protecting consumers, promoting value and safeguarding the future regulating privatised water:...

TRANSCRIPT

Protecting consumers, promoting value and safeguarding the future

Regulating Privatised Water: Lessons from England and Wales

Regina Finn

Chief Executive

– Protecting consumers, promoting value and safeguarding the future

Overview

The Water Industry in England and Wales

The Role of Comparative Competition

Development of Market Competition

Conclusion and Questions

– Protecting consumers, promoting value and safeguarding the future

The Context: Long Term Challenges

Water Industry affected by long term drivers:– Climate change – adaptation and mitigation– Weather volatility – floods and droughts– Population growth and location – water stress– Demand for water and how we value water

Ofwat is regulating to protect consumers, promote value and safeguard the future.

Protecting consumers, promoting value and safeguarding the future

The Water Industry in England and Wales

– Protecting consumers, promoting value and safeguarding the future

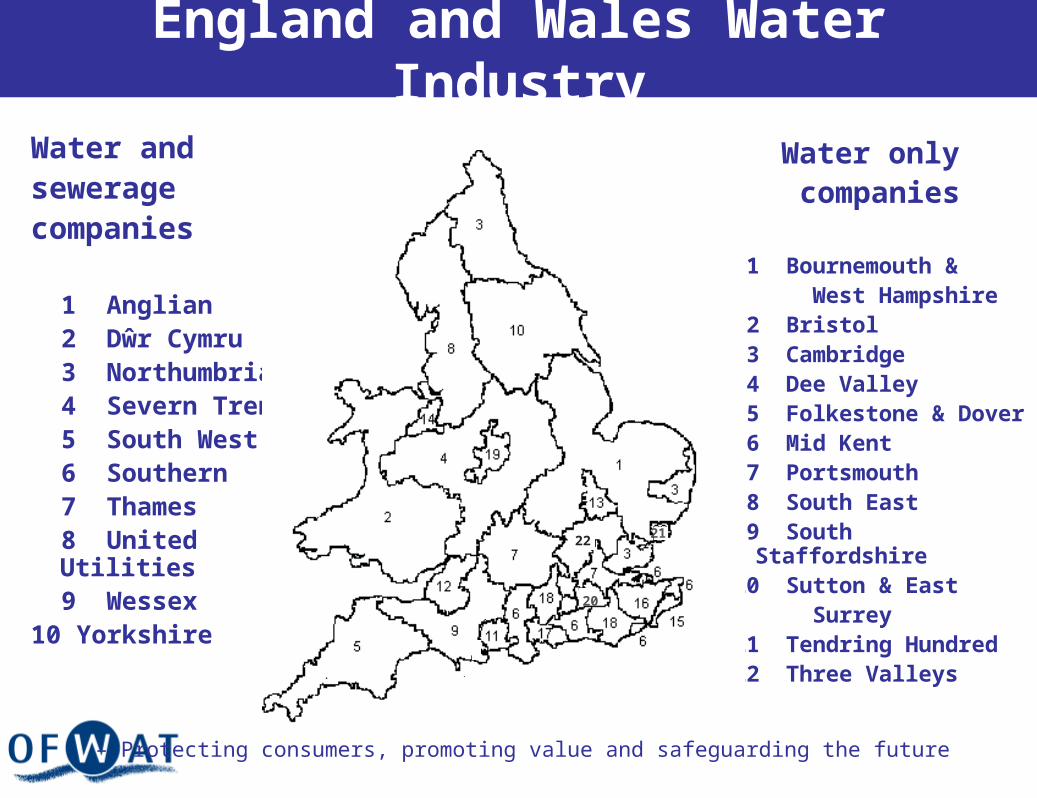

England and Wales Water Industry

Water and sewerage companies

1 Anglian 2 Dŵr Cymru 3 Northumbrian 4 Severn Trent 5 South West 6 Southern 7 Thames 8 United Utilities 9 Wessex10 Yorkshire

