prospects for global ship finance - petrofin by ted petropoulos head petrofin research 8th greek...

TRANSCRIPT

presented by

Ted Petropoulos HEAD

PETROFIN RESEARCH

8th Greek Shipping & Ship Finance Conference

20th May 2011

Prospects for global Ship Finance

Presentation of latest Petrofin Bank Research ©

PETROFIN RESEARCH

www.petrofin.gr

A. Analysis and trends of global ship finance

The total global portfolio today is estimated at approx. $500bn consisting of $450bn in drawn loans and $50bn in committed but undrawn loans.

PETROFIN RESEARCH

www.petrofin.gr A. Analysis and trends of global ship finance

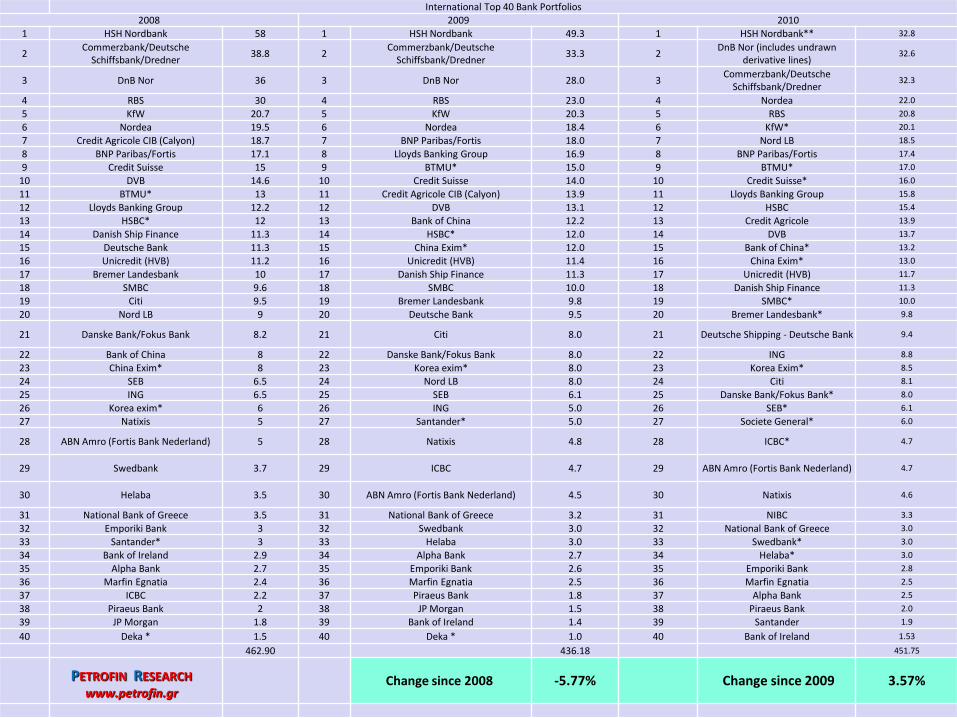

In the following graphs we show the loan portfolios of the top 40 banks, according to the latest Petrofin Bank Research © just concluded:

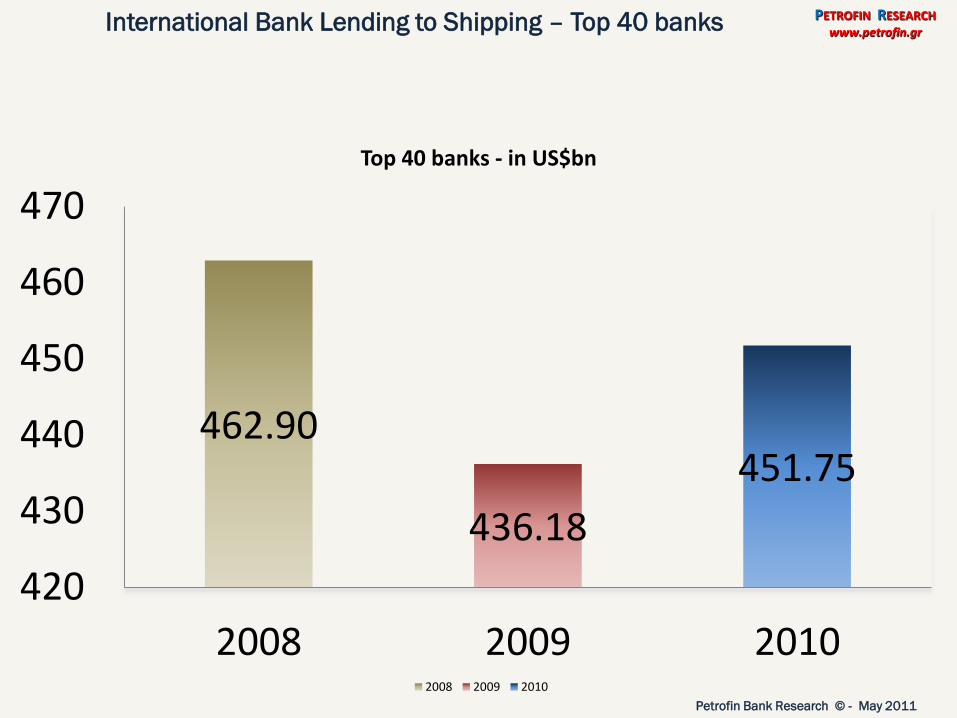

462.90

436.18

451.75

420

430

440

450

460

470

2008 2009 2010

Top 40 banks - in US$bn

2008 2009 2010

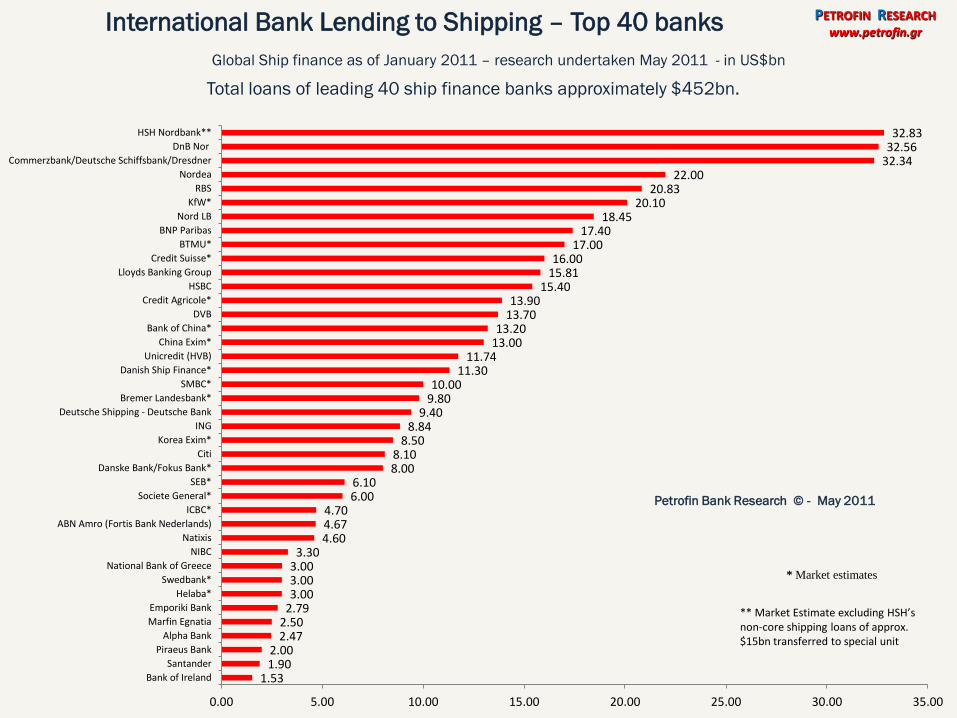

International Bank Lending to Shipping – Top 40 banks PETROFIN RESEARCH

www.petrofin.gr

Petrofin Bank Research © - May 2011

Their total portfolio: $229.51bn

Top 10 banks’ percentage of global portfolio: 50.8%

Top 10 Ship financing banks PETROFIN RESEARCH

www.petrofin.gr

Petrofin Bank Research © - May 2011

** Market Estimate excluding HSH’s non-core shipping loans of approx. $15bn transferred to special unit

* Market estimates

0.00 5.00 10.00 15.00 20.00 25.00 30.00 35.00

HSH Nordbank**

DnB Nor

Commerzbank/Deutsche Schiffsbank/Dresdner

Nordea

RBS

KfW*

Nord LB

BNP Paribas

BTMU*

Credit Suisse*

Top 10 Ship finance banks

Global Ship finance as of January 2011 – research undertaken May 2011 - in US$bn

Total loans of leading 40 ship finance banks approximately $452bn.

