proposed takeover directive and reforms ofeuropean corporate law professor joseph a. mccahery...

TRANSCRIPT

Proposed Takeover Directive and Reforms ofEuropean Corporate Law

Professor Joseph A. McCahery

Tilburg University, TILEC & Research Fellow, ECGI

Outline

• Winter I: Level Playing Field for Takeovers

• Draft Directive on Takeover Bids

• Fair Compensation Approach for Holders of Dual Class Shares

• Winter II

• Conclusion

Winter Committee Proposal on Takeover Bids

• Aim: to create a level playing field for takeover bids

• In absence of efficient capital markets, two general rules are required—– Shareholder decision-making (Art 9)– Proportionality between risk bearing and control;

holder of majority of risk decides (new rule proposed)

• Pre-bid measures--differentiated voting rights, voting caps, golden shares, voting trusts, etc. inconsistent with two legal principles

Article 9: Problem of Frustrating Actions

• HLG endorsed EC position that boards should be neutral after bid is announced

• Prior shareholder approval necessary for frustrating actions

• Scope of board action—board sets out option on bid; may seek other bids

• Art 9 alone insufficient to ensure that principle of proportionality (between risk-bearing and control) is adhered to once bid is made public

Break-through Rule

• All holders of risk-bearing capital attend AGM to vote in proportion to holdings

• Aim: allows bidder, upon acquisition of 75% of cash flow rights, to remove any barriers to takeover

• Two sub-rules—designed to eliminate:• 1) Provisions preventing exercise of proportional

voting rights• 2) Provisions that limit exercise of internal affairs

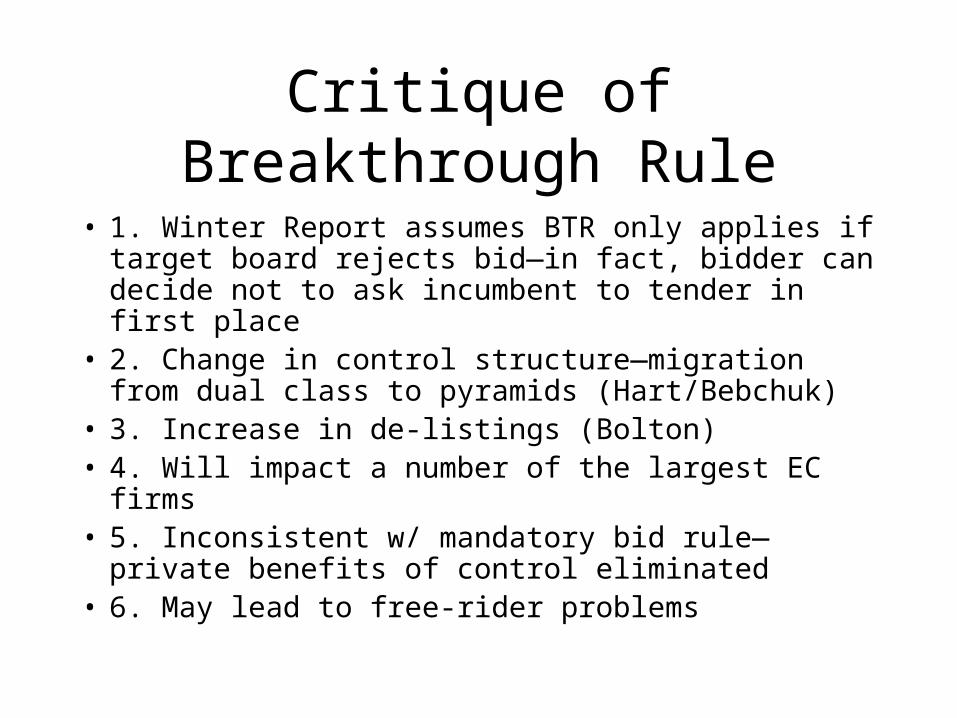

Critique of Breakthrough Rule

• 1. Winter Report assumes BTR only applies if target board rejects bid—in fact, bidder can decide not to ask incumbent to tender in first place

• 2. Change in control structure—migration from dual class to pyramids (Hart/Bebchuk)

