prohibition of interest

TRANSCRIPT

Prohibition Of Interest.....Does it Make Sense?

By: Rizwan Ansar K.M on the basis of the book " Prohibition of Interest, does it make sense?" By Mr. Umer Chapra

Quran and Riba (Interest)

(Surah Al-Baqra Verse 275)

TRADE RIBA (INTEREST)�

Reward Punishment (Fire)

Trade Vs Riba

The lender of money is an investor in trade and is prone to both profit and loss

Trade is majorily based on Equity

Trade is natural and therefore maintains the mass balance i.e increase or decrease in trade gets shared, thereby maintaining balance

There is possibility of attaining the humanitarian goal of Equality among people.

Trade by nature does Justice to Economy

The lender of money has no role in trade but expects a fixed positive return

Trade is majorly based on Debt

Interest is artificial/forced with restraints which is positively biased towards the lender, therefore it cannot maintain the mass balance.

No possibilities of Equality, By principle, Rich is destined to become Richer and Poor to Poorer.

Interest by nature inflicts damage and injustice to the borrower, and economy at large

Humanitarian Goals

1.General Need Fulfillment2.Full Employment3.Equitable Distribution of Income

and Wealth4.Economic Stability

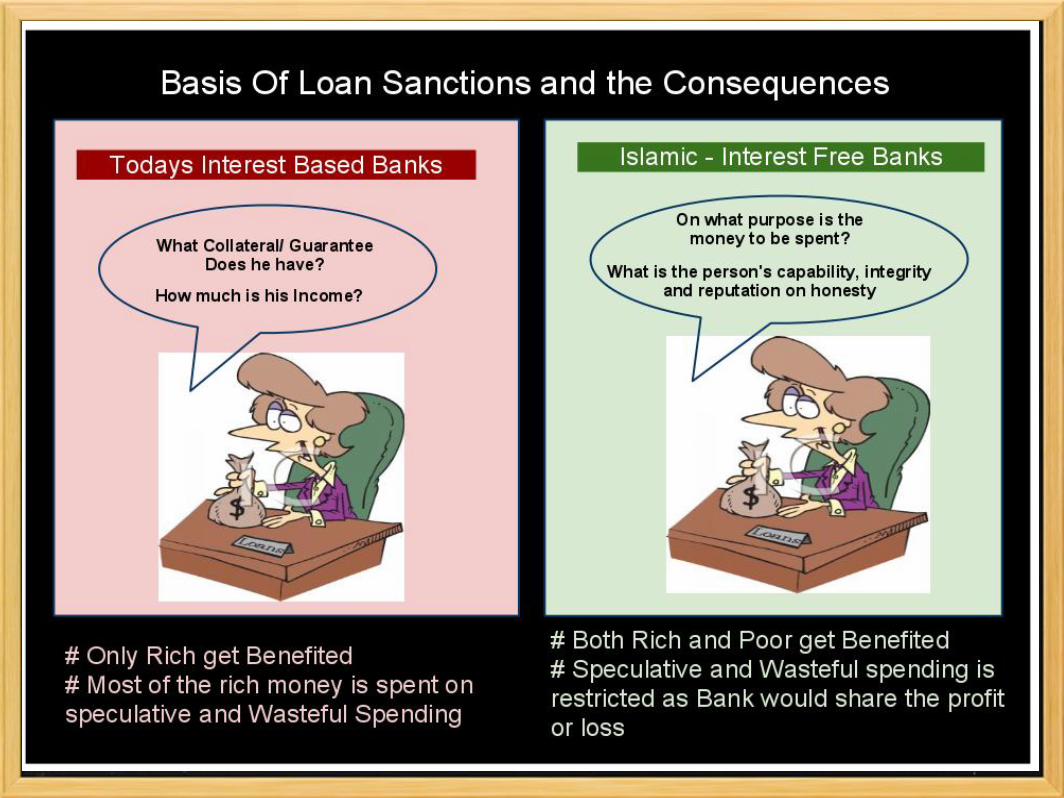

1. NEED FULFILLMENT

Interest Based

Financial allocation of resources are majorly based on Collateral to guarantee repayment

Rich gets the most benefited

Promotes Speculative and Wasteful Spending as the bank gets benefited of a positive return just by promoting spending

E.g. United States - richest country in the world unable to meet the essential needs of all its people inspite of latest technologies and abundant resources at its disposal.