International Bank Lending to Shipping – Top 40 banks PETROFIN RESEARCH

www.petrofin.gr

Petrofin Bank Research © - May 2011

32.83 32.56

32.34 22.00

20.83 20.10

18.45 17.40

17.00 16.00

15.81 15.40

13.90 13.70

13.20 13.00

11.74 11.30

10.00 9.80

9.40 8.84

8.50 8.10 8.00

6.10 6.00

4.70 4.67 4.60

3.30 3.00 3.00 3.00

2.79 2.50 2.47

2.00 1.90

1.53

0.00 5.00 10.00 15.00 20.00 25.00 30.00 35.00

HSH Nordbank**

DnB Nor

Commerzbank/Deutsche Schiffsbank/Dresdner

Nordea

RBS

KfW*

Nord LB

BNP Paribas

BTMU*

Credit Suisse*

Lloyds Banking Group

HSBC

Credit Agricole*

DVB

Bank of China*

China Exim*

Unicredit (HVB)

Danish Ship Finance*

SMBC*

Bremer Landesbank*

Deutsche Shipping - Deutsche Bank

ING

Korea Exim*

Citi

Danske Bank/Fokus Bank*

SEB*

Societe General*

ICBC*

ABN Amro (Fortis Bank Nederlands)

Natixis

NIBC

National Bank of Greece

Swedbank*

Helaba*

Emporiki Bank

Marfin Egnatia

Alpha Bank

Piraeus Bank

Santander

Bank of Ireland

** Market Estimate excluding HSH’s non-core shipping loans of approx. $15bn transferred to special unit

* Market estimates

International Top 40 Bank Portfolios 2008 2009 2010

1 HSH Nordbank 58 1 HSH Nordbank 49.3 1 HSH Nordbank** 32.8

2 Commerzbank/Deutsche

Schiffsbank/Dredner 38.8 2

Commerzbank/Deutsche Schiffsbank/Dredner

33.3 2 DnB Nor (includes undrawn

derivative lines) 32.6

3 DnB Nor 36 3 DnB Nor 28.0 3 Commerzbank/Deutsche

Schiffsbank/Dredner 32.3

4 RBS 30 4 RBS 23.0 4 Nordea 22.0

5 KfW 20.7 5 KfW 20.3 5 RBS 20.8

6 Nordea 19.5 6 Nordea 18.4 6 KfW* 20.1

7 Credit Agricole CIB (Calyon) 18.7 7 BNP Paribas/Fortis 18.0 7 Nord LB 18.5

8 BNP Paribas/Fortis 17.1 8 Lloyds Banking Group 16.9 8 BNP Paribas/Fortis 17.4

9 Credit Suisse 15 9 BTMU* 15.0 9 BTMU* 17.0

10 DVB 14.6 10 Credit Suisse 14.0 10 Credit Suisse* 16.0

11 BTMU* 13 11 Credit Agricole CIB (Calyon) 13.9 11 Lloyds Banking Group 15.8

12 Lloyds Banking Group 12.2 12 DVB 13.1 12 HSBC 15.4

13 HSBC* 12 13 Bank of China 12.2 13 Credit Agricole 13.9

14 Danish Ship Finance 11.3 14 HSBC* 12.0 14 DVB 13.7

15 Deutsche Bank 11.3 15 China Exim* 12.0 15 Bank of China* 13.2

16 Unicredit (HVB) 11.2 16 Unicredit (HVB) 11.4 16 China Exim* 13.0

17 Bremer Landesbank 10 17 Danish Ship Finance 11.3 17 Unicredit (HVB) 11.7

18 SMBC 9.6 18 SMBC 10.0 18 Danish Ship Finance 11.3

19 Citi 9.5 19 Bremer Landesbank 9.8 19 SMBC* 10.0

20 Nord LB 9 20 Deutsche Bank 9.5 20 Bremer Landesbank* 9.8

21 Danske Bank/Fokus Bank 8.2 21 Citi 8.0 21 Deutsche Shipping - Deutsche Bank 9.4

22 Bank of China 8 22 Danske Bank/Fokus Bank 8.0 22 ING 8.8

23 China Exim* 8 23 Korea exim* 8.0 23 Korea Exim* 8.5

24 SEB 6.5 24 Nord LB 8.0 24 Citi 8.1

25 ING 6.5 25 SEB 6.1 25 Danske Bank/Fokus Bank* 8.0

26 Korea exim* 6 26 ING 5.0 26 SEB* 6.1

27 Natixis 5 27 Santander* 5.0 27 Societe General* 6.0

28 ABN Amro (Fortis Bank Nederland) 5 28 Natixis 4.8 28 ICBC* 4.7

29 Swedbank 3.7 29 ICBC 4.7 29 ABN Amro (Fortis Bank Nederland) 4.7

30 Helaba 3.5 30 ABN Amro (Fortis Bank Nederland) 4.5 30 Natixis 4.6

31 National Bank of Greece 3.5 31 National Bank of Greece 3.2 31 NIBC 3.3

32 Emporiki Bank 3 32 Swedbank 3.0 32 National Bank of Greece 3.0

33 Santander* 3 33 Helaba 3.0 33 Swedbank* 3.0

34 Bank of Ireland 2.9 34 Alpha Bank 2.7 34 Helaba* 3.0

35 Alpha Bank 2.7 35 Emporiki Bank 2.6 35 Emporiki Bank 2.8

36 Marfin Egnatia 2.4 36 Marfin Egnatia 2.5 36 Marfin Egnatia 2.5

37 ICBC 2.2 37 Piraeus Bank 1.8 37 Alpha Bank 2.5

38 Piraeus Bank 2 38 JP Morgan 1.5 38 Piraeus Bank 2.0

39 JP Morgan 1.8 39 Bank of Ireland 1.4 39 Santander 1.9

40 Deka * 1.5 40 Deka * 1.0 40 Bank of Ireland 1.53

462.90 436.18 451.75

Change since 2008 -5.77% Change since 2009 3.57%

PETROFIN RESEARCH

www.petrofin.gr

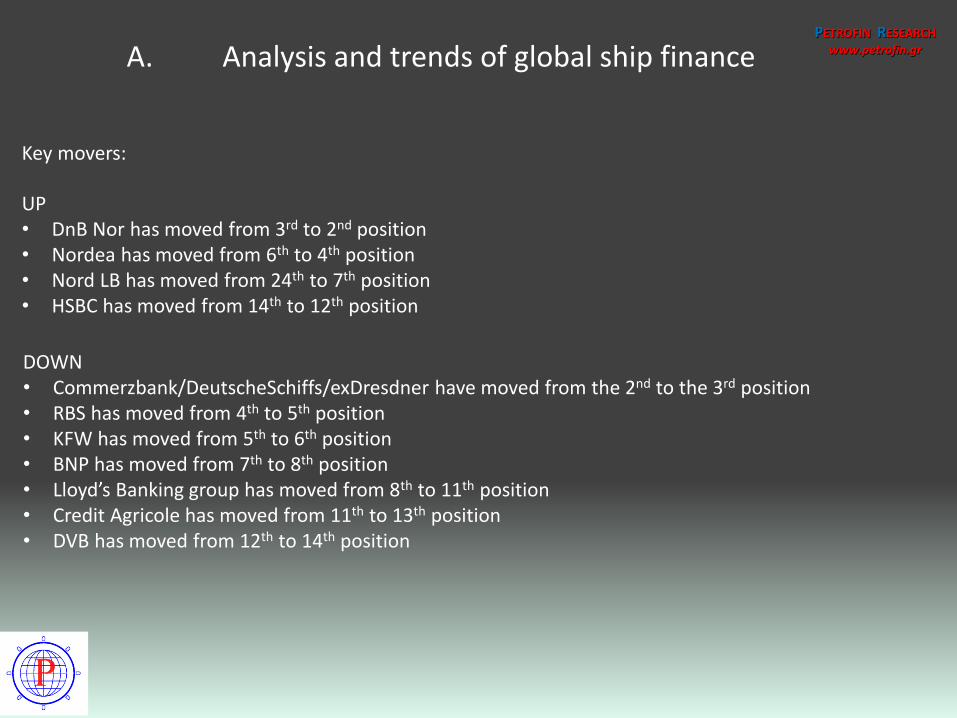

UP • DnB Nor has moved from 3rd to 2nd position • Nordea has moved from 6th to 4th position • Nord LB has moved from 24th to 7th position • HSBC has moved from 14th to 12th position

PETROFIN RESEARCH

www.petrofin.gr A. Analysis and trends of global ship finance

Key movers:

DOWN • Commerzbank/DeutscheSchiffs/exDresdner have moved from the 2nd to the 3rd position • RBS has moved from 4th to 5th position • KFW has moved from 5th to 6th position • BNP has moved from 7th to 8th position • Lloyd’s Banking group has moved from 8th to 11th position • Credit Agricole has moved from 11th to 13th position • DVB has moved from 12th to 14th position

