project report of finance of sonal kumar

TRANSCRIPT

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 1/81

1

A

Summer Training

Project Report

On

“Mutual fund analysis & portfolio management in mutual funds for

Ifians Financial Advisor”

Submitted in

The Partial Fulfillment of the Requirements for Award of

PGDM-AICTE

(2010-2012)

Submitted By Under Guidance of

Sonal Kumar Prof. Pankaj Nandurkar

SINHGAD INSTITUTE OF BUISNESS ADMINISTRATION &

RESERARCH (SIBAR), KONDHWA

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 2/81

2

Table of Contents

Chapter No. Title Page No.

Declaration

Certificate from company

Certificate from guide

Acknowledgement

Project Proposal Sheet

I Executive Summary 1-3

II Profile of the Organization 4-8

III Industrial Profile 9-13

IV Objective and Scope of project 14-15

V Research Design & Methodology 16-17

VI Conceptual Background 18-43

VII Data Analysis 44-47

VIII Findings 48-49

IX On The Job Training 50-60

X Conclusion 61-62

XI Suggestions 63-64

XII Limitations 65-66

XIII Bibliography 67-68

XIV Annexure 69-70

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 3/81

3

DECLARATION

I, the undersigned, hereby declare that the Project Report entitled

“Mutual fund analysis & portfolio management in mutual funds for

Ifians Financial Advisor” Written and submitted by me to University of

Pune, in the partial fulfillment of the requirement for the award of degree of

Post graduate diploma in management (PGDM) under the Guidance of Prof.

****************. This is my original work and the conclusions drawn

therein are based on the material collected by myself.

Place: Sonal Kumar

Date: (PGDM-Fin)

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 4/81

4

College Certificate

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 5/81

5

Company Certificate

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 6/81

6

Acknowledgement

He who does not thanks for little, will not thanks for much

Talent and capabilities are of course necessary but opportunities and good guidance are

two very important things without which no person can climb those infant ladders

towards progress.

At the time of making this report I express my sincere gratitude to all of them.

During the course of this project various person have rendered valuable help &

guidance to me. I am highly grateful to Mr. Praveen Nagpal who allowed me to do mysummer training in his prestigious organization.

I am thankful to Mr. Praveen Nagpal again whose calm demeanor and willingness to

teach has been a great help in successfully completing the project. My learning has been

immeasurable and working under him was a great experience. My sincere thanks also

extend to all the staffs of. Ifians Financial advisor for providing a helpful work

environment and making our summer training an exciting and memorable event

I am extremely thankful and obliged to Prof. ********************** (Internal Project

Guide) for providing streamed guidelines since inception, till the completion of the

project.

I would also thank Ifians Financial Advisor Securities Ltd, employees and customers

whom I met during the course of this project, for their support and for providing

valuable information which helped me, complete this project successfully.

Sonal Kumar

(PGDM- Finance)

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 7/81

7

Project Proposal Sheet

Project Title:-

“Mutual fund analysis & portfolio management in mutual funds for Ifians

Financial Advisor”

Name of the Company:-

Ifians Financial Advisor

Servicing:-

Portfolio Management Services, Mutual Funds, Commodities,

Depository Services, Equities, Derivatives, My Broker (E-Broking),

and IPO

Project Head & Supervisor:-

Mr. Praveen Nagpal

Project Duration:-

30 Days: - 16th July 2010 to 15th Aug 2011

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 8/81

8

LIST OF TABLES & ILLUSTRATIONS

SR. NO. PARTICULARS PAGE.NO.

1. Calculation of NAV 24

2. Tool showing fund characteristics 32

3. Figures showing how to maximize returns

while minimizing risk

35

4. Figures showing Portfolio Models:-

Conservative Portfolio

Moderately Portfolio

Moderately Aggressive Portfolio

Very Aggressive Portfolio

36

3637

38

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 9/81

9

Abbreviations

1) MF – Mutual Fund

2) AMC – Asset Management Company

3) SEBI – Securities Exchange Board Of India

4) DP – Depository Participants

5) PPF – Public Provident Fund

6) NAV – Net Asset Value

7) HNIs – High Net Worth Individuals

8) CRM – Customer Relationship Management

9) AUM – Asset Under Management

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 10/81

10

Chapter – I

Executive Summary

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 11/81

11

Introduction:

Right from its existence, Banks, whether nationalize or corporate, always dominated

others, in case of public investments or retail investments. But in past few years due to

various reasons like continuously falling of interest rates, various scams etc. investors

will have to look for various other investments avenues that will give them better

returns with minimization of risks. Here Mutual Funds Industry has very important role

to play in providing alternate investment avenue to entire gamut of investors in

scientific and professional manner.

Indian Mutual Fund Industry has been definitely maturing over the period. In four

decades of its existence in India Mutual Funds have gone through various structural

changes and gained prominent position in Financial Industry. Because of easy of

investments, professional management and diversification more and more investors are

gaining confidence in Mutual Funds. Even government policies like abolishment of long

term capital benefit taxes added advantage to growth of Mutual Funds. This is all the

way is leading to pool of more and more money from retail investors into the Mutual

Funds.

So I carried out project in Mutual Funds and its Portfolio Management for the period of

two months starting from 1st June 2008 to 31st July 2008 to understand Mutual Funds,

Mutual Fund Industry, analyze the trend in Mutual Funds, what has been the

performance so far and mapping various methods of Client prospecting and servicing,

what are the factors that attracts the investors to invest in Mutual Funds over other

investment avenues.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 12/81

12

The project study focused on increasing brand awareness at retail level clients and

various activities those results in brand awareness among the same. This project also

consists of generating and getting clients, generating database and after sales services to

retain client and make them happy investor.

While analyzing trend, I tried to map how Asset under Management (AUM) varied over

the period with BSE-Sensex to facilitate feature projections. It has been done separately

for Equity Schemes, Income Schemes, Balanced Schemes and Liquid Schemes.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 13/81

13

Chapter - II

Profile of the Company

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 14/81

14

ifians www.ifians.com

Financial solutions made easy

Organization Profile

Company Name: “IFIANS”

Ifians, a Company promoted in 1997 by Mr. Pravin K. Nagpal to assist people to ease their

financial needs. Our aim is to provide professional services to our clients at a reasonable cost using

state of the art technology

Professional Activities:

1. Filing of Income Tax Returns for 7500+ salaried employees of various companies.

2. Accounting, Payroll, Filing of Income Tax Returns, Service Tax Returns for more than 20 Tax AuditFirms and Corporate (Pvt. Ltd Companies).

3. Registration of Proprietor, Partnership, Private Ltd and Limited Companies.

4. IRDA Approved Advisor for LIC, ICICI PRU LIFE & ICICI Lombard Gen. Ins. Co. Ltd.

5. Involved with Investment consultation i.e. Mutual funds and Company fixed deposits (In

association with Enam Securities Ltd, Mumbai)

6. Business Associates (Sub Broker) of Ifians Financial Advisor Securities Ltd. for NSE & BSE.

7. Consultants for Real Estate Management.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 15/81

15

8. CII Awarded Portfolio Management Consultant.

9. Experts for Counseling of Students for Project Guidance and support.

Office Address: Off No – 4 & 5, Bldg No: D-14, Giridhar Nagar,

Mumbai – Bangalore Highway, Warje, Pune – 411052

Tel: 020 – 64705448 Cell: 8975969348 (HR) Cell: 9822015448 (Dir.)

Email: [email protected] www.ifians.com

Support:

Front End Support: Mr. Pravin K. Nagpal

Back End Support: Mrs. Puneet P. Nagpal (LLB, MPM – Symbiosys.)

Additional Support: Mr. Sunil Bhutada (F.C.A.) (attached with “ifians” for last 4 years).

Dedicated Human resource: Ms. Swapnil Sahu

Employee strength:

Total Ten Employees. (Mostly qualified as MBA / CA or ICWA (inter).

Proposed: Thirty by 2011 end.

About the Promoter and Director: Mr. Pravin K. Nagpal

Total Years of Work Experience: 14 years+.

Date of Birth: 04.05.1974

Educational Qualification: B.Com, DTL, C.A., CII (UK) Certified Financial Advisor.

Completed 3 years of Articles Training under the guidance of Mr.Yashwant V. Joshi (FCA, Pune).

