pt bumi resources minerals tbk. - nomura · pdf filethis presentation has been prepared by pt...

TRANSCRIPT

SG

00

0U

M7

_A

P_

08

10

PT Bumi Resources Minerals Tbk.Q1 Year 2011 Corporate Results & Updates

June 2011

SG

00

0U

M7

_A

P_

08

10

1

This presentation has been prepared by PT Bumi Resources Minerals Tbk (the “Company”) and is only for the informationof its investors. None of the information appearing in this presentation may be distributed to the press or other media orreproduced or redistributed in the whole or in part in any form at any time. This presentation is not intended as or formspart of any offer to sell or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities, andneither this presentation nor anything contained herein shall form the basis of or be relied on in connection with anycontract or commitment whatsoever.

This presentation may contain forward-looking statements and estimates with respect to the future operations andperformance of the Company and its affiliates. Investors and security holders are cautioned that forward-lookingstatements are subject to various assumptions, risks and uncertainties, many of which are difficult to predict and aregenerally beyond the control of the Company. Such assumptions, risks and uncertainties could cause actual results anddevelopments to differ materially from those expressed in or implied by the forward-looking statements.

Accordingly, no representation or warranty, either expressed or implied, is provided in relation to the accuracy,completeness or reliability of the information contained in this presentation, nor is it intended to be a complete statement orsummary of the resources markets or developments referred to in this presentation. It should not be regarded by recipientsas a substitute for the exercise of their own judgment.

Neither the Company or any other person assumes responsibility for the accuracy, reliability and completeness of theforward-looking statements contained in this presentation. The forward-looking statements are made only as of the date ofthis presentation. The Company is under no duty to update any of the forward-looking statements after this date toconform such statements to actual results or developments or to reflect the occurrence of anticipated results or otherwise.

Any opinions expressed in this presentation are subject to change without notice and may differ or be contrary to opinionsexpressed by other business areas or groups of the Company as a result of using different assumptions and criterion.

Confidentiality Notice

SG

00

0U

M7

_A

P_

08

10

2

Agenda

Asset Summary

IPO Completion & Financial Highlights

Company Highlights

Industry Outlook

Latest Corporate Achievements

1

2

3

4

5

SG

00

0U

M7

_A

P_

08

10

3

Company Highlights

SG

00

0U

M7

_A

P_

08

10

4

BRM Corporate StructurePost IPO & MCN Conversion

Calipso InvestmentPte. Ltd.

(“Calipso”)

International Minerals

Company LLC (“IMC”)

LemingtonInvestments Pte Ltd

(“Lemington”)

PT Citra PaluMinerals

(“Citra Palu”)PT Multi Capital

Bumi Holding S.A.S.Konblo Bumi Inc.(Liberia Project)

Bumi Mauritania SA

PT Gorontalo Minerals

(“Gorontalo”)

Herald ResourcesLtd

(“Herald”)

Gain and Win Pte Ltd

PT Dairi Prima Mineral(“Dairi”)

PT Multi Daerah Bersaing(“MDB”)

PT Newmont Nusa Tenggara

(“PT NNT”)

PT Bumi Resources Tbk

PT Bumi Resources Minerals Tbk

87%

96.97%100% 99.99%99.99%99.99%

60% 94.1%(2)80% (1)100%

100%

80%

75%

24% 99%

(1) Subject to progressive divestment to 49.0 % beginning from the end of the fifth year after commencement of production at the Gorontalo project(2) Subject to dilution to 80.0%

Bumi Resources Japan Company

Limited

100%

Investment Holding Companies

Operating/ Developing Companies

Legend

Marketing service company

Public

13%

SG

00

0U

M7

_A

P_

08

10

55

AFRICAINDONESIA

Stake: 80% (1)

Type: Copper & Gold.Mineral Inventory (100%): 125 mio tonGrade: 0.55 g/tonne Au, 0.75 Cu.Production: 2H 2014.

Stake: 94.1% (2)

Type: Diamonds, precious metals.Exploration stage with 7 exploration leases obtained.

Stake: 18%Type: Copper & Gold.Reserve (100%): 7.7 bio lbs copper & 7.6 mio oz gold (3)

Grade: 0.6% Cu, 0.5 g/t Au (Phase 6)Q1 2011 Prod: 88 Mio lbs copper & 96 thd oz gold.

World Class Asset Portfolio

Source: BRM.

Stake: 96.97% Type: Gold, Moly.Mineral Inventory (100%): 2.5 mio ton (gold), 106 mio ton(moly).Grade: 7.5 g/ton Au, 0.14% Moly.Production: 2H 2014.

(1) Subject to progressive divestment 49.0% beginning from the end of the fifth year after commencement of production at the Gorontalo Project.

(2) Subject to dilution to 80.0%(3) As of 31 December 2010.

Bumi Mauritania

Konblo Bumi (Liberia)

Stake: 80%.Type: Zinc, leadReserve (100%): 5.4 mio ton ore (Anjing Hitam).Resource (100%): 20.1 mio ton ore (Anjing hitam, Base Camp, Lae Jahe).Grade: 13.7% Zn, 8.2% Pb.Production: 2013.

Dairi Prima Minerals

Newmont Nusa Tenggara

Gorontalo Minerals Citra Palu Minerals

Stake: 60%.Type: Iron ore.Mineral Inventory (100%): 100 mio ton.Grade: 60% Fe.Production: 2012.

SG

00

0U

M7

_A

P_

08

10

6

The first phase focuses on the extension of existing mine life and development of existing reserves and mineral

inventory

− Batu Hijau Phase 6 pushback has commenced

− Dairi mine expected to commence production and ramp up to 1 million tonnes per annum of production in 2013(1)

− Complete feasibility studies for Gorontalo and Citra Palu

− Development activities in Mauritania

− Exploration in Liberia

The second phase focuses on the exploration and development of existing discoveries

The first immediate priority of BRM management is to focus on core asset development and commercializing its portfolio of mining assets

FIRST PHASE SECOND PHASE

Portfolio of Assets Across Various Stages of the Development Cycle

Source: BRM.(1): The company has received the requisite licence to conduct exploration activities at Dairi on 23 October 2010, and the exploitation license is pending approval.

