project on consumer behaviour

TRANSCRIPT

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 1/54

CHAPTER 1

INTRODUCTION

1.1. Problem statement:

Today, when Vietnam is going to market economy, three different types of

business that operated for profit: manufacturing, merchandising, and service business

are more growing up rapidly. Each type of business has unique characteristics.

Manufacturing businesses change basic input into products that are sold to

individual customers, such as Thai Tuan Textile and Garment Corporation, Dong Tam

Joint Stock Corporation…Merchandising businesses also sell products to customers.

However, rather than making the products, they purchase them from other businesses

(such as manufacturers). In this sense, merchandisers bring products and customers

together, such as 3A Pharmaceutical Co., Ltd - Abbott Authorized Distributor, Thuy

Loc Co., Ltd - Shiseido Authorized Distributor in Viet Nam or Metro Cash & Carry…

Service businesses provide services rather than products to customers, such Equinox

Hair & Beauty, YKC Beauty Spa…

One of the key factors underlying the growth of the Vietnam economy is

the trend toward selling goods and services on credit. Because, in today’s global

marketplace, competitive pressure and industry practice mandate that products and

services be on a credit vs. cash-on-delivery basis. This practice often produces a

receivable asset is one of the largest tangible assets on a company’s balance sheet. A

review of the 2004 Fortune 500 certainly reveals this truth. Receivables ranked among

the top three tangible assets for 75% of the top 100 companies. Surprisingly,

management of this multi-million (or multi-billion) Vietnam Dong asset rarelyreceives much senior management attention, except when a serious problem develops.

The custodians of the receivables asset are similar to umpires of a football game; they

are not noticed unless they do a bad job.

As you see above, merchandising is the type that is less complicated than

manufacturing, but more complex than service. So we choose merchandising business

Page 1 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 2/54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 3/54

1.3. Objectives of the thesis:

After studying in real case, you may know how receivable management is

important by

• Identifying accounts receivable in merchandising business.

• Describing how accounts receivable are recognized, valued and

disposed in the accounts.

• Interpreting the statement presentation and analysis of receivable.

• Illustrating receivable asset management effectively.

• Optimizing receivables.

• Providing proven principles for achieving benefits such as increased

cash flow, higher margins, and a reduction in bad debt loss.

• Supporting technology.

1.4. Scope of the thesis:

1.4.1. By time:

AAA Pharma has expended their business more than ten years with many

changes in receivable management. Because of limit time, I just focus within two

years to analyze and improve it for current and coming year.

1.4.2. By space:

AAA Pharma has not only a head quarter at Ho Chi Minh City but also

many branches in all three areas in Vietnam: Ha Noi, Da Nang, Can Tho, Nha Trang,

Hai Phong, Dong Nai, Nghe An and a representative office in Hue. Because of limit

space, my major is receivable management at head quarter in Ho Chi Minh City.

1.4.3. By topic:

The focus is primarily on commercial receivables management (business

to business, and business to consumer) and fast-growing consumer product.

Page 3 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 4/54

CHAPTER 2

LITERATURE REVIEW

i. Identify account receivables in merchandising business:

2.1.1. Types of receivables:

The term “receivables” refers to amounts due from individuals and other

companies. They are claims that are expected to be collected in cash. Receivables are

frequently classified as (1) accounts, (2) notes, and (3) other.

Accounts receivable are amounts owned by customers on account. They

result from the sale of goods. These receivable generally are expected to be collected

within 30 to 60 days. They are the most significant type of claim held by a company.

Notes receivable are claims for which formal instruments of credit are

issued as proof the debt. A note receivable normally extends for time periods of 60-90

days or longer and requires the debtors to pay interest.

Notes and accounts receivable that result from sale transactions are often

called trade receivable.

Other receivables include nontrade receivables. Examples are interest

receivable, loans to company officers, advances to employees, and income taxes

fundable. These are unusual. Therefore they generally classified and reported as

separate items in the balance sheet.

2.1.2. Reasons to offer credit: (chấp nhận cho nợ)

Most of companies want to sell for cash at that time they provide goods because cash sales are normally rung up on a cash register (cashbox) and recorded in

the accounts. But competitive pressure in the world economy mandates that goods are

sold on credit as promotion, customer convenience. You may thinks this credit they

offer is to bring more benefits only for customers. That is not enough. The more

customers you have, the more profit you earn and the higher market share you get in

Page 4 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 5/54

competitive pressure. Credit had existed in business environment for long time ago;

therefore it is available to customers and become a criterion they make buy decision.

ii. Three primary accounting issues are associated with

accounts receivable:

2.2.1. Recognizing accounts receivable:

Every sales transaction should be supported by a business document that

provides written evidence of the sales. A sales invoice provides support for a credit

sale. Two entries are made for each sale.

The first entry records the sale:

• Accounts receivable is increased by a debit.

• Sale is increased by a credit.

The second entry records the cost of goods sold:

• Cost of goods sold is increased by a debit.

• Merchandise inventory is decreased by a credit.

2.2.2. Valuing accounts receivable: (đánh giá khoản phải

thu)

Once receivables are recorded in the accounts, the next question is: how

should receivables be reported in the financial statements? They are relatively liquid

assets, usually converting into cash within a period of 30 to 60 days. Therefore

accounts receivable from customers usually appear in the balance sheet as current

asset. But determining the amount to report is sometimes difficult because some

receivables will become uncollectible.

Reflecting Uncollectible Accounts in the Finance Statements

Each customer must satisfy the credit requirements of the seller before the

credit sale is approved. Inevitably, though, some accounts receivable become

uncollectible. For example, one of your customers may not be able to pay because of

a decline in sales due to a downtown in the economy. Similarly, individuals may be

laid off from their jobs or be faced with unexpected hospital bills. Credit losses are

recorded as debit to Bad Debts Expense (or Uncollectible Accounts Expense). Such

losses are considered a normal and necessary risk of doing business on a credit basis.

Page 5 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 6/54

Two methods are used in accounting for uncollectible accounts:

2.2.2.1. Direct write-off Method for Uncollectible Accounts:

(phương pháp xóa sổ nợ khó đòi)

When a particular account us determined to be uncollectible, the loss is

charge to Bad Debts Expense. The entry is:

• Bad Debts Expense is increased by a debit.

• Accounts receivable is decrease by a credit.

Under the direct write-off method, Bad Debts Expense will show only

actual losses from uncollectible. Accounts receivable will be reported at its gross

amount. Although this method is simple, its use can reduce the usefulness of both the

income statement and balance sheet. Moreover, Bad Debts Expense is often recorded

in a period different from the period in which the revenue was recorded. No attempt is

made to match bad debt expense to sale revenues in the income statement. Nor does

the direct write-off method show accounts receivable in the balance sheet at the

amount actually expected to be receivable. Consequently, unless bad debts losses are

insignificant, the direct write-off method is not acceptable for financial reporting

purposes.

2.2.2.2. Allowance method for Uncollectible Accounts:

(Phương pháp dự phòng nợ khó đòi)

The allowance method of accounting for bad debts involves estimating

uncollectible accounts at the end of each period. This provides better matching on the

income statement and ensures that receivables are stated at their cash (net) realizable

value on the balance sheet. Cash (net) realizable value is the net amount expected to

be receivable in cash. It excludes amounts that the company estimates it will not

collect. Receivables are therefore reduced by estimated uncollectible receivable in the

balance sheet through use of this method.

The allowance method is required for financial reporting purposes when

bad debts are material in amount. It has three essential features:

Page 6 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 7/54

• Uncollectible accounts receivables are estimated. This estimate is

treated as an expense and is matched against sales in the same accounting period in

which the sales occurred.

• Estimated uncollectibles are debit Bad Debts expense and are

credited to Allowance for Doubtful Account (a contra asset account) through an

adjusting entry at the end of each period.

• When a specific account is written off, actual uncollectible are

debited to Allowance for Doubtful Accounts and credited to Accounts Receivable.

