promoting export in least developed countries - artisan … · promoting export in least developed...

TRANSCRIPT

Promoting Export in Least Developed Countries:

Canadian Market Entry Strategy for Ethiopian Specialty Handloom Woven Textile

Products

Submitted by:

Tsegaye Ginbo Gatiso

Research Officer, Ethiopian Development Research Institute (EDRI)

Addis Ababa, Ethiopia; Cellphone: +251910695336; Email: [email protected]

Wondwossen Shiferaw Woldemichael

Senior Marketing Expert, Ethiopian Textile Industry Development Institute (ETIDI)

Addis Ababa, Ethiopia; Cellphone: +251961642679; Email: [email protected]

Submitted to:

Trade Facilitation of Office Canada (TFO Canada) and International Development Research

Center (IDRC)

September 2016

ii

Abstract

This study investigated practical strategies for exporting Ethiopian handloom specialty textiles

and fabric products to the Canadian market. It presents an overview of the sector taking the

demand and supply side factors into consideration. Following a thorough selection process, the

study identified 10 small and medium size enterprises (SMEs) using criteria such as product

quality, potential to expand production and export readiness. Moreover, the SMEs selection

process benefited from the consultation of Trade Facilitation Office Canada experts who

reviewed the company profiles developed for the study purpose. To gather the required data,

we conducted individual discussions with each company owner as well as focus group

discussion. The latter focused on the production, distribution and marketing processes in order

to determine the prospects and challenges that small enterprises face when exporting their

products to Canada and other international markets. In addition, the study reviewed the market

access challenges on the Canadian market for specialty textile products and for least developed

countries including Ethiopia. By matching the Canadian market demand to the supply of

Ethiopian handloom products, the study identified various handloom woven specialty products

categories namely home accessories, gift hand‐woven textiles, clothing, and fashion

accessories to export to Canada. The samples of these products from participated small

enterprises taken to Canada for the three‐city roadshow. Finally, the study developed both

indirect and direct exporting strategies considering the associated levels of commitment, risk,

control and profit potentials. The purpose of this study is that small enterprises selected for the

roadshow can use either or both the indirect and direct exporting strategies and establish long‐

term business relationships, joint venture schemes and direct investments with Canadian

buyers. Furthermore, for the purpose of immediate market linkages, the study recommended

that Ethiopian small enterprises venture into direct exporting through a Canadian based agent,

distributor or wholesaler as this would be a viable strategy for selected small sized exporters to

take advantage of low resource requirement, low controls.

iii

Table of contents

Abstract ......................................................................................................................................................... ii

List of tables ................................................................................................................................................. iv

List of figures ................................................................................................................................................. v

List of acronyms ........................................................................................................................................... vi

Chapter one: introduction .............................................................................................................................. 1

1.1. Background of the study ........................................................................................................... 1

1.2. Design and methodology of the study ....................................................................................... 1

Chapter two: an overview of textile and apparel market in Canada ............................................................. 4

2.1. Market for general textile and apparel products in Canada ...................................................... 4

2.2. Market for handloom woven textile and apparel products ........................................................ 6

2.3. Trends of textile and apparel imports in Canada ...................................................................... 6

2.4. Quality standards, price condition and distribution schemes .................................................... 8

2.5. Access to and requirements of export to the Canadian market ................................................ 9

Chapter three: the Ethiopian textile and garment industry sector overview ............................................... 11

3.1. An overview of the Ethiopian textile sector ............................................................................. 11

3.2. Handloom-weaving industry in Ethiopia .................................................................................. 12

3.3. Competitive advantage of Ethiopian handloom woven sub sector ......................................... 18

3.4. Local initiatives to promote handloom weaving in Ethiopia .................................................... 19

3.5. SWOT analysis of handloom weaving sector in Ethiopia ....................................................... 22

Chapter four: Canadian market penetration strategy .................................................................................. 27

4.1. Marketing strategy development approach ............................................................................. 27

4.2. Strategy for Ethiopian handloom woven products .................................................................. 30

4.2.1. Distribution channel ................................................................................................................. 30

4.2.2. Sector and products promotion strategy ................................................................................. 32

4.2.3. Product strategies ................................................................................................................... 33

4.2.4. Pricing strategy ...................................................................................................................... 34

4.2.5. Strategy for increasing production capacity ............................................................................ 36

4.2.6. Marketing strategy ................................................................................................................... 36

Chapter five: recommendations .................................................................................................................. 38

References .................................................................................................................................................. 42

Appendix 1: Selected exporters and their products .................................................................................... 44

iv

List of tables

Table 1: Economic indicators of Canadian textiles market 4

Table 2: Retail clothing sales in Canada by type 7

Table 3: Export share of handloom-weaving in the textile sector 12

Table 4: Major players based on their export performance 14

Table 5: Destinations for Ethiopian general textile and handloom woven

products

14

Table 6: Ethiopian handloom woven Export by product type and category 17

Table 7: SWOT analysis of handloom weaving sector in Ethiopia 23

Table 8: Selected potential exporters and products 29

Table 9: Identified products, size and price range 35

Table 10: Recommendations of the study with their responsible bodies 37

v

List of figures

Figure 1: Indicative study design 2

Figure 2: Retail clothing sales 5

Figure 3: Canadian import of fashion accessories 7

Figure 4: Imports of fashion accessory In Canada by product 8

Figure 5: Export performance of the sector 11

Figure 6: Distribution strategies of handloom weavers 13

Figure 7: Percentage share of Ethiopian handloom export products 15

Figure 8: Show production flow of an exporting company 16

Figure 9: Handloom woven products export by product type and category 18

Figure 10: Marketing strategy development design 28

Figure 11: Potential distribution channel for Entering Canadian market 31

vi

List of acronyms

AGOA African Growth and Opportunity Act

BDS Business Development Service

CGTA Canadian Gift & Tableware Association

CSA Central Statistics Authority of Ethiopia

EDGET Ethiopians Driving Growth through Entrepreneurship and Trade

ETIDI Ethiopian Textile Industry Development Institute

ETGAMA Ethiopian Textile and Garment Manufacturers' Association

FeMSEDA Federal Micro and Small Enterprise Development Agency

FOB Free on board

FTA Free Trade Agreements

GPT General Preferential Tariff

GTZ German Technical Cooperation Agency

IDRC International Development Research Center

LDCs Least Developed Countries

LDCT Least Developed Countries Tariff Rules of Origin

MFN Most Favored Nation Tariff

MOI Ethiopian Ministry of Industry

NGO Non-governmental organization

vii

ReMSEDA Addis Ababa, Micro and Small Enterprise Development Agency

SMEs Small and Medium Size Enterprises

TFO Canada Trade Facilitation Office Canada

UNIDO United Nation Industrial Development Organization

Chapter one: Introduction

1.1. Background of the study

The International Development Research Center (IDRC) and the Trade Facilitation Office Canada

(TFO Canada) have commissioned, in February 2016, market entry studies pertaining to

“Promoting Specialty Textile and Fabrics in Least Developed Countries (LDCs)”. The project aims

at analyzing ways to promote exports of specialty textile and fabrics from five developing countries

(Bangladesh, Cambodia, Uganda, Lesotho and Ethiopia) to Canada.

The overall objective of this study is to analyze feasible ways to promote exports of Ethiopian

specialty textile (handloom woven cotton) products to Canada. It will inform different stakeholders

including producers, traders, and policy makers about the characteristics of Ethiopian textile (with

a focus on handloom woven products) and the apparel sector in general, the strategic relevance

of the sector, practical challenges, and solutions to overcome barriers to trade with Canada. It

also identifies eleven small scale entrepreneurs (producers) as potential exporters, and develops

a detailed business case strategy for market-entry into Canada considering different factors such

as production, transportation, marketing and legal requirements. Moreover, the study provides

advice to the potential exporters to tackle challenges and barriers they face in exporting process.

