profarma healthcare15 vf_2

TRANSCRIPT

January 13, 2015

J.P. Morgan Healthcare Conference

POSITIVE SECTOR DYNAMICS

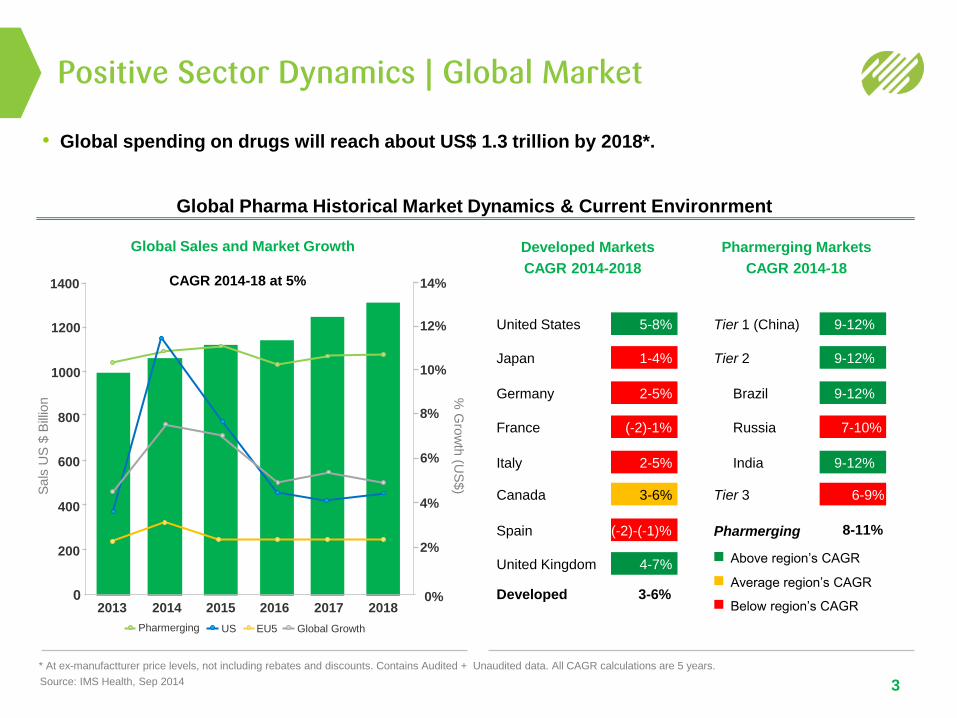

Positive Sector Dynamics | Global Market

3

* At ex-manufactturer price levels, not including rebates and discounts. Contains Audited + Unaudited data. All CAGR calculations are 5 years.

Global Sales and Market Growth

2013 2014 2015 2016 2017 2018

800

600

400

200

0

6%

4%

2%

0%

Sals

US

$ B

illio

n %

Gro

wth

(US

$)

Source: IMS Health, Sep 2014

1200

1000

United States 5-8% Tier 1 (China) 9-12%

Japan 1-4% Tier 2 9-12%

Germany 2-5% Brazil 9-12%

France (-2)-1% Russia 7-10%

Italy 2-5% India 9-12%

Canada 3-6% Tier 3 6-9%

Spain (-2)-(-1)% Pharmerging 8-11%

United Kingdom 4-7%

Developed 3-6%

Developed Markets

CAGR 2014-2018

Pharmerging Markets

CAGR 2014-18

Above region’s CAGR

Average region’s CAGR

Below region’s CAGR

Global Pharma Historical Market Dynamics & Current Environrment

CAGR 2014-18 at 5%

8%

• Global spending on drugs will reach about US$ 1.3 trillion by 2018*.

1400

10%

12%

14%

Pharmerging US EU5 Global Growth

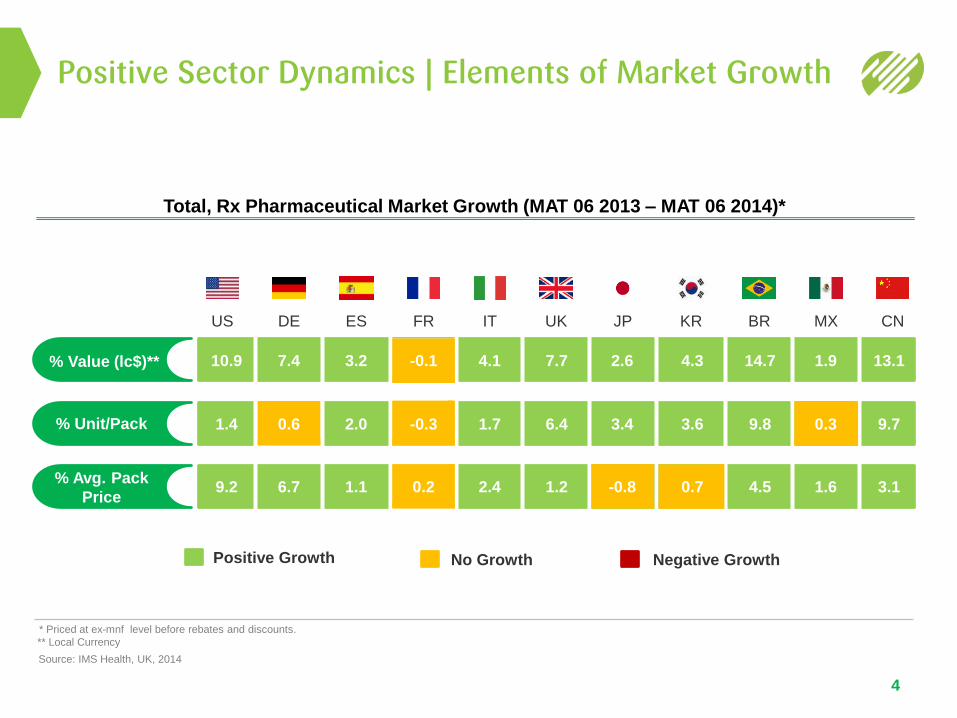

Positive Sector Dynamics | Elements of Market Growth

4

Source: IMS Health, UK, 2014

Total, Rx Pharmaceutical Market Growth (MAT 06 2013 – MAT 06 2014)*

US DE ES FR IT UK JP KR BR MX CN

% Value (lc$)**

% Unit/Pack

% Avg. Pack

Price 9.2 6.7 2.4 1.2 4.5 1.6 3.1 1.1 -0.8 -0.8 -0.8 0.7 -0.8 0.2

10.9 -0.8 -0.1 7.4 3.2 4.1 7.7 2.6 4.3 14.7 13.1 1.9

1.4 -0.8 -0.3 -0.8 0.6 2.0 1.7 6.4 3.4 3.6 9.8 9.7 -0.8 0.3

Positive Growth Negative Growth No Growth

* Priced at ex-mnf level before rebates and discounts.

