public disclosure authorized coffee, tea, and cocoa tea, and cocoa market prospects ... deepak lal,...

TRANSCRIPT

Coffee, Tea, and CocoaMarket Prospectsand Development Lending

OCP-22Shamsher Singh, Jos de Vries,John C. L. Hulley, and Patrick Yeung

WORLD BANK STAFF OCCASIONAL PAPERS Z NUMBER TWENTY-TWO

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

World Bank Staff Occasional Papers

No. 1. Herman G. van der Tak, The Economic Choice between Hy-droelectric and Thermal Power Developments.

No. 2. Jan de Weille, Quantification of Road User Savings.No. 3. Barend A. de Vries, The Export Experience of Developing

Countries (out of print).No. 4. Hans A. Adler, Sector and Project Planning in Transportation.No. 5. A. A. Walters, The Economics of Road User Charges.No. 6. Benjamin B. King, Notes on the Mechanics of Growth and

Debt.No. 7. Herman G. van der Tak and Jan de Weille, Reappraisal of a

Road Project in Iran.No. 8. Jack Baranson, Automotive Industries in Developing Coun-

tries.No. 9. Ayhan ,Cilingiroglu, Manufacture of Heavy Electrical Equip-

ment in Developing Countries.No. 10. Shlomo Reutlinger, Techniques for Project Appraisal under

Uncertainty.No. 11. Louis Y. Pouliquen, Risk Analysis in Project Appraisal.No. 12. George C. Zaidan, The Costs and Benefits of Family Planning

Programs.No. 13. Herman G. van der Tak and Anandarup Ray, The Economic

Benefits of Road Transport Projects.No. 14. Hans Heinrich Thias and Martin Carnoy, Cost-Benefit Analy-

sis in Education: A Case Study of Kenya.No. 15. Anthony Churchill, Road User Charges in Central America.No. 16. Deepak Lal, Methods of Project Analysis: A Review.No. 17. Kenji Takeuchi, Tropical Hardwood Trade in the Asia-Pacific

Region.No. 18. Jean-Pierre Jallade, Public Expenditures on Education and In-

come Distribution in Colombia.No. 19. Enzo R. Grilli, The Future for Hard Fibers and Competition

from Synthetics.No. 20. Alvin C. Egbert and Hyung M. Kim, A Development Model

for the Agricultural Sector of Portugal.No. 21. Manuel Zymelman, The Economic Evaluation of Vocational

Training Programs.No. 22. Shamsher Singh and others, Coffee, Tea, and Cocoa: Market

Prospects and Development Lending.No. 23. Shlomo Reutlinger and Marcelo Selowsky, Malnutrition and

Poverty: Magnitude and Policy Options.

WORLD BANK STAFF OCCASIONAL PAPERS r:1 NUMBER TWENTY-TWO

The views and interpretations in this book are those of the authors and shouldnot be attributed to the World Bank, to its affiliated organizations, or to anyindividual acting in their behalf.

SHAMSHER SINGH, JOS DE VRIES

JOHN C. L. HULLEY, AND PATRICK YEUNG

Coffee, Tea, and CocoaMarket Prospects

and Development Lending

Published for the World Bank

THE JOHNS HOPKINS UNIVERSITY PRESSBALTIMORE AND LONDON

Copyright © 1977 The International Bank for Reconstruction and Developmenc /The World BankAll rights reserved

Mau ufact ured in the Uniited States of .Ameiica

Library of Congress Cataloging in Publication DataMain entry under title:

Coffee, tea, and cocoa.

(World Bank staff occasional papers; 22)1. Coffee trade. 2. Cocoa trade. 3. Tea trade. 4. Economic assistance. 1. Singh,Shamsher, 1928- 11. International Bank for Reconstruction and Development. I][J.Title. IV. Series.HD9199.A2C64 380.141"37 76-17239ISBN 0-8018-1869-9

FOREWORD

I would like to explain why the World Bank doesresearch work and why this research is published. We feel anobligation to look beyond the projects that we help finance towardthe whole resource allocation of an economy and the effectiveness ofthe use of those resources. Our major concern, in dealings withmember countries, is that all scarce resources-including capital,skilled labor, enterprise, and know-how-should be used to theirbest advantage. We want to see policies that encourage appropriateincreases in the supply of savings, whether domestic or international.Finally, we are required by our Articles, as well as by inclination, touse objective economic criteria in all our judgments.

These are our preoccupations, and these, one way or another, arethe subjects of most of our research work. Clearly, they are also theproper concern of anyone who is interested in promoting develop-ment, and so we seek to make our research papers widely available.In doing so, we have to take the risk of being misunderstood.Although these studies are published by the Bank, the viewsexpressed and the methods explored should not necessarily beconsidered to represent the Bank's views or policies. Rather, they areoffered as a modest contribution to the great discussion on how toadvance the economic development of the underdeveloped world.

ROBERT S. MCNAMARA

PresidentThe World Bank

PREFACE

This paper consists of studies of the markets for coffee,cocoa, and tea prepared for the use of World Bank staff. The Bank'scommodity studies serve a dual purpose: to evaluate prospects forthe export earnings of borrowing member countries and to assessthe market prospects for individual commodities. Thus, they mayhelp to justify lending for increased production and for diversifica-tion into more promising fields.

The paper was prepared under the overall direction of ShamsherSingh, chief of the Commodities and Export Projections Division,who also wrote chapter 1. Chapter 2 was written by Jos de Vries,who also prepared Appendix A. Chapter 3 contains contributions byJohn Hulley and Patrick Yeung. Chapter 4 was written by PatrickYeung, who also prepared appendix B.

This paper has benefited greatly from the comments of severalpeople in the Bank. The authors are particularly indebted to RachelWeaving for editorial assistance in early drafts and to Maw-ChengYang and John E. Fisk for their help in data collection. The finalmanuscript was edited by Donald J. Pryor.

WOUTER TIMSDirector

Economic Analysis and Projections DepartmentWashington, D. C.

Summer 1976

CONTENTS

Foreword vPreface viiSynthesis and background 3

Economic characteristics 6 -The scope for increasing exportearnings 8 -The role of the World Bank 14 -Summaryof prospects: principal findings and conclusions 18

2. The world coffee market 24

Production and exports 27 -Imports and consumption 34-Prices and stocks 37 -Market outlook 43 -Theinternational coffee agreement 48

3. The world tea market 49

Production and exports 49 -Imports and consumption 58-Prices 61 -Market prospects 61 -Market shares andthe scope for international action 71

4. The world cocoa market 76

Production and exports 76 -Imports and consumption 87-Prices and stocks 96 -Market prospects 96 -Productionforecasts 99 -Demand projections 99 -Priceforecasts 100 -Sensitive factors 102 -The internationalcocoa agreement 103

Appendix A: An econometric model of the world coffee economy 104

The coffee model: equations, 1947/48 to 1972/73 110 -Thecoffee model: glossary of symbols 112

X CONTENTS

Appendix B: A comparative analysis of cocoa production in selectedcountries 115

The domestic resource cost approach 116 -Countrycoverage and data collection 118 -Findings for plantationproduction 119 -Findings for peasant production 123 --Comparison of findin,gs on the two methods of cocoaproduction 125 -Combined results for the twomethods 125 -Qualifications of findings 126 -

Conclusion 127

Appendix C: Development lending 128

Tables

1. World market shares of developing countries in, anddependence on, coffee, tea, and cocoa 4

2. Type of coffee grown, share in world production, growth rate,and share of coffee in export earnings: coffee-producingcountries 28

3. Price elasticities of coffee supply, by region 31

4. Share of coffee in foreign exchange receipts and GNP figuresfor countries highly dependent on coffee production 34

5. Average imports of coffee, total and per capita, majorimporting countries, 1950-53 and 1970-73 36

6. Price and income elasticities of demand for coffee, selectedyears, 1950-85 38

7. Coffee prices in the New York spot market 40

8. Average refunds to coffee importers under "contracts ofsupply" 41

9. Actual and projected coffee production and growth rates, byregion and year, 1970-86 and 1972-90 44

10. Actual and projected coffee consumption and growth rates, byregion and year, 1970-86 and 1972-90 46

11. Actual and projected coffee prices, and deflator, by year,1970-86 47

12. Average tea production, by region and country, and shares ofworld total, 1955-57 and 1971-73 51

13. Tea production, expcrts, and share of production exported,major producing countries, selected years, 1960-73 52

Contents xi

14. Average world tea exports, export value, export unit value, andLondon auction prices, 1955-57, 1960-62, and 1971-73,and annual percentage change, 1955-57 to 1960-62 and1960-62 to 1971-73 55

15. Value and market share of tea exports, Africa and South Asia,and per capita incomes 56

16. Average value of tea exports and tea share in world exportsand in total country export earnings, selected Asian andAfrican countries, 1955-57 and 1971-73 57