• 3. Increase in de-listings (Bolton)• 4. Will impact a number of the largest EC firms• 5. Inconsistent w/ mandatory bid rule—private

benefits of control eliminated • 6. May lead to free-rider problems

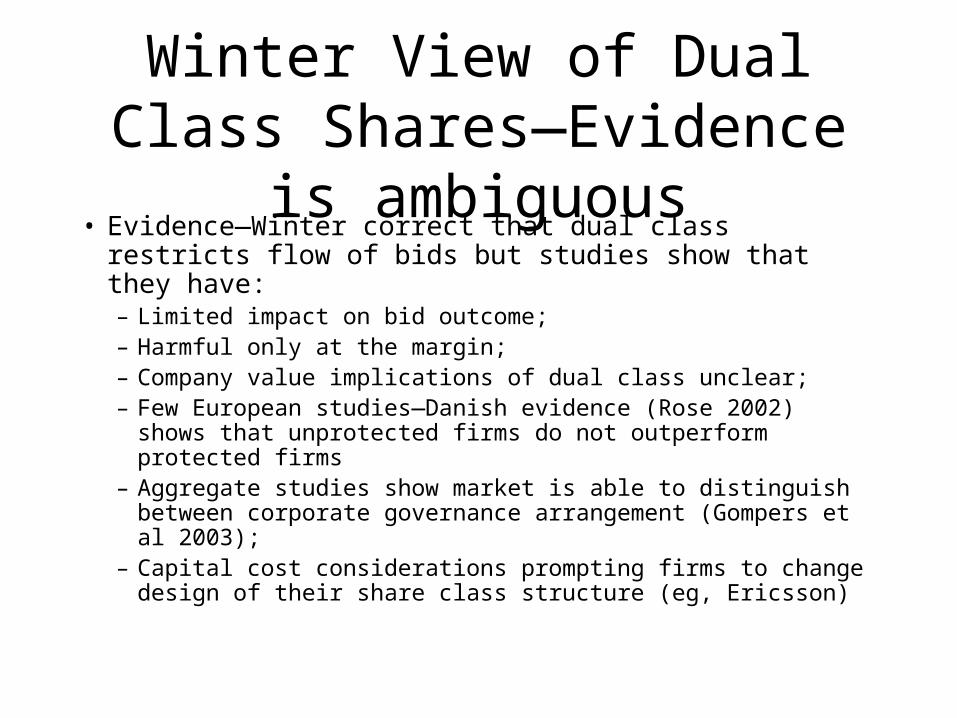

Winter View of Dual Class Shares—Evidence is ambiguous

• Evidence—Winter correct that dual class restricts flow of bids but studies show that they have:– Limited impact on bid outcome;– Harmful only at the margin;– Company value implications of dual class unclear;– Few European studies—Danish evidence (Rose 2002) shows

that unprotected firms do not outperform protected firms– Aggregate studies show market is able to distinguish

between corporate governance arrangement (Gompers et al 2003);

– Capital cost considerations prompting firms to change design of their share class structure (eg, Ericsson)