1.2. Design and methodology of the study

Study design

To build a sustainable and profitable export market for Ethiopian handloom woven products in

Canada, the study has adopted interactive and participatory approaches in selecting

entrepreneurs, identifying products and developing market strategies. The figure below

summarizes the indicative study design pursued in this study.

2

Figure 1: Indicative study design

Source: Authors’ computation based on the survey data

Sampling strategy

This study employed a two-stage purposive sampling technique. At the first stage, we decided to

focus on Ethiopia’s artistic hand woven specialty textile and fabrics products for three main

reasons. Firstly, these products use Ethiopian unique traditional designs that are beautiful and

exotic. In addition, Ethiopian handloom weaving industry has a long history and a rich experience

customarily practiced by small artisans known as weavers (traditionally named ‘Shemane’).

Secondly, the majority of people engaged in handloom woven manufacturing are poor women.

Inception meeting with TFO Canada Other stakeholders

Selection of entrepreneurs

Development of criterion Export readiness Export performance Organizational structure Production capacity

Desk study Data collection Export performance

analysis Previous studies review Study on Canadian

market Competitors analysis Evaluation

Factory visit Profile compilation and

evaluation Focus group discussion

Gap analysis and market bridging

Factory visit & discussion Identification of products for

each factory Focus group discussion Gap analysis Brainstorming with stakeholders SWOT analysis

Development of market entry

3

The spinning of cotton in preparation of weaving is often done by craftswomen, including elderly

women whereas handloom weaving is undertaken by men as it is demanding business. Moreover,

the sector is mainly owned by the local entrepreneurs who operate on small production scales.

Thirdly, the products are environmentally friendly as they are hand-woven and use on-power

driven machinery, and organic cotton. Handloom weavers use no chemicals and produce no

water wastes. They also use no coloring and other agents that are harmful to the environment.

Therefore, these products are highly needed in the global market.

At the second stage, the study purposively selected the sample of eleven small scale producers

of handloom woven who have good potential for exporting quality products. The selection of firms

used criterion such as product quality and uniqueness, production capacity, organizational

structure, export readiness and experience.

Methods of data collection and analysis

The study utilized both primary and secondary data. The detailed primary data was collected

using focus group discussions and structured interviews with entrepreneurs and trade experts.

Focus group discussions were conducted with eleven selected enterprises producing hand woven

specialty textile and fabrics and capable to export their products to Canada. It served to identify

the best products for export and the challenges faced in both production and the export process.

In addition, interviews with trade officials and practitioners were conducted to identify feasible

market entry strategies.

In addition, relevant secondary data was obtained from the Central Statistics Authority (CSA),

Federal Micro and Small Enterprises Development Agency (FeMSEDA), the Ethiopian Textile

Industry Development Institute (ETIDI), the Ethiopian Textile and Garment Manufacturers'

Association (ETGAMA) and the Ministry of Industry (MOI). After gathering all necessary data, the

study used descriptive methods of data analysis including percentages and ratios.

4

Chapter two: an overview of textile and apparel market in Canada

2.1. Market for general textile and apparel products in Canada

According to Trade Data Online (2016), the global demand for all textile fibers has grown by

slightly more than 50% over the past decade. This is due in part to an increasing world population,

urbanization, and consumerism, and then the fact that textiles are used in so many everyday

applications (clothing, filters, cloths, wipes, and in housing and transportation materials). The

report (2016) also revealed that even though global demand for textiles has increased, Canada's

textile industry has declined in size over the past decade and textile-related employment fell by

approximately 60% between 2004 and 2014. This is due to a number of reasons, in particular the

decrease in demand for textiles destined to general apparel manufacturing and the shift to

technical textile manufacturing which relies more on technology than on labor.

In Canada, technical textile is evolving in a business environment supported by academic

research and strong industrial knowledge which is conducive to even further growth of this sector.

Companies in the textile industry are integral to the supply chains of the many major industries in

Canada. Technological advances in textile sciences are resulting in the development of novel

textiles, or in textiles being increasingly adopted to replace traditional materials used in other

industries.

Table 1: Economic indicators of the Canadian textile market (in millions of CDN $)

Economic Indicators

2010 2011 2012 2013 2014 % change 2013-14

CAAGR 2010-2014

Total imports 4,461 4,668 4,803 4,924 5,293 7.5% 4.4% Total exports 2,129 2,177 2,201 2,127 2,207 3.8% 0.9% Re-exports 255 282 286 282 296 5.2% 3.8% Apparent domestic market

8,979 8,077 7,726 7,350 6,746 -8.2% -6.9%

Domestic market share

50.3% 42.2% 37.8% 33.0% 21.5% -11.5% -7.2%

Import penetration 49.7% 57.8% 62.2% 67.0% 78.5% 11.5% 7.2% Export orientation 32.0% 39.0% 43.0% 46.7% 60.3% 13.6% 7.1%

Source: Trade Data Online, 2016

Retail market scenario

According to 2012 data from Statistics Canada (TFO Canada, 2013a), retail clothing sales in

Canada rose to its highest level in five years, reaching $26.9 billion in 2012. The report also

indicates that sales of women’s clothing and accessories have risen slowly over the past four

5

years, reaching $15.1 billion in that same year (Ibid). More dramatic has been the rise in sales of

men’s clothing and accessories, which reached five year high of $8.6 billion following a low of

$7.1 billion four years previously (Ibid). Sales of children’s clothing also reached five year high,

amounting to $3.2 billion in 2012 (Ibid).

Figure 2: Retail clothing sales (in $ billions CAD)

Source: TFO Canada, 2013a

However, sales of clothing and accessories fell by 2.1% in the first quarter of 2013 compared with

the first quarter of 2012, led by women's clothing and accessories that decline by 2.8% (TFO

Canada, 2013a).

Table 2: Retail clothing sales in Canada by type (in billions of CAN $)

Type of clothing 2008 2009 2010 2011 2011 Women's clothing and accessories 14.6 14.3 14.9 15.0 15.1

Men's clothing and accessories 7.4 7.1 8.1 8.3 8.6

Girls', boys' and infants' clothing and accessories 3.0 2.9 3.1 3.0 3.2

Total 24.9 24.3 26.0 26.3 26.9

Source: TFO Canada, 2013a

Large retailers accounted for almost half of the total retail sales. According to the report, in 2012,

large retailers sold $8.2 billion worth of women’s clothing and accessories; $4.3 billion worth of

men’s clothing and accessories; and $2.2 billion worth of children’s and infants’ clothing (Ibid). As

well, large retailers sold $162 million worth of unisex clothing that can be used by both males and

females (Ibid).

23

24

25

26

27

28

2008 2009 2010 2011 2012

Retail clothing sales in Canada

6

2.2. Market for handloom woven textile and apparel products

Handicrafts are generally bought by importers specializing in house ware and giftware. The

products are distributed in specialty shops as well as through general retail stores. Canadian

demand for all forms of ethno-cultural clothing, jewelry, home furnishings and other related items

is largely influenced by interest in the artistic and cultural traditions of foreign countries which is

itself enhanced by the growing levels of immigrants in Canada, growing interest in fair trade,

increased travel by Canadians, and extensive media coverage of the cultural traditions of other

countries (TFO Canada, 2013a). Styles vary somewhat according to the region in Canada. For

example, consumers on the west coast tend to choose more casual decorations than in central

Canada (Ibid).

Fashion accessories

Fashion accessories cover a wide range of items including handbags, scarves, shawls, gloves,

mittens, belts, and ties. Leather remains a popular material due to its perceived luxury, durability

and softness, especially for mid to high-end handbags, gloves/mittens and belts. Following recent

fashion trends, leather is also used in non-traditional ways as a design accent or appliqué to

accessory items. Knitted wool is popular for winter accessories (mitts/gloves, hats and scarves),

while other textiles like cotton, felt, and silk are used year round. The best opportunities exist for

exporters who can differentiate their products with unique materials not yet seen in Canada, such

as alpaca wool and pima cotton from Latin American countries. Products made of recycled/up

cycled materials such as plastic bottles, recycled fibers, or repurposed second hand clothing can

tap into the growing niche of environment-friendly consumers.