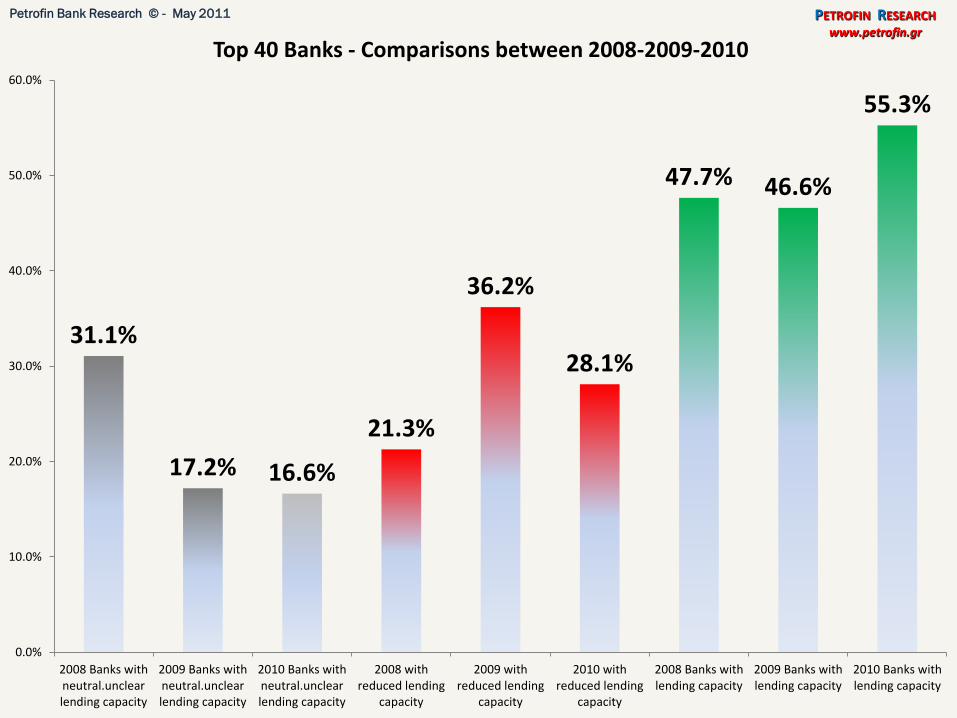

31.1%

17.2% 16.6%

21.3%

36.2%

28.1%

47.7% 46.6%

55.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2008 Banks withneutral.unclearlending capacity

2009 Banks withneutral.unclearlending capacity

2010 Banks withneutral.unclearlending capacity

2008 withreduced lending

capacity

2009 withreduced lending

capacity

2010 withreduced lending

capacity

2008 Banks withlending capacity

2009 Banks withlending capacity

2010 Banks withlending capacity

Top 40 Banks - Comparisons between 2008-2009-2010

PETROFIN RESEARCH

www.petrofin.gr

Petrofin Bank Research © - May 2011

PETROFIN RESEARCH

www.petrofin.gr

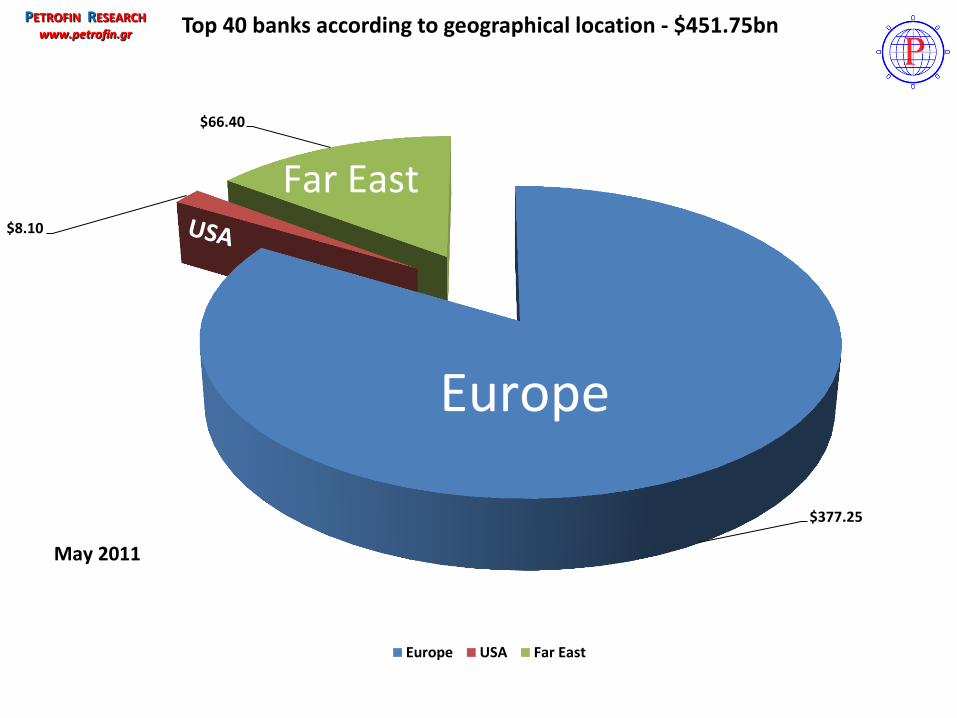

Global ship finance exposure – asymmetrical distribution

A. Analysis and trends of global ship finance

Total top banks’ portfolio: US$449.76bn

Europe

Far East

$377.25

$8.10

$66.40

Top 40 banks according to geographical location - $451.75bn

Europe USA Far East

Europe

Far East

PETROFIN RESEARCH

www.petrofin.gr

May 2011

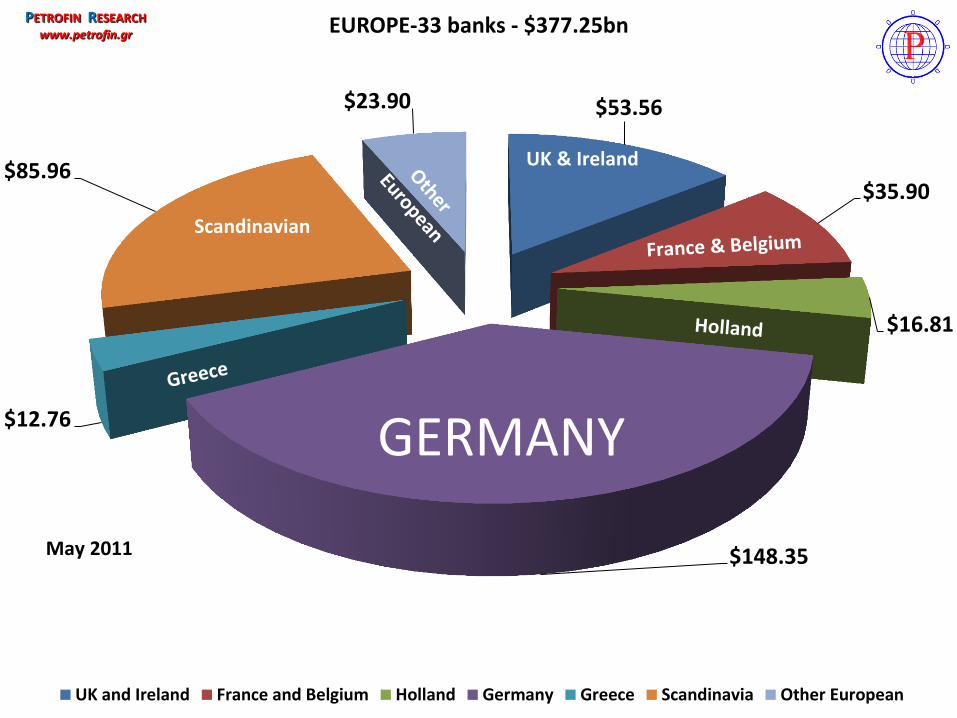

$53.56

$35.90

$16.81

$148.35

$12.76

$85.96

$23.90

EUROPE-33 banks - $377.25bn

UK and Ireland France and Belgium Holland Germany Greece Scandinavia Other European