Non-Interest Based(Islamic)

Financial allocation of resources are majorly based on End-Use i.e. for what cause the funds would be utilized.

Both Rich and Poor can get benefited

Restricts speculative and Wasteful spending as the bank shares the risks and rewards of financing.

E.g. Medina, could fulfill essential needs of all its people when the economy was interest free (1400 years back, the only recorded period of existence of such economy).

2. Full Employment

Interest BasedPromotion of "Living beyond Means" culture by easy facilitation of credit

Decrease in Savings leading to high level of real interest rates & lower investments leading to increased unemployment.

Credit is made available for lifestyle living, which is beyond means.

Bank does not share the risk and expects a positive return just by promoting spending, therefore bank financing doesnot much improve real economy growth and employment as it is utilised for wasteful spending and speculation

Non-Interest BasedPromotion of trade and equity based system by facilitation of productive investments.

Equity based promotes savings and thereby lowers real interest rates, Increases Investments and Employment.

Credit is primarily made available for real goods and services.

Bank shares the risk and reward of financing thereby by nature does due diligence and promotes productive investments therefore increasing Employment.

3. Equitable Distribution of Wealth

Interest Based

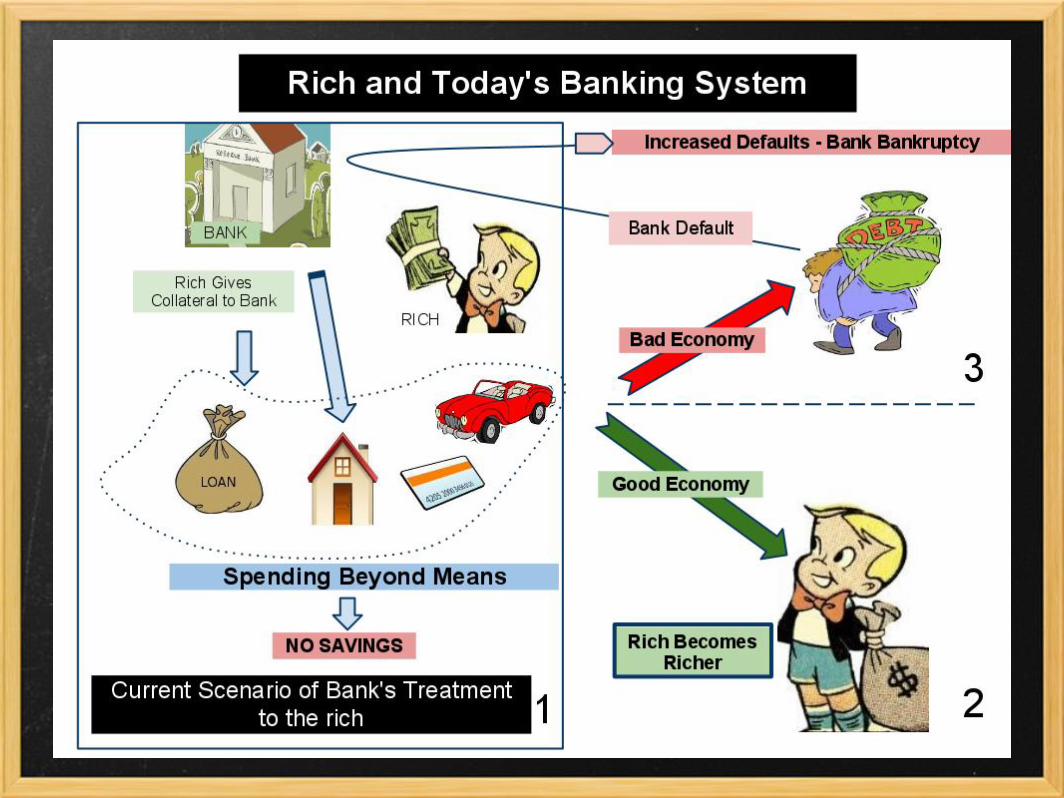

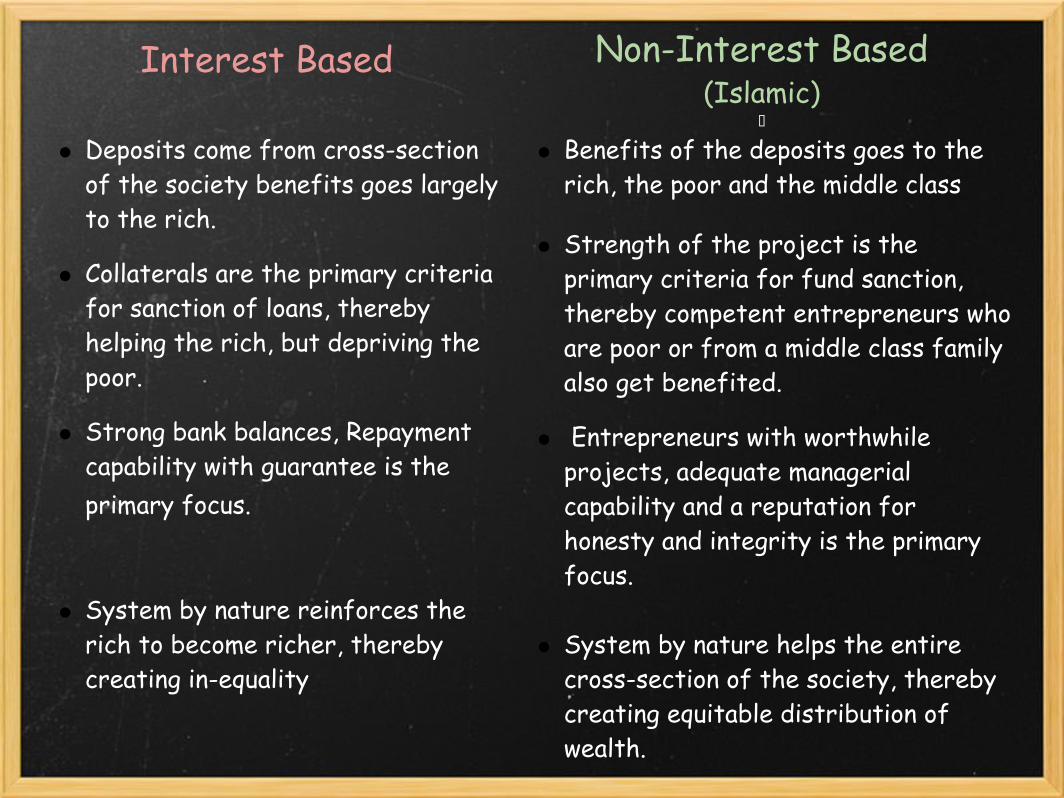

Deposits come from cross-section of the society benefits goes largely to the rich.

Collaterals are the primary criteria for sanction of loans, thereby helping the rich, but depriving the poor.

Strong bank balances, Repayment capability with guarantee is the primary focus.

System by nature reinforces the rich to become richer, thereby creating in-equality

Non-Interest Based(Islamic)

�

Benefits of the deposits goes to the rich, the poor and the middle class

Strength of the project is the primary criteria for fund sanction, thereby competent entrepreneurs who are poor or from a middle class family also get benefited.

Entrepreneurs with worthwhile projects, adequate managerial capability and a reputation for honesty and integrity is the primary focus.