2.3. Trends of textile and apparel imports in Canada

Canada imported nearly $1 billion worth of fashion accessories in 2014 (TFO Canada, 2015a).

Over the past five years (2010-2014), imports have grown steadily at an annual rate of 8% per

year, which is above the average of 5% for all consumer goods (Ibid). The growth over the past

five years (2011-2014) is driven primarily by increasing imports of gloves and mittens, handbags,

and scarves and shawls (Ibid). Hats and ties were the only items to experience a slight decline

during this same period (Ibid).

7

Figure 3: Canadian import of fashion accessories 2010-2014 (in millions of CAD $)

Source: Trade Data Online, 2016

Product breakdown

The majority of fashion accessory imports in 2014 were concentrated in handbags ($385 million),

gloves and mittens ($350 million), and scarves and shawls ($123 million) (TFO Canada, 2015a).

Other popular items include belts ($45 million), ties ($27 million) and hats ($553,000) (Ibid). A

further $40 million of other fashion accessories not elsewhere specified was also imported in 2014

(Ibid).

Figure 4: Imports of fashion accessory in Canada by product (2014)

Source: TFO Canada, 2015a

$658 $727 $770 $852

$972

$0

$200

$400

$600

$800

$1,000

$1,200

2010 2011 2012 2013 2014

39%

36%

13%

5%3% 4%

Handbags

Gloves and Mittens

Scarves and Shawls

Belts

Ties

Hats

Other

8

2.4. Quality standards, price condition and distribution schemes

Standards: Handicrafts intended for outdoor use must be able to withstand extremes in

temperature and moisture, while those intended for children must meet safety and flammability

standards such as workmanship, finish, weight, markings, chemical composition, hardness,

toughness, thickness, moisture absorption, flammability, resistance to frost and sudden

temperature changes, resistance to stains and acids, and color fastness.

Price condition: Product pricing is vital to remaining competitive. In the retail sector, for example,

Canadian businesses have followed the successful United States trend toward larger stores with

highly competitive prices. To this end, many retailers have invested in large discount-style

operations to expand sales in an increasingly competitive market. The emergence of high-volume

warehouse merchandising in this market is the direct result of consumer demand for competitively

priced quality goods. Value for dollar is the predominant purchasing determinant in both the

consumer and industrial markets. Generally, the retail price is 5 or 6 times the free on board (FOB)

price. The retailer will typically double the price paid to their supplier. Obviously the cheaper the

product, the more there is room for higher markups, which can reach 8 to 10 times the FOB price,

depending on the volume and the item.

Distribution and regulations: The Canadian Gift & Tableware Association (CGTA) estimates

that there are 63,000 stores in Canada that sell or have the potential to sell giftware; about 45,500

of these are independent retailers and 17,500 are chain stores (TFO Canada, 2013b).

Retailers: It is important to note the growing importance of digital retailing (e-commerce) in

Canada. Globally, digital retailing is headed toward 15% to 20% of total sales, although the

proportion will vary significantly by sector (TFO Canada, 2013b). Much digital retailing is now

highly profitable. For example, Amazon’s five-year average return on investment is 17%, whereas

traditional discount and department stores average 6.5% (Ibid). Experts estimate that digital

information already influences about 50% of store sales, and that number is growing rapidly (Ibid).

Traditional retail sales distribution is conducted through a variety of outlets including independent

crafts stores, general gift shops, department stores, and discount stores such as Home Sense.

Smaller, mass produced handicraft items are sold in ‘Dollar’ stores, where each item is sold for

around $1. Interesting beads, charms and other craft items are sold in specialty stores such as

‘The Sassy Bead Company,’ while other stores such as Ten Thousand Villages specialize in a

wide range of fair trade home décor items. Handicrafts are often used as accessories in specialty

9

stores to boost sales of furniture, household and garden items. This aids the consumer in selecting

styles, themes and color.

Several gallery stores and many of the more fashion oriented independent stores are excellent

outlets to sell imported items on an exclusive basis. Canadian retailers are often looking for

specialty fashion items such as handloom woven mirrors, picture frames, and art objects.

Boutique hotels and other businesses seeking to attract an exclusive clientele often source unique

handicrafts to enhance the atmosphere they are trying to achieve. In these instances, architects

and interior designers, acting on behalf of the end-use purchasers, play an important role in the

selection of handicrafts.

2.5. Access to and requirements of export to the Canadian market

Access to Canadian market: An initiative to increase exports in Canada has been launched in

2003 by the Government of Canada. The Market Access Initiative is governed by the General

Preferential Tariff (GPT) and Least Developed Countries Tariff Rules of Origin Regulations

SOR/2013-165, which are commonly referred to as the LDCT Regulations. The LDCT

Regulations are enforced by the Canadian Customs Tariff Act.

Before the Market Access Initiative came into force, most imports to Canada that originated from

developing and emerging economies were subject to an average duty rate of 19% (TFO Canada,

2015b). Determined by either the Most Favored Nation Tariff (MFN) or the GPT, this high level of

import duty did not encourage export to Canada. It also poised significant challenges for

businesses in developing and emerging economies. The Market Access Initiative was designed

to change this.

All of the 48 LDCs (Ethiopia being one of them) that benefit from the Market Access Initiative

signed a Memorandum of Understanding on the Least Developed Countries Market Access

Initiative with the Canadian government in 2003 (TFO Canada, 2015b). A number of these

countries also have bi-lateral economic cooperation agreements with the Government of Canada.

Almost all goods entering the Canadian market from these 48 LDCs are duty-free and quota free.

The only exclusions are raw and unprocessed forms of dairy, poultry and egg goods. These goods

are not entitled to duty-free or quota-free status. According to the LDCT Regulations, eligible

goods require proper proof of origin documentation (TFO Canada, 2015b).

10

Required documents for exporting to Canada: All goods entering Canada must be

accompanied by three documents:

Certificate of origin Customs invoice Bill of lading

There are no exceptions to these requirements. These documents are only valid for a single

export shipment. This means that each time goods are exported to Canada these documents

need to be provided. These documents can be in English or French, which are the official

languages of Canada. Although the Government of Canada does not require export documents

to be signed or certified by a delegated authority in the country of origin, the local government

may require this prior to exporting goods to Canada. It is essential to find out whether this is

necessary.

Other supporting documents required for exporters and producers (specially for textile and

apparel) are commercial invoices, specifications sheet, purchase orders (for inputs from GPT

countries, especially for yarns or fabrics), utilization reports, style design and number (sketches),

list of materials with costing sheet, product sample, supplier of yarns and fabrics, production

records, payroll records, and letter of credit or electronic bank transfers.

11

Chapter three: The Ethiopian textile and garment industry sector overview

3.1. An overview of the Ethiopian textile sector

Due to its labor intensive nature, the textile industry is an effective means of creating employment

opportunities to raise standard of living and alleviate poverty. Ethiopia considers the textile and

apparel industry to be the key to industrialization. At the moment, the textiles and apparel sector

consists of around 130 medium and large scale factories of which 37 are foreign owned (Dhyana,

2016).

The Government of Ethiopia has set ambitious plans to develop this industry. For instance, the

Growth and Transformation Plan-I increased from USD 21.8 million in 2009/10 to 1,000 million in

2014/15 (FDRE, 2011). To realize this, the government provided several incentives such as

exemption of duties on capital goods for industrial set up and exemption of duties on raw materials

meant for export goods. Income tax holiday were also granted to exporters and suppliers.

However, the overall performance in terms of export earnings lagged behind the targets. For

example, only USD 98.05 million was obtained from textile and garment exports in the July 2014

– June 2015 period (MOI, 2015). Recently, the share of textile export has reached only 23.2% of

the total manufacturing export and 3.5% of the total exports in 2015 (ETIDI, 2016). Despite the

low export performance, ongoing Growth and Transformation Plan-II has targeted to increase

textile industry export to USD 1 billion in 2019/2020 (MOI, 2015).