“Thank you for giving your most valuable time and your kindness”

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 16/81

16

PRODUCT AND SERVICES

Equities Portfolio Management Services

Derivatives Mutual Funds

My Broker (E-Broking) Commodities

IPO Depository Services

nstitutional

broking

Private Equitycommodity

Wealth Management

Investment

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 17/81

17

Chapter – III

Industrial Profile

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 18/81

18

Mutual Funds in India (1964-2000)

The end of millennium marks 36 years of existence of mutual funds in this country. The ride

through these 36 years is not been smooth. Investor opinion is still divided. While some are

for mutual funds others are against it.

UTI commenced its operations from July 1964. UTI came into existence during a period

marked by great political and economic uncertainty in India. With war on the borders and

economic turmoil that depressed the financial market, entrepreneurs were hesitant to enter

capital market.

The already existing companies found it difficult to raise fresh capital, as investors did not

respond adequately to new issues. Earnest efforts were required to canalize savings of the

community into productive uses in order to speed up the process of industrial growth.

The then Finance Minister, T.T. Krishnamachari set up the idea of a unit trust that would be

"open to any person or institution to purchase the units offered by the trust. However, this

institution as we see it, is intended to cater to the needs of individual investors, and even

among them as far as possible, to those whose means are small."

His ideas took the form of the Unit Trust of India, an intermediary that would help fulfill the

twin objectives of mobilizing retail savings and investing those savings in the capital market

and passing on the benefits so accrued to the small investors.

UTI commenced its operations from July 1964 "with a view to encouraging savings and

investment and participation in the income, profits and gains accruing to the Corporation

from the acquisition, holding, management and disposal of securities." Different provisions

of the UTI Act laid down the structure of management, scope of business, powers and

functions of the Trust as well as accounting, disclosures and regulatory requirements for the

Trust.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 19/81

19

One thing is certain – the fund industry is here to stay. The industry was one-entity show till

1986 when the UTI monopoly was broken when SBI and Canbank mutual fund entered the

arena. This was followed by the entry of others like BOI, LIC, GIC, etc. sponsored by public

sector banks. Starting with an asset base of Rs0.25bn in 1964 the industry has grown at a

compounded average growth rate of 26.34% to its current size of Rs1130bn.

The period 1986-1993 can be termed as the period of public sector mutual funds (PMFs).

From one player in 1985 the number increased to 8 in 1993. The party did not last long.

When the private sector made its debut in 1993-94, the stock market was booming.

The openings up of the asset management business to private sector in 1993 saw international

players like Morgan Stanley, Jardine Fleming, JP Morgan, George Soros and Capital

International along with the host of domestic players join the party. But for the equity funds,

the period of 1994-96 was one of the worst in the history of Indian Mutual Funds.

1999-2000 Year of the funds

Mutual funds have been around for a long period of time to be precise for 36 yrs but the year

1999 saw immense future potential and developments in this sector. This year signaled the

year of resurgence of mutual funds and the regaining of investor confidence in these MF‘s.

This time around all the participants are involved in the revival of the funds ----- the AMC‘s,

the unit holders, the other related parties. However the sole factor that gave lifr to the revival

of the funds was the Union Budget. The budget brought about a large number of changes in

one stroke. An insight of the Union Budget on mutual funds taxation benefits is provided

later.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 20/81

20

It provided centre stage to the mutual funds, made them more attractive and provides

acceptability among the investors. The Union Budget exempted mutual fund dividend given

out by equity-oriented schemes from tax, both at the hands of the investor as well as the

mutual fund. No longer were the mutual funds interested in selling the concept of mutual

funds they wanted to talk business, which would mean to increase asset base, and to get asset

base, and investor base they had to be fully armed with a whole lot of schemes for every

investor .So new schemes for new IPO‘s were inevitable. The quest to attract investors

extended beyond just new schemes. The funds started to regulate themselves and were all out

on winning the trust and confidence of the investors under the aegis of the Association of

Mutual Funds of India (AMFI)

One can say that the industry is moving from infancy to adolescence, the industry is maturing

and the investors and funds are frankly and openly discussing difficulties opportunities and

compulsions.

Future Scenario

The asset base will continue to grow at an annual rate of about 30 to 35 % over the next few

years as investor‘s shift their assets from banks and other traditional avenues. Some of the

older public and private sector players will either close shop or be taken over.

Out of ten public sector players five will sell out, close down or merge with stronger players

in three to four years. In the private sector this trend has already started with two mergers and

one takeover. Here too some of them will down their shutters in the near future to come.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 21/81

21

But this does not mean there is no room for other players. The market will witness a flurry of

new players entering the arena. There will be a large number of offers from various asset

management companies in the time to come. Some big names like Fidelity, Principal, Old

Mutual etc. are looking at Indian market seriously. One important reason for it is that most

major players already have presence here and hence these big names would hardly like to get

left behind.

The mutual fund industry is awaiting the introduction of derivatives in India as this would

enable it to hedge its risk and this in turn would be reflected in it‘s Net Asset Value (NAV).

SEBI is working out the norms for enabling the existing mutual fund schemes to trade in

derivatives. Importantly, many market players have called on the Regulator to initiate the

process immediately, so that the mutual funds can implement the changes that are required to

trade in Derivatives.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 22/81

22

Chapter – IV

Objective of the Study

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 23/81

23

Objectives:-

(1) To make investors aware of Ifians Financial Advisor.

(2) To understand ways of systematic financial planning.

(3) To compare various financial products.

(4) To study of basics of Mutual Fund market & overall industry.

(5) To enumerate risks associated with mutual fund scheme.

(6) To analyze mutual fund investment by comparing it‘s various investment avenues.

(7) To understand portfolio management in mutual Funds.

(8) To understand online trading and back office work at Ifians Financial Advisor.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 24/81

24

Chapter – V

Research Methodology

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 25/81

25

The focus of this chapter is on the methodology used for the collection of data for research.

Data constitutes the subject matter of the analyst. The primary sources of the collection of

sources of the collection of data are observations, Interviews and the questionnaire technique.

The secondary sources are collections of data are from the printed and annually published

materials..

Primary Data:

Data that is collected for the specific purpose at hand is called as primary Data.

Following methods are used to do this project:-

The history of the Ifians Financial Advisor.

People who came to give training in the Company.

People in mutual fund department.

Asking Questions to clients

Secondary Data:

Secondary data highlights the contextual familiarities for primary data collection. It provides

rich insights into the research process.

Secondary data is collected through following sources:

Visiting M.F sites.

Companies Website.

Reading leaflets, pamphlets, magazines, brochures that were already present in

the company.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 26/81

26

Sampling plan:

It includes all the information about universe, sample size, sample unit, sampling method,

sampling procedure, and contact method, sampling frame, data processing and place of

information.

Universe-Major Area in Pune region.

Sample size- 250 shop/coaching class/par lour

Sample Unit- Each individual shop/coaching class/par lour

Sampling procedure - Judgment and Convenience Sampling as met personally.

Contact method- Personal & Through calling.

TYPE OF SAMPLING:

PROBABILITY SAMPLING:

Simple Random Sampling

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 27/81

27

METHOD OF DATA ANALYSIS:

The methods followed by me arrange the data was as follows:

1). Collecting the data and arranging them as per the requirement. As the questions were

mostly close ended, so, I have not faced much problem.

2). After arranging the data, I have analyzed the data with the help of the pie charts and bar

graphs. These have helped me in making my research more presentable and understandable.

Sampling Methods-

There are mainly two sampling methods.

I) Probability Sampling

ii) Non-Probability Sampling

I) Probability Sampling:

In probability sampling method each unit of the population has the equal chance of

being selected in the sample. This method is sub-divided into following:-

Simple random sampling

Stratified random sampling

Cluster (area) sampling

ii) Non-probability:

In non-probability sampling researcher himself decide the basis of sample selection,

unlike the probability sampling in this method every unit of population does not have

the equal chance of being selected. This method is sub-divided in following types:

Convenience sampling

Judgment sampling

Quota sampling

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 28/81

28

Chapter – VI

Conceptual Background

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 29/81

29

A) INVESMENT AVENUES

1. Investment:

The money you earn is partly spent and the rest saved for meeting future expenses. Instead of

keeping the savings idle you may like to use savings in order to get return on it in the future.

This is called Investment.

2. Why should one invest?

One needs to invest to:

Earn return on your idle resources

Generate a specified sum of money for a specific goal in life

Make a provision for an uncertain future

One of the important reasons why one needs to invest wisely is to meet the cost of inflation.