2.2.2.2.1. Recording estimated uncollectible:

To illustrate the allowance method, assume that AAA Pharma has credit

sales of 120 million VND in 2002. Of this amount, 20 millions VND remains

uncollected at Dec 31. The credit manager estimates that 12 million VND of these

sales will be uncollected. The adjusting entry to record the estimates uncollectible is:

• Bad debts expense is increased by 12 millions debits.

• Allowance for Doubtful Accounts is increased by 12 millions

credits.

Bad debts expense is reported in the income statement as an operating

expense. Thus, the estimated uncollectible are matched with sales in 2002. The

expense is recorded in the same year the sales are made.

Allowance for Doubtful Accounts shows the estimated amount of claims

on customers that are expected to become uncollectible in the future. This contra

account is used instead of direct credit to Account Receivable because we do not

know which customers will not pay. The credit balance in the allowance account will

absorb the specific write-off when they occur. It is deducted from accounts receivable

in the current assets section of the balance sheet. Allowance for Doubtful is closed at

the end of the fiscal year.

2.2.2.2.2. Recording the write-off an uncollectible account:

Companies use various methods of collecting past-due accounts, such as

letters, calls, and legal action. When all means of colleting a past-due account have

been exhausted and collection appears impossible, the account should be written off.

Page 7 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 8/54

To illustrate a receivable write-off, assume that CFO of AAA Pharma

authorizes a write-off of the 5 millions VND balance owed by Tien Viet Company on

March 1, 2003. The entry to record the write-off of is

• Allowance for Doubtful Account is decreased by 5 million debits.

• Account receivable is decrease by 5 million credits.

Bad debts expense is not increased when the write-off occurs. Under

allowance method, every bad debt write-off is debited to the allowance account rather

than to Bad debts expense. A debit to Bad debts expense would be incorrect because

the expense has already been recognized when the adjusting entry was made for

estimated bad debts. Instead, the entry to record the write-off of an uncollectible

account reduces both Account Receivable and the Allowance for Doubtful Accounts.

A write-off affects only balance sheet accounts. The write-off the account

reduces both Accounts Receivable and Allowance for Doubtful Accounts. Cash

realizable value in the balance sheet, therefore, remains the same.

2.2.2.2.3. Recovery of an uncollectible account:

Occasionally, a company collects from a customer after the account has

been written off. Two entries are required to record the recovery of a bad debt: (1) the

entry made in writing off the account is reversed to reinstate the customer’s account.

(2) The collection is journalized in the usual manner.

Recovery of a bad debt, like the write-off of a bad debt, affects only

balance sheet accounts. The net effect of the two entries is debit to Cash and a credit

to Allowance for Doubtful. Receivable is debited and the Allowance for Doubtful is

credited in entry (1) for two reasons: First, the company made an error in judgment

when it wrote off the account receivable. Second, after customers did pay, Account

receivable in the general ledger and customer’s accounting the subsidiary ledger

should show the collection for possible future credit purposes.

2.2.2.2.4. Bases used for allowance method:

Company must estimate the amount of the expected uncollectible if they

use the allowance method. Two bases are used to determine this amount: (1)

percentage of sales, and (2) percentage of receivables. Both bases are generally

Page 8 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 9/54

accepted. The choice is a management decision. It depends on the relative emphasis

that management wishes to give to expenses and revenues on the one hand or to cash

realizable value of the accounts receivable on the other. The choice is whether to

emphasize income statement or balance sheet relationships.

Figure 1: Percentage of sales

In the percentage of sales basis, manager estimates what percentage of

credit sales will be uncollectible. This percentage is based on past experience and

anticipated credit policy. The percentage is applied to either total credit sales or net

credit sales of the current year.

For example, AAA Pharma estimated 1 percentage of net credit sales will

become uncollectible. If net credit sales for 2002 are 800 million, the estimated bad

debts expense is 8 million (1% * 800 million).

This basis of estimating uncollectible emphasizes the matching of

expenses with revenues. As a result, Bad Debts Expense will show a direct percentage

relationship to the sales base on which it is computed. When the adjusting entry is

made, the existing balance in Allowance for Doubtful Account is disregarded. The

adjusted balance in this account should be a reasonable approximation of the

uncollectible receivable. If actual write-off differs significantly from the amount

estimated, the percentage for future years should be modified.

Page 9 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 10/54

Figure 2: Percentage of receivables

Under the percentage of receivable basis, manager estimates what

percentage of receivable will result in losses from uncollectible accounts. An aging

schedule is prepared, in which customer balances are classified by the length of time

they have been unpaid. Because of its emphasis on time, the analysis is often called

aging the account receivable.

After the accounts are aged, the expected bad debt losses are determined.

This is done by applying percentages based on past experience to the totals in each

category. The longer a receivable is past due, the less likely it is to be collected. So,

the estimated percentage of uncollectible debts increases as the number of days past

due increase. An aging schedule for AAA Pharma is shown:

Page 10 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 11/54

Table 1: Aging schedule

Total estimated bad debts for AAA Pharma (2,228 millions) represent the

amount of existing customer claims expected to become uncollectible in the future.

This amount represents the required balance in Allowance for Doubtful accounts at

the balance sheet date. The amount of the bad debt adjusting entry is the difference

between the required balance and the existing balance in the allowance account. If the

trial balance shows Allowances for Doubtful account with a credit balance of 528

million, an adjusting entry for 1,700 million (2,228-528) is necessary.

Occasionally the allowance account will have a debit balance prior to

adjustment. This occurs when write-off during the year have exceeded previous

provision for bad debts. In such a case the debit balance is added to the required

balance when the adjusting entry made. Thus, if there had been a 500 million debit

balance in the allowance account before adjustment, the adjusting entry would have

been for 2,728 million (2,228+500) to arrive at a credit balance 2,228 millions.

The percentage of receivable method will normally result in the better

approximation of cash realizable value. But it will not result in the better matching of

expenses with revenues if some customers’ accounts are more than one year past due.

In such a case, bad debts expense for the current period would include amounts

related to the sales of a prior year.

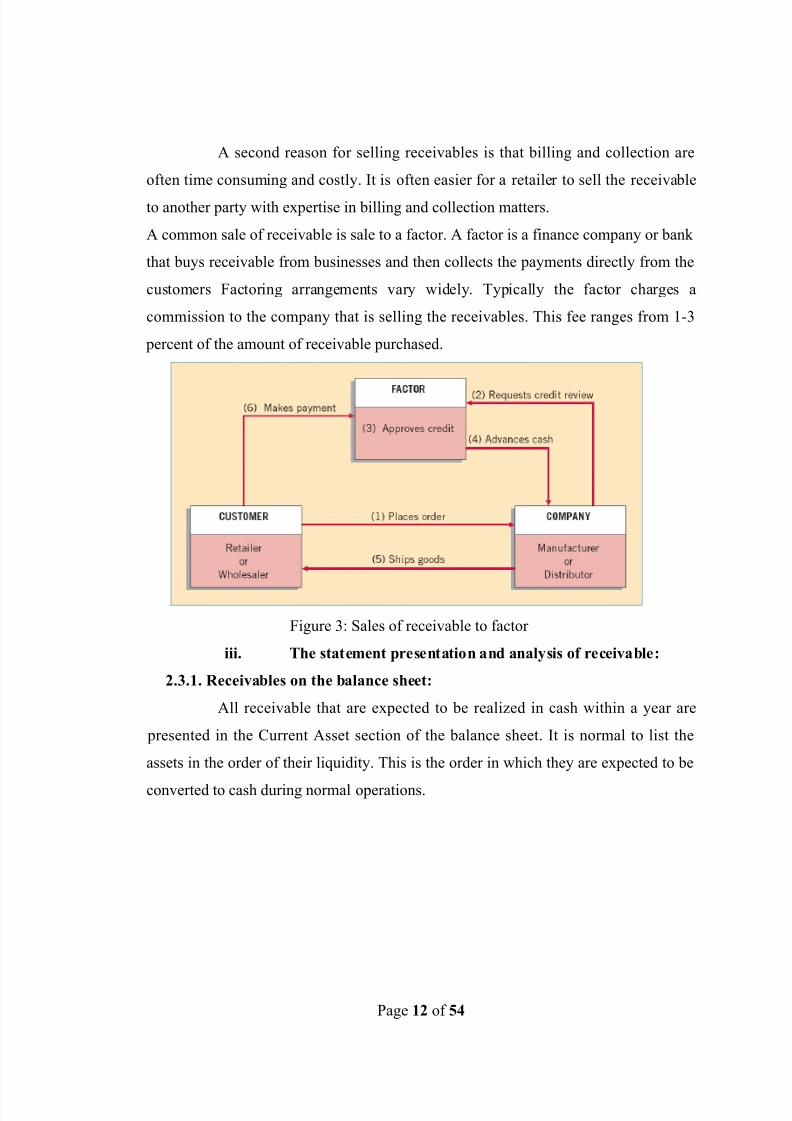

2.2.3. Disposing of Account Receivable:

In the normal course of events, accounts receivable are collected in cash

and removes from the books. However, as credit sales and receivables have grown in

significance, their “normal course of events” has changed. Companies now frequently

sell their receivables to another company for cash, thereby shortening the cash-to-cashoperating cycle.

Receivables are sold for two reasons. First, receivable may be sold because

they may be the only reasonable source of cash. When money is tight, companies may

not be able to borrow money in the usual credit markets. Or, if money is available, the

cost of borrow may be prohibitive.

Page 11 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 12/54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 13/54

Table 2: Balance sheet (partial)

2.3.2. Evaluating liquidity of receivable:Business that grant long credit terms tend to have relatively greater

amounts tied up in accounts receivable than those granting short credit terms. In either

case, it is desirable to collect receivables as promptly as possible. The cash collected

from receivable improves solvency and lessens the risk of loss from uncollectible

accounts. Two financial measures that are especially useful in evaluating the

efficiency in collecting receivables are (1) the receivable turnover ratio, (2) the

number of days’ sales in receivable or average collection period.

The receivable turnover ratio measures how frequently during the year

the account receivable are being converted to cash. For example, with credit terms of

2/10, n/30 days, account receivable should turn over less than 36 times per year.

Receivable turnover ratio is computed as follow:

The average net receivable can be determined by using monthly date or by

simply adding the beginning and ending account receivable balances and dividing by

two.

Page 13 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 14/54

The number of days’ sales in receivable or average collection period is an

estimate of the length of time the account receivable have been outstanding. With

credit term of 2/10, n/30 days, the number of days’ sales in receivable should be more

than 10 days. The number days’ sale in receivable is computed as follows:

An average daily sale is determined by dividing net sales by 365 days.

For the measures to be meaningful, a company should compare its current

measures with those from prior periods and with industry figures. An improvement in

the efficiency in collecting accounts receivable is indicated when the receivable

turnover ratio increases and the numbers of days’ sales in receivable decreases.

Table 3: Evaluate the liquidity of receivables

Page 14 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 15/54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 16/54

Quotation is the process of extending a formal offer for a product or

service to a prospective or existing customer. A clear, complete quotation lays the

foundation for excellent fulfillment of a customer order and accurate invoicing. The

two key attributes of a quotation that promote excellent receivables results are:

• Feasibility/deliverability of offering.

• Clear commercial terms and conditions agreed by both parties. The

six elements of a quotation that affect receivables results are:

1. The unit and total price (clearly stated including all

discounts)

2. Applicable sales or use tax

3. Freight/delivery (actual versus allowance, who pays it)

4. Payment terms (when is payment due?)

5. The timing of issuing the invoice (upon shipment, at the

start or completion of a project, on reaching a milestone)

6. Description of product or service offered (product

number, layman’s description, proper or trademarked product

name).

Page 16 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 17/54

2.4.1.2. Contract administration:

From a receivables management perspective, contract administration is all

about charging the correct price on the invoice. Price discrepancies are the

leading cause of disputed invoices, which result in delayed payments, short payments,

and substantial rework.

Contracts are used for larger customers who will receive frequent

shipments of products and/or delivery of services over a period of time and are

looking to ensure supply and receive the lowest price. Infrequent customers are

usually served via individual orders covered by their written, electronic, or verbal

purchase order. Contracts govern the commercial terms and conditions of the orders

(or releases against the contract) that are received during the time period in which the

contract is in effect. As we said in the “Quotation” section, it is vital that the contract

clearly define the agreed commercial terms and conditions.

In addition, the time period covered by the contract must be specified.

2.4.1.3. Pricing administration:

Page 17 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 18/54

Price discrepancies are the leading cause of invoice disputes. This is not

surprising when you think of all the pricing incentives and promotions offered to give

a company a competitive advantage and/or to affect customer buying behavior.

Examples of pricing mechanisms designed to alter buying behavior are:

• Shifting orders from a busy season of peak demand to a slow season

• Increasing individual order or shipment size

• Increasing total volume purchased within a specified time period and so

on.

Many of these pricing incentives overlap and can be quite complex,

causing confusion among the supplier’s pricing and billing staff and the customer’s

accounts payables and procurement staff. System tools may not be able to

accommodate complicated pricing schemes and accurately price invoices.

Unfortunately, the results can be very damaging.

2.4.1.4. Credit controls:

The objective of credit controls is to manage the risk inherent in the

extension of credit to promote sales. This risk is known as credit risk, and is the same

risk incurred by lenders of money, such as banks. A company that sells only on cash-

in-advance or cash-on-delivery terms and requires a secure form of payment has no

credit risk. However, global marketplace runs on credit. Goods are routinely delivered

Page 18 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 19/54

with the expectation that payment will be made according to the agreed payment

terms. Credit risk has two dimensions: The first is the risk that payment will never be

made. The second risk is that payment will be made late.

Credit Limits: Credit limits quantify the VND amount of risk a

company is willing to bear with an individual customer. It is analogous to the size of a

loan or line of credit a bank would extend to one of its customers. In principle, it is a

“line in the sand” beyond which the risk is intolerable.

• Establishing Credit Limits for New Customers: A credit

investigation is necessary to establish a credit limit for a new customer.

o Start with a credit application from the customer to your

company requesting a credit account.

o Investigate the applicant’s credit, secure payment, default,

litigation reliable payment history information.

o If you are unable to establish a credit limit with the above

sources of information, proceed to check the trade and bank references.

o Evaluate the information and assign a credit limit and a date the

limit expires or is to be reevaluated.

- Financial strength (financial ratio analysis).

- Exposure calculated by the sum of estimated

monthly sales and customized inventory to be held for the customer, multiplied by the

payment terms. The exposure to any related parties must be added to aggregate total

exposure to an entity.

- Payment history with other suppliers as reported

by credit reporting service.

- Profitability of sales to customer .

- Building a Specific Reserve for High-Risk

Customers

• Building a Specific Reserve for High-Risk Customers:

Page 19 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 20/54

If management still wants to sell on credit beyond the limits the credit

investigation indicates is prudent, an innovative technique is to provision the bad debt

reserve for a specific customer at higher rates until the reserve is adequate to cover the

risk of the exposure of that customer. Thus, the sale is made, but the added risk is

recognized, and over time, the reserve is built up to cover any bad debt loss incurred

from the customer(s). For example, management wants to sell VND 100,000 millions

per month to a very high-risk customer on net 30-day payment terms. A credit

investigation judges a VND 30,000 millions credit limit to be prudent. To enable this

trading and cover the risk, all sales to this individual customer would be accompanied

by an additional provision to the bad debt reserve of 25% of sales. Over a period of

four months, assuming no bad debt loss and the customer paying promptly, thereby

maintaining its receivable at VND 100,000 millions, a specific reserve would exist

sufficient to totally cover the VND 100,000 millions exposure to bad debt loss. At that

point, the specific provisioning would be tailored to maintain the reserve at the same

level as the receivable. The company will have gained the profit from the additional

sales yet still have recognized the risk of a potential bad debt loss.

Credit management forwards these to the designated managers for

approval with a summary of the financial impact of the nonstandard terms expressed

in:

• The cost of financing the receivables for the extended period of time

• The incremental exposure to bad debt loss and the additional expense for

the provision for bad debt loss

• The cost of prompt payment discounts

• The profitability of the sales to the customer

• Updating Existing Credit Limits:

In many respects, updating a credit limit involves repeating the steps taken

in establishing the initial credit limit. However, there are two significant differences:

(1)You have the customer’s historical payment performance for your

invoices. This may be the most reliable and valuable data you have, particularly the

trend in that payment performance.

Page 20 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 21/54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 22/54

• Fewer concessions of disputed items.

• Enhanced customer service and satisfaction

2.4.2. Collection process:

Management of the receivables asset begins when all of the antecedent

functions are completed and a receivable is posted to the detailed accounts receivable

ledger (a comprehensive list of all amounts owed the company). The receivables

begin aging immediately, increasing the cost of financing them and increasing the risk

of nonpayment.

Management of this asset (which is one of the largest assets of the

company) involves safeguarding the asset and accelerating cash inflow (increasing

asset turnover). If you view this asset as a vault of cash, think of the precautions a

bank takes to protect its cash reserves. However, receivables are much more fluid and

an integral part of doing business, so the safeguarding and acceleration of turnover

must be accomplished:

• At low cost

• Without strangling sales volume

• Without alienating customers and colleagues.

Collection Timeline:

Page 22 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 23/54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 24/54

• It is customer service–oriented, to promptly identify and resolve any

discrepancies with the order fulfillment or invoice. If no problems exist, inquire if the

invoice is scheduled to be paid by the due date.

• It occurs prior to the due date, so resolution can be effected to ensure that

payment can be received by the due date. It also educates the customer that you are

serious about enforcing your payment terms.

• It is still a collection call. Ask for the payment on the due date.

Proactive contact should be focused on large balance accounts, as it is

more time consuming than a “straight” collection call on past due invoices.

Customer Contact Methods:

The most effective method of customer contact is made via telephone,

which can elicit a timely or, it is hoped, immediate response. Once you have the

proper person on the phone, you are well positioned to secure a commitment to pay or

determine the reason for nonpayment.

E-mail is a very effective method of communicating with accounts

payable departments. Many people respond more promptly to e-mails than voice

mails, and the e-mail message is much better at conveying invoice numbers, amounts

due, and so on.

Collection letters have limited effectiveness. They are best used with low-

priority, small-balance accounts that probably will not receive a call or personalized

e-mail. For such accounts, a collection letter is better than no contact at all.

Negotiation Skills and Empowerment:

In practices, collection process includes empowering collectors to

negotiate and to concede charge during negotiation. Limits must be placed on theamount that can be conceded. Concessions can also be limited to late payment fees

and unearned prompt payment discounts. However, to achieve best results most

efficiently , a collector must be empowered to write off certain amounts. This

empowers collectors with the customer and eliminates the time required to secure

approvals.

2.4.3. Evaluating the liquidity of receivables:

Page 24 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 25/54

As I mention in part 2.3.2, we have to evaluate the efficiency in collecting

receivables by (1) the receivable turnover ratio, (2) the number of days’ sales in

receivable or average collection period.

After evaluating liquidity of receivable, we get two points: (1) how much

money we are able to collect at due day, (2) how much money we have to collect for

past due invoices, then making critical collection process.

2.4.4. Financing of the receivable asset:

There are various techniques for using the receivables asset to obtain

accelerated funding instead of waiting for customers to pay the invoices. All of these

techniques:

• Involve an incremental financing or borrowing cost.

• Impose duties and restrictions on the borrower.

• Are structured differently.

Sales of receivables:

This is the simplest form of financing, where a company sells its

receivables asset to a financing entity. The financing entity takes title to the asset and

pays a lump sum in return. Of course, the seller does not receive 100 cents for every

dollar of receivables sold. The purchase price is reduced for:

• The interest value of the money advanced by the buyer. The rate is based

on prevailing interest rates, the length of time the lender expects to wait before

receiving payment for all invoices purchased, and the risk premium the lender

perceives for the risk of nonpayment of the purchased receivables.

• Expected dilution (deductions, discounts, etc.) incurred in collecting the

receivables.• The cost to the buyer of collecting the receivables. Since the receivables

have been sold to the buyer, the buyer will have to collect them. Usually, the seller

mails a letter to customers informing them of the assignment of the receivables to the

buyer and how to pay (payee name, address).

• Aprofit element.

In addition, the buyer may not purchase all of the receivables offered.

Page 25 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 26/54

The buyer may eliminate receivables owed by high-risk customers, either individual

customers or a class of customers, such as foreign accounts.

The advantage to the seller is that it receives the funds in a matter of days

instead of waiting 30 or more days. However, this can be an expensive way to obtain

financing.

Factoring receivable:

Factoring of receivables is very similar to the sale technique described

above. The major difference is that factoring is a continuous, ongoing purchase of

receivables, compared to a transaction for a finite portfolio of receivables.

The factor serves as the seller’s receivables management function,

performing credit, collection, and payment processing functions. However, the factor

will purchase receivables from only customers whose creditworthiness has been

vetted and approved. If the seller sells to customers not accepted to the factor, the

seller has to perform the receivables management function itself.

Collateralizing Receivable:

Collateralizing receivables involves pledging the asset as collateral for a

loan. The simplest form is pledging them as a condition for obtaining a term loan.

The company continues to administer them as always, except there will be covenants

specifying standards of aging, concentration, and so on to be met, and reporting

requirements from the lender.

Often the lender will exclude receivables over 90 days past due and

expected dilution from the collateral valuation and reduce the amount financed.

Another form of collateralization is securitization, where the receivables

asset is used to secure commercial paper or other financing instrument issued to third- party investors. Securitization is an ongoing financing instrument with acceptable

receivables purchased by the financing entity on a continuous basis. The seller

manages the asset as always, but with additional procedural and reporting duties and

covenants.

The cost of all of these financing techniques is inversely related to the

quality of the receivables asset. The discount or interest rate used will be based on the

Page 26 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 27/54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 28/54

world new ideas and products that have transformed human health and well-being.

Every invention, every product, every breakthrough has been powered by generations

of employees who are inspired to make a difference. They credit their strength and

endurance to a consistent approach to managing their business, and to the character of

their people. They are guided in everything they do by Their Credo, a management

document authored more than 60 years ago by Robert Wood Johnson, former

chairman from 1932 to 1963, and by four strategic principles. (See in Appendix)

The corporation's headquarters is located in New Jersey, United States.

The corporation includes some 250 subsidiary companies with operations in over 57

countries. Its products are sold in over 175 countries. Johnson & Johnson's brands

include numerous household names of medications and first aid supplies. Among its

well-known consumer products are the Band-Aid Brand lines of bandages, Tylenol

medications, Johnson's baby products, Neutrogena skin and beauty products, Clean &

Clear facial wash and Acuvue contact lenses.

Johnson & Johnson's commitment to innovative health care products has

resulted in consistent financial performance. It has 75 consecutive years of sales

increases and 45 consecutive years of dividend increases. Its common stock is a

component of the Dow Jones Industrial Average and the company is listed among the

Fortune 500.

• Company milestones:

AAA Pharma Co., Ltd was established under Business License No.

041476 dated June 5th 1997 by Department of Planning and Investment of Ho Chi

Minh City and Establishment Permit No. 1155/ GP-UB dated May 26 th 1997 by the

People’s Committee of Ho Chi Minh City, which the original trading name was AAA

Trading Company limited. AAA Trading Co., Ltd started operations on June 1997,

which had a legal entity, private seal and independent bank account.

The business scope which Board of Directors stated at the beginning was

to import and to distribute Health Care products of Johnson & Johnson in Vietnam,

but the company had to sell other products in order to avoid profit loss for beginning

Page 28 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 29/54

period. Thus they traded in handicraft, chemical cosmetics, textile, clothing, office

stationery industry and trading services at first merchandising activities.

Once the company recognized that revenues from these kinds of products

would decrease in the near future because of strong competition of substitutes,

moreover; the operation situation was strong enough to distribute Johnson & Johnson

Health Care products as they stated at the beginning. Then the company changed

gradually from unstable sources of these other products to target Johnson & Johnson

products. Based on Vietnam law, distributors of medical products, like Johnson &

Johnson health care product, have to pharmaceutical companies. So from July 2004,

AAA trading company limited changed their name to AAA Pharmaceutical Company

limited with their new logo:

Tax code: 030.1000.691

Email: [email protected]

AAA Pharma was founded with VND 1.2 Billion charter capital in 1997.

As Dec 2005, AAA charter capital mounted to VND 15 Billion.

AAA Pharma Headquarter in Ho Chi Minh City plays the key function in

operating all the main activities. And this is also the center of training and upgrading

the staff quality for all of our nationwide branches. They have the most extensive

infrastructure network in Vietnam with branches in Hanoi, Da Nang, Can Tho, Nha

Trang, Hai Phong, Dong Nai, Nghe An and representative office in Hue. In response

Page 29 of 54

DISTRIBUTION NETWORK

1998 : Ha Noi Office

2006 : Da Nang Office

2004 : Can Tho Office

2006 : Hai Phong Office

2006 : Dong Nai Office

1997 : HCM Headquarter

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 30/54

to their rapid growth, an expansion plan for the next coming years is to open more

branches in some key provinces such as Thanh Hoa, Kon Tum, Vung Tau, etc…

Figure 6: Distribution network

• Company organization:

a. Company structure:

i. Board of directors:

Head of the company’s managers is the Board of Directors. Chairman of

Board of Directors is an operation manager, representative legal entity. He takes all

responsibilities for results of merchandising business and fulfils obligations to

Vietnam’s government. There are two vice directors and an assistant in operating the

business. They can be as representative chairman in solving some problems, making

contracts under their authorities.

ii. Accounting-Finance department: (see figure xx in Appendix)

The accounting department includes ERP, cashier and many accountants.

Head is chief accountant that take responsibilities in

- Recording all transactions incurred and doing financial reports about

business performance and business situation.

- Balancing capital sources, monitoring and allocating profit for the

business.

- Using both financial accounting and estimated data to aid management in

running day-to-day operations and in planning future operations.

- Gathering and reporting all information that is relevant and timely to the

decision-making needs of management, and other involved appropriate authorities.

- Implementing financial banking system, monitoring tax payment.

- Supporting to make plan for importing goods, contracting with banking

and preparing all relevant import documents. Monitoring imported tax, valued added

tax to Vietnam’s tax authorities.

- Receiving and storing all documents related to accounting activities.

iii. Admin department : (see figure xx in Appendix)

- Organize and implement work related to administration.

Page 30 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 31/54

- Implement and solve administrative formalities (internal and external).

- Solve problems related to administration happened. Ensure admin

activities are to support other departments.

- Examine all business contracts, ordering and buying POP used in

operation.

- Monitor documents in and out, materials, and files; deliver them to right

place. Take responsibility in maintaining and storing documents, files is to ensure that

all information is safe and security.

- Organize to monitor and use all tangible assets, equipments in company

such as car, truck, official equipments, and communication equipments…

- Create comfortable working environment followed by board of directors.

- Gather and report organization and administrative things to board of

directors.

iv. Marketing department:

- Take all responsibilities in building and improving company’s image.

- Find out alternative solutions to support sales department to increase sale

volume.

- Propose and implement promotional programs to end user and

wholesalers.

• DGT (Demand Generation team):

- They are sales promoters. They market J&J products in

hospitals, pharmacies …in order to create the demand. In addition, they also report

their activities and results monthly to their CD Sup.

- They frequently make a proposal, plan to sales departments.

v. Sales department:

3.3.1.5.1. Customer Develop Director (CD Director):

Head of sales department is CD director. His main role is to monitor whole

sales system in order to fulfill sales targets by planning, organizing, controlling and

evaluating them.

- Together with board of directors, they make sales strategies.

Page 31 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 32/54

- Specific sales plans and tactics to implement their strategies.

- Set up sales target; analyze and forecast to order and monitor credit

customers.

- Deploy sales plan to CD Sup.

3.3.1.5.2. Customer Develop Supervisor (CD Sup):

- Receive sales plan, target form CD Director, then set up and deploy sales

targets for CD Rep in their areas.

- Make a plan to control and assess effectiveness of CD Rep.

- Motivate juniors and monitor credit customers.

- Juniors of CD Sup are CD Rep, CD Rep Supermarket, and DGT.

3.3.1.5.3. Customer Develop Representative (CD Rep):

- CD Rep is middle point between CD Sup and agency.

- Each CD Rep manages each agency and takes responsibility in

monitoring and assessing taskforce to implement sales target that CD Sup requires.

3.3.1.5.4. Customer Develop Representative

supermarket (CD Rep Supermarket):

- CD Rep is middle point between CD Rep Supermarket and Supermarket.

- Responsibilities of CD Rep Supermarket are the same to one of CD Rep.

- Also manage promoters at supermarket.

3.3.1.5.5. Promoter:

- They are youngest and account for most of staffs in the company (40%).

They are students that are studying and working as part-time job. They have good

communication skill and well-informed about company’s products thorough training

programs.- Support promotional program from J&J to taskforce and DGT.

- Weekly reports about sale volume of supermarkets, shops and outlets that

they manage to their CD Rep.

3.3.1.5.6. Taskforce:

- They play role in selling, marketing, distributing from the company to

wholesalers and retailers. And they have to seek new customers.

Page 32 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 33/54

- Direct contact to customers, satisfies customers’ demand, and explains all

information that customers need.

- Periodic reports about sale operation to their CD Rep.

- Support promotional program from J&J.

vi. Inventory:

This department consists of chief inventory, warehouse-keeper, labors in

sticking line, inbound, outbound and delivery team…They take responsibilities for

- Managing all activities in inventory followed specific functions and

missions delegated to get best results.

- Supervising imported products from ports and air to inventory.

Receiving, storing and delivering goods, arranging workforce in inventory, ensuring

goods in and out to follow business’s plan.

- Arranging and storing goods is followed right standard of product.

- Following to deliver goods to branches.

- Be responsible for the quantity and quality of goods in warehouse.

Conserve and arrange goods to ensure that they are easy to find, look, take and check.

- Implementing all the labor regulations and internal rules in the warehouse.

- Building up and continuously improving the warehouse’s operations in

order to get more professional and effective.

- Coordinate to other departments to insure an effective working process.

b. Company workforce:

At AAA Pharma, they consider human resources as their utmost important

key for success. AAA Pharma invests in the development of workforce through a

combination of classroom learning and online training that offers high quality coursecurriculum that facilitates continuous learning. These training resources for our

valued employees are designed to enhance the mastery of vital competencies for

career development.

There were a few of staffs that operated separately at first, now AAA

Pharma is proud of younger staffs that are active, sincerity, honest…. There are 700

staffs (full time-520, part time-180, 70% female)

Page 33 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 34/54

All staffs recruited have to follow recruitment process, and get consistent

training, advanced training and updated learning to adapt environment working,

company’s culture.

Special training program: career day and management trainee.

- In order to build up workforce, AAA Pharma organizes often career day

in Ho Chi Minh City and these provinces that company has its branch. This is not

only an opportunity that students have a job to get income but also opportunity that

orient students’ career and work in real through part time job.

- In response to their rapid growth, AAA Pharma set up Management

trainee program for supporting the middle managers. The first program is done in Ho

Chi Minh City with the first upgraded students at International University. This takes

one year to train, then based on their results and abilities; they are allocated in specific

department.

• Merchandizing operation:

1. Products:

AAA Pharmaceutical Co., Ltd is the authorized distributor of health care

J&J products in Vietnam. They divide products into three groups:

- J&J group: including products used in baby care such as body wash,

shampoo contained anti-infective ingredients that not make allergic to baby’s body,

skin and eyes; powder classic, powder prickly heat, powder double protect blossom

and Cologne blossom, …these are main goods in AAA Pharma, they are accounted

for 65% of sales volume.

- Beauty group: including products used in skin care, oral care, such as

CLEAN & CLEAR Facial wash, CLEAN & CLEAR Acne Clearing Cleanser,

CLEAN & CLEAR Balancing Moisturizer, CLEAN & CLEAR Deep Action

Cleanser…These are potential goods in AAA Pharma, but they are new kinds in

Vietnam, so they just are accounted for 18% of sale volume.

- Consumer Health Care group: including products used in women’s

health care fields such as tampon, feminine hygiene solution under Carefree and

Page 34 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 35/54

Modess. Like Beauty group, these are potential goods, but they just are accounted for

17% of sale volume because of entrance in Vietnam.

2. Distribution network:

AAA Pharma distributes goods thorough 2 channels:

- General Trade channel: is a channel that AAA Pharma uses to

distribute their goods to whole national retailer: shops, outlets, retailers, pharmacy….

This is main channel, and accounted for 76% whole distributed goods. Because 70-

75% Vietnamese lives in countryside and they are not familiar with shopping in

supermarket. So AAA Pharma considers General Trade as main channel for a long

time.

- Modern Trade channel: is a channel that AAA Pharma uses to

distribute their goods to whole national supermarkets and bookshops such as Metro,

Big C, Co-op Mark, Maximax, Citimax, Vinatex…This is a potential channel because

sale volume of each supermarket is greater than one of retailer and always stable.

Now, this channel is accounted for 24% whole distributed goods and so increase more

in large city Nha Trang, Ho Chi Minh, Ha Noi, Hai Phong, Can Tho, Da Nang.

• Orientations from now to 2010:

3.5.1. Infrastructures:

Company’s development plan from today until 2010:

- Focus on invest in infrastructure of office and storage at Dong Nai

branch. .This will be main office to develop market of company in future.

- Implement and finish project that move main office of the company to

Cat Lai – Binh Duong (5ha) in 2015.On the other hand, office at HCM city will

become branch at HCM cit

- Improve continuously office and warehouse at HCM city to meet current

development demand of the company.

3.5.2. Developing Strategies:

Human resource: Board of Director always improves effective in human

resource management. It is core element in every plan, restructure and operation of

Page 35 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 36/54

company. Developing strongly human resource program is to bring high efficient.

Invest much in training specialize knowledge and integrity for employees.

In 2008, the company is implementing and applies Quality Control

Management ISO 9001:2000.

The objectives that board of Directors plan in applying and implementing

International Quality Control Management:

Figure 7: Company’s Vision

3.5.3. Merchandizing activities:

Products:

- The company‘s objective is that focus on traditional product J&J

(account for 65%), on the other hand, develop products in Beauty and CHC

- In 2008, the company will distribute one more product – Listerine. This

is a familiar product with consumer that had market and market shares. So, the

Company believes that this product will contribute in development of the company.

Distribution channel:

- In response to our rapid growth, an expansion plan for the next coming

years is to open more branches in some key provinces such as Thanh Hoa, Kon Tum,

Vung Tau, ect …

- The objective is that hold market of GT channel because this is

competitive advantage of AAA Pharma compare with competitors about: physical

Page 36 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 37/54

system, manpower and relations. Besides, the company focus on develop of MT

channel (this channel have stable revenue and development ability)

- Today until 2010, the company will build 1 new distribution channel, this

is distribution channel that distribute all pharmaceutical products – OTC channel.

Physical system and human resource that serve for this channel are being prepared.

CHAPTER 4

EMPIRICAL STUDY

The operating cycle of AAA Pharma: consists of the following basic

transactions: (1) purchases of merchandise, (2) sales of merchandise, often on account

(3) collection of the account receivable from customers. As the word cycle suggests,

this sequence of transactions repeats continuously. Some of the cash collected from

the customers is used to purchase more merchandise, and the cycle begins new. This

continuous sequence of merchandising transactions is illustrated below:

a. Methodology:

By recognizing the importance of accounts receivable management, I want

to analyze and improve accounts receivable management in specific case, AAA

Pharma Co., Ltd.

Page 37 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 38/54

Firstly, I analyze receivable policy for each type of customers in

distribution network.

Secondly, I estimate how these receivable policies affect on cash flow by:

• Aging report.

• Receivable turnover ratio.

Thirdly, I evaluate each receivable policy by:

• How are order taken?

• Credit processing.

• Credit decision.

• Collection efforts

After having the view in general, I make an interview with:

• Sales Director.

• Account receivable manager in ERP and accounting department.

• CD rep.

• Chief financial officer.

b. EMPIRICAL STUDYAs I mention above, AAA Pharma distributes goods thorough 2 channels:

- General Trade channel : is a channel that AAA Pharma uses to distribute

their goods to whole national retailer: shops, outlets, retailers, pharmacy…. This is

main channel, and accounted for 76% whole distributed goods.

- Modern Trade channel : is a channel that AAA Pharma uses to distribute

their goods to whole national supermarkets and bookshops such as Metro, Big C, Co-

op Mark, Maximax, Citimax, Vinatex… Now, this channel is accounted for 24%

whole distributed goods.

4.2.1. Receivable policy in AAA Pharma:

In Modern Trade channel: including Supermarket such as Coop, Big C,

Fivimart, Van Lang, Maxi, Vinatex, Binh Dan… and Hypermarket such as Metro.

This is a potential channel because sale volume of each supermarket is greater than

one of retailer and always stable. So they have to get the contract signed, they give

Page 38 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 39/54

more benefits or accept some of requirements in contract. For example, advertising

support, incentive rebate, additional bonus, opening support, renovation support,

damaged goods allowance, barcode charge, transportation and installation support,

and quality assurance support.

Hypermarket Supermarket

Credit line No limit No limit

Discount on 3% pretax price on 4% pretax price

Payment term 45 days from invoice date 15 days from invoice date

Payment method bank transfer bank transfer

On-time payment incentive 3% on invoice paid by 45

days

2% on invoice paid by 15

days

3% on invoice paid by 7days

4% on invoice paid on

delivery

Overdue payment penalty 0.75%/month on overdue

invoice value if overdue

exceeds 45 days from

invoice date.

0.75%/month on overdue

invoice value if overdue

exceeds 45 days from

invoice date.

Table 4: Receivable policy in Modern Trade channel

In General Trade channel: because of focus of Trade marketing, they

divide GT channel into 2 types of trade. (See figure xx in Appendix)

Firstly, Trade Systems are Distribution Accounts that focus on Revenue

base. It is like AAA Pharma but at smaller size. In Ho Chi Minh network, for

example, they divide Sales Organization into many branches based on administrative

division, which means Districts. In every district, they choose one large Distribution

Accounts to manage whole this area.

Secondly, Trade Sales are DNAs (Developed new accounts) that focus on purpose base. It is so flexible to develop new accounts and enlarge their size, volume

for entering trade systems; or to cover the market for higher market share. Trade Sales

is including direct sales and retailers.

Total 6 Cities - Val% - Baby Segment DEC05 DEC06 DEC07 MAR08

Johnson's Baby 66,6 68,9 67,8 70,2

Pigeon 17,0 19,5 18,6 16,3

Pureen 16,3 11,4 11,0 11,1

Page 39 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 40/54

Pureen Kids NA NA 2,6 2,3

Table 5: Market share in baby segment

Total 6 Cities - Val% - Total Shower Gel DEC05 DEC06 DEC07 MAR08

Johnson's Baby 11,9 13,3 12,0 10,9

Lux 12,1 10,2 10,4 10,1

Dove 11,4 10,1 9,1 8,8

Enchanteur 7,4 7,3 6,9 8,6

X-Men 6,3 5,6 6,7 5,7

Double Rich 3,8 4,3 4,9 4,7

Lifebuoy 1,6 2,1 4,5 4,6

Romano 4,0 3,5 3,7 3,2

Pigeon 3,0 3,7 3,3 NA

Palmolive 4,3 2,9 3,2 3,1

Table 6: Market share in Shower Gel

The receivable policy in Trade Systems is similar to Supermarket, except

they have credit line based on their area and sales strategy of company and discount

on 5% pretax price.

To trade Sales, they have specific for each type:

Retailer Market

Credit line Limit Limit

Discount No discount on 2% pretax price

Payment term 1 days from invoice date 1 days from invoice date

Payment method Cash on delivery Cash on delivery

Collectors Sales men Sales men

4.2.2. Estimate how these receivable policies affect on cashflow:

Items that affect Cash flow from Accounts Receivables:

• Competition.

• Written corporate policy that include:

- Terms of sales.

- Collection techniques incorporated.

Page 40 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 41/54

- Support by upper management of its credit department versus sales

department.

• Corporate customer philosophy referring to how a customer is treated.

• Size and kill/experience level of the individuals in the credit and

collections areas.

• Lack of computer systems that are conducive to improving cash flow

efforts

• Sales support of cash flow as well as cooperation with the credit area

and their integrity plus incentive to cooperate.

• Actual top management support of cash flow, not just a written policy

and procedures manual.

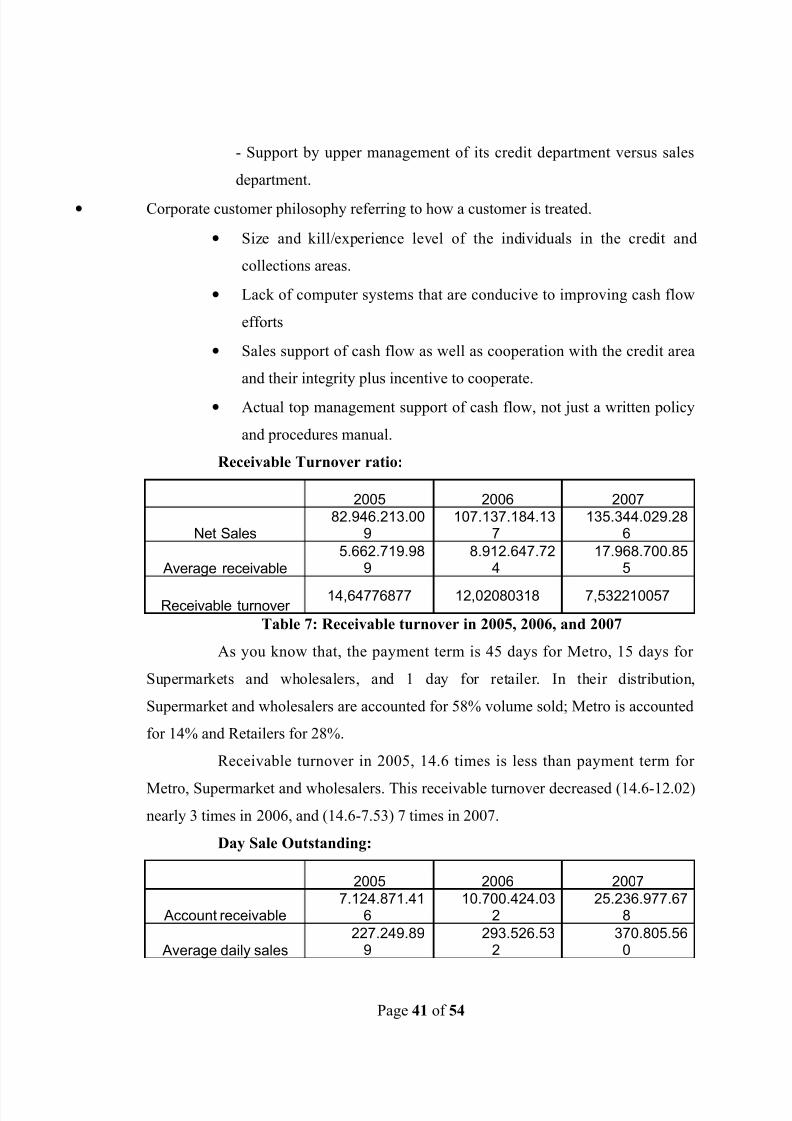

Receivable Turnover ratio:

2005 2006 2007

Net Sales82.946.213.00

9107.137.184.13

7135.344.029.28

6

Average receivable5.662.719.98

98.912.647.72

417.968.700.85

5

Receivable turnover 14,64776877 12,02080318 7,532210057

Table 7: Receivable turnover in 2005, 2006, and 2007

As you know that, the payment term is 45 days for Metro, 15 days for

Supermarkets and wholesalers, and 1 day for retailer. In their distribution,

Supermarket and wholesalers are accounted for 58% volume sold; Metro is accounted

for 14% and Retailers for 28%.

Receivable turnover in 2005, 14.6 times is less than payment term for

Metro, Supermarket and wholesalers. This receivable turnover decreased (14.6-12.02)

nearly 3 times in 2006, and (14.6-7.53) 7 times in 2007.

Day Sale Outstanding:

2005 2006 2007

Account receivable7.124.871.41

610.700.424.03

225.236.977.67

8

Average daily sales227.249.89

9293.526.53

2370.805.560

Page 41 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 42/54

DSO31,35258347 36,45470808 68,05986863

Table 8: DSO in 2005, 2006, and 2007You see that DSO is increasing from 2005 to 2007. DSO in 2007 is double

DSO in 2005. It means that many invoices were past due.

From this point, we may think that receivable management is not good.

Now we turn to see Bad debt at 12/31/2006 and at 12/31/2007(see full

table xx in Appendix)

2005 2006

Bad debts

53.671.54

2

11.196.85

7Account

receivable7.124.871.41

610.700.424.03

2

% Bad debt 0,75% 0,10%

Table 9: Percentage bad debts of Account Receivable

2005 2006

Bad debts53.671.542

11.196.857

Net Sales

82.946.213.00

9

107.137.184.13

7% Bad debt 0,06% 0,01%

Table 10: Percentage bad debts of Net Sales

2004 2005 2006 2007

Bad debts14.678.53

853.671.54

211.196.85

7 0

Table 11: Bad debt in 2004, 2005, 2006, and 2007 based on invoice day

Bad debts percentage of Account Receivable and Net Sales was

decreasing. And these bad debts are in accepted limit.

4.2.3. Evaluate each receivable policy:

a. How are order taken? (Receivable Antecedents)

To Metro, Supermarket, and wholesales they receive order via fax. To

retailers, they receive form sales men. In 2005 and 2006, they had

taken an order for 2 days, 3-4 days if so far. They use Rhub to make a

tax invoice. Rhub is software used to manage good inventory, make an

Page 42 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 43/54

invoice based on what information you had input already: price, tax

rate, discount, customer’s address, payment term…

b. Credit processing:

From Credit application to credit –Approved Customers, they take 8

days to 15 days making decision. The CD Sup receives Credit

application, assesses Credit application, then make a proposal to Sales

Director. Sales Director review and assess this proposal, then discuss

to CFO and Marketing Director to giving Credit line if approved.

It has been approved by Sales Director, CFO and Marketing Director.

c. Credit decision:

The main Credit decision makes on Credit line. It is calculated by a

special formula of CD Sup including target sales, market share at this

area. To wholesaler, after calculating, they assign target sales to

customers within 4 weeks, and then they divide by 4. It is an amount

the customers have to take a deposit with the company or letter of

credit from banks. The triple of the amount is credit limit that is the

largest of volume customers can make an order.

d. Collection efforts

The system provides a list of customers that are past due as of day; call

a past due notice to them, followed by form letters, followed by a call

and more form letter; end by either collecting or placing for collection.

Page 43 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 44/54

CHAPTER 5

DISCUSSION

i. If it was easy, everyone would do it (well):

Management of the receivables asset is a demanding task. The vast

majority of companies expect that over 99.9% of all billings will be collected.

Collecting ninety five percent of revenue is not good enough.

Companies will tolerate bad debt expense of several tenths of a percent of revenue,

but not much more. Which other departments are expected to perform at 99 plus

percent effectiveness?

It is generally expected that a high percentage of invoices will be paid on

time and over 90% within 15 days of the due date. Management expects that the asset

will be managed to promote sales and that all customers will be served promptly,

courteously, and professionally. Astoundingly, most firms also expect this all to be

accomplished for a cost equal to about two to three tenths of a percent of

revenue. Quite a bargain!

Management of the receivables asset is a complex task. It addresses the

ramifications of practices and processes usually outside the span of control of the

responsible manager. It requires balancing of opposing priorities. It is affected by the

state of the domestic and global economy, interest rates, foreign exchange rates,

banking regulations and practices, business law, and other factors. Excellence in

receivables management is a combination of art as well as science; it involves

business process, technology tools, staff skills, motivation, company culture, changing

behavior of customers and coworkers, the right organization structure and metrics,

incentives, and flexibility to deal with changing external influences.

ii. Influences outside the control of the responsible manager:

Page 44 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 45/54

The receivables asset is sometimes called the garbage can of the company.

This is because the receivables asset reflects the quality of the entire revenue cycle

operation. If an error is made in taking an order, fulfilling it, invoicing it, applying the

customer payment, or if the customer is dissatisfied with the product or service, it will

manifest itself as a past due or short payment in the receivables ledger. The quality of

the receivables asset is an excellent barometer of customer service. It is feedback the

customer willingly and quickly gives. It is tempting to call it a free quality control

measurement system, except it is not free. The firm does not have to pay customers

for the feedback, but it does incur costs in remediating the problems.

iii. Conflicting priorities:

Excellence in receivables management requires trade-offs between

conflicting goals. The trade-offs are best balanced in accordance with the company’s

overriding strategic objectives. To optimize the trade-off, the relative ranking of these

strategic objectives must be understood:

• Sales growth

• Profitability

• Cash generation

• Market share

Page 45 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 46/54

• Risk tolerance

The conflicting objectives are to:

• Loosen credit acceptance criteria and controls to boost sales versus

tightening credit controls to minimize the investment in receivables and the exposure

to bad debt loss.

• Achieve strong receivables management results and provide excellent

financial service to your customers versus minimizing the cost of the function.

iv. Credit policy:

The global marketplace runs on credit. Goods and services are routinely

delivered with the expectation that payment will be made according to the agreed

payment terms. Credit risk has two dimensions. The first is the risk that payment will

never be made. This loss is known as bad debt. The second risk is that payment will

be made late; that is, beyond agreed payment terms. This loss is known as

delinquency. It is considered a loss on the basis that a company will have to borrow

money and pay interest to replace the funds not received on time. Naturally, bad debt

loss is the more devastating of the two losses and the risk that receives the most

management attention. The critical task to managing credit risk is to balance the need

for credit sales, and the profit earned on those sales, against the perceived risk of

extending credit to a customer. There is no easy answer or magic formula for

balancing these factors. The proper balance varies by individual company and is

based on a firm’s profit margins, strategic goals, and whether a product can be

repossessed and resold. There are many techniques and tools to investigate, evaluate,

and monitor credit risk; however, balancing that risk against the other company

priorities is unique to each firm, requires judgment, and is never easy.v. Bookkeeping for Accounts Receivable:

Companies have two methods available to them for measuring the net

value of account receivables, which is computed by subtracting the balance of an

allowance account from the accounts receivable account. The first method is the

allowance method, which establishes a contra asset account as the offset to accounts

receivable in the balance sheet. The amount of the allowance can be computed in two

Page 46 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 47/54

ways; through the analysis based on sales method and analysis based on accounts

receivable method. The reason a contra asset receivable account is necessary is to

adhere to the matching principle of accounting, which mandates that accrual basis

companies match all revenues and expenses with the period in which they are earned

and incurred, respectively. The second method, the direct write off method, is

simpler than the allowance method in that allows for one simple entry to reduce

accounts receivable to its net realizable value.

For tax reporting purposes, the direct write-off method must be used;

however, for financial reporting purposes, it is necessary to use the allowance method

because it matches a period's revenue with associated expenses-a fundamental

concept of accounting known as the matching principle.

vi. Organization structure:

The “right” organizational structure is one that will:

• Deploy the proper skills to each of the functions within receivables

management to maximize effectiveness

• Staff the positions with the appropriate level of knowledge and

experience to be cost efficient

Page 47 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 48/54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 49/54

Monthly estimates of credit losses: At the end of each month,

management should again estimate the probable amount of uncollectible accounts and

adjust the Allowance for Doubtful to this new estimate. Based on past experience, the

uncollectible accounts expense is estimated at percentage of receivable by Rhub

software. The computer software is quickly and easily prepares monthly aging

schedules of account receivable.

With this method, it is useful to management in review the status of

individual accounts receivable and in evaluating the overall effectiveness of credit and

collection policies. The longer an account is past due, the greater the likelihood that it

will not be collected in full. Base on past experience, the credit manager estimates the

percentage of credit losses likely to occur in each the age group of account receivable.

This percentage, when applied to the total amount in the age group, gives the

estimated uncollectible portion for that group. By adding together the estimated

uncollectible portions for all age groups, the required balance in Allowance for

Doubtful Accounts is determined (see in table 1).

It is related to taw government; the company has prepared for at least 2

years to change in this method.

Page 49 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 50/54

REFERENCE

1. Johnson & Johnson homepage at http://www.jnj.com/connect/

2. John G. Salek,(2004) Wiley Best Practices, Accounts Receivable Management

Best Practices

3. Weygrandt, Kieso, Kimmel.(2003), John Wiley & Sons, Financial Accounting

4. Warren Reeve Fess, (2005), Thomason 21e, Accounting

5. Williams Haka Bettner Carcello, (2008), Mc Graw-Hill, Financial Accounting

6. Michelle Dunn , (2006), Entrepreneur Magazine’s, Credit and Collections

handbook

7. Pay Attention to Internal Collections- Darin Ball, January 16 2008.

www.collectionadvisor.com

8. Seven Habits - and Rewards - of Highly Efficient Collections Operations -

Lois Brown, January 17 2008

9. Optimizing Receivables - Yu-Soon Koh, January 28 2008

Source: CreditandCollectionsWorld.com

10. Best Practice in Consumer Collections - Astrid Rial, January 21 2008

Page 50 of 54

8/6/2019 Project on Consumer Behaviour

http://slidepdf.com/reader/full/project-on-consumer-behaviour 51/54

APPENDICES

Customer name InvoiceInvoice

day

Delivery

day

pay

mentA/R Aging

79.546.936

PHUÙAN THÒNH 8867 13/10/200514/10/2005COD 477.489 443

PHUÙAN THÒNH 10579 11/11/200512/11/2005COD 828.289 414

TM-DV COÂNG NGHEÄTRÍ VIEÄT 3782 28/01/200529/01/2006COD 14.101.542 336 TM-DV COÂNG NGHEÄTRÍ VIEÄT 3805 29/01/200529/01/2006COD 1.778.159 336

TM-DV COÂNG NGHEÄTRÍ VIEÄT 3806 29/01/200529/01/2006COD 3.251.526 336