Figure 5: Export performance of the sector (in thousand USD $)

Source: Data from Ethiopian Revenues and Customs Authority, 2016

0

10000

20000

30000

40000

50000

60000

70000

80000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Yarn

Fabric

Apparel

Handloom products

12

The above data depicts that export performance of textile sector is increasing on average of

37.5%, but the export performance of 2015 shows a -12 % growth rate due in part to global price

increase of cotton (Ethiopian Revenues and Customs Authority, 2016).

3.2. Handloom-weaving industry in Ethiopia

The Ethiopian manufacturing industry is divided into three major groups (CSA, 2010). These are:

large and medium scale manufacturing establishments engaging 10 or more persons and using

power-driven machinery; small scale manufacturing establishments engaging less than 10 and

use power-driven machinery; and cottage/handicraft manufacturing establishments performing

their activities by hand (i.e., using non-power driven machinery). Handloom weaving is one of the

most important segment of cottage based industries in Ethiopia through its wide spread

employment creation, next to agriculture.

As part of the handicrafts heritage, the handloom sector constitutes the bulk of the informal sector

and is an important source of livelihood for large number of people. As such, it is a very important

industry for income generation both in the rural and urban areas. In addition to its huge

employment creation, the handloom sector has strategic importance in the economic

development of the country through its strong linkage with the agricultural sector and the

potentials for having a progressive transformation into modern establishments.

Table 3: Export share of handloom-weaving in the textile sector

Product category 2010 2011 2012 2013 2014 2015

Total export from the textile sector 23,210 2,224 84,626 98,988 111,353 98,061 Handloom products 1,696 3,382 4,361 4,916 4,738 4,647.08 Export share of handloom (%) 7.31 5.44 5.15 4.97 4.25 5.0Yearly growth rate of handloom products (%) 343 99 29 12.7 -3.6 -1.9

Source: Data from Ethiopian Revenues and Customs Authority, 2016

Employment in handloom weaving sector

In Ethiopia, handloom weaving is a particularly important sub-sector, being the most important

employer of rural families after agriculture (Abdella and Ayele, 2008). Handloom weaving is one

of the most important nonagricultural sources of income in Ethiopia (Central Statistics Agency,

2003). According to the Central Statistics Agency’s 2003 Cottage/Handicraft Manufacturing

Industries Survey, the textile industry has the second highest number of establishments in the

13

cottage and handicraft manufacturing industry (221,847), representing 23% of the total number

of cottage and handicraft enterprises, with almost 55% of these located in rural areas. The report

also shows that, across the nation, the textile industry employs the second highest number of

people among the cottage and handicraft manufacturing industries, following food products and

beverages (ibid). This industry accounts for 23% of the total employment in the cottage and

handicraft manufacturing industries, and 20% of the rural employment in the cottage and

handicraft manufacturing industries (Ibid). Weaving enterprises make up 73.2% of the textile

industry in number of establishments, and 42.8% in total number of workers (Ibid). The following

table presents figures on the other types of nonfarm, small-scale industries (Ibid).

Marketing & distribution

Handloom woven products are destined for both domestic and foreign markets. However, the

major portion of the handloom products is consumed domestically. Ethiopians abroad and other

foreigners are the users of hand woven non-garment product items like tablecloths, pillow covers,

etc.

Figure 6. Distribution strategies of handloom weavers

Source: Authors’ computation based on the survey data

Note: Exporters have their own weavers and garments, but when they have large orders they

outsource (subcontract) to cooperatives.

Weavers (mainly cooperatives)

Wholesalers

Exporters*

Retailers

Consumers

Export market

Retailer

Consumers

14

Table 4: Major players based on their export performance

S.N Name of the company Value in USD

(from July 2009 - April 2016)

% share from total

export 1 Muya Ethiopia P.L.C (Sara Abera Garment) 5,198,106.32 17.32 SabaSilk/SabaHar P.L.C. 2,790,373.52 9.33 Sami Mohammed Abdela Export P.L.C. (Nigist Ethiopia

P.L.C.) 718,385.78 2.44 Ellilita products 463,351.84 1.545 Salem’s Ethiopia 219,580.92 0.736 Trio Craft P.L.C 97,135.34 0.327 Paradise Fashion 20,921.81 0.078 K design weaving and dress making 9,835.82 0.039 Don Door Handi-Craft P.L.C. 2,557.00 0.0110 Sabatebieb cultural hand crafts and jewelery plc 527.80 0.00211 Others 20,559,448.64 68.3512 Total export 30,080,224.79

Source: Data from Ethiopian revenue and custom authority report, 2016

Ethiopian textiles and products are being exported to different countries across the world. Table

7 presents the destination countries along with percentage shares. The United States, Germany

and Turkey are the main recipient countries for the textile products exported from Ethiopia.

Table 5: Destinations for Ethiopian general textile and handloom woven products

S.N Destination country Value in USD (from July

2009 - April 2016) % share from total

export 1 United States 6,947,156.18 592 Germany 1,509,036.16 12.83 Turkey 750,757.71 6.44 Djibouti 462,364.94 3.95 Italy 405,239.33 3.46 Israel 403,642.89 3.47 Australia 335,340.27 2.88 United Kingdom 208,937.43 1.89 Norway 175,925.41 1.510 France 135,236.30 1.111 China 117,641.70 1.0012 Canada 106,259.91 0.9013 Others 18,522,686.56 2.114 Total export 30,080,224.79

Source: Data from Ethiopian revenues and customs authority, 2016

As illustrated in the table below, the main products exported are clothing which includes pants,

shirts, and traditional cloths, which take 55% of the total export value.

15

Figure 7: Percentage share of Ethiopian handloom export products

Source: Data from Ethiopian revenue and custom authority, 2016

Value chain of Ethiopian handloom weaving

The handloom sub-sector in Ethiopia is derived from the cotton sub-sector and is an example of

a traditional-based and home grown activity. In the value chain context, the major products of the

handloom sector can be divided into semi-finished fabrics and finished products. While the semi-

finished fabrics are usually channeled to the domestic garment factories for further processing,

the finished products are divided into traditional clothing categories like ‘Netela’, ‘Gabi’, ‘Kemis’,

and ‘Kuta’ which are sold mainly in the domestic market and to Ethiopians living abroad, and

home furnishing textiles, which are destined to the international market (Abdella and Ayele 2008).

Herewith, we tried to show the typical production flow of an exporting company (Muya Ethiopia

P.L.C):

4%

18%

10%

2%6%

0%

0%

55%

5%

Product type Analysis shawl

scarf

Towel (Batch, bath, beachand hand towel)Table runner, Placemats &NapkinsHand woven textile

Bed sheet/pillow cover

bags

16

Figure 8: Production flow of a typical handloom woven products exporting company

No Yes

Source: Authors’ computation based on the survey data

Receiving export production

order

Discussion on the production

order with production

supervision

Discussion on the design and

on time delivery

Make sure that raw materials

and other inputs are ready

Warp sizing

Warping operation

Pin winding

Sample making by master

weavers (product developer)

Is the sample

meeting the

specification

Allocation of work order for

weavers

Grey fabric inspection

Fringing

Washing

Ironing before sewing

Sewing

Ironing after sewing

Final inspection and packing

Pricing

17

Ethiopian handloom weavers are producing different product categories for their target markets.

Products for the domestic market are Netela, Kemis, Gabi and Kuta (traditional clothes).

Handloom weaving products for international markets include table cloths, decorative wear, bed

furnishings, window coverings and wall and ceiling coverings (for aesthetic and functional

purposes including noise absorption).