Water only companies

11 Bournemouth & West Hampshire12 Bristol13 Cambridge14 Dee Valley15 Folkestone & Dover16 Mid Kent17 Portsmouth18 South East19 South Staffordshire20 Sutton & East Surrey21 Tendring Hundred22 Three Valleys

20

2122

– Protecting consumers, promoting value and safeguarding the future

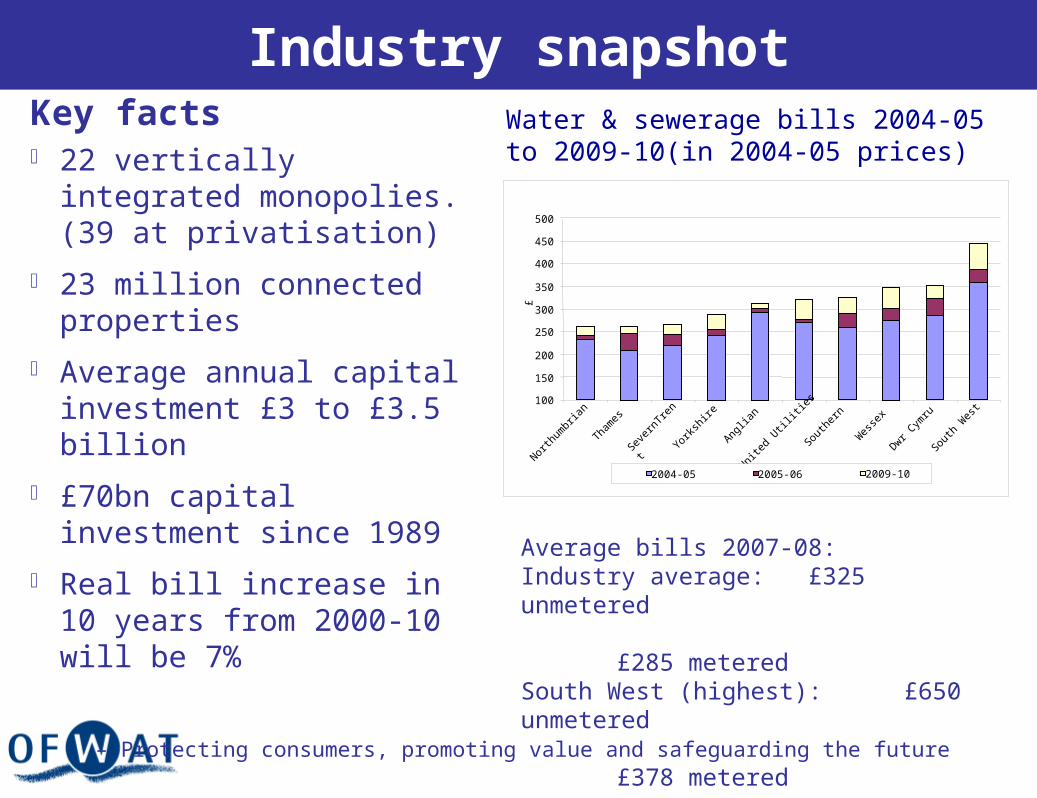

Industry snapshotKey facts 22 vertically integrated

monopolies. (39 at privatisation)

23 million connected properties

Average annual capital investment £3 to £3.5 billion

£70bn capital investment since 1989

Real bill increase in 10 years from 2000-10 will be 7%

100

150

200

250

300

350

400

450

500

North

umbr

ian

Tham

es

Sever

nTre

nt

Yorks

hire

Anglia

n

United

Utili

ties

South

ern

Wes

sex

Dwr Cym

ru

South

Wes

t

£

2004-05 2005-06 2009-10

Water & sewerage bills 2004-05 to 2009-10(in 2004-05 prices)

