public sector trends report - ipa

TRANSCRIPT

Research Paper Nº8

Public Sector Trends 2012

State of the Public Service Series

November 2012

Richard Boyle

0

120

100

80

60

40

20

0

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1

Public Sector Trends 2012

State of the Public Service Series

November 2012

Research Paper Nº8

Public Sector Trends 2012Richard Boyle

2

Public Sector Trends 2012

3

Public Sector Trends 2012

Foreword 4

Main findings 5

1. Introduction 9

2. The size and cost of the public sector 11

3. The quality of public administration 21

4. Public service efficiency and performance 27

5. Trust and confidence in public administration 42

6. Conclusion 46

References 47

Appendix 1 Indicators used to make up the Public Administration Quality indicator 48

Contents

Dr. Richard Boyle is Head of Research, Publishing and Corporate Relations with the Institute of Public

Administration. He has written extensively on public service reform and on the evaluation of public services.

4

Public Sector Trends 2012

In the State of the Public Service research series, we seek to provide evidence-informed research and commentary

on key aspects of contemporary Irish public administration. The authors of these reports bring their considerable

expertise and practical knowledge to the topics selected so as to provide evidence, insights and recommendations to

support future development. Our aim is that these reports will not only inform, but also challenge current thinking

about how the Irish public service performs. It is intended that these short research reports will be of relevance and

use not only to public servants, but also to policy makers and the wider public.

This report examines trends in public sector development and is the third in our annual series. The intention is

to help inform the debate on Ireland’s public sector and public administration, and its role in Irish society. There

has been much talk recently about the continued relevance of the Public Service (Croke Park) Agreement and the

role and efficiency of public servants. Much of the discussion takes place based on anecdote, without accessing

information on how the public sector is performing and how it compares internationally.

Here we try to bring some evidence to bear on the important debate on the future shape and size of the public

sector. Using data gathered from a number of sources, information on the size and cost of the public sector, the

quality of public administration, efficiency and performance, and levels of trust and confidence is presented in a

simple but rigorous manner.

Foreword

Brian CawleyDirector GeneralInstitute of Public Administration

5

Public Sector Trends 2012

Main findings

In terms of overall performance, the data presented in this paper would tend to suggest that the quality of Ireland’s public

administration remains close to the average for the European Union. Indeed, there are some signs that aspects of quality

are seen as having improved in recent times. This is a notable achievement for a small state such as Ireland, especially at

a time of reducing numbers of public servants and limited resources available for public services.

The size and cost of the public sector

• From 2008 to 2010, as GDP shrank as a result of the recession in Ireland, Ireland’s government expenditure as a

percentage of GDP increased rapidly. In 2011, however, expenditure as a percentage of GDP dropped to 48.1 per cent,

just a little below the European average. Using GNI (gross national income) rather than GDP, the size of the public sector

has been above the EU average since 2008. In 2011 government expenditure as a percentage of GNI was 59.1 per cent.

This is the highest level in the EU, above Denmark at 57.9 per cent of GDP.

• Public expenditure per head of population, which had been growing significantly faster than the EU average up to

2010, fell back in 2011. It is still above the European average, but is now closer to the average.

• There has been a significant drop in the numbers employed in both the public sector and public service from 2008,

with a drop of around 8 per cent in each case. Numbers employed in the public sector and public service in 2012 are

now back down to close to 2005 levels of employment.

• Two out of every three people employed in the public service work in either health or education. In 2012, there were

approximately 102,000 people employed in the health sector and 92,000 people employed in the education sector.

• Numbers have fallen in all sectors since 2008. The biggest drop proportionally has been in the non commercial state

agencies (19 per cent), local authorities (14 per cent) and the justice sector (13 per cent). The smallest drop proportionally

has been in the education sector (3 per cent).

• A growing population and shrinking public workforce mean that public sector employees per 000 population has

been dropping since 2008 and is at 73.6 public sector employees per 000 population in 2012. Public service employment

is around 65.5 public servants per 000 population.

• The Exchequer pay and pensions bill reached a peak of €18.753bn in 2008. From 2008 to 2012, as the cutbacks in

numbers and pay introduced by the Government have taken effect, the Exchequer pay and pensions bill has decreased

to €16.904bn in 2012.

• While the Exchequer pay bill has continued to decrease each year from 2008, the Exchequer pensions bill has increased,

from €1.656bn in 2008 to €2.502bn in 2012.

• The health and education sectors account for the vast majority of the Exchequer pay bill. In 2012, the health pay bill

(€5.986bn) was 41.6 per cent of the total and the education pay bill (€4.846bn) 33.6 per cent of the total.

• The non-commercial state-sponsored bodies share of the Exchequer pay bill has fallen significantly between 2002 and

2012, from 4.3 per cent to 2.7 per cent.

6

Public Sector Trends 2012

The quality of public administration

• Surveys of business executives show that the quality of Ireland’s public administration is seen as above the European

average. Ireland’s score on a quality of public administration index increased slightly in 2012 compared to European

averages. Ireland came 5th of the EU27 on this indicator in 2012. Ireland’s ranking on this quality indicator tends to have

been slightly above the EU15 average and well above the EU27 average over the last decade. The Nordic countries lead

the way, with Finland, Sweden and Denmark being the top three ranked for the last five years.

• Ireland’s score on an indicator ranking the upholding of traditional public service values such as independence from

political interference, freedom from bribery and corruption, and reliability and administrative fairness improved in 2012.

So too did Ireland’s score on an indicator assessing the encouragement of competition and provision of a supportive

regulatory environment. In 2012, Ireland ranked 3rd of the EU27, behind Sweden and Finland, improving from 6th in

2011.

• The World Bank produces an annual composite indicator of government effectiveness. Ireland’s government effectiveness

score was slightly above the EU15 average from 2005 to 2008, but declined over that time period, and in 2009 fell below

the EU15 average. It stabilised in 2010 (the latest year for which information is available on this indicator) when Ireland

ranked 12th of the EU27.

• Against the World Bank regulatory quality indicator, Ireland’s score remained well above the European average in

2010. However, in 2008, Ireland ranked first of all EU countries on this indicator. The impact of the regulatory problems

identified in the financial sector in 2009 clearly impacted on the indicator, and Ireland dropped to 7th ranked European

country on this indicator in 2010, with Denmark now having the highest ranking.

Public service efficiency and performance

• Surveys of business executives show that Ireland is seen as relatively un-bureaucratic when it comes to dealing with

businesses. Only in Sweden, Finland, Denmark and Estonia is bureaucracy seen as less of a hindrance to business activity.

• The same opinion surveys show that there is a perception that the composition of government spending is wasteful.

However, Ireland’s score on this wastefulness indicator has improved over the last two years and is now close to the EU27

average score, with Ireland ranking 13th of the EU27 on this indicator.

• Perceptions that government decisions are effectively implemented in Ireland have improved in the last two years,

after getting worse for a number of years before that.

• Overall, Ireland continues to do relatively well amongst EU countries against World Bank indicators that assess the

impact of public administration on the ability of companies to do business. The efficiency of the tax regime comes out

particularly strongly.

• Ireland is close to, but generally just below, the EU27 average with regard to how changes in public services to

businesses to support innovation in recent years are concerned. Ireland scores quite well with regard to providing options

to complete government forms over the internet and providing access to information on government services over the

internet. But Ireland is rated relatively poorly with regard to issues such as reductions in time required to obtain permits

or licenses, faster response times and securing reductions in financial costs to companies.

7

Public Sector Trends 2012

• While Ireland is close to the EU27 average with regard to perceived public service support for innovation in businesses,

Ireland scores relatively well with regard to the perceived quality of services provided to support businesses being innovative.

The provision of high quality information and advice and accessibility of that information and advice are ranked particularly

highly.

• In terms of high-level sectoral outcomes, taking education first, Ireland’s scores worsened between 2006 and 2009

in terms of educational attainment, particularly in maths. But the competitive advantage of our education system is

perceived to have improved in 2011 and 2012; Ireland ranked third European country on this indicator in 2012, behind

Finland and Denmark.

• In health, life expectancy and child mortality are around the European average. Similarly against a ‘basket’ of outcomes

assessed by the Euro Health Consumer Index, Ireland performs around the EU15 average. As with most other European

countries, Ireland improved its score on this health outcomes index between 2009 and 2012. Sweden, the Netherlands

and Finland achieve the top three rankings on this index.

Trust and confidence in public administration

• There have been dramatic shifts in the level of trust in government in Ireland. From 2008 to 2010 levels of trust in

government fell significantly. In autumn 2010, Ireland expressed the lowest level of trust in government of any of the

EU27 (10 per cent). By spring 2011, the level of public trust had increased significantly to 42 per cent expressing trust

in the Irish government, close to the EU15 average. But this fell back to 22 per cent by autumn 2011 and 24 per cent in

spring 2012.

• Trust in parliament displays a similar pattern to trust in government, dropping to an all time low of 12 per cent in 2010

and recovering to 39 per cent in spring 2011. This level of trust fell again to 21 per cent in autumn 2011, and increased

slightly to 24 per cent in spring 2012. The Nordic countries of Sweden, Denmark and Finland display the highest levels

of trust in their national parliaments.

• Trust in regional and local authorities in Ireland is low. The level of trust in regional and local authorities in Ireland

was at 26 per cent in 2011, down from 40 per cent in 2008. It increased slightly to 30 per cent in spring 2012. This is

one of the lowest levels of trust in the EU. Only Greece, Italy and Spain report lower levels of trust in regional and local

authorities in 2012.

8

Public Sector Trends 2012

Conclusions

• Numbers employed in the public sector continue to fall. As a percentage of total employment, public service numbers

are not excessive by European standards. As the population continues to increase (placing increasing demands on public

services) and as numbers are reduced further to meet fiscal and economic targets, the challenge of maintaining services

and the skills and capacity needed to provide those services increases. This focuses particular attention on the need for

process improvement to enhance efficiencies and for reducing programme expenditure in some areas (not only more for

less but also less for less).

• The local authority and justice sectors have been particularly hit by staffing reductions. Capacity development in these

areas is of pressing concern.

• The Exchequer pay bill continues to decline from its high in 2008. But the pensions bill is increasing as numbers leaving

and taking early retirement impact on the bill. The need for fiscal discipline to be maintained in these areas remains.

• Given the reductions in numbers and public expenditure, perceptions of the quality of public administration have held

up remarkably well. Irish public services are seen as relatively un-bureaucratic compared to most European countries. The

quality of services to businesses is ranked relatively highly. There is much of Irish public service provision that is seen in a

positive light despite the challenges being faced.

• Trust in government and parliament remains fragile, and trust in local government is low. Much remains to be done

to re-build and maintain the trust of the Irish people in government.

9

Public Sector Trends 2012

There are no clear or agreed definitions for comparative ranking of public administrations. But most people would agree

that a number of elements need to be included in any assessment:

• The size and cost of the public sector. While size and cost alone are not the sole or even main determinants of

good public administration, nevertheless in terms of value for money in the delivery of public services, keeping check on

the size and cost of the public sector and public service is an important consideration.

• Thequalityofpublicadministration. Public administration includes policy making, policy legislation and management

of the public sector. Such dimensions of public administration can only be measured by subjective indicators of quality

which give a sense of how good the public administration is.