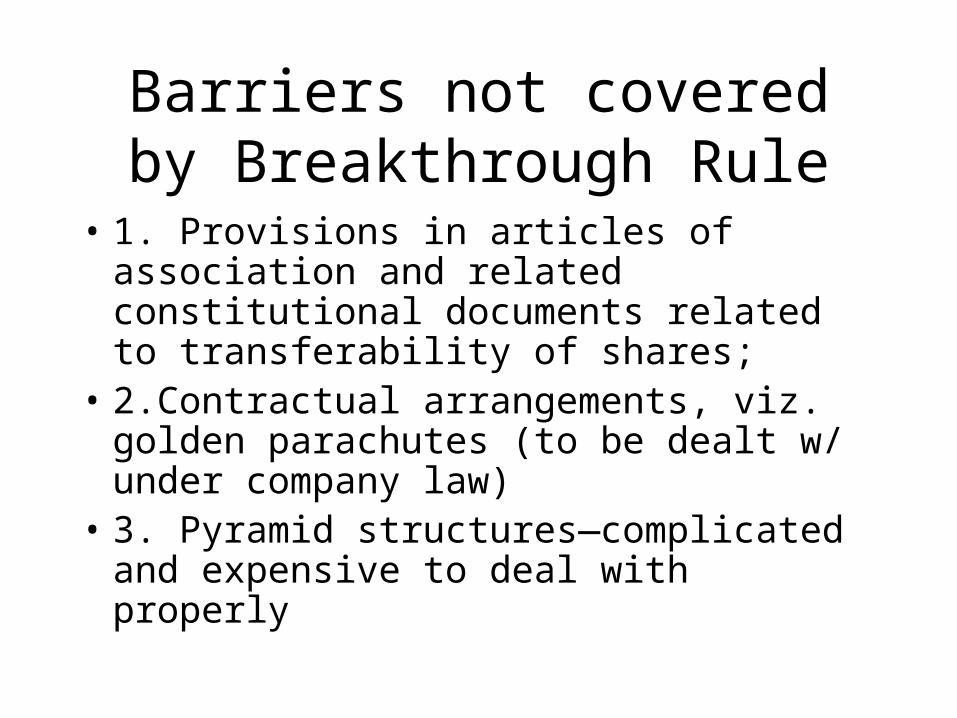

Barriers not covered by Breakthrough Rule

• 1. Provisions in articles of association and related constitutional documents related to transferability of shares;

• 2.Contractual arrangements, viz. golden parachutes (to be dealt w/ under company law)