Exploration

P

rodu

ction Asset 2010 2011 2012 2013 2014 2015

NNT (Batu Hijau) Production

Mauritania Development DSO Production Production

Dairi (Anjing Hitam) Development Production

Gorontalo Feasibility Studies Development Production

Citra Palu Feasibility Studies Development Production

Konblo Bumi (Liberia) Exploration and development activities

SG

00

0U

M7

_A

P_

08

10

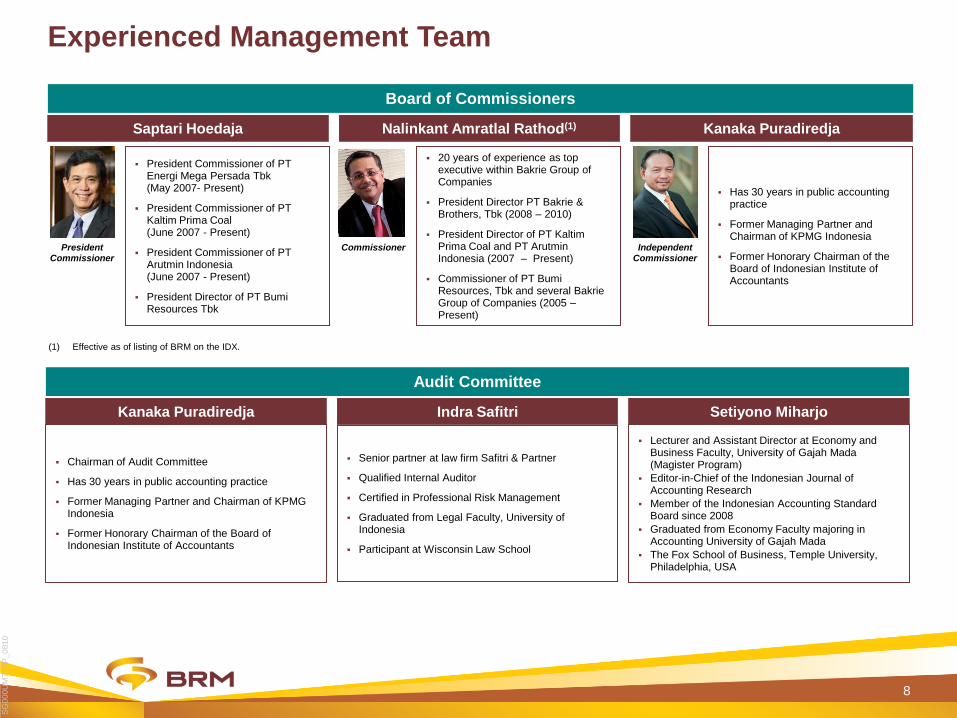

Experienced Management Team

7

Director of PT Bumi Resources Tbk since 2004 and

Chairman of Herald Resources

Commissioner of PT Kaltim Prima Coal and PT Arutmin

Indonesia since 2001

21 years work experience in mining sector from BHP

Billiton

Kenneth Patrick Farrell

President Director

Currently Chief Executive Officer of PT Kaltim Prima

Coal

Has held several senior positions in PT Bumi Resources

Extensive experience in mining operations, project

development and operations management

Endang Ruchijat

Director

Finance Director of Bakrie Energy International Pte. Ltd.

Previously Finance Director of PT Bakrie & Brothers Tbk

(2004 – 2009)

Previously Head of Corporate Banking, Bank Credit

Lyonnais, Indonesia (1995 – 2002)

Member of the Indonesia Stock Exchange (IDX) Listing

Committee

Yuanita Rohali

Director

Appointed as Unaffiliated Director

Previously Corporate Finance Director of PT Capitalinc

Investment (July 2009 – June 2010),

Assistant Vice President in Corporate Finance Division of

PT Recapital Securities

Febriansyah Marzuki

Director

Senior Management

Chief Executive Officer of Herald Resources and Dairi Prima Minerals

Managing Director of Kaltim Prima Coal with PT Bumi Resources (2003 – 2006)

Over 20 years experience in mining sector from Rio Tinto and Western Mining Corp.

Evan Ball

Head of Investor

Relations

Over 7 years experience in finance and Investor Relations within upstream oil & gas industries

Corporate Banker with ABN Amro (Global Corporate Group) and Citibank (Financial Institutions & Public Sector) (1998 – 2003)

Herwin Wahyu Hidayat

Corporate Secretary / Chief Legal

Officer

Expert in Indonesian mining law

Director of PT Multi Daerah Bersaing (owner of 24% stake in Newmont Nusa Tenggara Copper & Gold project)

Senior Legal Officer of PT Arutmin Indonesia for 5 years

Mohammad Sulthon

Board of Directors

CEO Dairi Prima Minerals

SG

00

0U

M7

_A

P_

08

10

8

Board of Commissioners

President Commissioner

President Commissioner of PT Energi Mega Persada Tbk (May 2007- Present)

President Commissioner of PT Kaltim Prima Coal (June 2007 - Present)

President Commissioner of PT Arutmin Indonesia (June 2007 - Present)

President Director of PT Bumi Resources Tbk

Saptari Hoedaja

Commissioner

20 years of experience as top executive within Bakrie Group of Companies

President Director PT Bakrie & Brothers, Tbk (2008 – 2010)

President Director of PT Kaltim Prima Coal and PT Arutmin Indonesia (2007 – Present)

Commissioner of PT Bumi Resources, Tbk and several Bakrie Group of Companies (2005 –Present)

Nalinkant Amratlal Rathod(1)

Independent Commissioner

Has 30 years in public accounting practice

Former Managing Partner and Chairman of KPMG Indonesia

Former Honorary Chairman of the Board of Indonesian Institute of Accountants

Kanaka Puradiredja

(1) Effective as of listing of BRM on the IDX.

Audit Committee

Senior partner at law firm Safitri & Partner

Qualified Internal Auditor

Certified in Professional Risk Management

Graduated from Legal Faculty, University of Indonesia

Participant at Wisconsin Law School

Indra Safitri

Lecturer and Assistant Director at Economy and Business Faculty, University of Gajah Mada (Magister Program)

Editor-in-Chief of the Indonesian Journal of Accounting Research

Member of the Indonesian Accounting Standard Board since 2008

Graduated from Economy Faculty majoring in Accounting University of Gajah Mada

The Fox School of Business, Temple University, Philadelphia, USA

Setiyono Miharjo

Chairman of Audit Committee

Has 30 years in public accounting practice

Former Managing Partner and Chairman of KPMG Indonesia

Former Honorary Chairman of the Board of Indonesian Institute of Accountants

Kanaka Puradiredja

Experienced Management Team

SG

00

0U

M7

_A

P_

08

10

Asset Summary

SG

00

0U

M7

_A

P_

08

10

1010

Newmont Nusa Tenggara

Batu Hijau is a large scale open pit gold and copper

mine located in South-west Sumbawa, Indonesia

BRM currently owns 18%(1) effective interest in Batu

Hijau with the opportunity to acquire a further 7%

through PT Multi Daerah Bersaing in the near-term

One of only three mines in the world with total ore

tonnage in excess of 1 billion tonnes and gold

grades higher than 0.2g/t

Contract of Work signed with Indonesian

Government in 1986

One of the lowest cost gold or copper operations in

the world ($ 0.7/ lb copper ; $ 237/ oz gold)