• Publicserviceefficiencyandperformance. There is an onus on public administration, all the more so in times of

financial stringency, to show that services are being provided efficiently and that performance is of the highest standard.

The delivery of social and economic outcomes in an efficient manner is central to an effective public administration.

• Trustandconfidenceinpublicadministration. The general public ultimately must have trust and confidence in

the public administration of a country if it is to be effective.

In this study we examine indicators for each of these four elements of public administration. Where possible and

appropriate, data is included for other European countries, to enable comparisons to be made. Also, where data are

available, we have provided trend data going back over the last decade. The intention is to provide a snapshot of trends

in public administration performance in Ireland, to highlight where we are doing well and what challenges are presented

and where improvements need to be made.

In a number of charts, as well as showing Ireland’s rating relative to the EU15 and EU27 averages, the top ranked and

bottom ranked country at the most recent data gathering are included for comparative purposes.

In its style and content, the report draws on a number of efforts to benchmark and compare public sector efficiency

and performance. These include a European Central Bank (ECB) international comparison of public sector efficiency1, a

study by the Netherlands Social and Cultural Planning Office (SCP) of comparative public sector performance2, the World

Bank governance indicators project3, the OECD Government at a Glance project4, and an IPA study comparing public

administrations5.

1. Introduction

1 Afonso et al (2003)2 Social Cultural and Planning Office (2004) 3 See http://info.worldbank.org/governance/wgi/index.asp 4 See http://www.oecd.org/gov/indicators/govataglance5 Boyle (2007)

10

Public Sector Trends 2012

A word of caution about data limitations

The data presented here needs to be interpreted with great care. First, there is the issue of whether the indicators used

to represent public administration provision and quality really captures what public service is about. Indicators, by their

nature, only give a partial picture. Second, much of the international comparative data in this report is qualitative data

derived from opinion surveys. This survey data comprises small-scale samples of opinion from academics, managers and

experts in the business community. The survey data is thus limited both in terms of its overall reliability and the fact that

it represents the views of limited sections of the community. Third, the point scores arrived at on some indicators (on a

scale from 1–10 for the IMD and WEF data and between –2.5 and +2.5 for the World Bank governance indicators) should

not be interpreted too strictly, as there are margins of error associated with these estimates. Fourth, changes over time

should be viewed cautiously. Many of the indicators assessed represent ‘snapshots’ at one particular point in time. Small

shifts in annual ranking are not particularly meaningful.

In all, when interpreting the findings set out in this paper, these limitations should be borne in mind. In particular, small

variations in scores should be interpreted cautiously. These may be no more than random variations to be expected given

the data being used. What is of interest is to identify broad patterns emerging from the data.

11

Public Sector Trends 2012

There are a range of indicators that show the size and cost of the public sector and public service6. Government expenditure

as a share of GDP/GNI7, level of public expenditure per head of population and public sector employment trends all give

a sense of size. The cost of the public sector is shown by data on the Exchequer pay and pensions bill.

2. The size and cost of the public sector

6 In this study, the public service is defined as the public sector minus the commercial state-sponsored bodies.7 Gross National Income (GNI) is equal to Gross National Product (GNP) plus EU subsidies less EU taxes. The relationship between GDP and GNI in Ireland is

unusual among EU countries, with Luxembourg the only other country where the difference between the two measures is more than 10% of GDP.

The gap reflects the magnitude of repatriated profits from Ireland that inflates the GDP figure.

12

Public Sector Trends 2012

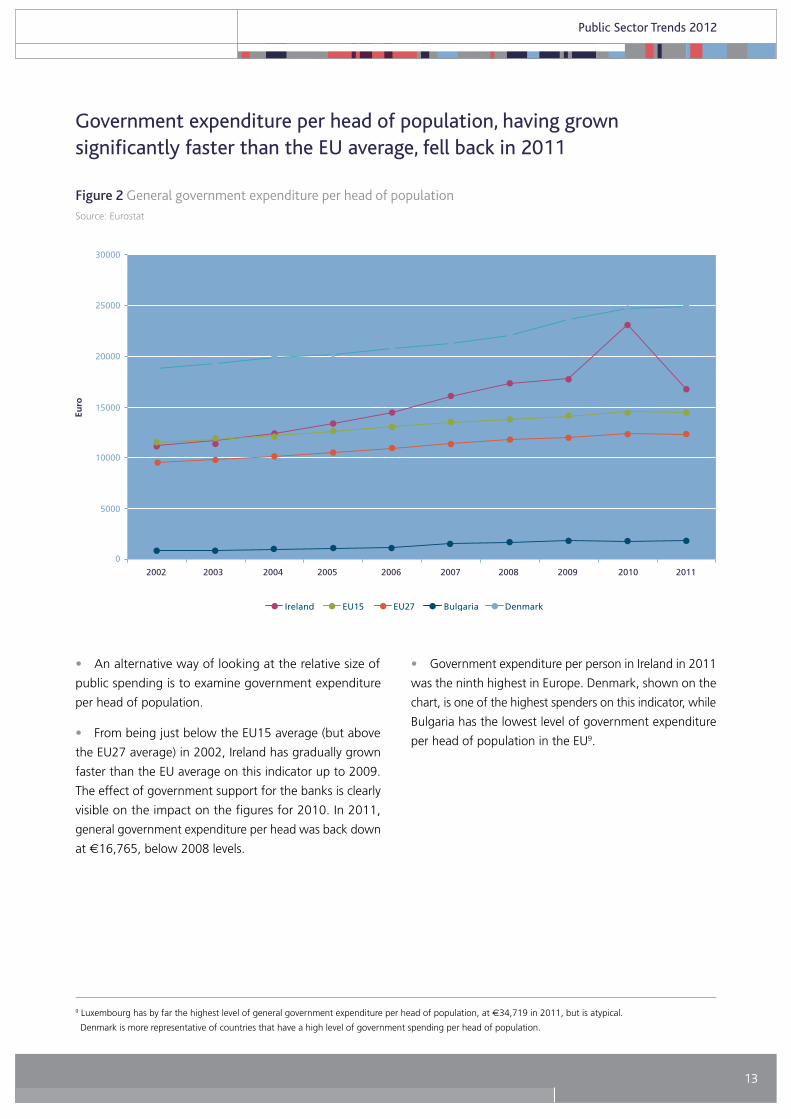

Government expenditure as a share of the economy in Ireland grew rapidly in recent years both absolutely and when compared to the rest of Europe, but fell back in 2011

Source: CSO; Eurostat

Figure 1 General government expenditure as share of GDP/GNI

8 See for example Foley (2009), pp.75-76. Ireland and Luxembourg are the two EU countries where there is a substantial difference between GDP and GNI.

In most other countries the two figures are broadly similar.

• A commonly used indicator of public spending in the

economy is expenditure as a percentage of GDP (gross

domestic product). Historically, using this indicator, Ireland

is shown as having a very small share of public spending

compared to most EU countries.

• However, from 2008 to 2010, as GDP shrank as a

result of the recession in Ireland, Ireland’s government

expenditure as a percentage of GDP increased rapidly.

The particularly large jump from 2009 to 2010 is mostly

explained by the impact on government expenditure of

specific government support to banks during the financial

crisis, in the form of capital injections. In 2011, expenditure

as a percentage of GDP had dropped back down to 48.1

per cent, just a little below the European average.

• An alternative indicator to assess the comparative size

of Ireland’s public spending is to use GNI (gross national

income) rather than GDP, as GNI does not include repatriated

profits from Ireland which inflate the GDP figure8. Using this

GNI indicator, the size of the public sector was still below

the EU average up to 2007, but has been above the EU

average since then. In 2011 government expenditure as a

percentage of GNI was 59.1 per cent. This is the highest

level in the EU, above Denmark at 57.9 per cent of GDP.

13

Public Sector Trends 2012

Government expenditure per head of population, having grown significantly faster than the EU average, fell back in 2011

9 Luxembourg has by far the highest level of general government expenditure per head of population, at €34,719 in 2011, but is atypical.

Denmark is more representative of countries that have a high level of government spending per head of population.

Source: Eurostat

Figure 2 General government expenditure per head of population

• An alternative way of looking at the relative size of

public spending is to examine government expenditure

per head of population.

• From being just below the EU15 average (but above

the EU27 average) in 2002, Ireland has gradually grown

faster than the EU average on this indicator up to 2009.

The effect of government support for the banks is clearly

visible on the impact on the figures for 2010. In 2011,

general government expenditure per head was back down

at €16,765, below 2008 levels.

• Government expenditure per person in Ireland in 2011

was the ninth highest in Europe. Denmark, shown on the

chart, is one of the highest spenders on this indicator, while

Bulgaria has the lowest level of government expenditure

per head of population in the EU9.

14

Public Sector Trends 2012

Numbers employed in the public sector and the public service continue to decline

Source: Department of Finance, Budgetary and Economic Statistics

Figure 3 Numbers employed in the public sector and public service

• The total number of people employed in the public

sector grew from around 317,000 in 2001 to 360,000 in

2008, a growth of 14 per cent.

• Excluding commercial state-sponsored bodies, the

numbers employed in the public service grew from 270,000

in 2000 to 320,000 in 2008, a growth of 19 per cent.

• There has been a significant drop in the numbers

employed in both the public sector and public service from

2008, with a drop of around 8 per cent in each case.

• Numbers employed in the public sector and public

service in 2012 are now back down to close to 2005 levels

of employment.

15

Public Sector Trends 2012

The health and education sectors continue to account for the vast majority of public sector jobs

Source: Department of Finance, Budgetary and Economic Statistics

Figure 4 Public sector employment by sector

• Growth in public sector numbers from 2001 to 2008

was primarily concentrated in the health and education

sectors.

• Two out of every three people employed in the public

service work in either health or education. In 2012, there

were approximately 102,000 people employed in the health

sector and 92,000 people employed in the education sector.

• Numbers have fallen in all sectors since 2008. The

biggest drop proportionally has been in the non commercial

state agencies (19 per cent), local authorities (14 per cent)

and the justice sector (13 per cent). The smallest drop

proportionally has been in the education sector (3 per

cent).

• Those employed in non-commercial state-sponsored

bodies (so called quangos) account for under 4 per cent

of the public service workforce.