The main categories of Ethiopian handloom woven products which are produced for international

markets are summarized as follows:

Home accessories and gift: Table cloth (table runner, placemats, napkins), cushion cover

and pillow cover, bed cover /bed runner, curtain panels and wall mat, cotton/wool made flat

rugs and carpets

Hand-woven textile and clothing: Caftans (poncho), causal and occasional outfits, bridal

gown & accessories, skirts, pant, shirt, traditional cloth and baby blanket

Fashion accessories: Scarves, belts, sashes & hair bands, event bag and different bags,

beach chic, throws, cotton shawl and hand towels/ bath towel/ beach towels

The table below shows that Ethiopia has been mainly exporting handwoven textile and clothing

followed by fashion accessory and home accessory respectively.

Table 6: Ethiopian handloom woven export by product type and category

Types of product Product category FOB Value in USD

in 2015 % share in 2015

Shawl Fashion accessory 113,276.14

31.39

Scarf Fashion accessory 525,995.72

Towel (batch, bath, beach and hand towel) Fashion accessory 281,661.27

Bags Fashion accessory 2,423.85

Table runner, placemats & napkins Home accessory 51,823.94

2.22 Bed sheet/pillow cover Home accessory 13,465.64

Hand woven textile Hand-woven textile and clothing 185,432.69

61.06 Clothing (pants, shirts, traditional cloth) Hand-woven textile and clothing 1,610,826.21

Others 156,955.58 5.3

Total export 2,941,861.03 Source: Data from Ethiopian Revenues and Customs Authority, 2016

18

As can be seen from Table 8 and Figure 9, the main export product category is textile and clothing

which constitutes about 65% followed by fashion accessories (33%). Whereas, the export of home

accessories constitutes only 2% of the export value of handloom woven products.

Figure 9: Handloom woven products export by product type and category

Source: Data from Ethiopian revenues and customs authority, 2016b 3.3. Competitive advantage of Ethiopian handloom woven sub sector

Beside their unique features, Ethiopian handloom woven products are highly diversified in design,

style and ethical to different ethnic group of nations and nationalities at every corner of the country.

Ethiopia’s population is highly diverse, containing over 80 different ethnic groups and all these

ethnic groups have their own colors, styles and symbols. Therefore, the different fashions can be

an incentive for Ethiopia to develop new products and produce for international customers.

Competitive advantage is defined as the capability of an organization or firm to create a defensible

position over its competitors. Alan et al. (2011) stated that international competitiveness ultimately

depends upon the linkages between a firm’s unique, idiosyncratic capabilities (firm specific

advantages) and its home country assets (country-specific advantages). With this regard,

Ethiopian hand-woven products have the following advantages:

Availability of resources: Ethiopia has suitable agro-climatic conditions for the

production of cotton i.e. Ethiopia has 2.6 million hectares that are suited for cotton

cultivation, which serves as the main raw material of the sector; there is abundance and

relatively lower cost of labor power; and immense indigenous designs which are used as

assets to increase the competitive advantage of these products.

Fashion accessory 33%

Home accessory 2%

Hand‐woven textile and Clothing 65%

Handloom women products (2015)

19

Unique features: The features, colors and embroidery create a center of attention and

satisfy customers easily.

They are made from 100% cotton

They are highly colorful, attractive and decorative

They remind of the Ethiopian heritage

Diversification of the designs: Hand-woven products in Ethiopia are highly diversified in

design, color and styles. Producers are flexible to change the designs at any time

depending on the customer needs.

Market accessibility: Ethiopia benefits from the Free Trade Agreements (FTA) and

AGOA to the United-States market and everywhere on the globe. In addition, fashions are

global businesses which are purchased by international costumers.

The production processes: Ethiopian handloom woven products are designed by an

indigenous knowledge. The weaving and garment technology, and the production

process, can be seen as a competitive advantage.

3.4. Local initiatives to promote handloom weaving in Ethiopia

Different actors intervene to promote handloom weaving in Ethiopia, including the government,

NGOs and the private sector. Selected examples are below:

Federal Micro and Small Enterprise Development Agency (FeMSEDA): FeMSEDA is a

nonprofit entity which was established by the Council of Ministers Regulation No.33/1998 in1998

(Hibret. N, 2009). Its objective is to encourage, coordinate and assist institutions which provide

support to the development and expansions of SMEs in the country at large. In order to achieve

this objective, it focuses on providing supportive services such as training of trainers, prototype

development and dissemination, information and consultancy, facilitation, marketing, and

technological database to stakeholders.

In collaboration with regional governments, SME development agencies, NGOs, and the private

sectors; the Agency mainly provides training and marketing services. Training services include

business skills and management trainings; technical skill trainings like pattern making; handicraft

skill training such as carpet making, weaving, and Tie dye and Silk; technology development and

transfer training; and awareness creation on total quality management. The marketing services

that are mainly provided by the agency include: sales and promotion; market information and

consultancy; and local and international business networking services. The Agency’s report on

20

handicraft and technology training for the year between 2003/4 to 2008/9 shows limited outreach

in trainings (FeMSEDA, 2009). The number of trainee in the period was 4421 only. Out of this,

garment making accounts the largest number 1,560 (35%) and followed by weaving 410 (9.3%),

while the rest shared by trainees on other handcraft and technology trainings.

Addis Ababa, Micro and Small Enterprise Development Agency (ReMSEDA): ReMSEDA

was established in 2003 under the Trade and Industry Bureau. Its structure extends to sub-city

and kebele levels (Ageze, 2006). The objective of the agency is to reduce urban poverty through

increasing employment opportunities and to promote industrial development through expansion

and development of SMEs (Ibid). It has engaged in organizing community members with different

skills into cooperatives and trade association and providing various supportive services. BDS

(business development service) is one of the tools. BDS that are provided by the agency in

collaboration NGOs include: facilitating access to finance, training, appropriate technology, and

working and marketing premises; facilitating market linkage and raw material supply; information

and advisory services; and tax payers’ and job seekers registration services. These services have

been provided in a one-stop service model to facilitate SMEs’ immediate access to all type of

available services (Ibid).

United Nation Industrial Development Organization (UNIDO): UNIDO has been undertaking

handloom sector cluster development for cooperatives since 2005 as a pilot project. The objective

of the intervention is to ensure firms in clusters benefit from larger sales volumes, lower costs,

improved workers’ skills and product quality; and enhance productivity by promoting joint activities

in marketing, production and improved sectoral training programs (Miftah, 2008). UNIDO provides

both financial and technical assistance for the project. Accordingly, in collaboration with the

FeMSEDA and ReMSEDA, UNIDO has been providing basic business management and modern

weaving skill upgrading training to weavers at handloom clusters; and technical supports to

facilitators who work with these weavers’ clusters.

Beyond that, the project has played much role in addressing marketing problems of weavers

through creating networks among weavers and between weavers’ cooperatives and exporters.

The latter is mostly through arranging subcontracts. In addition, with respect to reducing

marketing cost, UNIDO has introduced innovative marketing systems by initiating and providing

financial supports (during initial periods) in hiring marketing officers to weavers’ cooperatives.

Currently cooperatives that hired marketing officers are fully financing the payment by

21

themselves. Similarly, UNIDO has contributed in the establishment of common show room

(display centre) to weavers’ cooperatives where they can market their product to tourists, local

traders and users.

GTZ Development Program on SMEs: The German Technical Cooperation Agency (GTZ) has

been working toward SMEs development from 1996 till now in three phases. The objective of the

SMEs program was to support their promotion by providing capacity building, networking, and

Training for Trainers support to intermediary organizations that help them to implement efficient

BDS and perform their activities in a coordinated way (Hibret. N, 2009). Accordingly, the program

has contributed in creating enabling environments to the SME development throughout these

periods. Since 2005, GTZ is working with the Ethiopian government in the Engineering Capacity

Building Program. Accordingly, it supports handlooms sector by sponsoring market development

activities such as exhibitions and bazaars, information dissemination, capacity building training

for facilitators, and introducing advanced handloom technologies which is called “Flying Eight”.