** Local Currency

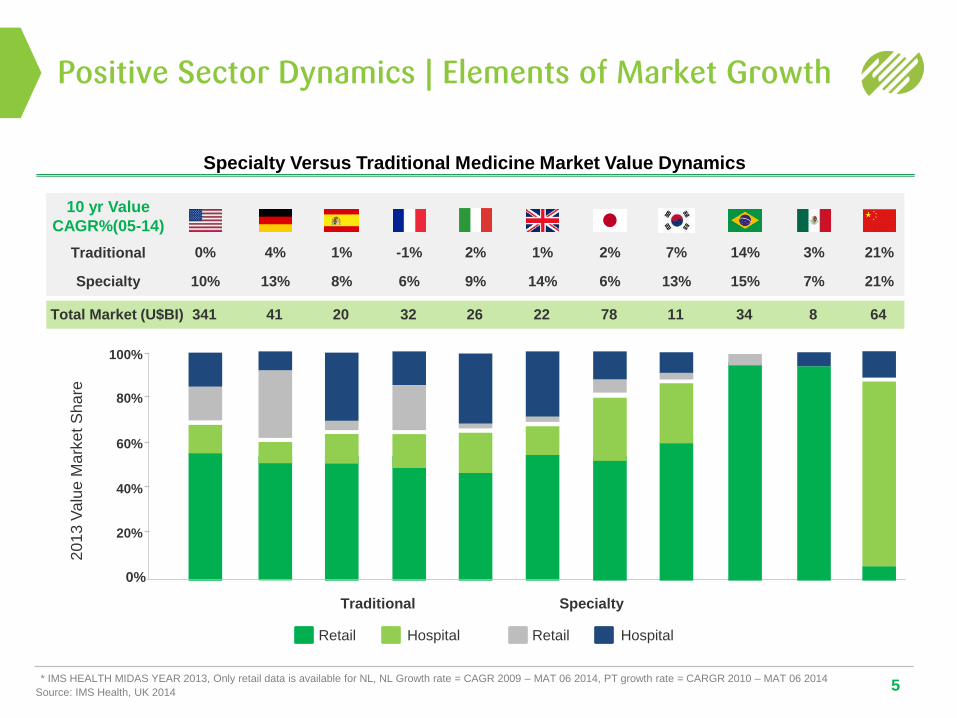

Positive Sector Dynamics | Elements of Market Growth

5 Source: IMS Health, UK 2014

Specialty Versus Traditional Medicine Market Value Dynamics

* IMS HEALTH MIDAS YEAR 2013, Only retail data is available for NL, NL Growth rate = CAGR 2009 – MAT 06 2014, PT growth rate = CARGR 2010 – MAT 06 2014

Retail Hospital

Traditional

Retail Hospital

Specialty

20

13

Va

lue

Ma

rket S

ha

re

80%

60%

40%

20%

0%

100%

0%

10%

Traditional

Specialty

10 yr Value

CAGR%(05-14)

4%

13%

1%

8%

-1%

6%

2%

9%

1%

14%

2%

6%

7%

13%

14%

15%

3%

7%

21%

21%

341 Total Market (U$BI) 41 20 32 26 22 78 11 34 8 64

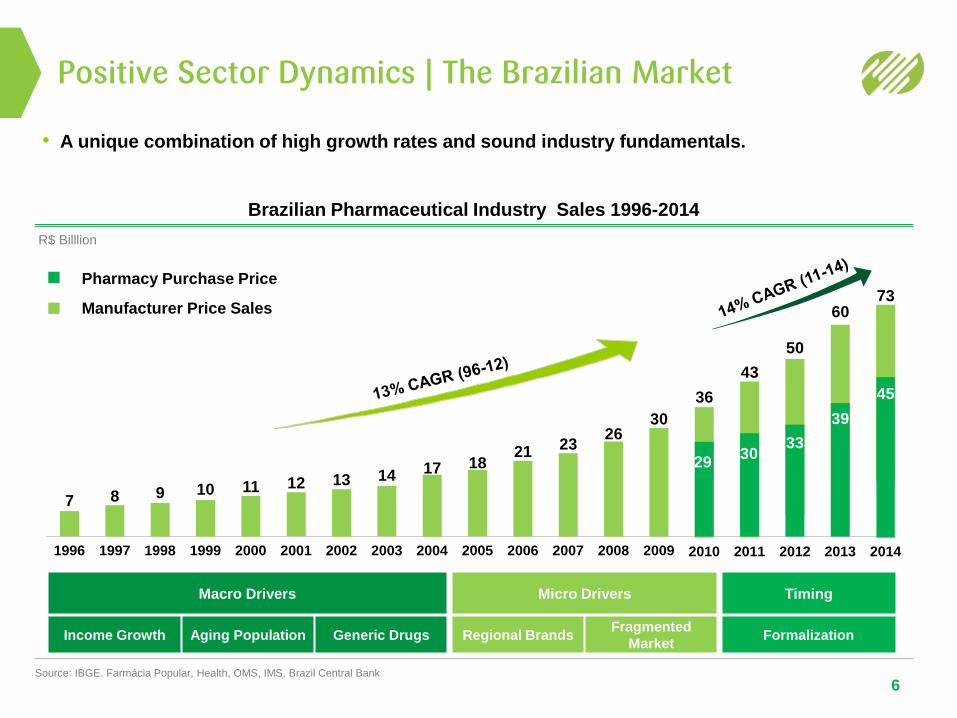

Positive Sector Dynamics | The Brazilian Market

6 Source: IBGE. Farmácia Popular, Health, OMS, IMS, Brazil Central Bank

Macro Drivers Micro Drivers Timing

Income Growth Aging Population Generic Drugs Regional Brands Fragmented

Market Formalization

Pharmacy Purchase Price

Manufacturer Price Sales

Brazilian Pharmaceutical Industry Sales 1996-2014

• A unique combination of high growth rates and sound industry fundamentals.

R$ Billlion

7

1996

8

1997

9

1998

10

1999

11

2000

12

2001

13

2002

14

2003

17

2004

18

2005

21

2006

23

2007

26

2008

30

2009

50

33

2012

39

60

2013

45

73

2014

43

2011

30

36

2010

29

7

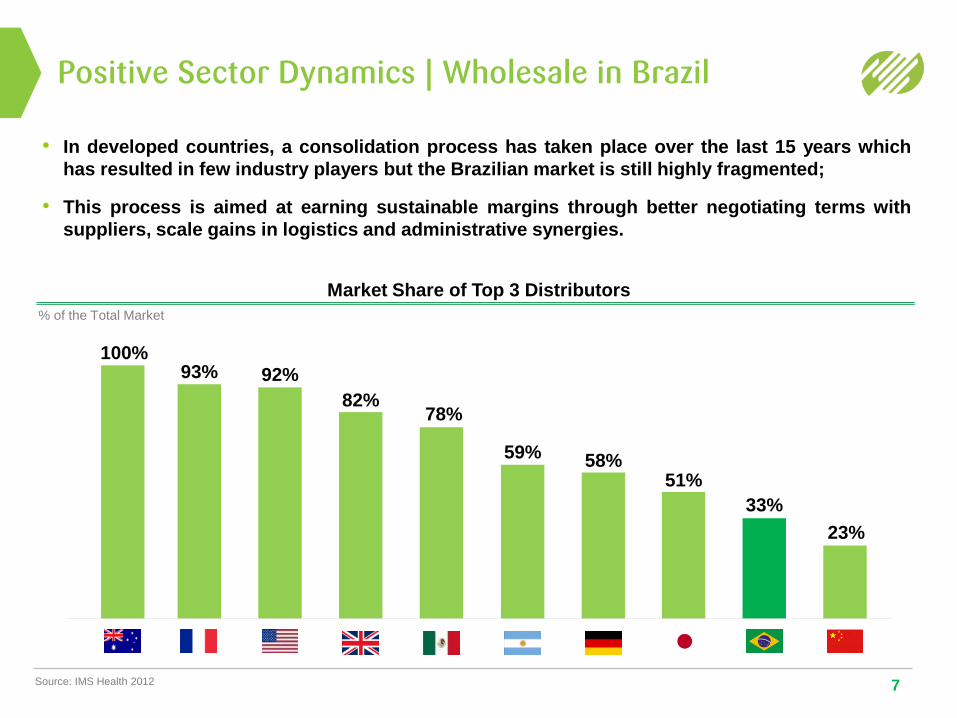

Market Share of Top 3 Distributors

% of the Total Market

Source: IMS Health 2012

100% 93% 92%

82% 78%

59% 58% 51%

33%

23%

• In developed countries, a consolidation process has taken place over the last 15 years which

has resulted in few industry players but the Brazilian market is still highly fragmented;

• This process is aimed at earning sustainable margins through better negotiating terms with

suppliers, scale gains in logistics and administrative synergies.

Positive Sector Dynamics | Wholesale in Brazil

Positive Sector Dynamics | The Retail Industry in Brazil

8

• Brazil’s retail market is still highly fragmented, with nearly 67,000 drugstores. Independent

stores continue to play an important role in the retail sector.

• The top chains in Brazil are consolidating their positions through geographical expansion,

whereas medium-sized chains are consolidating their positions regionally.

Groups # of Stores Names

Source: Market Share IMS MAT Oct/14.