16

Public Sector Trends 2012

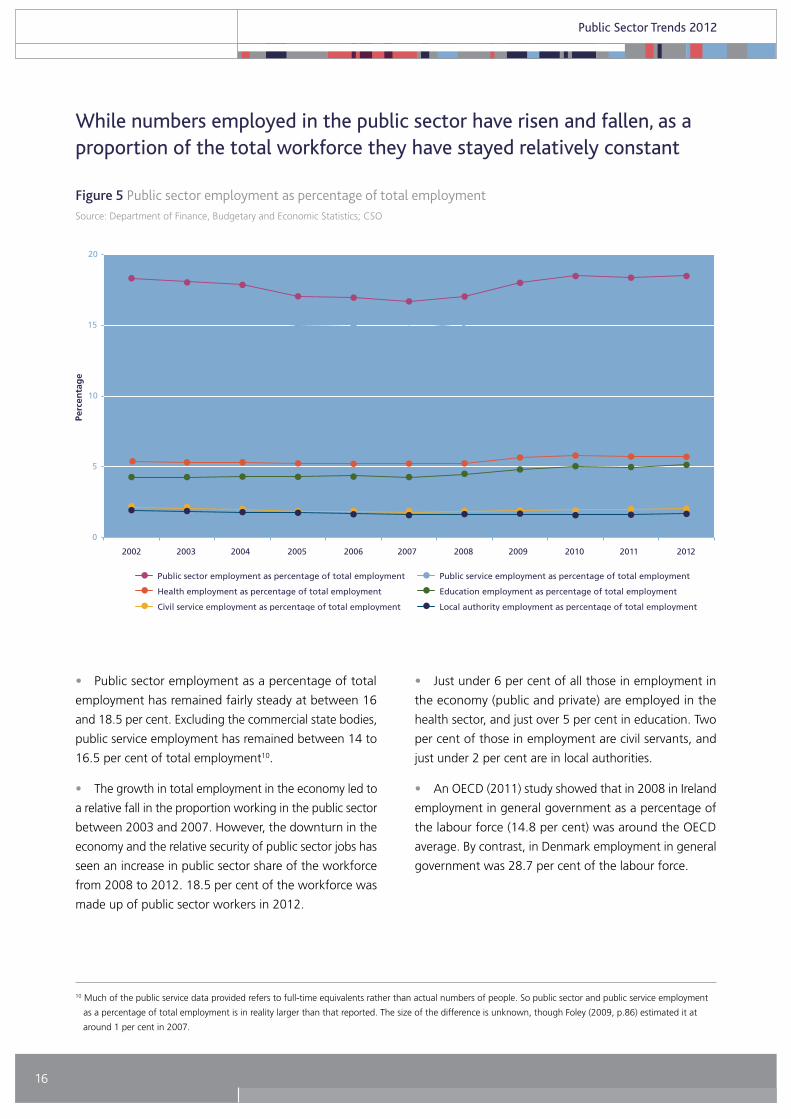

While numbers employed in the public sector have risen and fallen, as a proportion of the total workforce they have stayed relatively constant

Source: Department of Finance, Budgetary and Economic Statistics; CSO

Figure 5 Public sector employment as percentage of total employment

10 Much of the public service data provided refers to full-time equivalents rather than actual numbers of people. So public sector and public service employment

as a percentage of total employment is in reality larger than that reported. The size of the difference is unknown, though Foley (2009, p.86) estimated it at

around 1 per cent in 2007.

• Public sector employment as a percentage of total

employment has remained fairly steady at between 16

and 18.5 per cent. Excluding the commercial state bodies,

public service employment has remained between 14 to

16.5 per cent of total employment10.

• The growth in total employment in the economy led to

a relative fall in the proportion working in the public sector

between 2003 and 2007. However, the downturn in the

economy and the relative security of public sector jobs has

seen an increase in public sector share of the workforce

from 2008 to 2012. 18.5 per cent of the workforce was

made up of public sector workers in 2012.

• Just under 6 per cent of all those in employment in

the economy (public and private) are employed in the

health sector, and just over 5 per cent in education. Two

per cent of those in employment are civil servants, and

just under 2 per cent are in local authorities.

• An OECD (2011) study showed that in 2008 in Ireland

employment in general government as a percentage of

the labour force (14.8 per cent) was around the OECD

average. By contrast, in Denmark employment in general

government was 28.7 per cent of the labour force.

17

Public Sector Trends 2012

Public sector employment continues to decline relative to the total population

Source: Department of Finance, Budgetary and Economic Statistics; CSO

Figure 6 Public sector and public service employment per 000 population

• Public sector employment relative to the population

was relatively stable at between 80 and 85 public sector

employees per 000 population, but has been dropping

since 2008 and was at 73.6 public sector employees per

000 population in 2012.

• Public service employment is around 65.5 public servants

per 000 population in 2012, also showing a significant

decline from 2008.

• An OECD (2010) study comparing 8 countries (Denmark,

Sweden, Finland, the UK, Canada, Ireland, the Netherlands

and New Zealand) showed that Ireland had the third lowest

general government employment per 000 population (67)

in 2006, and significantly behind Denmark (137), Sweden

(125) and Finland (99).

18

Public Sector Trends 2012

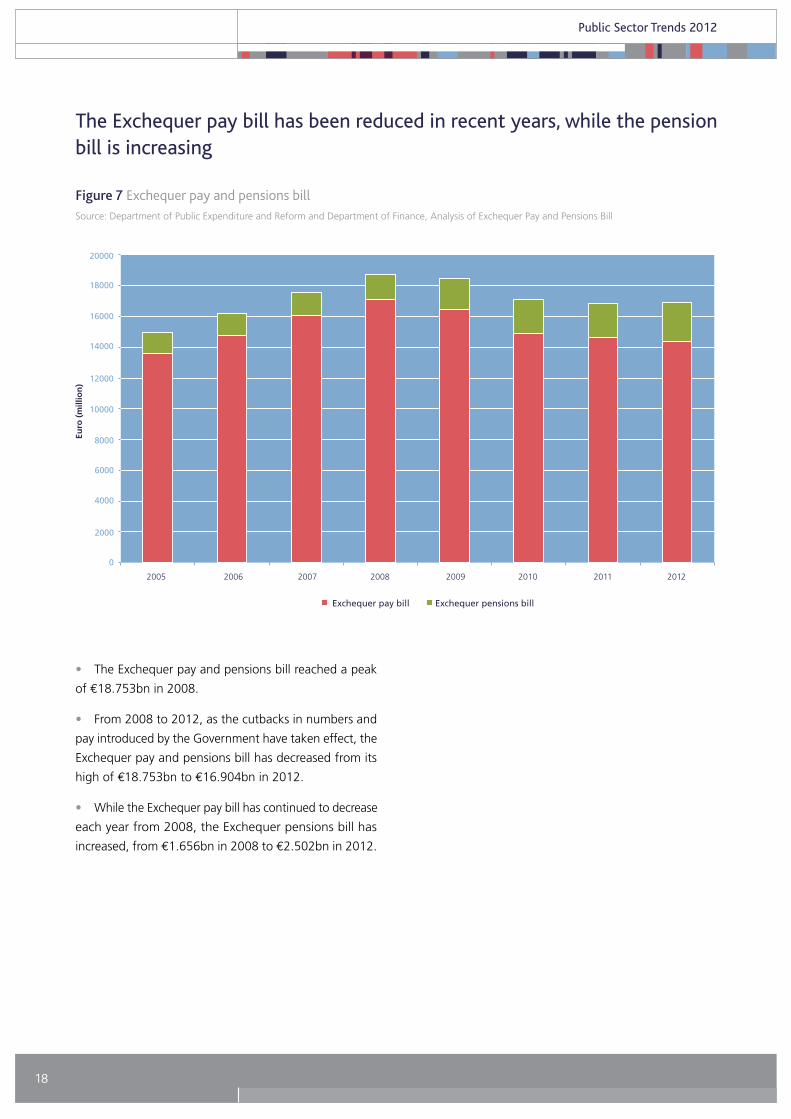

The Exchequer pay bill has been reduced in recent years, while the pension bill is increasing

Source: Department of Public Expenditure and Reform and Department of Finance, Analysis of Exchequer Pay and Pensions Bill

Figure 7 Exchequer pay and pensions bill

• The Exchequer pay and pensions bill reached a peak

of €18.753bn in 2008.

• From 2008 to 2012, as the cutbacks in numbers and

pay introduced by the Government have taken effect, the

Exchequer pay and pensions bill has decreased from its

high of €18.753bn to €16.904bn in 2012.

• While the Exchequer pay bill has continued to decrease

each year from 2008, the Exchequer pensions bill has

increased, from €1.656bn in 2008 to €2.502bn in 2012.

19

Public Sector Trends 2012

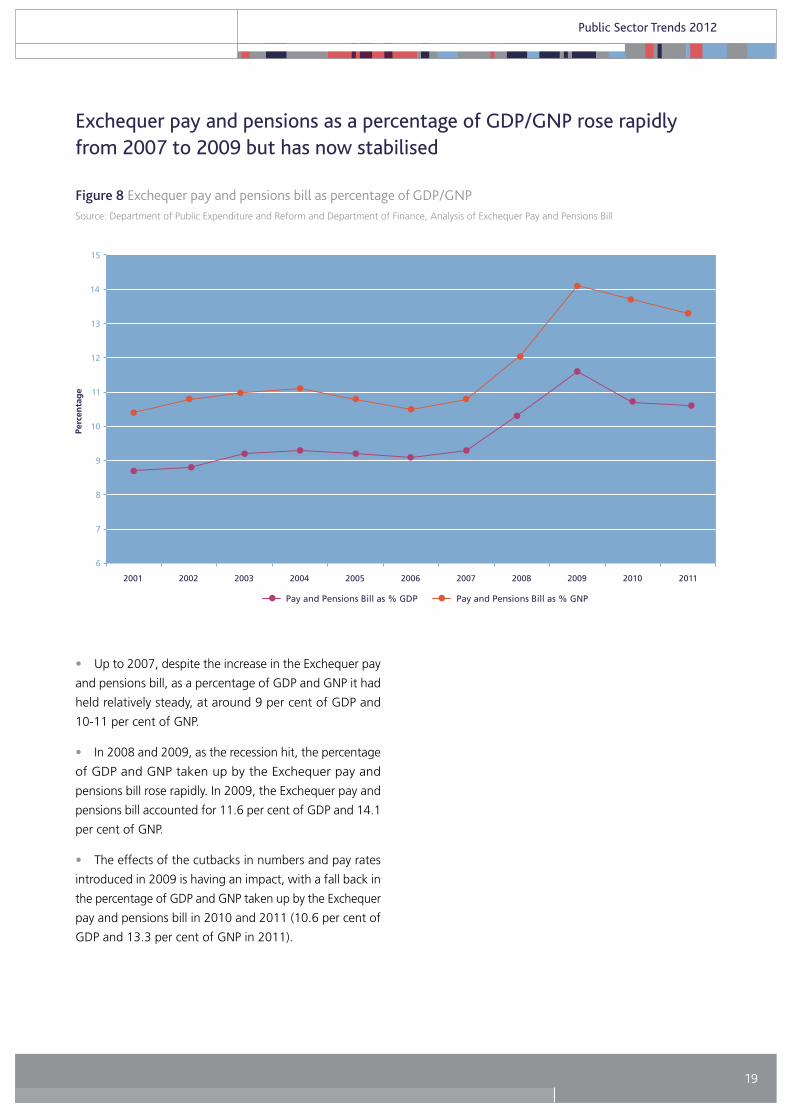

Exchequer pay and pensions as a percentage of GDP/GNP rose rapidly from 2007 to 2009 but has now stabilised

Source: Department of Public Expenditure and Reform and Department of Finance, Analysis of Exchequer Pay and Pensions Bill

Figure 8 Exchequer pay and pensions bill as percentage of GDP/GNP

• Up to 2007, despite the increase in the Exchequer pay

and pensions bill, as a percentage of GDP and GNP it had

held relatively steady, at around 9 per cent of GDP and

10-11 per cent of GNP.

• In 2008 and 2009, as the recession hit, the percentage

of GDP and GNP taken up by the Exchequer pay and

pensions bill rose rapidly. In 2009, the Exchequer pay and

pensions bill accounted for 11.6 per cent of GDP and 14.1

per cent of GNP.

• The effects of the cutbacks in numbers and pay rates

introduced in 2009 is having an impact, with a fall back in

the percentage of GDP and GNP taken up by the Exchequer

pay and pensions bill in 2010 and 2011 (10.6 per cent of

GDP and 13.3 per cent of GNP in 2011).