• 3. Pyramid structures—complicated and expensive to deal with properly

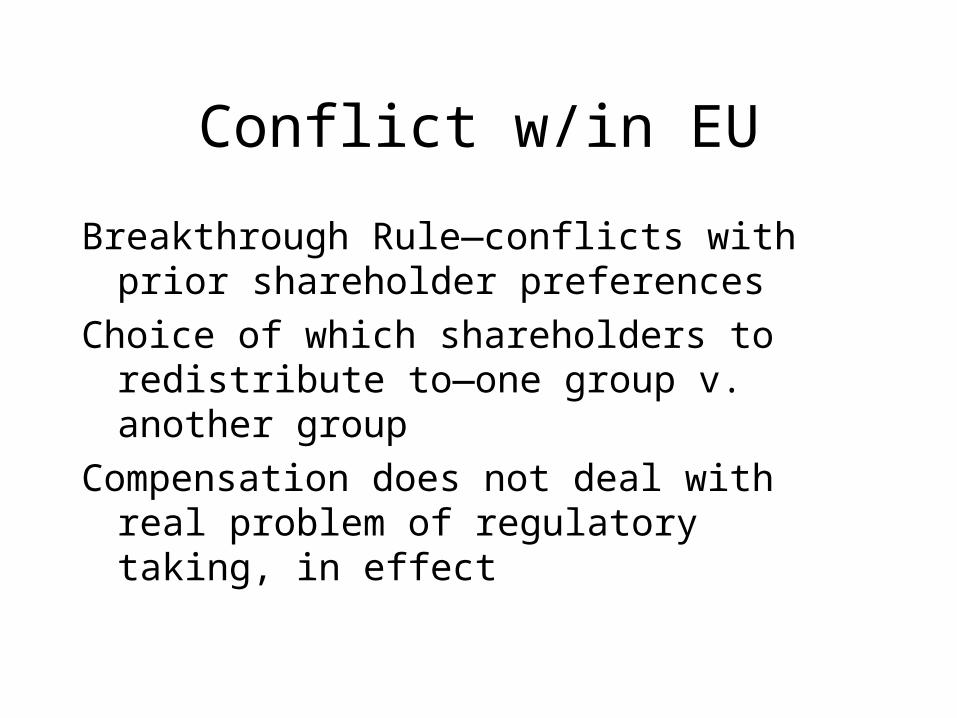

Conflict w/in EU

Breakthrough Rule—conflicts with prior shareholder preferences

Choice of which shareholders to redistribute to—one group v. another group

Compensation does not deal with real problem of regulatory taking, in effect

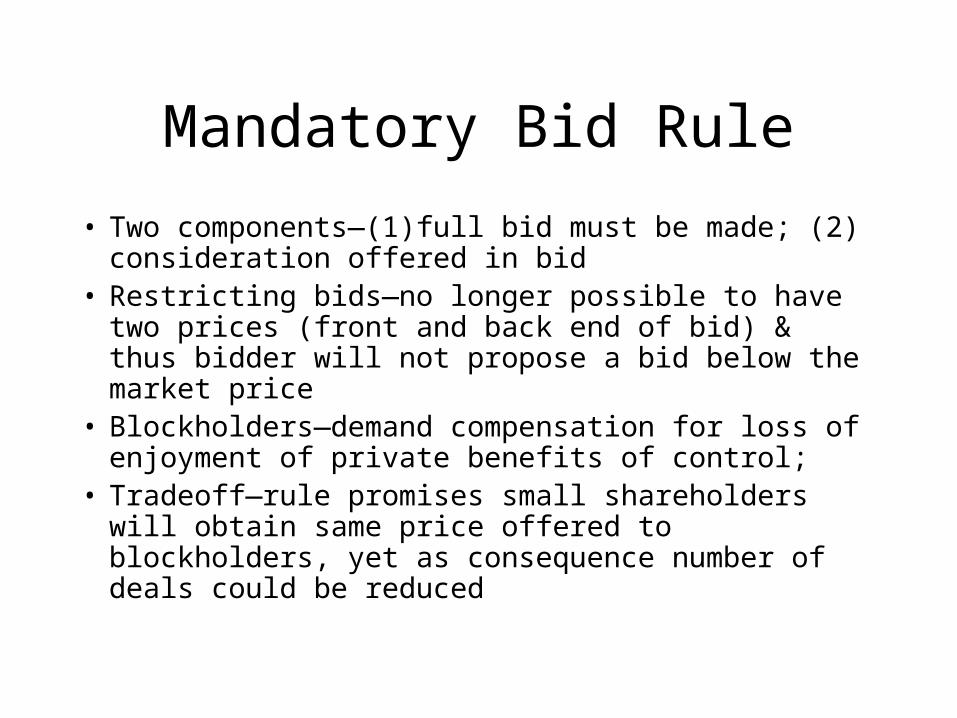

Mandatory Bid Rule

• Two components—(1)full bid must be made; (2) consideration offered in bid

• Restricting bids—no longer possible to have two prices (front and back end of bid) & thus bidder will not propose a bid below the market price

• Blockholders—demand compensation for loss of enjoyment of private benefits of control;

• Tradeoff—rule promises small shareholders will obtain same price offered to blockholders, yet as consequence number of deals could be reduced

Squeeze and sell out rights

• Squeeze out threshold (right to by minority shares to be exercised): 90% or 95% of capital (also where there are several classes of securities)

• Sell-out rights: 90% threshold triggers undertaking that would allow minority shareholders to request their shares to be acquired

Critique of Winter I

• Art 9—severe restrictions on defensive measures will limit auctioning of firms; also leave certain firms exposed (US-EU level playing field considerations);

• Breakthrough rule—question of compensation (Sweden—European Court of Human rights issue)

• Volkswagen statute—special statute should not be set aside

Proposed Directive on Takeover Bids (Oct. 2, 2002)

• Provides for:• Strict board neutrality on part of target board• Mini-breakthrough rules that stipulate that during

period of acceptance any restrictions on transfer of securities in Articles or contractual arrangements are not enforceable