Batu Hijau’s reserve of 7.7bn lbs of copper and

7.6mn oz of gold (Reserve life of 10 years for Gold

and 14 years for Copper based on 2010 production

rate)

Elang copper and gold deposit is estimated to be a

potentially larger resource than Batu Hijau

Elang exploration permit received: 27 Sep 2010 – 28

Feb 2030

Potential to extend Batu Hijau mine life through

conversion of resources

(1) BRM holds 75% of MDB which holds 24% of PT NNT.(2) Merukh Family’s interest effectively controlled by Newmont through loans made by Newmont.(3) Newmont and Sumitomo hold a 56% interest in PTNNT through the Nusa Tenggara

Partnership. Newmont is the operator.

CoW BlockProspect Location

Mine Operation

Batu HijauPinjam Pakai Area

Project AreaDrilling Programs

Alas Strait

SUMBAWA

BESAR

WEST SUMBAWA

Lunyuk

Ropang

Lemurung

Plampang

Labangka

V

VIIII

IV

Taliwang

Jereweh

Maluk

Benete Port

Alas

Utan

Langam

Pl.Tano

II

Buin batu

NORTH LUNYUK

TELUK PANAS

60 km

RINTI

BATU HIJAU ELANG RINTI

Source: Newmont

Producing Asset with Exploration UpsideBatu Hijau Gold Reserves Tonnage (Ore) Grade Contained Gold

2010 100% Equity Gold 100% Equity

(’000 tons) (oz/ton) (’000 oz) (’000 oz)

Proved 348,500 62,640 0.014 4,872 877

Probable 609,000 109,620 0.004 2,436 438

Proved and Probable 957,000 172,260 0.008 7,656 1,378

Batu Hijau Copper Reserves Tonnage (Ore) Grade Contained Copper

2010 100% Equity Copper 100% Equity

(’000 tons) (’000 tons) (%) (mm lbs) (mm lbs)

Proved 348,500 62,640 0.5% 3,584 645

Probable 609,000 109,620 0.35% 4,125 743

Proved and Probable 957,000 172,260 0.40% 7,709 1,388

SG

00

0U

M7

_A

P_

08

10

11

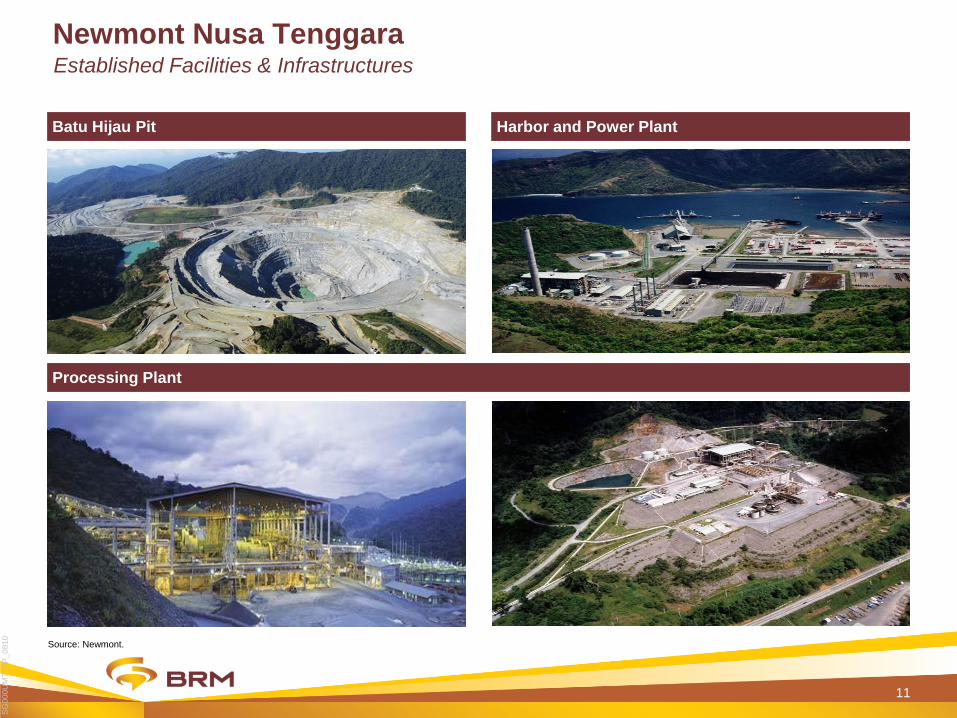

Batu Hijau Pit Harbor and Power Plant

Processing Plant

Source: Newmont.

Newmont Nusa TenggaraEstablished Facilities & Infrastructures

SG

00

0U

M7

_A

P_

08

10

12

Copper Production (On 100% Basis)(1)

Source: Newmont.(1) Note that BRM has 18% effective interest in PT NNT which was acquired in November 2009 and March 2010.

Gold Production (On 100% Basis)(1)

Newmont Nusa Tenggara• Temporary production drop in 2011 – 2012 due to phase 6 pushback. Phase 6 already commenced in 2010 and will complete in 2012• 2013 production rate is expected to be similar to peak performance in 2010

145

88

0

20

40

60

80

100

120

140

160

1Q 2010 1Q 2011Copper (mm lb)

Q1 2011

Copper Production (On 100% Basis)(1)

166

96

0

20

40

60

80

100

120

140

160

180

1Q 2010 1Q 2011

Gold (koz)

Q1 2010 Q1 2011

Gold Production (On 100% Basis)(1)

Q1 2010

SG

00

0U

M7

_A

P_

08

10

13

Copper Production Cost per Pound Sold (US$/lb)(3) Gold Production Cost per Ounce Sold (US$/oz)(3)

(US$ / Ib) (US$ / oz)Current spot price(2): US$4.41/lb Current spot price(2): US$1,419/oz

Copper Production Cost per Pound Sold (US$/lb)(2) Gold Production Cost per Ounce Sold (US$/oz)(2)

(US$ / Ib) (US$ / oz)Current spot price(1): US$4.27/lb Current spot price(1): US$1,437.8/oz

Depreciation & AmortizationCost Applicable to Production Depreciation & AmortizationCost Applicable to Production

Newmont Nusa TenggaraEfficient Copper & Gold Producer

Source: Newmont.(1) Bloomberg as at 31 March 2011(2) Newmont Mining Corp 10-K Annual Report Sec Filings

Q1 2010 Q1 2011 Q1 2010 Q1 2011

SG

00

0U

M7

_A

P_

08

10

14

2010A Cu Production

(million pounds)

Source: 31 Dec 2010 Xstrata Production Report, Freeport 10-K Form, BHP Production Report, OK Tedi Q4 Results, OZ Mineral Annual Report, Newmont Operating Stats

Batu Hijau is one of the largest producing copper and gold mines in the world with further upside from the potential development of the large scale Elang copper and gold deposit

Newmont Nusa TenggaraOne of the Top Producing Copper Mines in Asia Pacific

SG

00

0U

M7

_A

P_

08

10

15

Dairi is a very high grade zinc resource located in NorthSumatra and is proposed to be developed as anunderground mining operation

Strategic location with respect to smelters andshipping routes

Contract of Work signed with Indonesian Governmentin 1998, subject to a 30 year term from thecommencement of production

Obtained exploration borrow and use permit onOctober 11, 2010 to undertake exploration activities inthe protected forest area

Presidential Decree to allow underground mining withinprotected forest area is in place on 19 May 2011 (nextstep: exploitation borrow & use permit from Ministry ofForestry)

One of the highest grade zinc deposits in the world(Grades of 13.7% Zn, 8.2% Pb and 9.9 g/t Ag)

Low estimated net by-product cash cost of US$0.21/lb

Initial 7 year mine life based on 5.4 million tonnes of orereserves at Anjing Hitam which is expected to befollowed by production from the Lae Jehe deposit

Total Resources of 20.1 million tonnes (Anjing Hitam =8 mio tonnes, Lae Jahe = 11.3 mio tonnes, Base Camp =0.8 mio tonnes)

Source: BRM.

Dairi Prima MineralNear Term Producing asset with High Zinc Grade

Tonnage (Ore) Grade Contained Zinc

Anjing Hitam Zinc Reserves 100% Equity Zn 100% Equity

(’000 tonnes) % (mm lbs) (mm lbs)

Proved 4,400 3,500 13.9 1,354 1,083

Probable 1,000 800 12.7 293 235

Total zinc reserves 5,400 4,300 13.70 1,648 1,318

Tonnage (Ore) Grade Contained Lead

Anjing Hitam Lead Reserves 100% Equity Pb 100% Equity

(’000 tonnes) % (mm lbs) (mm lbs)

Proved 4,400 3,500 8.4 818 655

Probable 1,000 800 7.4 171 137

Total Lead reserves 5,400 4,300 8.20 989 791

SG

00

0U

M7

_A

P_

08

10

1616

Significant Zinc and Lead Reserves and Resources

Source: BRM, Mining Plus Pty Ltd and Herald Resources.

One of the Highest Zinc Grade Assets in the World

Source: AME estimates.

# of ProjectsGrade (% / g/t) Contained Metal (mm Ibs / oz)

Reserves

Tonnes

(000s) Zn Pb Ag Zn Pb Ag

Proven 4,400 13.9% 8.4% 10.0 1354.2 818.3 1.420

Probable 1,000 12.7% 7.4% 9.6 293.4 171.0 0.323

Total 5,400 13.7% 8.2% 9.9 1647.6 989.3 1.744

Resources

Measured 5,400 16.5% 10.2% 1,964.3 1,214.3

Indicated 9,700 11.7% 6.5% 2,502.0 1,390.0

Inferred 5,000 9.4% 5.3% 1,036.2 584.2

Total 20,100 12.5% 7.2% 5,502.5 3,188.5

Total zinc, lead and silver equity reserves and resources at the Anjing

Hitam prospect as of July 26, 2010 are set out in the table above.

Tonnages are rounded to the nearest 100,000.

Dairi

Dairi Prima MineralOne of the Higher Grade Zinc Projects in the World

SG

00

0U

M7

_A

P_

08

10

1717

Significant Life of Mine Production

Source: BRM, Mining Plus Pty Ltd and Herald Resources.

Source: AME estimates.

Estimated Global Zinc Cash Costs by Mine Site 2012

400.0 400.0

360.0 360.0

320.0 320.0

280.0 280.0

240.0 240.0

200.0 200.0

160.0 160.0

120.0 120.0

80.0 80.0

40.0 40.0

0.0 0.0

-400.0 -400.0

-300.0 -300.0

-200.0 -200.0

-100.0 -100.0

0.0 0.0

0 2000 4000 6000 8000 10000

Dairi

US¢/lb US¢/lb

Cumulative Production

Dairi Prima MineralSteady State Production Estimate

Life of MineTotal Ore Production (‘000s tonnes) 5,473

Total Zinc Metal Production (‘000s tonnes) 750

Total Lead Metal Production (‘000s tonnes) 450

Total Silver Production (‘000s oz.) 1,749

Mining Opex (US$/tonne) US$45.99

Processing Costs US$36.32

Overheads and Royalties US$21.40Total Cash Costs (US$/tonne) US$103.71Budgeted Capital Expenditure US$311mSteady State Production (‘000 tonnes p.a.) 115 (Zn); 60 (Pb)

SG

00

0U

M7

_A

P_

08

10

18

Overview

Location

Currently active in these two following areas:

− Tamagot region, south of the town of Akjoujt,

and 250 km North-East of the capital

Nouakchott

− S’fariat region, 250 km north of the town of

Zouerat in northern Mauritania

Potential for two producing operations

− Direct shipping ore from Tamagot region

(Drilling completed in Aug 2010, awaiting

chemical analysis results)

− Concentrate for pellet feed from S’fariat

region

Additional development opportunity recently

acquired through phosphate tenements in

South of Mauritania. Drilling to commence in 4Q

2010

DSO production expected to commence in late

2011

Source: BRM.

Bumi MauritaniaNear Term Producing Iron Ore Project

Mineral Inventory

Tonnage (Ore)

Mineral Grade

Contained Metal

100% Equity 100% Equity

(’000 tonnes)

Mauritania Project 100,000 60,000 Iron 58% 58,000 Mt 34,800 Mt

SG

00

0U

M7

_A

P_

08

10

19

Overview

Location

Has COW rights to a 36,070 hectare mining

concession located in the Bone Bolango Regency

(Province of Gorontalo)

Based on explorations to date, the following have

been identified in the concession:

− Four copper and gold systems

− Three gold, silver and copper systems

− Four gold and silver systems

Currently working on advanced exploration and

feasibility studies for development of the mines

Conducted a scout drilling program in the South of

the COW area in 2008

JORC Resource to be completed by end 2012 with

commissioning expected in 2H 2014

Target large scale porphyry style mine similar to

Batu Hijau

Focus on projects at Cabang Kiri East and Sungai

Mak for porphyry copper and Tulabolo for

epithermal mineralization

Conceptual development model is to build a 25

million tonnes per annum (feed tonnes) copper

concentration plant that would be able to process

0.6% of copper and 0.6 grams per tonne of gold

material

Source: BRM.(1) Subject to progressive divestment to 49.0% beginning from the end of the fifth year after commencement of productino at the Gorontalo Project.

Gorontalo MineralsMedium Term Growth Copper & Gold Asset

Mineral Inventory

Tonnage (Ore)

Mineral Grade

Contained Metal

100% Equity 100% Equity

(’000 tonnes)

Gorontalo Project 125,000 100,000

Gold 0.55 g/tonne 2.4 mm oz 1.9 mm oz

Copper 0.75% 2,067 mm lbs 1,653 mm lbs

SG

00

0U

M7

_A

P_

08

10

20

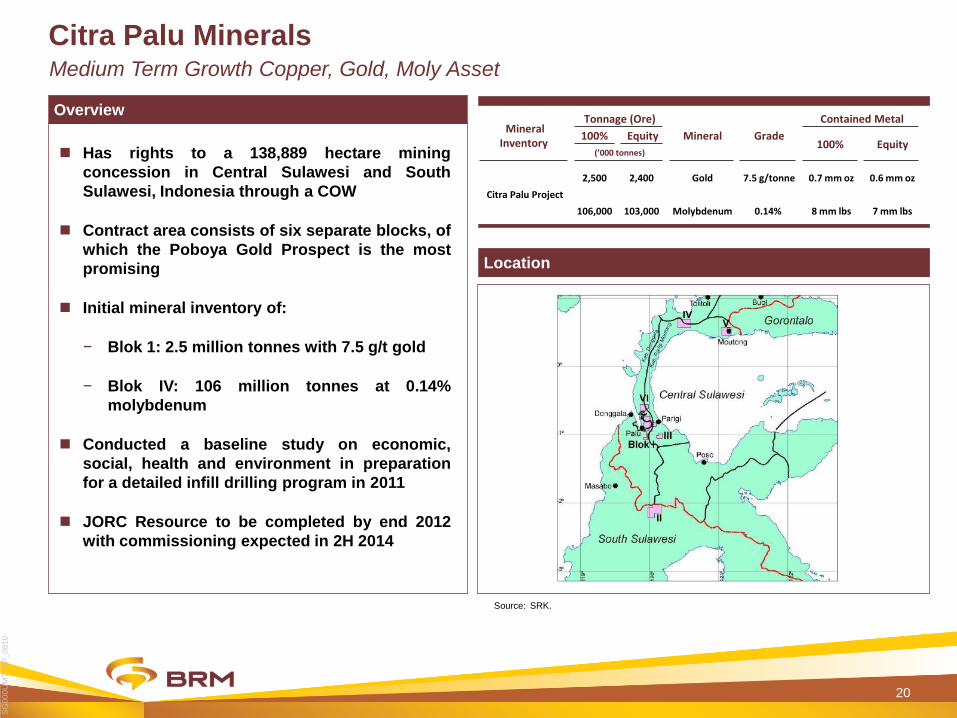

Overview

Location

Has rights to a 138,889 hectare mining

concession in Central Sulawesi and South

Sulawesi, Indonesia through a COW

Contract area consists of six separate blocks, of

which the Poboya Gold Prospect is the most

promising

Initial mineral inventory of:

− Blok 1: 2.5 million tonnes with 7.5 g/t gold

− Blok IV: 106 million tonnes at 0.14%

molybdenum

Conducted a baseline study on economic,

social, health and environment in preparation

for a detailed infill drilling program in 2011

JORC Resource to be completed by end 2012

with commissioning expected in 2H 2014

Source: SRK.

Medium Term Growth Copper, Gold, Moly Asset

Citra Palu Minerals

Mineral Inventory

Tonnage (Ore)

Mineral Grade

Contained Metal

100% Equity 100% Equity

(’000 tonnes)

Citra Palu Project

2,500 2,400 Gold 7.5 g/tonne 0.7 mm oz 0.6 mm oz

106,000 103,000 Molybdenum 0.14% 8 mm lbs 7 mm lbs

SG

00

0U

M7

_A

P_

08

10

21

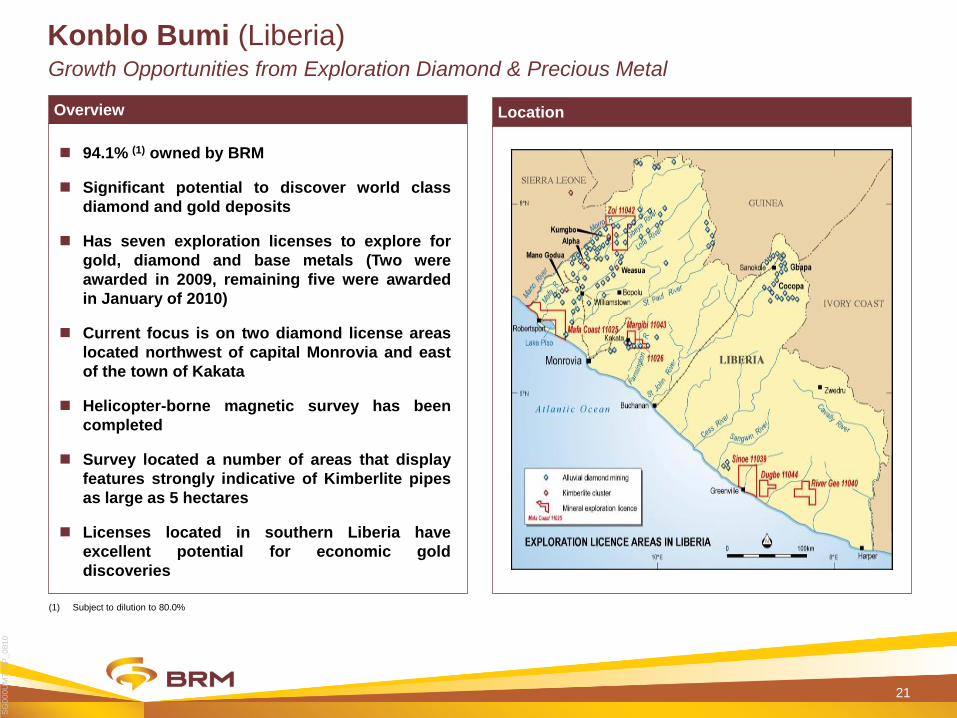

Overview Location

94.1% (1) owned by BRM

Significant potential to discover world class

diamond and gold deposits

Has seven exploration licenses to explore for

gold, diamond and base metals (Two were

awarded in 2009, remaining five were awarded

in January of 2010)

Current focus is on two diamond license areas

located northwest of capital Monrovia and east

of the town of Kakata

Helicopter-borne magnetic survey has been

completed

Survey located a number of areas that display

features strongly indicative of Kimberlite pipes

as large as 5 hectares

Licenses located in southern Liberia have

excellent potential for economic gold

discoveries

(1) Subject to dilution to 80.0%

Growth Opportunities from Exploration Diamond & Precious Metal

Konblo Bumi (Liberia)

SG

00

0U

M7

_A

P_

08

10

22

Industry Outlook

SG

00

0U

M7

_A

P_

08

10

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

2007 2008 2009 2010 2011 2012

10,000

11,000

12,000

13,000

Historical (LHS) Forward curve (LHS) Demand (RHS)

$0

$300

$600

$900

$1,200

$1,500

2007 2008 2009 2010 2011 2012

3,800

4,000

4,200

4,400

4,600

Historical (LHS) Forward curve (LHS) Demand (RHS)

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

2007 2008 2009 2010 2011 2012

17,000

18,000

19,000

20,000

Historical (LHS) Forward curve (LHS) Demand (RHS)

23

Strong Industry Outlook with Exposure to High Margin MetalsBRM’s portfolio: Exposure to highly attractive commodities with strong fundamentals

Copper (US$/lb), estimated demand (kt)(3)

Gold (US$/oz), estimated demand (kt)(3)

Zinc (US$/lb), estimated demand (kt)(3)

(1): UN Department of Economic & Social Affairs.(2): IMF World Economic Outlook.(3): Demand data from AME estimates, historical and forward prices from Bloomberg (as of

1 October 2010)

Drivers of Gold Demand

In 2008 and 2009, estimated gold demand from the investment sectorrose significantly, driving a substantial increase in the price of gold overthis period

This trend has continued throughout 2010 with gold prices reachingrecent highs as a result of investors’ fears in the value of currency andthe risks relating to other asset classes

AME forecasts that the price of gold will remain at relatively high levelsuntil 2012 as investor demand for gold remains strong relative tohistorical levels

GDP growth forecasts(2)

Global migration to urban environments(1)

$5.00

$4.00

$3.00

$2.00

$1.00

$0.00

2007 2008 2009 2010 2011 2012

20,000

19,000

18,000

17,000

Historical (LHS) Forward Curve (LHS) Demand (RHS)

$1,500

$1,200

$900

$600

$300

$0

2007 2008 2009 2010 2011 2012

Historical (LHS) Forward Curve (LHS) Demand (RHS)

4,600

4,400

4,200

4,000

3,800

$2.50

$2.00

$1.50

$1.00

$0.50

$0.00

2007 2008 2009 2010 2011 2012

Historical (LHS) Forward Curve (LHS) Demand (RHS)

13,000

12,000

11,000

10,000

SG

00

0U

M7

_A

P_

08

10

24

Newmont / Sumitomo hold a

56% stake in Batu Hijau and

are obliged to divest a further

7%

Newmont (market cap1:

US$27.0bn) is one of the

world's largest gold producers

Strength in large scale open

pit mining operations

(Nevada, Yanacocha,

Boddington)

Batu Hijau is a major source

of operating income

Sumitomo Corporation

(“SMC”) (market cap1:

US$10.04bn) is a trading

company that imports and

exports a wide variety of

goods such as metals,

machinery, fuel, and food

products

Newmont / Sumitomo hold a

56% stake in Batu Hijau and

are obliged to divest a further

7%

Antam is 20% owner of Dairi

Minerals

Antam (market cap1:

US$2.5bn) is a vertically

integrated, Indonesian state-

owned enterprise

Antam’s main products are

ferronickel, nickel ore, gold,

silver and bauxite

Antam currently operates:

− one nickel mine

− three ferronickel

smelters in Southeast

Sulawesi

− three nickel mines in

North Maluku

− one gold mine and one

gold smelter in West

Java

− one bauxite mine in Riau

− one precious metal

refinery in Jakarta

Bumi Resources (market cap1

US$8.0bn) is one of the

leading coal miners in

Indonesia

Its principal business includes

the exploration and

exploitation of coal deposits,

coal mining and selling, and

oil exploration

Bumi hold rights to mine for

coal through its two

subsidiaries:

- KPC: c. 90,960

hectares in East

Kalimantan until 2021

- Arutmin: c. 70,153

hectares in South

Kalimantan until 2019

Synergies with High Quality and Industry Leading Partners

Source: Public disclosures of the relevant company.Note: Based on currency conversion of USD/IDR of 8,928 and USD/JPY of 83.37.(1) Bloomberg as of March 31, 2011

SG

00

0U

M7

_A

P_

08

10

25

IPO Completion & Financial Highlights

SG

00

0U

M7

_A

P_

08

10

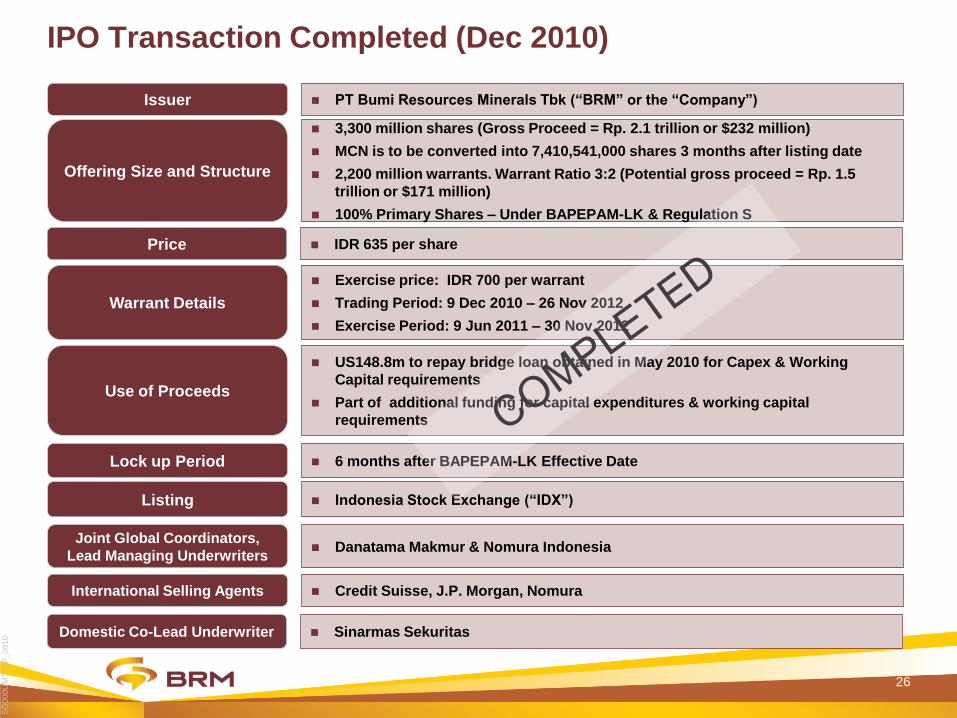

IPO Transaction Completed (Dec 2010)