GERMANY

UK & Ireland

PETROFIN RESEARCH

www.petrofin.gr

May 2011

Scandinavian

PETROFIN RESEARCH

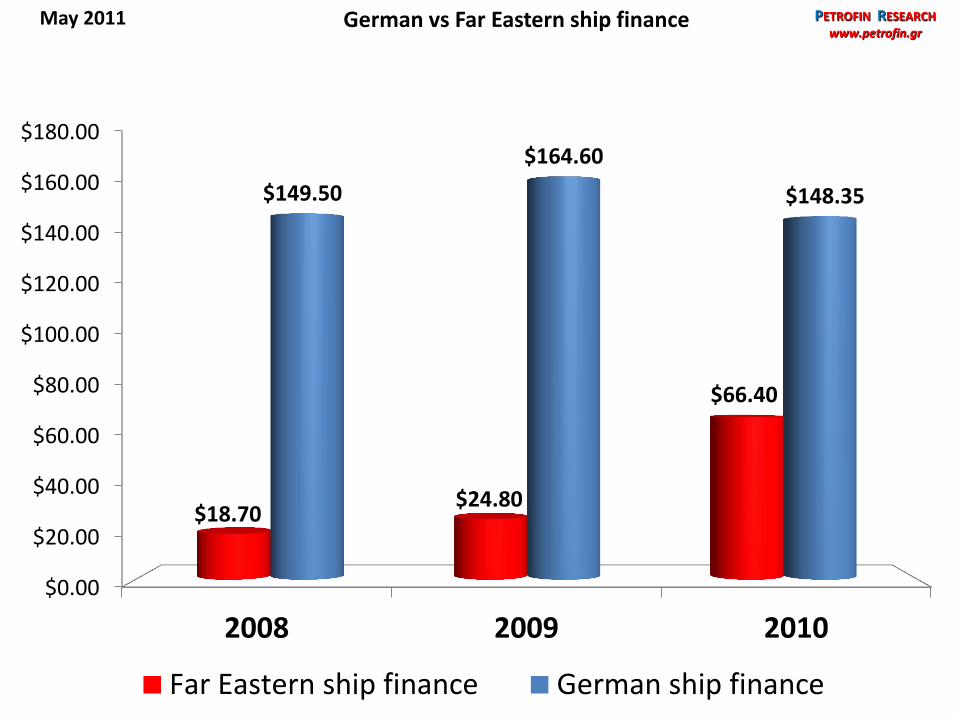

www.petrofin.gr May 2011 German vs Far Eastern ship finance

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

2008 2009 2010

$18.70 $24.80

$66.40

$149.50

$164.60

$148.35

Far Eastern ship finance German ship finance

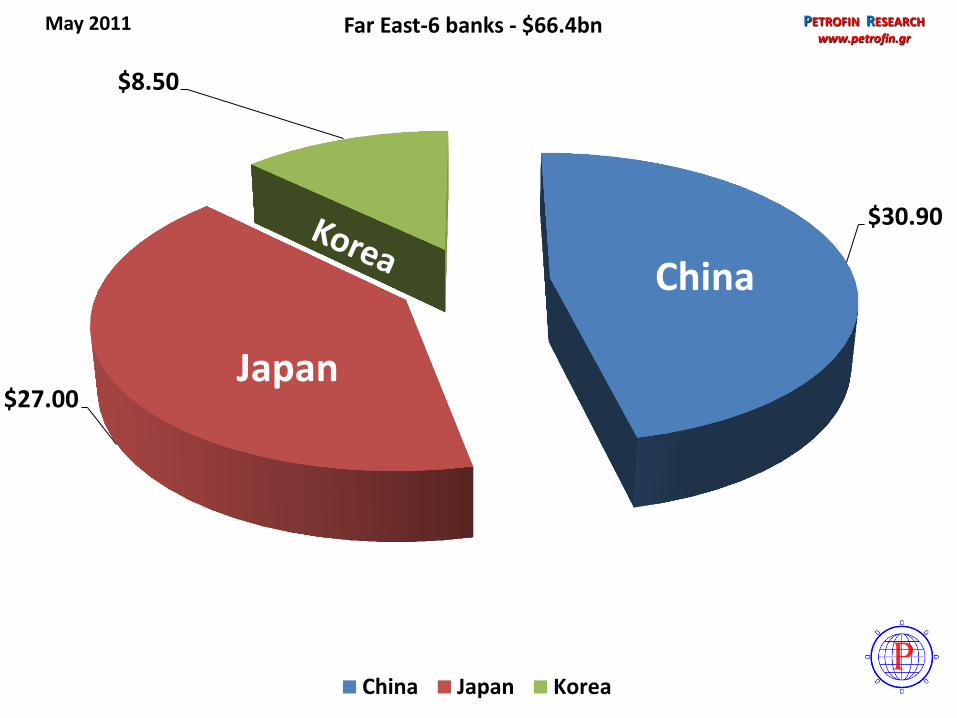

China

$30.90

$27.00

$8.50

Far East-6 banks - $66.4bn

China Japan Korea

China

PETROFIN RESEARCH

www.petrofin.gr May 2011

Japan

Trends and expectations over the next 3 years

PETROFIN RESEARCH

www.petrofin.gr

A. Analysis and trends of global ship finance

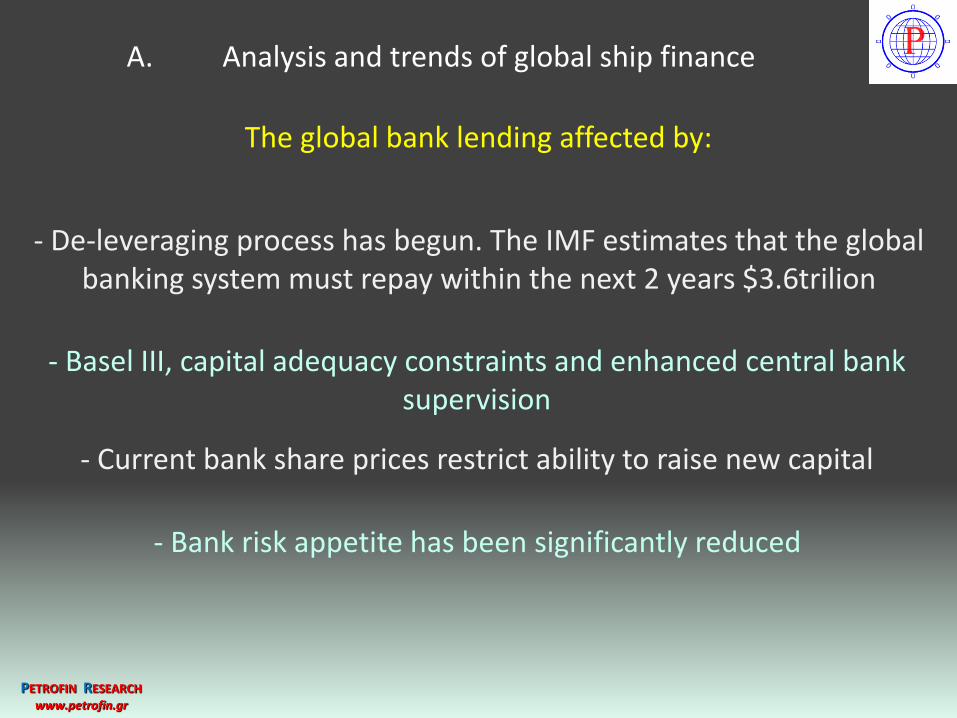

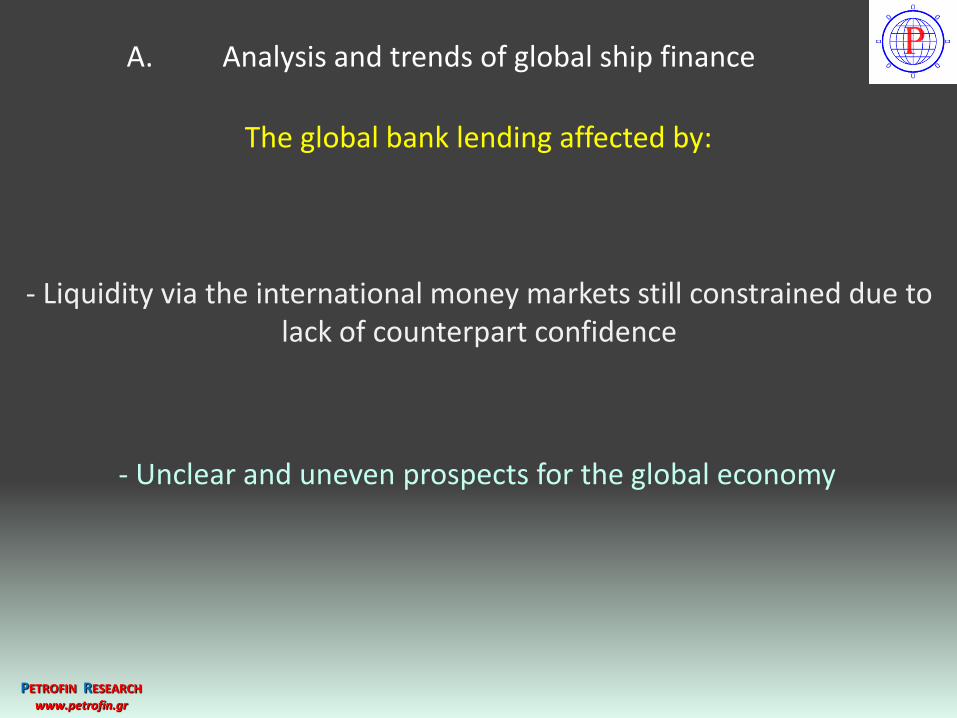

The global bank lending affected by:

PETROFIN RESEARCH

www.petrofin.gr

- De-leveraging process has begun. The IMF estimates that the global banking system must repay within the next 2 years $3.6trilion

A. Analysis and trends of global ship finance

- Basel III, capital adequacy constraints and enhanced central bank supervision

- Current bank share prices restrict ability to raise new capital

- Bank risk appetite has been significantly reduced

The global bank lending affected by:

PETROFIN RESEARCH

www.petrofin.gr

- Liquidity via the international money markets still constrained due to lack of counterpart confidence

A. Analysis and trends of global ship finance

- Unclear and uneven prospects for the global economy

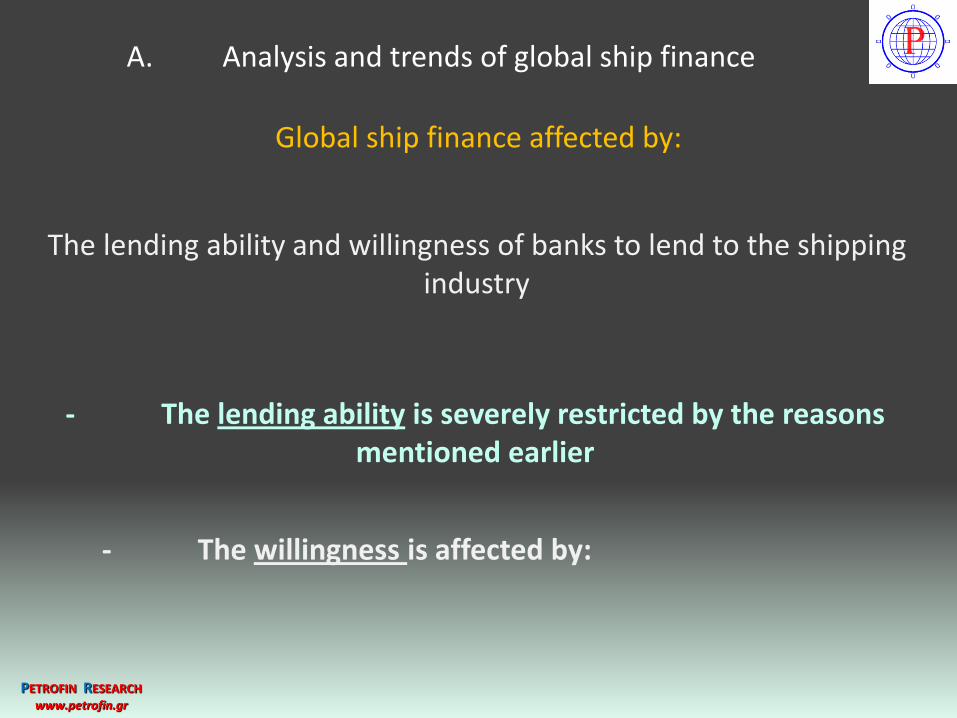

Global ship finance affected by:

PETROFIN RESEARCH

www.petrofin.gr

The lending ability and willingness of banks to lend to the shipping industry

A. Analysis and trends of global ship finance

- The lending ability is severely restricted by the reasons mentioned earlier

- The willingness is affected by:

Global ship finance affected by:

PETROFIN RESEARCH

www.petrofin.gr

A. Analysis and trends of global ship finance

• The uncertain prospects for the shipping industry, i.e. over capacity and cyclicality considerations

• Vessel prices and cashflows

• Quality of lenders’ existing loan portfolios, level of provisions and losses

• High loan margins and fees

Global ship finance affected by:

PETROFIN RESEARCH

www.petrofin.gr

A. Analysis and trends of global ship finance

• Risk / reward for lending to the shipping industry versus other sectors / lending opportunities

• Will ship finance banks re-lend what they receive via their loan portfolio run offs?

• Strict client selection

• High loan margins and fees

Global ship finance affected by:

PETROFIN RESEARCH

www.petrofin.gr

A. Analysis and trends of global ship finance

• Strict terms and financial covenants

• Competition among shipfinance lenders

• Level of loan to asset advances

• Availability of secured income

• Quoted vs. unquoted shipping borrowers

PETROFIN RESEARCH

www.petrofin.gr

B. Will there be finance for all?

The total fleet order book

PETROFIN RESEARCH

www.petrofin.gr

Order book

Delivery year World Merchant Fleet Number of vessels

2011

Total fleet 3016 Bulkers 1340 Tankers 207 Others 1469

2012

Total fleet 1654 Bulk Carriers 895

Tankers 121 Others 638

2013

Total fleet 458 Bulk Carriers 229

Tankers 53 Others 176

Overall total n/b orders 2011-2013 5128

Source: Clarksons - October 2010

B. Will there be finance for all?

PETROFIN RESEARCH

www.petrofin.gr

B. Will there be finance for all?

Conversions / cancellations; some estimates

Additional newbuilding orders

Can the demand for newbuilding finance be accommodated?