• Set of disclosure rules• Squeeze out and sell out rules

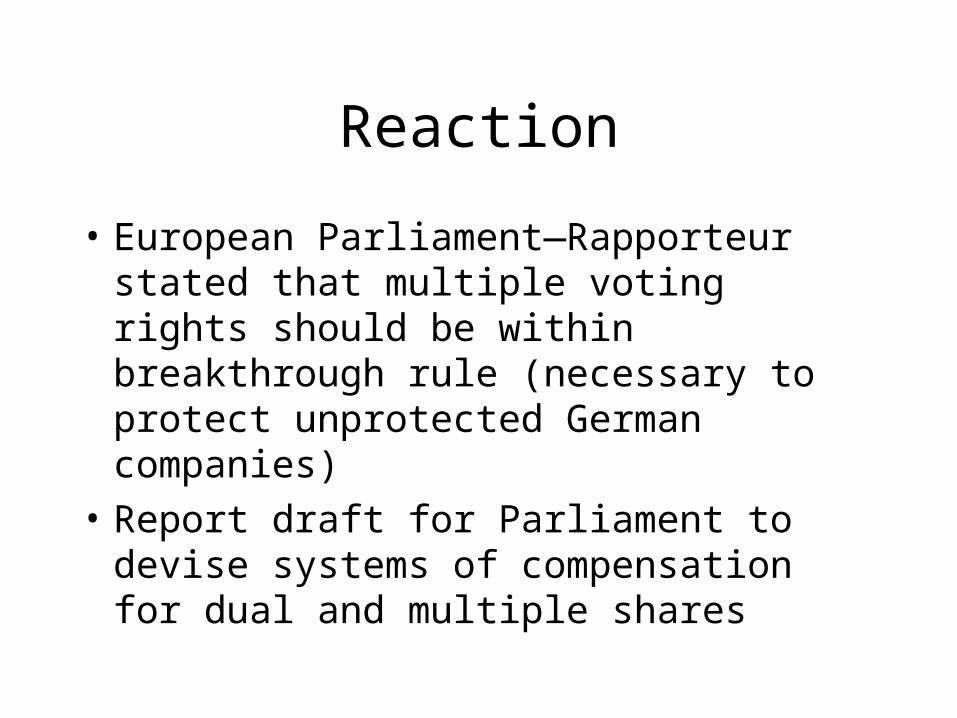

Reaction

• European Parliament—Rapporteur stated that multiple voting rights should be within breakthrough rule (necessary to protect unprotected German companies)

• Report draft for Parliament to devise systems of compensation for dual and multiple shares

Proponents of BTR

• EP Study (2003): multiple voting rights should be within scope of BTR

• Justifications:• 1) dual class shares are designed primarily

to block takeovers;• 2) Aim of EC legislation is to enhance legal

certainty and takeovers which dual and multiple class shares deny

Fair Compensation Proposal—EP Study (Jan. 2003)

• Concept of fair Compensation for holders of dual class shares (rule out by Winter Report)

• Compensation Approaches:• 1) based on difference between ordinary and

voting shares—use average premium paid on dual class shares

• 2) But fair price does not have to be market price• 3) Adopt average of premiums—between 10%-

20%: 15% (EU average 14% Dyck & Zingales 2002)

Critique

• Premiums range from 80% to 5% across EU• Compensation rule reverses causality—premiums

would move toward 15%• Case by case approach (default rule of EP)• -creates legal uncertainty;• -higher legal costs• -a flexible approach—delegated to MS--would