17. Imports of tea, selected countries, yearly, 1968-73 58

18. Comparison of tea imports and reexports of the UnitedKingdom with world totals, selected years, 1955-73 60

19. Average tea consumption, by region and country and shares ofworld total, 1955-57 and 1971-73 62

20. Price and income elasticities of the demand for tea, selectedcountries 64

21. Annual average tea prices for selected countries at Londonauctions, by year, 1955-75 66

22. Summary of tea production, consumption, and trade, 1955-57,1967-69, and 1973, with projections to 1980 and 1985 68

23. Price elasticity of demand for exports of tea, market share, andper capita GNP, selected countries, 1967-69 72

24. World production and exports of cocoa beans 7825. Export value of cocoa beans and products, selected countries,

and share in world totals and in national export earnings80

26. World summary of cocoa production, grindings, stocks, prices,exports, and imports, 1946-75 82

27. Export volume and total and unit value of cocoa beans 8428. Imports of cocoa beans, selected countries, 1957-61, 1967-71,

and 1973 88

29. Trade in cocoa beans by main areas of origin and destination,1970 89

30. Cocoa bean grindings by country, 1934-38 to 1973 90

31. Cocoa consumption of selected countries, 1957-61, 1967-71,and 1972 92

32. Elasticities of demand for cocoa in bean equivalent, selectedcountries 94

33. Price elasticity of demand for cocoa: three estimates 95

Xii CONITENITS

34. World cocoa production: actual, 1967-71, and projections for1980 and 1985 98

35. Basic projections of world demand for cocoa, 1980, using FAOmodel 101

B1. Estimated ratios of D:RC to SER (and to FX) for cocoaproduction 120

B2. Estimated ranges of I)RC/SER ratios for plantation cocoaproduction, various countries 122

B3. Computed DRCs and related measures of comparativeadvantage in 1972 for major cocoa-producing countries,using the average world spot price for 1972 123

B4. Original estimates of DRC/SER ratios, major cocoa-producingcountries 126

Cl. World Bank lending for cocoa and tea planting 129

Figures

1. Tea production in major producing countries and Africa,1955-74 53

2. Volume, total value, and unit value of world exports of tea,1955-73 54

3. Average annual tea prices at London auctions, selectedcountries, 1955-75 65

4. Elasticity of demand and market shares of tea-exportingcountries 74

5. Volume, total value, and unit value of world exports of cocoabeans, 1950-73. 86

6. Surplus or deficit of stocks and market prices for cocoa,1947-73 97

Al. Actual and simulated coffee prices since 1949 106A2. Price projections for coffee under different assumptions about

frost 107A3. Price projections for coffee at different levels of inflation 108A4. Price projections for coffee at different levels of income

growth 109

Coffee, Tea, and CocoaMarket Prospects

and Development Lending

1

SYNTHESIS AND BACKGROUND

THE INTEREST OF THE WORLD BANK' in the marketprospects for primary commodities stems from a variety of consider-ations. Primary products account for four-fifths of the total exportsof the Bank's developing members, its principal borrowers. Al-though exports of manufactured goods from these countries havebeen rising rapidly-by 13 percent a year in 1955-72-the startingbase is small, and primary commodities remain the main determi-nant of their overall export performance and ability to serviceexternal debt. The ability of Bank investments to enlarge theproductive base of the primary sector is directly affected by themarket outlook for the products involved. Coffee, tea, and cocoa areamong the more important primary commodities and are studied bythe Bank staff on a continuous basis. Coffee, in fact, is second only tooil as an earner of foreign exchange for developing countries. In1972-74, when the total export earnings of developing countriesfrom primary commodities other than oil were estimated at approxi-mately $47,000 million, the value of their exports of coffee was$3,700 million; of tea, $660 million; and of cocoa (beans), $1,000million.2 They are especially important in the export earnings ofsmall, poor countries (see table 1).

Studies of the three products have been combined in one bookbecause the economics of coffee, tea, and cocoa have much in

1. As used in this paper, the term "World Bank" refers to both the Interna-tional Bank for Reconstruction and Development and its affiliate, The Interna-tional Development Association.

2. All money amounts are in U.S. dollars unless otherwise specified. Tons aremetric tons.

3

Table 1. World Market Shares of Developing Countries in, and Dependence on, Coffee, Tea, and Cocoa

Countsy share in commodity exports Commodity sitares in country exports 1970-72Population, GNP per 1970-72 (percent) (percent)mid-1972 capita 1972

Region and counbly' (millions) (U.S. dollars) Coffte Cocoa Tea Coffee Cocoa Tea Total

T'otal, developing countries 96.8 100.0 83.1 4.9 1.3 1.0 7.2

Latin America and Caribbean

l3razil 98.2 530 30.2 8.7 0.5 27.7 2.1 0.1 29.9Colombia 23.0 400 14.4 0.0 0.0 58.8 0.0 0.0 58.8Costa Rica i.8 b3o 2.4 (.3 (0.0 28.9 0.9 0.0 29.8Dominicari Republic 4.2 480 0.8 2.1 0.0 8.5 G.0 0.0 14.5

4 Ecuador 6.5 360 1.5 3.1 0.0 16.8 9.2 0.1 26.1El Salvador 3.7 340 3.5 0.0 0.0 42.0 0.0 0.0 42.0Guatemala 5.6 420 3.5 0.0 0.0 33.7 0.1 0.0 33.8Haiti 4.4 130 0.6 0.1 0.0 43.3 1.6 0.0 44.9Honduras 2.7 320 0.9 (.0 0.0 14.7 0.0 0.0 14.7Nicaragua 2.2 470 1.0 0.0 0.0 15.5 0.1 0.0 15.6West Indies (British) n.a. n,a. 0.0 0.3 0.0 0.0 14.1 0.0 14.1Total 63.7 16.7 2.0 10.2 0.7 0.1 11.0

Africa

Angola 5.6 390 4.8 0.0 0.( 31.4 0.1 0.0 31.5Beniii 2.9 110 0.0 0.8 0.0 3.2 16.8 0.0 20.0Burundi 3.5 70 0.6 0.0 0.0 73.0 0.0 0.0 73.0Cameroon 6.1 200 1.9 6.5 0.I 25.1 22.7 0.3 48.1Central Africani Republic 1.7 160 0.2 0.( 0.( 20.6 (.0 0.( 20.6C.oniomo islatds Il.<l. n.a. 0.0 0.0 0.0 5.0 (.0 0.0 5.0

Equatorial Guinea n.a. n.a. 0.2 2.0 0.0 27.7 69.1 0.0 96.8Ethiopia 25.9 80 2.5 0.0 0.0 53. 3 0.0 0.0 53.3Ghana 9.1 300 0.0 31.7 0.0 0.3 62.0 0.0 62.3Guinea 5.1 90 0.2 0.0 0.0 11.7 0.0 0.0 11.7Ivory Coast 5.4 340 5.5 11.6 0.0 32.7 17.9 0.0 50.6Kenya 12.1 170 2.1 0.0 5.7 26.6 0.0 17.1 43.7Madagascar 7.4 140 1.4 0.1 0.0 26.3 0.3 0.0 26.6Malawi 4.7 100 0.0 0.0 2.0 0.3 0.0 20.3 20.6Nigeria 69.5 130 0.1 23.7 0.0 0.1 10.3 0.0 10.4

Rwanda 3.9 60 0.4 0.0 0.2 57.3 0.0 6.4 63.7Sao Tome and Principe n.a. n.a. 0.0 0.7 0.0 1.7 83.3 0.0 85.0Sierra Leone 2.7 190 0.2 0.5 0.0 6.4 3.6 0.0 10.0Tanzania 13.6 120 1.5 0.0 0.9 16.1 0.1 2.4 18.6Togo 2.1 160 0.3 2.3 0.0 18.0 34.5 0.0 52.5

Uganda 10.5 150 4.9 0.0 2.1 58.8 0.0 5.9 64.7Zaire 19.1 100 1.3 0.3 0.2 5.8 0.3 0.2 6.3

Total 28.3 80.7 13.1 6.1 4.5 0.7 11.3

Asia and Oceania

Bangladesh 72.5 70 0.0 0.0 4.9 0.0 0.0 11.0 11.0India 563.5 110 1.4 0.0 28.8 1.9 0.0 9.5 11.4Papua New Guinea 2.6 290 0.8 1.9 0.1 16.2 9.9 0.5 26.6Portuguese Timor n.a. n.a. 0.1 0.0 0.0 90.5 0.0 0.0 90.5Sri Lanka 13.2 110 0.0 0.1 27.4 0.0 0.3 59.5 59.8Yemen, Arab Republic of 6.1 90 0.1 0.0 0.0 35.0 0.0 0.0 35.0

Total 4.7 2.6 68.0 0.5 0.1 1.9 2.5

n.a. Not available.a. Only those countries have been included in which at least one of the three cotmmodities accounts for 5 percent or more of export earnings.Sources: Shares in exports, "Commodity Trade and Price Trends," Report EC-166/75 (Washington, D.C., 1974); Population and GNP per capita, World Bank Atlas

1974 (Washington, D.C., 1974).

6 COFFEE, TEA, AND COCOA

common and the Bank's lending policies toward their production,processing, and marketing are guided by virtually identical criteria.All are tropical products, exported almost exclusively by developingcountries. Production is largely concentrated in poor countries thatdepend heavily on them fcr their foreign exchange earnings. Theirmain markets are in the developed countries. Demand for them inthe major importing countries grows slowly, since their incomeelasticity is low.3 Their real prices have tended to decline, and thereis little scope for increasing their aggregate export earnings in rcalterms.4 Prospects for raising (as opposed to stabilizing) pricesthrough producer action or international agreement are limnited.Benefits could accrue to the developing countries, however, if themajor importing countries were to eliminate their internal taxes onthese commodities and liberalize their imports of processed pro,d-ucts.

Chapters 2 through 4 deal in general terms with the markets forcoffee, tea, and cocoa, respectively. For each product, an overvilew isgiven of production and exports and of consumption and imports,followed by a section on the market outlook. The two appendixes,one on coffee and the other on cocoa, summarize two of the studiesthat lay behind the market forecasts in chapters 2 and 4.

ECONOIAIC CHARACTERISTICS

Coffee, tea, and cocoa are tree crops with gestation periods of aboutfive years. They mature in from seven to ten years and have aneconomic life of about forty years. The new hybrid varieties startyielding in the third year, mature earlier than the older varieties, andhave a shorter economic life. Capital costs of establishing newplantings are high. Among recurrent costs, those for labor predomrli-nate, for both cultivation and harvesting are highly labor intensive.Price changes have little effect on supply in the short run, lbut adecided effect in the long run; when prices are high, therc is atendency toward overinvestment. Thus, price movements tend to be

3. In the language of econorrics, elasticity is the degree to which one variablewill change in response to change in another. Thus the elasticity of A with respectto B (or the B elasticity of A) is the percentage increase in A resulting from a Ipercent increase in B.

4. Relative to their import pur chasing power, for example, the nuhnber of bagsor tons of coffee, tea, or cocoa required to import a tractor or other vehicle.

Synthesis and Background 7

cyclical, with periods of boom often being followed by long periodsof oversupply and low prices.

By far the greater proportion of output from developing countriesenters international trade; with a few major exceptions-notablyBrazil in the case of coffee and India in the case of tea-domesticconsumption is small. In each case a small number of producingcountries accounts for a large share of world exports: Brazil,Colombia, and the Ivory Coast for coffee (48 percent of worldexports in 1970-72); India, Sri Lanka, and the Eastern Africancountries for tea (73 percent); and Ghana, Nigeria, and Brazil forcocoa (54 percent).5

A large number of producing countries are dependent on thesecommodities for a high proportion of their export earnings: abouttwenty-five derive more than a fourth of their export earnings froma single one, and several obtain a high proportion from coffee andtea or coffee and cocoa combined. Many of these countries haveannual per capita incomes of less than $200 and low rates of growthof gross national product (GNP).

Developed countries with market economies are the principalimporters of these beverages.' In 1970-72 they accounted for 92percent of the value of coffee exports from the developing countries,79 percent in the case of cocoa, and 61 percent in the case of tea.These percentages have changed little over the years, although theSoviet Union has emerged as an important importer of cocoa anddeveloping countries that do not produce tea now import largequantities of the less costly varieties.

In general, the elasticity of demand for these commodities in themajor importing countries is low with respect to both income andprice, at least within historical price ranges. Global price elasticities ofdemand 7 have been estimated at about -0.25 for coffee, -0.3 fortea, and -0.4 for cocoa. In most of the importing countries, incomeelasticities of demand for all three have tended to decline as percapita incomes have risen.

5. See table 1.6. Traditionally, cocoa was used as a beverage, hot chocolate; now its main use

is in confectionary. Cocoa's nomenclature as a beverage is thuts notional.7. Proportionate change in price required to induce a given change in demand.

For example, a price elasticity of -0.2 means that, for the market to absorb Ipercent of additional supplies, price would have to fall by 5 percent. Whenelasticities are low, the producers do not benefit from bringing additional supplieson the market.

8 COFFEE, TEA, AND COCOA

Since demand in the industrialized countries is relatively unres-ponsive to changes in price, increases in aggregate supply in excessof long-term demand depress international prices so that real exportearnings stagnate. Thus, between 1950 and 1972 the volume ofworld exports of coffee grew at an average rate of 3 percent a year,but the real value grew by only an average 0.6 percent a year. Overthe same period, the volume of world cocoa exports increased by 2.4percent a year and their real value by 1.7 percent; the volume ofworld exports of tea grew by 2 percent a year and their real value byonly 0.25 percent.

Under the assumptions detailed in the following chapters, worldimport demand for coffee is expected to increase by less lthan 2percent a year between 1973 and 1980 and consumption in theUnited States, the largest importer, is expected to decline at amarginal rate. World supplv and demand will be in a precariousbalance because of the destructive effects of the Brazilian frost ofJuly 1975; real prices are expected to remain relatively high in thenext few years, at a level of between 80 and 85 cents a pound (in1974 terms). Thereafter, a slow but steady decline in prices willaccompany the expected price-induced expansion of production.

As in the past, the international tea market is likelv to remaincharacterized by surpluses and weakening prices. World consump-tion of tea is expected to grow at an average rate of 3 percent a yearin the decade ahead, expanding more slowly than during the last twodecades. In real terms, tea prices are expected to decline substan-tially between 1970-72 and 1980.

The growth in world cocoa exports, which averaged nearly 3percent a year in the 1960s, dedined to less than 2 percent in theearly 1970s as supplies were reduced. Cocoa exports are expected toremain sluggish until 1976, then to turn up again as production risesin response to the high prices of the recent past and demand picksup in response to the downward adjustment in prices. Real prices ofcocoa are expected to decline to the low levels prevailing in 1970-72.

THE SCOPE FOR. INCREASING EXPORT EARNINGS

In general, there is little scope for rapid and sustained increases inthe earnings of developing countries from exports of coffee, tea, andcocoa. The most effective way to increase the total export earnings ofmany producers of these commodities would be to encourage

Synthesis and Background 9

diversification into the production of other crops for the domesticmarket and into the production of other exportable commodities forwhich prospects for demand are more favorable. FoI small and poorcountries, such a strategy may be unrealistic; for them, internationalmeasures to help increase their earnings from these staple commodi-ties may be crucial.

Several small and poor producers of coffee, tea, and cocoa have infact been able to expand their total export earnings relatively fast byexpanding their shares of the market for one or more of thesecommodities. They have done so at the expense of other exporters,whose market shares were correspondingly reduced. For example,the Ivory Coast increased the value of its cocoa exports by 10.5percent a year between 1960-62 and 1967-69, while the value ofworld cocoa exports grew by only 4 percent a year. This had anadverse effect upon the value of cocoa exports from Ghana, which atthe end of the 1960s still depended on cocoa for about 69 percent ofits export earnings. The Ivory Coast's dependence on cocoa was onlyof the order of 24 percent. In the case of coffee, Colombia and, evenmore notably, Brazil have been able to implement diversificationpolicies. In addition, recognizing their own interest in keepinginternational prices up, they deliberately restricted their coffeeexports.

It cannot be assumed, however, that important exporters ofcoffee, tea, or cocoa will always choose to diversify out of theirtraditional export staples, at least to any great extent, as they developthe capacity to do so. For example, the value of Indian and SriLankan tea on world markets continues to be eroded as the EasternAfrican countries expand their exports. If these two largest produc-ers were to restrict their exports voluntarily to take account of thenew producers' increasing shares of the market, they would benefitfrom the resulting effect on international price (provided, of course,the African expansion was held within reasonable limits). Untilrecently, however, neither has shown any clear propensity to do soor to promote diversification out of tea on a significant scale.

Three possible areas of action to enhance the prospects foraggregate export earnings from these commodities are consideredbriefly in the remainder of this section: increasing import demand inthe developed countries through trade liberalization; increasing thevalue-added component of exports by developing processing indus-tries in producing countries; and stabilizing or raising world pricesthrough international agreements.

10 COFFEE, TEA, AND COCOA

Liberalization of trade

Coffee, tea, and cocoa are noncompeting commodities in markets ofdeveloped countries in that they have no close substitutes (althoughconsumers' tastes may change) and cannot be produced in thesecountries.8 Thus, trade restrictions are not a highly significantconstraint on export earnings and are not as important as they arefor many other commodities, such as sugar.

Nonetheless, the benef.ts of trade liberalization should riot beunderestimated. A World Bank study9 shows that the gradualremoval of tariffs and of nontariff barriers (such as quantitativerestrictions and internal taKes) might enable developing countries toearn an additional $300 rnillion to $350 million annually (in 1974constant terms) from exports of these products. This estimate is onthe conservative side because it does not include the effect of theremoval of voluntary or subtle restrictions such as those on Brazilianexports of soluble coffee lo the United States. It also excludes theeffects of the possible contraction of tea production in Japan afterthe high Japanese import duty has been removed.

Tariffs on coffee are generally low or nonexistent. The EuropeanEconomic Community (EEC) levies an import duty of 7 percent, butcoffee from a number of African, Caribbean, and Pacific countriesenters duty free under the Lome agreement of 1975. Nontariffbarriers are even less comnion, but internal taxes are extremely highin Italy and West Germany. If trade in coffee were further liberal-ized, the effects on export earnings would be small, except for thesuppliers to West Germany (the largest importer of coffee after theUnited States), in which a sharp reduction in retail price (given alsothe relatively high price elasticity of demand) would mean expandedimports. The major share of the gains would go to producers of mildarabica coffees, which are preferred by the West German market.

Quantitative restrictions Dn tea have been removed by virtually alldeveloped countries. There are no import duties on tea into theUnited States and Canada. Tea from African, Caribbean and Placif-ic(ACP) countries enters the EEC duty free. Import duties are high,however, in Japan and mcst developing countries, such as those in

8. Japan is an exception; it accounted for about 9 percent of world teaproduction in 1969-7 1. Japan, h owever, is still a net importer of tea.

9. Wouter Tims, Possible Effects of Trade Liberalization on Trade in PrimanvCommodities, Working Paper no. 193 (Washington, D.C.: World Bank, Januwry1975).

Synthesis and Background 11

the Near East. Duties are also high on imports by many countries oftea extracts, essences, or concentrates. This situation adds to theproblems of developing export-oriented processing industries inproducing countries.

Import duties on cocoa beans and cocoa products have beenconsiderably reduced since the early 1960s, and none remain in mostdeveloped countries. As a result of the Lom& Agreement, cocoabeans and cocoa products originating in the African, Caribbean, andPacific (ACP) signatory countries enter any member state of the EECduty free as of July 1, 1975. Because of the inelastic demand forcocoa and the few tariffs remaining, the scope for increasing theconsumption of cocoa beans and products through further tariffreduction is rather limited. This is not the case, however, withrespect to chocolate products, for which tariffs and other duties stillplay an important role. Trade liberalization could greatly enhancethe manufacture of chocolate in developing countries.

Increasing the value-added component

Possibilities of expanding the value of exports by increasing the valueadded appear to be substantial. Currently, about 17 percent of theexports of cocoa from developing countries is in the form ofintermediate products, compared with about 6 percent in 1960, andthis rising trend is expected to continue. Cocoa-processing industriesgrew rapidly in West African producing countries during the 1960s,and processed products now account for a significant part of thevalue of their cocoa exports. Nevertheless, the growth of processedexports could be even further accelerated.

Coffee is sold in retail markets of developed countries at all stagesof processing, but traditionally roasting and grinding have not beencarried out in exporting countries because roasted beans rapidly losetheir freshness when exposed to air. Demand for soluble coffee hasbeen increasing rapidly over the past two decades, particularly inimporting countries where high per capita coffee consumption is arecent development (for example, the United Kingdom). At present,exports of soluble coffee account for less than 4 percent of coffeeexports from developing countries, principally Brazil. A lowering oftrade barriers will certainly help the developing countries to capturea larger share of this market.

Developing countries are gradually establishing facilities for theprocessing of raw tea into such products as instant tea or tea bags.Instant tea factories, for example, are already found in India, Sri

12 COFFEE, TEA, AND COCOA

Lanka, and Uganda. At present their output is exported mainly tothe United States and the United Kingdom. Potential marketsinclude the EEC countries. Canada, Australia, and the Soviet Union.

International agreements

Because coffee, tea, and cocoa are noncompeting commodities intheir main markets (and thus the maintenance of remunearativeinternational prices is unlikely to encourage substitution or theimposition of high tariffs in importing countries), the possibilities Forstabilizing export earnings through international agreements arerelatively bright. The negctiation and implementation of agreementsdesigned to stabilize earnings through export quotas for primarycommodities facing inelastic demand may confront many difficulties,however, as shown by the history of previous attempts to organizethe coffee, cocoa, and tea markets.

For example, unless controls are imposed, high prices maintainedby the agreement may stimulate excessive production, bringingpressure by member countries against the continued restriction ofexports on which the maintenance of price depends. Conflicts overthe size of market shares can be another obstacle to the negotiationor maintenance of such an agreement. There may also be adverseeffects on the distribution of income within a producing country ifthe volume of exports is successfully restricted: if the internationlalprice rises, well-establishec. producers may benefit at the expense ofthe newly emerging producers, who may be in greater need of anopportunity to increase their incomes. It may also be difficult toensure the cooperation oif consuming countries, particularly if theagreement is to have a price-raising effect. Without their coopera-tion, an export quota system may easily be abused by individualexporters, and the conseqluent depressing effect on prices will bespread over all.

International commodity agreements nevertheless have great po-tential value in stabilizing export earnings, let alone internationalprices. If only for this reason, there is a strong case for redoubledefforts to negotiate such schemes and maintain the machinery evenwhen economic provisions are not in force. There is also the ne,ed, asshown by experience, to keep their operation flexible. The Interna-tional Coffee Agreement of 1968 was based on a system of flexibleexport quotas, which were fixed at the beginning of each crop yearand adjusted whenever t:ne price moved out of a preestablishedrange. The effectiveness of such a system depends in large part on

Synthesis and Background 13

the willingness of participants to abide by its rules. Because theburden of stocks that can result from a limitation of exports has tobe borne by the individual producing country, such a system hasinvariably broken down when backed by producers alone. Moderatesuccess was achieved by the Coffee Agreement when consumersjoined producers to monitor the system, but when they refused toagree to a revision of price ranges to cope with world inflation andexchange rate changes, cooperation broke down.

Negotiations to arrive at a new International Coffee Agreementhave been in progress since 1973. In December 1975 producers andconsumers finally agreed upon the text of a new agreement, tobecome effective October 1, 1976. As in the previous agreement, themechanism of market control is the export quota system. There aretwo points, however, on which the present agreement differs fromits predecessors. First, the distribution of quotas among producingcountries depends not only on past export performance but also onstocks. This provision is intended to guarantee supplies to consumersby giving producers an incentive to accumulate stocks. Second, ifprices rise above certain levels, the quota system will automatically besuspended. This provision is intended to give the agreement moreflexibility and prevent it from breaking down in the face of strongupward pressure on prices.

Efforts to organize the tea market have not yet been fruitful. Atthe initiative of the exporters, who remain divided, the Intergovern-mental Group on Tea of the Food and Agriculture Organization ofthe United Nations (FAO) set up a working party in June 1974 tostudy proposals for an international agreement. Proposals underreview include the establishment of a minimum export price, coordi-nation and regulation of marketing to avert the buildup of stocks inimporting countries, which would have a depressing effect on prices,and increased promotion of world consumption.

The first International Cocoa Agreement between producers andconsumers came into force in June 1973. It provided for annualexport quotas, a buffer stock with capacity to purchase up to 250,000tons, and a fixed price range of 23 to 32 U.S. cents a pound. Theexport quota system and the price have never been applied. Theaverage price of cocoa (New York, spot, Accra)"0 in 1974 was threetimes higher than the agreement's ceiling price, and there were no

10. Ghanian cocoa of specified quality sold at New York for spot, or immediate,delivery.

14 COFFEE, TEA, AND COCOA

accumulated buffer stocks that could be sold, and thus used ats amoderating influence on prices. Many producing countries hadurged that the agreed puice range be revised upward, but tlhis wasnot accepted by the consumers. The agreement will expire at theend of the 1975-76 quota year: the second cocoa agreement,retaining the essential features of the first, has been renegotiated.The stipulated size of the buffer stock remains unchanged but theprice range has been raised to reflect the expected state of themarket.

THE ROLE OF THE WORLD BANK

Since its inception, the A'World Bank has invested in the agriculturalsector in developing countries, originally with an emphasis on majorland development and irrigation schemes and the improvement ofinfrastructure. Direct lending for agricultural and rural developmentprojects began in the mid-1960s. Since then there has been a slowbut steady evolution in Bank policy toward financing the incrementalproduction of primary prDducts.

Until recently, Bank lending policies toward the production ofprimary commodities were guided largely by the demand outlook:that is, the expected capacity of world markets to absorb additicnalsupplies at remunerative prices. Staff studies assessed the imarketoutlook for individual commodities, highlighting products facingencouraging market prospects and those in potential difficulty. Oneof the earliest examples is a 1958 Bank report on "The CoffeeProblem," by Dragoslav Avramovic, which pointed out, among otherthings, that heavy surpluses and sharply declining prices lay aheadfor the world coffee economy. Although no formal policy concern-ing Bank lending for commodities in oversupply was formulated,the effect of the report was to forestall further investment by theBank in coffee, either direct]y or indirectly.

The first formal policy action pertaining to a commodity insurplus supply was taken in 1961. Although the product to which itrelated was sugar, it would have been applicable equally to, otherproducts in a similar state of market. At that time the Bank'sexecutive directors agreed to impose restrictions on lending forsugar, which was then in a state of persistent oversupply." Hence-

11. See Lester B. Pearson and others, Partners in Development, Report of theCommission on International I)evelopment (New York: Praeger, 1969).

