project report logistics industry economic linkage ... report logistics industry economic linkage...

TRANSCRIPT

Project Report

Logistics Industry Economic Linkage Analysis Prepared for

Rockford/RMAP Regional Freight Transportation Study Rockford, Illinois

Submitted by

Economics Research Associates, an AECOM company (ERA)

August 2009

ERA Project No. 18309

3 0 3 E as t Wa ck er Dr i ve Su i te 12 50

C h i c a g o , I L 6 0 60 1

3 1 2 .3 73 . 7 55 8 F AX 3 12 . 37 3 .1 1 09 w w w .er a .a ec o m.c o m

Table of Contents I. Summary of Findings........................................................................................ 4

Analysis of Rockford Area Transportation Sector Economic Linkages .................................. 4 Lessons Learned from Other Logistics Hubs......................................................................... 8

II. Rockford Economic Linkage Analysis .......................................................... 10 IMPLAN Social Accounting Matrices (SAM) ........................................................................ 10

SAM Example.....................................................................................................................12 Insights from the SAM........................................................................................................12 Industries............................................................................................................................13

Metrics of Interest ................................................................................................................ 14 SAM Results ........................................................................................................................ 16

Air & Rail Industry Notes ....................................................................................................31 III. Logistics Hub Case Studies ........................................................................... 33

Employment Growth Comparison ........................................................................................ 33 Data Source........................................................................................................................33 Summary of Employment ...................................................................................................33 Detailed Charts...................................................................................................................36

Review of Selected Logistics Hub Developments................................................................ 39 Rickenbacker Intermodal Terminal ....................................................................................39 UPS Worldport & Louisville-Area Logistics ........................................................................41 Alliance Airport ...................................................................................................................43

IV. The Auto Industry Summary.......................................................................... 47

ERA/AECOM Project No.18309 Page 1

Index of Tables/Figures

Table 1. Change in Industry Total Output, 2001-2007 (Values in $ millions) ................................ 5 Table 2. Total Output ($ millions) ................................................................................................ 16 Table 3. Change in Total Output ($ millions)............................................................................... 16 Table 4. Transportation as a Share of the Economy (Geographically centered)......................... 17 Table 5. Total Commodity Supply ($ millions)............................................................................. 17 Table 6. Total Commodity Demand ($ millions) .......................................................................... 18 Table 7. Commodity Supply-Demand Ratio ................................................................................ 18 Table 8. Regional Purchase Coefficient ...................................................................................... 19 Table 9. Regional Sales Coefficient ............................................................................................ 19 Table 10. Domestic Exports ($ millions)...................................................................................... 20 Table 11. Foreign Exports ($ millions)......................................................................................... 20 Table 12. Total Imports ($ millions) ............................................................................................. 20 Table 13. Change in Total Imports (values in $ millions)............................................................. 20 Table 14. Indirect Multipliers (Measured as indirect impact for each $1 direct impact) ............... 21 Table 15. Induced Multipliers (Measured as induced impact for each $1 direct impact) ............. 22 Table 16. Commodity Inputs, Warehousing ................................................................................ 23 Table 17. Commodity Inputs, Air Transportation (Inputs in $ millions) ........................................ 24 Table 18. Commodity Inputs, Truck Transportation (Inputs in $ millions).................................... 24 Table 19. Commodity Inputs, Courier Services (Inputs in $ millions) .......................................... 25 Table 20. Top Commodity Inputs, Rail Transportation (Inputs in $ millions) ............................... 25 Table 21. Top Commodity Imports, Warehousing ($ millions)..................................................... 26 Table 22. Top Commodity Imports, Air Transportation ($ millions) ............................................. 26 Table 23. Top Commodity Imports, Truck Transportation ........................................................... 27 Table 24. Top Commodity Imports, Courier Services.................................................................. 27 Table 25. Top Commodity Imports, Rail Transportation.............................................................. 28 Table 26. Industry Expenditures on Warehousing ($ millions) .................................................... 29 Table 27. Industry Expenditures on Air Transportation ($ millions)............................................. 29 Table 28. Industry Expenditure on Truck Transportation ($ millions) .......................................... 30 Table 29. Industry Expenditure on Courier Services ($ millions)................................................. 30 Table 30. Industry Expenditure on Rail Transportation ($ millions)............................................. 31 Table 31. Total Employment, All Sectors .................................................................................... 36 Table 32. Employment, NAICS 481-Air Transportation............................................................... 37 Table 33. Employment, NAICS 484-Truck Transportation .......................................................... 37 Table 34. Employment, NAICS 488-Support Activities for Transportation .................................. 37 Table 35. Employment, NAICS 492-Couriers and Messengers .................................................. 37 Table 36. Employment, NAICS 493-Warehousing and Storage.................................................. 37 Table 37. Employment, Sum of Logistics Sectors....................................................................... 38 Table 38. Employees in Logistics Industry, Per 1,000 Total Employees ..................................... 38 Table 39. Compound Annual Growth Rate by Sector, 2001 to 2007 .......................................... 38

ERA/AECOM Project No.18309 Page 2

General & Limiting Conditions

Every reasonable effort has been made to ensure that the data contained in this report are accurate

as of the date of this study; however, factors exist that are outside the control of Economics Research

Associates, an AECOM company (ERA) and that may affect the estimates and/or projections noted

herein. This study is based on estimates, assumptions and other information developed by

Economics Research Associates from its independent research effort, general knowledge of the

industry, and information provided by and consultations with the client and the client's

representatives. No responsibility is assumed for inaccuracies in reporting by the client, the client's

agent and representatives, or any other data source used in preparing or presenting this study.

This report is based on information that was current as of August, 2009 and Economics Research

Associates has not undertaken any update of its research effort since such date.

Because future events and circumstances, many of which are not known as of the date of this study,

may affect the estimates contained therein, no warranty or representation is made by Economics

Research Associates that any of the projected values or results contained in this study will actually be

achieved.

Possession of this study does not carry with it the right of publication thereof or to use the name of

"Economics Research Associates" in any manner without first obtaining the prior written consent of

Economics Research Associates. No abstracting, excerpting or summarization of this study may be

made without first obtaining the prior written consent of Economics Research Associates. This report

is not to be used in conjunction with any public or private offering of securities, debt, equity, or other

similar purpose where it may be relied upon to any degree by any person other than the client, nor is

any third party entitled to rely upon this report, without first obtaining the prior written consent of

Economics Research Associates. This study may not be used for purposes other than that for which

it is prepared or for which prior written consent has first been obtained from Economics Research

Associates.

This study is qualified in its entirety by, and should be considered in light of, these limitations,

conditions and considerations.

ERA/AECOM Project No.18309 Page 3

I. Summary of Findings

The AECOM Transportation team has completed this economic linkage analysis for the northern

Illinois freight transportation network to better understand industry relationships as part of the overall

regional freight transportation study. This document aims to clarify two main freight study goals:

1) To describe the current economic linkage between transportation industries and the

broader economy, as well as show how these ties have evolved over the recent past

2) To highlight potential areas for strategic investment in freight transportation

infrastructure within the region, with a focus on transportation support services and

business linkages which have either the potential to grow stronger, or have been

successful in areas with similar situations to Rockford.

As part of the overall analysis scope, the AECOM team evaluated agreed upon economic

development metrics to investigate the linkages between transportation industry segments and the

broader economy centered upon Rockford, Illinois. This effort included a detailed analysis of the

IMPLAN economic impact model system, a review of Rockford area transportation infrastructure and

shipper locations, and a case study analysis of three major domestic logistics hubs with comparable

characteristics to Rockford. A summary of core findings is presented in this section of the report with

supporting documentation described in subsequent sections.

The area of concentration for the study effort in this report is the Rockford global inland port area.

The Rockford inland port consists of infrastructure from three major freight modal alternatives: airport,

railroad, and highway systems. Geographically, the main focus of the regional freight transportation

study encompasses transportation infrastructure and facilities including the Rockford airport,

proposed rail consolidation to the east of the airport and track systems within 3 to 5 miles, and major

arterial highway connections to I-39, I-90, Highway 20, and Illinois Route 251. Furthermore, business

locations and access to these locations are important features within the context of the overall

system.

Analysis of Rockford Area Transportation Sector Economic Linkages

AECOM examined the economic linkages between select transportation sectors in the Rockford area

and the broader economy to understand the interdependence between industries. Using IMPLAN

economic impact model data from years 2001 and 2007, AECOM analyzed these linkages within the

local economy for the air transportation, rail transportation, truck transportation, warehousing and

ERA/AECOM Project No.18309 Page 4

storage, water transportation, and courier and messenger industries. The metrics investigated during

this portion of the analysis include the following:

Total output

Total commodity supply and demand

Regional purchase and sales coefficients

Domestic and foreign exports

Indirect and induced economic multipliers (economic growth measures related to industries

buying from other industries, as well as induced household spending derived from household

income generated from a development)

Commodity demand

Rockford Logistics Industry Growth, 2001-2007

The examination of the above listed metrics showed significant growth, measured in output dollar

value, in overall logistics industry sectors between 2001 and 2007. This finding was also supported

by a subsequent employment growth analysis. The following table shows growth in total output for

selected transportation sectors for Winnebago and Boone counties, as well as the State of Illinois

which is used here as a benchmark. Over the study period, total output grew significantly across

logistics sectors in Winnebago County including a 20% annual growth rate for air transportation

industry output, a 12% annual growth rate for rail transportation industry output, and a 15% annual

growth rate in warehousing and storage industry output. Boone County also saw increases in

logistics industry output, especially in the warehousing and storage industry, which grew at a 36%

annual rate over the period.