better meet the needs of diverse firms and member states

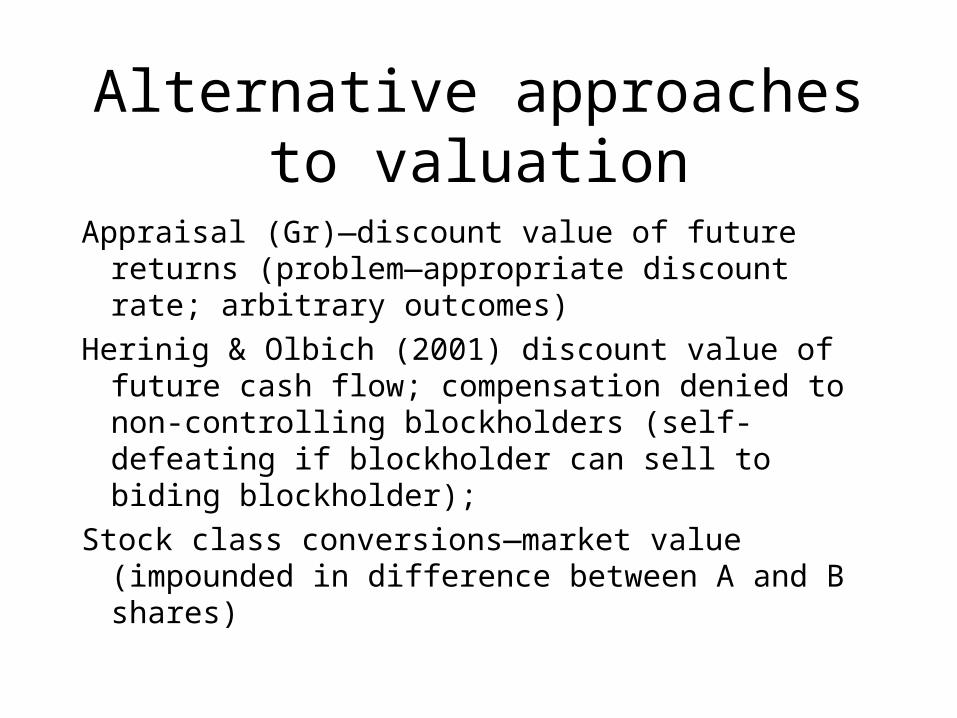

Alternative approaches to valuation

Appraisal (Gr)—discount value of future returns (problem—appropriate discount rate; arbitrary outcomes)

Herinig & Olbich (2001) discount value of future cash flow; compensation denied to non-controlling blockholders (self-defeating if blockholder can sell to biding blockholder);

Stock class conversions—market value (impounded in difference between A and B shares)

Board Neutrality—Commission’s proposal requires affirmative

vote• Commission correctly favors shareholder voting

as a means to allow shareholders the opportunity to accept bid or not;

• Shareholders are better informed after bid and have incentives to analyze its effects;

• Limits the potential coercive effect of a bid;• Allows for more than passivity in face of bid• Simple coordination approach is better than

complex rules which provide conficting signals about limits of ex post board intervention

Conflict with Germany

• Art 33 German Takeover Code—permits post bid intervention

• Exceptions—actions that would have been taken in interests of company & actions to which supervisory board has agreed

• Scope of Art 33—actions taken by supervisory board

• Pre-bid actions—reserve authorizations, share repurchases

• Conflict w/ Art 9—Commission wants simple rule

Proposal—UK/Germany compromise

Open issues

• Level playing field—US v. Europe (rescind Art 9—proposal)

• Volkswagen statute—second thoughts by Commission

• Golden Shares—Left out of directive (Gr. Wants back in)

Winter II

• Corporate Governance • 3.1 Annual report publishes corporate governance

rules and practices of firm• 3.2 Listed firms publish on website information

relevant to shareholders• 3.3 Companies should disclose how investors can

ask questions & how they will be answered• 3.4 Voting in absentia—direct vote or proxy

(electronic means)• 3.5 Attendance via electronic means

Recommendations

• 3.7 Institutional investors—disclose investment policy and policy w/r/t/ voting rights – --assumes that institutional investor voting

matters ( for dissenting view Cf. Romano 2002)– If investors have 5-10 % can apply to court for

special investigation (3.8)

Board Structure & non-Execs.

• Firms should have option to select single or dual board structure (consistent with Euro Company Statute)

• 3.10 Listed firms ensure that nomination and payment of directors & audit decided by non-execs or supervisors who are indep.

• Principles of independence—list of relationships; publish in annual account directors that are independent; publish statement of board composition (qualifications, etc.)

Remuneration/Responsibilities

• 3.11 Disclosure of executive pay in detailed financial statements

• Executive pay linked to index should obtain prior shareholder approval

• Executive compensation should appear on balance sheet (no exemption for high tech)

• 3.12 Financial Statements—management responsible for financial and governance statements

• 3.13 Wrongful trading—liability • 3.14 Director sanctions—liability for filing misleading

statements, fines

Groups & Pyramids

• Law of Groups unnecessary

• Reform suggestions– Transparency of group structures– Tension between groups– Pyramid structures

Transparency

• Transparency not main issue

• Information: group structure, managing system, governance structure, rights & responsibilities

• Mandatory disclosure– Consolidated financial statements (7th Dir.

Accompanied by key information—intra-group services, etc; non-financial information