3. Various options available for investment:

I. Physical Assets:

Real Estate

Real Estate investment is also on of the good investment option available. Real Estate

investment means investments in the Land, Buildings, Flats, and Houses etc. Now a day the

growth in the prices of real estate is very rapid. That‘s why investor gets good returns in this

investment. But the growth of real estate investment is in the long term only. In short term

there is no growth in this. It requires very huge investment. Only big investors can invest in

this... In Real Estate investment you will not have the liquidity. Buying & selling of property

is not so easy at least in India. The Procedures & Documentation of ‗Transfer of Property‘ is

very lengthy. It takes time & money. For transfer you have pay taxes & duties & some

charges.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 30/81

30

Commodity:

Commodities market, contrary to the beliefs of many people, has been in existence in India

through the ages. However the recent attempt by the Government to permit Multi-commodity

National levels exchanges has indeed given it, a shot in the arm. As a result two exchanges

Multi Commodity Exchange (MCX) and National Commodity and derivatives Exchange

(NCDEX) have come into being. These exchanges, by virtue of their high profile promoters

and stakeholders, bundle in themselves, online trading facilities, robust surveillance measures

and a hassle-free settlement system. The futures contracts available on a wide spectrum of

commodities like Gold, Silver, Cotton, Steel, Soya oil, Soya beans, Wheat, Sugar, Channa

etc., provide excellent opportunities for hedging the risks of the farmers,

Importers, exporters, traders and large-scale consumers. They also make open an avenue for

quality investments in precious metals. The commodities market, as the movements of the

stock market or debt market do not affect it provides tremendous opportunities for better

diversification of risk. Realizing this fact, even mutual funds are contemplating of entering

into this market.

II Financial Assets:

Investment in Capital Market:

Capital Market is a place where buyers and sellers of securities can enter into transactions to

purchase and sell shares, bonds, debentures etc. Further, it performs an important role of

enabling corporate, entrepreneurs to raise resources for their companies and business ventures

through public issues. Transfer of resources from those having idle resources (investors) to

others who have a need for them (corporate) is most efficiently achieved.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 31/81

31

Through the securities market. Stated formally, securities markets provide channels for

reallocation of savings to investments and entrepreneurship. Savings are linked to

investments by a variety of intermediaries, through a range of financial products,

Called ‗Securities‘.

Small Saving Instruments:

It is again classified in to short term and long term saving instruments.

Short term saving instruments:

Broadly speaking, savings bank account, money market/liquid funds and fixed deposits with

banks may be considered as short-term financial investment options:

Savings Bank Account: It is often the first banking product people use, which offers low

interest (4%-5% p.a.), making them only marginally better than fixed deposits.

Money Market or Liquid Funds:

These funds are a specialized form of mutual funds that invest in extremely short-term fixed

income instruments and thereby provide easy liquidity. Unlike most mutual funds, money

market funds are primarily oriented towards protecting your capital and then, aim to

maximise returns. Money market funds usually yield better returns than savings accounts, but

lower than bank fixed deposits.

Fixed Deposits with Banks:

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 32/81

32

These are also referred to as term deposits and minimum investment period for bank FDs is

30 days. Fixed Deposits with banks are for investors with low risk appetite, and may be

considered for 6-12 months investment period as normally interest on less than 6 months

bank FDs is likely to be lower than money market fund returns.

Long Term Financial options available for investment:

Post Office Savings Schemes, Public Provident Fund, Company Fixed Deposits, Bonds and

Debentures, Mutual Funds etc.

Public Provident Fund:

A long-term savings instrument with a maturity of 15 years and interest payable at 8% per

annum compounded annually. A PPF account can be opened through a nationalized bank at

anytime during the year and is open all through the year for depositing money. Tax benefits

can be availed for the amount invested and interest accrued is tax-free. A withdrawal is

permissible every year from the seventh. Financial year of the date of opening of the account

and the amount of withdrawal will be limited to 50% of the balance at credit at the end of the

4th year immediately preceding the year in which the amount is withdrawn or at the end of

the preceding year whichever is lower the amount of loan if any.

Bonds:

It is a fixed income (debt) instrument issued for a period of more than one year with the

purpose of raising capital. The central or state government, corporations and similar

institutions sell bonds. A bond is generally a promise to repay the principal along with a fixed

rate of interest on a specified date, called the Maturity Dat e

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 33/81

33

B) PRODUCT PROFILE

MUTUAL FUNDS:-

These are funds operated by an investment company, which raises money from the public and

invests in a group of assets (shares, debentures etc.), in accordance with a stated set of

objectives. It is a substitute for those who are unable to invest directly in equities or debt

because of resource, time or knowledge constraints. Benefits include professional money

management, buying in small amounts and diversification. Mutual fund units are issued and

redeemed by the Fund Management Company based on the fund's net Asset value (NAV),

which is determined at the end of each trading session.

Diagrammatical Representation of the concept of mutual funds.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 34/81

34

Calculation of NAV

The most important part of the calculation is the valuation of the assets owned by the fund.

Once it is calculated, the NAV is simply the net value of assets divided by the number of

units outstanding. The detailed methodology for the calculation of the asset value is given

below.

NAV = NET VALUE OF ASSETS

NUMBER OF UNITS OUTSTANDING

Asset value is equal to

Sum of market value of shares/debentures

+ Liquid assets/cash held, if any

+ Dividends/interest accrued

Amount due on unpaid assets

Expenses accrued but not paid

Details on the above items:-

For liquid shares/debentures, valuation is done on the basis of the last or closing

market price on the principal exchange where the security is traded

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 35/81

35

For illiquid and unlisted and/or thinly traded shares/debentures, the value has to be

estimated. For shares, this could be the book value per share or an estimated market

price if suitable benchmarks are available. For debentures and bonds, value is

estimated on the basis of yields of comparable liquid securities after adjusting for

illiquidity. The value of fixed interest bearing securities moves in a direction opposite

to interest rate changes Valuation of debentures and bonds is a big problem since most

of them are unlisted and thinly traded. This gives considerable leeway to the AMCs

on valuation and some of the AMCs are believed to take advantage of this and adopt

flexible valuation policies depending on the situation.

Interest is payable on debentures/bonds on a periodic basis say every 6 months. But,

with every passing day, interest is said to be accrued, at the daily interest rate, which

is calculated by dividing the periodic interest payment with the number of days in

each period. Thus, accrued interest on a particular day is equal to the daily interest

rate multiplied by the number of days since the last interest payment date.

You can make money from a mutual fund in three ways:

1) Income is earned from dividends on stocks and interest on bonds. A fund pays out nearly

all income it receives over the year to fund owners in the form of a distribution.

2) If the fund sells securities that have increased in price, the fund has a capital gain. Most

funds also pass on these gains to investors in a distribution.

3) If fund holdings increase in price but are not sold by the fund manager, the fund's shares

increase in price. You can then sell your mutual fund shares for a profit.

4)Funds will also usually give you a choice either to receive a check for distributions or to

reinvest the earnings and get more shares.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 36/81

36

Mutual Funds: Costs (Look On It)

Costs are the biggest problem with mutual funds. These costs eat into your return, and they

are the main reason why the majority of funds end up with sub-par performance.

What's even more disturbing is the way the fund industry hides costs through a layer of

financial complexity and jargon. Some critics of the industry say that mutual fund companies

get away with the fees they charge only because the average investor does not understand

what he/she is paying for.

Annual Fund Operating Expenses

Management Fees — fees that are paid out of fund assets to the fund's investment

adviser for investment portfolio management, any other management fees payable to

the fund's investment adviser or its affiliates, and administrative fees payable to the

investment adviser that are not included in the "Other Expenses" category (discussed

below).

Distribution [and/or Service] Fees — fees paid by the fund out of fund assets to

cover the costs of marketing and selling fund shares and sometimes to cover the costs

of providing shareholder services. "Distribution fees" include fees to compensate

brokers and others who sell fund shares and to pay for advertising, the printing and

mailing of prospectuses to new investors, and the printing and mailing of sales

literature. "Shareholder Service Fees" are fees paid to persons to respond to investor

inquiries and provide investors with information about their investments.

Other Expenses — expenses not included under "Management Fees" or "Distribution

or Service (12b-1) Fees," such as any shareholder service expenses that are not

already included in the 12b-1 fees, custodial expenses, legal and accounting expenses,

transfer agent expenses, and other administrative expenses.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 37/81

37

Total Annual Fund Operating Expenses ("Expense Ratio") — the line of the fee

table that represents the total of all of a fund's annual fund operating expenses,

expressed as a percentage of the fund's average net assets. Looking at the expense

ratio can help you make comparisons among funds.