Market Share

12,6%

31,7%

55,7% Top Chains

RaiaDrogasil

DPSP

BR Pharma

Pague Menos

Panvel*

Nissei

Extrafarma *

Araújo

Onofre

1.045

830

723

718

317

226

187

130

47

Other Chains Other Chains (Incl. Profarma)

7,998 121

Independent Independent 51,500

*Mixed Model

Top Chains with Established Positions – 2014 Ranking by Number of Stores

9

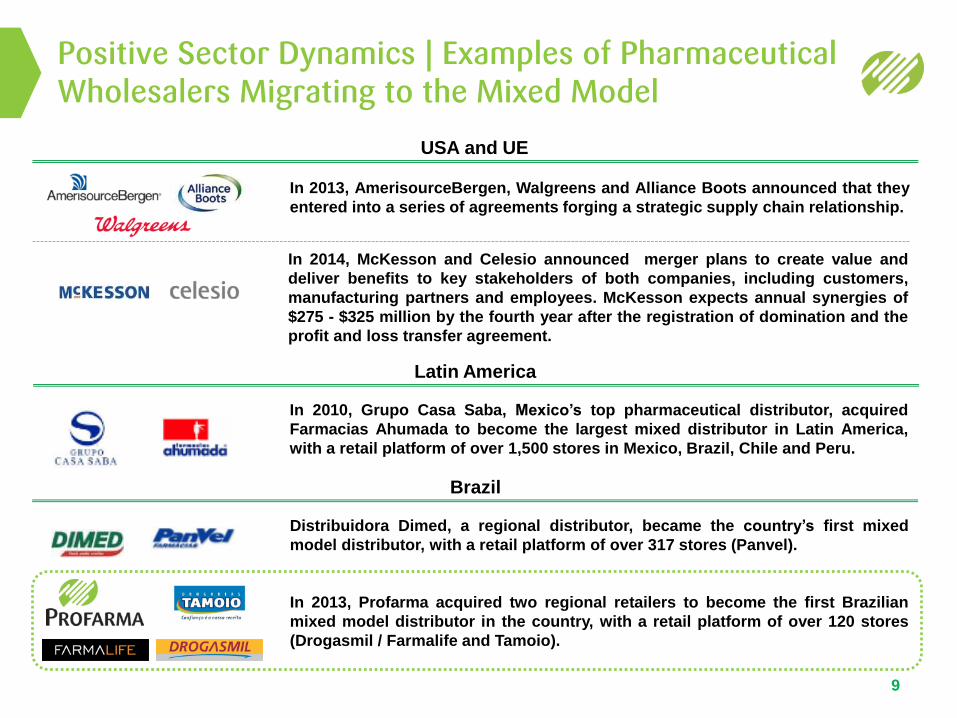

Positive Sector Dynamics | Examples of Pharmaceutical Wholesalers Migrating to the Mixed Model

In 2013, AmerisourceBergen, Walgreens and Alliance Boots announced that they

entered into a series of agreements forging a strategic supply chain relationship.

USA and UE

Latin America

In 2010, Grupo Casa Saba, Mexico’s top pharmaceutical distributor, acquired

Farmacias Ahumada to become the largest mixed distributor in Latin America,

with a retail platform of over 1,500 stores in Mexico, Brazil, Chile and Peru.

Distribuidora Dimed, a regional distributor, became the country’s first mixed

model distributor, with a retail platform of over 317 stores (Panvel).

Brazil

In 2013, Profarma acquired two regional retailers to become the first Brazilian

mixed model distributor in the country, with a retail platform of over 120 stores

(Drogasmil / Farmalife and Tamoio).

In 2014, McKesson and Celesio announced merger plans to create value and

deliver benefits to key stakeholders of both companies, including customers,

manufacturing partners and employees. McKesson expects annual synergies of

$275 - $325 million by the fourth year after the registration of domination and the

profit and loss transfer agreement.

Positive Sector Dynamics | The Retail Sector in Brazil

10

• Strategic competitive position in Rio de Janeiro State - Retail Segment.

Groups # of Stores Names

Top 4 Chains

Pacheco

Drogasmil / Farmalife / Tamoio (Profarma)

Raia / Drogasil

Venâncio

352

121

79

33

585 Total

2014 Top Chains in Rio de Janeiro State by Gross Revenue

Source: Companies’ Website

COMPANY’S OVERVIEW

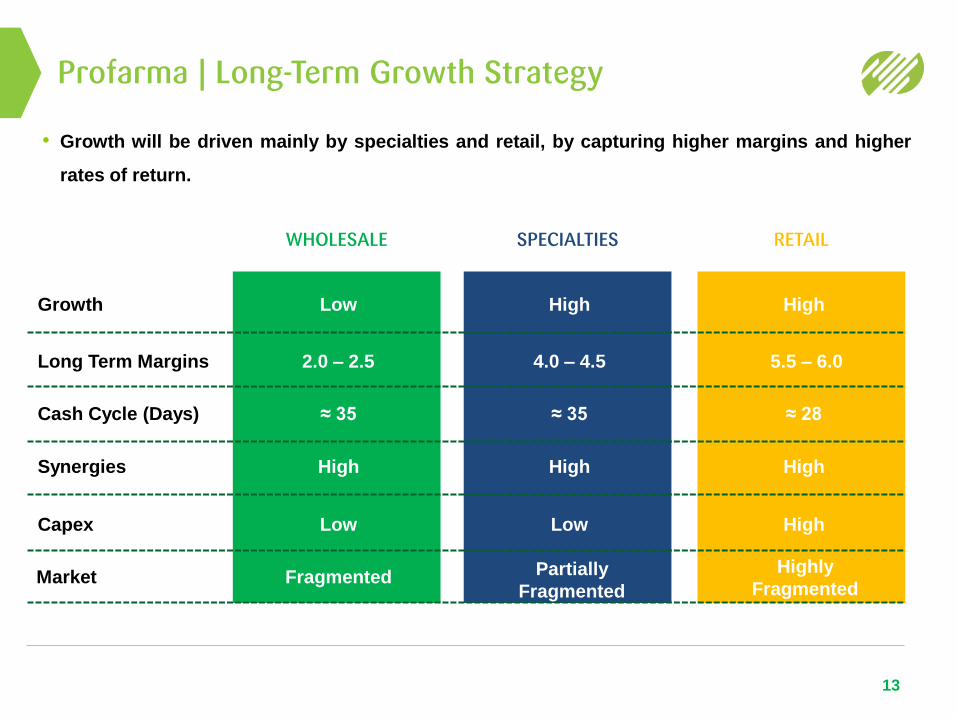

• Profarma’s long-term growth strategy is to be well positioned to capture the opportunities in the

Brazilian Pharmaceutical Market.

Profarma | Long-Term Growth Strategy

12

Wholesale 53 years of operation

REGIONAL EXPANSION

NEW SEGMENTS / PRODUCTS

STRATEGIC ASSOCIATION RETAIL

• Growth will be driven mainly by specialties and retail, by capturing higher margins and higher

rates of return.

Profarma | Long-Term Growth Strategy

13

WHOLESALE SPECIALTIES RETAIL

Growth

Long Term Margins

Cash Cycle (Days)