GTZ chandelles these services through government either in terms of cost sharing or fully

financing.

Private BDS providers: The commercial BDS provider has been involving in providing new or

improved looms and technical training related to assembling. In this case, the operators and

service providers did not have a direct contact and the arrangement was only through government

agencies. This has been limiting flexibility of service provision and availability of diversified and

demand driven services. Those services include: technical advice, information, product

development service like design, input combination and post production quality management; as

well as input supplies (Hibret. N, 2009).

Ethiopian Textile Industry Development Institute (ETIDI): ETIDI was established in 2010

following the implementation of the Industrial Development Strategy. Its main objective is to

enable the Ethiopian textile industry to be competent in the global market by promoting and

supporting investment, providing consultancy service and training, conducting research and

development activities and giving laboratory inspection and marketing support. Different donors

like the Economic Competitiveness Forum are supporting initiatives. These supports include

advanced machinery, recruiting international expatriates, and capacity building training (Council

of Ministers Regulation No. 180/2010, 2010).

22

Elilita woven at risk: Elilita woven at risk is a local NGO. It started back in 1992 to reduce the

barriers of youth employment in the country. Elilita woven at risk is primarily working in the capital

of Ethiopia, Addis Ababa, to empower people through sustainable social and business

development such as Elilita product PLC (a company elected for this project). This NGO

empowers women through the production and exportation of handloom products to the USA

(Women at Risk, n.d).

Ethiopians Driving Growth through Entrepreneurship and Trade (EDGET): Ethiopians

Driving Growth, Entrepreneurship and Trade (EDGET) is a value chain development project

working in the handloom textiles sub-sector. EDGET, which means progress in Amharic, works

to integrate smallholder rice farmers and small-scale textile artisans into higher value markets

through increased market linkages (including input, services, and final markets) and enhanced

productivity (MCDP, 2012). Program participants benefit from commercial access to support

services from local, sustainable providers with these services continuing to operate after the

program ends.

3.5. SWOT analysis of handloom weaving sector in Ethiopia

As part of this project, government institutions, handloom woven manufacturers, handloom woven

traders, and weavers were visited. Focus group discussions were also held with handloom

manufacturers, NGOs, women exporter associations, and ETIDI.

The following table summarizes the issues which have been noted during the analysis:

23

Table 7: SWOT analysis of handloom weaving sector in Ethiopia

Description Strengths Limitations Opportunities Threats

Marketing Increasing marketing

efforts (rising market size)

Unique traditionally

designed products

Demand in the local

market is increasing which

give them experience for

foreign markets

Producing different

designs as per the

demand

No organized marketing system

Little promotional efforts

No product diversification

Lack of a quality controlling system

Lack of good market linkages (vertical, sub-

contracting, etc.)

Traders are the main beneficiary in this sector

(weavers are not direct beneficiary)

Lack of consistent orders over the year

No budget allocated for promotion

Outdated website, broachers & pamphlets

Low participation in international trade fairs

Uncompetitive pricing structures and policies,

due to high costs of imports, labor costs,

inefficiencies, etc.

Absence of market intelligence information,

networks and experiences of promoters and

industrialists

Most factories have not realized the

importance of maintaining sales records and

an updated customer database

Most producers don’t have samplings for

customers in the export market

Increased demand

both in domestic and

international markets

Willingness and

commitment for

support

Positive change of

attitude for local

products and export

Most tourists are

familiar with

handloom woven

products

Competition

Insufficient

production

capacity

24

Description Strengths Limitations Opportunities Threats

Technology Appropriateness

Locally available

Applies traditional

technology

Uses local materials

Traditional

Doesn't allow to produce all types of hand-

woven products

Availability of an

improved handloom

technology

High cost for

acquiring new

technology

Inputs Raw material mainly,

cotton is easily available

Spare parts for handloom

are easily available

Natural raw materials like

wood

Existence of strong linkage

(vertical integration)

between cooperatives and

exporters

Shortage of working capital

High cost of raw materials

Sub-standard quality of raw

materials

Price of raw material fluctuation

Shortage of raw material (mainly thread)

Absence of appropriate accessories

manufacturers and suppliers

More raw material

suppliers and/or

manufacturers are

coming in to business

Yarn manufacturers

are expanding

Duty free import for

exporters

Low quality of raw

materials

(imported)

Since thread

importers are in

the hands of few,

the price is

uncertain

Skills Traditionally acquired skills

Willing to upgrade

Can easily copy the design

they got from the buyer

Poor design skills

Low skills in business management

Poor productivity

Lack of appropriate training

No formal skills training

More access for skills

development

Affordability

for the artisans

Business

environment

Conducive policy

environment

Provides incomes for the

poor

No coordinated effort among stakeholders in

the clusters

Loose functional relationship

No enough awareness about international

market

Both national &

International

conducive policy

environment

Strong market

requirements in

international

market

25

Description Strengths Limitations Opportunities Threats

Employ more people

(specifically in the clusters

and cooperatives)

Non-existence of appropriate

commercial institutes supporting the

subsector

No quota in the

international market

Productive

capacity

Large pool of cheap labor

available

Real full fledge integration

is possible in this industry

ETIDI is giving technical,

capacity building and

import-export facilitation

support

The expanded cluster

development made it

possible for weavers to

learn and enjoy the

benefits of working in this

subsector

Productivity is mainly based on the number of

employees

Mostly the size of the loom (width) is limited

Undetermined capacity since they are

producing different product category in which

the design vary

Lack of or limited finances, financial supports

and investment opportunities

Lack of standards (in quality and other inputs)

in this subsector as well as a lack of culture in

research and development

Though clusters are expanded, weavers are

scattered

Lack of product specialization

Lack of quality management system except

some of export oriented company

The quality of the fabric depends greatly on

the yarn being used and the yarn which is

handmade count is not similar

Lack of a physical performance test

Evenness of dyeing may happen

Relatively low skill of pattern making and

garmenting

New innovations are

coming thanks to the

support of different

government and

NGOs

Long loom sizes are

emerging as per the

nature of products

There is not a well-

organized institute or

university specialized

in this subsector

New innovations

may affect the

natural behavior of

production

Following new

innovations, they

might lose the

primitive nature

which was a key

for demand

26

Description Strengths Limitations Opportunities Threats

Export

readiness

Due to the growth of local

market, quality is improved

Government support for

exporters

Awareness of international

market is rising

Organic/nearly organic raw

material usage

Unique product design

Various designs since

there are more than 80

ethnic groups in the

country

Lack of or limited finances, financial support

and investment opportunities

Lack of knowledge about quality standards for

the international market

Due to limited production capacity, they are

unable to handle bulk orders

Low market promotion

Lack of funds to finance export orders and

work in progress; because of this most of

them are doing in advance payment basis

Limited international exposure and very little

participation in international trade fairs

Various opportunities,

such as the AGOA,

and Everything but

Arms initiative

Preferential market

access in different

countries including

Canada

Having agents and

sub-contractors

(cooperatives and

clusters)

Stiff competition

from China and

India

Low capacity of

formulating market

entry strategy

Source: Authors’ computation based on the survey data

27

Chapter four: Canadian market penetration strategy

4.1. Marketing strategy development approach

A well-designed marketing strategy is required to penetrate the Canadian market, since the

products will be facing strong international competition. The following illustration provides an

overview of the various phases the study pursued to develop the market entry strategy for

Ethiopian handloom woven products.

Figure 10: Marketing strategy development design

Source: Authors’ computation based on the survey data

Focus group discussion and evaluation of companies’ capacity and product analysis

SWOT analysis

Marketing strategy

Marketing mix instrument Product identification for Canada market Price analysis Communication Distribution

Developing market entry strategy

Canada market and companies’ analysis through: Factory visit and making one to one discussion Focal group discussion Secondary data review

28

Selection of potential exporters

In order to select exporters of handloom woven products to Canada, we categorized producers

into three main segments: home accessories and gift exporters, hand-woven textile and clothing

exporters, and fashion accessories exporters. But since none of the entrepreneurs exclusively

produce products which fall under one segment, we selected unique products for the targeted

Canadian market.