Average bills 2007-08:Industry average: £325 unmetered

£285 meteredSouth West (highest): £650 unmetered

£378 metered

– Protecting consumers, promoting value and safeguarding the future

Ownership of Companies

Five listed companies (United Utilities, Northumbrian, Severn Trent, South West and Dee Valley)

One recently delisted (Yorkshire)

Rest privately owned

Range of owners including private equity firms and pension funds

– Protecting consumers, promoting value and safeguarding the future

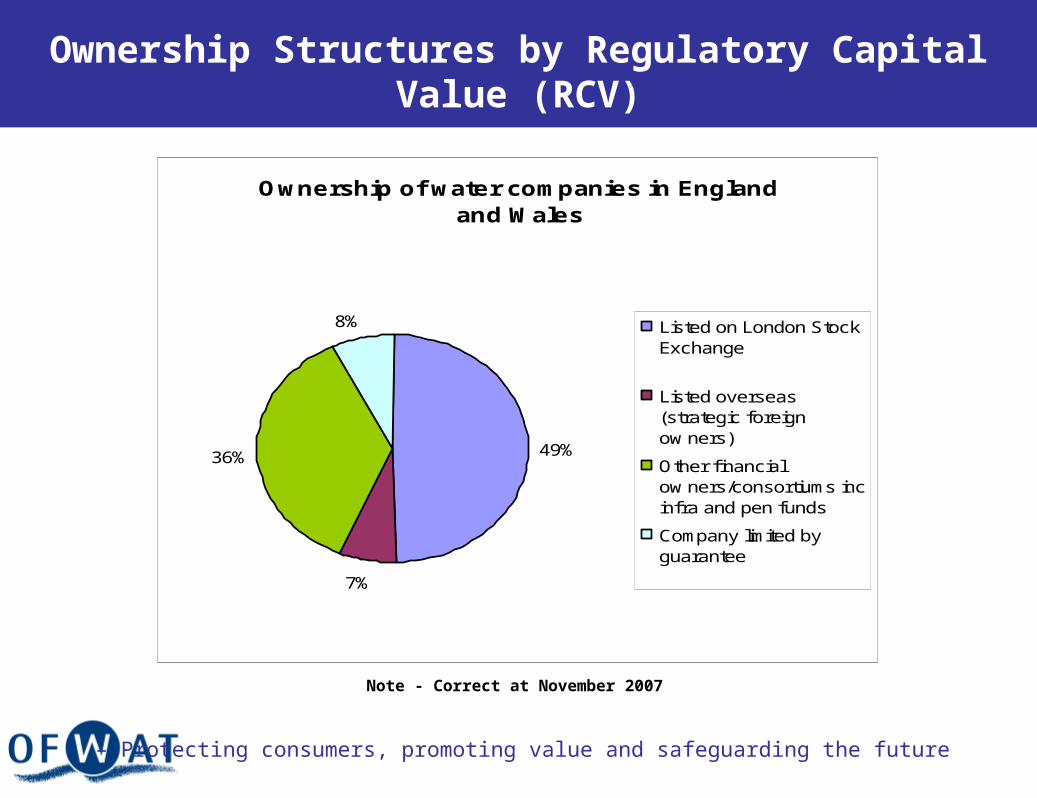

Ownership Structures by Regulatory Capital Value (RCV)

Ownership of water companies in England and Wales

49%

7%

36%

8% Listed on London StockExchange

Listed overseas(strategic foreignow ners)

