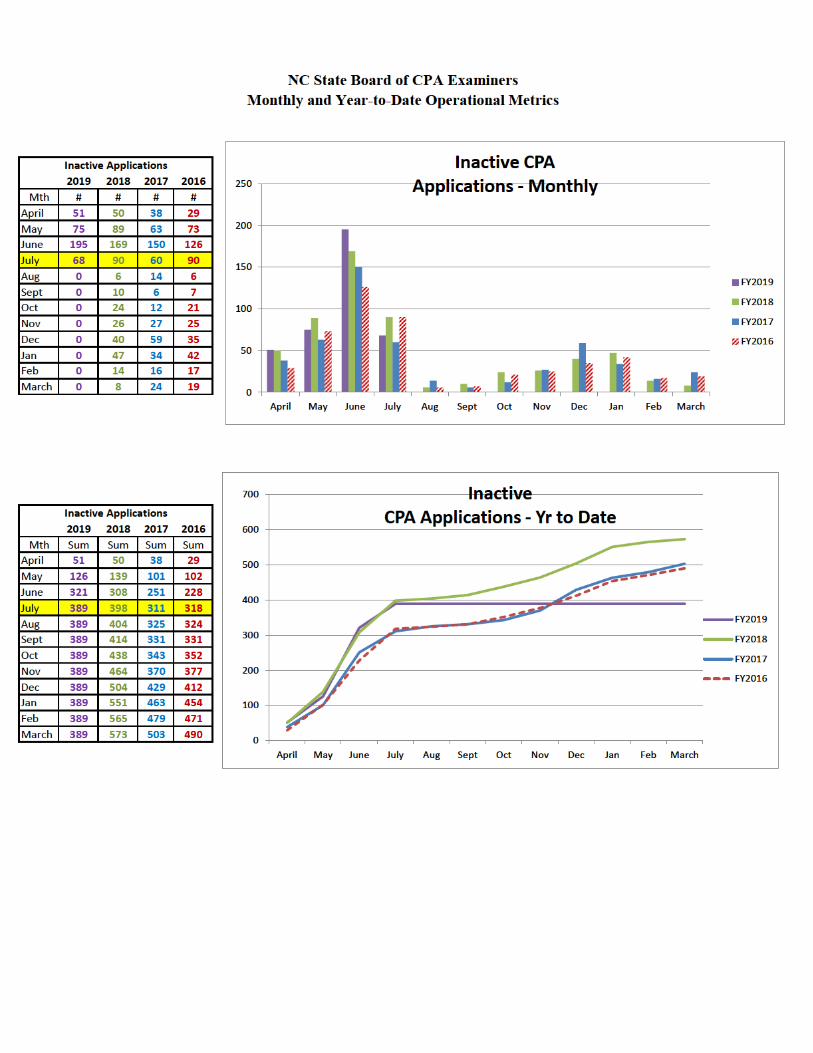

Month Original Re-Exam Month Original Reciprocal Month Total Month Begin Bal Open Closed End Bal Month TotalJan-15 107 130 Jan-15 96 51 Jan-15 18 Jan-15 202 66 54 214 Jan-15 47Feb-15 62 110 Feb-15 64 16 Feb-15 20 Feb-15 214 22 40 196 Feb-15 13Mar-15 82 227 Mar-15 48 4 Mar-15 12 Mar-15 196 40 38 198 Mar-15 18Apr-15 97 180 Apr-15 48 61 Apr-15 18 Apr-15 198 7 38 167 Apr-15 29

May-15 78 151 May-15 40 11 May-15 11 May-15 167 26 18 175 May-15 73Jun-15 77 312 Jun-15 0 4 Jun-15 17 Jun-15 175 6 21 160 Jun-15 126Jul-15 66 178 Jul-15 60 54 Jul-15 13 Jul-15 160 10 32 138 Jul-15 90

Aug-15 52 155 Aug-15 100 21 Aug-15 11 Aug-15 138 31 27 142 Aug-15 6Sep-15 51 296 Sep-15 44 5 Sep-15 25 Sep-15 142 27 33 136 Sep-15 7Oct-15 64 154 Oct-15 74 70 Oct-15 13 Oct-15 136 53 32 157 Oct-15 21Nov-15 62 151 Nov-15 45 27 Nov-15 14 Nov-15 157 26 25 158 Nov-15 25Dec-15 139 276 Dec-15 0 2 Dec-15 22 Dec-15 158 9 24 143 Dec-15 35Jan-16 121 139 Jan-16 133 36 Jan-16 28 Jan-16 143 12 17 138 Jan-16 42Feb-16 101 141 Feb-16 68 12 Feb-16 16 Feb-16 138 17 21 134 Feb-16 17Mar-16 92 305 Mar-16 43 3 Mar-16 17 Mar-16 134 34 19 149 Mar-16 19Apr-16 97 191 Apr-16 60 69 Apr-16 3 Apr-16 149 27 31 145 Apr-16 38