ADVANTAGE’S OF MUTUAL FUNDS

Professional Management - The primary advantage of funds (at least theoretically)

is the professional management of your money. Investors purchase funds because

they do not have the time or the expertise to manage their own portfolio. A mutual

fund is a relatively inexpensive way for a small investor to get a full-time manager to

make and monitor investments.

Diversification - By owning shares in a mutual fund instead of owning individual

stocks or bonds, your risk is spread out. The idea behind diversification is to invest in

a large number of assets so that a loss in any particular investment is minimized by

gains in others. In other words, the more stocks and bonds you own, the less any one

of them can hurt you Large mutual funds typically own hundreds of different stocks

in many different industries.

Economies of Scale - Because a mutual fund buys and sells large amounts of

securities at a time, its transaction costs are lower than you as an individual would

pay.

Liquidity - Just like an individual stock, a mutual fund allows you to request that

your shares be converted into cash at any time.

Simplicity - Buying a mutual fund is easy! Pretty well any bank has its own line of

mutual funds, and the minimum investment is small. Most companies also have

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 38/81

38

automatic purchase plans whereby as little as $100 can be invested on a monthly

basis.

DISADVANTAGES OF MUTUAL FUNDS:

Professional Management- Did you notice how we qualified the advantage of

professional management with the word "theoretically"? Many investors debate

over whether or not the so-called professionals are any better than you or I at

picking stocks. Management is by no means infallible, and, even if the fund loses

money, the manager still takes his/her cut.

Costs - Mutual funds don't exist solely to make your life easier--all funds are in it

for a profit. The mutual fund industry is masterful at burying costs under layers of

jargon. These costs are so complicated that in this tutorial we have devoted an

entire section to the subject.

Dilution - It's possible to have too much diversification because funds have small

holdings in so many different companies, high returns from a few investments

often don't make much difference on the overall return. Dilution is also the result

of a successful fund getting too big. When money pours into funds that have had

strong success, the manager often has trouble finding a good investment for all

the new money.

Taxes - When making decisions about your money, fund managers don't consider

your personal tax situation. For example, when a fund manager sells a security, a

capital-gain tax is triggered, which affects how profitable the individual is from

the sale. It might have been more advantageous for the individual to defer the

capital gains liability.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 39/81

39

TYPES OF MUTUAL FUNDS

No matter what type of investor you are there is bound to be a mutual fund that fits your

style. According to the last count there are over 10,000 mutual funds in North America! That

means there are more mutual funds than stocks.

It's important to understand that each mutual fund has different risks and rewards. In general,

the higher the potential return, the higher the risk of loss. Although some funds are less risky

than others, all funds have some level of risk--it's never possible to diversify away all risk.

This is a fact for all investments.

Each fund has a predetermined investment objective that tailors the fund's assets, regions of

investments, and investment strategies. At the fundamental level, there are three varieties of

mutual funds:

1) Equity funds (stocks)

2) Fixed-income funds (bonds)

3) Money market funds

All mutual funds are variations of these three asset classes. For example, while equity

funds that invest in fast-growing companies are known as growth funds, equity funds that

invest only in companies of the same sector or region are known as specialty funds.

Let's go over the many different flavors of funds. We'll start with the safest and then work

through to the more risky.

Money Market Funds

the money market consists of short-term debt instruments, mostly T-bills. This is a safe

place to park your money. You won't get great returns, but you won't have to worry about

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 40/81

40

losing your principal. A typical return is twice the amount you would earn in a regular

checking/savings account and a little less than the average certificate of deposit (CD).

We've got a whole tutorial on the money market if you'd like to learn more about it.

Bond/Income Funds

Income funds are named appropriately: their purpose is to provide current income on a

steady basis. When referring to mutual funds, the terms "fixed-income," "bond," and

"income" are synonymous. These terms denote funds that invest primarily in government

and corporate debt. While fund holdings may appreciate in value, the primary objective of

these funds is to provide a steady cash flow to investors. As such, the audience for these

funds consists of conservative investors and retirees.

Bond funds are likely to pay higher returns than certificates of deposit and money market

investments, but bond funds aren't without risk. Because there are many different types of

bonds, bond funds can vary dramatically depending on where they invest. For example, a

fund specializing in high-yield junk bonds is much more risky than a fund that invests in

government securities; also, nearly all bond funds are subject to interest rate risk, which

means that if rates go up the value of the fund goes down.

Balanced Funds

The objective of these funds is to provide a "balanced" mixture of safety, income, and

capital appreciation. The strategy of balanced funds is to invest in a combination of fixed-

income and equities. A typical balanced fund might have a weighting of 60% equity and

40% fixed-income. The weighting might also be restricted to a specified maximum or

minimum for each asset class.

A similar type of fund is known as an asset allocation fund. Objectives are similar to

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 41/81

41

those of a balanced fund, but these kinds of funds typically do not have to hold a specified

percentage of any asset class. The portfolio manager is therefore given freedom to switch

the ratio of asset classes as the economy moves through the business cycle.

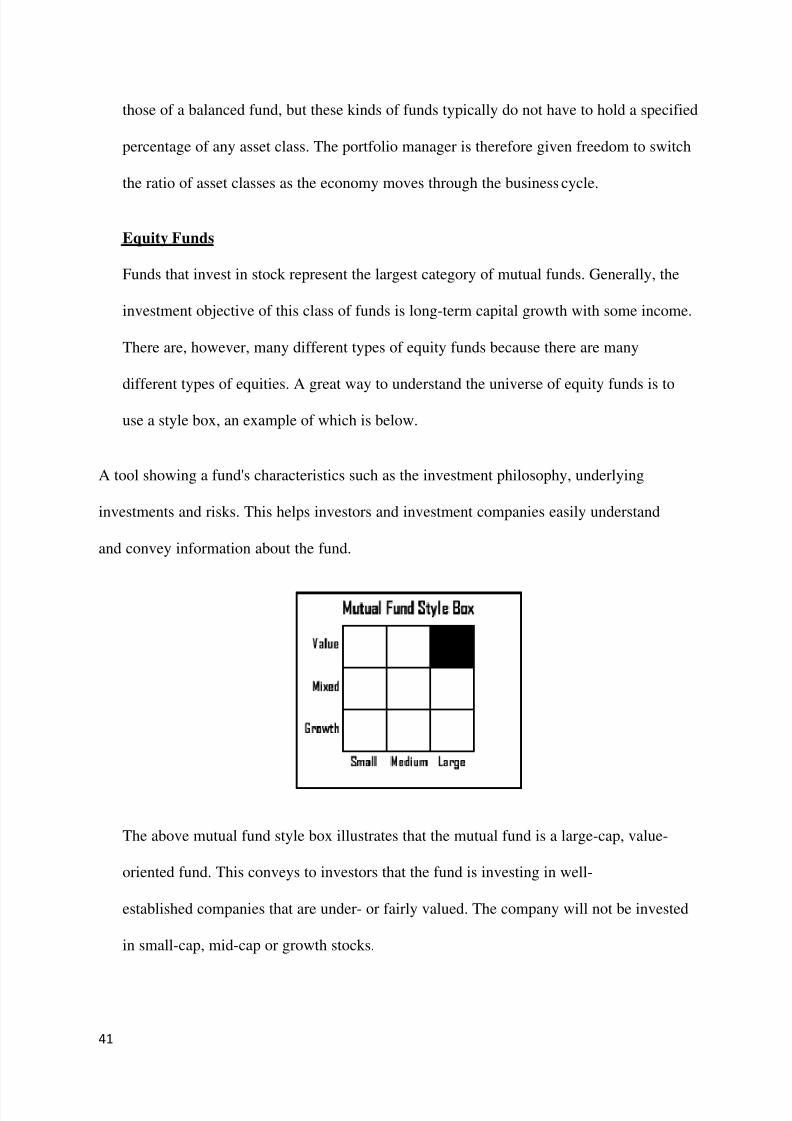

Equity Funds

Funds that invest in stock represent the largest category of mutual funds. Generally, the

investment objective of this class of funds is long-term capital growth with some income.

There are, however, many different types of equity funds because there are many

different types of equities. A great way to understand the universe of equity funds is to

use a style box, an example of which is below.

A tool showing a fund's characteristics such as the investment philosophy, underlying

investments and risks. This helps investors and investment companies easily understand

and convey information about the fund.