Other f inancialow ners/consortiums incinfra and pen funds

Company limited byguarantee

Note - Correct at November 2007

– Protecting consumers, promoting value and safeguarding the future

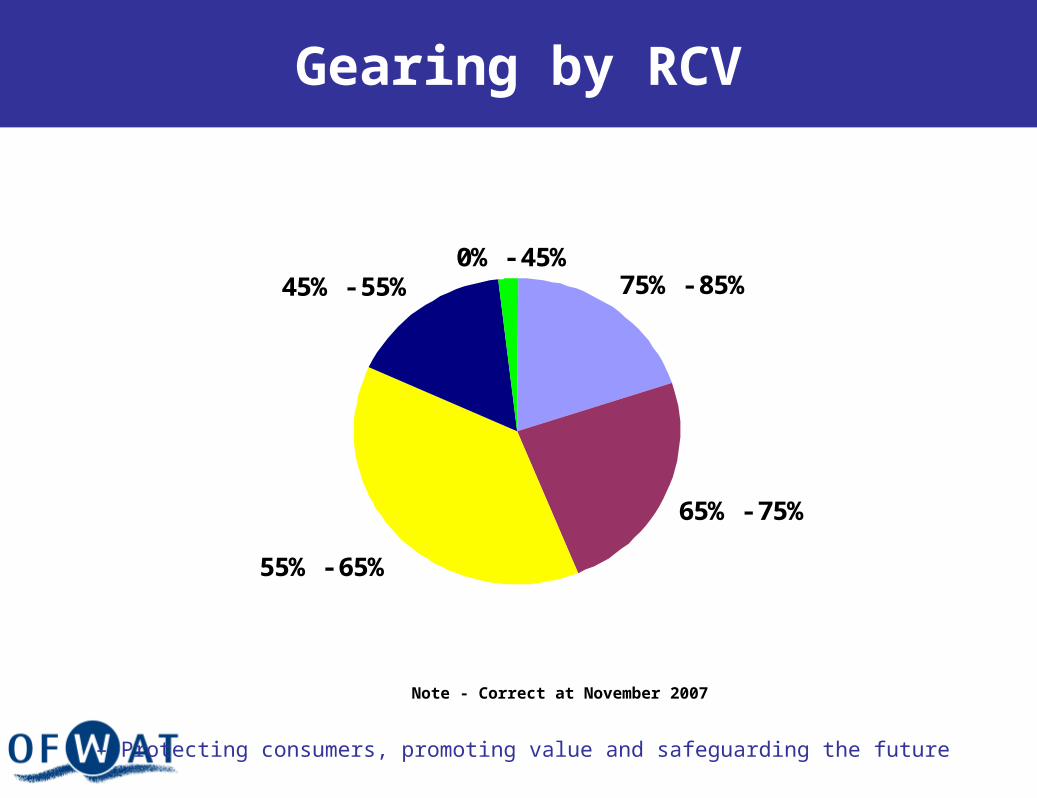

Gearing by RCV

55% - 65%

75% - 85%0% - 45%

65% - 75%

45% - 55%

Note - Correct at November 2007

Protecting consumers, promoting value and safeguarding the future

The Role of Comparative Competition

– Protecting consumers, promoting value and safeguarding the future

Comparative Competition

Simple metrics - such as interruptions to water and supply number of complaints

Advanced modelling of expenditure and procurement efficiency, and

International benchmarking where possible

Key tool for regulating monopoly water industry:

– Protecting consumers, promoting value and safeguarding the future

Advantages of Comparative Competition

Keeps regulation “small” Uses real information to

drive performance – difficult to challenge

Allows companies to manage their own business

Lets company performance speak for itself

– Protecting consumers, promoting value and safeguarding the future

What the Regulatory Regime Has Delivered (1)