System by nature helps the entire cross-section of the society, thereby creating equitable distribution of wealth.

4. Economic Stability

Interest Based

High degree of interest rate volatility injects great uncertainty into the investment market making long-term investment decisions difficult for entrepreneurs.

Drives borrowers and lenders into short end of the financial market resulting in highly leveraged short term debt, which plays an important role in de-stabilizing the economy.

Short-term debts are easily reversible for lenders but borrowers find it difficult to repay if funds are invested in medium or long term returns, thereby creating crisis with even slight economic turbulence

Non-Interest Based

No interest, equity based financing with sharing on profits and losses helps making long term decisions relatively easier for entrepreneurs.

Lenders are primarily investors in business and therefore, see a win-win situation in helping the business grow and taking a bigger share, thereby enhancing long term co-operation.

Islam allows a reasonable amount of short term debt, while the majority is for long term, thereby helping withstand economic turbulences.

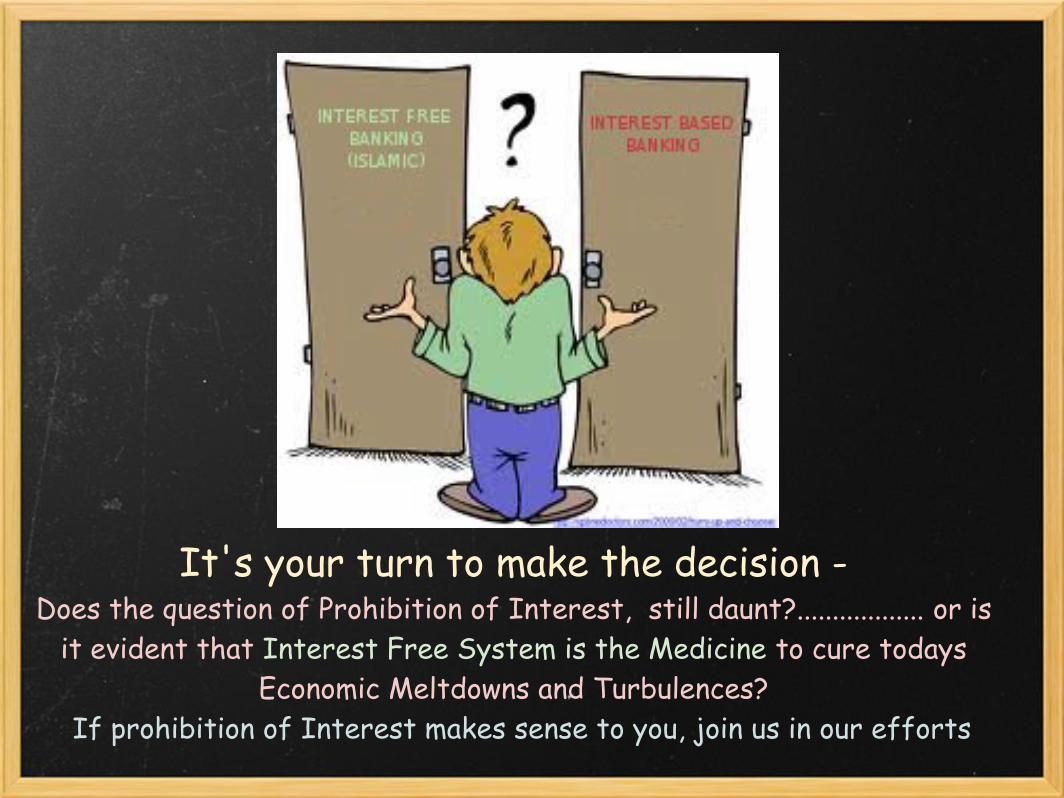

It's your turn to make the decision - Does the question of Prohibition of Interest, still daunt?.................. or is

it evident that Interest Free System is the Medicine to cure todays Economic Meltdowns and Turbulences?

If prohibition of Interest makes sense to you, join us in our efforts