Synergies

Capex

Low High High

2.0 – 2.5 4.0 – 4.5 5.5 – 6.0

Low Low High

≈ 35 ≈ 35 ≈ 28

High High High

Market Fragmented Partially

Fragmented

Highly

Fragmented

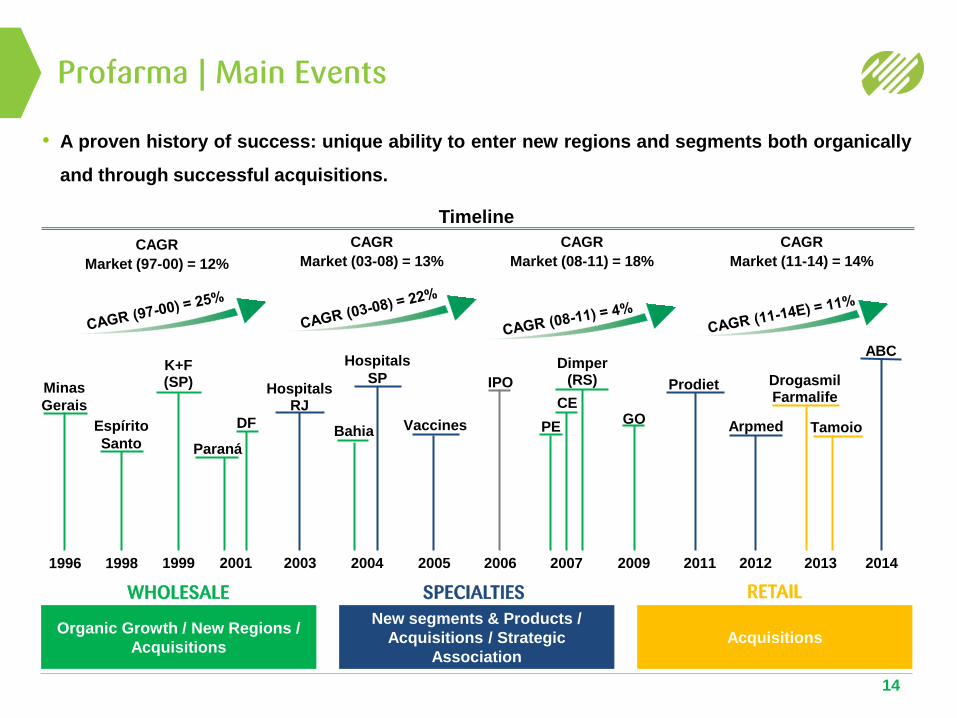

Profarma | Main Events

14

Timeline

Organic Growth / New Regions /

Acquisitions

New segments & Products /

Acquisitions / Strategic

Association

Acquisitions

Espírito

Santo

1998

K+F (SP)

1999

Minas

Gerais

1996

DF

Paraná

2001

Hospitals RJ

2003

Vaccines

2005

IPO

2006

PE

Dimper (RS)

CE

2007 2009

Prodiet

2011

Arpmed

2012

Bahia

2004

Hospitals

SP

2013

Tamoio

Drogasmil Farmalife

ABC

2014

GO

• A proven history of success: unique ability to enter new regions and segments both organically

and through successful acquisitions.

SPECIALTIES WHOLESALE RETAIL

CAGR

Market (11-14) = 14%

CAGR

Market (08-11) = 18%

CAGR

Market (03-08) = 13% CAGR

Market (97-00) = 12%

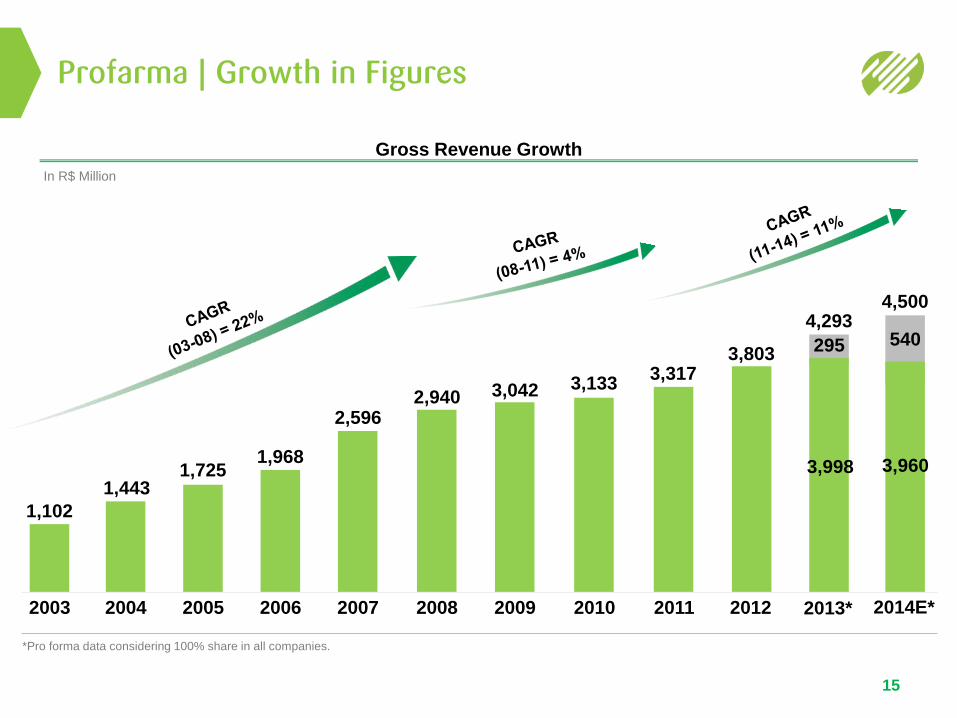

Profarma | Growth in Figures

15

In R$ Million

1,102

2003

1,443

2004

1,725

2005

1,968

2006

2,596

2007

2,940

2008

3,042

2009

3,133

2010

Gross Revenue Growth

2011

3,317

2012

3,803

4,293

2013*

3,998

295

4,500

2014E*

3,960

540

*Pro forma data considering 100% share in all companies.

68.1

80.1 78.7

110.7

74.6 73.0

92.2

125.1** 126.1**

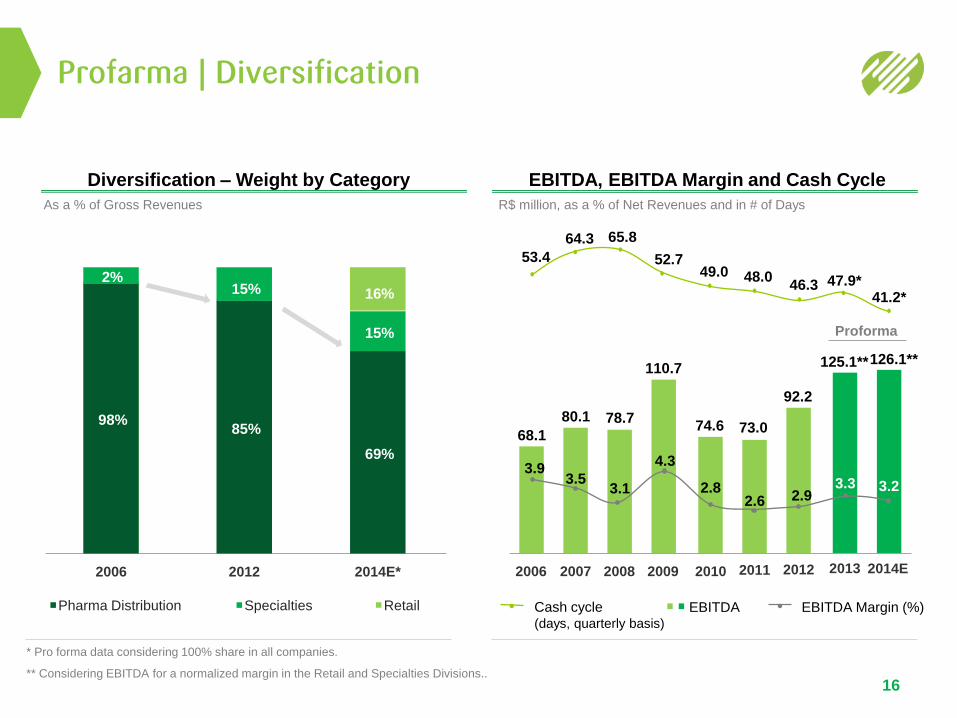

Profarma | Diversification

Diversification – Weight by Category EBITDA, EBITDA Margin and Cash Cycle

As a % of Gross Revenues R$ million, as a % of Net Revenues and in # of Days

EBITDA EBITDA Margin (%) Cash cycle (days, quarterly basis)

Pharma Distribution Specialties Retail

2006 2012

98%

2%

85%

15%

69%

15%

16%

2014E* 2006 2007 2008 2009 2010 2011 2012 2013

52.7

64.3

53.4

65.8

49.0 48.0 47.9*

4.3

3.5 3.9

3.1 2.8 2.6 2.9

3.3

46.3

2014E

41.2*

3.2

Proforma

* Pro forma data considering 100% share in all companies.