Significant capital investment privately financed

£70bn invested in water sector since 1989

Major efficiency gains resulting in lower bills to customers

The average customer bill in 2010 will be £100 lower than it would have been

– Protecting consumers, promoting value and safeguarding the future

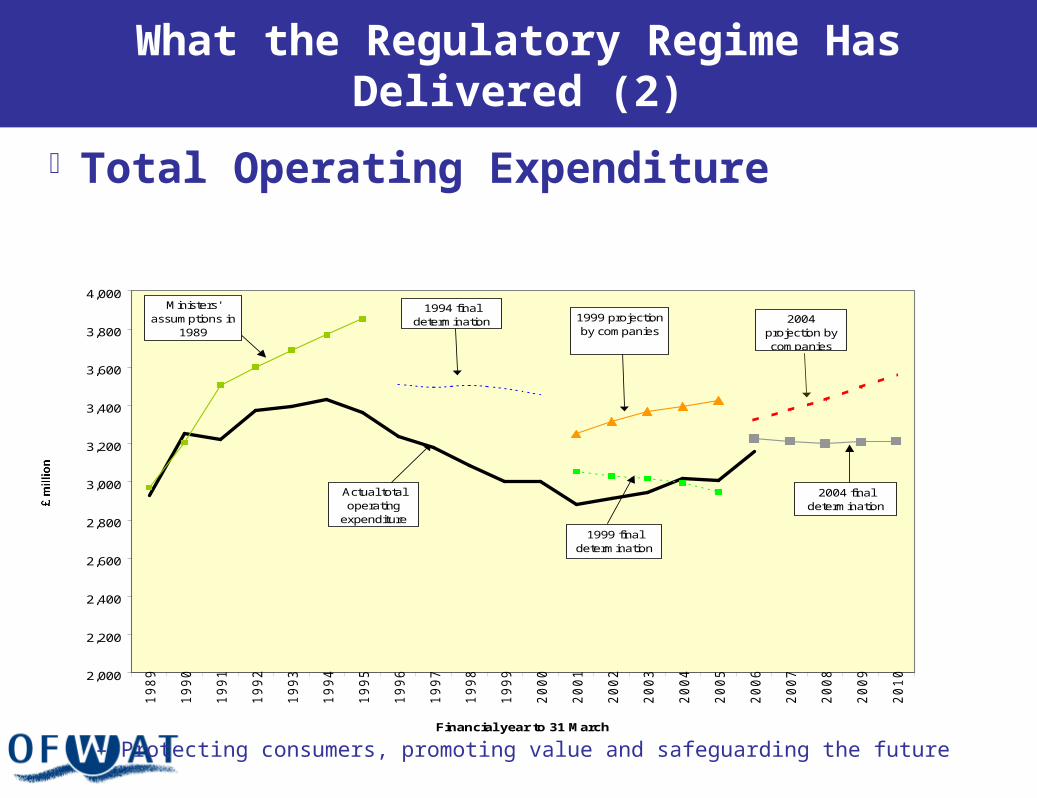

What the Regulatory Regime Has Delivered (2)

Total Operating Expenditure

2,000

2,200

2,400

2,600

2,800

3,000

3,200

3,400

3,600

3,800

4,000

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Financial year to 31 March

1999 projection by companies

1994 final determination

Actual total operating

expenditure

Ministers' assumptions in

19892004

projection by companies

2004 final determination

1999 final determination

– Protecting consumers, promoting value and safeguarding the future

What the Regulatory Regime Has Delivered (3)

Essential services safeguarded

Improved reliability and quality of service

Improved water quality - safe, reliable drinking water

Reduced leakage Reduced risk of

sewer flooding

– Protecting consumers, promoting value and safeguarding the future

Reduced Leakage

Total leakage 1994-95 to 2004-05 (Ml/d)

51124980

4505

3989

3551

33063243

3414

3605 3649 3608

2000

2500

3000

3500

4000

4500

5000

5500

1994-95 1995-96 1996-97 1997-98 1998-99 1999-2000 2000-01 2001-02 2002-03 2003-04 2004-05