PETROFIN RESEARCH

www.petrofin.gr

B. Will there be finance for all?

PETROFIN RESEARCH

www.petrofin.gr

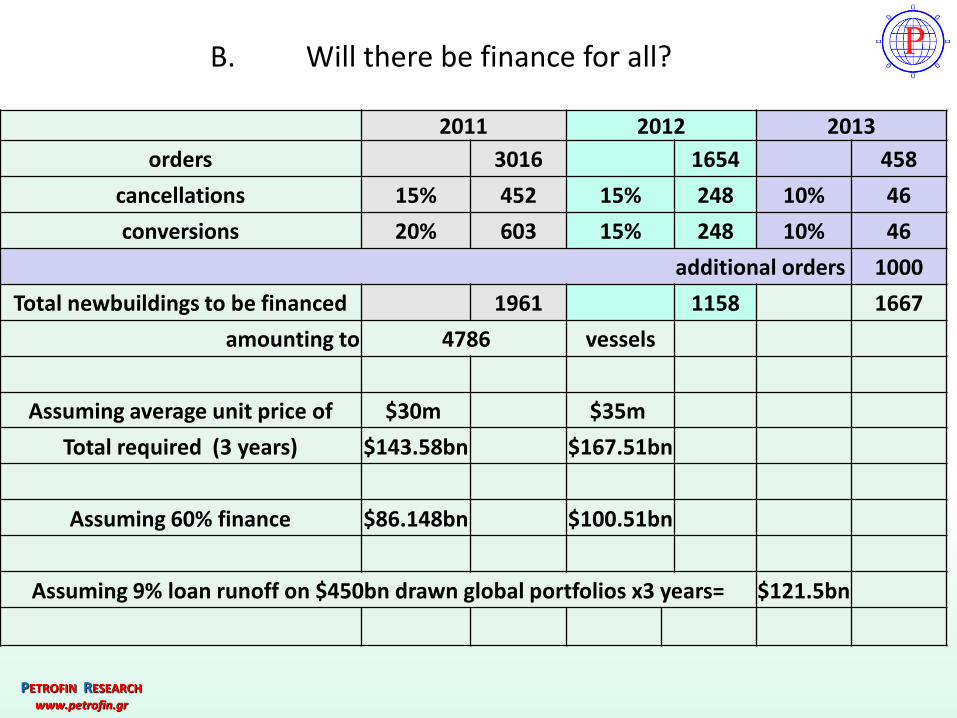

2011 2012 2013

orders 3016 1654 458

cancellations 15% 452 15% 248 10% 46

conversions 20% 603 15% 248 10% 46

additional orders 1000

Total newbuildings to be financed 1961 1158 1667

amounting to 4786 vessels

Assuming average unit price of $30m $35m

Total required (3 years) $143.58bn $167.51bn

Assuming 60% finance $86.148bn $100.51bn

Assuming 9% loan runoff on $450bn drawn global portfolios x3 years= $121.5bn

B. Will there be finance for all?

PETROFIN RESEARCH

www.petrofin.gr

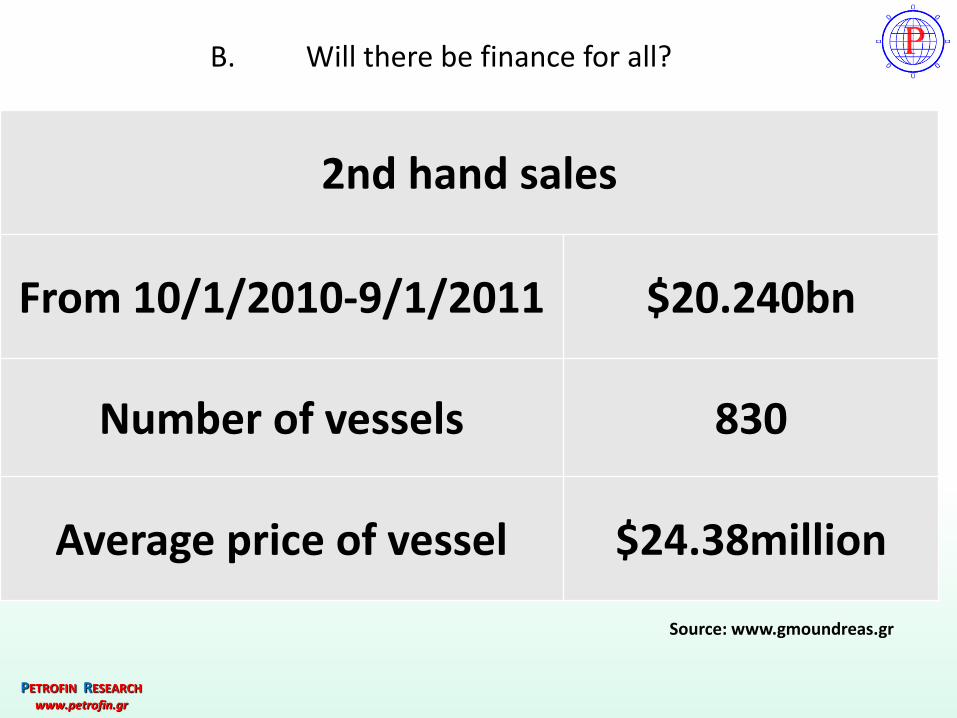

2nd hand sales

From 10/1/2010-9/1/2011 $20.240bn

Number of vessels 830

Average price of vessel $24.38million

Source: www.gmoundreas.gr

B. Will there be finance for all?

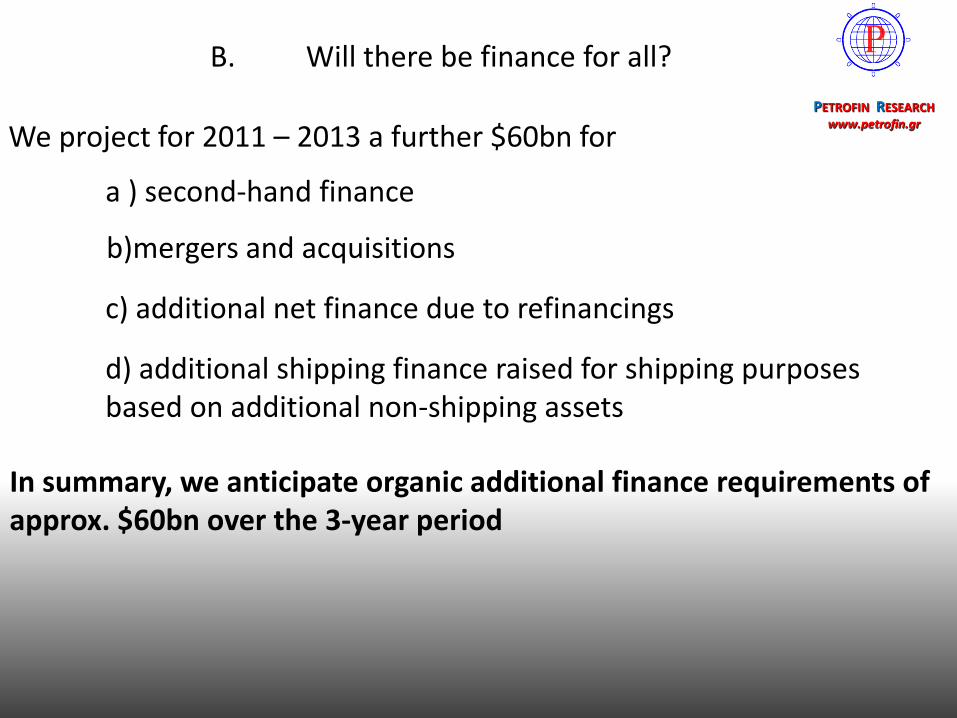

We project for 2011 – 2013 a further $60bn for

a ) second-hand finance

b)mergers and acquisitions

c) additional net finance due to refinancings

d) additional shipping finance raised for shipping purposes based on additional non-shipping assets

In summary, we anticipate organic additional finance requirements of approx. $60bn over the 3-year period

PETROFIN RESEARCH

www.petrofin.gr

B. Will there be finance for all?

Consequently, the total ship finance requirements in excess of loan run-offs of the 3-year period for both newbuildings and organic shipping finance is expected be between 5% and 7.8% of global ship finance ($25 to $39bn) over the 3-year period.

The question remains, though, will ship finance banks re-lend the estimated $121.5bn over 2011-13 to shipping, in the first place?

PETROFIN RESEARCH www.petrofin.gr

B. Will there be finance for all?

Greek ship finance – presenting the latest Petrofin Bank Research as of end 2010, released April 2011

PETROFIN RESEARCH

www.petrofin.gr

C. Petrofin Bank Research for Greek ship finance

$0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000

Royal Bank of Scotland

Deutsche Schiffsbank

Credit Suisse*

HSH Nordbank*

National Bank of Greece

DNB Nor

Emporiki Bank

DB - Deutsche shipping

Marfin Egnatia

Alpha Bank

$11,288

$5,007

$3,500

$2,881

$2,545

$2,297

$2,126

$2,439

$2,181

$2,120

$1,151

$549

$1,000

$241

$459

$580

$604

$174

$302

$350

Drawn Loans

Committed but Undrawn Loans

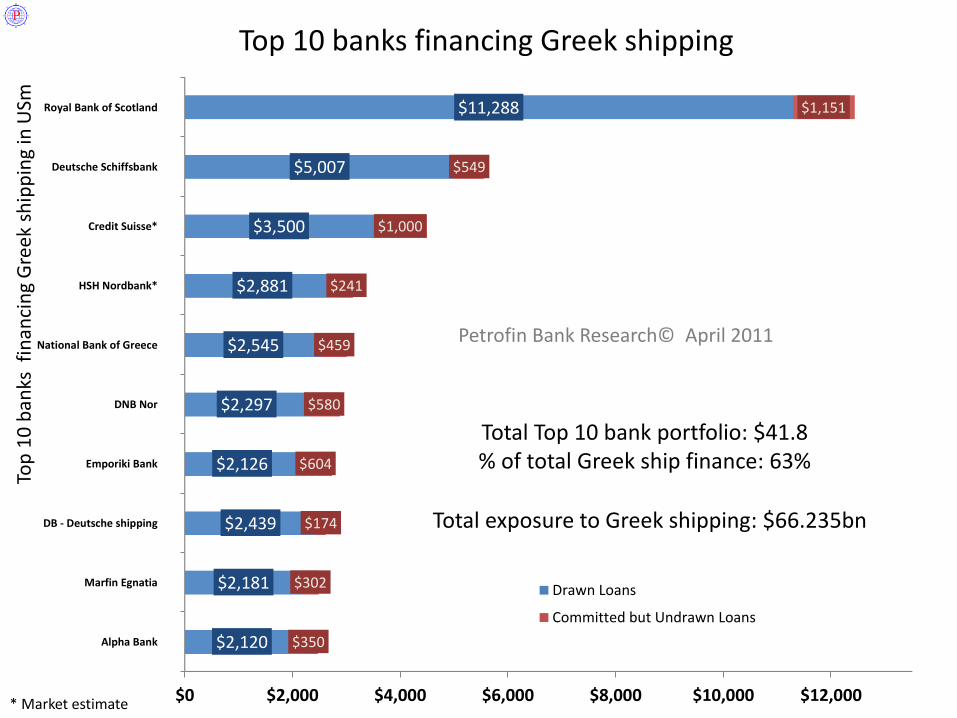

Total exposure to Greek shipping: $66.235bn

Total Top 10 bank portfolio: $41.8 % of total Greek ship finance: 63%

Petrofin Bank Research© April 2011

* Market estimate

Top

10

ban

ks f

inan

cin

g G

reek

sh

ipp

ing

in U

Sm

Top 10 banks financing Greek shipping

* Market estimate

All

ban

ks f

inan

cin

g G

reek

sh

ipp

ing

in U

Sm

$0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000

Royal Bank of Scotland

Deutsche Schiffsbank

Credit Suisse*

HSH Nordbank*

National Bank of Greece

DNB Nor

Emporiki Bank

DB - Deutsche shipping

Marfin Egnatia

Alpha Bank

HSBC

BNP Paribas

DVB

Calyon*

Piraeus Bank*

Unicredit

EFG Eurobank

LBG Shipping Finance

Nordea

Citibank

Bremer Landesbank

First Business Bank

Nord LB

CHINA EXIM*

KFW*

Natixis

ING

KEXIM*

Bank of Cyprus

ABN AMRO (Fortis Bank Netherlands)

Aegean Baltic

Proton Bank

Beremberg*

Bank of Ireland

Deka*

Tbank - ex Aspis Bank

Agricultural Bank of Greece

Santander (ex Alliance and Leicester)