Furthermore, the study considered different important factors for the selection. In order of priority,

the selection criteria included: Export readiness and commitment, actual or previous export

experience, production capacity and quality standards, number of employee (considering this

project focused on SMEs having less than 500 employees), organizational structure/management

structure, ability to finance export orders and previous and intended investments to upgrade

production set up.

Based on the above criteria, we initially selected 13 small firms and submitted their profiles for

the first audition by experts from TFO Canada. Then, TFO Canada approved the selection of

finally 11 handloom manufacturers. The selected firms are listed in Table 10 below. The two

companies that didn’t pass the first audition are Abeba Knit and Cultural Dresses Production and

Distribution and Yoas Handloom woven (Tibeb) P.L.C due to their low production and financial

capacity.

Selection of products for potential export

After analyzing the Canadian hand-woven market (demand) and Ethiopian product categories

(supply), we selected different products in each category. The selected products for potential

export to Canada are:

Home accessories and gift: Table cloth (table runner, placemats, napkins), cushion cover

and pillow cover, bed cover /bed runner, and cotton/wool made flat rugs

Hand-woven textile and clothing: Caftans (poncho), traditional cloth, baby blanket,

butterfly dress, and kaftans top

Fashion accessories: Scarves (woven and knitted) and knitted hats, tote bags, throws

(woven and knitted), cotton shawl, and beach towels

29

After undertaking factory visit, focus group discussions and analyzing each company’s product

category with respect to the demand of Canadian market, the study has selected different product

items in each company. The table below lists the companies with their selected products for export

to the Canadian market. These products were selected in collaboration with TFO Canada,

researchers and companies’ owners (see the Appendix for the detailed description of selected

companies and their sample products).

Table 8: Selected potential exporters and products

S.N Name of company Selected product items for export*

1 Sabahar/Sabasilk P.L.C Towels (beach towels, bath towels, hand towels), and shawls

2 St. George Interior Decoration and Art Gallery

Cushion cover, and sets (table mats, table runner & napkins)

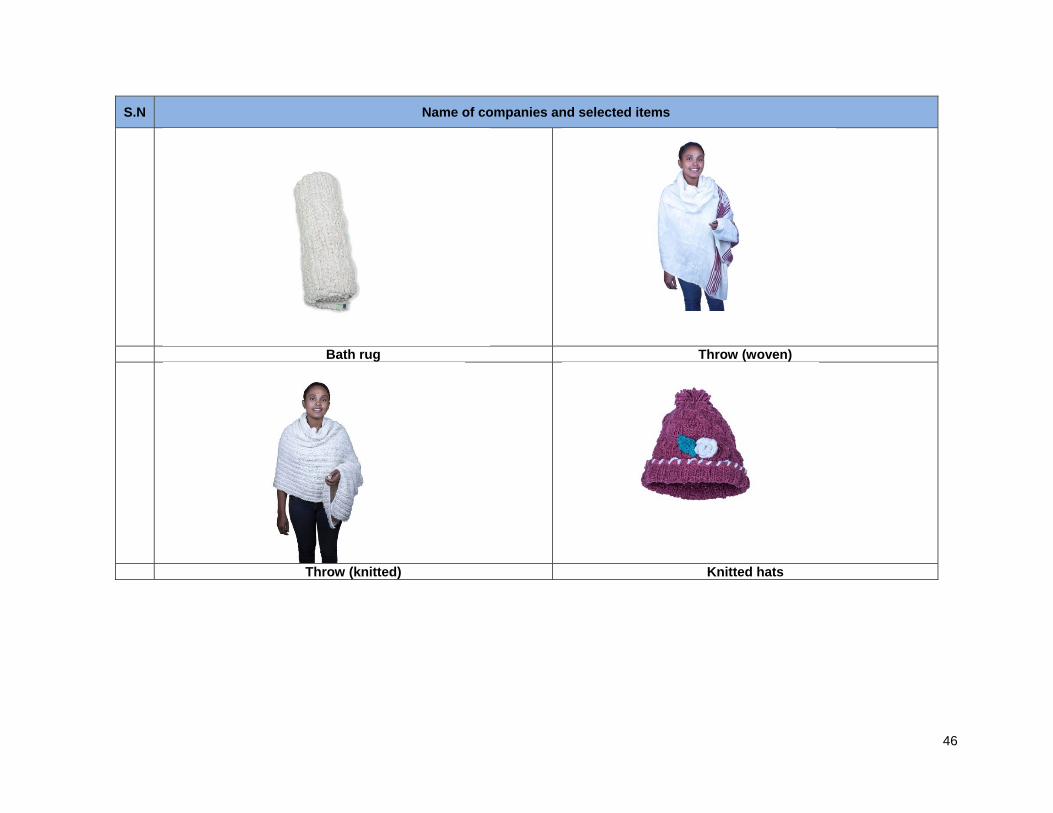

3 Salem’s Ethiopia Bath rug, throws (woven and knitted), knitted hats, and tote bags

4 Paradise Fashion Kaftans top, shawl, and scarves (woven) 5 Sami Mohammed Abdela Export P.L.C.

(Nigist Ethiopia P.L.C.) Scarves (woven), and ponchos

6 Muya Ethiopia P.L.C (Sara Abera Garment) Baby blanket, and scarves (woven) 7 K design weaving and dress making Top dress (tonique), ponchos, scarves

(woven), and butterfly dress 8 Don Door Handi-Craft P.L.C. Scarves (made of silk), and tote bag 9 Ellilita products Scarves (woven) 10 Trio Craft P.L.C Rugs, cushion covers, throw, scarves

(woven), and table runner 11 Sabatibeb P.L.C Scarves (woven and knitted neck scarf),

shawls, and knitted hat

Source: Authors’ computation based on the survey data

Note*: Even though the Canadian market is saturated by Indian and China made table runners, towels and napkins, we selected some items because their uniqueness.

30

4.2. Strategy for Ethiopian handloom woven products

4.2.1. Distribution channel

The figure below illustrates the possible distribution channels that can be used by the exporting

handloom manufacturers of Ethiopia.

Figure 11: Potential distribution channel for entering Canadian market

Source: Authors’ computation based on the survey data

Focusing on importing wholesalers, importing manufacturers and agents in Canada: It’s

strongly recommended to create market linkages with these actors for the following reasons:

Since these channels are selling their products to importing retailers or non-importing retailers,

their profit margin over Ethiopian manufacturer is high because they are going to compensate

from selling to importing wholesalers or non-importing retailers.

As mentioned in the SWOT analysis, Ethiopian handloom woven manufacturers are facing

market inconsistency. As these channels are big in size, their market linkage will be more

sustainable.

Since these importing wholesalers are giving bulk or high quantity order, Ethiopian handloom

woven producers will subcontract to cooperatives and hence create market opportunity.

Furthermore, this will help them to increase their production capacity.

Ethiopian handloom woven product exporting manufacturers

Importing wholesalers Importing manufacturers Agents

Importing retailers

Departmental store

Fashion stores

Specialty stores

Online seller

Large retailer

Non‐importing retailers

31

Focusing on large retailers: From the study of the Canadian market, we depict that large

retailers accounted for almost half of the total retail sales (TFO Canada, 2013a). In 2012, large

retailers sold $8.2 billion worth of women’s clothing and accessories; $4.3 billion worth of men’s

clothing and accessories; and $2.2 billion worth of children’s and infants’ clothing (Ibid). As well,

large retailers sold $162 million worth of unisex clothing which can be used by both males and

females (Ibid). For these stores, all product categories of handloom woven products in general

and particularly fashion accessory and hand-woven textiles and clothing are expected to be sold.