PT Bumi Resources Minerals Tbk (“BRM” or the “Company”)Issuer

3,300 million shares (Gross Proceed = Rp. 2.1 trillion or $232 million)

MCN is to be converted into 7,410,541,000 shares 3 months after listing date

2,200 million warrants. Warrant Ratio 3:2 (Potential gross proceed = Rp. 1.5

trillion or $171 million)

100% Primary Shares – Under BAPEPAM-LK & Regulation S

Offering Size and Structure

Indonesia Stock Exchange (“IDX”)Listing

US148.8m to repay bridge loan obtained in May 2010 for Capex & Working

Capital requirements

Part of additional funding for capital expenditures & working capital

requirements

Use of Proceeds

Danatama Makmur & Nomura IndonesiaJoint Global Coordinators,

Lead Managing Underwriters

6 months after BAPEPAM-LK Effective DateLock up Period

Credit Suisse, J.P. Morgan, NomuraInternational Selling Agents

26

Exercise price: IDR 700 per warrant

Trading Period: 9 Dec 2010 – 26 Nov 2012

Exercise Period: 9 Jun 2011 – 30 Nov 2012

Warrant Details

IDR 635 per sharePrice

Sinarmas SekuritasDomestic Co-Lead Underwriter

SG

00

0U

M7

_A

P_

08

10

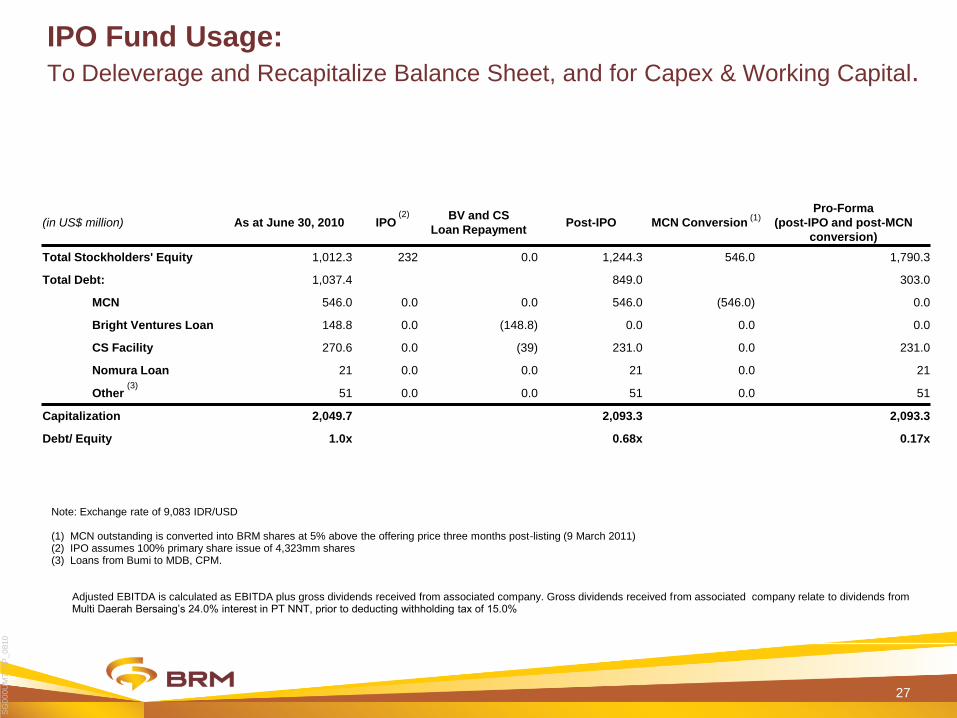

IPO Fund Usage:

27

(in US$ million) As at June 30, 2010 IPOBV and CS

Loan RepaymentPost-IPO MCN Conversion

Pro-Forma

(post-IPO and post-MCN

conversion)

Total Stockholders' Equity 1,012.3 232 0.0 1,244.3 546.0 1,790.3

Total Debt: 1,037.4 849.0 303.0

MCN 546.0 0.0 0.0 546.0 (546.0) 0.0

Bright Ventures Loan 148.8 0.0 (148.8) 0.0 0.0 0.0

CS Facility 270.6 0.0 (39) 231.0 0.0 231.0

Nomura Loan 21 0.0 0.0 21 0.0 21

Other 51 0.0 0.0 51 0.0 51

Capitalization 2,049.7 2,093.3 2,093.3

Debt/ Equity 1.0x 0.68x 0.17x

(1)(2)

(3)

Note: Exchange rate of 9,083 IDR/USD

(1) MCN outstanding is converted into BRM shares at 5% above the offering price three months post-listing (9 March 2011)(2) IPO assumes 100% primary share issue of 4,323mm shares(3) Loans from Bumi to MDB, CPM.

Adjusted EBITDA is calculated as EBITDA plus gross dividends received from associated company. Gross dividends received from associated company relate to dividends from Multi Daerah Bersaing’s 24.0% interest in PT NNT, prior to deducting withholding tax of 15.0%

To Deleverage and Recapitalize Balance Sheet, and for Capex & Working Capital.

SG

00

0U

M7

_A

P_

08

10

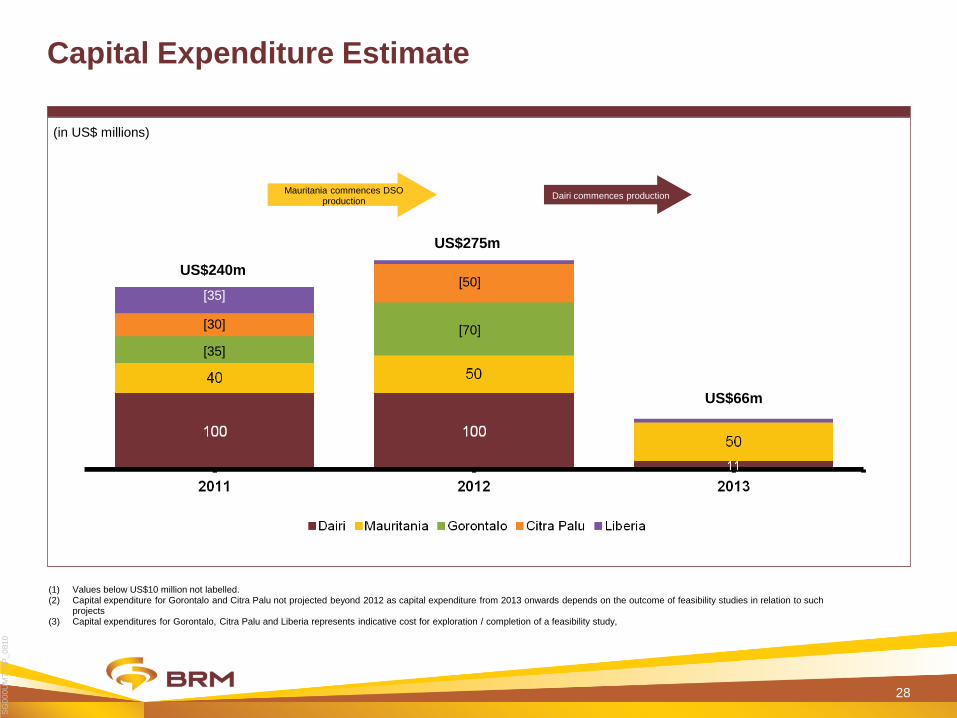

Capital Expenditure Estimate

(1) Values below US$10 million not labelled.(2) Capital expenditure for Gorontalo and Citra Palu not projected beyond 2012 as capital expenditure from 2013 onwards depends on the outcome of feasibility studies in relation to such

projects(3) Capital expenditures for Gorontalo, Citra Palu and Liberia represents indicative cost for exploration / completion of a feasibility study,

(in US$ millions)

28

[35]

[35]

[30] [ ]

[50]

Dairi commences productionMauritania commences DSO

production

[35]

[30]

[35]

[50]

[70]

US$240m

US$275m

US$66m

SG

00

0U

M7

_A

P_

08

10

29

Financial Highlights Q1 Year 2011

Q1 2010 Q1 2011

Revenues (‘000) - 37,573,888

Interest & financing Charges (‘000) (205,805,274) (100,408,747)

EBITDA (‘000) (679,101) 7,550,300

Equity in Net Income of Assoc. Company (‘000) 511,511,195 359,013,935

Net Profit (‘000) 271,283,972 138,525,501

Cash & Equivalents (‘000) 35,821,920 687,266,848

Total Debt (‘000) 7,882,721,140 2,675,908,843

Equity (‘000) 9,330,184,200 16,760,163,463

Debt to Equity 0.84X 0.15X

Net Debt to Equity 0.84X 0.11X

Q1 2010 Q1 2011

NNT Copper production (100%) (lb) 145,000,000 88,000,000

NNT Gold production (100%) (oz) 166,000 96,000

NNT Copper realized price $3.33/lb $4.00/lb

NNT Gold realized price $1,106/oz $1,382/oz

SG

00

0U

M7

_A

P_

08

10

30

Corporate Achievements

SG

00

0U

M7

_A

P_

08

10

Obtained exploration permit for Dairi Prima - Herald’sconcession (Zinc & lead)

Oct 2010

Obtained exploration permit for Gorontalo Mineral’s concession(Copper & gold)

Dec 2010

31

Completed IPO transaction and used the fund to repay $148.8 mio BrightVenture’s loan and to finance working capital & capex of assets (DERimproved to 0.7 x)

Dec 2010

Corporate Achievements (Sep 2010 – Jun 2011)

Received Award for year 2010 Best Equity Deal in Southeast Asia from theAlpha Magazine in Singapore

Feb 2011

BUMI Converted its $546 mio Mandatory Convertible Note into equityownership in BRMS (DER improved to 0.1x)

Mar 2011

Presidential Decree no. 28 year 2011 was issued on 19 May 2011. TheDecree allows conditional underground mining in the protected forestarea

May 2011

SG

00

0U

M7

_A

P_

08

10

32

Attachment

SG

00

0U

M7

_A

P_

08

10

33

Company History

BRM, in its present form, was formed through a series of

transactions principally in 2009 and 2010

− July 2009 – Bumi purchased 99.8% of Panorama from an

independent third party. In May 2010, Panorama changed its

name to BRM

− Nov 2009 – Bumi entered into a $850 mm facility(1) with

MDB, which was used to purchase 24% of PTNNT

− Dec 2009 – BRM purchased receivables under the

shareholder loans provided by Bumi to Calipso, Lemington,

IMC and Citra Palu (collectively “the Subsidiaries”) using

various promissory notes

− Feb 2010 – Part of the receivables from the Subsidiaries

were converted to equity

− Feb 2010 – BRM repaid its promissory notes to BUMI after

issuance of new shares of BRM, which was fully subscribed

by BUMI

− June 2010 – BRM signed conditional SPA with BUMI to

transfer MDB loan to BRM and BRM has agreed to issue

mandatory convertible notes to BUMI which will be

converted three months after the listing date

− June 2010 – BRM signed SPA with Bumi to purchase 100%

of shares in Bumi Japan

2003 Company established as PT Panorama Timur Abadi

(“Panorama”)

2005

Bumi Resources acquired 80% of Gorontalo Mineralsfrom BHP Billiton

Acquired 100% of Citra Palu Minerals from NewcrestMining

2007

In July 2007, Bumi Resources entered into a jointventure, Bumi Holding S.A.S., with a local partner inMauritania. Bumi Holding S.A.S. incorporated BumiMauritania to conduct activities in Mauritania

Bumi Resources launched a takeover bid for HeraldResources

In 2007, Bumi Resources established Konblo Bumi inLiberia

2009

Bumi Resources acquired the Company from theexisting owner (Risty Istiana)

Bumi Resources completes takeover of HeraldResources

2010

Company changed its name to PT Bumi ResourcesMinerals Tbk

BRM completed the acquisition of its 24% stake in PTNNT through its 75%-owned subsidiary, MDB

BRM undertook a stock split and reduced par value ofits share from IDR1,000,000 per share to IDR625 pershare

Reorganization

(1) Later amended in Feb 2010.

2004 Bumi Resources established Bumi Resources Japan

Company Limited (“Bumi Japan”) in Japan as amarketing service company