20

Public Sector Trends 2012

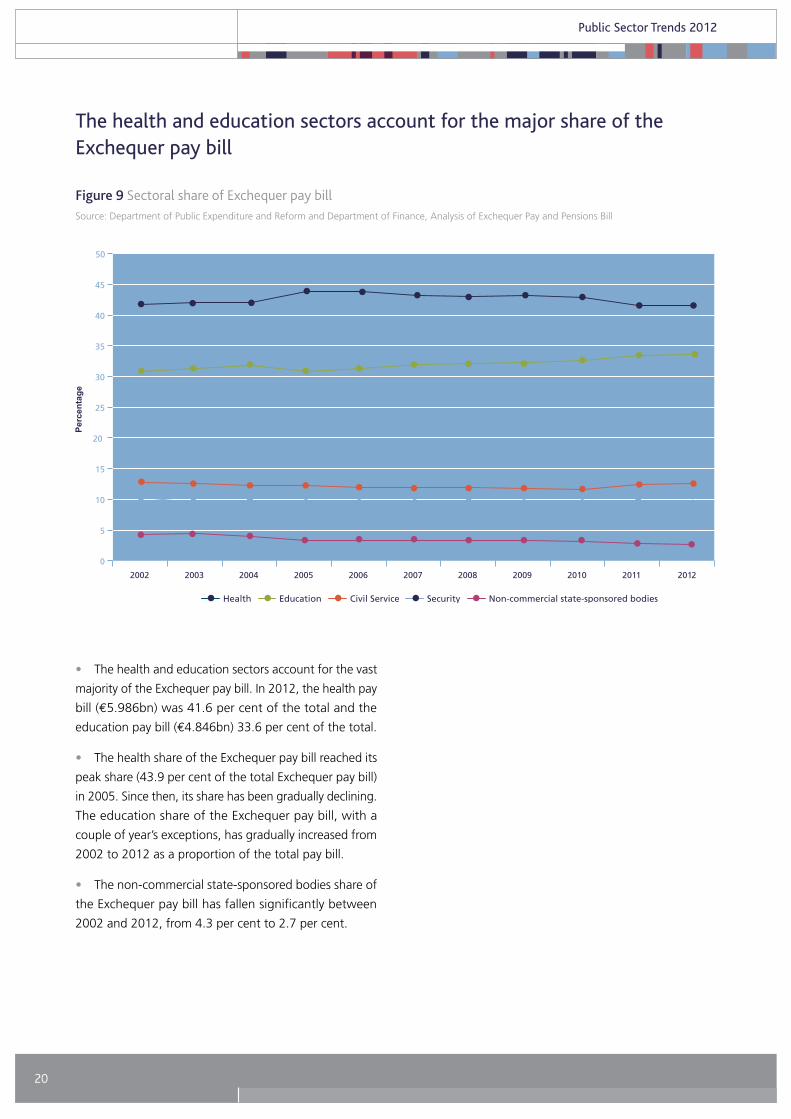

The health and education sectors account for the major share of the Exchequer pay bill

Source: Department of Public Expenditure and Reform and Department of Finance, Analysis of Exchequer Pay and Pensions Bill

Figure 9 Sectoral share of Exchequer pay bill

• The health and education sectors account for the vast

majority of the Exchequer pay bill. In 2012, the health pay

bill (€5.986bn) was 41.6 per cent of the total and the

education pay bill (€4.846bn) 33.6 per cent of the total.

• The health share of the Exchequer pay bill reached its

peak share (43.9 per cent of the total Exchequer pay bill)

in 2005. Since then, its share has been gradually declining.

The education share of the Exchequer pay bill, with a

couple of year’s exceptions, has gradually increased from

2002 to 2012 as a proportion of the total pay bill.

• The non-commercial state-sponsored bodies share of

the Exchequer pay bill has fallen significantly between

2002 and 2012, from 4.3 per cent to 2.7 per cent.

21

Public Sector Trends 2012

An indicator of the quality of public administration, based on work undertaken by the Social and Cultural Planning Office

(2004) in the Netherlands and taken further by Boyle (2007) is used to assess the quality of public administration. Sixteen

indicators derived from both IMD and WEF executive opinion surveys are combined to make up an aggregate public

administration quality indicator (see Appendix 1 for details)11. It is complemented by two subsets of this indicator, one of

which shows trends in perception about the application of traditional public service values in public administration, the

other showing perceptions of the type of competitive and regulatory regime fostered by public administration.

These indicators are supplemented by World Bank indicators of government effectiveness and regulatory quality, developed

as part of the World Bank’s brief to promote good governance.

3. The quality of public administration

11 This quality of public administration indicator was developed by the IPA and has been used internationally, notably in work for the Hong Kong administration

benchmarking their public service.

22

Public Sector Trends 2012

The quality of Irish public administration is seen as above the European average and has improved comparatively over the last couple of years

Source: IPA analysis based on IMD and WEF data

Figure 10 Quality of public administration score 2003-2012

• Ireland’s score on the quality of public administration

index increase slightly in 2012 compared to European

averages. Ireland came 5th of the EU27 on this indicator

in 2012.

• Ireland’s ranking on this quality indicator tends to have

been slightly above the EU15 average and well above the

EU27 average over the last decade.

• The Nordic countries lead the way, with Finland, Sweden

and Denmark being the top three ranked for the last five

years.

23

Public Sector Trends 2012

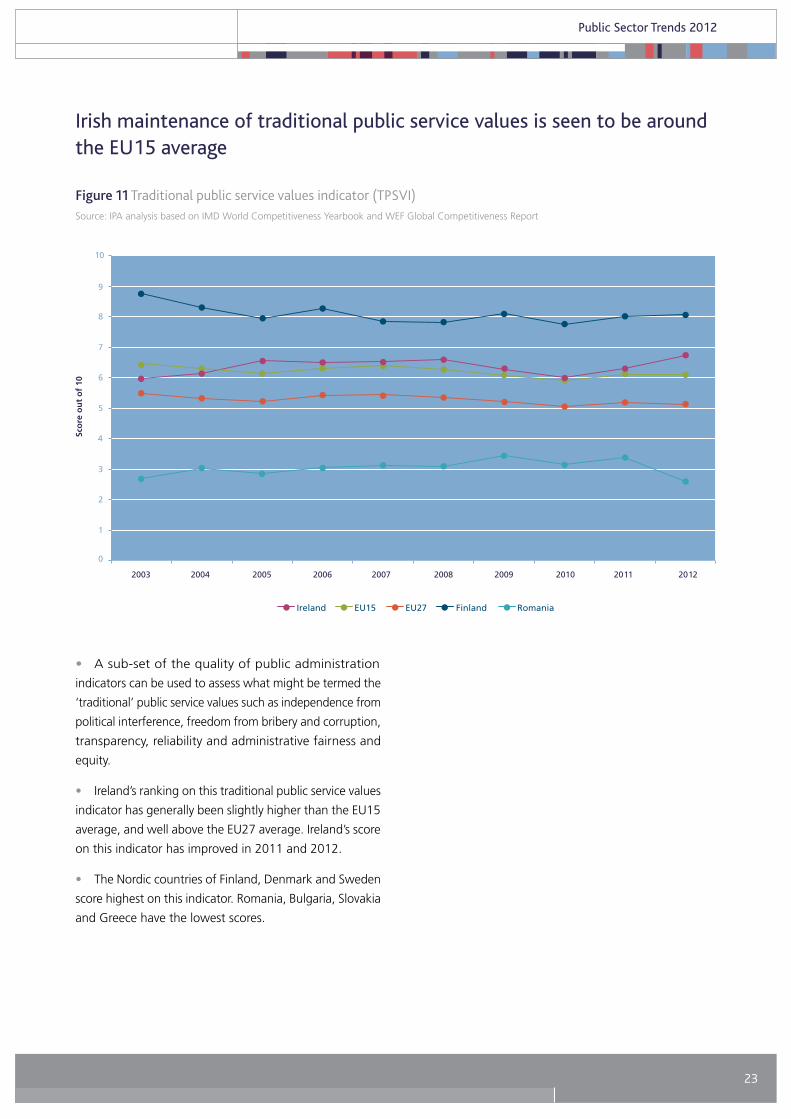

Irish maintenance of traditional public service values is seen to be around the EU15 average

Source: IPA analysis based on IMD World Competitiveness Yearbook and WEF Global Competitiveness Report

Figure 11 Traditional public service values indicator (TPSVI)

• A sub-set of the quality of public administration

indicators can be used to assess what might be termed the

‘traditional’ public service values such as independence from

political interference, freedom from bribery and corruption,

transparency, reliability and administrative fairness and

equity.

• Ireland’s ranking on this traditional public service values

indicator has generally been slightly higher than the EU15

average, and well above the EU27 average. Ireland’s score

on this indicator has improved in 2011 and 2012.

• The Nordic countries of Finland, Denmark and Sweden

score highest on this indicator. Romania, Bulgaria, Slovakia

and Greece have the lowest scores.

24

Public Sector Trends 2012

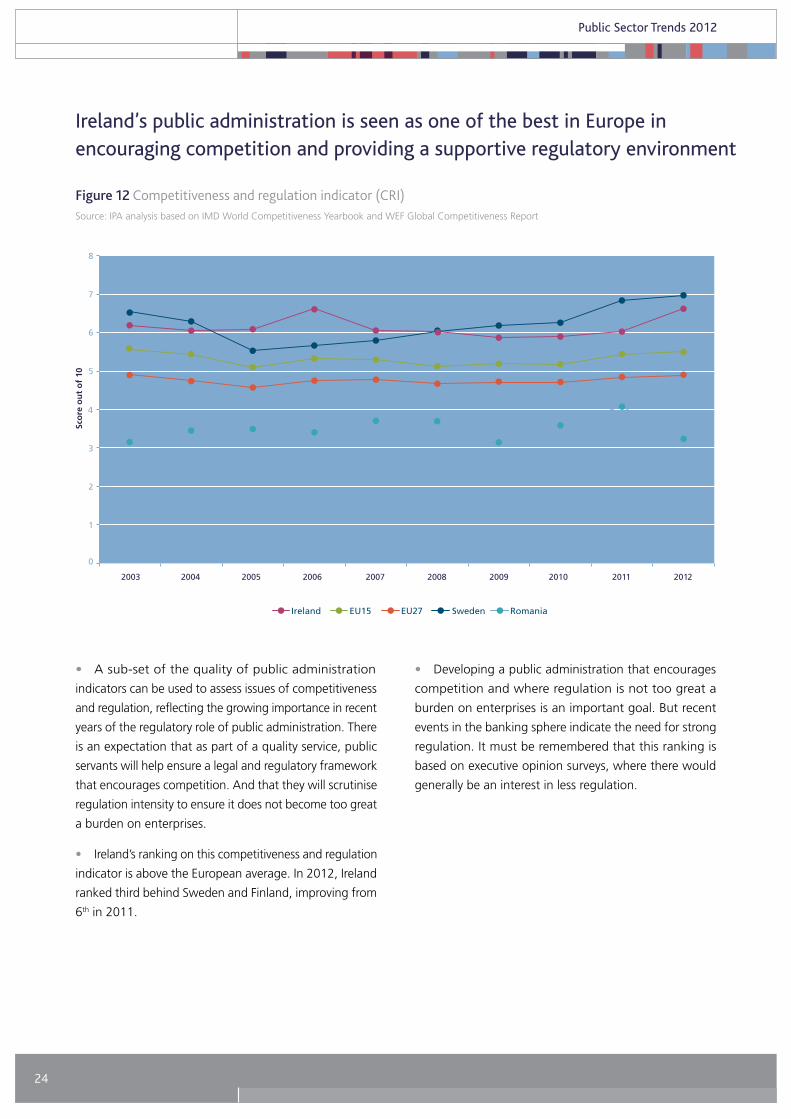

Ireland’s public administration is seen as one of the best in Europe in encouraging competition and providing a supportive regulatory environment

Source: IPA analysis based on IMD World Competitiveness Yearbook and WEF Global Competitiveness Report

Figure 12 Competitiveness and regulation indicator (CRI)

• A sub-set of the quality of public administration

indicators can be used to assess issues of competitiveness

and regulation, reflecting the growing importance in recent

years of the regulatory role of public administration. There

is an expectation that as part of a quality service, public

servants will help ensure a legal and regulatory framework

that encourages competition. And that they will scrutinise

regulation intensity to ensure it does not become too great

a burden on enterprises.