Table 1. Change in Industry Total Output, 2001-2007 (Values in $ millions)

Value Percent Value Percent Value Percent Value PercentAir Transportation 32.1 20% 0.5 32.5 20% 1,914 3%Rail Transportation 3.5 12% 0.6 2% 4.1 6% 2,565 13%Water Transportation 0.9 0.0 0.9 131 2%Truck Transportation 57.8 4% 14.2 6% 72.1 5% 3,259 5%Support activities, etc. 10.0 5% 32.0 42.1 16% 272 1%Couriers and Messengers -3.2 0.3 -2.8 -271Warehousing & Storage 34.5 15% 8.7 36% 43.2 16% 1,297 8%All Industries 4,343 4% 1,171 5% 5,514 4% 318,316 5%

Winnebago County

0% 0% -2%

Boone County State of IllinoisBoth Counties

Source: IMPLAN, AECOM

In addition to growth in output for logistics industries within the region, other core findings from the

analysis of economic linkages within the Rockford area include:

Transportation investments will aid in industry attraction by providing improved access for

industrial operations

ERA/AECOM Project No.18309 Page 5

Logistics sectors grew at a faster pace than the overall economy across all three study areas

including notable Winnebago County growth in air transportation, rail transportation, and

warehousing and storage sectors.

The ratio of total commodity supply to total commodity demand, a metric gauging how fully the

local market satisfies local demand, increased for air transportation and warehousing and storage

sectors in Winnebago County from 2001 and 2007. This is a sign that local suppliers have been

attracted to the area as a result of local transportation demand levels.

Supply-demand ratio levels in the Rockford area are generally lower than those at the state level

indicating less economic industry integration in Rockford compared with the state benchmark.

This is not surprising considering the state is considered well-integrated in these sectors.

However, it could be an indication that further economic integration may be possible which would

likely increase the efficiency of the goods movement system and decrease the costs to shippers

and consumers, and may foreshadow a growth in local employment.

Total import levels for logistics industries decreased over the study period, another indication of a

regional trend towards greater integration.

Logistics industries within the study area currently import a significant quantity of commodity

inputs from other regions including management and administrative resources, manufactured

products, and contract employment. Some of these identified import sectors may be strategic

areas of focus for company recruitment in the future.

Expenditures on transportation and logistics services in the Rockford area come from a variety of

local, regional, and external industries – one notable industry that purchases transportation

services is the motor vehicle parts manufacturing industry.

Power generation, motor vehicle parts manufacturing, and food production companies are both

significant purchasers of rail and other modal forms of transportation within the study area.

Specific to the air freight industry, pharmaceutical/biotech/healthcare businesses are major

purchasers as well.

Intermodal linkages between truck and rail transportation modes have increased over the study

period, where modal investments complement the connecting transportation assets.

Logistics Metrics for the Rockford MSA

The analysis of key logistics metrics contained in this report provides a view of recent area growth in

the logistics industry as a whole, as well as a set of measurable impacts to monitor moving forward

with the planning and economic development efforts underway. As such, the following key metrics

are highlighted for the region:

Logistics industries grew at a much faster rate than the broader economy at all three study area

levels (Boone and Winnebago counties, and the State of Illinois).

ERA/AECOM Project No.18309 Page 6

The state’s rail transportation industry experienced strong growth, doubling over the time period

studied (2001-2007). Winnebago County’s rail transportation industry fared almost as well,

increasing from $3.7 million in total output to over $7 million. This measurement only includes the

output generated based on area industry employment activity and is probably under-represented

as an economic benefit because of the nature of the rail industry (employment concentrated in

major origin and destination areas such as Chicago).

Warehousing and Storage was a growth sector for each study area. Boone County’s industry

blossomed from $1.6 million in 2001 to over $10 million in 2007. The industry more than doubled

in Winnebago County as well.

Boone County’s primary contribution to the logistics industry is in trucking, and more recently,

support activities for transportation.

Almost every logistics sector gained relative importance in both Winnebago and Boone counties.

Rockford Rail and Air Industry

The importance of the freight transportation industry to Rockford businesses is significant, and rail

and air freight industries within the region contribute to the economic competitiveness of local

businesses. Some highlights of the linkage analysis specific to rail and air freight include:

In both 2001 and 2007, power generation is the number one customer of rail transportation firms

– by a wide margin. In 2001, the power generation industry accounted for one-quarter of

business spending on rail transportation, or three times higher than any other single industry.

The second largest customer in 2001 was the motor vehicle parts manufacturing industry. Power

generation companies in the area purchase goods such as oil, natural gas, coal, petroleum, and

wind turbines. These firms spend most of their dollars on rail and pipeline transportation.

From 2001 to 2007, motor vehicle parts manufacturers went from representing 8 percent of rail

firms’ business revenues to 3 percent. These businesses decreased from the second-largest

source of rail revenue to the seventh-largest, and the total output contributed fell from $2.2 million

to $1.5 million.

Truck transportation firms are significant customers of rail transportation firms in the area,

representing a portion of the region’s intermodal linkages. In 2007, truck transportation firms

represented 6.6 percent of rail firms’ business inputs, up from 4 percent in 2001.

The food production industry is a key customer of rail transportation firms. The top twelve overall

industry purchasers of rail transportation in the area includes: candy manufacturers; cookie,

cracker, and pasta manufacturers; snack food manufacturers; and dog and cat food

manufacturers. Paint and coating manufacturers are also a key customer of the rail

transportation industry.

ERA/AECOM Project No.18309 Page 7

The air transportation industry has also seen revenues from the motor vehicle parts

manufacturing industry decline since 2001. In 2001, motor vehicle parts manufacturers were the

biggest industry customer of the air transportation industry, representing 7 percent of its business

revenues. By 2007, this spending level fell 60 percent to represent only 2 percent of the air

transportation industry’s revenues. Supplier parks may be one contributing factor.

Hospitals, health care providers, the US Postal Service, directory and mailing list vendors,

wholesalers, and restaurants were among the largest industry customers of area air

transportation businesses in both years.

Petroleum refineries are among the largest recipients of the air transportation industry’s

expenditures – obviously, spending on fuel is a key input to the process of air transportation. In

2001, such expenditures represented 17 percent of the industry outlays to other firms; by 2007, it

became 38 percent. (Note that this is a percentage of spending on goods and services, and

excludes labor.) Very little of that spending stays in Winnebago County. It is no surprise to see,

then, that the indirect multiplier has fallen for the air transportation industry, as so much more

business spending has been going toward fuel from outside of the county.

Lessons Learned from Other Logistics Hubs

AECOM reviewed employment metrics and conducted interviews of stakeholders at three major US

logistics hubs to understand the economic development implications related to public and private

investments in freight transportation infrastructure the three hubs include. Factors which were

considered when choosing case study development areas include the ability to maximize freight

industry infrastructure asset value and to maximize access to industry facilities in an effort to promote

efficient and economic shipper freight movements. Key points developed during the analysis include:

Logistics industry infrastructure is most effective when it is linked with a coordinated, broadly

engaged planning effort involving partnerships between public and privates stakeholders and the

community.

Funding for transportation infrastructure development is generated from private sources as well

as federal, state, and local public stakeholders – often times the privately funded portion includes

support from railroads and air logistics companies. Commonly, incentive packages from public

sources include tax credits, complementary road and rail access and infrastructure

improvements, and job training/educational options for company employees.

The freight logistics industry is competitive, and each of the profiled case study developments is

seen to be proactive and innovative when considering strategic investments.

ERA/AECOM Project No.18309 Page 8

The logistics industry, area businesses/shippers, and the community as a whole each benefit

from a more geographically integrated infrastructure, focused on providing efficient multi-modal

transportation alternatives.

The mitigation of traffic/congestion impacts, as they may arise on local and regional

transportation networks, is an important planning factor, economic, and community benefit.

Warehousing and storage firms and employment experienced consistent high growth rates

across all of the case study areas, resulting from efforts to expand freight transportation

infrastructure and support capacity.

Winnebago County exhibited the lowest number of transportation employees per thousand total

employees compared with the case study counties. This could be an indication that increased

freight transportation industry integration is achievable in the near-term and could have significant

positive efficiency and economic results.

Opportunities for the Rockford MSA

The Rockford MSA demonstrates industry sectors with strong inter-industry relationships, where

supply chains are closely connected and investments for transportation infrastructure will

resonate throughout the supply chain

Industry sectors favorably situated within the Rockford MSA, or could be attracted, include

aerospace production and research & development, warehouse / distribution centers, industrial

machinery manufacturing, metals manufacturing, chemicals and plastics manufacturing, food

processing, transportation equipment manufacturing, as well as green technology and alternative

energy development and production

The Rockford MSA demonstrates attributes that are found in the evolving definition of an inland

port, an area of significant transportation assets linked across modes and logistics functions

The value of existing transportation and industrial assets is maximized by transportation

investments that increase access to area industries

ERA/AECOM Project No.18309 Page 9

II. Rockford Economic Linkage Analysis

This section examines the economic linkages between select transportation sectors and the local

economies in Boone and Winnebago Counties. Specifically, this analysis will show the extent to

which transportation sectors—air, water, truck, freight rail, and related support industries—are

integrated with other firms in the local marketplace. We compare economic data from 2001 and 2007.