The above mutual fund style box illustrates that the mutual fund is a large-cap, value-

oriented fund. This conveys to investors that the fund is investing in well-

established companies that are under- or fairly valued. The company will not be invested

in small-cap, mid-cap or growth stocks.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 42/81

42

MANAGING PORTFOLIO

ASSET ALLOCATION

The process of dividing a portfolio among major asset categories such as bonds, stocks or

cash. The purpose of asset allocation is to reduce risk by diversifying the portfolio. The ideal

asset allocation differs based on the risk tolerance of the investor. For example, a young

executive might have an asset allocation of 80% equity, 20% fixed income, while a retiree

would be more likely to have 80% in fixed income and 20% equities.

What Is Asset Allocation?

Asset allocation is an investment portfolio technique that aims to balance risk and create

diversification by dividing assets among major categories such as cash, bonds, stocks, real

estate and derivatives. Each asset class has different levels of return and risk, so each will

behave differently over time. For instance, while one asset category increases in value,

another may be decreasing or not increasing as much. Some critics see this balance as a

settlement for mediocrity, but for most investors it's the best protection against major loss

should things ever go amiss in one investment class or sub-class.

The consensus among most financial professionals is that asset allocation is one of the most

important decisions that investors make. In other words, your selection of stocks or bonds is

secondary to the way you allocate your assets to high and low-risk stocks, to short and long-

term bonds, and to cash on the sidelines. We must emphasize that there is no simple formula

that can find the right asset allocation for every individual.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 43/81

43

ACHIEVING OPTIMAL ASSET ALLOCATION

The important task of appropriately allocating your available investment funds amongdifferent assets classes can seem daunting, with so many securities to choose from.

Essentially, asset allocation is an organized and effective method of diversification. To

help determine which securities, asset classes and subclasses are optimal for your portfolio;

let's define some briefly:

Large-cap stock - These are shares issued by large companies with a market

capitalization generally greater than $10 billion.

Mid-cap stock - These are issued by mid-sized companies with a market cap

generally between $2 billion and $10 billion.

Small-cap stocks - These represent smaller-sized companies with a market cap of less

than $2 billion. These types of equities tend to have the highest risk due to lower

liquidity.

International securities - These types of assets are issued by foreign companies and

listed on a foreign exchange. International securities allow an investor to diversify

outside of his or her country, but they also have exposure to country risk - the risk that

a country will not be able to honor its financial commitments.

Emerging markets - This category represents securities from the financial markets of

a developing country. Although investments in emerging markets offer a higher

potential return, there is also higher risk, often due to political instability, country risk

and lower liquidity. The fixed-income asset class comprises debt securities that pay

the holder a set amount of interest, periodically or at maturity, as well as the returnof principal when the security matures. These securities tend to have lower volatility

than equities, and have lower risk because of the steady income they provide. Note

that though the issuer promises payment of income, there is a risk of default. Fixed-

income securities include corporate and government bonds.

Money market - Money market securities are debt securities that are extremely liquid

investments with maturities of less than one year. Treasury bills make up the majority

of these types of securities.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 44/81

44

Real-estate investment trusts (REITs) - REITs trade similarly to equities, except the

underlying asset is a share of a pool of mortgages or properties, rather than ownership

of a company.

MAXIMIZING RETURN WHILE MINIMISING RISK

The main goal of allocating your assets among various asset classes is to maximize return for

your chosen level of risk, or stated another way, to minimize risk given a certain expected

level of return. Of course to maximize return and minimize risk, you need to know the risk-

return characteristics of the various asset classes. The following chart compares the risk and

potential return of some of the more popular ones:

As each asset class has varying levels of return for a certain risk, your risk tolerance,

investment objectives, time horizon and available capital will provide the basis for the asset

composition of your portfolio.

To make the asset allocation process easier for clients, many investment companies create a

series of model portfolios, each comprising different proportions of asset classes. These

portfolios of different proportions satisfy a particular level of investor risk tolerance. In

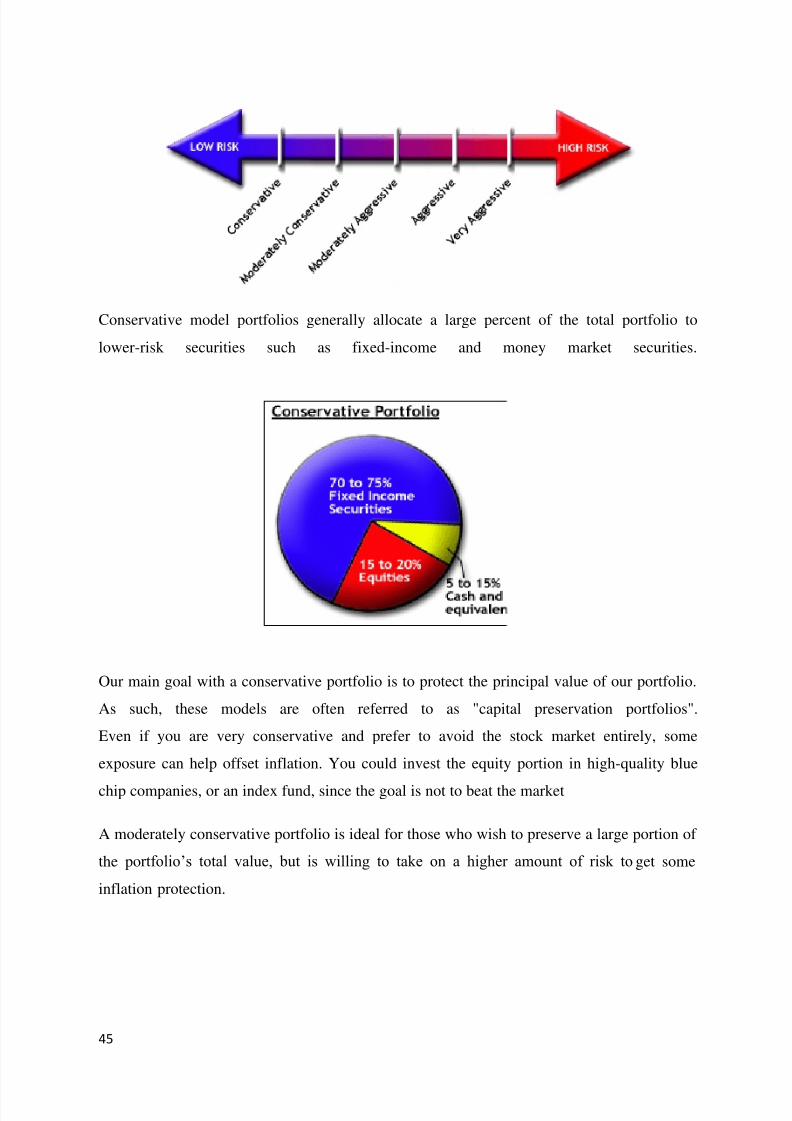

general, these model portfolios range from conservative to very aggressive:

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 45/81

45

Conservative model portfolios generally allocate a large percent of the total portfolio to

lower-risk securities such as fixed-income and money market securities.

Our main goal with a conservative portfolio is to protect the principal value of our portfolio.

As such, these models are often referred to as "capital preservation portfolios".

Even if you are very conservative and prefer to avoid the stock market entirely, some

exposure can help offset inflation. You could invest the equity portion in high-quality blue

chip companies, or an index fund, since the goal is not to beat the market

A moderately conservative portfolio is ideal for those who wish to preserve a large portion of

the portfolio‘s total value, but is willing to take on a higher amount of risk to get some

inflation protection.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 46/81

46

A common strategy within this risk level is called "current income". With this strategy, you

chose securities that pay a high level of dividends or coupon payments.