** Considering EBITDA for a normalized margin in the Retail and Specialties Divisions.. 16

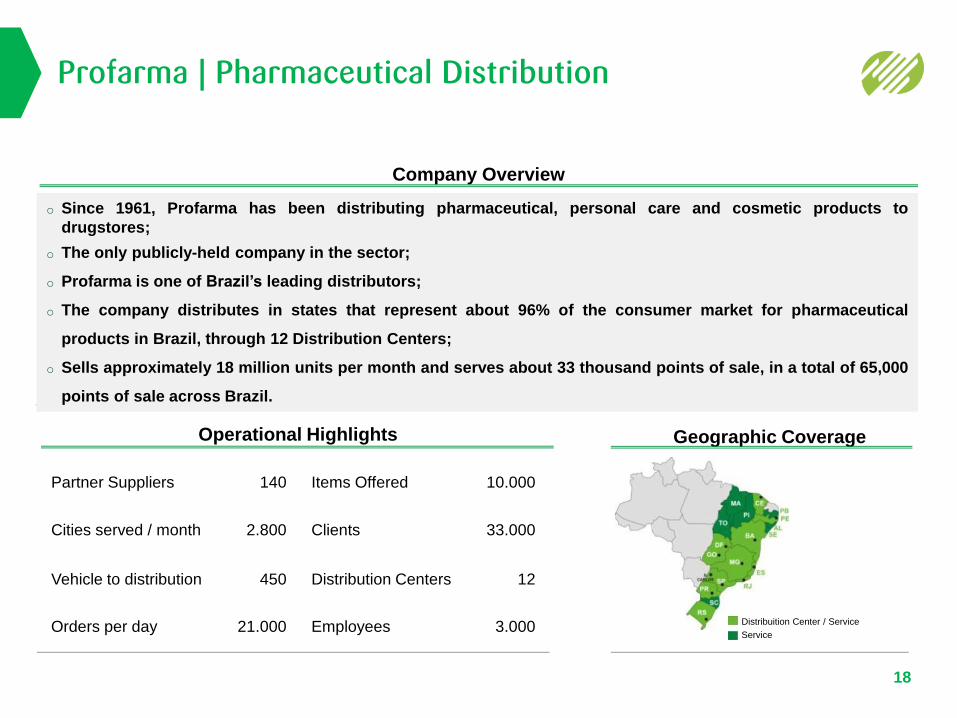

PHARMACEUTICAL DISTRIBUTION

Profarma | Pharmaceutical Distribution

18

Orders per day 21.000

Items Offered 10.000

Clients 33.000

Employees 3.000

Distribution Centers 12

Partner Suppliers 140

Cities served / month 2.800

Vehicle to distribution 450

Company Overview

Operational Highlights Geographic Coverage

Distribuition Center / Service

Service

o Since 1961, Profarma has been distributing pharmaceutical, personal care and cosmetic products to

drugstores;

o The only publicly-held company in the sector;

o Profarma is one of Brazil’s leading distributors;

o The company distributes in states that represent about 96% of the consumer market for pharmaceutical

products in Brazil, through 12 Distribution Centers;

o Sells approximately 18 million units per month and serves about 33 thousand points of sale, in a total of 65,000

points of sale across Brazil.

SPECIALTIES

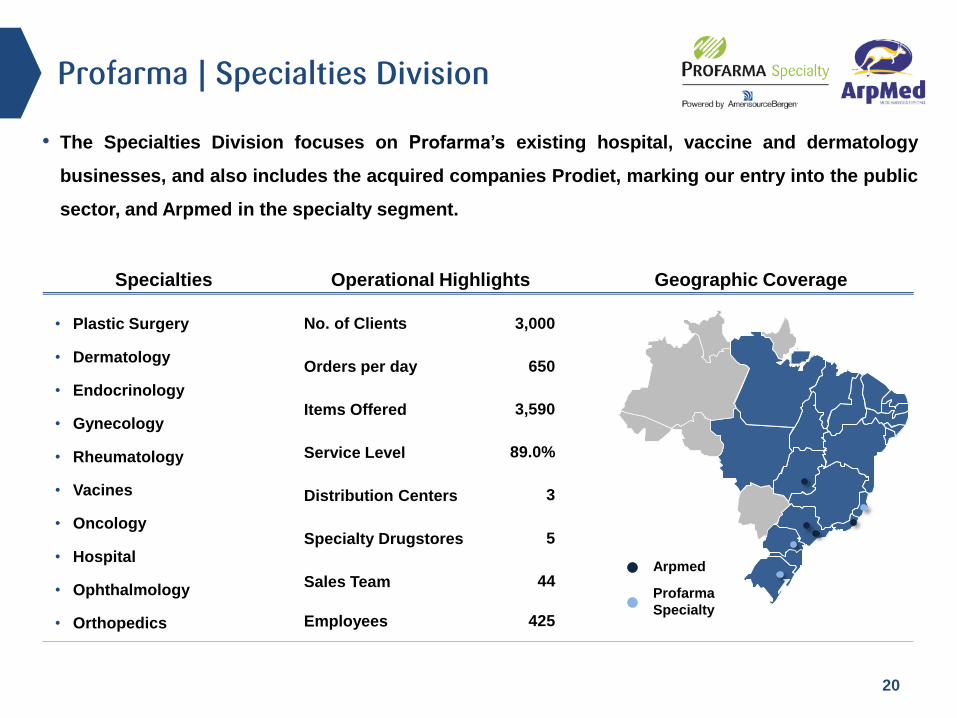

• The Specialties Division focuses on Profarma’s existing hospital, vaccine and dermatology

businesses, and also includes the acquired companies Prodiet, marking our entry into the public

sector, and Arpmed in the specialty segment.

20

Profarma | Specialties Division

Cobertura Geográfica

• Plastic Surgery

• Dermatology

• Endocrinology

• Gynecology

• Rheumatology

• Vacines

• Oncology

• Hospital

• Ophthalmology

• Orthopedics

Specialties Geographic Coverage Operational Highlights

Arpmed

Profarma

Specialty

Orders per day 650

Specialty Drugstores 5

Distribution Centers 3

No. of Clients 3,000

Items Offered 3,590

Sales Team 44

Employees 425

Service Level 89.0%

21

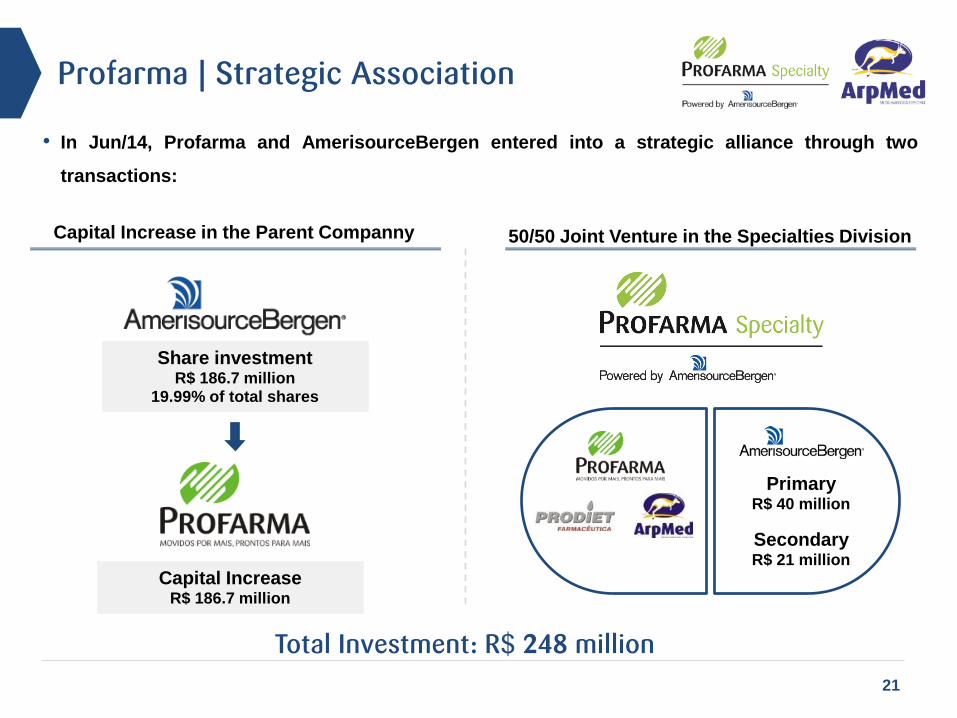

Profarma | Strategic Association

50/50 Joint Venture in the Specialties Division Capital Increase in the Parent Companny

Total Investment: R$ 248 million

Share investment R$ 186.7 million

19.99% of total shares

Primary R$ 40 million

Secondary R$ 21 million

Capital Increase R$ 186.7 million

• In Jun/14, Profarma and AmerisourceBergen entered into a strategic alliance through two

transactions:

• One of the largest global pharmaceutical services companies dedicated exclusively to increasing

supply chain efficiency.