• Ireland’s ranking on this competitiveness and regulation

indicator is above the European average. In 2012, Ireland

ranked third behind Sweden and Finland, improving from

6th in 2011.

• Developing a public administration that encourages

competition and where regulation is not too great a

burden on enterprises is an important goal. But recent

events in the banking sphere indicate the need for strong

regulation. It must be remembered that this ranking is

based on executive opinion surveys, where there would

generally be an interest in less regulation.

25

Public Sector Trends 2012

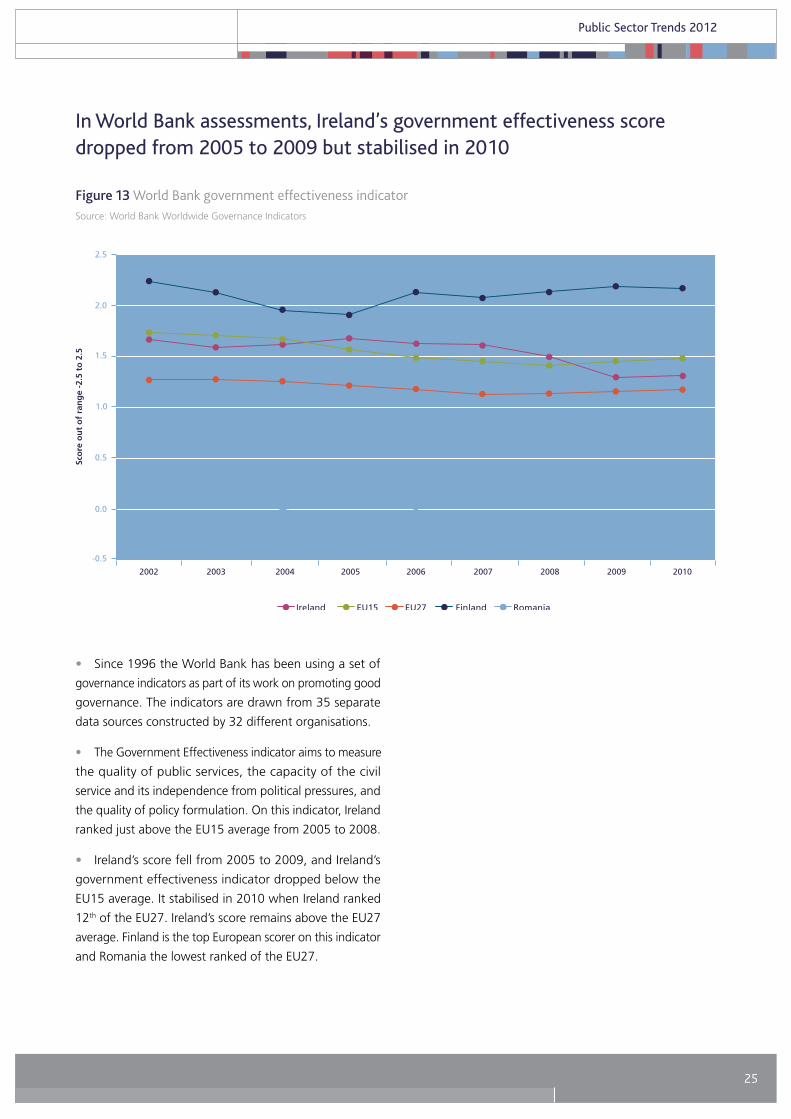

In World Bank assessments, Ireland’s government effectiveness score dropped from 2005 to 2009 but stabilised in 2010

Source: World Bank Worldwide Governance Indicators

Figure 13 World Bank government effectiveness indicator

• Since 1996 the World Bank has been using a set of

governance indicators as part of its work on promoting good

governance. The indicators are drawn from 35 separate

data sources constructed by 32 different organisations.

• The Government Effectiveness indicator aims to measure

the quality of public services, the capacity of the civil

service and its independence from political pressures, and

the quality of policy formulation. On this indicator, Ireland

ranked just above the EU15 average from 2005 to 2008.

• Ireland’s score fell from 2005 to 2009, and Ireland’s

government effectiveness indicator dropped below the

EU15 average. It stabilised in 2010 when Ireland ranked

12th of the EU27. Ireland’s score remains above the EU27

average. Finland is the top European scorer on this indicator

and Romania the lowest ranked of the EU27.

26

Public Sector Trends 2012

In World Bank assessments, Ireland’s regulatory quality indicator remains above the European average

Source: World Bank Worldwide Governance Indicators

Figure 14 World Bank regulatory quality indicator

• The Regulatory Quality indicator aims to measure

the ability of the government to provide sound policies

and regulations that enable and promote private sector

development. On this indicator Ireland ranks as well above

the EU15 and EU27 average scores, particularly from 2006

onwards.

• In 2008, Ireland ranked first of all EU countries on this

indicator. However, the impact of the regulatory problems

identified in the financial sector in 2009 clearly impacted

on the indicator, and Ireland has dropped to 7th ranked

European country on this indicator in 2010, with Denmark

now having the highest ranking.

27

Public Sector Trends 2012

Information from executive opinion surveys shows perceptions of business people regarding the efficiency of public services.

The World Bank Doing Business indicator set provides some information on the efficiency of service provided to business

by public administration. Data from a 2012 Eurobarometer study of perceptions of businesses on innovation in the public

service and its impact on business is included as a guide to performance in this important sphere of governmental activity12.

Ultimately, the provision of public administration is intended to achieve social outcomes in sectors such as health, education,

law and order and transport. As such it is important that any review of public administration looks at sectoral outcomes.

In this report, some high-level education and health indicators are included, given that these areas are the largest areas

of public expenditure.

Attainment and enrolment are two important indicators of the education system, enrolment focusing on process and

attainment on outcome. The European Central Bank (ECB, 2003) and Netherlands Social and Cultural Planning Office

(SCP, 2004) used secondary school enrolment and educational achievement indicators in their international comparisons

of public sector efficiency and performance. They are the main indicators used in this report.

In the health sector, two commonly used indicators, again used in the ECB and SCP studies, are life expectancy and infant

mortality. They are used here to illustrate outcomes in the health sector. They are supplemented by a composite health

outcomes index developed as part of the Euro Health Consumer Index.

4. Public service efficiency and performance

12 European Commission (2012), Innovation in the Public Sector: Its Perception in and Impact on Business, Flash Eurobarometer 343,

http://ec.europa.eu/public_opinion/flash/fl_343_sum_en.pdf (accessed 24 September 2012).

28

Public Sector Trends 2012

Irish public services are seen as relatively un-bureaucratic compared to most European countries

Source: IMD World Competitiveness Yearbook

Figure 15 Bureaucracy hinders business activity

• Respondents to the executive opinion survey carried out

by IMD for their World Competitiveness Yearbook indicate

that compared to most European countries, bureaucracy

in Ireland is seen as less of a hindrance to business activity.

• Only in Sweden, Finland, Denmark and Estonia is

bureaucracy seen as less of a hindrance to business activity.

The comparative trends have been fairly consistent since

2006, with improvements in the scores for Ireland and

the EU averages in 2011 and 2012. By contrast, Greece,

the lowest European scorer on this indicator, has seen its

score decrease since 2007.

29

Public Sector Trends 2012

There is a perception of wastefulness of public spending in Ireland but things are seen as having improved in the last two years

Source: WEF Global Competitiveness Report

Figure 16 The composition of public spending is wasteful

• Respondents to the WEF Global Competitiveness Report

executive opinion survey suggest that there is a perception

that Ireland is more wasteful in its public spending than

many other European countries.

• There was a worsening of the perception about the

wastefulness of public spending in Ireland from 2008 to

2010, with a slight pick up in 2011 which has continued

in 2012.

• Ireland’s score on this indicator has improved over the

last two years and is now close to the EU27 average score,

with Ireland ranking 13th of the EU27 on this indicator.

• Sweden is seen as having the least wasteful public

spending in Europe, a perception that has improved

significantly since the early 2000s when it was below the

EU15 average. By contrast, Greece scores worst on this

indicator.

30

Public Sector Trends 2012

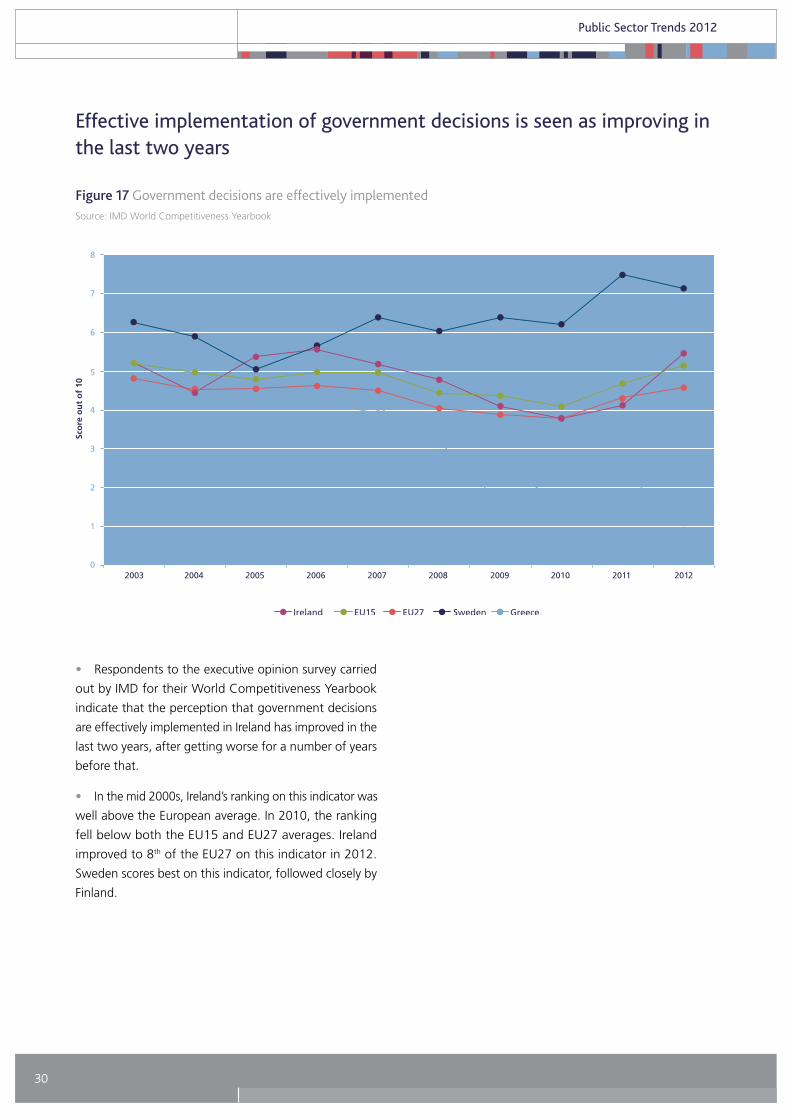

• Respondents to the executive opinion survey carried

out by IMD for their World Competitiveness Yearbook

indicate that the perception that government decisions

are effectively implemented in Ireland has improved in the

last two years, after getting worse for a number of years

before that.