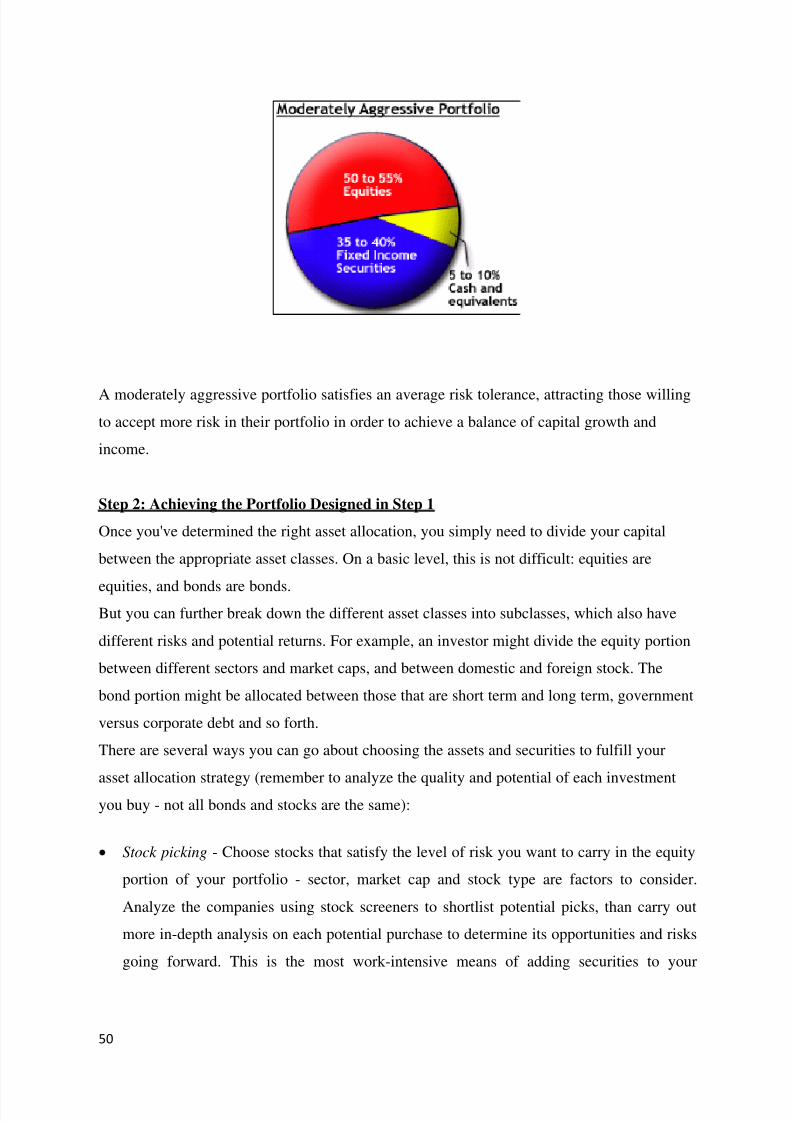

Moderately aggressive model portfolios are often referred to as "balanced portfolios" since

the asset composition is divided almost equally between fixed-income securities and equities

in order to provide a balance of growth and income.

Since these moderately aggressive portfolios have a higher level of risk than those

conservative portfolios mentioned above, select this strategy only if you have a longer time

horizon (generally more than five years), and have a medium level of risk tolerance.

Aggressive portfolios mainly consist of equities, so these portfolios' value tends to fluctuate

widely. If you have an aggressive portfolio, your main goal is to obtain long-term growth of

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 47/81

47

capital. As such the strategy of an aggressive portfolio is often called a "capital growth"

strategy.

To provide some diversification, investors with aggressive portfolios usually add some fixed-

income securities.

Very aggressive portfolios consist almost entirely of equities. As such, with a very aggressive

portfolio, your main goal is aggressive capital growth over a long time horizon.

Since these portfolios carry a considerable amount of risk, the value of the portfolio will vary

widely in the short term.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 48/81

48

MAINTAINING YOUR PORTFOLIO

Once you have chosen your portfolio investment strategy, it is important to conduct periodic

portfolio reviews, as the value of the various assets within your portfolio will change,

affecting the weighting of each asset class. For example, if you start with a moderately

conservative portfolio, the value of the equity portion may increase significantly during the

year, making your portfolio more like that of an investor practicing a balanced portfolio

strategy, which is higher risk!

In order to reset your portfolio back to its original state, you need to rebalance your portfolio.

Rebalancing is the process of selling portions of your portfolio that have increased

significantly, and using those funds to purchase additional units of assets that have declined

slightly or increased at a lesser rate. This process is also important if your investment strategy

or tolerance for risk has changed.

A GUIDE TO PORTFOLIO CONSTRUCTION

In today's financial marketplace, a well-maintained portfolio is vital to any investor's success.

As an individual investor, you need to know how to determine an asset allocation which best

conforms to your personal investment goals and strategies. In other words, your portfolio

should meet your future needs for capital and give you peace of mind. Investors can construct

portfolios aligned to their goals and investment strategies by following a systematic

approach. Here we go over some essential steps for taking such an approach.

Step 1: Determining the Appropriate Asset Allocation for You

Ascertaining your individual financial situation and investment goals is the first task in

constructing a portfolio. Important items to consider are age, how much time you have to

grow your investments, as well as amount of capital to invest and future capital needs. A

single college graduate just beginning his or her career and a 55-year-old married person

expecting to help pay for a child's college education and plans to retire soon will have

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 49/81

49

disparate investment strategies. A second factor to take into account is your personality and

risk tolerance. Are you the kind of person who is willing to risk some money for the

possibility of greater returns? Everyone would like to reap high returns year after year, but if

you are unable to sleep at night when your investments take a short-term drop, chances arethe high returns from those assets are not worth stressful.

As you can see, clarifying your current situation and your future needs for capital, as well as

your risk tolerance, together will determine how your investments should be allocated among

different asset classes. The possibility of greater returns comes at the expense of greater risk

of losses (a principle known as the risk/return tradeoff) - you don't want to eliminate risk so

much as optimize it for your unique condition and style. For example, the young person who

won't have to depend on his or her investments for income can afford to take greater risks in

the quest for high returns. On the other hand, the person nearing retirement needs to focus on

protecting his or her assets and drawing income from these.

Generally, the more risk you can bear, the more aggressive your portfolio will be, devoting a

larger portion to equities and less to bonds and other fixed-income securities. Conversely, the

less risk that's appropriate, the more conservative your portfolio will be. Here are two

examples: one suitable for a conservative investor and another for the moderately aggressive

investor.

The main goal of a conservative portfolio is to protect its value. The allocation shown above

would yield current income from the bonds, and would also provide some long-term capital

growth potential from the investment in high-quality equities.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 50/81

50

A moderately aggressive portfolio satisfies an average risk tolerance, attracting those willing

to accept more risk in their portfolio in order to achieve a balance of capital growth and

income.

Step 2: Achieving the Portfolio Designed in Step 1

Once you've determined the right asset allocation, you simply need to divide your capital

between the appropriate asset classes. On a basic level, this is not difficult: equities are

equities, and bonds are bonds.But you can further break down the different asset classes into subclasses, which also have

different risks and potential returns. For example, an investor might divide the equity portion

between different sectors and market caps, and between domestic and foreign stock. The

bond portion might be allocated between those that are short term and long term, government

versus corporate debt and so forth.

There are several ways you can go about choosing the assets and securities to fulfill your

asset allocation strategy (remember to analyze the quality and potential of each investmentyou buy - not all bonds and stocks are the same):

Stock picking - Choose stocks that satisfy the level of risk you want to carry in the equity

portion of your portfolio - sector, market cap and stock type are factors to consider.

Analyze the companies using stock screeners to shortlist potential picks, than carry out

more in-depth analysis on each potential purchase to determine its opportunities and risks

going forward. This is the most work-intensive means of adding securities to your

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 51/81

51

portfolio, and requires you to regularly monitor price changes in your holdings and stay

current on company and industry news.

Bond picking - When choosing bonds, there are several factors to consider including the

coupon, maturity, the bond type and rating, as well as the general interest rate

environment.

Mutual funds - Mutual funds are available for a wide range of asset classes and allow you

to hold stocks and bonds that are professionally researched and picked by fund managers.

Of course, fund managers charge a fee for their services, which will detract from your

returns. Index funds are another choice as they tend to have lower fees since they mirror

an established index and are thus passively managed.

Exchange-traded funds (ETFs) - If you prefer not to invest with mutual funds, ETFs can

be a viable alternative. You can basically think of ETFs as mutual funds that trade like a

stock. ETFs are similar to mutual funds in that they represent a large basket of stocks -

usually grouped by sector, capitalization, country and the like - except they are not

actively managed, but instead track a chosen index or other basket of stocks. Because

they are passively managed, ETFs offer cost savings over mutual funds while providing

diversification. ETFs also cover a wide range of asset classes and can be a useful tool to

round out your portfolio.

Step 3: Re-assessing Portfolio Weightings

Once you have an established portfolio, you need to analyze and rebalance it periodically

because market movements may cause your initial weightings to change. To assess your

portfolio's actual asset allocation, quantitatively categorize the investments and determine

their values' proportion to the whole.

The other factors that are likely to change over time are your current financial situation,

future needs and risk tolerance. If these things change, you may need to adjust your portfolio

accordingly. If your risk tolerance has dropped, you may need to reduce the amount of

equities held. Or perhaps you're now ready to take on greater risk and your asset allocation

requires a small proportion of your assets to be held in riskier small-cap stocks.