22

AmerisourceBergen | Overview

23

GlobalSourcing & Distribution Services Manufacturer Solutions

Provider Solutions Pharmacy Solutions

• Generic purchasing programs;

• Pharmacy network and programs;

• Business consulting services;

• Technology solutions;

• Packaging solutions.

• Source and distribute branded, generic, specialty, OTC pharmaceuticals and other healthcare products;

• Source 50,000+ items from 1,500+ manufacturers;

• Part of the largest global generics sourcing organization;

• Provides 95% of hospitals with specialty pharmaceuticals;

• Largest community pharmacy distribution network and distributor of oncology products to private practices.

• Specialty physician group purchasing organizations;

• National specialty pharmacy and nursing services;

• Business consulting services;

• Clinical, operational and financial improvement solutions;

• Clinical / operational education programs.

• Strategic consulting services;

• Global specialty logistics;

• Market-leading specialty physician group

purchasing organizations;

• Patient support services;

• Product awareness and marketing services.

AmerisourceBergen | Services & Solutions

RETAIL

25

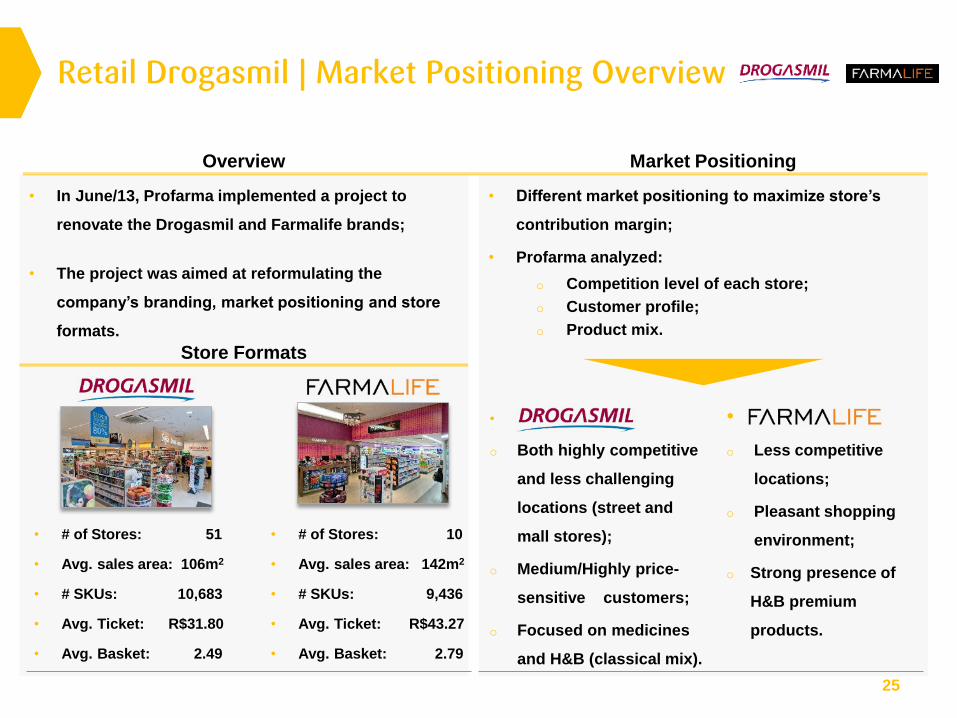

Overview Market Positioning

• Different market positioning to maximize store’s

contribution margin;

• Profarma analyzed:

o Competition level of each store;

o Customer profile;

o Product mix.

•

o Both highly competitive

and less challenging

locations (street and

mall stores);

o Medium/Highly price-

sensitive customers;

o Focused on medicines

and H&B (classical mix).

•

o Less competitive

locations;

o Pleasant shopping

environment;

o Strong presence of

H&B premium

products.

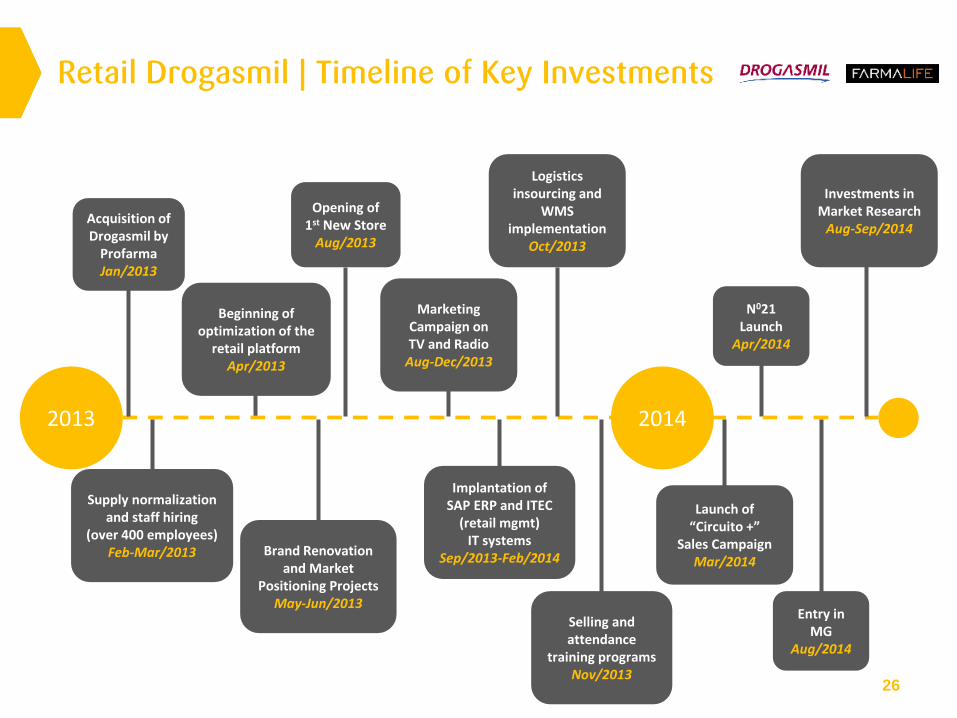

• In June/13, Profarma implemented a project to

renovate the Drogasmil and Farmalife brands;

• The project was aimed at reformulating the

company’s branding, market positioning and store

formats.