We examine several economic metrics that approach this question in different ways. By comparing

several metrics over this time period, we will be able to show the ways in which the industries have

shaped and potentially deepened their connections with other local industries.

IMPLAN Social Accounting Matrices (SAM)

The primary tool for this analysis is the IMPLAN economic impact model. Widely used to gauge the

economic impact of new local demand, such as a new factory or government spending, the IMPLAN

model contains extensive data regarding how well firms are linked to others in a local economy. Its

system of social accounts show how dollars flow among various institutions: firms, households,

government agencies, and exports and imports.

IMPLAN Social Accounting Matrices (SAM) estimate the trade flows among businesses and other

institutions in an economy. These matrices take into account businesses (arranged by industry),

households, government agencies, new investment capital, and foreign and domestic trade.

A social accounting matrix can be constructed for any study area. Many of the data sources that are

used to construct the matrices are reported by various U.S. government agencies on the county level.

Therefore, the smallest advisable study area is the county. In this report, ERA uses study areas for

Boone County, Winnebago County, and the entire state of Illinois.

The SAM estimates dollars flowing among institutions in the economy. The following are examples of

institutions, as we use the term in this report:

Firms. Business firms are an institution; in turn, they are divided into over 400 different industries,

representing types of firms. These are based on the NAICS code; the industries used in the

IMPLAN SAM generally correspond to three-digit NAICS codes. (For example, the “truck

transportation” sector corresponds with NAICS 484.) This institution covers local firms only.

Households. Consistent with the conventions in economics, the “household” is considered the

functional economic unit of individuals. Households act as suppliers of labor (individuals work)

and as consumers, as individuals buy things from firms. The institution covers local households.

Households of different income levels spend their money in different ways, so the SAM groups

ERA/AECOM Project No.18309 Page 10

them into nine income categories. They are arranged by total household income category. The

nine household income categories range from Less Than $10,000 to Over $150,000.

Government. In the IMPLAN model, government institutions are broken down into several

different categories. Examples include Federal Government (excluding defense), Federal

Government Defense, State & Local Government (excluding public schools), Public Schools, and

the like.

Domestic Trade. Any dollar flows that go into or out of the local study area (the county or the

state) are considered domestic trade. A household buying consumer goods from the adjacent

county or the business employing workers from another state would all be included in “domestic

trade.”

Foreign Trade. Similar to domestic trade, any dollar flows going out of the U.S. or coming into the

U.S. from abroad are counted as foreign trade.

Other. Other institutions, less important to our analysis, include capital, additions to inventory, and

commodities.

The SAM also estimates how these institutions interact with each other. The following are some

examples of how funds flow among these institutions:

Firms to firms: Business firms buy materials to produce their product. Restaurants buy food and

supplies. Hotels buy linens and cleaning supplies. Manufacturers buy raw materials. A portion,

though never all, of a firm’s revenue goes toward buying things from other firms.

Firms to households: This is primarily employee compensation. The social accounts consider a

household to be a functioning economic unit providing labor to firms in exchange for dollars.

Households to firms: Households take some of the money they earn from labor and spend it on

goods and services provided by firms—groceries, supplies, entertainment, and services.

Firms to domestic trade: When firms make a product that is purchased by households or other

firms outside the local study area, this is considered domestic trade and leaves the local

economy.

And so forth. When put completely together, the SAM will account for all the ways in which these

institutions shuffle money from one to another—as well as dollars new to the study area and dollars

leaving the study area.

The next section shows a simple example of a SAM.

ERA/AECOM Project No.18309 Page 11

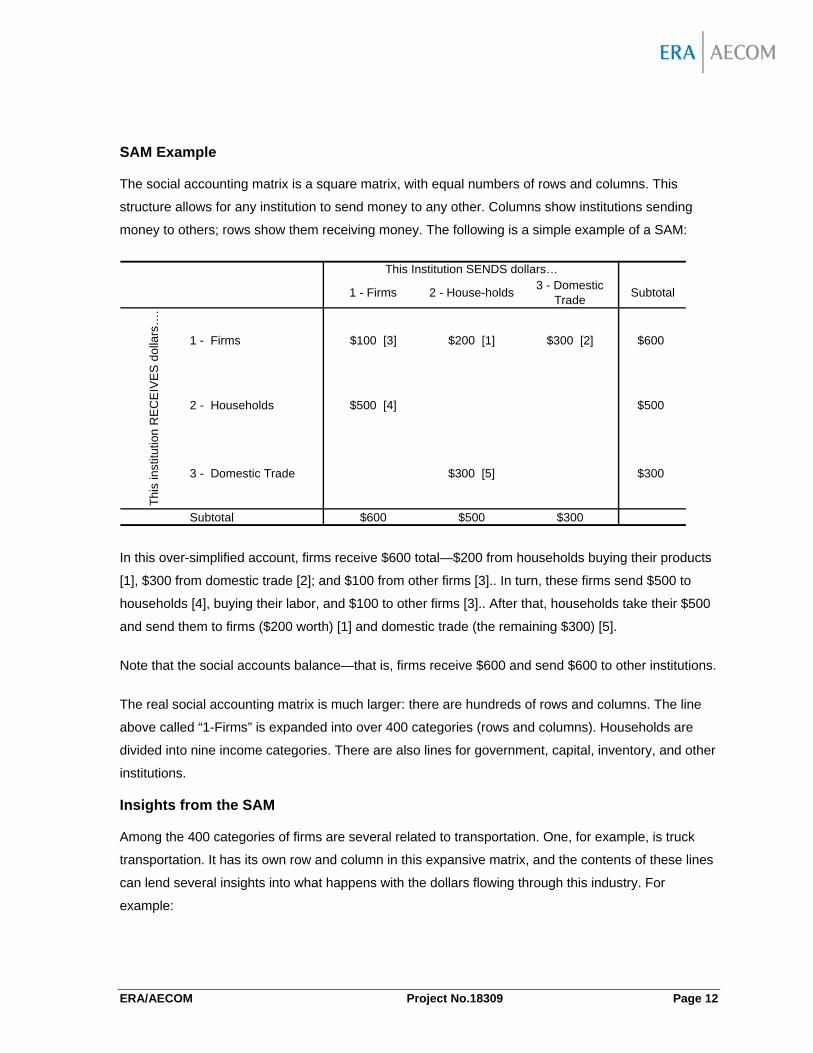

SAM Example

The social accounting matrix is a square matrix, with equal numbers of rows and columns. This

structure allows for any institution to send money to any other. Columns show institutions sending

money to others; rows show them receiving money. The following is a simple example of a SAM:

1 - Firms 2 - House-holds3 - Domestic

TradeSubtotal

1 - Firms $100 [3] $200 [1] $300 [2] $600

2 - Households $500 [4] $500

3 - Domestic Trade $300 [5] $300

Subtotal $600 $500 $300

Th

is in

stitu

tion

RE

CE

IVE

S d

olla

rs…

.

This Institution SENDS dollars…

In this over-simplified account, firms receive $600 total—$200 from households buying their products

[1], $300 from domestic trade [2]; and $100 from other firms [3].. In turn, these firms send $500 to

households [4], buying their labor, and $100 to other firms [3].. After that, households take their $500

and send them to firms ($200 worth) [1] and domestic trade (the remaining $300) [5].

Note that the social accounts balance—that is, firms receive $600 and send $600 to other institutions.

The real social accounting matrix is much larger: there are hundreds of rows and columns. The line

above called “1-Firms” is expanded into over 400 categories (rows and columns). Households are

divided into nine income categories. There are also lines for government, capital, inventory, and other

institutions.

Insights from the SAM

Among the 400 categories of firms are several related to transportation. One, for example, is truck

transportation. It has its own row and column in this expansive matrix, and the contents of these lines

can lend several insights into what happens with the dollars flowing through this industry. For

example:

ERA/AECOM Project No.18309 Page 12

It is possible to determine how much the industry spends on goods and services in order to

produce its product. Some of these will be from local firms, others from outside the study area,

and still others from foreign sources. Among local purchases, it is possible to see in what

proportions the industry buys goods and services from each of the over 400 categories of firms.

The supply and demand balance in a local study area can also be studied. For example, the

trucking industry based in the study area will do a certain amount of business—some of it

satisfied by local clients, others by clients outside the study area. Conversely, local firms and

households will spend money on trucking industry. It is possible to tell how much of the trucking

product is bought locally and how much of the trucking demand is sourced locally.

It is also possible to determine how much the industry pays to households in employee

compensation.

These examples show how the social accounting matrix can be used to gain specific insights into the

practices of firms, households, and other institutions in the local study area. The specific metrics that

we examine are set out in detail in the next section.

Throughout the analysis, it is important to keep in mind that all the data are estimates and aggregates

of observed conditions and activity. SAMs do not attempt to explain or even estimate the behavior of

individual firms or households; only the household category or entire industries of firms. Moreover,

many government data are self-reporting, and thus, may not be captured in the same manner as

private industries.

Industries

ERA has identified several industries of interest to track in this analysis. Because our primary data

source is IMPLAN’s social accounting matrix, we are restricted to using industries tracked in this

particular model. They roughly align with three-digit NAICS codes. It is also important to note that

data are collected by firm, and each firm belongs to one industry. Therefore, although a firm may

provide many different services, it is classified in only one industry category. The following are

industries we examined in their evaluation.

Air Transportation (NAICS 481). This industry is comprised of air transportation for passengers and

cargo on both scheduled and non-scheduled routes. Scheduled air transportation covers the largest

part of the industry, including air cargo operations. Non-scheduled service can include both cargo and

passengers and comprises general aviation for special, corporate, personal or other unscheduled

aviation. This industry does NOT include courier services; see below.

ERA/AECOM Project No.18309 Page 13

Rail Transportation (NAICS 482). This industry includes both short line and line haul railroads. Line

haul railroads operate networks over wide geographic areas with multiple facilities throughout the

U.S. Short line railroads are often confined to a small geographic area. This industry also includes

passenger rail service.

Truck Transportation. (NAICS 484). The truck transportation industry includes firms that provide

over the road freight transportation, usually in a trailer or standard shipping container. This includes

local pickup and delivery, sorting, line haul, and terminal operations. It also includes specialized

freight trucking, which would be freight that has specialized requirements—whether from a large size

to refrigeration requirements, tankers, or other type of special equipment.

Warehousing & Storage (NAICS 493). Firms in this industry primarily provide warehousing and

storage to other firms: they do not sell goods to consumers or other businesses. Specialized

warehousing is also included (such as refrigeration). These firms can sometimes provide a range of

warehouse-related services, such as sorting, packing, order fulfillment, and other logistical services.

Water Transportation (NAICS 483). This industry includes firms that provide deep sea, great lakes,

intracoastal, and inland water transportation, including freight.

Couriers and Messengers (NAICS 492). These firms provide delivery of parcels, whether in one city

or among different cities. A courier service primarily handles small parcels that can be picked up and

delivered by hand—large shipments of commodities, for example, would be handled by a truck or

freight rail industry, or by some specialized shipper. Firms in this industry can range from a

messenger on bicycle in one city to a large international shipping network like UPS or FedEx. It does

not include the postal service.

Metrics of Interest

The metrics that we examine in our analysis are all derived from the social accounting matrix. The

simple example should help frame some of the metrics that are below. Many of the metrics we

examine arise from ratios and other simple manipulations of the social accounting matrix.

Total Output

These metrics describe the size of the industry. Total output is the value of all goods and services

provided by the industry—it is akin to GDP or total revenue for the firm.

ERA/AECOM Project No.18309 Page 14

Total Commodity Supply, Demand, and Supply-Demand Ratio

These metrics describe how much of a given commodity is made in the local area (very closely

related to total output) and compares it to how much is demanded in the local area. These can then

be used to create a ratio of supply to demand. This shows whether a region has more or less of a

given commodity than its firms and households are demanding. A low ratio shows that there is more

demand than local businesses can supply. A high ratio shows there is more supply than the local

area demands.

Regional Purchase Coefficient & Regional Sales Coefficient

The previous metrics do not say anything about whether local buyers and local sellers actually meet

in the marketplace: it only shows how much is supplied and how much is demanded. The regional

purchase coefficient estimates how much of local purchases are indeed sourced by local sellers.

Conversely, the regional sales coefficient estimates how much of a local seller’s revenues come from

local buyers. (Even if the market is in balance, local buyers may choose to buy from out of the region;

local sellers may find customers elsewhere, as well.)

Domestic Exports and Foreign Exports

These two metrics quantify the value of goods and services that are exported to other regions or

outside the U.S. by local sellers.

Multipliers

The indirect multipliers show how additional dollars in a given industry reverberate throughout the rest

of the economy. A high indirect multiplier indicates that the industry has a high level of local suppliers;

a low multiplier suggests the opposite. Induced impacts show how additional dollars in an industry

reverberate via the spending by employees of the firms.

Commodity Demand

Each of the preceding metrics has a single value per industry. For example, truck transportation has a

single dollar amount for value added, a single regional purchase coefficient, and so on. The

commodity demand is a list of things that a given industry buys; it expands the “intermediate gross

outlay.” The intermediate gross outlay shows how much of a firm’s dollars go to other businesses; the

commodity demand expands that to specify exactly where those dollars go. Due to the size of the

SAM, it is possible to show hundreds of different inputs that firms buy. In our analysis, we present the

top commodities that firms buy. Therefore, for each industry we study, we will provide a list of the top

commodities the firm buys in the local study area. This will show the types of local firms that are most

affected by the presence of the industries we are considering.

ERA/AECOM Project No.18309 Page 15

SAM Results

Total Output

Total output is the total value of goods and services produced in a given industry. It is akin to GDP.

Essentially, the tables below show GDP by industry by group:

Table 2. Total Output ($ millions)

2001 2007 2001 2007 2001 2007Air Transportation 16.2 48.2 0.0 0.5 9,038 10,953Rail Transportation 3.7 7.3 5.5 6.1 2,408 4,973Water Transportation 0.0 0.9 0.0 0.0 1,179 1,310Truck Transportation 202.8 260.7 31.6 45.9 10,678 13,938Support activities, etc. 28.8 38.8 0.0 32.0 3,360 3,632Couriers and Messengers 112.2 109.1 0.0 0.3 2,061 1,790Warehousing & Storage 27.4 61.9 1.6 10.3 2,295 3,592All Industries 16,558 20,901 3,330 4,501 841,659 1,159,975

Winnebago County Boone County State of Illinois

Table 3. Change in Total Output ($ millions)

Value Percent Value Percent Value Percent Value PercentAir Transportation 32.1 20% 0.5 32.5 20% 1,914 3%Rail Transportation 3.5 12% 0.6 2% 4.1 6% 2,565 13%Water Transportation 0.9 0.0 0.9 131 2%Truck Transportation 57.8 4% 14.2 6% 72.1 5% 3,259 5%Support activities, etc. 10.0 5% 32.0 42.1 16% 272 1%Couriers and Messengers -3.2 0.3 -2.8 -271Warehousing & Storage 34.5 15% 8.7 36% 43.2 16% 1,297 8%All Industries 4,343 4% 1,171 5% 5,514 4% 318,316 5%

Winnebago County

0% 0% -2%

Boone County State of IllinoisBoth Counties

Logistics industries grew at a much faster rate than the economy at large in all three study areas.

Air Transportation in Winnebago tripled its total output from 2001 to 2007, compared to statewide

industry growth of 21 percent.

The state’s rail transportation industry experienced strong growth, doubling over the time period

studied. Winnebago County’s rail transportation industry fared almost as well, increasing from

$3.7 million in total output to over $7 million.

Warehousing & Storage also was a growth industry for each study area. Boone County’s industry

blossomed from $1.6 million of business in 2001 to over $10 million in 2007. The industry in

Winnebago County also more than doubled.

Boone County’s primary contribution to the logistics industry is in truck transportation, and, more

recently, support activities for transportation.

ERA/AECOM Project No.18309 Page 16

Total Output as a Percentage of the Economy

The table below shows that transportation industries are between 2.0 and 2.5 percent of their

respective economies in Winnebago, Boone, and the state:

Table 4. Transportation as a Share of the Economy (Geographically centered)

2001 2007 2001 2007 2001 2007 2001 2007Air Transportation 0.10% 0.23% 0.00% 0.01% 0.08% 0.19% 1.07%Rail Transportation 0.02% 0.03% 0.17% 0.05% 0.05% 0.29% 0.43%Water Transportation 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.14%Truck Transportation 1.22% 1.25% 0.95% 1.02% 1.18% 1.21% 1.27%Support activities, etc. 0.17% 0.19% 0.00% 0.71% 0.14% 0.28% 0.40%Couriers and Messengers 0.68% 0.00% 0.01% 0.56% 0.24%Warehousing & Storage 0.17% 0.30% 0.05% 0.23% 0.15% 0.28% 0.27% 0.31%Transportation Industries 2.36% 2.52% 1.16% 2.11% 2.16% 2.45% 2.36% 2.52%

State of Illinois

0.94%0.13%

0.11%1.20%0.31%

0.52% 0.43% 0.15%

Winnebago County Boone County Both Counties

Almost every sector gained relative importance in the economy in Winnebago and Boone County.

The transportation industries as a group gained as a percentage of the state economy, but gains

in warehousing and rail transportation were offset by losses in the five other sectors.

Total Commodity Supply & Total Commodity Demand

Total Commodity Supply refers to the production of a given commodity (good or service) in the study

area. It is very similar to total output, and indeed we see that it is similar to total output. Total

Commodity Demand shows how much of a given good or service is purchased by other firms or

households in the given study area. Neither of these metrics makes any comment on whether the

buyers and sellers meet in the marketplace—it only measures what firms and households are buying

and what they are producing.

Table 5. Total Commodity Supply ($ millions)

2001 2007 2001 2007 2001 2007Air Transportation 19.0 50.5 0.0 2.3 9,369 11,164Rail Transportation 4.4 8.3 5.5 6.9 2,482 5,076Water Transportation 0.2 1.5 0.0 0.5 1,200 1,364Truck Transportation 204.2 265.8 31.6 50.1 10,834 14,421Support activities, etc. 27.5 34.9 0.6 25.5 3,106 3,035Couriers and Messengers 112.2 109.1 0.0 0.3 2,069 1,790Warehousing & Storage 27.5 61.9 1.6 10.3 2,301 3,592All Industries 16,928 21,418 3,368 4,577 856,494 1,186,320

Winnebago County Boone County State of Illinois

ERA/AECOM Project No.18309 Page 17

Table 6. Total Commodity Demand ($ millions)

2001 2007 2001 2007 2001 2007Air Transportation 106.9 115.3 18.7 19.6 5,789 6,872Rail Transportation 34.4 55.3 6.5 16.1 1,698 3,451Water Transportation 23.1 17.9 2.6 3.4 1,168 1,375Truck Transportation 194.3 234.5 46.1 59.6 9,068 11,913Support activities, etc. 26.0 33.1 2.9 4.2 2,532 2,615Couriers and Messengers 55.3 51.7 6.0 6.8 3,051 3,022Warehousing & Storage 43.8 57.8 7.5 7.8 1,708 2,581All Industries 16,680 21,323 5,067 6,677 839,607 1,171,099

Winnebago County Boone County State of Illinois

Table 7. Commodity Supply-Demand Ratio

2001 2007 2001 2007 2001 2007Air Transportation 0.2 0.4 0.0 0.1 1.0 1.0Rail Transportation 0.1 0.1 0.7 0.4 1.0 1.0Water Transportation 0.0 0.1 0.0 0.1 0.8 0.7Truck Transportation 1.0 1.0 0.6 0.8 1.0 1.0Support activities, etc. 0.9 0.9 0.2 1.0 1.0 1.0Couriers and Messengers 1.0 1.0 0.0 0.0 0.7 0.5Warehousing & Storage 0.6 1.0 0.2 1.0 1.0 1.0

Winnebago County Boone County State of Illinois

The supply-demand ratio is an indicator of how well balanced, locally, a given industry is. The closer

to 1.0, the closer the market is to well-satisfied. (Values where supply exceeds demand are shown as

1.0.) The table above shows that, particularly in the case of air transportation, logistics industries

moved toward satiating local demand more fully. Shortened and more efficient supply chains can

lead to local employment growth, e.g., the Chrysler Supplier Park.

In this ratio, supply is the numerator and demand is the denominator. Therefore, if much more

product is demanded than is supplied, the ratio will be low. A low ratio in this table means that local

firms must look elsewhere to buy their products.

ERA notes that air transportation and warehousing & storage made gains in this ratio Winnebago

County. This means that local suppliers are likely to have been attracted to the county as a result of

the local demand. As one would expect, the larger the study area, the closer the markets are to being

balanced. The state has many more values closer to 1.0.

Regional Purchase Coefficient & Regional Sales Coefficient (RPC & RSC)

The metrics above compared the total amount of supply and the total amount of demand, but RPC

and RSC measure whether the buyers and sellers actually met in the marketplace.

ERA/AECOM Project No.18309 Page 18

The regional purchase coefficient and regional sales coefficient describe the extent to which local

buyers and sellers (respectively) buy and sell products with other local firms. High values for the RPC

and RSC indicate that industries are well-integrated with each other. The RPC and RSC are scaled

from 0 to 1.

Table 8. Regional Purchase Coefficient

2001 2007 2001 2007 2001 2007Air Transportation 0.15 0.38 0.00 0.12 0.46 0.46Rail Transportation 0.11 0.14 0.73 0.40 1.00 1.00Water Transportation 0.01 0.07 0.00 0.14 0.82 0.67Truck Transportation 0.97 1.00 0.63 0.80 1.00 1.00Support activities, etc. 0.70 0.70 0.20 0.70 0.70 0.70Couriers and Messengers 0.70 0.70 0.00 0.04 0.68 0.52Warehousing & Storage 0.62 1.00 0.22 1.00 1.00 1.00

Winnebago County Boone County State of Illinois

In the table above, air transportation had a RPC of 0.15 in 2001 and 0.38 in 2007. This means that

local buyers who required these services spent 15 percent of their dollars locally in 2001 and 38

percent of their dollars locally in 2007. Again, one expects the RPC to be higher with larger study

areas, and they often are.

Table 9. Regional Sales Coefficient

2001 2007 2001 2007 2001 2007Air Transportation 0.85 0.87 0.00 0.97 0.29 0.28Rail Transportation 0.88 0.94 0.86 0.94 0.68 0.68Water Transportation 1.00 0.79 1.00 1.00 0.80 0.67Truck Transportation 0.93 0.88 0.93 0.95 0.84 0.83Support activities, etc. 0.66 0.66 1.00 0.12 0.57 0.60Couriers and Messengers 0.34 0.33 1.00 0.88 1.00 0.88Warehousing & Storage 0.99 0.93 0.99 0.76 0.74 0.72

Winnebago County Boone County State of Illinois

Why are regional sales coefficients higher than regional purchase coefficients? The RSC corresponds

with sellers (or, supply). The RPC corresponds with buyers (or, demand). Recall from previous tables

that supply is much lower than demand: that is, firms and households want more of these

commodities than what is produced there. It is only logical to expect that sellers, who face a very

large pool of buyers, can satisfy many of their sales locally. By contrast, buyers, who all compete for

relatively small pool of suppliers, must look elsewhere. And in fact it is true: the RSC is higher than

the RPC in most industries. The exceptions are the industries that have a supply-demand ratio near

or equal to 1.0, namely couriers and support activities.

ERA/AECOM Project No.18309 Page 19

Table 10. Domestic Exports ($ millions)

2001 2007 2001 2007 2001 2007Air Transportation 0.0 0.0 0.0 0.0 5,116 6,543Rail Transportation 0.0 0.0 0.0 0.0 457 1,280Water Transportation 0.0 0.0 0.0 0.0 0 0Truck Transportation 0.0 16.3 0.0 0.0 966 1,702Support activities, etc. 6.0 6.9 0.0 18.6 945 756Couriers and Messengers 73.5 59.9 0.0 0.0 0 0Warehousing & Storage 0.0 3.4 0.0 2.4 562 970All Industries 6,090 7,507 1,367 1,597 221,907 312,197

Winnebago County Boone County State of Illinois

Table 11. Foreign Exports ($ millions)

2001 2007 2001 2007 2001 2007Air Transportation 2.8 6.4 0.0 0.1 1,578 1,446Rail Transportation 0.5 0.5 0.7 0.4 327 344Water Transportation 0.0 0.3 0.0 0.0 238 445Truck Transportation 15.2 15.1 2.4 2.7 799 806Support activities, etc. 3.3 4.8 0.0 4.0 389 449Couriers and Messengers 0.0 12.9 0.0 0.0 0 212Warehousing & Storage 0.4 0.7 0.0 0.1 31 42All Industries 1,346 1,657 243 572 47,846 73,692

Winnebago County Boone County State of Illinois

Table 12. Total Imports ($ millions)

2001 2007 2001 2007 2001 2007Air Transportation 90.7 71.2 18.7 17.4 3,114 3,697Rail Transportation 30.5 47.5 1.7 9.6 0 0Water Transportation 22.9 16.7 2.6 2.9 206 456Truck Transportation 5.2 0.0 16.8 12.1 0 0Support activities, etc. 7.8 9.9 2.3 1.3 760 785Couriers and Messengers 16.6 15.5 5.9 6.5 982 1,444Warehousing & Storage 16.7 0.0 5.8 0.0 0 0All Industries 7,189 9,069 3,308 4,269 252,866 370,668

Winnebago County Boone County State of Illinois

Table 13. Change in Total Imports (values in $ millions)

Value Percent Value Percent Value Percent Value PercentAir Transportation -19.5 -1.3 -20.8 583 3%Rail Transportation 16.9 8% 7.9 33% 24.8 10% 0Water Transportation -6.1 0.4 2% -5.8 250 14%Truck Transportation -5.2 -4.8 -10.0 0Support activities, etc. 2.1 4% -1.0 1.1 2% 25 1%Couriers and Messengers -1.1 0.5 1% -0.6 462 7%Warehousing & Storage -16.7 -5.8 -22.5 0All Industries 1,880 4% 960 4% 2,840 4% 117,802 7%

Winnebago County

-4% -1% -3%

-5% -4%-100% -5% -10%

-9%-1% 0%

-100% -100% -100%

Boone County State of IllinoisBoth Counties

ERA/AECOM Project No.18309 Page 20

Total imports in logistics, over this period, went down in general, consistent with our existing findings

that supply and demand are, in general, becoming more balanced in these industries.

Multipliers

Many of the above metrics are indicators of how the industries interact with each other and with other

counties in the U.S. The economic impact multiplier is the most succinct summary of this indication. In

general, a higher multiplier means that new business to firms in a given industry has a higher effect

on the local economy than it would have previously. However, it should be noted that a smaller

multiplier over time may simply represent a variety of factors, observable and not observable, and can

be caused by things entirely out of control of the policymakers or even the business leaders in the

area. (Think of an industry that is somewhat in balance. Then, suppose the industry expands its

production in the market area, but must source many of its inputs from outside the study area. The

multiplier would probably decrease—but it’s still better than not having the industry expand at all.)

Below we present indirect and induced multipliers. The indirect multiplier indicates the extent to which

firms buy from other firms in the local study area. These rise in three of seven industries in

Winnebago County and in six of seven in Boone County. The induced multipliers indicate the extent

to which the economy benefits by the employees of these firms having higher incomes—which they

re-spend in the economy on goods and services. The induced multipliers rise in six of seven

industries in Winnebago County and five of seven industries in Boone County.

Table 14. Indirect Multipliers (Measured as indirect impact for each $1 direct impact)

2001 2007 2001 2007 2001 2007Air Transportation 0.39 0.27 0.00 0.20 0.54 0.59Rail Transportation 0.18 0.27 0.10 0.16 0.46 0.51Water Transportation 0.00 0.43 0.00 0.00 0.68 0.52Truck Transportation 0.37 0.33 0.16 0.18 0.58 0.53Support activities, etc. 0.28 0.24 0.00 0.14 0.41 0.27Couriers and Messengers 0.37 0.12 0.00 0.07 0.48 0.24Warehousing & Storage 0.16 0.29 0.10 0.17 0.24 0.31

Winnebago County Boone County State of Illinois

ERA/AECOM Project No.18309 Page 21

Table 15. Induced Multipliers (Measured as induced impact for each $1 direct impact)

2001 2007 2001 2007 2001 2007Air Transportation 0.28 0.30 0.00 0.06 0.47 0.41Rail Transportation 0.33 0.26 0.11 0.11 0.45 0.39Water Transportation 0.00 0.23 0.00 0.00 0.33 0.31Truck Transportation 0.30 0.36 0.10 0.15 0.44 0.51Support activities, etc. 0.37 0.46 0.00 0.21 0.55 0.64Couriers and Messengers 0.27 0.42 0.00 0.26 0.46 0.62Warehousing & Storage 0.41 0.42 0.16 0.19 0.57 0.62

Winnebago County Boone County State of Illinois

Commodity Inputs & Imports

For four industries, we detail the commodity inputs and commodity imports. The tables below refer to

Winnebago County in the year 2007.

Commodity inputs are the goods and services the industry buys in order to produce its product.

(These are all part of the social accounting matrix.) The industries we have considered have about

one hundred to 150 commodity inputs. In the tables below, we choose the top twelve industries for

each category. The metrics included in his table are the following:

Gross absorption coefficient. This is the percentage of each $1 in industry outlay that is

dedicated to a given input. Recall that not all of an industry’s dollar goes toward other firms: some

portion goes toward employee compensation, dividends, taxes, etc. Therefore, the gross

absorption coefficients usually add up to .25 or .75.

Gross inputs. Based on the size of the industry, this is the amount, in millions of dollars, that the

entire industry spends on a given commodity. Whereas the gross absorption coefficient measures

how much of each dollar goes to a certain commodity, the gross input says how many dollars that

is. For example, if an industry spends $1 million in total outlay, and the gross absorption

coefficient for a given commodity is .02, then the gross input is $20,000. In other words, the

industry spends 2 percent of its dollars on this commodity, and it adds up to $20,000 in total

spending.

Regional absorption coefficient. Similar to the gross absorption coefficient, this describes the

percentage of one dollar spent on a given commodity in the local study area. It will be some

portion of the gross absorption coefficient. In the example above, if an industry’s gross absorption

coefficient is .02 and it spends half of that in the local study area, then its regional absorption

coefficient is .01.

ERA/AECOM Project No.18309 Page 22

Regional inputs. Regional inputs describe the dollar amount of spending on a given commodity

in the local study area. It is derived by multiplying the regional absorption coefficient by the

industry’s total output. Again, in the example above, the regional input would be $10,000; that is,

the industry in question spends $20,000 on a given commodity, $10,000 of which is spent in the

local study area.

Table 16. Commodity Inputs, Warehousing

NAICS CommodityGross

Absorption Coefficient

Gross Inputs ($ millions)

Regional Absorption Coefficient

Regional Inputs ($ millions)

531 Real Estate 0.070 4.32 0.041 2.56493 Warehousing and Storage 0.047 2.93 0.047 2.93

2211Electric power generation, transmission, and distribution

0.025 1.58 0.019 1.2

491 U.S. Postal Service 0.013 0.8 0.010 0.6

55 Management of companies and enterprises 0.012 0.74 0.001 0.06

492 Couriers and messengers 0.011 0.71 0.008 0.55613 Employment services 0.010 0.63 0.008 0.55241 Insurance carriers 0.009 0.56 0.006 0.383363 Motor vehicle parts manufacturing 0.009 0.55 0.005 0.3

32411 Petroleum Refineries 0.009 0.54 0.000 042 Wholesale trade 0.009 0.54 0.008 0.51

5617 Services to buildings and dwellings 0.008 0.51 0.006 0.39Total Commodity Demand 0.369 22.816 0.234 14.51

ERA/AECOM Project No.18309 Page 23

Table 17. Commodity Inputs, Air Transportation (Inputs in $ millions)

NAICS CommodityGross

Absorption Coefficient

Gross Inputs

Regional Absorption Coefficient

Regional Inputs

32411 Petroleum Refineries 0.234 11.31 0.001 0.03

487, 488Scenic and sightseeing transportation and support activities for transportation

0.078 3.75 0.054 2.62

5324Commercial and industrial machinery and equipment rental and leasing

0.043 2.06 0.020 0.99

722 Food services and drinking places 0.037 1.8 0.031 1.51

5615 Travel arrangement and reservation services 0.034 1.66 0.011 0.54

531 Real Estate 0.024 1.16 0.014 0.695241 Insurance carriers 0.018 0.85 0.012 0.58517 Telecommunications 0.012 0.6 0.006 0.342 Wholesale trade 0.012 0.56 0.011 0.53

336411 Aircraft manufacturing 0.011 0.54 0.000 0

336413Other aircraft parts and auxiliary equipment manufacturing

0.010 0.49 0.007 0.33

5418 Advertising and related services 0.010 0.46 0.008 0.37

Total Commodity Demand 0.616 29.713 0.209 10.08

Table 18. Commodity Inputs, Truck Transportation (Inputs in $ millions)

NAICS CommodityGross

Absorption Coefficient

Gross Inputs

Regional Absorption Coefficient

Regional Inputs

484 Truck transportation 0.048 12.5 0.048 12.5491 U.S. Postal Service 0.040 10.49 0.030 7.87492 Couriers and messengers 0.036 9.31 0.025 6.525241 Insurance carriers 0.035 9.17 0.024 6.255613 Employment services 0.024 6.35 0.019 5.0842 Wholesale trade 0.015 3.85 0.014 3.66

487, 488Scenic and sightseeing transportation and support activities for transportation

0.016 4.28 0.011 2.99

3363 Motor vehicle parts manufacturing 0.020 5.14 0.011 2.76493 Warehousing and Storage 0.009 2.27 0.009 2.27531 Real Estate 0.014 3.77 0.009 2.235617 Services to buildings and dwellings 0.007 1.93 0.006 1.47

81111-2, 811191, 811198

Automotive repair and maintenance, except car washes

0.006 1.64 0.005 1.4

tal Commodity Demand 0.499 130.144 0.262 68.16

ERA/AECOM Project No.18309 Page 24

Table 19. Commodity Inputs, Courier Services (Inputs in $ millions)

NAICS CommodityGross

Absorption Coefficient

Gross Inputs

Regional Absorption Coefficient

Regional Inputs

32411 Petroleum Refineries 0.077 8.4 0.000 0.03491 U.S. Postal Service 0.014 1.49 0.010 1.12

55 Management of companies and enterprises 0.013 1.41 0.001 0.12

492 Couriers and messengers 0.012 1.32 0.008 0.93

487, 488Scenic and sightseeing transportation and support activities for transportation

0.012 1.31 0.008 0.92

531 Real Estate 0.012 1.26 0.007 0.755613 Employment services 0.010 1.04 0.008 0.8342 Wholesale trade 0.008 0.9 0.008 0.85

5611 Office administrative services 0.006 0.64 0.001 0.065241 Insurance carriers 0.006 0.63 0.004 0.43

53221-2, 53229, 5323

General and consumer goods rental except video tapes and discs

0.005 0.54 0.004 0.4

5617 Services to buildings and dwellings 0.005 0.54 0.004 0.41

Total Commodity Demand 0.237 25.855 0.098 10.72

Table 20. Top Commodity Inputs, Rail Transportation (Inputs in $ millions)

NAICS CommodityGross

Absorption Coefficient

Gross Inputs

Regional Absorption Coefficient

Regional Inputs

32411 Petroleum Refineries 0.059 0.43 0.000 0

23*Maintenance and repair construction of nonresidential

0.054 0.39 0.054 0.39

5324Commercial and industrial machinery and equipment rental and leasing

0.051 0.37 0.024 0.18

3365 Railroad rolling stock manufacturing 0.050 0.36 0.000 0

5222-3Nondepository credit intermediation and related activities

0.044 0.32 0.023 0.17

523Securities, commodity contracts, investments, and related activities

0.039 0.28 0.017 0.13

3211 Sawmills and wood preservation 0.013 0.1 0.002 0.0142 Wholesale trade 0.013 0.1 0.012 0.09

541512 Computer systems design services 0.012 0.09 0.002 0.015411 Legal services 0.010 0.08 0.008 0.05

5412Accounting, tax preparation, bookkeeping, and payroll services

0.010 0.07 0.008 0.06

5615 Travel arrangement and reservation services 0.009 0.07 0.003 0.02

Total Commodity Demand 0.481 3.492 0.213 1.54

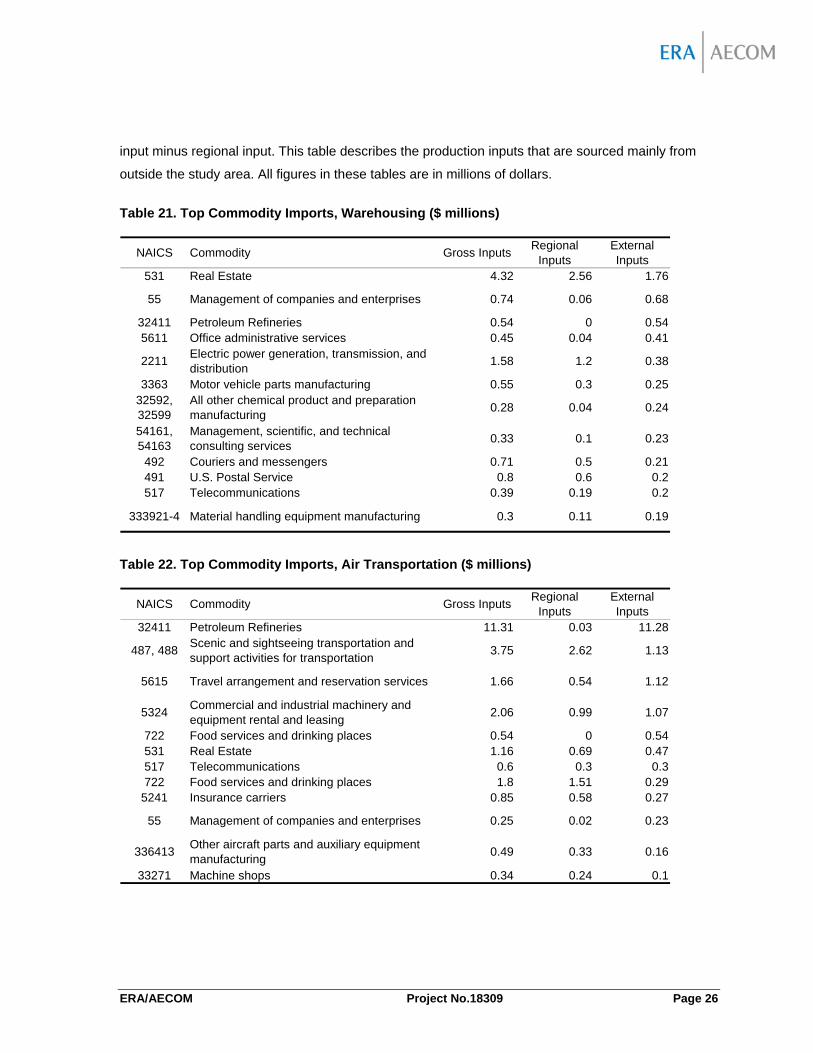

Commodity imports are related. In these tables, we present the goods and services that each industry

imports in the largest quantities. That is, the industries are sorted by external input, which is gross

ERA/AECOM Project No.18309 Page 25

input minus regional input. This table describes the production inputs that are sourced mainly from

outside the study area. All figures in these tables are in millions of dollars.

Table 21. Top Commodity Imports, Warehousing ($ millions)

NAICS Commodity Gross InputsRegional

InputsExternal Inputs

531 Real Estate 4.32 2.56 1.76

55 Management of companies and enterprises 0.74 0.06 0.68

32411 Petroleum Refineries 0.54 0 0.545611 Office administrative services 0.45 0.04 0.41

2211Electric power generation, transmission, and distribution

1.58 1.2 0.38

3363 Motor vehicle parts manufacturing 0.55 0.3 0.2532592, 32599

All other chemical product and preparation manufacturing

0.28 0.04 0.24

54161, 54163

Management, scientific, and technical consulting services

0.33 0.1 0.23

492 Couriers and messengers 0.71 0.5 0.21491 U.S. Postal Service 0.8 0.6 0.2517 Telecommunications 0.39 0.19 0.2

333921-4 Material handling equipment manufacturing 0.3 0.11 0.19

Table 22. Top Commodity Imports, Air Transportation ($ millions)

NAICS Commodity Gross InputsRegional

InputsExternal Inputs

32411 Petroleum Refineries 11.31 0.03 11.28

487, 488Scenic and sightseeing transportation and support activities for transportation

3.75 2.62 1.13

5615 Travel arrangement and reservation services 1.66 0.54 1.12

5324Commercial and industrial machinery and equipment rental and leasing

2.06 0.99 1.07

722 Food services and drinking places 0.54 0 0.54531 Real Estate 1.16 0.69 0.47517 Telecommunications 0.6 0.3 0.3722 Food services and drinking places 1.8 1.51 0.29

5241 Insurance carriers 0.85 0.58 0.27

55 Management of companies and enterprises 0.25 0.02 0.23

336413Other aircraft parts and auxiliary equipment manufacturing

0.49 0.33 0.16

33271 Machine shops 0.34 0.24 0.1

ERA/AECOM Project No.18309 Page 26

Table 23. Top Commodity Imports, Truck Transportation

NAICS Commodity Gross InputsRegional

InputsExternal Inputs

32411 Petroleum Refineries 27.27 0.08 27.195611 Office administrative services 3.85 0.35 3.55241 Insurance carriers 9.17 6.25 2.92492 Couriers and messengers 9.31 6.52 2.79

55 Management of companies and enterprises 2.99 0.26 2.73

491 U.S. Postal Service 10.49 7.87 2.62333 Transport by rail 3.02 0.42 2.6

3363 Motor vehicle parts manufacturing 5.14 2.76 2.38531 Real Estate 3.77 2.23 1.54

487, 488Scenic and sightseeing transportation and support activities for transportation

4.28 2.99 1.29

5613 Employment services 6.35 5.08 1.2732621 Tire manufacturing 1.18 0 1.18

Table 24. Top Commodity Imports, Courier Services

NAICS Commodity Gross InputsRegional

InputsExternal Inputs

32411 Petroleum Refineries 8.4 0.03 8.37

55 Management of companies and enterprises 1.41 0.12 1.29

5611 Office administrative services 0.64 0.06 0.58531 Real Estate 1.26 0.75 0.51492 Couriers and messengers 1.32 0.93 0.39

487, 488Scenic and sightseeing transportation and support activities for transportation

1.31 0.92 0.39

491 U.S. Postal Service 1.49 1.12 0.37517 Telecommunications 0.53 0.26 0.27

32621 Tire manufacturing 0.23 0 0.235613 Employment services 1.04 0.83 0.215241 Insurance carriers 0.63 0.43 0.2

336411 Aircraft manufacturing 0.18 0 0.18

ERA/AECOM Project No.18309 Page 27

Table 25. Top Commodity Imports, Rail Transportation

NAICS Commodity Gross InputsRegional

InputsExternal

Input32411 Petroleum Refineries 0.43 0 0.433365 Railroad rolling stock manufacturing 0.36 0 0.36

5324Commercial and industrial machinery and equipment rental and leasing

0.37 0.18 0.19

523Securities, commodity contracts, investments, and related activities

0.28 0.13 0.15

5222-3Nondepository credit intermediation and related activities

0.32 0.17 0.15

3211 Sawmills and wood preservation 0.1 0.01 0.09541512 Computer systems design services 0.09 0.01 0.0833151 Ferrous metal foundries 0.06 0 0.065615 Travel arrangement and reservation services 0.07 0.02 0.05

541513, 541519

Other computer related services, including facilities management

0.04 0.01 0.03

482 Rail Transportation 0.03 0 0.03

3311 Iron and steel mills and ferroalloy manufacturing 0.02 0 0.02

Industry Expenditures

The tables below show the various industries that buy the services of our select transportation

industries. Whereas above, the tables showed where transportation industries sent their dollars, the

tables below show where they get their dollars. The industries listed below are the customers of the

logistics industry in Winnebago County. As above, there are usually over one hundred industries that

buy the services of any given transportation industry. For convenience, we list the top twelve, sorted

by “Gross Input,” which is the amount spent by the industry listed.

ERA/AECOM Project No.18309 Page 28

Table 26. Industry Expenditures on Warehousing (Inputs in $ millions)

NAICS Sector GAC Gross InputsRegional Inputs

42 Wholesale Trade 0.010 10.58 10.58333995-6 Fluid power process machinery 0.003 2.96 2.96

493 Warehousing and storage 0.047 2.93 2.93484 Truck Transportation 0.009 2.27 2.27445 Retail - Food and beverage 0.011 2.12 2.12453 Retail - Miscellaneous 0.012 2.11 2.11452 Retail - General merchandise 0.011 2.08 2.08

33272Turned product and screw, nut, and bolt manufacturing

0.003 1.45 1.45

444 Retail - Building material and garden supply 0.010 1.20 1.20

3363 Motor vehicle parts manufacturing 0.002 0.93 0.9333271 Machine shops 0.004 0.85 0.85

623 Hospitals 0.001 0.84 0.84

Total Industries 0.717 54.13 54.13

Table 27. Industry Expenditures on Air Transportation (Inputs in $ millions)

NAICS Sector GAC Gross InputsRegional Inputs

42 Wholesale Trade 0.002 1.94 0.745613 Employment services 0.006 1.16 0.44

6211-3Offices of physicians, dentists, and other health practitioners

0.002 1.07 0.41

5619 Other support services 0.004 1.02 0.39722 Food services and drinking places 0.002 0.97 0.37

33271 Machine shops 0.004 0.89 0.345614 Business support services 0.008 0.89 0.34

51114, 51119

Directory, mailing list, and other publishers 0.008 0.85 0.32

491 Postal Service 0.010 0.84 0.32

33272Turned product and screw, nut, and bolt manufacturing

0.002 0.83 0.32

521, 5221Monetary authorities and depository credit intermediation

0.002 0.82 0.32

3363 Motor vehicle parts manufacturing 0.002 0.75 0.29

Total Industries 0.607 35.91 13.74

ERA/AECOM Project No.18309 Page 29

Table 28. Industry Expenditure on Truck Transportation (Inputs in $ millions)

NAICS Sector GAC Gross InputsRegional Inputs

484 Truck Transportation 0.048 12.50 12.50334111 Fluid power process machinery 0.010 10.38 10.38

23Construction of new residential permanent site single- and multi-family structures

0.020 7.11 7.11

3363 Motor vehicle parts manufacturing 0.012 5.94 5.94

333515Cutting tool and machine tool accessory manufacturing

0.026 5.24 5.24

311511-2 Fluid milk and butter manufacturing 0.028 5.04 5.0442 Wholesale trade 0.004 4.07 4.07

33272Turned product and screw, nut, and bolt manufacturing

0.009 4.02 4.02

31191 Snack food manufacturing 0.030 3.64 3.6432732 Ready-mix concrete manufacturing 0.102 3.58 3.58

722 Food services and drinking places 0.007 3.23 3.23

23Construction of new nonresidential commercial and health care structures

0.009 3.09 3.09

Total Industry 2.698 158.41 158.41

Table 29. Industry Expenditure on Courier Services (Inputs in $ millions)

NAICS Sector GAC Gross InputsRegional Inputs

42 Wholesale Trade 0.013 13.27 9.29484 Truck Transportation 0.036 9.31 6.52

51114, 51119

Directory, mailing list, and other publishers 0.019 2.03 1.42

5614 Business support services 0.014 1.59 1.12

487488Scenic and sightseeing transportation and support activities for transportation

0.037 1.45 1.01

5619 Other support services 0.006 1.44 1.01492 Couriers and messengers 0.012 1.32 0.93445 Retail - Food and beverage 0.005 1.04 0.73442 Retail - Motor vehicle and parts 0.006 1.04 0.73452 Retail - General merchandise 0.006 1.02 0.71

51112 Newspaper publishers 0.015 0.90 0.63

8134, 8139Grantmaking, giving, and social advocacy organizations

0.010 0.76 0.53

Total Industries 0.532 48.91 34.24

ERA/AECOM Project No.18309 Page 30

Table 30. Industry Expenditure on Rail Transportation (Inputs in $ millions)

NAICS SectorGross Absorption Coefficient

Gross InputsRegional Inputs

2212Electric power generation, transmission, and distribution

0.022 8.50 1.20

484 Truck Transportation 0.012 3.02 0.43

31134 Nonchocolate confectionery manufacturing 0.011 2.48 0.35

32551 Paint and coating manufacturing 0.013 1.77 0.2532221 Paperboard container manufacturing 0.016 1.76 0.25

333995-6 Fluid power process machinery 0.002 1.68 0.243363 Motor vehicle parts manufacturing 0.003 1.46 0.21

32561 Soap and cleaning compound manufacturing 0.008 1.37 0.19

311111 Dog and cat food manufacturing 0.022 1.23 0.17

31182 Cookie, cracker, and pasta manufacturing 0.014 1.07 0.15

31191 Snack food manufacturing 0.008 0.98 0.14

23Construction of new residential permanent site single- and multi-family structures

0.002 0.84 0.12

Total Industries 0.747 46.00 6.47

In many cases, the industry listed above roughly corresponds to the good or service being

transported. For example, “Motor Vehicle Parts Manufacturing” industry is a key customer in several

industries. This likely indicates that the product being shipped or stored is motor vehicle parts. A key

exception is the top customer of rail transportation, Electric Power Generation. This energy-intensive

industry, in turn, buys (and likely requires shipment of) significant amounts of petroleum, coal, natural

gas, and similar energy products.

Rail & Air Industry Notes

AECOM has been able to make some limited comparisons of the inputs and outputs of the air

transportation and rail transportation sectors from 2001 to 2007 for the geographic area. We should

caution here that economies are consistently in flux and the changes we observe can be due to a

variety of factors beyond our current understanding. Even so, we can draw some broad conclusions

about how the industry has changed over that period.

Rail

In both 2001 and 2007, power generation is the number one customer of rail transportation

firms—by a wide margin. In 2001, it represented 25 percent of intermediate (business) spending

on rail transportation, or three times higher than the next-nearest industry, motor vehicle parts

manufacturing. Power generation firms in this county consume goods such as oil, natural gas,

ERA/AECOM Project No.18309 Page 31

coal, petroleum, and wind turbines. These firms spend most of their transportation dollars on

pipeline and rail transportation.

From 2001 to 2007, motor vehicle parts manufacturers went from representing 8 percent of rail

firms’ business revenues to 3 percent. They went from the second-largest source of rail revenue

to the seventh-highest, as they contributed just $1.5 million in output in 2007, as compared with

$2.2 million in 2001.

Truck transportation firms are customers of rail transportation firms. This relationship is part of the

region’s intermodal linkages. In 2001, truck transportation firms represented about 4 percent of

the rail firms’ business inputs; by 2007, that had risen to 6.6 percent.

The food production industry is a key customer of rail transportation firms. The top twelve

industries for rail transportation firms include candy (nonchocolate confectionary) manufacturers;

cookie, cracker, and pasta manufacturers; snack food manufacturers; and dog and cat food

manufacturers. Paint and coating manufacturers are also a key customer of this industry.

Air

The air transportation industry has also seen revenues from motor vehicle parts manufacturers

decline. In 2001, motor vehicle parts manufacturers were the biggest industry customer of the air

transportation industry, representing 7 percent of its business revenues. By 2007, the spending

by motor vehicle parts manufacturers on air transportation fell by 60 percent and represented just

2 percent of the air transportation industry’s business revenues. Supplier parks may be one

contributing factor.

Hospitals, health care providers, the U.S. Postal Service, directory and mailing list vendors,

wholesalers, and restaurants were among the largest customers of air transportation in both

years.

Petroleum refineries are among the largest recipients of the air transportation industry’s

expenditures—obviously spending on fuel is a key input to the process of air transportation. In

2001, such expenditures represented 17 percent of industry outlays to other firms; by 2007, it

became 38 percent. (Note that this is a percentage of spending on goods and services and

excludes labor.) Very little of that spending stays in Winnebago County. It is no surprise to see,

then, that the indirect multiplier has fallen for the air transportation industry, as so much more

business spending has been going toward fuel from out of the county.

ERA/AECOM Project No.18309 Page 32

III. Logistics Hub Case Studies

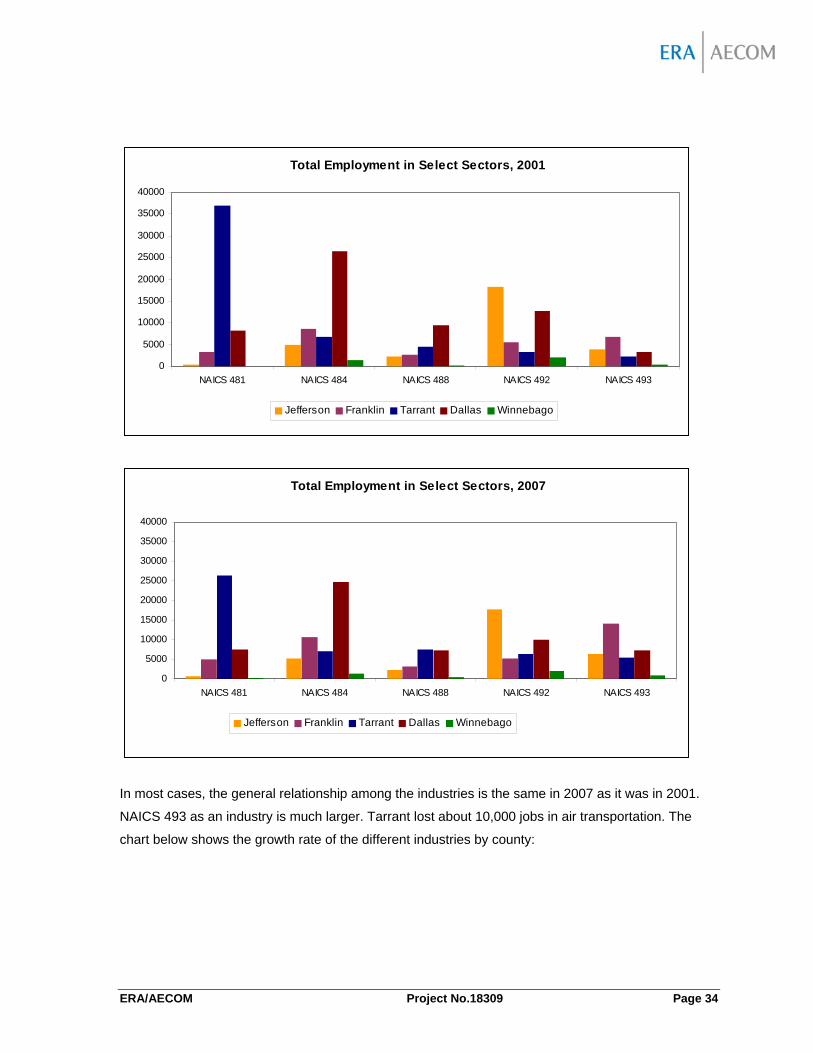

Employment Growth Comparison

This section describes employment in select logistics industries for the following counties:

Jefferson County, Kentucky (Louisville)

Franklin County, Ohio (Columbus)

Tarrant County, Texas (Fort Worth)

Dallas County, Texas (Dallas)

Winnebago County, Illinois (Rockford)