Corner*

$11,288

$5,007

$3,500

$2,881

$2,545

$2,297

$2,126

$2,439

$2,181

$2,120

$1,900

$1,980

$2,080

$1,500

$1,870

$1,701

$1,211

$1,272

$1,050

$780

$449

$663

$525

$500

$333

$442

$402

$200

$360

$304

$291

$202

$200

$161

$100

$81

$66

$50

$25

$1,151

$549

$1,000

$241

$459

$580

$604

$174

$302

$350

$400

$264

$94

$500

$130

$183

$199 $89

$300

$160

$454

$25

$162

$150 $225

$16

$0

$200

$16

$42

$36

$18

$50

$30

Drawn Loans Committed but undrawn loans

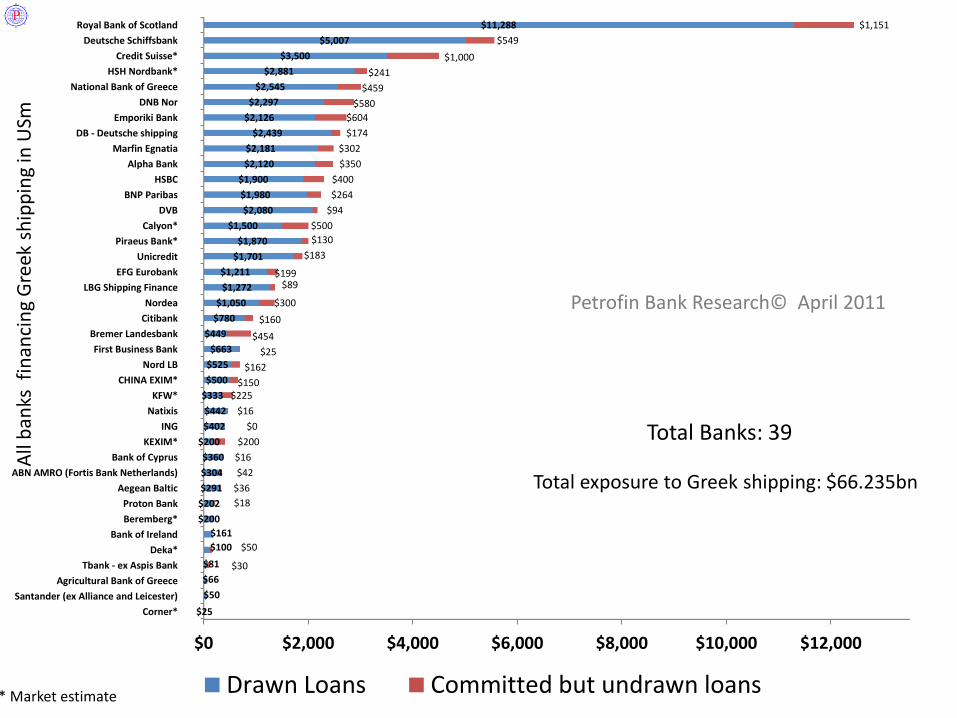

Total exposure to Greek shipping: $66.235bn

Total Banks: 39

Petrofin Bank Research© April 2011

PETROFIN RESEARCH

www.petrofin.gr

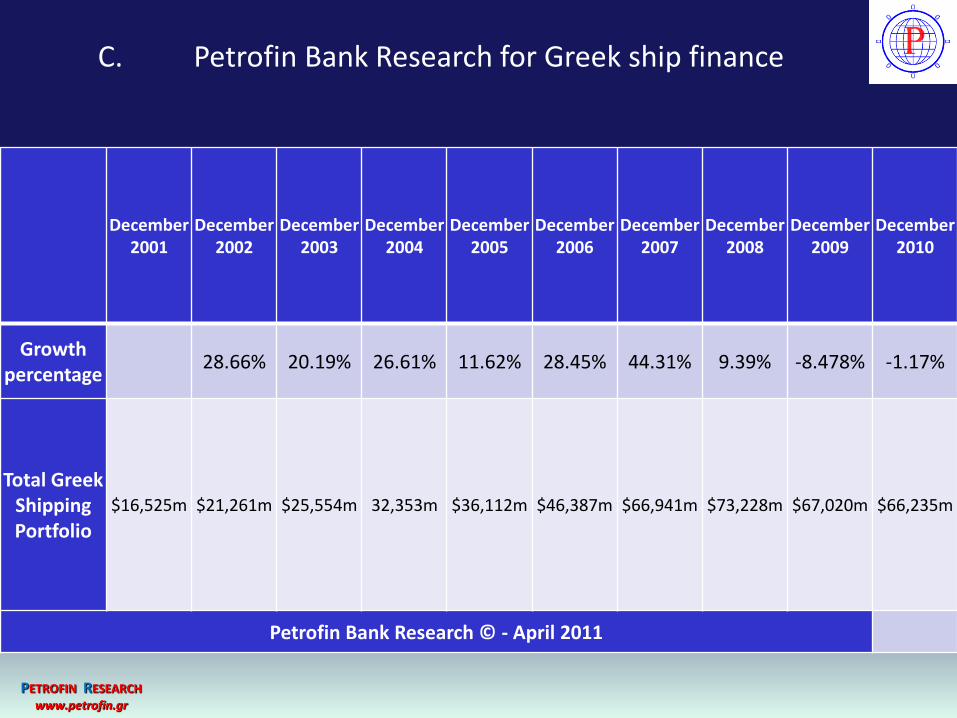

December

2001 December

2002 December

2003 December

2004 December

2005 December

2006 December

2007 December

2008 December

2009 December

2010

Growth percentage

28.66% 20.19% 26.61% 11.62% 28.45% 44.31% 9.39% -8.478% -1.17%

Total Greek Shipping Portfolio

$16,525m $21,261m $25,554m 32,353m $36,112m $46,387m $66,941m $73,228m $67,020m $66,235m

Petrofin Bank Research © - April 2011

C. Petrofin Bank Research for Greek ship finance

PETROFIN RESEARCH

www.petrofin.gr

Petrofin Bank Research © April 2011

Overall Greek ship lending portfolio as of end 2010

Overall Greek ship lending portfolio as of end 2009

Overall Greek ship lending portfolio as of end 2008

Percentage of growth between December 2009 and December

2010

Percentage of growth between December 2008 and December

2009

Percentage of growth between December 2001 and December

2010

Average yearly growth since 2001

International Banks WITH a

Greek presence

$35,882.29 $36,777.31 $38,984.4 -2.43% -5.66% 408.97%

(Between 2001 and 2009: 421.66%)

19.82% (Between 2001 and

2009: 22.93%)

International Banks

WITHOUT a Greek

presence

$14,468.76 $14,101.65 $17.299.5 +2.60% -18.49% 134.69%

(Between 2001 and 2009: 128.74%)

9.94% (Between 2001 and

2009: 10.9%)

Greek banks $15,883.60 $16,140.55 $16,944.24 -1.59% -4.74% 379.87%

(Between 2001 and 2009: 387.63%)

19.04% (Between 2001 and

2009: 21.9%)

Total $66,234.65 $67,019.51 $73,228.14 -1.17% -8.48% 300.81%

(Between 2001 and 2009: 305.56%)

16.68% (Between 2001 and

2009: 19.13%)

Petrofin Bank Research © - April 2011

C. Petrofin Bank Research for Greek ship finance

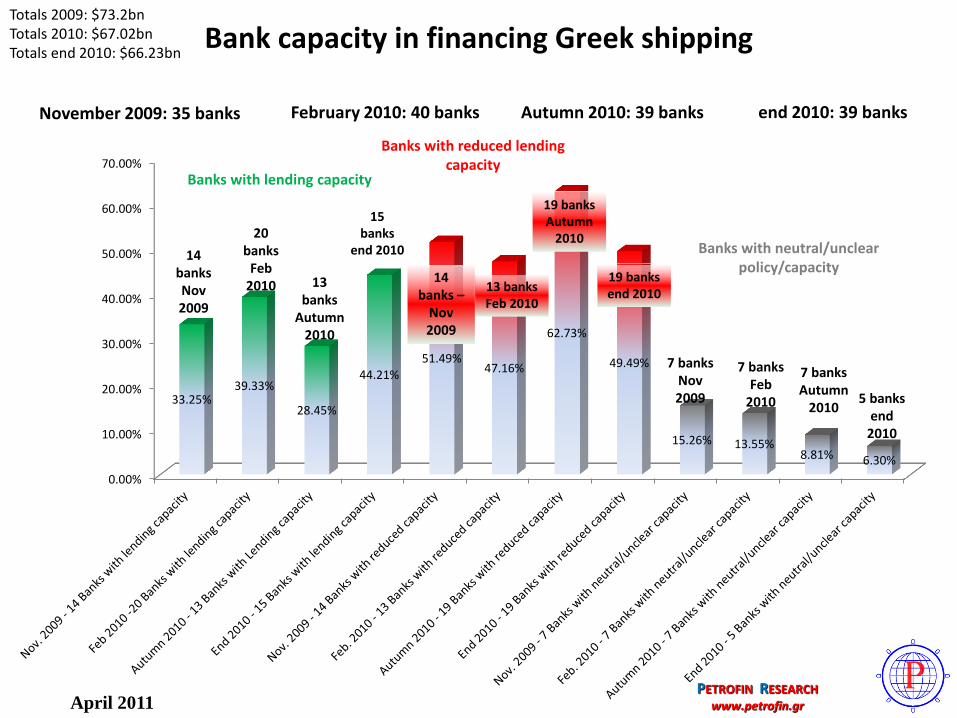

Bank capacity in financing Greek shipping

November 2009: 35 banks February 2010: 40 banks Autumn 2010: 39 banks

Totals 2009: $73.2bn Totals 2010: $67.02bn Totals end 2010: $66.23bn

April 2011 PETROFIN RESEARCH

www.petrofin.gr

end 2010: 39 banks

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

33.25% 39.33%

28.45%

44.21% 51.49%

47.16%

62.73%

49.49%

15.26% 13.55% 8.81% 6.30%

14 banks Nov 2009

20 banks

Feb 2010 13

banks Autumn

2010

15 banks

end 2010

14 banks –

Nov 2009

13 banks Feb 2010

19 banks Autumn

2010

19 banks end 2010

Banks with neutral/unclear policy/capacity

7 banks Nov 2009

7 banks Feb

2010

7 banks Autumn

2010 5 banks

end 2010

Banks with reduced lending capacity

Banks with lending capacity

PETROFIN RESEARCH

www.petrofin.gr

C. Petrofin Bank Research for Greek ship finance

Trends and expectations for Greek ship finance over the next 3 years

PETROFIN RESEARCH

www.petrofin.gr

C. Petrofin Bank Research for Greek ship finance

Greek ship finance has been adversely affected by

1) Reliance on western banks, which have an overall limited ability to maintain lending / expand

2) Difficult position of Greek banks due to the Greek Economic crisis

3) Difficulties faced by some of the lending banks to the Greek sector

PETROFIN RESEARCH

www.petrofin.gr

C. Petrofin Bank Research for Greek ship finance

Greek ship finance has been adversely affected by

4) Absence of new banks (other than Far Eastern banks)

5) Uncertain prospects for the shipping industry

6) Concern over future vessel values and future cashflows affecting banks’ loan portfolios

PETROFIN RESEARCH

www.petrofin.gr

C. Petrofin Bank Research for Greek ship finance

However,

1. Greek shipping has been remarkably free of shipping company failures

2. Greek owners are proving adept to coping with shipping crises

3. Greece’s confidence in shipping remains strong

4. Greek shipping still cashflow positive

5. Bank loan portfolios for Greek shipping still strong

6. Current tight Greek ship finance conditions enhance bank loan yields and ability to obtain stricter terms / financial covenants

PETROFIN RESEARCH

www.petrofin.gr

C. Petrofin Bank Research for Greek ship finance

However,

7. Loan to asset new advances remain attractively low

8. Banks able to select clients / loan transactions

9. Greek shipping’s cash reserves an attractive consideration for banks

10. Credit relationships between banks and Greek borrowers remain strong and mutually supportive

11. Greek shipping sector remains attractive in relation to other potential lending sectors

Other providers of debt and equity; alternative finance, private capital, the role of public companies

PETROFIN RESEARCH

www.petrofin.gr

D. Additional sources of ship finance

PETROFIN RESEARCH

www.petrofin.gr

Listed Companies - as of January 2011

from Newsfront GSI - 1st April 2011

1 Aegean Marine US 15 Goldenport UK

2 Baltic Trading (BALT) US 16 Hellenic Carriers UK

3 Capital Product US 17 Navios Holdings US

4 Costamare Inc US 18 Navios Marit Acquis US

5 Crude Carriers US 19 Navios Marit Partners US

6 Diana Shipping US 20 Newlead Holdings US

7 Dry Ships (DRYS) US 21 Oceanfreight US

8 Eagle Bulk Shipping US 22 Omega Navigation US

9 Euroseas Ltd US 23 OSG Ship Mngt (GR) US

10 Excel Maritime US 24 Paragon Shipping US

11 Freeseas US 25 Safe Bulkers US

12 Genco Ship & Trading US 26 Seanergy Maritime US

13 Genmar US 27 Star Bulk Carriers US

14 Globus Maritime US 28 Stealthgas US

29 TEN US

30 Top Ships US

31 Torm US

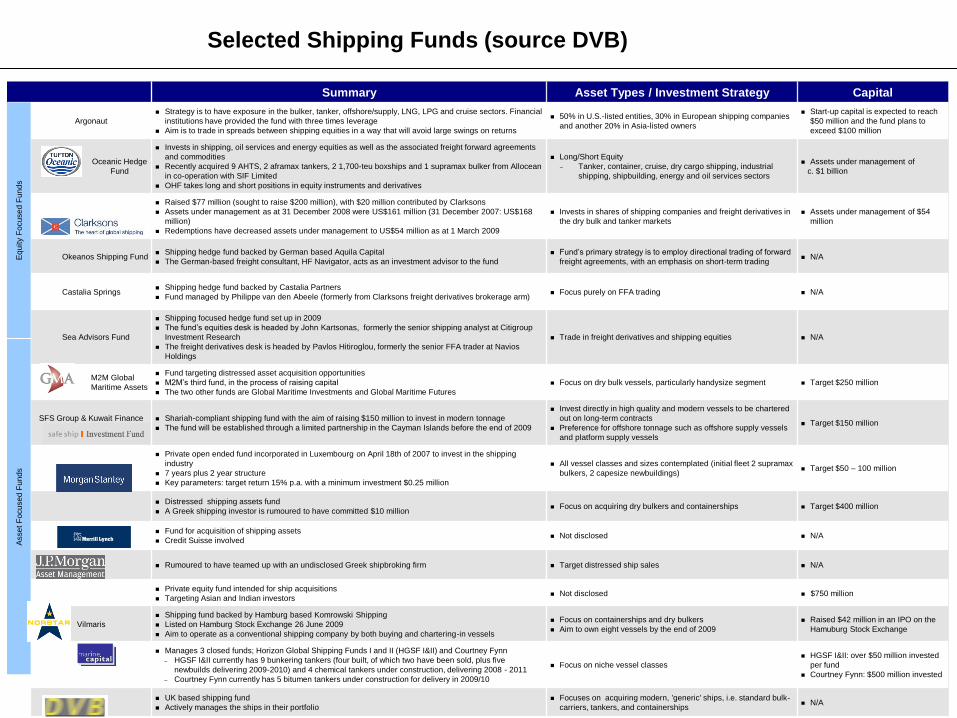

Selected Shipping Funds (source DVB)

Summary Asset Types / Investment Strategy Capital

Argonaut

Strategy is to have exposure in the bulker, tanker, offshore/supply, LNG, LPG and cruise sectors. Financial

institutions have provided the fund with three times leverage

Aim is to trade in spreads between shipping equities in a way that will avoid large swings on returns

50% in U.S.-listed entities, 30% in European shipping companies

and another 20% in Asia-listed owners

Start-up capital is expected to reach

$50 million and the fund plans to

exceed $100 million

Oceanic Hedge

Fund

Invests in shipping, oil services and energy equities as well as the associated freight forward agreements

and commodities

Recently acquired 9 AHTS, 2 aframax tankers, 2 1,700-teu boxships and 1 supramax bulker from Allocean

in co-operation with SIF Limited

OHF takes long and short positions in equity instruments and derivatives

Long/Short Equity

– Tanker, container, cruise, dry cargo shipping, industrial

shipping, shipbuilding, energy and oil services sectors

Assets under management of

c. $1 billion

Raised $77 million (sought to raise $200 million), with $20 million contributed by Clarksons

Assets under management as at 31 December 2008 were US$161 million (31 December 2007: US$168

million)

Redemptions have decreased assets under management to US$54 million as at 1 March 2009

Invests in shares of shipping companies and freight derivatives in

the dry bulk and tanker markets

Assets under management of $54

million

Okeanos Shipping Fund Shipping hedge fund backed by German based Aquila Capital

The German-based freight consultant, HF Navigator, acts as an investment advisor to the fund

Fund’s primary strategy is to employ directional trading of forward

freight agreements, with an emphasis on short-term trading N/A

Castalia Springs Shipping hedge fund backed by Castalia Partners

Fund managed by Philippe van den Abeele (formerly from Clarksons freight derivatives brokerage arm) Focus purely on FFA trading N/A

Sea Advisors Fund

Shipping focused hedge fund set up in 2009

The fund’s equities desk is headed by John Kartsonas, formerly the senior shipping analyst at Citigroup

Investment Research

The freight derivatives desk is headed by Pavlos Hitiroglou, formerly the senior FFA trader at Navios

Holdings

Trade in freight derivatives and shipping equities N/A

M2M Global

Maritime Assets

Fund targeting distressed asset acquisition opportunities

M2M’s third fund, in the process of raising capital

The two other funds are Global Maritime Investments and Global Maritime Futures

Focus on dry bulk vessels, particularly handysize segment Target $250 million

SFS Group & Kuwait Finance

House

Shariah-compliant shipping fund with the aim of raising $150 million to invest in modern tonnage

The fund will be established through a limited partnership in the Cayman Islands before the end of 2009

Invest directly in high quality and modern vessels to be chartered

out on long-term contracts

Preference for offshore tonnage such as offshore supply vessels

and platform supply vessels

Target $150 million

Private open ended fund incorporated in Luxembourg on April 18th of 2007 to invest in the shipping

industry

7 years plus 2 year structure

Key parameters: target return 15% p.a. with a minimum investment $0.25 million

All vessel classes and sizes contemplated (initial fleet 2 supramax

bulkers, 2 capesize newbuildings) Target $50 – 100 million

Distressed shipping assets fund

A Greek shipping investor is rumoured to have committed $10 million Focus on acquiring dry bulkers and containerships Target $400 million

Fund for acquisition of shipping assets

Credit Suisse involved Not disclosed N/A

Rumoured to have teamed up with an undisclosed Greek shipbroking firm Target distressed ship sales N/A

Private equity fund intended for ship acquisitions

Targeting Asian and Indian investors Not disclosed $750 million

Vilmaris

Shipping fund backed by Hamburg based Komrowski Shipping

Listed on Hamburg Stock Exchange 26 June 2009

Aim to operate as a conventional shipping company by both buying and chartering-in vessels

Focus on containerships and dry bulkers

Aim to own eight vessels by the end of 2009

Raised $42 million in an IPO on the

Hamuburg Stock Exchange

Manages 3 closed funds; Horizon Global Shipping Funds I and II (HGSF I&II) and Courtney Fynn

– HGSF I&II currently has 9 bunkering tankers (four built, of which two have been sold, plus five

newbuilds delivering 2009-2010) and 4 chemical tankers under construction, delivering 2008 - 2011

– Courtney Fynn currently has 5 bitumen tankers under construction for delivery in 2009/10

Focus on niche vessel classes

HGSF I&II: over $50 million invested

per fund

Courtney Fynn: $500 million invested

UK based shipping fund

Actively manages the ships in their portfolio

Focuses on acquiring modern, 'generic' ships, i.e. standard bulk-

carriers, tankers, and containerships N/A

Eq

uity F

ocu

se

d F

un

ds

Asse

t F

ocu

se

d F

un

ds

Conclusions

PETROFIN

RESEARCH

www.petrofin.gr

1. Global ship finance conditions to gradually ease over the next few years, as western bank confidence, liquidity and capital adequacy returns.

2. Greek ship finance to remain tight for 2011/2012 but to start easing thereafter, due to

a. The recovery and strengthening of the western banks

b. The growth of Far East lending

c. The anticipated recovery of the Greek banks

d. The expected influx of new lenders

e. The possible easing of overcapacity concerns and

f. The return of market equilibrium and the recovery of vessel values and freight rates

Conclusions, cont.

PETROFIN

RESEARCH

www.petrofin.gr

3. Tight lending conditions affecting particularly small to medium shipping companies shall persist until intense bank competition shall return

4. Ship finance lending conditions and appetite shall be affected by the length and severity of the current slump affecting vessel values and freight rates, as well as the recovery prospects for global shipping

PETROFIN

RESEARCH

www.petrofin.gr