Essentially, to rebalance, you need to determine which of your positions are over-weighted

and those that are under-weighted. For example, say you are holding 30% of your current

assets in small-cap equities, while your asset allocation suggests you should only have 15%

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 52/81

52

of your assets kept in that class. You need to determine how much of this position you need

to reduce and allocate to other classes.

Step 4: Rebalancing Strategically

Once you have determined which securities you need to reduce and by how much, decide

which under-weighted securities you will buy with the proceeds from selling the over-

weighted securities. To choose your securities, use the approaches discussed in step 2.

When selling assets to rebalance your portfolio, take a moment to consider the tax

implications of readjusting your portfolio. Perhaps your investment in growth stocks has

appreciated strongly over the past year, but if you were to sell all of your equity positions to

rebalance your portfolio, you may incur significant capital gains taxes. In this case it might be

more beneficial to simply not contribute any new funds to that asset class in the future while

continuing to contribute to other asset classes. This will reduce your growth stocks' weighting

in your portfolio over time without incurring capital gains taxes.

At the same time, however, always consider the outlook of your securities. If you suspect that

those same over-weighted growth stocks are ominously ready to fall, you may want to sell in

spite of the tax implications. Analyst opinions and research reports can be useful tools to help

gauge the outlook for your holdings. And tax-loss selling is a strategy you can apply to

reduce tax implications.

Step 5 Remember the Importance of Diversification.

Throughout the entire portfolio construction process, it is vital that you remember to maintain

your diversification above all else. It is not enough simply to own securities from each asset

class; you must also diversify within each class. Ensure that your holdings within a given

asset class are spread across an array of subclasses and industry sectors.

As we mentioned, investors can achieve excellent diversification by utilizing mutual funds

and ETFs. These investment vehicles allow individual investors to obtain the economies of scale that large fund managers enjoy, which the average person would not be able to produce

with a small amount of money.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 53/81

53

Chapter - VII

Data Presentation, Analysis and

Interpretation

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 54/81

54

A ROAD MAP FOR YOUR INVESTMENTS

As per my study I have taken data of various age group people like age group of 20‘s ,30‘s

etc

According to the study I have drawn this table which easily shows the content of the study

and gives the idea that which type of portfolio suited to which age group and how we can

make different asset allocation groups suited to various age group peoples.

Let’s take a look on this

STAGE AGE CIRCUMSTANCES INVESTMENT STRATEGY

I-Young

Adult

20s Has no dependants, low

investible surplus

Pursue growth aggressively as risk

taking ability is high at this stage..

II-Young

family

30’s Married, with young

children; starts investing in

earnest

Continue aggressive wealth

creation.

III-Mature

family

40’s Higher education of

children approaching;

income peaking

Start lowering risk in investment

portfolio by moving funds to safer

instruments.

IV-Empty

nesters

50’s Children independent;

surpluses peak; preparing

for liquidation

Divert new surpluses to building

retirement corpus; keep reducing

portfolio risk

V-Retired 60+ Creating regular cash

flows and beating

inflation and priority

Create adequate cash flows from

safe investments.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 55/81

55

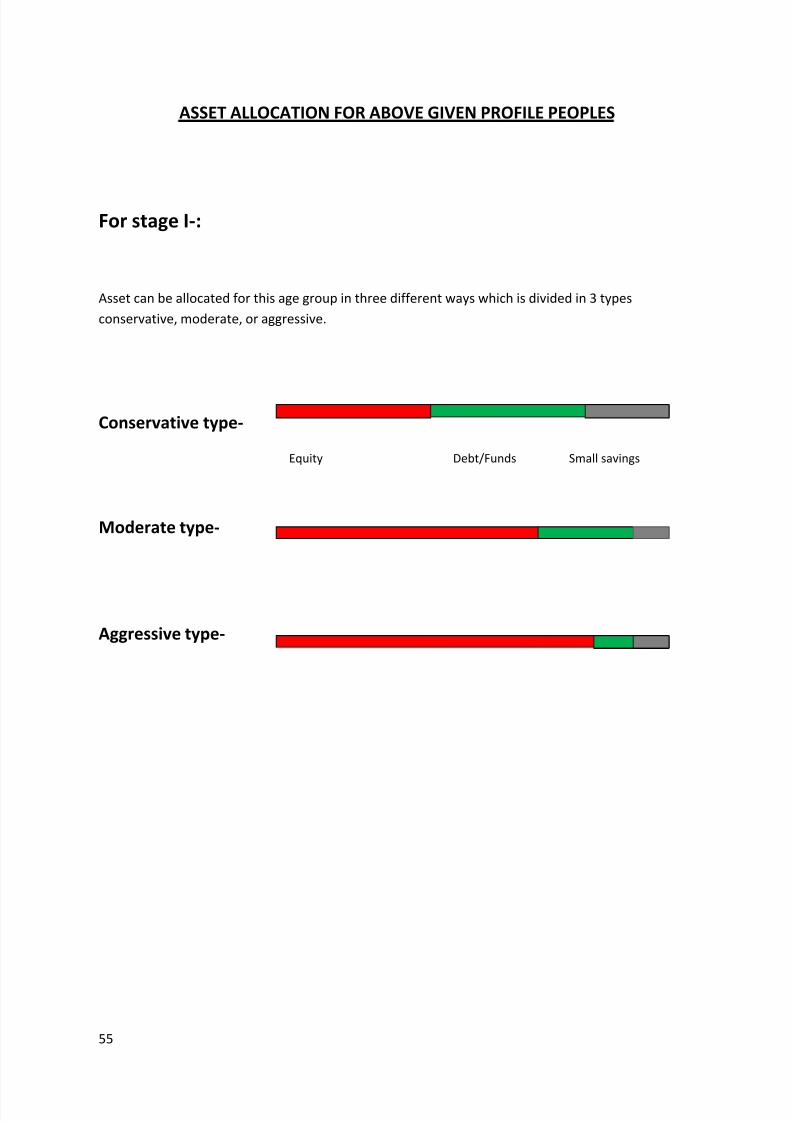

ASSET ALLOCATION FOR ABOVE GIVEN PROFILE PEOPLES

For stage I-:

Asset can be allocated for this age group in three different ways which is divided in 3 types

conservative, moderate, or aggressive.

Conservative type-

Equity Debt/Funds Small savings

Moderate type-

Aggressive type-

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 56/81

56

For stage II-:

Conservative type-

Equity Debt/Funds Small savings

Moderate type-

Aggressive type-

For stage III-:

Conservative type-

Equity Debt/Funds Small savings

Moderate type-

Aggressive type-

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 57/81

57

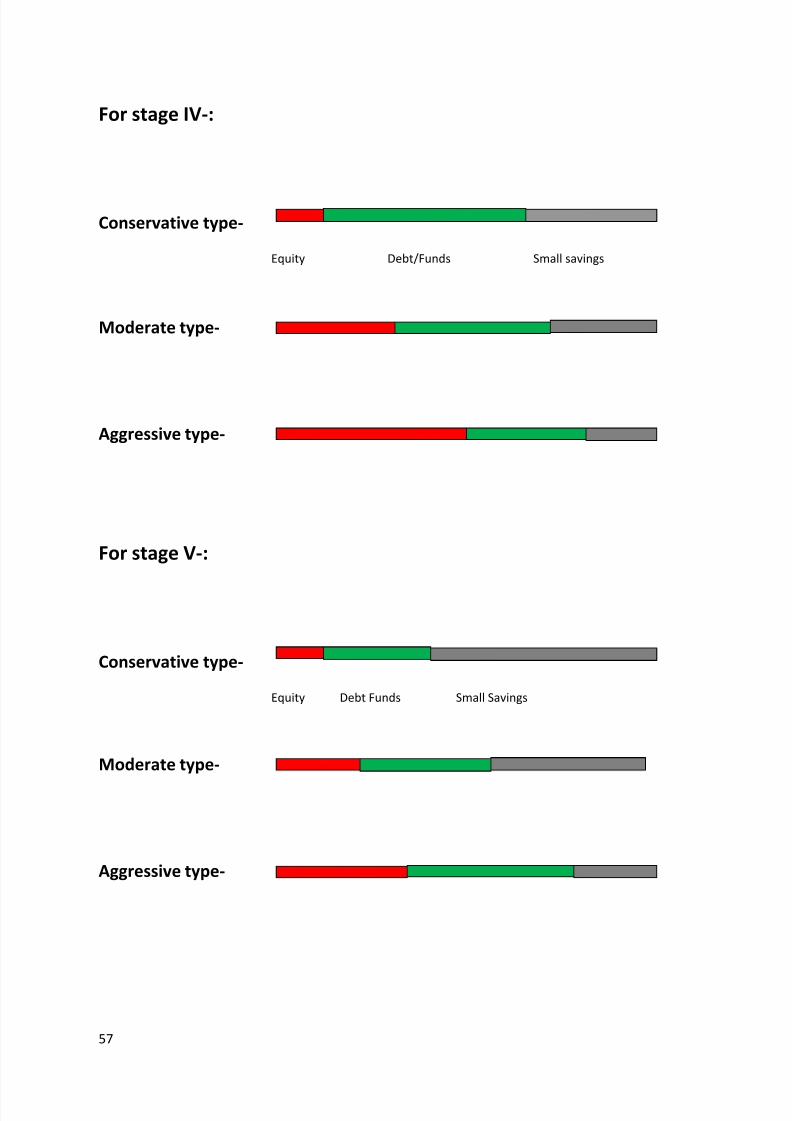

For stage IV-:

Conservative type-

Equity Debt/Funds Small savings

Moderate type-

Aggressive type-

For stage V-:

Conservative type-

Equity Debt Funds Small Savings

Moderate type-

Aggressive type-

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 58/81

58

Chapter – VIII

Findings

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 59/81

59

Finding:

Generally speaking when you are young, you can invest a greater proportion in equities. Atthat stage financial responsibility are fewer, and you can commit to equities for long periods

of time, which help you reap the unmatched returns they promise. Also since you are not

relying on this money to meet recurring expenses or approaching financial goal, losing some

of it temporarily in the pursuit of higher returns won‘t have you reach for the panic button or

strain your finances as much as it would in later years. As you grow older, your portfolio

should progressively tilt towards debt. At that stage of life, safety of principal becomes more

important than growth. Approaching retirement your prime concern should be putting in

place an alternative income stream, which is better met by debt than equity.

Based on the study I have drawn up indicative asset allocation models to see you through life.

These asset break ups are not sacrosanct. Your asset allocation can differ from my study at all

stages, depending on your life circumstances, financial needs and investing preferences. For

example approaching retirement you find that even after ensuring an alternative income

stream you still have some surplus left from which you would like higher returns. If you

don‘t mind the uncertainty you can stretch your equity allocation suitably.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 60/81

60

Chapter - IX

On The Job Training

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 61/81

61

Purpose-:

OJT is basically to give intern exposure to the outside world and it help to teach

him/her the real world work by giving him practical knowledge. Through OJT I learn that the

theory we have learned is difficult to implement in practical work. And we have to apply

them in a very different way.

As I am learning about mutual funds, handling the back office work etc. Before this I was just

aware of the theory part of it i.e. definition of mutual funds, its requirement, why a company

need additional capital etc. But after working here I came to know that it is very important to

learn the practical procedure of handling the mutual funds because the main part is the

dealing with the customers, convincing them to buy our product and make him to invest with

us and providing him best service.

I have started my OJT from the very first day. And the day to day work that I am suppose to

do is my OJT and it is not fixed what I have to do and before start working I have to learn the

work which is assigned to me. Then I got work related to mutual funds. The details of the

following are explained here-:

So the objectives of my OJT are as follows-

Customer Service-:

o When a customer is asking some query I have to answer him but if I am not

sure I have to ask to my senior and solve his problem.

o By interacting customer we can study the main problems faced by them, as

they are not expert of the financial products so they need clear explanation.

Telemarketing -:

Our primary objective is to get an appointment.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 62/81

62

o Don‘t sale over phone, just make the call and the sale will follow.

o Determine the objection accurately before you start overcoming it.

o How to talk to a prospective customer who can become our customer.

Attracting customers in this field is easy, if the person is ready to invest. He doesn‘t have

knowledge about financial products so we have convinced him for the same.

About Mutual Funds-:

o History

o Types of mutual funds scheme

By structure

By investment objectives

By various options

o I got training for the software INVESTWELL. This is for maintaining the data

of mutual funds and this software provides the facility to make clients

portfolio in various types so that it become easy for us to give service to our

customers.

o Understanding & Executing the back office work.

o Learning about capital markets, Share trading, IPO‘s, Mutual Funds & other

concepts etc.

o Generation of leads.

o Handling customer‘s queries if any.

o Operating the mutual funds software to work on it.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 63/81

63

Strategy Employed to achieve the targets-:

o By practically handling the work.

o Asking to colleagues, guides & browsing net for understanding concepts of

Capital market, Share Trading, Mutual Funds & IPO‘s etc.

o By training program arranged by the company many thing got clear.

o By asking queries to the company guide and others.

o Assisting the concerned person doing IPO‘s and Mutual funds.

INTERNET TRADING & BACK OFFICE WORK

E-BROKING

Today is world of technology. So, the person who adopt it, get the success. So, E-Broking

means broking through electronic means. E-Broking is the broking in which the investors

who are familiar with the use of computer and Internet they directly trade in stock market.

They trade any time at any place when the stock market is open. The cost of transaction is

also reducing with time. The investors have a large range of option for the trading. It is a

paperless transaction so it reduces the cost of company. There was a facility of live streaming

quotes, which give exact price of share which prevailing in the market at that time.

Discount online brokers allow you to trade via Internet at reduced rates. Some provide quality

research, other don‘t. Full service online brokerage is linked to existing brokerage. These

brokers allow their client to place online orders with the option of talking/chatting to brokers

if advice is needed. Brokerage rates here are higher. Online trading is still in its infancy stage

in India.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 64/81

64

PROCEDURE FOR INTERNET TRADING

Step-1: Those investors interested in doing the trading over internet system, that is,

NEAT-ISX, should approach the brokers and register with the Stock Broker.

Step-2: After registration, the broker will provide to them a login name, password and a

personal identification number (PIN).

Step-3: Actual placement of an order. An order can then be placed by using the place

order window as under:

First by entering the symbol and series of stock and other parameters such as

quantity and price of the scrip on the place order window.

Second, fill in the symbol, series and the default quantity.

Step-4: Thus, the investor has to review the order placed by clicking the review option.

He may also re-set to clear the values.

Step-5: After the review has been satisfactory; the order has to be sent by clicking on the

send option.

Step-6: The investor will receive an ``Order Confirmation'' message along with the order

number and the value of the order.

Step-7: In case the order is rejected by the Broker or the Stock Exchange for certain

reasons such as invalid price limit, an appropriate message will appear at the bottom of

the screen. At present, a time lag of about ten seconds is there in executing the trade.

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 65/81

65

Step-8: It is regarding charging payment, for which there are different modes. Some

brokers will take some advance payment from the investors and will fix their trading

limits. When the trade is executed, the broker will ask the investor for transfer of funds by

the investor to his account.

FACTORS TO KEEP IN MIND WHILE SELECTING ONLINE BROKERS

Brokerage cost:

It is important to weigh up the subscription and trading costs charged by an online broker

against benefits offered by the site. All online brokers display their charges on their sites.

Some make sure you find the charges easily, while with others you will have to search a bit.

Safety:

Please make sure site has 128-bit encryption to ensure safety of transaction online.

ICICIDirect.com, 5paisa.com are few sites with 128-bit encryption. You normally get a

secured Login id and password. It is always advisable to frequently change trading password.

Ideally online trading site should be fully integrated. The greater the backward integration,

the better it is for the customer. Ideally broking account, demat account and bank account

should be linked electronically.

Rate refresh:

Rate refresh has to be real-time with no time lag. The speed and reliability comes with huge

investment in technology. It is always advisable to check rates of online broking sites with

BSE/ NSE terminal rates.

Speed of execution:

System has to be fast and reliable that does just one job- executes your trades. The last thing

you need is a site that is heavily congested with the users who are downloading heavy jpeg

graphs or pulling the latest story why market is moving. The

8/4/2019 Project Report of Finance of SONAL KUMAR

http://slidepdf.com/reader/full/project-report-of-finance-of-sonal-kumar 66/81

66

site should be one click wonder where squaring off all your positions or canceling all your

pending orders takes one click and a confirmation of action.

Trading limit:

For trading, all sites provide 4 times buy and sell limit against margin money put in by

customer. For delivery of shares, buying limit is equal to margin money put in by customer.

Couple of sites also provides margin funding for buying of shares.

Free trial period: