project pegasus - investor presentation

TRANSCRIPT

Management Presentation

NOK [324] - [463] million | IPO on Euronext Growth Oslo

[•] July 2021 | Strictly Private & Confidential

The Management Presentation contains only company highlights and must be read in conjunction with the Investor Presentation. The Management Presentation must not be solely relied upon when forming an investment decision

DRAFT

Strictly Private & Confidential

DR

AF

T

2

Disclaimer

By reading this company presentation or attending any meeting or oral presentation held in relation thereto (collectively the “Presentation”), you (the “Recipient”) agree to be bound by the following terms, conditions and limitations. The Presentation has

been produced by Astrocast SA (the “Company”).

THE PRESENTATION HAS BEEN PREPARED FOR INFORMATION PURPOSES ONLY AND DOES NOT CONSTITUTE, AND SHOULD NOT BE CONSTRUED AS, AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY SECURITIES IN

ANY JURISDICTION. THIS PRESENTATION AND ITS CONTENTS ARE STRICTLY CONFIDENTIAL. NEITHER THE PRESENTATION, NOR ANY PART OF IT, MAY BE DISCLOSED, REPRODUCED OR DISTRIBUTED, DIRECTLY OR INDIRECTLY, WITHOUT

THE PRIOR WRITTEN CONSENT OF THE COMPANY.

Distribution of this Presentation to any person other than the Recipient or its advisors, and any disclosure of any of the contents of this Presentation, without the prior written consent of the Company, is prohibited.

This document will be used during an oral presentation, and is therefore not a complete summary of the presentation held. The information contained in this Presentation has not been independently verified. This Presentation contains information which has

been sourced from third parties believed to be reliable, but without independent verification. None of the Company or any of its subsidiary undertakings or affiliates, or any directors, officers, employees, advisors or representatives (collectively

“Representatives”) make any representation or warranty (express or implied) whatsoever as to the accuracy, completeness or sufficiency of any information contained herein, and nothing contained in this Presentation is or can be relied upon as a promise

or representation by the Company or any of its Representatives.

None of the Company or any of its Representatives shall have any liability whatsoever (in negligence or otherwise) arising directly or indirectly from the use of this Presentation or its contents, including but not limited to any liability for errors, inaccuracies,

omissions or misleading statements in this Presentation, or violation of distribution restrictions. The Recipient acknowledges that it will be solely responsible for its own assessment of the Company, the market and the market position of the Company and

that you will conduct its own analysis and be solely responsible for forming its own view of the Company and of the potential future performance of the Company’s business. The content of this Presentation are not to be construed as legal, business,

investment or tax advice or other professional advice. The Recipient should consult with its own professional advisers for any such matter and advice.

This Presentation contains certain forward-looking statements relating to inter alia the business, financial performance and results of the Company and the industry in which it operates. Forward-looking statements concern future circumstances and results

and other statements that are not historical facts, sometimes identified by the words “believes”, “expects”, “predicts”, “intends”, “projects”, “plans”, “estimates”, “aims”, “foresees”, “anticipates”, “targets”, and similar expressions.

Furthermore, forward-looking information in this Presentation pertaining to financial performance is derived from the Company management's general model for budgeting (unless otherwise specifically mentioned) and is based on various assumptions. Such

information shall be viewed as management's financial targets, and shall neither be deemed nor construed as any form for guiding or forecast.

Any forward-looking statements contained in this Presentation, including assumptions, opinions and views of the Company, or cited from third party sources, are solely opinions and forecasts and are subject to risks, uncertainties and other factors that may

cause actual results and events to be materially different from those expected or implied by the forward-looking statements. None of the Company or its Representatives provides any assurance that the assumptions underlying such forward-looking

statements are free from errors nor do any of them accept any responsibility for the future accuracy of opinions expressed in this Presentation or the actual occurrence of forecasted developments.

This Presentation contains financial information derived from the Company's audited consolidated financial statements, the Company’s un-audited interim financial reports, as well as unaudited management reports. To obtain complete information of the

Company's financial position, operational results and cash flow, the financial information in this Presentation must be read in conjunction with the Company's audited financial statements and other regulatory financial information made public by the

Company.

This Presentation contains or may contain information about inter alia (A) views and opinions regarding the Company's performance, products and prospective products, including the attractiveness, usage, potential usage, competiveness and results of

such products, and (B) the markets in which the Company competes, including market growth, market size and market segment sizes, market share information and information on competing products, the Company's competitive position and the

competitive position of other market parties. The Company has assembled information about the aforementioned through formal and informal contacts with industry professionals, various other third party sources, annual reports and other information of its

competitors as well as its own experiences and collected information. Such sourced information from third parties is believed to be reliable, but has not been verified by independent experts, and there is no guarantee that such information is accurate or

complete and not misleading. Unless otherwise is specifically stated, the Company is the source of information included in this Presentation.

This Presentation speaks as at the date set out on herein. Neither the delivery of this Presentation nor any further discussions of the Company or its Representatives with the Recipient shall, under any circumstances, create any implication that there has

been no change in the market or the affairs of the Company since such date. Neither the Company nor its Representatives assumes any obligation to update or revise the Presentation or disclose any changes or revisions to the information contained in the

Presentation.

This Presentation is subject to Swiss law. Any dispute, controversy or claim arising out of, or relating to, this Presentation shall be finally settled by arbitration in Oslo in accordance with the Norwegian Arbitration Act 2004.

Strictly Private & Confidential

DR

AF

T

Transaction highlights

Issuer: • Astrocast SA, a company incorporated under the laws of Switzerland

Transaction:• Private Placement of NOK [324] - [463]m (the NOK equivalent of CHF 35 - 50 million) in gross proceeds (the “Private Placement”) of which CHF [•] is subscribed by way of conversion of debt

instruments (“CLAs”) that have been entered into in connection with an ongoing equity financing round led by Adit Ventures

Subscription Price: • NOK [27.75] (the NOK equivalent of CHF 3.00) per share, corresponding to a pre-money valuation of CHF [75,000,000] including outstanding employee options

Subscription Period:

• The subscription period will commence on [•] 2021 and close on [•] 2021 at 12:00 hours (CET)

• Notification of conditional allocation and payment instructions will be distributed on or about [•] 2021

• The application period may close earlier or later at the discretion of the Company's Board of Directors. If the application period is extended or shortened other dates referred to herein may be

changed accordingly

Use of proceeds: • Financing of capital expenditures in connection with the launch of nanosatellites and continued technical developments as well as the financing of negative operational cashflow

Current share capital:• 23,447,500 shares, each with a nominal value of CHF 0.01 per share

• 1,552,500 employee stock options (grantable and outstanding), each giving rise to a common share of a nominal value of CHF 0.01 for an exercise price determined by the Board of Directors

• [535,930] warrants, of which [430,030] warrants granted in connection with the issuance of CLAs, all to be exercised at CHF 0.01 at the time of completion of the Private Placement

Number of new shares: • [11,666,667] - [16,666,667] shares, each with a nominal value of CHF 0.01 per share

Minimum application:• The Private Placement is directed only towards investors who may lawfully participate in the Private Placement provided a minimum application and allocation of shares with a value of no less

than the NOK equivalent to EUR 100,000, unless relevant exceptions from applicable prospectus obligations are available

Allocation criteria:• At the sole discretion of the Board of Directors in consultation with the Manager, taking into consideration i.a. existing ownership, timeliness of the application, relative order size, sector

knowledge, perceived investor quality and investment horizon

Conditions to the

Share Issue:

• Completion of the Private Placement is subject to satisfaction of the following conditionsi. Final resolutions by the Company’s board of directors based on shareholder approval granted at the extraordinary general meeting held on 12 May 2021

ii. Payment being received for the offer shares

iii. Registration of the share capital increase pertaining to the Private Placement

Listing: • The Board of Directors intend to apply for listing on Euronext Growth in Oslo shortly following completion of the Private Placement

Lock-up:• Company: 12 months

• Executive management, founders and board of directors: 12 months (existing and new shares)

• Other shareholders: 6 months (existing shares only)

Target market:

• The manufacturer Target Market (MIFID II product governance) for the Private Placement is a) eligible counterparties, professional clients and retail clients (all distribution channels) and who; b)

have at least a common/normal understanding of the capital markets, c) is able to bear the losses of their invested amount and, d) is willing to accept risks connected with the shares, and e)

have an investment horizon which takes into consideration the liquidity of the shares. The negative target market for the Offer Shares is clients that seek full capital protection or full repayment

of the amount invested, are fully risk averse/have no risk tolerance or need a fully guaranteed income or fully predictable return profile

Manager: • Bryan, Garnier & Co3

Term sheet

Strictly Private & Confidential

DR

AF

T

FABIEN

JORDAN

CEO/FOUNDER

15-year experience in

nanosatellite business,

key engineer of the

SwissCube project,

worked on ESA

ExoMars mission

4

KJELL

KARLSEN

CFO

Former President of Sea

Launch AG. Led its

restructuring in 2010.

Participated in 39

launches with a total

payload value in excess

of $7 billion

Today’s presenters

JOSE

ACHACHE

CHAIRMAN

Former Director of Earth

Observation Programs

at ESA and Deputy

Director General for

Research and

Technology at CNES

ANTONIO

WALLER

VP OF

GLOBAL SALES

15+ years of general

sales, management and

business development

experience with a focus

on B2B technological

sectors, IoT, Fleet

Telematics, M2M and

Telecoms (Orbcomm in

particular)

Strictly Private & Confidential

DR

AF

T

5

High-level introduction

5

1

5

4

2

3

• Strong growth for IoT connectivity market

• Satellite coverage required for true global IoT connectivity

• Raising CHF 35 - 50m to complete first phase of satellite constellation

• Astrocast is ahead of the curve with a live system with key technology differentiation

• Nanosatellites offer radically lower costs and will drive satellite IoT connections

Strictly Private & Confidential

DR

AF

T

Source: Lora Alliance (2019) – Global cellular systems coverage & London Economics (2019) – Nanosatellite Telecommunications: A Market Study for IoT/M2M applications

Note: LoRa Alliance analysis does not include data for certain countries, notably China

6

Why satellite IoT? Global coverage at low cost!

Astrocast reduces major cost gap between terrestrial and satellite IoT

The ultimate success of global IoT coverage will depend on the active support of satellite networks

Astrocast racing down the cost curve unlocking massive IoT

market opportunity

Global cellular systems coverage overview

Cellular systems cover roughly 10% of the world’s surface area;

LPWANs cover only a fraction of this

Current satellite IoT Cellular IoT

Cost

Strictly Private & Confidential

DR

AF

T

Selected Tier 1 launchers and strategic partners of Astrocast

7

Commercial launch in January 2021

First 5 commercial satellites launched in January followed by 5 more in June

24 January 2021 launch 30 June 2021 launch

Strictly Private & Confidential

DR

AF

T

Introduction to Astrocast

Disrupting the fast-growing satellite IoT market with a leading integrated solution

• Enabling low-cost satellite IoT communication through

targeted 100 satellite infrastructure, fully designed and

assembled in-house

• Secured global commercial access to L-Band, the most

reliable and efficient spectrum for Satellite IoT applications

• Outperforming competition on power consumption, antenna

size and cost

8

Key partnersAt a glance

Established satellite operatorASIC & M2M protocol

Ground station servicesGrants & technical validation

Production partnerASIC development

Strictly Private & Confidential

DR

AF

T

9

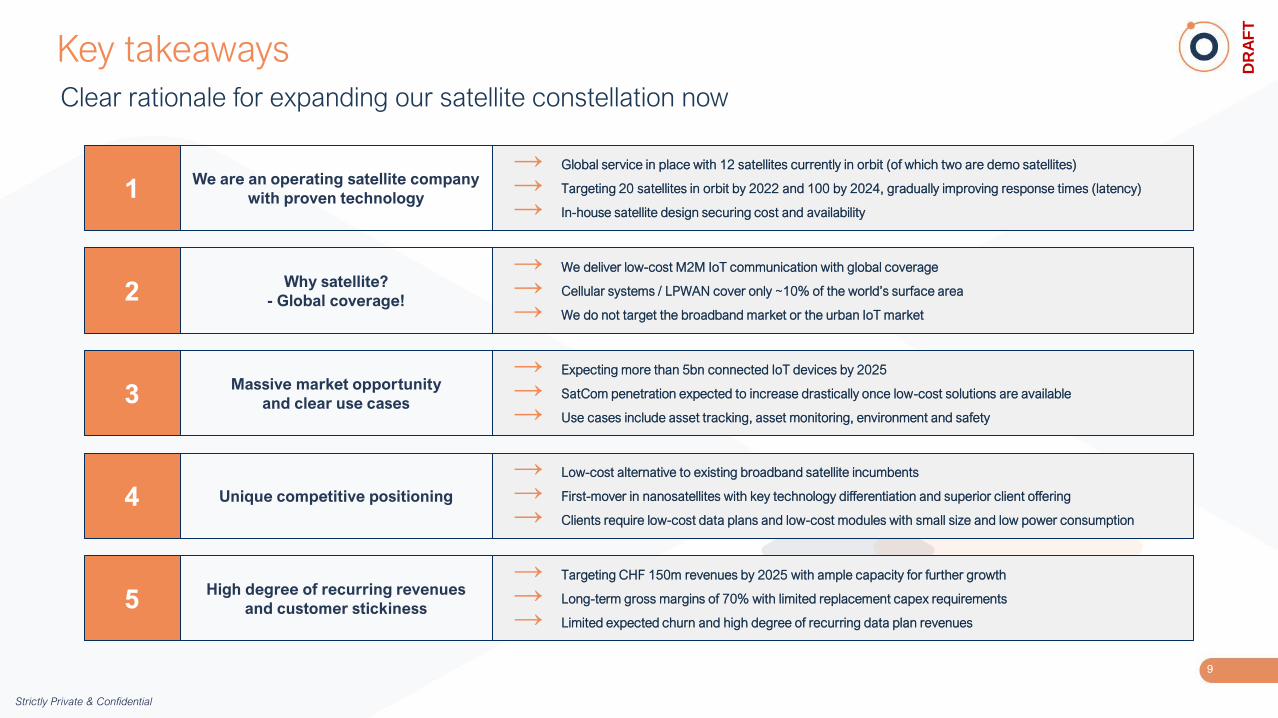

Key takeaways

9

Clear rationale for expanding our satellite constellation now

We are an operating satellite company

with proven technology

Why satellite?

- Global coverage!

→ Global service in place with 12 satellites currently in orbit (of which two are demo satellites)

→ Targeting 20 satellites in orbit by 2022 and 100 by 2024, gradually improving response times (latency)

→ In-house satellite design securing cost and availability

Massive market opportunity

and clear use cases

Unique competitive positioning

High degree of recurring revenues

and customer stickiness

→ We deliver low-cost M2M IoT communication with global coverage

→ Cellular systems / LPWAN cover only ~10% of the world’s surface area

→ We do not target the broadband market or the urban IoT market

→ Expecting more than 5bn connected IoT devices by 2025

→ SatCom penetration expected to increase drastically once low-cost solutions are available

→ Use cases include asset tracking, asset monitoring, environment and safety

→ Low-cost alternative to existing broadband satellite incumbents

→ First-mover in nanosatellites with key technology differentiation and superior client offering

→ Clients require low-cost data plans and low-cost modules with small size and low power consumption

→ Targeting CHF 150m revenues by 2025 with ample capacity for further growth

→ Long-term gross margins of 70% with limited replacement capex requirements

→ Limited expected churn and high degree of recurring data plan revenues

1

2

3

4

5

Strictly Private & Confidential

DR

AF

T

10

Vast number of use cases

Numerous sectors to benefit from low-cost satellite IoT connectivity

Asset monitoring

Industrial equipment tracking

Panic buttons

Environment & Utilities

Water infrastructure, environmental

sensors, smart metering

Oil, Gas & Mining

Heavy equipment, tracking and monitoring, well head

monitoring, cathodic protection, environmental sensors,

security

Maritime

Fishing buoys, navigation

and environmental buoys

Connected Vehicles

Vehicle telematics, commercial fleet

and rental vehicle tracking, mobile tank tracking,

fuel-chemical food tank monitoring

Agriculture & Livestock

Agriculture sensors, livestock

and species tracking

Strictly Private & Confidential

DR

AF

T

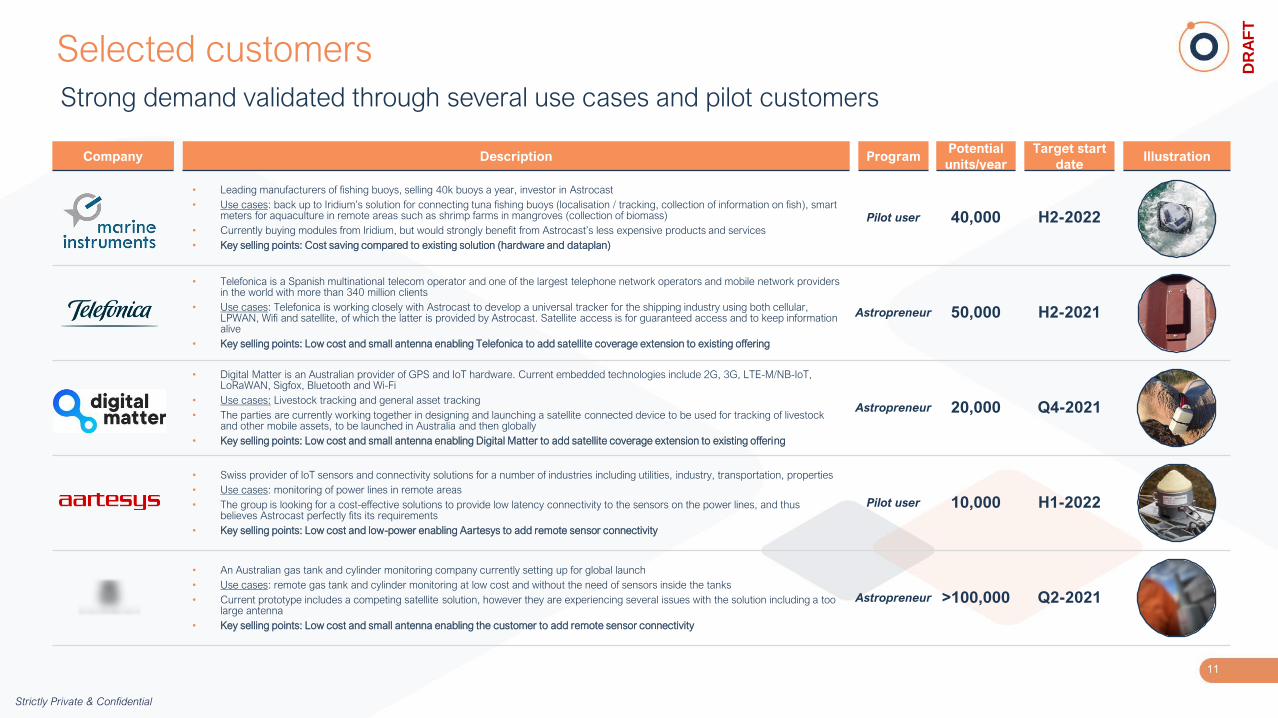

• Leading manufacturers of fishing buoys, selling 40k buoys a year, investor in Astrocast

• Use cases: back up to Iridium’s solution for connecting tuna fishing buoys (localisation / tracking, collection of information on fish), smart meters for aquaculture in remote areas such as shrimp farms in mangroves (collection of biomass)

• Currently buying modules from Iridium, but would strongly benefit from Astrocast’s less expensive products and services

• Key selling points: Cost saving compared to existing solution (hardware and dataplan)

• Swiss provider of IoT sensors and connectivity solutions for a number of industries including utilities, industry, transportation, properties

• Use cases: monitoring of power lines in remote areas

• The group is looking for a cost-effective solutions to provide low latency connectivity to the sensors on the power lines, and thus believes Astrocast perfectly fits its requirements

• Key selling points: Low cost and low-power enabling Aartesys to add remote sensor connectivity

• Digital Matter is an Australian provider of GPS and IoT hardware. Current embedded technologies include 2G, 3G, LTE-M/NB-IoT, LoRaWAN, Sigfox, Bluetooth and Wi-Fi

• Use cases: Livestock tracking and general asset tracking

• The parties are currently working together in designing and launching a satellite connected device to be used for tracking of livestock and other mobile assets, to be launched in Australia and then globally

• Key selling points: Low cost and small antenna enabling Digital Matter to add satellite coverage extension to existing offering

• Telefonica is a Spanish multinational telecom operator and one of the largest telephone network operators and mobile network providers in the world with more than 340 million clients

• Use cases: Telefonica is working closely with Astrocast to develop a universal tracker for the shipping industry using both cellular, LPWAN, Wifi and satellite, of which the latter is provided by Astrocast. Satellite access is for guaranteed access and to keep information alive

• Key selling points: Low cost and small antenna enabling Telefonica to add satellite coverage extension to existing offering

11

Selected customers

Strong demand validated through several use cases and pilot customers

• An Australian gas tank and cylinder monitoring company currently setting up for global launch

• Use cases: remote gas tank and cylinder monitoring at low cost and without the need of sensors inside the tanks

• Current prototype includes a competing satellite solution, however they are experiencing several issues with the solution including a too large antenna

• Key selling points: Low cost and small antenna enabling the customer to add remote sensor connectivity

Company Description Program IllustrationTarget start

date

Potential

units/year

Pilot user

Astropreneur

Astropreneur

Pilot user

Astropreneur

40,000 H2-2022

50,000 H2-2021

20,000 Q4-2021

10,000 H1-2022

>100,000 Q2-2021

Strictly Private & Confidential

DR

AF

T

12

Strong ESG profile

Actively supporting sustainability and poverty relief

Humanitarian relief Wildlife tracking Biodiversity

Wildfire detection, animal tracking,

water monitoring & vehicle monitoring

Wildlife tracking, supporting

biodiversity

Satellite connected beehive

monitoring

Strictly Private & Confidential

DR

AF

T

13

Market to grow >50% annually

Satellite connectivity required to deploy global IoT

Number of satellite IoT connections & penetration

2.5 m

30.3 m

2019 2025E

Satellite penetration expected to increase 3-4x by 2025

Source: Ericsson Mobility Report (2020), Transforma Insight, ReTHINK 2019 and company estimates

~ 0.2%

+3 - 4x

CAGR:

52%

SatCom penetration2

1. Cellular includes LPWAN (NB-IoT / LTE-M) access technologies as well as 2G/3G/4G/5G

2. Calculated as satellite IoT connections divided by cellular IoT connections

Comments

• Number of cellular IoT connected

devices market will increase massively:

• Ericsson forecasts 5.2bn in

2025

• Transforma Insight forecasts

3.8bn in 2025

• Cellular IoT is driving growth in satellite

connected devices, as satellite

connectivity will play an essential role in

providing and unlocking true global

coverage thus expected to grow in

penetration

• ReTHINK forecasts that there will be

30.6m satellite connected IoT devices

in 2025 – growing 52% annually from

2019

• Estimates varies significantly between

market research firms

Strictly Private & Confidential

DR

AF

T

14

Astrocast’s constellation is optimized for M2M/IoT

Clear differentiation for nanosatellites against incumbents and broadband providers

Nano Micro Mini Small Medium-Intermediate Large

Heavy/

Extra heavy

(1 – 10) (10 – 200) (200 – 600) (600 – 1,200) (1,200 – 4,200) (4,200 – 5,400) (5,400 – +7,000)Mass

(KG)

Example

Cost per

satellite2

Lifetime

Orbit

since

Inmarsat 5-F2

6,100 kg

~250,000,000

USD

200,000,000

USD

Telephone and

data services

Direct

broadcasting

+15 years15 years

~150,000,000

USD

Fixed telecommunications

and direct-to-home

television broadcasting

15 years

~40,000,000

USD

Global mobile

satellite network

15 years

~1,000,000

USD

Broadband

internet access

1-5 years

~6,500,000

USD

Communication

M2M/IoT, traffic

monitoring

+5 years

~250,000

USD

Communication

M2M3/IoT

3-5 years

Iridium NEXT

860 kg

Target

user(s)

2013

(in GEO)

2009

(in GEO)

2008

(in GEO)

2017

(in LEO)

2019

(in LEO)

2012

(in LEO)

2019

(in LEO)

Orbcomm OG2

172 kg

Astrocast 0.2

(CubeSat1 3U)

4 kg

Starlink Block v1.0

260 kg

Thor 5

1,960 kgHotbird 10

4,900 kg

Source: UCS Satellite Database, Skyrocket, Company websites 1) One CubeSat unit measures 10x10x10 cm, 2) Estimated cost, 3) M2M = Machine to machine

Typical

receiver

Astronode

Patch antenna

Strictly Private & Confidential

DR

AF

T

15

Astrocast in pole position to capture key IoT segments

Asset

tracking Telemetry

Telematics /

analytics

Fixed safety,

security &

emergency

Mobile safety,

security &

emergency

Command &

control

Mobile

telephony Video

Internet

broadband

Cargo logistics

Long-range tracking

Location tracking

Animal tracking

Asset & equipment

monitoring

Meter reading

Tanker tracking

Vehicle diagnostics

Fishery management

Flow monitoring

Systems monitoring

Weather data

Fuel management

Dispatch optimisation

Route optimisation

Maintenance

optimisation

Authentication

systems

Anti-theft systems

Panic alerts

Theft prevention

Security

management

Emergency response

Emergency

assistance

Accident or incident

First responders

Security alert

systems

Automation

Door/gate locking &

unlocking

Alarm management

Asset/station control

Communication

Border patrols

Coast guard

CCTV cameras

Video monitoring

Broadband internet

access

Use cases

Astrocast target use

cases and applications

Source: London Economics (2017): “Nanosatellite Telecommunications: A Market Study for IoT/M2M applications”

Wide variety in requirements for satellite communication

Selected

applications

1 2 3 4 5 6 7 8 9

Selected

players1

Low bandwidth, high latency Low bandwidth, moderate/low latency High bandwidth, ultra-low latency

Note 1: non-exhaustive list of players

Strictly Private & Confidential

DR

AF

T

Unmatched combination of technologies

Proprietary ultra-low power M2M modules In-house satellite design

Enabling low-cost connectivity and small-size devices

• 100% internally designed; small-sized and low-

power L-band antenna significantly reducing

satellite weight and cost

• 3-5 year lifespan1

• 3 axis pointing system and state-of-the-art

propulsion system securing position and

altitude control and allows for collision

avoidance maneuvers – reducing the risk of

losing the satellite and creating debris in space

• Two different products addressing different

needs;

1. Module: Off-the-shelf solution for easy

integration of satellite communication into

existing applications using reliable

communication standards

2. Chipset: For customers looking to embed

RF app to own products (available from

2023)

5m

m

16Note 1: Assuming ~3 year lifespan, balancing unit capex and technical obsolescence against longevity. Functional lifespan is demonstrated to be higher than 3 years.

Small form-factor Antenna

• Antenna is a critical part of the form-factor of

the IoT system, and while modules can be

miniaturized further, antennas offers less

flexibility

• L-Band antennas are the most versatile in the

market and can take the form of a patch in a

similar way as a GPS antenna

• Satellite IoT solutions based on other spectrum

such as UHF/VHF could result in a bulkier

solution

+ +

Astrocast patch antenna

Astrocast antenna vs.

competitor antenna

Strictly Private & Confidential

DR

AF

T

17

Strong competitive edge driven by L-Band access

Astrocast is superior on key metrics such as cost, power consumption and size

Commercial access to L-Band

• The L-Band spectrum offers superior

performance over more commonly

used UHF frequencies, including

1. Smaller antennas (reducing weight

and cost)

2. Less power consumption due to

more efficient radio frequency

components

3. More reliable two-way connection

(less interference or weather-related

perturbation risk)

• L-Band access is secured via an

exclusive strategic partnership with

Thuraya, and is a major advantage

for Astrocast in the satellite IoT

industry

Competitive positioning

Antenna size Frequency Peak power Latency Cost per module

L-Band Low <$50

UHF/VHF Medium <$50

UHF - Medium -

VHF Low $119

UHF/VHF - Low -

L-Band Low <$120

Antenna size Frequency Peak power LatencyCost per

module

Source: Management assessments

Strictly Private & Confidential

DR

AF

T

Tentative deployment schedule

Constellation to be scaled with increasing customer base

18

Deployment

schedule

(tentative)

Customer

focus1

2021

2022

2023

2024

2025

2021

2023

2024

2022

2025

Expected number of satellites in the constellation

Successful launch of the

1st orbital plane in January

24th (5 3U satellites on-

boarded)

Launch of the 2nd orbital

plane in Q3 (5 3U

satellites on-boarded)

Launch of the 4th/5th/6th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 3rd orbital

plane between Q4 & Q1

(10 6U satellites on-

boarded)

Launch of the 7th orbital

plane between Q1 & Q2

(10 3U satellites on-

boarded)

Launch of the 8th/9th/10th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 11th/12th/13th

orbital planes between Q2 & Q4

(10 6U satellites on-boarded)

5

10

20

30

40

50

60

70

80

90

90

95

100

Start of the deployment of

the 6U satellites

Start of the replacement of

the oldest satellites in the

constellation

Optimal targeted latency

reached in key areas

Optimal targeted

latency reached

globally

5

2021

2023

2024

2022

2025

Expected number of satellites in the constellation

Successful launch of the

1st orbital plane in January

24th (5 3U satellites on-

boarded)

Launch of the 2nd orbital

plane in Q3 (5 3U

satellites on-boarded)

Launch of the 4th/5th/6th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 3rd orbital

plane between Q4 & Q1

(10 6U satellites on-

boarded)

Launch of the 7th orbital

plane between Q1 & Q2

(10 3U satellites on-

boarded)

Launch of the 8th/9th/10th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 11th/12th/13th

orbital planes between Q2 & Q4

(10 6U satellites on-boarded)

5

10

20

30

40

50

60

70

80

90

90

95

100

Start of the deployment of

the 6U satellites

Start of the replacement of

the oldest satellites in the

constellation

Optimal targeted latency

reached in key areas

Optimal targeted

latency reached

globally

10

2021

2023

2024

2022

2025

Expected number of satellites in the constellation

Successful launch of the

1st orbital plane in January

24th (5 3U satellites on-

boarded)

Launch of the 2nd orbital

plane in Q3 (5 3U

satellites on-boarded)

Launch of the 4th/5th/6th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 3rd orbital

plane between Q4 & Q1

(10 6U satellites on-

boarded)

Launch of the 7th orbital

plane between Q1 & Q2

(10 3U satellites on-

boarded)

Launch of the 8th/9th/10th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 11th/12th/13th

orbital planes between Q2 & Q4

(10 6U satellites on-boarded)

5

10

20

30

40

50

60

70

80

90

90

95

100

Start of the deployment of

the 6U satellites

Start of the replacement of

the oldest satellites in the

constellation

Optimal targeted latency

reached in key areas

Optimal targeted

latency reached

globally

20

2021

2023

2024

2022

2025

Expected number of satellites in the constellation

Successful launch of the

1st orbital plane in January

24th (5 3U satellites on-

boarded)

Launch of the 2nd orbital

plane in Q3 (5 3U

satellites on-boarded)

Launch of the 4th/5th/6th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 3rd orbital

plane between Q4 & Q1

(10 6U satellites on-

boarded)

Launch of the 7th orbital

plane between Q1 & Q2

(10 3U satellites on-

boarded)

Launch of the 8th/9th/10th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 11th/12th/13th

orbital planes between Q2 & Q4

(10 6U satellites on-boarded)

5

10

20

30

40

50

60

70

80

90

90

95

100

Start of the deployment of

the 6U satellites

Start of the replacement of

the oldest satellites in the

constellation

Optimal targeted latency

reached in key areas

Optimal targeted

latency reached

globally

50+

2021

2023

2024

2022

2025

Expected number of satellites in the constellation

Successful launch of the

1st orbital plane in January

24th (5 3U satellites on-

boarded)

Launch of the 2nd orbital

plane in Q3 (5 3U

satellites on-boarded)

Launch of the 4th/5th/6th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 3rd orbital

plane between Q4 & Q1

(10 6U satellites on-

boarded)

Launch of the 7th orbital

plane between Q1 & Q2

(10 3U satellites on-

boarded)

Launch of the 8th/9th/10th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 11th/12th/13th

orbital planes between Q2 & Q4

(10 6U satellites on-boarded)

5

10

20

30

40

50

60

70

80

90

90

95

100

Start of the deployment of

the 6U satellites

Start of the replacement of

the oldest satellites in the

constellation

Optimal targeted latency

reached in key areas

Optimal targeted

latency reached

globally

80+

2021

2023

2024

2022

2025

Expected number of satellites in the constellation

Successful launch of the

1st orbital plane in January

24th (5 3U satellites on-

boarded)

Launch of the 2nd orbital

plane in Q3 (5 3U

satellites on-boarded)

Launch of the 4th/5th/6th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 3rd orbital

plane between Q4 & Q1

(10 6U satellites on-

boarded)

Launch of the 7th orbital

plane between Q1 & Q2

(10 3U satellites on-

boarded)

Launch of the 8th/9th/10th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 11th/12th/13th

orbital planes between Q2 & Q4

(10 6U satellites on-boarded)

5

10

20

30

40

50

60

70

80

90

90

95

100

Start of the deployment of

the 6U satellites

Start of the replacement of

the oldest satellites in the

constellation

Optimal targeted latency

reached in key areas

Optimal targeted

latency reached

globally

Successful launch of

the 1st orbital plane on

January 24th (5 3U

satellites on-boarded)

Launch of the 3rd

orbital plane (10 3U

satellites on-boarded)

Small and agile companies with pre-

defined demand and incoming calls

Target

industries1

+ Local market-leaders with higher volumes + Global market-leaders

Tank monitoring, Environmental, Ag-

Tech, Infrastructure, Utilities,

Livestock and Wildlife Tracking

+ Fishing buoys and Fisheries, Container

tracking, Oil and Gas, Vehicle telematics

+ SOS systems (e.g. automotive

industry)

Build brand and reference casesValidate technology Scale up and broaden industry reach Target major players

Launch of the 4th/5th/6th

orbital planes (10 6U

satellites on-boarded in

each plane)

Improved latency makes available new industries

Launch of the 7t/8th/9th or

more orbital planes (10 6U

satellites on-boarded in

each plane)

Start of the

deployment of the

6U satellite

Start of the replacement of

the oldest satellites in the

constellation

Note 1: Significant overlap expected

2021

2023

2024

2022

2025

Expected number of satellites in the constellation

Successful launch of the

1st orbital plane in January

24th (5 3U satellites on-

boarded)

Launch of the 2nd orbital

plane in Q3 (5 3U

satellites on-boarded)

Launch of the 4th/5th/6th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 3rd orbital

plane between Q4 & Q1

(10 6U satellites on-

boarded)

Launch of the 7th orbital

plane between Q1 & Q2

(10 3U satellites on-

boarded)

Launch of the 8th/9th/10th

orbital planes between Q3

& Q4 (10 6U satellites on-

boarded in each plane)

Launch of the 11th/12th/13th

orbital planes between Q2 & Q4

(10 6U satellites on-boarded)

5

10

20

30

40

50

60

70

80

90

90

95

100

Start of the deployment of

the 6U satellites

Start of the replacement of

the oldest satellites in the

constellation

Optimal targeted latency

reached in key areas

Optimal targeted

latency reached

globally

= cumulative # of satellites

Market canvassing

and pilot testing

Testing and evaluation

for a broad range of

applications

Successful launch of the

2nd orbital plane on 30 June

(5 3U satellites on-

boarded)

Strictly Private & Confidential

DR

AF

T

19

Key financials

Astrocast expects revenue of more than CHF 150m in 2025

Market share 2025Expecting strong growth towards break even in 2025

• By 2025 Astrocast estimates a

market share of ~25% for

connected satellite IoT devices

~25%~75%

Astrocast Others

Total market

size of 30m

units

• Astrocast expects strong revenue development driven by ramp-up of sales activities and continuous deployment of satellites

• As more satellites are deployed and latency is reduced, additional market segments becomes available and increases total

addressable market

CHFm

• Long-term gross

margins of 70%

• Long-term EBITDA

margins of >50%

• Estimated capacity

utilization 2025 (KB)

of less than 25%

• Annual replacement

Capex of CHF ~17m~30%

~30%

~40%

2025e

COGS

Opex

EBITDA

1Not significant

>150

2020a 2021e 2022e 2023e 2024e 2025e

Other

Data plan

Hardware

Strictly Private & Confidential

DR

AF

T

20

Recurring revenues to increase by installed base

Device battery life creates a sticky customer base

Revenue break-down by sales categoryProducts

100%

2021e 2024e2022e

100%

2023e 2025e

100% 100% 100%

Other salesHardware sales Data plan sales

~80%data plan

recurring revenue target

Modules:

• Off-the-shelf solution for easy integration of satellite communication

• Module cost less than EUR 50

Chips:

• For customers looking to embed RF app to own products (available from

2023)

• Very compact ASIC / Price below EUR8

• Data plan revenues are based on monthly flat fee typically between USD 0.5

and 3.0 per month per device which includes up to 5 kilobytes

• No activation fees or hidden fees

• Data plans will make up an increasing share of revenues going forward

Modules & chips

Data plans (estimated prices)

Strictly Private & Confidential

DR

AF

T

2020a 2021e 2022e 2023e 2024e 2025e

Total capex

21

CHF 50m provides cash runway out 2022

Secures payment for 201 additional satellites

Capex development2EBITDA development

Cash requirements breakdown Comments

• Gross proceeds of 50m provides sufficient cash for estimated Capex (deployment and

R&D), Opex and any working capital requirements until end of 2022. Gross proceeds of

CHF 35m provides sufficient cash runway until end of H1-2022

• Total funding requirements before any new financing is c. CHF 120m which occurs in

end of 2024, at which point the company expects to turn cash flow positive

• Significant milestones before end of 2022 are payment for 201 satellites (in addition to

the 10 in orbit) and ramp-up of sales and marketing which is expected to secure strong

inflow of customers. Gross proceeds of CHF 35 secures payment for 10 satellites

• Capex requirements beyond 2025 are expected to remain at CHF 17m, of which the

majority will be satellite replacement Capex

• As of May 2021, Astrocast has a net debt position of CHF 10.3m

CHFm CHFm

40%

60%

Cumulative cash requirement (CHFm)

CHF

c.120m

After

2022e

Until

2022e

30%

40%

30%

Use of proceeds

CHF

c.120m

S&M,

Operations,

regulatory &

other expenses

Constellation

Capex

R&D

Opex &

Capex

Note 1: Launch costs are usually prepaid well ahead of launch, thus there is a delay from payment to launch of satellite. Targeting a total of 20 satellites in orbit within end of 2022

Note 2: Includes Constellation Capex and R&D

Steady-state Capex

requirement of CHF

~17m

Capex peak in 2023 and 2024

due to accelerated satellite

launches and R&D related to

development of chipset

Targeting

~30% EBITDA

margin in 2025

2020a 2021e 2022e 2023e 2024e 2025e

EBITDA

Strictly Private & Confidential

DR

AF

T

Introduction to transaction

In pole position for growth

IPO to unlock an untapped, massive market opportunity

IPO considerations

• Astrocast has spent 7 years and CHF 24m developing a complete end-to-

end nanosatellite solution, including satellites, communications platform

and modules

• Positioned well ahead of any competitor for providing global, low-cost

satellite IoT coverage with small modules offering long battery life

• Astrocast is now engaging commercial discussions with partners across

the globe from large international corporates and asset owners, to IoT and

maritime equipment specialists

• Extension of an ongoing financing round1 to CHF 35 - 50m by tapping

public markets through a Euronext Growth Oslo IPO

• The ongoing financing round is led by US based Adit Ventures, whose

track record includes Palantir, SpaceX, Klarna, Spotify, AirBnB and

Snapchat. Palantir have pre-committed to subscribe for CHF 5m. CEO

Fabien Jordan and family has subscribed for CHF 0.7m

• CHF 50m secures payment for 202 satellites in addition to the 10 currently

in orbit, full commercial launch and provides cash runway until end of

2022. CHF 35m secures 12 months cash

• Total financing need for full constellation of 100 satellites is estimated at

CHF ~120m

22

The satellite and module Lead investor

Note 1: The ongoing financing round (to be extended with IPO) of up to CHF 15m is done by way of convertible loan notes with mandatory conversion at IPO

Note 2: Launch costs are usually prepaid well ahead of launch, thus there is a delay from payment to launch of satellite. Targeting a total of 20 satellites in orbit within end of 2022

5-8kg (6U version)

Strictly Private & Confidential

DR

AF

T

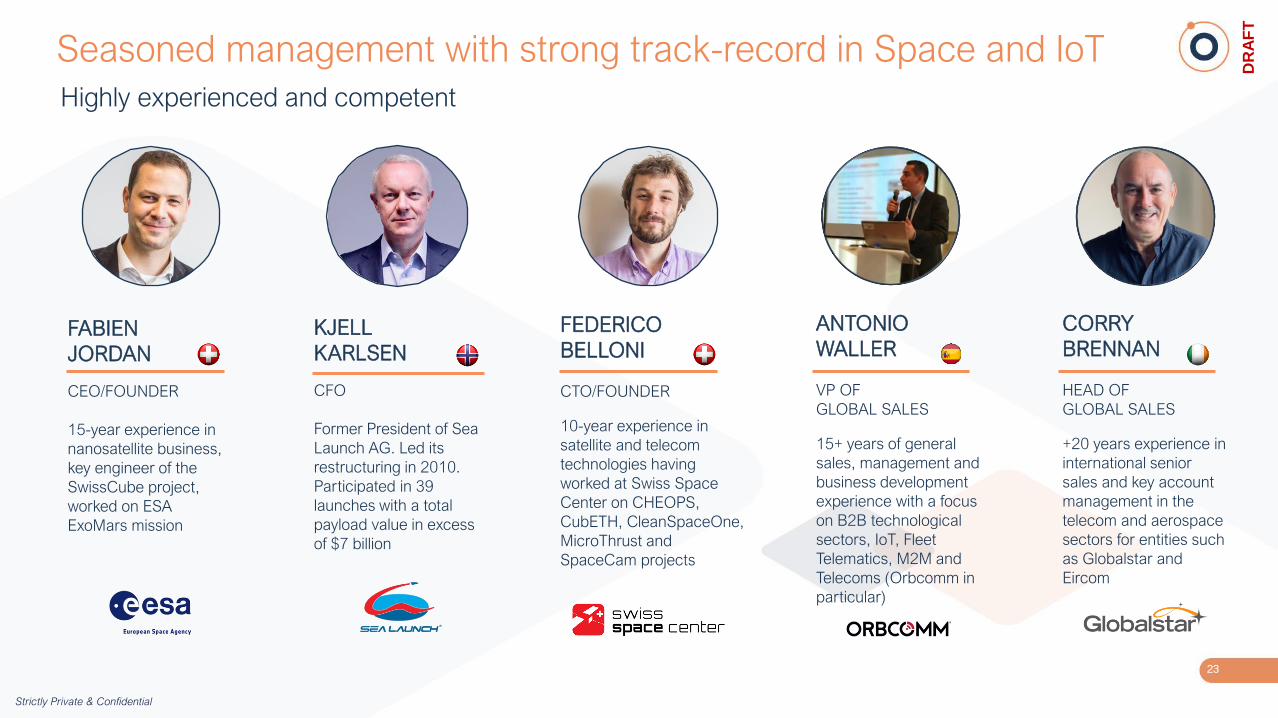

FEDERICO

BELLONI

CTO/FOUNDER

10-year experience in

satellite and telecom

technologies having

worked at Swiss Space

Center on CHEOPS,

CubETH, CleanSpaceOne,

MicroThrust and

SpaceCam projects

FABIEN

JORDAN

CEO/FOUNDER

15-year experience in

nanosatellite business,

key engineer of the

SwissCube project,

worked on ESA

ExoMars mission

23

KJELL

KARLSEN

CFO

Former President of Sea

Launch AG. Led its

restructuring in 2010.

Participated in 39

launches with a total

payload value in excess

of $7 billion

CORRY

BRENNAN

HEAD OF

GLOBAL SALES

+20 years experience in

international senior

sales and key account

management in the

telecom and aerospace

sectors for entities such

as Globalstar and

Eircom

Seasoned management with strong track-record in Space and IoT

Highly experienced and competent

ANTONIO

WALLER

VP OF

GLOBAL SALES

15+ years of general

sales, management and

business development

experience with a focus

on B2B technological

sectors, IoT, Fleet

Telematics, M2M and

Telecoms (Orbcomm in

particular)

Strictly Private & Confidential

DR

AF

T

24

Senior and competent Board of Directors

Strong industry expertise

JOSE

ACHACHE

CHAIRMAN

Former Director of

Earth Observation

Programs at ESA and

Deputy Director

General for Research

and Technology at

CNES

FEDERICO

BELLONI

CTO/FOUNDER &

BOARD MEMBER

10-year experience in

satellite and telecom

technologies having

worked at Swiss Space

Center on CHEOPS,

CubETH,

CleanSpaceOne,

MicroThrust and

SpaceCam projects

FABIEN

JORDAN

CEO/FOUNDER &

BOARD MEMBER

15-year experience in

nanosatellite business,

key engineer of the

SwissCube project,

worked on ESA

ExoMars mission

ROLAND

LOOS

BOARD MEMBER

Extensive experience

in satellite and telecom

technologies having

worked as COO and

EVP of ITC Global,

founder of NewSat

Communications as

well as Director at

Verestar

YVES

PILLONEL

BOARD MEMBER

More than 25 years of

experience as Portfolio

Manager and focusing

on client acquisition at

leading banks and

private institutions

including UBS and

Pictet. Currently Senior

VP Private Banking at

Suntrust Investment

JAN EYVIN

WANG

BOARD MEMBER

(to be appointed)

Joined Wilhelmsen in

1981 and currently

holds the position as

Executive Vice

President New Energy.

Has held several senior

positions in Norway

and abroad.

JON

CHOLAK

BOARD MEMBER

(to be appointed)

Seasoned venture

investor and software

professional with over

15 years of industry

experience. Currently

serving as Managing

Director of Adit

Ventures

Strictly Private & Confidential

DR

AF

T

Shareholder overviewShareholder list

Shareholders

Shareholder overview and CLAs

There are currently several share classes, however all shares will be converted into ordinary shares in connection with the Private Placement

There are [1,552,500] employee stock options (grantable and outstanding), each giving rise to a common share of a nominal value of CHF 0.01 for an exercise price determined by the Board of Directors

Founders34.4%

Management5.5%

Advisors3.9%Angel Investors

15.0%

Institutional investors

33.1%

Employees1.8%

ESOP6.2%

Overview based on a fully diluted basis but before conversion of CLAs

25

Convertible Loan Agreements (CLA)

• An ongoing financing round is conducted by way of Convertible Loan Agreements (CLA). The

CLAs convert at the share price in the Private Placement and include a warrant package.

Total signed CLAs amount to CHF [8,940,000], of which [8,440,000] have already been paid

to the Company. The Private Placement of NOK [324] – [463]m (CHF 35 - 50m) includes both

the CLAs as well as new equity, i.e., the equity requirement is reduced by the CLA amount

• The issued CLAs include a total warrant package (pre-funding bonus) of [430,030] warrants

which is exercisable at the time of completion for the Private Placement at CHF [0.01] per

share

# Investor Category Shares Shares %

1 Schroder & Co Banque SA Institutional investors 3,590,800 14.4%

2 Fabien Jordan Founders 1,736,700 6.9%

3 Federico Belloni Founders 1,705,900 6.8%

4 Julian Harris Founders 1,670,500 6.7%

5 Jean-Michel Jordan Founders 1,648,600 6.6%

6 Bertil Chapuis Founders 1,640,500 6.6%

7 Coges Corraterie Gestion SA Institutional investors 1,026,000 4.1%

8 José Achache Management 700,100 2.8%

9 Nest Sammelstiftung Institutional investors 691,800 2.8%

10 Roland Loos Angel investors 652,000 2.6%

11 Airbus Group Ventures Fund II, L.P. Institutional investors 625,000 2.5%

12 François Stieger Advisors 493,300 2.0%

13 Richard Samuel Friedrich von Tcharner Angel investors 485,400 1.9%

14 Adit Growth Equity III, LLC Institutional investors 401,000 1.6%

15 CHANCO HOLDINGS ADVISORS SA Institutional investors 387,800 1.6%

16 André Jolivet Angel investors 360,000 1.4%

17 Kjell Karlsen Management 310,000 1.2%

18 Muriel Richard Advisors 292,000 1.2%

19 Verve Investment Syndicates LLC Institutional investors 266,400 1.1%

20 David Wicki Angel investors 247,400 1.0%

21 SIMPRA INVESTMENT HOLDING LIMITED Institutional investors 242,000 1.0%

22 Marco Germoni Angel investors 241,900 1.0%

23 Philippe Bertherat Angel investors 238,700 1.0%

24 Cocktail Fund Ltd. Institutional investors 213,900 0.9%

25 Bryan Eagle Management 200,000 0.8%

26 Sveinung Melbo Angel investors 200,000 0.8%

27 Maurice Hälg Angel investors 199,200 0.8%

28 Gaëtan Marti Angel investors 199,200 0.8%

29 DAA Capital - Tech 1291 Ventures I Institutional investors 199,200 0.8%

30 Nicholas Petrig Founders 197,400 0.8%

Total top 30 21,062,700 84.3%

Rest (48 shareholders) 2,384,800 9.5%

Total 23,447,500 93.8%

Options 1,552,500 6.2%

Total (fully diluted) 25,000,000 100.0%