Synthesis and Background 15

forth, the Bank was to lend for the expansion of sugar productiononly to net importing countries in which additional output wasjustified by existing domestic demand and in which prices at thefactory compared favorably with those in other sugar importingcountries.

The formulation of a systematic policy toward Bank financing ofprimary commodities has its roots in the recommendations of thePearson Commission Report"2 and in a set of policy guidelinesadopted by the Bank in 1969, following a joint study by the Bankand the International Monetary Fund (IMF) on the stabilization ofprices of primary products.' 3 The executive directors of the Bankdecided, among other things, that "the World Bank Group will seekto intensify its efforts to promote diversification of production on aneconomic basis, giving special consideration to diversification projectswhich help restrain or reduce overproduction of primary products."Subsequently, the Bank entered into consultative arrangements withestablished international commodity bodies to ascertain their viewson the market effect of Bank-financed projects and the advisabilityof proceeding with proposed investments to increase production.The Bank agreed that it would not normally proceed with a projectif the international commodity body concerned advised against it.

In 1973 the Bank adopted a far-reaching policy limiting furtherinvestment to increase production of such primary commodities ascoffee, tea, and cocoa that faced inelastic demand. Thus, as a generalrule the Bank is not prepared to undertake further investments thatwould increase the output of these commodities.

This policy was applied almost immediately in the case of tea. Intea, there was a tendency toward persistent disequilibrium betweenproduction and consumption, reflected in either a chronic accumula-tion of stocks or a chronic underuse of productive capacity. Marketanalysis showed that any further investment in tea would onlycontribute to the chronic oversupply problem, and thus aggragatethe plight of tea exporting countries. Of course, the criterion thatweighs most heavily in any decision concerning the financing ofproduction expansion is the market outlook for the product, includ-ing the prospect for increasing the total export earnings that can bederived from it. It is on this ground that the Bank continues to lend

12. Ibid.13. International Monetary Fund and World Bank, The Problem of Stabilization of

Prices of Primary Products, parts I and II (Washington. D.C., 1969).

16 COFFEE, TEA, AND COCOA

for the expansion of cocoa production in several countries, as isdiscussed below.

For some countries, exDorts of coffee, tea, and cocoa neverthelessoffer the best-and somietimes the sole-opportunity to increaseincome. In such cases, the Bank is prepared to make exceptions tothe rule, after carefully balancing their needs against those of other(often larger and better established) exporters, whose earnings rnaybe threatened by an increase in supply from other sources.

The Bank is also prepared to make exceptions when the long-termmarket prospects for a commodity are favorable or where aninternational agreement is in force. In the latter case, it is preparedto consider financing increased production within global limits ornational quotas set under the agreement, after consultation with thebody in question.

The Bank recognizes that, for countries that are highly dependenton exports of primary commodities facing inelastic demand, devel-opment policies may be more critical to the growth of exportearnings than trade pol..cies, which are the principal concern ofseveral international organizations. This is because developmentpolicies directly affect their capacity to make the structural changesnecessary for the diversification of production and exports. But theextent to which the Bank (and other international organizations) canhope to increase the export opportunities of countries with a strongcomparative advantage in production of coffee, cocoa, or tea byencouraging and financing diversification by other exporting coun-tries which may have lost such an advantage can be answered only asspecific situations arise.

Coffee-producing countries in the main are aware of the clangersof overproduction, and many are limiting production expansion. Asfor the World Bank, it int;ends, as a general rule, to limit lending forincreased output to countries with little opportunity to diversif.y theirsources of export earnings-and then only if the aggregate impacton world production levels, and hence on prices, is likely to beinsignificant. This policy takes account of the likelihood that addi-tional production would tend to lower international coffe prices, andthat resultant losses would not be compensated by a long-term rise indemand.

So far the Bank has financed only three projects to increase coffeeoutput: a rehabilitation program for Burundi in 1968 and twocombination cocoa and coffee projects, one in Togo in 1974 and onein Liberia in 1975. The secretariat of the International CoiffeeOrganization (ICO) was consulted on these projects. It supported the

Synthesis and Background 17

first on the ground that coffee production in Burundi had sufferedas a result of natural disaster and internal political difficulties. Itraised no objection to the other two projects because it was felt thatthe increments to world production would not be out of proportionto the anticipated rate of growth of demand for coffee.

In principle, the Bank is prepared to finance coffee rehabilitationprojects involving no increase in output. Such projects would includea reduction in coffee hectarage to offset productivity gains andprovide for diversification of released areas to other crops. TheBank is also willing to consider financing projects to improve qualityor to increase the value-added element of coffee exports: forexample, the development of coffee processing. A loan was made toEthiopia in 1972 for washing coffee and improving quality.

In 1970-73 the Bank committed about $22 million for develop-ment in cocoa projects or projects with cocoa components in fiveproducing countries: Ghana, Indonesia, the Ivory Coast, Malaysia,and Nigeria. So far, of course, the output from these projects isnegligible, but by 1980 it will be about 50,000 metric tons, and willincrease to more than 55,000 metric tons by 1985. These quantitieswill amount to about 2.8 percent of expected world production in1980 and 2.6 percent in 1985.14

In 1974-75 six additional cocoa undertakings were approved inCameroon, Ecuador, Ghana, Liberia, Nigeria, and Togo. The Bank'scommitment to these cocoa projects was about $67 million. Tenta-tively, it is estimated that by 1980 these projects will produce about27,000 metric tons, increasing to 83,000 metric tons or more by1985. These figures represent about 1.5 and 3.9 percent of esti-mated world production in 1980 and 1985, respectively. From allBank projects, the Bank's share in world cocoa production in 1980and 1985 would be on the order of more than 4.2 and 6.5 percent,respectively.

A significant proportion of the Bank projects involves rehabilita-tion and replanting in dilapidated cocoa areas. By 1985 more than40 percent of the combined output of projects under considerationwill be the result of rehabilitation and replanting. The projectedcontribution of Bank-financed cocoa projects to world supply hasbeen included in the mo-.e detailed forecasts presented later in thisbook.

Further investments to increase tea production in exportingcountries with small market shares might yield high returns in the

14. For statistics on World Bank lending for cocoa and tea, see appendix C.

18 COFFEE, TEA, AND COCOA

short run, but over the long term any significant increase inproduction capacity can have major ill effects on all tea exporters.Thus, as already explained, the Bank does not in general intend tofinance increased production of tea unless the market outlookimproves considerably. It is prepared, however, to make exceptionsin countries with no other opportunities for productive investment.It will also consider rehabilitation schemes to raise productivity,along with provisions for diversification out of tea and projects toincrease the value-added element of tea exports (such as thedomestic manufacture of tea bags and instant tea).

The impact of past Bar[k tea investments on the volume of worldsupply has been substantial. In 1964-73 the Bank financed eightprojects involving tea planiting, including some financed as part ofother activities such as agricultural credit schemes. Because teabushes mature slowly, output from these projects will build up onlygradually during the 1970s. By 1980 it is expected to reach about53,000 metric tons and by 1985, about 69,000 metric tons, or aboutthree percent of projectecl world output in 1980-85. Assuming that90 percent of the incremental output from the projects is exported,this would account for about 6 percent of projected total worldexports in 1980.

In certain countries thc share of tea output contributed by Bankprojects will be much greater than the 3 percent mentioned above.By 1980, Bank tea investments will have contributed roughly 22percent toward total output in Indonesia, 28 percent in Kenya, 34percent in Mauritius, 46 percent in Tanzania, and 10 percent inUganda.

The current policy reflects the interdependence of countries withrespect to their developrrent policies. It implies recognition on thepart of the Bank that, in is lending operations, it has a responsibilitythat goes beyond the interests of the individual borrowing country.

SUMMARY OF PROSPECT',: PRINCIPAL FINDINGS AND CONCLUSIONS

As regards broad policies affecting the financing of commloditiesfacing inelastic demand (as discussed above), Bank decisions tofinance suitable projects will probably continue to be guided by themarket outlook for the reiulting output. Market considerations haveweighed heavily in past lending decisions and undoubtedly willcontinue to do so. Therefore, these prospects are reviewed inchapters 2 (for coffee), 3 (for tea), and 4 (for cocoa). The analyticalframework and the methodology followed are different in each case,as conditions vary. The main findings of these chapters are included

Synthesis and Background 19

in the summary review below-with the caution that the forecastingof commodity prices is a continuing activity in the Bank, and paperson market outlook are updated periodically.

Coffee

In 1950-75 world coffee production grew at the rate of just under 3percent a year, but the growth was rather uneven. Few newplantings had taken place during the war years, when exports toEurope fell and prices were depressed. Following the postwarrecovery in demand, the sharp rise in prices attracted large-scaleinvestment into new plantings. For the I950s as a whole, productionexpanded by about 75 percent; ensuing surpluses were enormous,and by 1960 oversupply had become a critical problem, and pricesfell steeply. Production actually declined during the 1960s, althoughprincipally the result of the diversification policies pursued by Brazil.New plantings elsewhere remained generally at a standstill, underthe surveillence exercised by the International Coffee Agreement.Expansion during the 1970s has so far been restrained and outputsomewhat irregular.