• In the mid 2000s, Ireland’s ranking on this indicator was

well above the European average. In 2010, the ranking

fell below both the EU15 and EU27 averages. Ireland

improved to 8th of the EU27 on this indicator in 2012.

Sweden scores best on this indicator, followed closely by

Finland.

Effective implementation of government decisions is seen as improving in the last two years

Source: IMD World Competitiveness Yearbook

Figure 17 Government decisions are effectively implemented

31

Public Sector Trends 2012

Ireland’s public administration continues to provide a relatively efficient level of service to business

Source: WEF Global Competitiveness Report

Figure 18 World Bank Doing Business indicators 2011

• A ‘bottom-up’ approach to assessing efficiency of public

administration is taken by the World Bank in some of their

Doing Business indicator set, with performance assessed

from a service user perspective.

• The number of days estimated that it takes an

entrepreneur to start a business in Ireland has remained

at 13 for the last five years, which is the EU15 average

(the EU15 average was 15 days in 2010). In Belgium and

Hungary it takes 4 days.

• The number of days to complete all procedures required

for a business in the construction industry to build a

standardised warehouse was estimated at 141 days in

Ireland in 2011, down from 192 days in 2010, and lower

than the EU15 average (155 days) and the EU27 average

(189 days). The best performers are Finland and Denmark

with an estimated 66 days and 67 days respectively.

• The number of hours it takes a medium-sized company

to pay tax in a given year is estimated as significantly lower

in Ireland, at 76 hours, than it is for the EU15 (158 hours)

and EU27 (208 hours) averages, though the European

averages are coming down while Ireland’s performance is

static. Ireland ranks second in the EU behind Luxembourg

on this indicator.

• Overall, Ireland does relatively well in the EU against

these World Bank indicators that assess the impact of public

administration on the ability of companies to do business.

32

Public Sector Trends 2012

• Ireland is close to, but generally just below, the EU27

average with regard to how changes in public services

to businesses to support innovation in recent years are

concerned.

• Ireland scores quite well with regard to providing

options to complete government forms over the internet

and providing access to information on government

services over the internet. Though it is still ranked some

way behind European leaders in these areas such as Latvia,

France, Finland and Slovenia.

• Ireland is rated relatively poorly, as are many other

countries, with regard to reductions in time required

to obtain permits or licenses, faster response times and

securing reductions in financial costs to companies.

Public service supports for business innovation are seen as around the European average

Source: Eurobarometer

Figure 19 Changes in public services to business to support innovation

33

Public Sector Trends 2012

Ireland is rated relatively well with regard to the perceived impact of public service innovations on businesses

Source: Eurobarometer

Figure 20 Impact of public service innovations on businesses

• Ireland rates relatively well compared to many European

countries with regard to the perceived impact of public

service innovations on business.

• The quality of information and advice provided and

minimising the time spent by companies using public

services are rated particularly highly. Response time from

the public sector is also rated above the European average.

• Ireland rates less well overall and comparatively

with regard to the impact of public services on costs for

companies, and the role of the public education system

and training programmes in supporting the provision of

skilled personnel for companies.

34

Public Sector Trends 2012

Ireland around the European average in terms of supporting innovation in business

Source: Eurobarometer

Figure 21 Business views on public service support for innovation

• Ireland is close to the EU27 average with regard to

perceived public service support for innovation in businesses.

• Ireland is seen as slightly above the European average

with regard to the role of the regulatory and fiscal system

in supporting company innovation.

• Ireland is slightly below the European average regarding

how public services are seen as doing a good job in creating

the right conditions for companies to innovate. Luxembourg,

Malta, Finland and Estonia are seen as leading here.

35

Public Sector Trends 2012

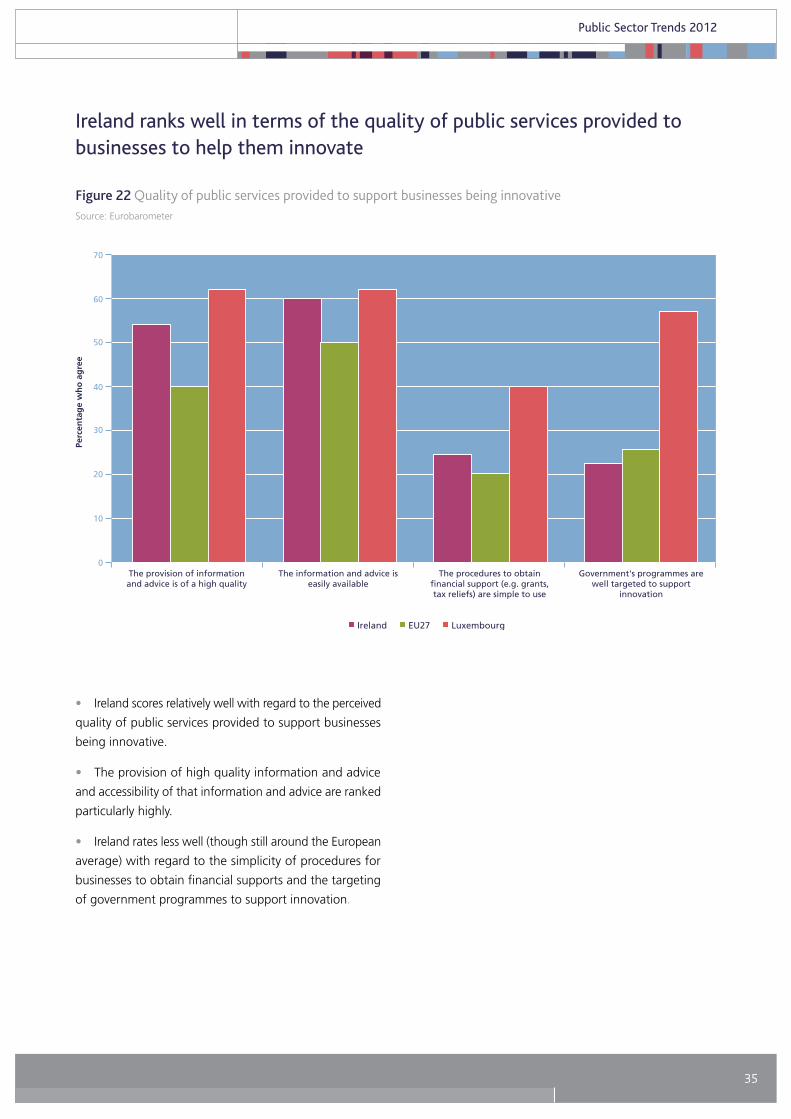

Ireland ranks well in terms of the quality of public services provided to businesses to help them innovate

Source: Eurobarometer

Figure 22 Quality of public services provided to support businesses being innovative

• Ireland scores relatively well with regard to the perceived

quality of public services provided to support businesses

being innovative.

• The provision of high quality information and advice

and accessibility of that information and advice are ranked

particularly highly.

• Ireland rates less well (though still around the European

average) with regard to the simplicity of procedures for

businesses to obtain financial supports and the targeting

of government programmes to support innovation.

36

Public Sector Trends 2012

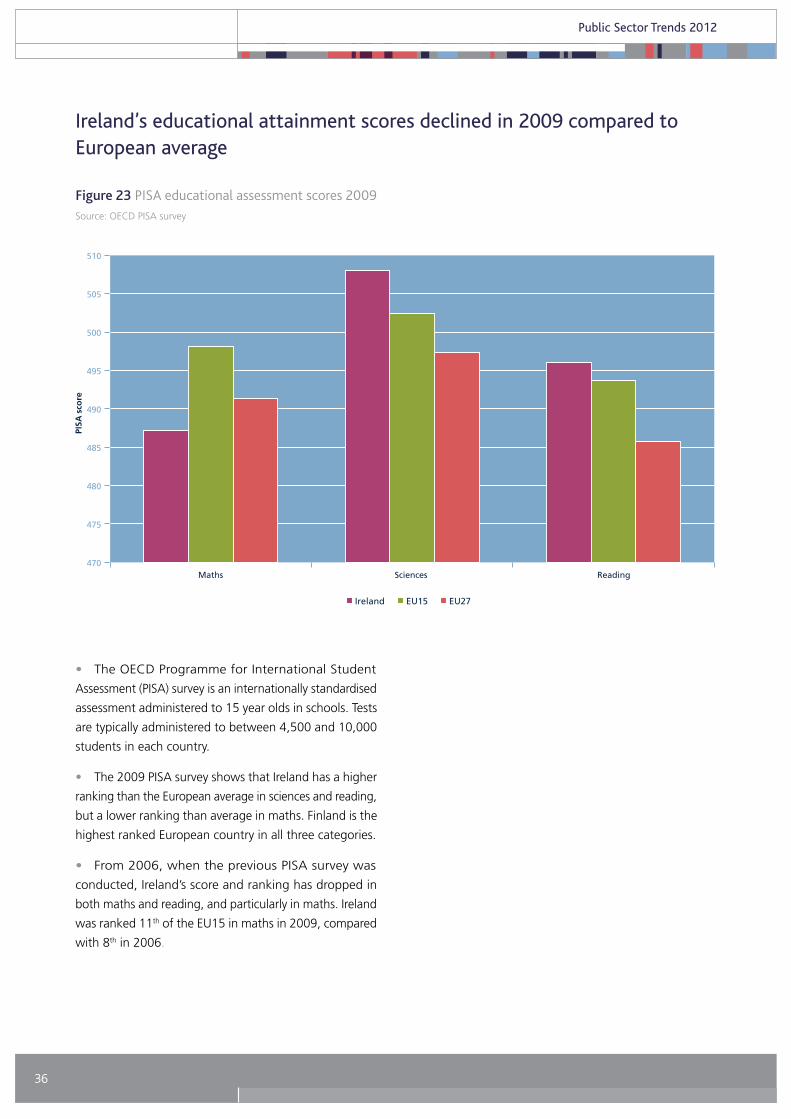

• The OECD Programme for International Student

Assessment (PISA) survey is an internationally standardised

assessment administered to 15 year olds in schools. Tests

are typically administered to between 4,500 and 10,000

students in each country.

• The 2009 PISA survey shows that Ireland has a higher

ranking than the European average in sciences and reading,

but a lower ranking than average in maths. Finland is the

highest ranked European country in all three categories.

• From 2006, when the previous PISA survey was

conducted, Ireland’s score and ranking has dropped in

both maths and reading, and particularly in maths. Ireland

was ranked 11th of the EU15 in maths in 2009, compared

with 8th in 2006.

Ireland’s educational attainment scores declined in 2009 compared to European average

Source: OECD PISA survey

Figure 23 PISA educational assessment scores 2009

37

Public Sector Trends 2012

Secondary school enrolment is somewhat behind the European average

Source: IMD World Competitiveness Yearbook

Figure 24 Secondary school enrolment

• In 2009, the last year for which comparative data is

available, the percentage in full-time education in Ireland

was 89 per cent, compared to 93 per cent average for the

EU15.

• The percentage in full-time education has been

consistently rising in Ireland in recent years. But it is still

somewhat below the European average. France, Slovakia

and Sweden had the best enrolment rates in 2009.

38

Public Sector Trends 2012

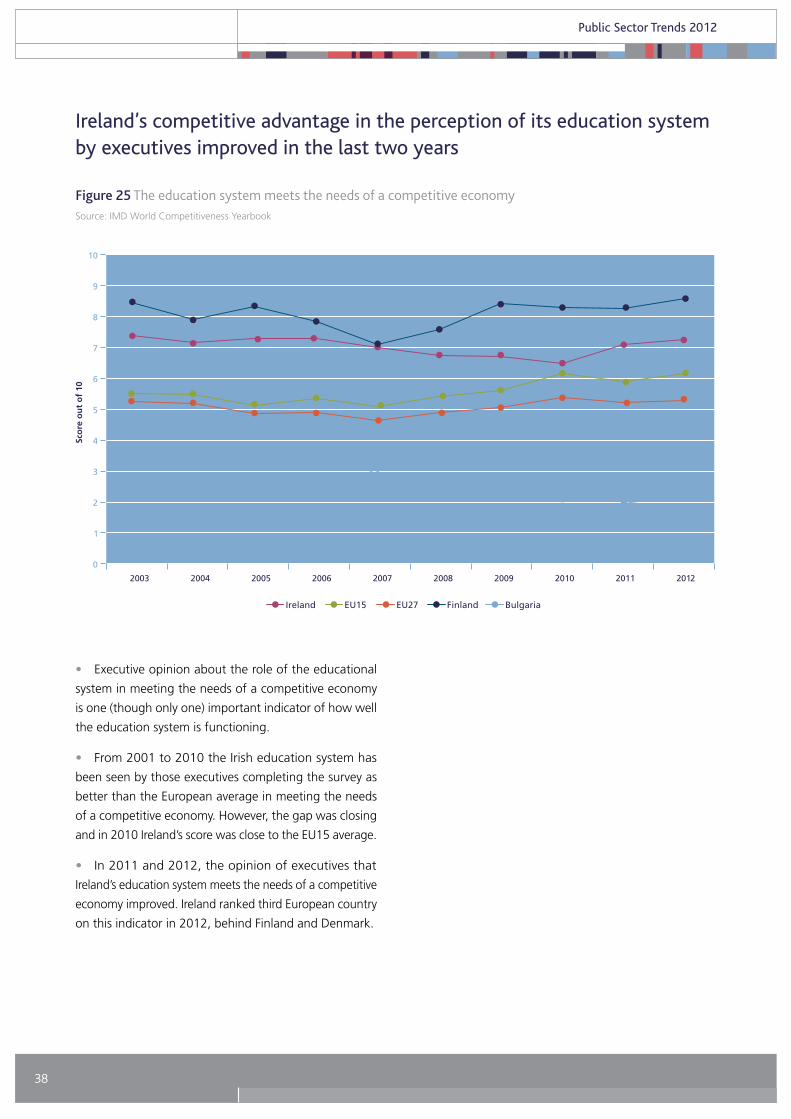

• Executive opinion about the role of the educational

system in meeting the needs of a competitive economy

is one (though only one) important indicator of how well

the education system is functioning.

• From 2001 to 2010 the Irish education system has

been seen by those executives completing the survey as

better than the European average in meeting the needs

of a competitive economy. However, the gap was closing

and in 2010 Ireland’s score was close to the EU15 average.

• In 2011 and 2012, the opinion of executives that

Ireland’s education system meets the needs of a competitive

economy improved. Ireland ranked third European country

on this indicator in 2012, behind Finland and Denmark.

Ireland’s competitive advantage in the perception of its education system by executives improved in the last two years

Source: IMD World Competitiveness Yearbook

Figure 25 The education system meets the needs of a competitive economy

39

Public Sector Trends 2012

Life expectancy is around the European average

Source: WHO, WHOSIS (life expectancy); IMD World Competitiveness Yearbook (healthy life expectancy)

Figure 26 Life expectancy

• Lifeexpectancyatbirthin2009at80yearswasjust

around the average for the EU15 and better than the EU27

average.

• Healthylifeexpectancyatbirth(theaveragenumber

of years that a person can expect to live in ‘full health’) in

2009 in Ireland was 73 years, around the EU15 average.

40

Public Sector Trends 2012

• Under 5 infant mortality per 000 live births in Ireland

has fallen from 6 in 2004 to 4 in 2011.

• For most countries in the EU15 the infant mortality

rate is around 3 or 4 per 000 live births. Sweden had the

lowest mortality rate at 2.8 in 2011, and Romania the

highest at 12.5.

Child mortality is around the European average

Source: WHO, WHOSIS

Figure 27 Child mortality

41

Public Sector Trends 2012

Ireland ranks around the EU15 average in achieving desirable health outcomes

Source: Euro Health Consumer Index 2012

Figure 28 European consumer health outcomes index

• The Euro Health Consumer Index 2012 (Health Consumer

Powerhouse 2012) includes a composite ‘basket’ measure

of a sub-set of indicators focused on health outcomes13.

The higher the score on this index, the better the outcomes.

• As with most other European countries, Ireland improved

its score on this outcomes index between 2009 and 2012.

• Ireland ranks around the EU15 average on this health

outcomes index. Sweden, the Netherlands and Finland

achieve the top three rankings.

13 The outcomes measured in 2012 are: heart infarct case mortality; infant deaths; ratio of cancer deaths to incidence; preventable years of life lost;

mrsa infections; caesarean sections; undiagnosed diabetes; depression.

42

Public Sector Trends 2012

Twice a year Eurobarometer measures the level of public confidence in the national government and the national parliament.

National government is not defined, and the extent to which it covers both political and administrative elements of

government is unclear. But it is likely to primarily reflect levels of trust in the political parties in power at the time of the

survey. Periodic surveys of trust in regional and local authorities by Eurobarometer are also examined.

5. Trust and confidence in public administration

43

Public Sector Trends 2012

Trust in government remains volatile

Source: Eurobarometer

Figure 29 Level of trust in government

• The level of public trust in government in Ireland tended

to be slightly below the EU15 average from 2001 to 2008,

and at or around the EU27 average from 2004 to 2008.

• However, there was a dramatic fall in the level of trust

in government in Ireland from 2008 to 2010. Trust in

government in the rest of Europe also fell, but only slightly.

In autumn 2010, Ireland expressed the lowest level of trust

in government of any of the EU27 (10 per cent).

• By spring 2011, the level of public trust had increased

significantly to 42 per cent expressing trust in the Irish

government, close to the EU15 average. This fell back to

22 per cent by autumn 2011 and 24 per cent in spring

2012.

44

Public Sector Trends 2012

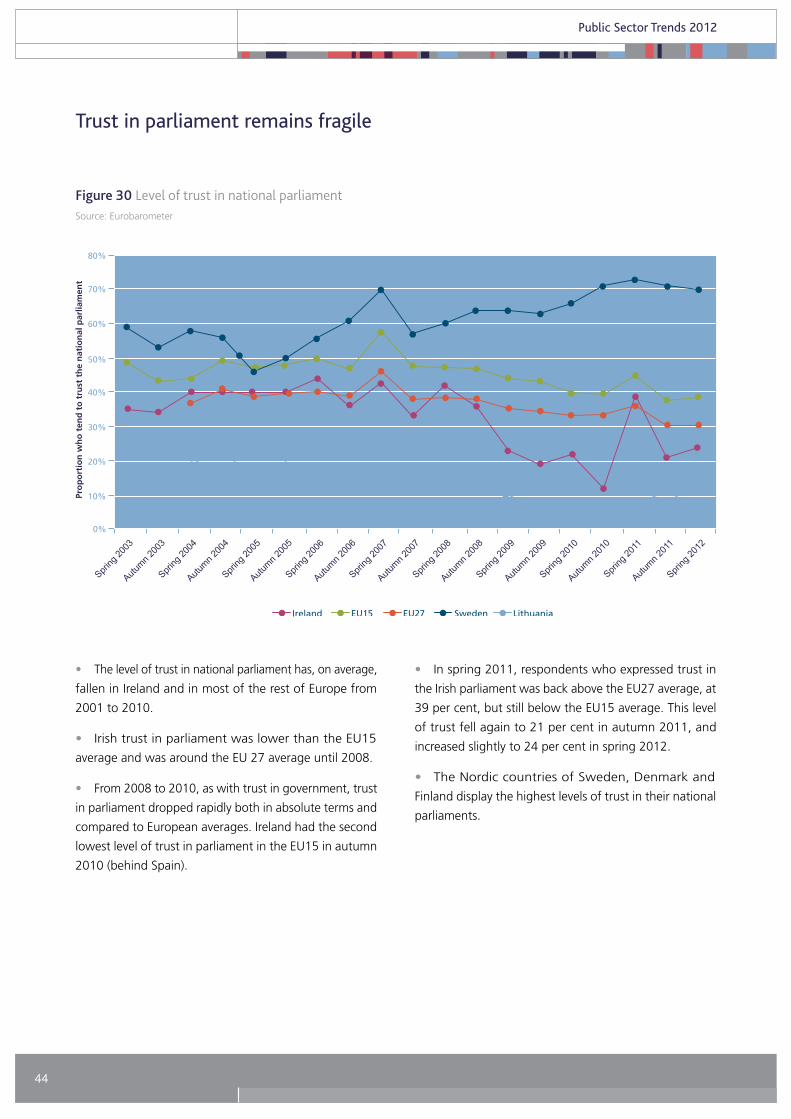

• The level of trust in national parliament has, on average,

fallen in Ireland and in most of the rest of Europe from

2001 to 2010.

• Irish trust in parliament was lower than the EU15

average and was around the EU 27 average until 2008.

• From 2008 to 2010, as with trust in government, trust

in parliament dropped rapidly both in absolute terms and

compared to European averages. Ireland had the second

lowest level of trust in parliament in the EU15 in autumn

2010 (behind Spain).

• In spring 2011, respondents who expressed trust in

the Irish parliament was back above the EU27 average, at

39 per cent, but still below the EU15 average. This level

of trust fell again to 21 per cent in autumn 2011, and

increased slightly to 24 per cent in spring 2012.

• The Nordic countries of Sweden, Denmark and

Finland display the highest levels of trust in their national

parliaments.

Trust in parliament remains fragile

Source: Eurobarometer

Figure 30 Level of trust in national parliament

45

Public Sector Trends 2012

Trust in regional and local authorities is low

Source: Eurobarometer

Figure 31 Level of trust in regional or local public authorities

• The level of trust in regional and local authorities in

Ireland was at 26 per cent in 2011, down from 40 per

cent in 2008. It increased slightly to 30 per cent in spring

2012.