May-16 85 203 May-16 42 18 May-16 14 May-16 145 16 23 138 May-16 63Jun-16 110 266 Jun-16 0 2 Jun-16 8 Jun-16 138 33 20 151 Jun-16 150Jul-16 74 204 Jul-16 96 53 Jul-16 6 Jul-16 151 17 42 126 Jul-16 60

Aug-16 85 237 Aug-16 36 8 Aug-16 14 Aug-16 126 68 27 167 Aug-16 14Sep-16 83 297 Sep-16 42 4 Sep-16 8 Sep-16 167 65 27 205 Sep-16 6Oct-16 60 177 Oct-16 56 82 Oct-16 9 Oct-16 205 53 53 205 Oct-16 12Nov-16 104 183 Nov-16 72 32 Nov-16 14 Nov-16 205 22 72 155 Nov-16 27Dec-16 115 276 Dec-16 0 4 Dec-16 30 Dec-16 155 7 26 136 Dec-16 59Jan-17 129 189 Jan-17 108 34 Jan-17 24 Jan-17 136 35 49 122 Jan-17 34Feb-17 58 130 Feb-17 66 17 Feb-17 18 Feb-17 122 17 30 109 Feb-17 16Mar-17 67 276 Mar-17 70 12 Mar-17 19 Mar-17 109 16 22 103 Mar-17 24Apr-17 55 178 Apr-17 32 68 Apr-17 7 Apr-17 103 30 25 108 Apr-17 50

May-17 58 182 May-17 51 9 May-17 12 May-17 108 24 16 116 May-17 89Jun-17 57 159 Jun-17 0 1 Jun-17 16 Jun-17 116 5 18 103 Jun-17 169Jul-17 38 146 Jul-17 68 58 Jul-17 19 Jul-17 103 36 16 123 Jul-17 90

Aug-17 50 187 Aug-17 39 4 Aug-17 22 Aug-17 123 65 29 159 Aug-17 6Sep-17 59 267 Sep-17 42 2 Sep-17 14 Sep-17 159 29 42 146 Sep-17 10Oct-17 47 196 Oct-17 62 93 Oct-17 23 Oct-17 146 24 17 153 Oct-17 24Nov-17 79 126 Nov-17 46 25 Nov-17 15 Nov-17 153 7 18 142 Nov-17 26Dec-17 79 154 Dec-17 0 24 Dec-17 15 Dec-17 142 6 23 125 Dec-17 40Jan-18 131 178 Jan-18 117 12 Jan-18 30 Jan-18 125 18 15 128 Jan-18 47Feb-18 39 107 Feb-18 73 20 Feb-18 18 Feb-18 128 16 11 133 Feb-18 14Mar-18 66 236 Mar-18 36 5 Mar-18 10 Mar-18 133 14 14 133 Mar-18 8

Exam Applications Certificate Applications CPA Firm Registrations Professional Stds Cases Inactive

Month Original Re-Exam Month Original Reciprocal Month Total Month Begin Bal Open Closed End Bal Month Total

Exam Applications Certificate Applications CPA Firm Registrations Professional Stds Cases Inactive

Apr-18 70 211 Apr-18 32 52 Apr-18 12 Apr-18 133 27 16 144 Apr-18 51May-18 78 136 May-18 61 13 May-18 13 May-18 144 95 44 195 May-18 75Jun-18 61 149 Jun-18 0 0 Jun-18 7 Jun-18 195 61 68 188 Jun-18 195Jul-18 67 236 Jul-18 57 59 Jul-18 3 Jul-18 188 58 54 192 Jul-18 68

Aug-18 0 0 Aug-18 0 0 Aug-18 0 Aug-18 192 0 0 192 Aug-18 0Sep-18 0 0 Sep-18 0 0 Sep-18 0 Sep-18 192 0 0 192 Sep-18 0Oct-18 0 0 Oct-18 0 0 Oct-18 0 Oct-18 192 0 0 192 Oct-18 0Nov-18 0 0 Nov-18 0 0 Nov-18 0 Nov-18 192 0 0 192 Nov-18 0Dec-18 0 0 Dec-18 0 0 Dec-18 0 Dec-18 192 0 0 192 Dec-18 0Jan-19 0 0 Jan-19 0 0 Jan-19 0 Jan-19 192 0 0 192 Jan-19 0Feb-19 0 0 Feb-19 0 0 Feb-19 0 Feb-19 192 0 0 192 Feb-19 0Mar-19 0 0 Mar-19 0 0 Mar-19 0 Mar-19 192 0 0 192 Mar-19 0Apr-19 0 0 Apr-19 0 0 Apr-19 0 Apr-19 192 0 0 192 Apr-19 0