Year

To

tal

Lea

ka

ge

– Protecting consumers, promoting value and safeguarding the future

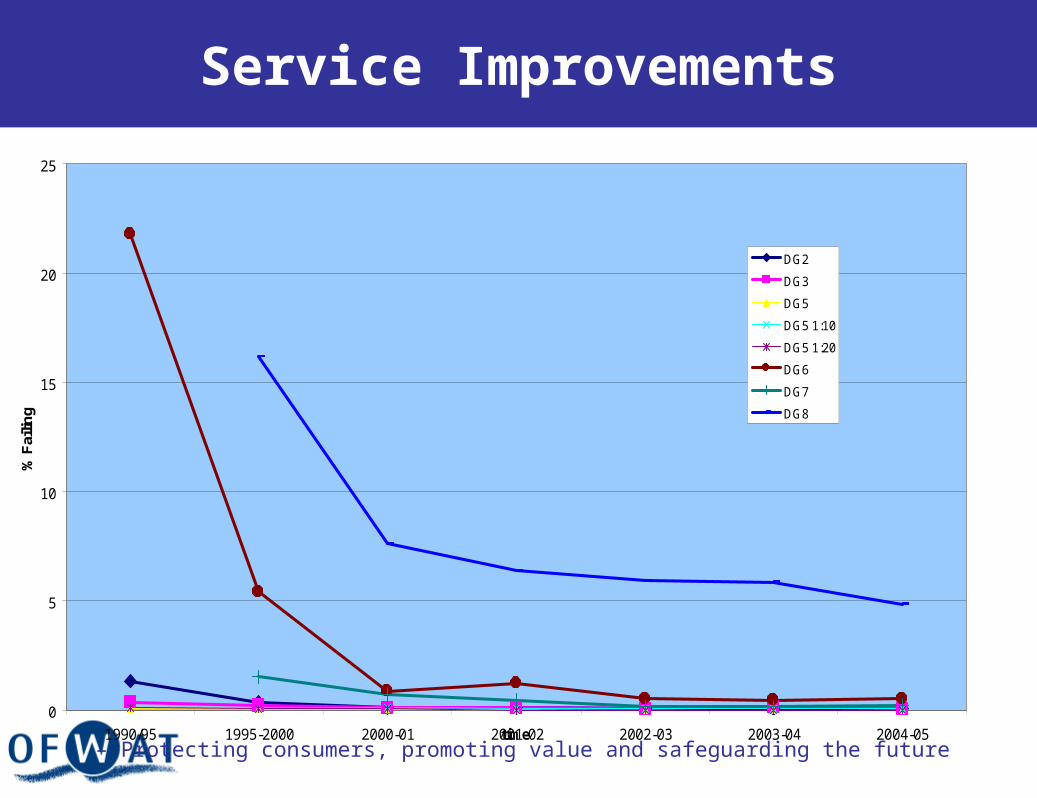

Service Improvements

0

5

10

15

20

25

1990/95 1995-2000 2000-01 2001-02 2002-03 2003-04 2004-05time

% F

ailin

g

DG2

DG3

DG5

DG5 1:10

DG5 1:20

DG6

DG7

DG8

– Protecting consumers, promoting value and safeguarding the future

Drawbacks of Comparative Competition

Imperfect proxy for effective competition

Companies tempted to ‘game’

Data collection is an onerous and expensive exercise for both companies and regulator