• This is one of the lowest levels of trust in the EU. Only

Greece, Italy and Spain report lower levels of trust in local

authorities in 2012.

46

Public Sector Trends 2012

In terms of overall performance, the data presented in this paper would tend to suggest that the quality of Ireland’s

public administration remains close to the average for the European Union. Indeed, there are some signs that aspects of

quality are seen as having improved in the last two years. This is a notable achievement for a small state such as Ireland,

especially at a time of reducing numbers of public servants and limited resources available for public services.

Knowing where we rank in Europe can point out areas where we need to improve, and identify countries we might learn

from. Many of the indicators used here are based on people’s perceptions of the public service and are clearly influenced

by general economic, political and cultural conditions rather than necessarily any actual change in service. Nevertheless,

such indicators are important in that perceptions influence how people see Ireland as a place to live, do business and

invest. Findings emerging in this light include:

• Numbers employed in the public sector continue to fall. As a percentage of total employment, public service numbers

are not excessive by European standards. As the population continues to increase (placing increasing demands on public

services) and as numbers are reduced further to meet fiscal and economic targets, the challenge of maintaining services

and the skills and capacity needed to provide those services increases. This focuses particular attention on the need for

process improvement to enhance efficiencies and for reducing programme expenditure in some areas.

• The local authority and justice sectors have been particularly hit by staffing reductions. Capacity development in these

areas is of pressing concern.

• The Exchequer pay bill continues to decline from its high in 2008. But the pensions bill is increasing as numbers leaving

and taking early retirement impact on the bill. The need for fiscal discipline to be maintained in these areas remains.

• Given the reductions in numbers and public expenditure, perceptions of the quality of public administration have held

up remarkably well. Irish public services are seen as relatively un-bureaucratic compared to most European countries. The

quality of services to businesses is ranked relatively highly. There is much of Irish public service provision that is seen in a

positive light despite the challenges being faced.

• Trust in government and parliament remains fragile, and trust in local government is low. Much remains to be done

to re-build and maintain the trust of the Irish people in government.

6. Conclusion

47

Public Sector Trends 2012

Afonso, A., L. Schuknecht and V. Tanzi (2003), Public Sector Efficiency: An International Comparison, Working Paper

No. 242, Frankfurt: European Central Bank

Boyle, R. (2007), Comparing Public Administrations, Committee for Public Management Research Report No. 7, Dublin:

Institute of Public Administration

Boyle, R. and M. MacCarthaigh (2011), Fit for Purpose? Challenges for Irish Public Administration and Priorities for

Public Service Reform, Dublin: Institute of Public Administration, http://www.ipa.ie/pdf/Fit_For_Purpose_New_Report.pdf

(accessed November 8 2012)

Foley, A. (2009), ‘The size, cost and efficiency of the public service’, Administration, Vol. 57, No. 1, pp69-101

Health Consumer Powerhouse (2012), Euro Health Consumer Index 2012, Health Consumer Powerhouse, http://www.

healthpowerhouse.com/files/Report-EHCI-2012.pdf (accessed November 8 2012)

OECD (2011), Government at a Glance 2011, Paris: OECD, http://www.oecd.org/gov/indicators/govataglance, (accessed

November 8 2012)

OECD (2010), Public Administration After New Public Management, OECD: Paris

Social and Cultural Planning Office (2004), Public Sector Performance: An International Comparison of Education,

Health Care, Law and Order and Public Administration, The Hague: Social and Cultural Planning Office.

References

48

Public Sector Trends 2012

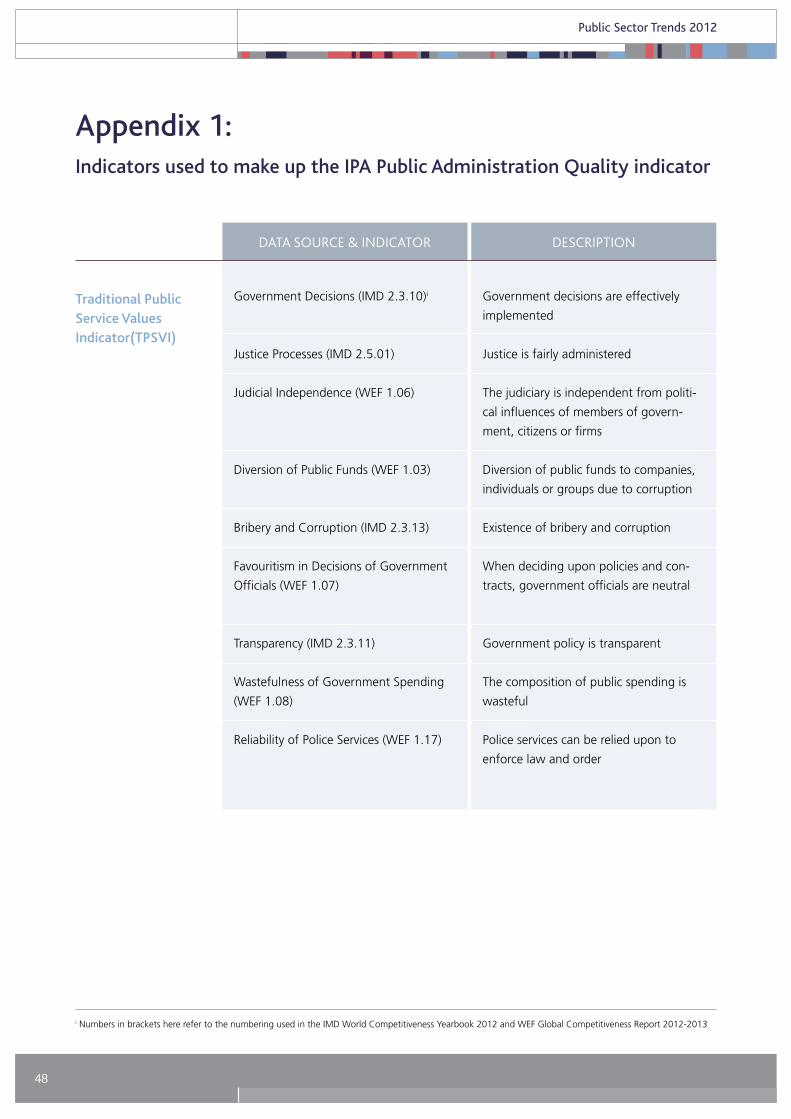

Appendix 1: Indicators used to make up the IPA Public Administration Quality indicator

DATA SouRCE & INDICAToR DESCRIPTIoN

Government Decisions (IMD 2.3.10)i

Justice Processes (IMD 2.5.01)

Judicial Independence (WEF 1.06)

Diversion of Public Funds (WEF 1.03)

Bribery and Corruption (IMD 2.3.13)

Favouritism in Decisions of Government

Officials (WEF 1.07)

Transparency (IMD 2.3.11)

Wastefulness of Government Spending

(WEF 1.08)

Reliability of Police Services (WEF 1.17)

Traditional Public Service Values Indicator(TPSVI)

Government decisions are effectively

implemented

Justice is fairly administered

The judiciary is independent from politi-

cal influences of members of govern-

ment, citizens or firms

Diversion of public funds to companies,

individuals or groups due to corruption

Existence of bribery and corruption

When deciding upon policies and con-

tracts, government officials are neutral

Government policy is transparent

The composition of public spending is

wasteful

Police services can be relied upon to

enforce law and order

i Numbers in brackets here refer to the numbering used in the IMD World Competitiveness Yearbook 2012 and WEF Global Competitiveness Report 2012-2013

49

Public Sector Trends 2012

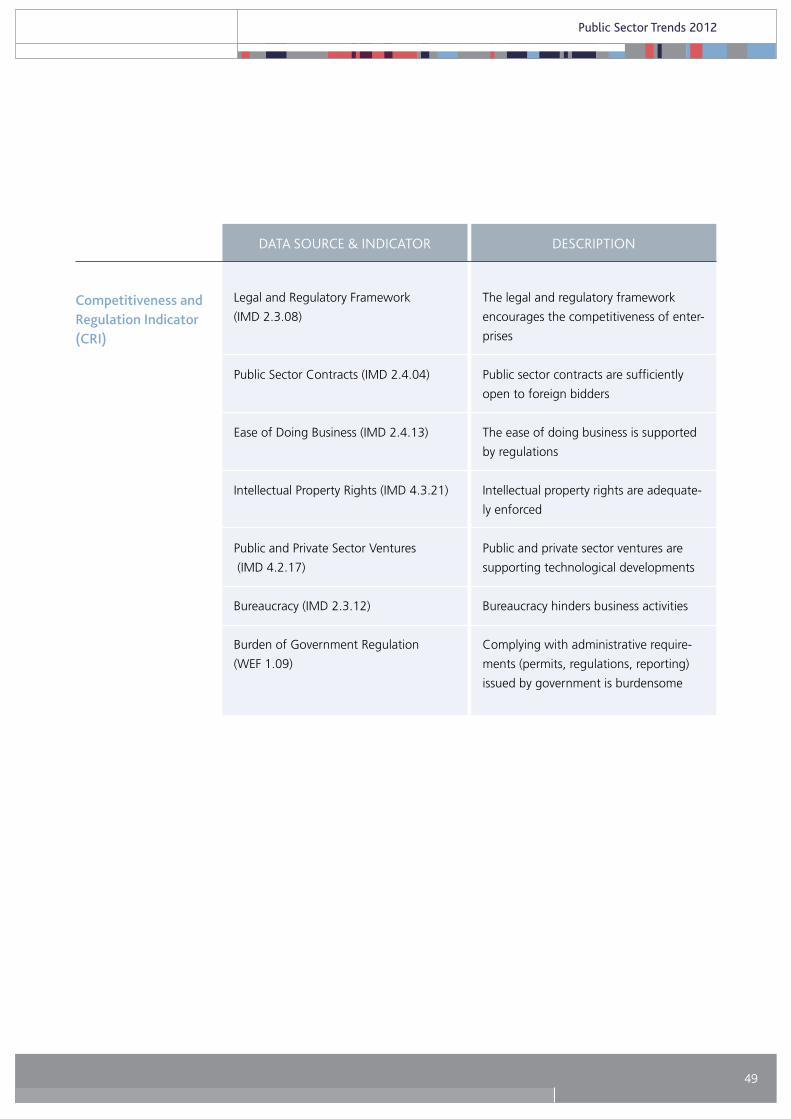

DATA SouRCE & INDICAToR DESCRIPTIoN

Legal and Regulatory Framework

(IMD 2.3.08)

Public Sector Contracts (IMD 2.4.04)

Ease of Doing Business (IMD 2.4.13)

Intellectual Property Rights (IMD 4.3.21)

Public and Private Sector Ventures

(IMD 4.2.17)

Bureaucracy (IMD 2.3.12)

Burden of Government Regulation

(WEF 1.09)

Competitiveness and Regulation Indicator (CRI)

The legal and regulatory framework

encourages the competitiveness of enter-

prises

Public sector contracts are sufficiently

open to foreign bidders

The ease of doing business is supported

by regulations

Intellectual property rights are adequate-

ly enforced

Public and private sector ventures are

supporting technological developments

Bureaucracy hinders business activities

Complying with administrative require-

ments (permits, regulations, reporting)

issued by government is burdensome