Store Formats

• # of Stores: 51

• Avg. sales area: 106m2

• # SKUs: 10,683

• Avg. Ticket: R$31.80

• Avg. Basket: 2.49

• # of Stores: 10

• Avg. sales area: 142m2

• # SKUs: 9,436

• Avg. Ticket: R$43.27

• Avg. Basket: 2.79

Retail Drogasmil | Market Positioning Overview

26

2013 2014

Acquisition of Drogasmil by

Profarma Jan/2013

Supply normalization and staff hiring

(over 400 employees) Feb-Mar/2013

Beginning of optimization of the

retail platform Apr/2013

Brand Renovation and Market

Positioning Projects May-Jun/2013

Marketing Campaign on TV and Radio

Aug-Dec/2013

Implantation of SAP ERP and ITEC

(retail mgmt) IT systems

Sep/2013-Feb/2014

Logistics insourcing and

WMS implementation

Oct/2013

Selling and attendance

training programs Nov/2013

Launch of “Circuito +”

Sales Campaign Mar/2014

N021 Launch

Apr/2014

Entry in MG

Aug/2014

Investments in Market Research

Aug-Sep/2014

Opening of 1st New Store

Aug/2013

Retail Drogasmil | Timeline of Key Investments

Retail Drogasmil | Brand and Store Renovation

Before

After

Retail Drogasmil | Brand and Store Renovation

Before

After

Retail Drogasmil | Brand and Store Renovation

Before

After

Retail Drogasmil | Brand and Store Renovation

Before

After

31

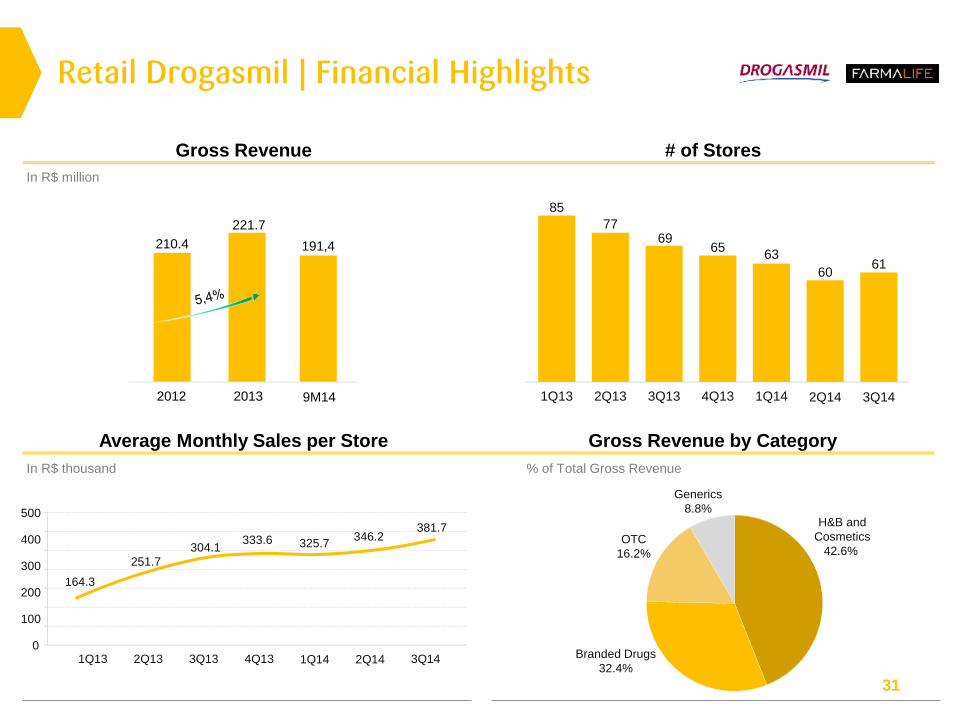

In R$ million

% of Total Gross Revenue In R$ thousand

63 61

1Q13 2Q13 3Q13 4Q13 1Q14

164.3

381.7

1Q13 2Q13 3Q13 4Q13 3Q14 0

100

200

300

400

500 H&B and

Cosmetics

42.6%

Branded Drugs

32.4%

OTC

16.2%

Generics

8.8%

Retail Drogasmil | Financial Highlights

# of Stores Gross Revenue

Gross Revenue by Category Average Monthly Sales per Store

60

69 77

65

85

2Q14 3Q14

1Q14 2Q14

251.7

304.1 333.6 325.7

346.2

210.4

221.7

2012 2013

191,4

9M14

32

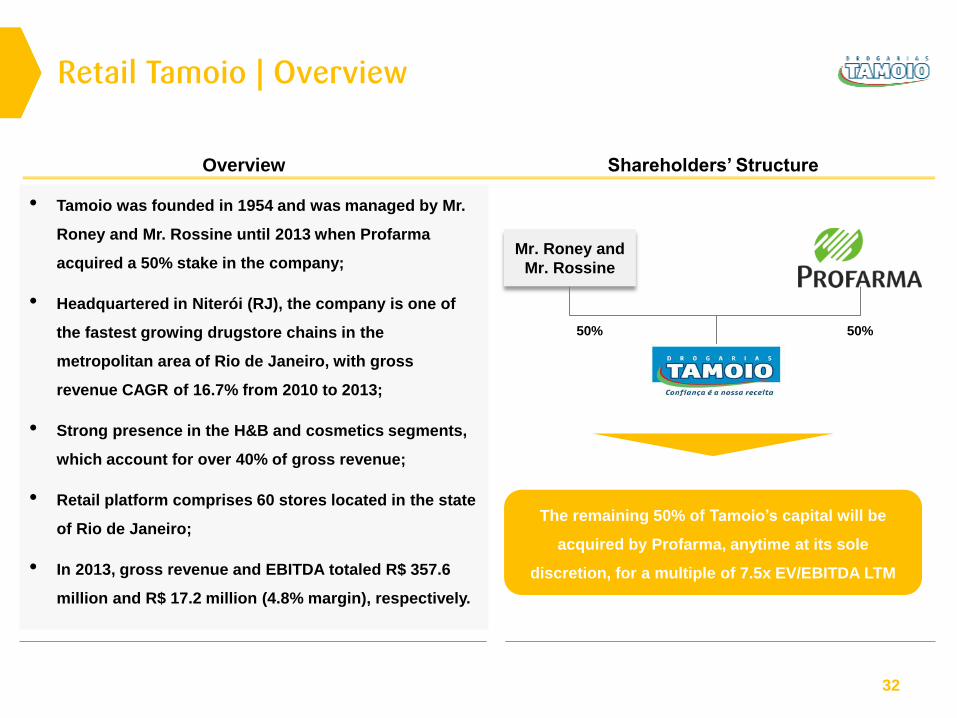

• Tamoio was founded in 1954 and was managed by Mr.

Roney and Mr. Rossine until 2013 when Profarma

acquired a 50% stake in the company;

• Headquartered in Niterói (RJ), the company is one of

the fastest growing drugstore chains in the

metropolitan area of Rio de Janeiro, with gross

revenue CAGR of 16.7% from 2010 to 2013;

• Strong presence in the H&B and cosmetics segments,

which account for over 40% of gross revenue;

• Retail platform comprises 60 stores located in the state

of Rio de Janeiro;

• In 2013, gross revenue and EBITDA totaled R$ 357.6

million and R$ 17.2 million (4.8% margin), respectively.