Information asymmetry – companies have the advantage

And…

– Protecting consumers, promoting value and safeguarding the future

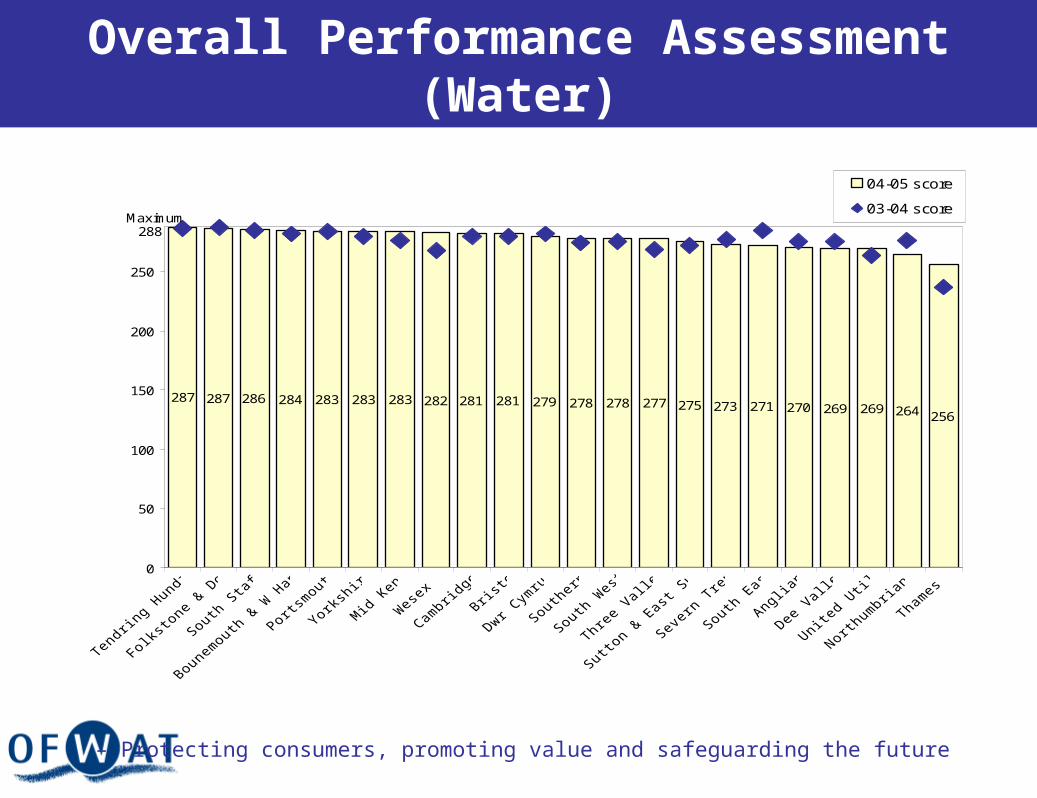

Overall Performance Assessment (Water)

287 287 286 284 283 283 283 282 281 279 278 278 277 275 273 271 270 269 269 264 256281