The growth in world exports, although it matched productionover this quarter of a century, has been more orderly. The gapbetween these two growth patterns was bridged by stocks held in theproducing countries, principally in Brazil. Coffee stocks rose contin-uously until 1966. Since then, as production continuously fell belowconsumption, stocks were steadily drawn down, to immediate pipe-line requirements. Prices began to react slowly at, first and thensharply following the major frost damage of 1975 in Brazil.

In recent years the rate of growth in world consumption has beenslowing down. The income elasticity of demand has been decliningin the traditional markets, as coffee consumption has become subjectto definite saturation levels. In the United States per capita con-sumption has been declining since 1962 in spite of increasedincomes. Growth is slowing down also in Western Europe, thoughthe United Kingdom, where coffee threatens the position of tea as anational drink, is a notable exception. Consumption in Japan hasbeen rising sharply, and it could rise rapidly in the Soviet Union andEastern Europe if more foreign exchange were made available bythe authorities for coffee imports.

The future behavior of coffee production, consumption, stocks,and prices has been simulated from 1949 onwards through theeconometric model described in Appendix A, which yields forecastsup to 1985. The variables used to estimate supply by regions include

20 COFFEE, TEA, AND COCOA

past production, lagged real prices, the biennial production cycle forarabicas, and, for Brazil, ratio of stock changes to output, plantingprograms, and effects of fi-osts. Demand is projected as a function ofprices and income. The equations are specified in such a way as toyield price elasticities of demand that increase in t]he case ofexporting countries and the United States, and to yield incomeelasticities of demand that decrease with increasing incomes in theimporting countries. The price equation includes as its main variablethe supply-and-demand balance, the one-year lagged price, ancl avariable to capture the effect of inflation on real prices. Projectionsare made on different assumptions concerning the three exogenousvariables (as given or developed externally) in the model: incomes,inflation, and frosts.

The results indicate that although prices may recede somewhatfrom their present high levels in the near future, they are expectedto remain relatively high through 1978-79, after which they maydecline rapidly and reach low levels in the mid-1980s. The expecteddevelopment of production and stocks mirrors the expected devel-opment of prices: low production and stocks through 1978-79 a:ndrapidly increasing production and stocks thereafter, reaching a highin the mid-1980s. The growth in world demand, although somrewhatslower at first, will average 2 percent a year in 1975-85.

Tea

Most of the world output and exports of tea are accounted for by afew countries in South Asia and East Africa. In 1955-73 growth ofworld production averaged about 3.3 percent a year, ranging from alow of 1.3 percent a year for Sri Lanka to a high of nearly 10 percentfor East Africa (which had begun from a low base). During the sameperiod, the volume of world exports grew rather slowly, averagingless than 2 percent a year. A continuous state of surplus and ofdifficulty in storing tea for long periods of time led to a steadydecline in tea prices. The unit value of world exports fell from 45pence a kilogram to 36 pence over the period. The decline in realprices was even steeper.

In 1973 the developed countries accounted for about three-fifhisof world tea imports; the United Kingdom was the largest singlemarket, followed by the United States. The imports of these coun-tries grew at a dwindling r ate, averaging barely 0.5 percent a year in1955-73. In the United Kingdom absolute as well as per capitaconsumption fell, and dermand in the developed countries was not

Synthesis and Background 21

highly responsive to changes in either price or income. In thedeveloping countries, however, consumption as well as their importsexpanded rapidly, averaging 5.4 percent and 4.6 percent a year,respectively.

The methodology used in this study to forecast supply, demand,and prices is eclectic, comprising techniques and information se-lected from various sources. On the supply side, past trends inhectarage and yields were adjusted to take account of countryproduction targets and the likelihood of their achievement. Thedemand was estimated on the basis of existing per capita consump-tion and the effects of tastes and income changes, using availableinformation on price and income elasticities of demand.

The results indicate that expansion in world production of teaduring 1973-85 will slow down slightly, to 3 percent a year. Importdemand of the developed countries will remain sluggish, expandingat less than 1 percent a year. But, the import demand of thedeveloping countries-and consumption in the exporting countriesthemselves-will remain buoyant, as a result of which the overall rateof growth in world imports will rise from 2 percent a year in 1955-73 to nearly 3 percent in 1973-85 because the developing countries,with their faster growth, will acquire a larger share of the total tradein tea. By 1985 the volume of imports of the developing countrieswill nearly match that of the developed countries. Total worldconsumption of tea will by then be shared by the developed,developing, and centrally planned countries in a 25:50:25 ratio. Thereal price of tea will continue to decline, but the fall will not be assteep as in the past.

Given the price elasticity of demand, a drop in the total volume oftea exports would improve its aggregate export earnings. A neces-sary condition for bringing this about is a market-sharing arrange-ment among the exporting countries. An important obstacle tonegotiating such an arrangement has been the divergence of viewsbetween the large, long-established producers and exporters and thecountries that have more recently become exporters. The former donot wish to recluce their export volumes, whereas the latter continueto add to the available in amounts larger than the market canhandle. Given the price elasticities of demand facing individualcountries, half of any increase in export volume of India or SriLanka would be offset by an associated price decline; for othercountries, the offset would be less than 10 percent. Therefore, itwould be of advantage to India and Sri Lanka to relinquishsystematically a share of the market to smaller exporters-provided,

22 COFFEE, TEA, AND COCOA

of course, the latter so restrain their expansion that total volume ofworld exports is consistent with the price objective.

Cocoa

Cocoa is exported almost entirely to the developed and the centrallyplanned countries; the latter's share of the market averaged about 14percent in 1970-75. Cocoa is exported chiefly in the form of beans,although exports of processed products have been gradually risinlg,amounting to 17 percent (in bean equivalent) of exports in 1973.Cocoa stocks are held almost entirely in importing countries.

The volume of exports expanded at 2.3 percent a year during the1950s, but there was little gain in the value of exports, since pricesweakened. The volume and value grew at 3.6 and 3.3 percent a year,respectively, during the 1960s, although prices remained weak in thefirst half of the 1960s and reached their lowest level in 1965, theyimproved considerably in the second half of the decade. Growth inthe value of exports in the 1970s has so far been a remarkable 8percent a year, with volume actually contracting as a consequence ofshort supplies-illustrating how value and price move in the sa:medirection while volume and value move in the opposite.

World consumption of cocoa grew at 4.1 percent a year during1955-73. Expansion was slower in the late 1960s and early 1970s asproduction fell following the very low price of 1960-65. In 1973--76there was an actual decline in consumption because of scarcity ofsupplies and relatively high.i prices.

The export outlook fDr cocoa is examined here within theframework of a market-clearing model. Production in the principalcountries was forecast on the basis of expert knowledge of cocoapolicies and of plans being executed in those countries. For minorproducers, FAO projections for 1980 were used and extrapolated to1985. The results showed that world production will tend to rise atabout 2.6 percent a year iri the 1970s and 3 percent in 1980-85, butcould be higher if cocoa-producing countries compete excessively inexpanding their output. Demand forecasts were made using theFAO model, which works under a variety of price assumptions anduses real income and real price among the variables. Equilibratingsupply and demand, the rnodel yields a real price (in 1973 constantterms) of 43 U.S. cents a pound in 1980. The forecast was tested withan alternative model; the results proved to be identical. At theseprices, consumption is forecast to expand at about 3 percent a yearin 1976-85.

Synthesis and Background 23

In connection with the financing of additional output of acommodity, a variety of issues arise concerning the selection ofprojects. One of these issues pertains to the comparative advantagein the production of a product enjoyed by one country as comparedwith another. In order to examine this problem, an experimentalempirical study on cocoa was undertaken by the World Bank staff.Various methods, including the Domestic Resource cost approach,were examined-as summarized in appendix B. The results con-cerning the relative comparative advantage of countries were incon-clusive and not of direct operational significance.

2

THE WO RLD COFFEE MARKETr

COFFEE IS A TREE CROP. The first harvest comes in aboutthree to four years after planting, and it takes two more years beforethe tree reaches its normal yield. Yields normally start to declineabout fifteen years after planting, but under good management thedrop in production is not rapid, and the tree can have an economiclife of up to fifty years. In rnost countries, however, the managementof coffee holdings is poor and trees have to be replaced after twentyto thirty years.

There are two main types of coffee: arabicas and robustas.Robustas can be grown in hot and humid climates. Arabicas requirelower temperatures and are therefore grown either at higheraltitudes or farther from the equator than robustas. Coffee is heavilydamaged, however, when temperatures fall below freezing, and thiislimits the area where it can be grown. There are also two other typesof coffee, liberica and excelsa, both of which are grown in WesternAfrica, but they account fcr less than half of one percent of worldproduction and exports.

Arabica coffees are divided into washed, or mild, arabicas andunwashed arabicas. If the coffee cherry is dried and then depulpedto free the coffee beans, the coffee is classified as unwashed. I[f thecherries are depulped immediately and the beans then placed inwater to facilitate later rermoval of the mucilage, the coffee is calledwashed. The washed, or mild, coffees are further divided into"Colombian milds" and "other milds," but this distinction is of littlerelevance from a technical point of view.' There are no comparableclassifications among the rcbustas.