Mr. Roney and

Mr. Rossine

50% 50%

The remaining 50% of Tamoio’s capital will be

acquired by Profarma, anytime at its sole

discretion, for a multiple of 7.5x EV/EBITDA LTM

Retail Tamoio | Overview

Overview Shareholders’ Structure

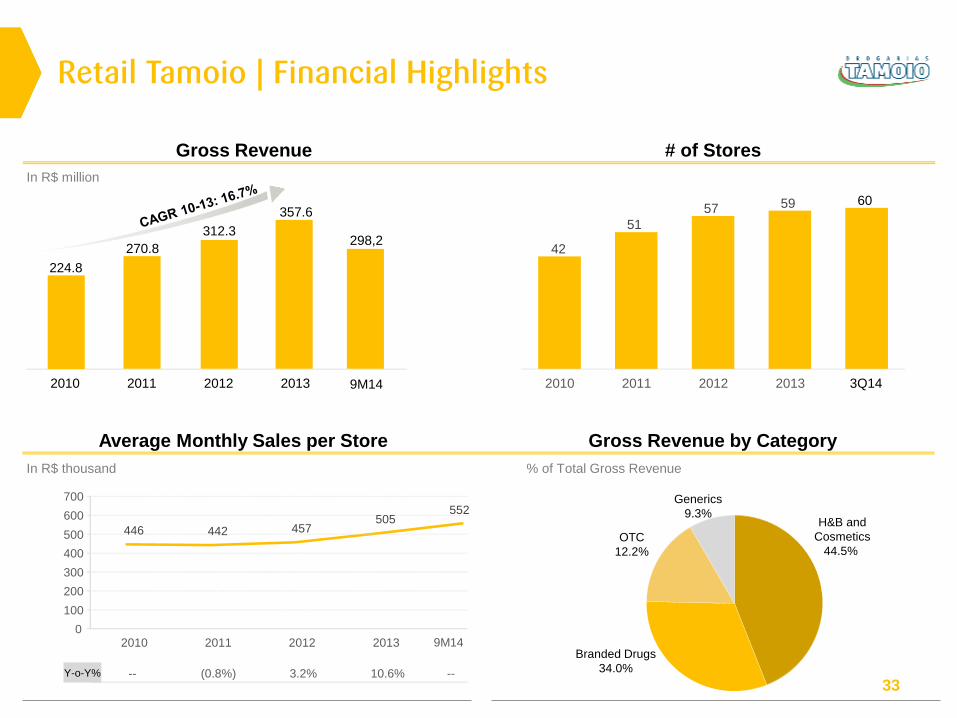

33

In R$ million

% of Total Gross Revenue In R$ thousand

42

51

57 59 60

2010 2011 2012 2013 3Q14

H&B and

Cosmetics

44.5%

Branded Drugs

34.0%

OTC

12.2%

Generics

9.3%

Retail Tamoio | Financial Highlights

# of Stores Gross Revenue

Gross Revenue by Category Average Monthly Sales per Store

Y-o-Y% -- (0.8%) 3.2% 10.6%

446 442 457 505

2010 2011 2012 2013 0

100

200

300

400

500

600

700

9M14

552

224.8

270.8

312.3

357.6

2010 2011 2012 2013

298,2

9M14

--

Distribution to

hospitals, clinics

and doctors

Future opportunity:

franchise Future opportunity:

proprietary brand

Top 3

domestic distributors

Specialties

Consolidation of

retail

Profarma | New Strategic Positioning

32

Key Takeaways

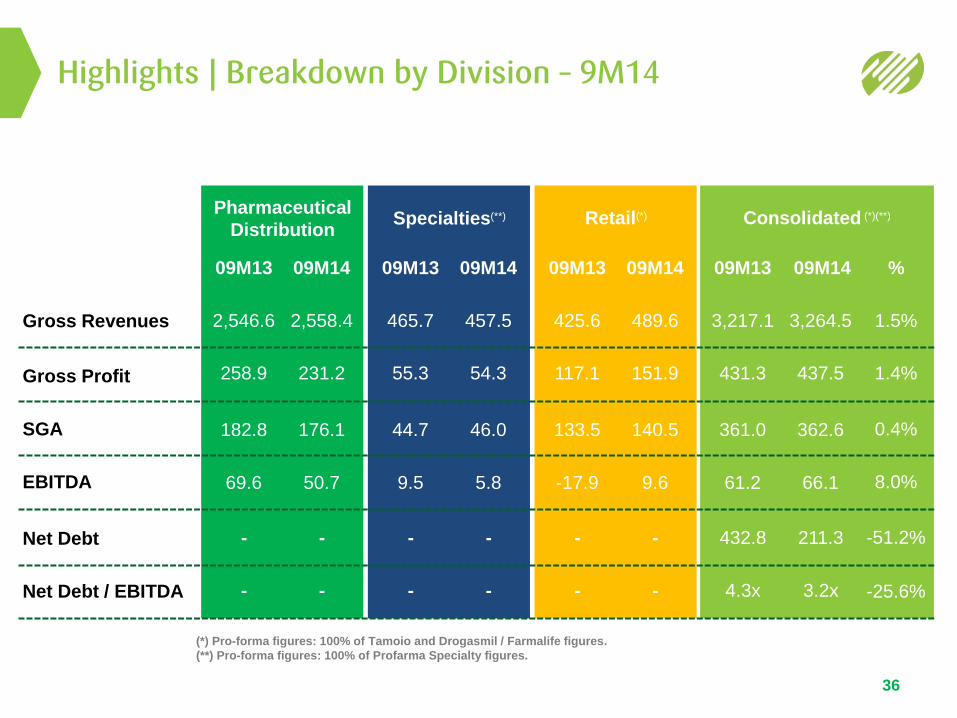

CONSOLIDATED PERFORMANCE

Specialties(**)

09M13 09M14

465.7

55.3

44.7

9.5

457.5

54.3

46.0

5.8

-

-

-

-

Retail(*)

09M13 09M14

425.6

117.1

133.5

-17.9

489.6

151.9

140.5

9.6

-

-

-

-

Consolidated (*)(**)

09M13 09M14

3,217.1

431.3

361.0

61.2

3,264.5

437.5

362.6

66.1

432.8

4.3x

211.3

3.2x

%

1.5%

1.4%

0.4%

8.0%

-51.2%

-25.6%

Pharmaceutical

Distribution

09M13 09M14

2,546.6

258.9

182.8

69.6

2,558.4

231.2

176.1

50.7

-

-

-

-

Highlights | Breakdown by Division – 9M14

36

Gross Revenues

Gross Profit

SGA

EBITDA

(*) Pro-forma figures: 100% of Tamoio and Drogasmil / Farmalife figures.

(**) Pro-forma figures: 100% of Profarma Specialty figures.

Net Debt

Net Debt / EBITDA

ANALYST COVERAGE

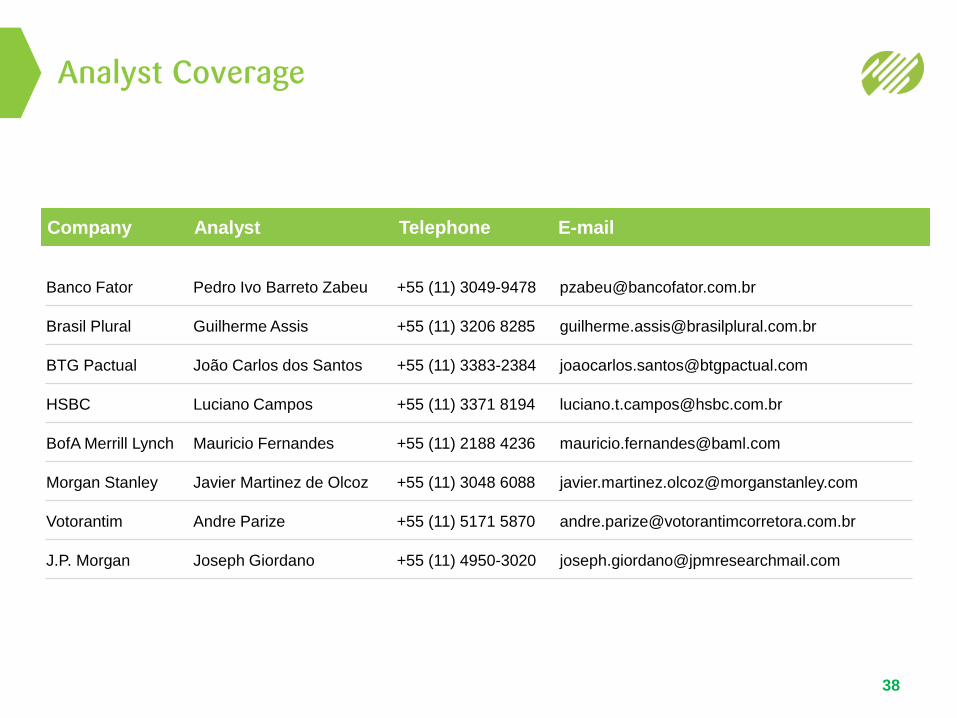

Analyst Coverage

38

Company Analyst Telephone E-mail

Banco Fator Pedro Ivo Barreto Zabeu +55 (11) 3049-9478 [email protected]

Brasil Plural Guilherme Assis +55 (11) 3206 8285 [email protected]

BTG Pactual João Carlos dos Santos +55 (11) 3383-2384 [email protected]

HSBC Luciano Campos +55 (11) 3371 8194 [email protected]

BofA Merrill Lynch Mauricio Fernandes +55 (11) 2188 4236 [email protected]

Morgan Stanley Javier Martinez de Olcoz +55 (11) 3048 6088 [email protected]

Votorantim Andre Parize +55 (11) 5171 5870 [email protected]

J.P. Morgan Joseph Giordano +55 (11) 4950-3020 [email protected]

Max Fischer - CFO & IRO | Beatriz Diez – IR Manager

www.profarma.com.br/ir | Tel.: 55 (21) 4009-0276 | E-mail: [email protected]