Focusing on specialty stores: Handicrafts, mainly hand-woven products, are generally bought

by importers specializing in house wares and/or giftware in Canada. For these stores, it’s better

to present products having novelty or a luxury nature like silk made scarves, different top dresses

like ponchos, beach throws as well as home accessory.

Clothing/fashion stores: According to a Canadian textile and apparel market study report, it is

estimated that 70% of clothing stores sell jewelry and accessories to compliment other sales (TFO

Canada, 2015a). Specialty shoe stores and luggage/handbags stores also offer a range of jewelry

and accessories, such as Aldo, Spring and Bentley. In these stores, handloom woven fashion

accessories are expected to be sold easily.

Online sellers (E-commerce): In the Canadian market scenario, E-commerce plays an important

role for jewelry and fashion accessories. Retailers in all segments and price points now offer

sophisticated online product catalogues which allow consumers to quickly compare product

features and price points across different stores. For artisanal products, sites like Etsy and the

recently launched Handmade by Amazon are enabling small designers from around the world to

tap into a global pool of consumers looking for unique and handmade items (TFO Canada,

2015a). Creating a market linkage with these known sites needs to be facilitated. Consignment

selling will work in this case.

In addition to the above listed distribution channels, nominating an agent in Ethiopia can help to

control the quality, production and shipment process when buying from different local producers.

This strategy will help Ethiopian producers by reducing the transportation cost, and will also

reduce the buyers’ costs by shipping all products at once, once they are verified and approved by

the agent.

32

4.2.2. Sector and products promotion strategy

Repositioning the image of Ethiopia

To improve the image of the sub-sector internationally, the following actions can be implemented.

Advertise in local and international specialized press,

Advertise in the “Selamta” magazine on Ethiopian Airlines flights to Canada,

Participate in handloom woven trade fairs and road shows in Canada,

Promote the history of Ethiopian weavers as it has more than 80 ethnic groups with their own

language, culture and distinct design of handloom woven product.

Promotion of the products

It is also recommended to promote Ethiopian handloom woven products in the following platforms:

Promotion in key spending seasons: The key spending seasons of Canadian consumers are

spring (March to May), summer (June to August) and Christmas. In addition, other religious or

cultural festivities (Chinese New Year, Eid al- Fitr, etc.) are increasingly important dates. Importers

make their purchases well in advance of these seasons, for instance, buying in January and

February for Christmas in December.

Promotion in targeted trade fairs: Canadian importers and a number of retail buyers usually

visit foreign markets and their suppliers once a year. They normally organize such trips to coincide

with the most important foreign trade shows where they can explore possibilities for imports and

industry trends.

Important consumer shows in Canada include:

One of a Kind Christmas Canadian Craft Show and Sale in Toronto

(www.oneofakindshow.com),

the Salon des métiers d’art du Québec in Montréal (https://www.metiersdart.ca/en/salon-

metiers-art-montreal), and the Salon Plein Art in Québec (www.salonpleinart.com).

CGTA Gift Show owned and managed by The Canadian Gift and Tableware Association,

which takes place in Toronto in January and August every year. Exhibitors participate in

this event with a comprehensive and stylish range of new gift ideas, decorative

accessories, bed, bath and linens, as well as the latest products and services for store

operations. (https://www.cangift.org/toronto-gift-fair/en/home/). Retail buyers from across

Canada attend this show.

33

There are also permanent home fashions showrooms in Toronto (e.g., Designers Walk:

www.designerswalk.com) and Montreal (e.g., Centre international du design:

www.centredudesign.fr.)

Other Canadian trade and consumer shows include: Alberta Gift Show (Edmonton); Atlantic Craft

Tradeshow (Halifax);By Hand, Canada's Artisan Gift Show (Toronto, Alberta, Vancouver,

Montreal); Canadian Toy & Hobby Fair (Toronto); Creative Crafting, Arts & Decor Festival

(Toronto); Creative Sewing and Needlework Festival (Toronto); Montreal Gift Show; Global

Interactive Gaming Summit & Expo (Montreal); Signatures Craft Shows Ltd. (Montreal, Ottawa,

Toronto, London, Winnipeg, Edmonton, Vancouver); Toronto International Gift Fair; Toronto

Mode Accessories Show; and Vancouver Gift Show.

Handloom woven producer information exchange web platform: The platform should be user

friendly, and it needs to be continuously updated to reflect the changes taking place. The web

platform should have interactive information on handloom woven producers, production

capabilities and contact details, readily accessible to potential buyers. There is no isolated web

site developed for the sub-sector so far. If well-conceived and frequently updated, it can become

an attractive tool for buyers and retailers looking for new suppliers.

Directory of exporters: Whilst having a company website is important, there are also several

on-line directories of exporters to which producers can subscribe to. Some examples are:

Importers & Exporters for Textiles, Clothing, Garments & Fabrics (http://www.importers-

exporters.com/textiles_clothing2.htm)

Fiber to Fashion (http://www.fibre2fashion.com/)

4.2.3. Product strategies

Upgrading and modernization: The producers should give attention to the upgrading and

modernization of their equipment. For instance, most handloom woven producers loom width size

is limited to a maximum of 1 meter. This means they cannot adjust to all buyer’s inquiries.

Product diversification: The existing products can be made softer, and the existing

traditional/indigenous motifs can be used for new product development. Product diversification

and new product development that suit high-end domestic and niche retailers in targeted export

markets are seen as key strategies.

34

Product specialization: All handloom manufacturers produce a variety of different products. In

order to be competitive in the international/Canadian market, producers need to know what makes

them unique and focus more on this distinctive product.

Quality in handloom products: Innovative weaving processes and techniques to increase

efficiency will make the handloom industry more competitive and profitable. It will be required to

penetrate international markets.

Unique materials and techniques: Being able to sell a unique product and tell the story of the

craftspeople and artisans who made it will attract the attention of both buyers and consumers.

Design trends: When purchasing jeweler and fashion accessories, Canadians tend to place a

high importance on design and style. Unique materials and techniques offer strong marketing

opportunities; however, these items will only sell if they have an appealing design that is aligned

with major fashion trends. Ethiopian producers need to study fashion trends in Canada and adjust

their production according to the demand.

Finishing of the product: Producers should use various finishing and packaging techniques for

a better marketing of their products. Calendaring units can be set up in weavers’ service centers

of each district.

4.2.4. Pricing strategy

While Canadians are price-conscious, they are willing to pay a small premium for jewelry and

fashion accessories that are handmade or made from rare materials such as pima cotton, silk and

alpaca wool. Canada’s market for jewelry and fashion accessories offers distinct price points at

low, mid and high-end segments. Competition in the industry is pushing retailers to carry items at

a wider range of price points in order to catch both the luxury and mid-range consumers.

High-end: Fine jewelry and designer accessories are luxury items that can sell for

thousands of dollars at specialty retailers, brand name stores or department stores. Sales

of fine jewelry tend to depend more on disposable income than on price promotions.

35

Mid-end: Medium priced jewelry is the most widespread in Canada, with approximately

70% of jewelry and fashion accessory here sold under $100 at the retail level. Profit

margins for costume jewelry are generally slimmer than for fine jewelry but are sold at

higher volumes following the fast fashion trend.

Low-end: Mass produced costume jewelry and fashion accessories can be sold at low

prices from $5 to $50 at mass merchandisers, discount retailers and even dollar stores.

These items are made from less durable materials and consumers generally do not expect

them to keep for a long lifespan.

Ethiopian made handloom woven products can fall in either of the above. The identified product

with respect to their manufacturing company’s price is presented as follow:

Table 9: Identified products, size and price range

S.N Name of company Identified product item Product size Price of the

product (USD) 1 Sabahar/Sabasilk P.L.C Beach towels, bath towels,

hand towels

Shawls

2 St. George Interior Decoration and Art Gallery

Cushion cover 54.13

Set (table mats, table runner & napkins)

105.50

Set (table mats and napkins)

73.40