1. Until 1966 under the International Coffee Agreement, only nmild arabicas,unwashed arabicas, and robustas were distinguished.

24

The World Coffee Market 25

Arabica coffees are generally preferred by consumers. They havea milder flavor and contain less caffeine than robustas. The tree ismore susceptible to diseases, however, and gives lower yields. Ara-bica coffee also gives a lower yield of instant coffee per pound ofbeans. The steady increase in the consumption of instant relative toregular coffee, therefore, has improved the position of robustas inthe world market and may explain in part the decline of the pricepremium of arabicas over the past decade.

The share of robusta coffee in total world production has in-creased steadily, from slightly more than 10 percent shortly afterWorld War II to more than 30 percent, and the share of arabicas hasbeen correspondingly reduced. Initially, the expansion of robustacoffee production was accompanied by low prices: until the mid-1960s New York spot prices of robusta coffees were from 20 to 40percent below those of coffees in the "other mild" group.2 Since thenthis gap has narrowed considerably, to the extent that in 1975 thespot prices of robustas at times exceeded those of the other milds.This development has been caused both by the increased consump-tion of instant coffee and by the growing tendency of coffee roastersto sell on the basis of brand names, with no indication of the type ofcoffee used in the blend.3 The latter practice enables the roaster tochange the coffee mix used in his blend in response to changes inthe relative prices of the various types and has thus greatly increasedthe cross-price elasticity between the different types of coffee.

The ease with which coffee can be stored is evident from thehistory of the world market: large stocks have been a fairly persistentfeature, especially in the 1960s, and in 1966 total producer stocksreached a peak of almost 90 million bags, equal to nearly two yearsof world import demand. In general, coffee can be stored for two tothree years with only a marginal deterioration in quality. Only in hotand humid climates are air-conditioned warehouses required forstorage. Storage for five years or more has been practiced, notably inBrazil, but coffee held for such long periods has always beendiverted to the domestic market, with the more recent growths beingused for exports.

The technical aspects of the conversion of coffee beans into coffeeas a beverage are fairly simple: the green beans are roasted, ground,

2. Spot prices are for immediate delivery from the warehouse in the marketindicated, in this case New York.

3. This practice is especially prominent in the United States. In Europe there isstill a definite premium for higher-quality coffees.

26 COFFEE, TEA, AND COCOA

and the soluble parts are then extracted with hot water. The resultcan either be consumed directly or it can be resolidified by evapora-ting or freezing the water, yielding soluble coffee.

Soluble coffee was first sold in the United States in 1951 and hasbeen consumed in increasing quantities ever since. Its share in themarket, which depends to a large extent on local tastes and habits, isabout 17 percent in the United States and 80 percent in the UnitedKingdom, but only about 5 percent in the Scandinavian countries.The share of soluble coffee in the retail market tends to be largest incountries where the popularity of coffee as a beverage is only arecent phenomenon.

The existence of soluble coffee causes statistical problems on boththe consumption and the production side. As a general rule, onepound of soluble coffee is taken to be the equivalent of three poundsof green coffee beans. From the point of view of consumption, thisratio is too low: one pound of soluble coffee yields up to 50 percentmore cups of coffee than can be extracted by the consumer from theequivalent amount of roasted coffee beans.4 This means thiat,although the rise of solub:le coffee may have increased the numberof cups of coffee consumed, it has not necessarily increased theconsumption of coffee beans. From the point of view of productionthe ratio of three to one is too high: many manufacturers of solulblecoffee manage to use only 2.5 pounds of green beans in making onepound of soluble coffee.5

Coffee is traded and soll to consumers in all stages of processing:as green beans, roasted coffee, ground coffee, and soluble coffee.Roasted and ground coffee, however, are not generally exported bydeveloping countries. All ;rade and consumption statistics are con-verted into "green bean equivalents" according to ratios establishedby the International Coffee Organization. One pound of roasted orground coffee is equivalent to 1.19 pounds of green beans, and onepound of soluble coffee is equivalent to three pounds of greenbeans. Slightly different conversion ratios are used for U.S. con-sumption statistics.

4. One pound of roasted coffee is equivalent to 1.19 pounds of green coffee.Therefore, one pound of soluble is equivalent to 2.52 pounds of roasted cof fee.

5. The amount of coffee used can be estimated by dividing the amount ofcaffeine found in the soluble co:Tfee by the amount of caffeine per pound of greenbeans, since all caffeine contained is removed.

The World Coffee Market 27

PRODUCTION AND EXPORTS

Although coffee is indigenous to Africa and reached Latin Americaonly by way of Asia, Latin America has been the dominant coffeeproducer for the last 100 years. Its share slowly declined during thefirst half of this century, but around 1950 it still accounted for 85percent of world production. Since then its share has been decliningmore rapidly. Latin America now accounts for 60 percent of worldproduction, Africa for 30 percent, and Asia and Oceania for theremaining 10 percent (see table 2).

Most coffees grown in both South and North America arearabicas; only Trinidad and Tobago produce exclusively robustacoffee. Robusta is also grown in the valleys of the state of EspiritoSanto in Brazil, but its production is still insignificant. Africaproduces both robustas and arabicas, but robustas account for by farthe larger share, about 70 percent. Arabicas are grown in Kenya,Ethiopia, Rwanda, and Burundi. Several African countries growboth types of coffee, but only Tanzania produces more arabicas thanrobustas. In Asia and Oceania as well, more robustas than arabicasare produced. Indonesia, the area's largest producer, grows almostexclusively robusta coffee. The production of arabicas is concen-trated in India and Papua New Guinea, which also produce robustacoffees.

In the distribution of world coffee production by countries (seetable 2), Brazil clearly dominates the scene. The importance of Brazilin this respect is illustrated by the fact that, in some of the yearsbefore World War II, a single Brazilian state, Sao Paulo, producedup to 90 percent of world coffee requirements. After the war Brazil'sshare in total world production has declined markedly; the countryas a whole now accounts for less than 30 percent of world produc-tion. Brazil is followed by Colombia, with a little more than 10percent of world production, and then by a long list of smallerproducers, among the largest of which are Angola and the IvoryCoast, each with a share of from 5 to 6 percent.

Most producing countries export virtually all of the coffee theygrow. A few, however, such as Brazil, India, and Mexico, consume asubstantial share of their own production, and all Philippine coffee isconsumed domestically. Thus, there is some divergence betweencountry shares in total production and in exportable production, thelatter being defined as total production minus domestic consump-tion. For example, the share of Brazil in exportable production over

Table 2. Type of Coffee Grown, Share in World Production, Growth Rate, and Share of Coffeein Export Earnings: Coffee-Producing Countries

Production" and shares Share ofAnnual coffee in

1948-52 1958-62 1968-72 growth ratec export

1947-48 to receipts"Thoufabds Thousands 7housands 1972-73 1970-72

Producing country Type of co]jeea of bags Percent of bags Percent of bags Percent (percent) (percent)

World total 38,591 100.0 70,370 100.0 65,454 100.0 2.87 4.95

Arabicas0 .33,696 87.3 56,860 80.8 45,801 70.0 1.7 9.9NO Robustas0 4,895 12.7 13,510 19.2 19,653 30.0 7.2 2.100

South America 26,139 67.7 44,237 62.9 28,309 43.3 0.8 11.7Brazil Unwashed arabica 19,486 50.5 34,250 48.7 17,275 26.4 -0.0 27.7Colombia Colombian mild arabica 5,593 14.5 7,783 11.1 7,904 12.1 1.6 58.8Ecuador Other mild arabica 299 0.8 735 1.0 1,048 1.6 6.4 8.5Peru Other mild arabica 102 0.3 568 0.8 980 1.5 11.7 4.4Venezuela Other mild arabica 625 1.6 829 1.2 926 1.4 1.2 0.4

North and Central 6,262 16.2 9,501 13.5 12,101 18.5 3.3 7.2America and Caribbean

Costa Rica Other mild arabica 368 1.0 1,062 1.5 1,320 2.0 6.2 28.9Dominican Republic Other mild arabica 387 1.0 546 0.8 677 1.0 2.7 8.5El Salvador Other mild arabica 1,216 3.2 1,613 2.3 2,332 3.6 3.3 16.8Guatemala Other mild arabica 1,103 2.9 1,600 2.3 1,908 2.9 3.0 33.7Haiti Other mild arabica 614 1.6 572 0.8 529 0.8 -0.9 43.2Honiduras Other mild arabica 174 0.4 332 ().5 605 0.9 6.4 14.7

Mexico Other mild arabica 1,158 3.0 2,117 3.0 3,231 4.9 5.4 4.9Nicaragua Other mild arabica 336 0.9 436 0.6 625 1.0 3.4 15.5