0

50

100

150

200

250

04-05 score

03-04 scoreMaximum

288

– Protecting consumers, promoting value and safeguarding the future

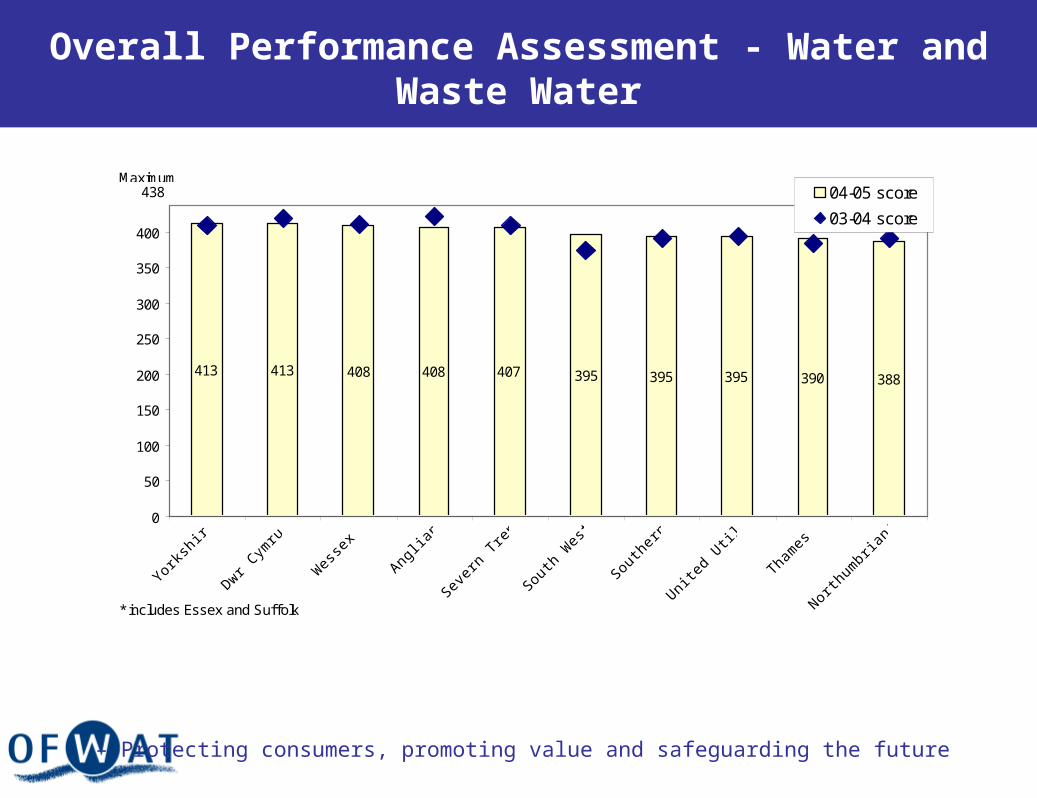

Overall Performance Assessment - Water and Waste Water

413 413 408 408 407 395 395 395 390 388

0

50

100

150

200

250

300

350

400

York

shire

Dwr Cym

ru

Wes

sex

Anglia

n

Sever

n Tr

ent

South

Wes

t

South

ern

United

Utili

ties

Tham

es

North

umbr

ian(*)

04-05 score

03-04 score

438Maximum

* includes Essex and Suffolk

– Protecting consumers, promoting value and safeguarding the future

So What Next?

Evolution of the comparative competition – eg capital incentive scheme

Review what we compare and measure – eg customer experience measures

Promote effective competition in the market – reduce regulation

Protecting consumers, promoting value and safeguarding the future

The Promotion of Market Competition

– Protecting consumers, promoting value and safeguarding the future

Promoting Competition: Why?

Ofwat has a duty to promote competition

Competition can drive dynamic efficiency and innovation

Comparative competition has delivered– But risk of diminishing

returns over time Competition has delivered

benefits elsewhere Customers want choice

– Protecting consumers, promoting value and safeguarding the future

Ofwat Competition Review – Part One

Conclusions: Existing regime ineffective Need to remove the access

pricing rule from primary legislation

– Replace with principles Reduce the threshold for non-

household customer competition from 50Ml to zero

Enable retail competition for sewerage

Develop accounting separation…

– Protecting consumers, promoting value and safeguarding the future

Accounting Separation

Meets multiple goals, including promoting competition

Will require separation of the natural monopoly part of the value chain from contestable activities

Will provide greater visibility for new entrants on costs and potential margins

Will facilitate cost reflective access tariffs Will ensure level playing field between

incumbents and entrants New reporting from 2009

– Protecting consumers, promoting value and safeguarding the future

Ofwat Competition Review – Part Two

Inform Government Review of competition in the sector

Will examine the potential for competition throughout the value chain;

Detailed paper in Spring Objective

– Secure innovative entry, efficient investment and customer benefits;

– Protect water quality and security

– Contribute to social and environmental objectives

– Protecting consumers, promoting value and safeguarding the future

Ofwat Competition Review – Part Two

Key principles: Similarities with other network utilities Regulatory unbundling – early step Structural unbundling of retail – early step Mechanisms to secure innovation in resources All customers should benefit Separate cross-subsidies from the functioning of

the market Simple and transparent market models and

access pricing

– Protecting consumers, promoting value and safeguarding the future

Conclusion

The England and Wales Regulatory Regime has delivered significant benefits for water consumers

To continue to deliver, we need to build on the success of the past and develop new tools to tackle the challenges of the future

– Protecting consumers, promoting value and safeguarding the future

More information is available from our

website:

www.ofwat.gov.uk