May-19 0 0 May-19 0 0 May-19 0 May-19 192 0 0 192 May-19 0Jun-19 0 0 Jun-19 0 0 Jun-19 0 Jun-19 192 0 0 192 Jun-19 0

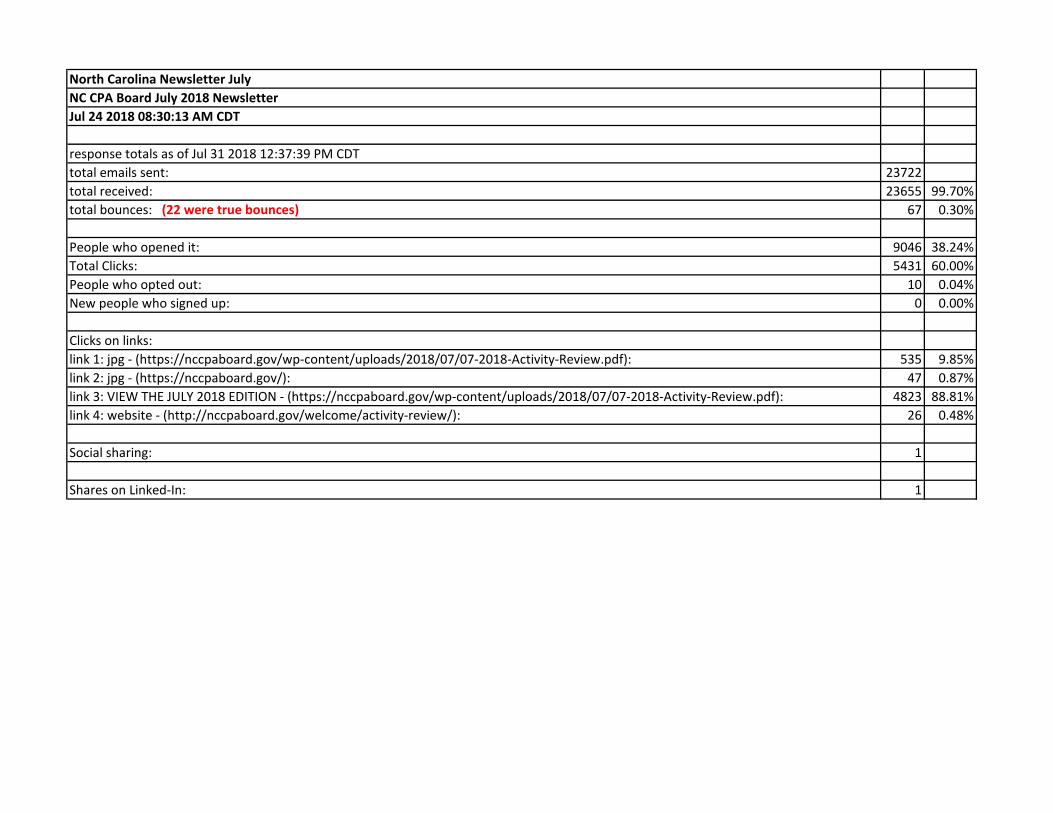

North Carolina Newsletter JulyNC CPA Board July 2018 NewsletterJul 24 2018 08:30:13 AM CDT

response totals as of Jul 31 2018 12:37:39 PM CDTtotal emails sent: 23722total received: 23655 99.70%total bounces: (22 were true bounces) 67 0.30%

People who opened it: 9046 38.24%Total Clicks: 5431 60.00%People who opted out: 10 0.04%New people who signed up: 0 0.00%

Clicks on links:link 1: jpg - (https://nccpaboard.gov/wp-content/uploads/2018/07/07-2018-Activity-Review.pdf): 535 9.85%link 2: jpg - (https://nccpaboard.gov/): 47 0.87%link 3: VIEW THE JULY 2018 EDITION - (https://nccpaboard.gov/wp-content/uploads/2018/07/07-2018-Activity-Review.pdf): 4823 88.81%link 4: website - (http://nccpaboard.gov/welcome/activity-review/): 26 0.48%

Social sharing: 1

Shares on Linked-In: 1

EXECUTIVE STAFF REPORT JULY 2018

Service to the Board: Julia has completed her first year of her second term of employment with the Board. Thanks for your service, Julia.

Breakfast with the NCACPA: On July 10, Bob and David had their monthly meeting with the NCACPA’s Sharon Bryson and Mark Soticheck.

NCACPA Recognition Dinner: Bob and David attended the annual NCACPA Recognition Dinner held on July 31 at the JW Marriott in Raleigh. Board members L. Samuel Williams, Jr., CPA; Arthur M. Winstead, Jr, CPA; and Wm. Hunter Cook, CPA;also attended.

ITEM IX-C