Western Hemispheretotal 32,401 84.0 53,738 76.4 40,410 61.7 1.4 10.2

Ajiica 4,732 12.3 13,140 18.7 19,758 30.2 7.2 6.1Angola Robusta 749 1.9 2,382 3.4 3,346 5.1 7.8 31.4Ethiopia Unwashed arabica 968 2.5 2,977 4.2 4,676 7.1 6.2 29.5Ivory Coast, Togo, Robusta 521 1.3 1,258 1.8 2,100 3.2 6.8 53.3

and Guinca'Kenya Colombian mild arabica 175 0.5 513 0.7 974 1.5 8.5 26.6Madagascar Robusta 547 1.4 873 1.2 1,040 1.6 3.1 26.3Tanzania Colombian nlild arabica 258 0.7 443 0.6 855 1.3 6.1 16.1Uganda Robusta 609 1.6 1,982 2.8 3,065 4.7 8.2 58.8Za'ire Robusta 536 1.4 1,089 1.5 1,248 1.9 3.4 5.8

Asia 1,459 3.8 3,491 5.0 5,285 8.1 7.0 .5India Other mild arabica 341 0.9 908 1.3 1,462 2.2 7.0 1.9Indonesia Robusta 822 2.1 1,730 2.5 2,288 3.5 6.5 5.2

a. Classifications of the International Coffee Organization.b. Weighted averatge over five years with wveights of 1, 3, 4, 3, 1 respectively.c. Determined by regressing the logarithm of production on time.d. Developing countries only.e. Arabica producers are those in Latin America plus Keniya, Tanzania, Ethiopia, and India. Some minor producers are excluded because of the unavailability oif

data. Robusta producers are taken to be all other countries.f. More than 90 percent of production in the Ivory Coast.Sources: Production data, U.S. Department of Agriculture; shares of coffee itl export receipts, World Bank data.

30 COFFEE, TEA, AND COCOA

the last few years was only 20 percent, as compared with a share intotal production of slightily less than 30 percent. Mexico, which isfirst among Central American countries as a coffee producer, ranksthird as an exporter.

If coffee could not be stored for relatively long periods, acountry's share in world cxportable production would give a directclue to its share in the wsrld export market. When stocks can beaccumulated or drawn down, however, a country's exports candeviate markedly from its exportable production. This has beenparticularly relevant in the case of Brazil. In the early 1960s Braziltried to stem the downward pressure on prices by storing part of itsexportable production, and in the years after 1966, when itsproduction had fallen drastically, it drew upon these stocks to keepits exports from declining. Thus, up to 1973, Brazil was able tomaintain a 30 percent share in the world export market despite itsmuch smaller share in world exportable production. The shares ofmost other countries roughly correspond to their shares in totalproduction.

World production has grown at an average rate of 3 percent ayear in the postwar period, but the rate of growth has been uneven.Until the mid-1950s, except for the recovery that naturally followedthe low level of production during World War II, there was hardlyany growth in coffee production. Demand recovered more rapidly inthis period, however, and a shortage of coffee was the unavoidableconsequence. Prices increased to record highs in 1954, with one lotof Colombian coffee selling at an all-time high of $1 a pound. Thissituation triggered an expansion of coffee production around theglobe. Output increased from about 40 million bags in 1950-54 toabout 70 million bags at the end of the decade. The ensuing surpluswas enormous; it depressed the growth of production to such anextent that the 1959-60 harvest of 79 million bags has since beenexceeded only once.6

The decline in production during the 1960s was due exclusively toBrazilian coffee policy. From 1962 to 1967, out of a total stock of 4.1thousand million coffee trees in 1962, an estimated 1.7 thousarndmillion were eradicated, most of them (about 1.4 thousand million)in response to government subsidies.

6. In 1965-66, when the Brazilian crop recovered sharply after frost damagedthe crop of the preceeding year, and world production reached an all-time high of82 million bags. The next largest crop in the period after 1959-60 was in 1974-75:about 78 million bags.

The World Coffee Market 31

Table 3. Price Elasticities of Coffee Supply, by Region

Elasticity of supply with respect to pice'

Short term Long termh' Long termb

Region or country (lag ] year) (lag 7 years) (full adaptation)

Brazil 0.20 0.44 0.66Colombia 0.03 0.18 0.40Other South America 0.06 0.46 10.70North and Central America

and Caribbean 0.03 0.14 0.77Africa 0.12 0.44 1.87Asia 0.10 0.43 3.01

a. For the derivation of these elasticities, see Jos de Vries, "Structur-e and Prospects of theWorld Coffee Economy," Staff Working Paper 208 (Washington, D.C.: World Bank, 1975).Figures in the three columns give the percentage increase or decrease in production resultingfrom a I percent increase or decrease in price after one year, seven years, and a theoreticallyinfinite number of years respectively. Dunng these periods of time, the price is assumed toremain at its increased level.

b. References in the text to long-term elasticities are exclusively to those shown in thesecond column. The values in the third column are derived by dividing those in the secondcolumn by the complement of the coefficient of lagged production. Although it is these valuesthat are normally regarded as the true long-term elasticities, they are of no relevance in thiscontext because the lags involved are much too long. Their size, insofar as it is determined bvthe complement of the coeffident of lagged production, indicates only the extent to whichthere has been a noticeable slowdown in the propensity of coffee production to grow inresponse to a given price level. Not surprisingly, this slowdown is strongest in countries thatalready have large areas under coffee and therefore face increasing marginal costs ofproduction in the expansion process.

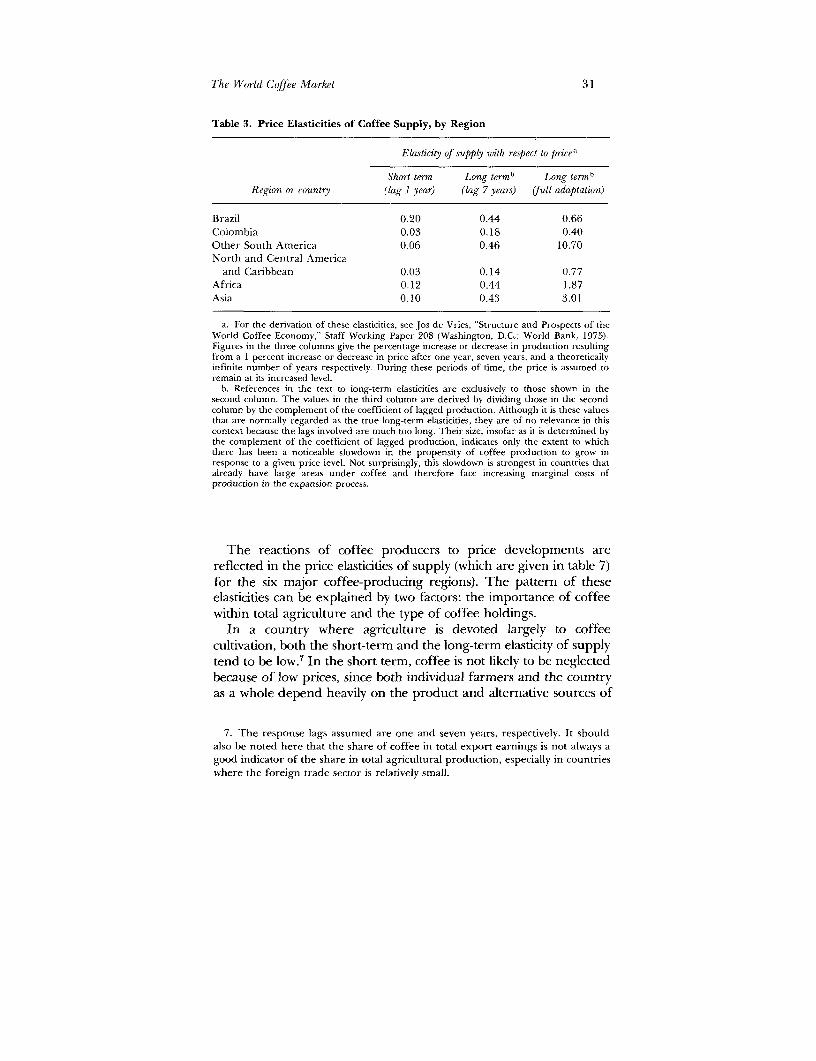

The reactions of coffee producers to price developments arereflected in the price elasticities of supply (which are given in table 7)for the six major coffee-producing regions). The pattern of theseelasticities can be explained by two factors: the importance of coffeewithin total agriculture and the type of coffee holdings.

In a country where agriculture is devoted largely to coffeecultivation, both the short-term and the long-term elasticity of supplytend to be low.7 In the short term, coffee is not likely to be neglectedbecause of low prices, since both individual farmers and the countryas a whole depend heavily on the product and alternative sources of

7. The response lags assumed are one and seven years, respectively. It shouldalso be noted here that the share of coffee in total export earnings is not always agood indicator of the share in total agricultural production, especially in countrieswhere the foreign trade sector is relatively small.

32 COFFEE, TEA, AND COCOA

income are few. In the long run, since a large portion of agriculturalland is already occupied by coffee, the possibilities for expansion arerelatively limited.