prof. michael segalla « best in france » jamie brownlee (uk) daniela sanchez hernandez (mexico)...

TRANSCRIPT

Prof. Michael Segalla« BEST IN FRANCE »

Jamie Brownlee (UK)Daniela Sanchez Hernandez (Mexico)

Anne-Lynke Kikstra (Netherlands)Jaeyoun You (Korea)

Prof. Michael Segalla« BEST IN FRANCE »

Jamie Brownlee (UK)Daniela Sanchez Hernandez (Mexico)

Anne-Lynke Kikstra (Netherlands)Jaeyoun You (Korea)

Monday 10th December, 2007Monday 10th December, 2007

AgendaAgenda

Introduction Capital One

Analysis Why France The French move Pulling out of France

Recommendation Advice for new companies Advice for France

Conclusion

Introduction Capital One

Analysis Why France The French move Pulling out of France

Recommendation Advice for new companies Advice for France

Conclusion

Introduction

Analysis

Recommendation

Conclusion

Introduction

Analysis

Recommendation

Conclusion

Who is Capital One? Capital One Financial Corporation operates as the holding company for the

Capital One Bank and Capital One, F.S.B, which offers various commercial banking services in the United States. The company is headquartered in McLean, Virginia. It listed on the NYSE for the first time in 1994

In less than 20 years it has managed to gain 40 million customers globally.

Capital One provides: - Home loans, healthcare finance, auto finance, commercial and consumer loans

In addition, the company offers:- Commercial credit cards, treasury management services, trust services, and other banking related products ( e.g. insurance, brokerage services, merchant services, and investment banking services.)

It offers its products and services to:- Consumer, commercial and small business customers.

What’s in your wallet?What’s in your wallet? Capital One: one of the America's largest consumer franchises with almost 50 million customer accounts worldwide One of America’s most recognised brands. Now, the fourth largest customer of the United States Postal Service

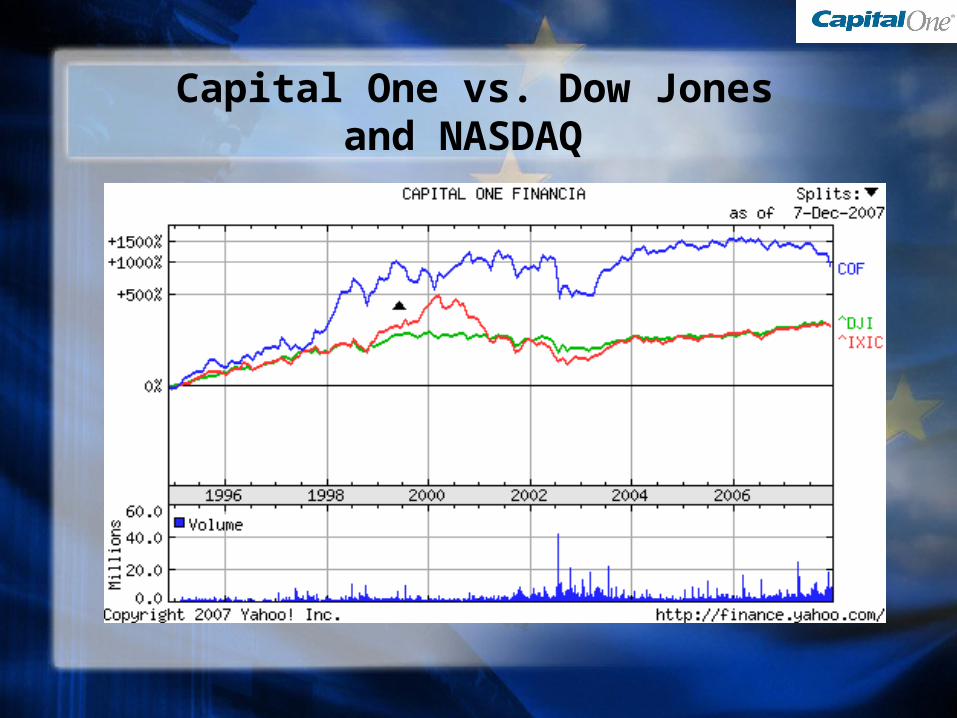

Capital One vs. Dow Jones and NASDAQ

Capital One vs. Competitors

AXP: American Express CompanyBAC: Bank of America CorporationDFS: Discover Financial Services LLCCOF: Capital One

Introduction

Analysis

Recommendation

Conclusion

Introduction

Analysis

Recommendation

Conclusion

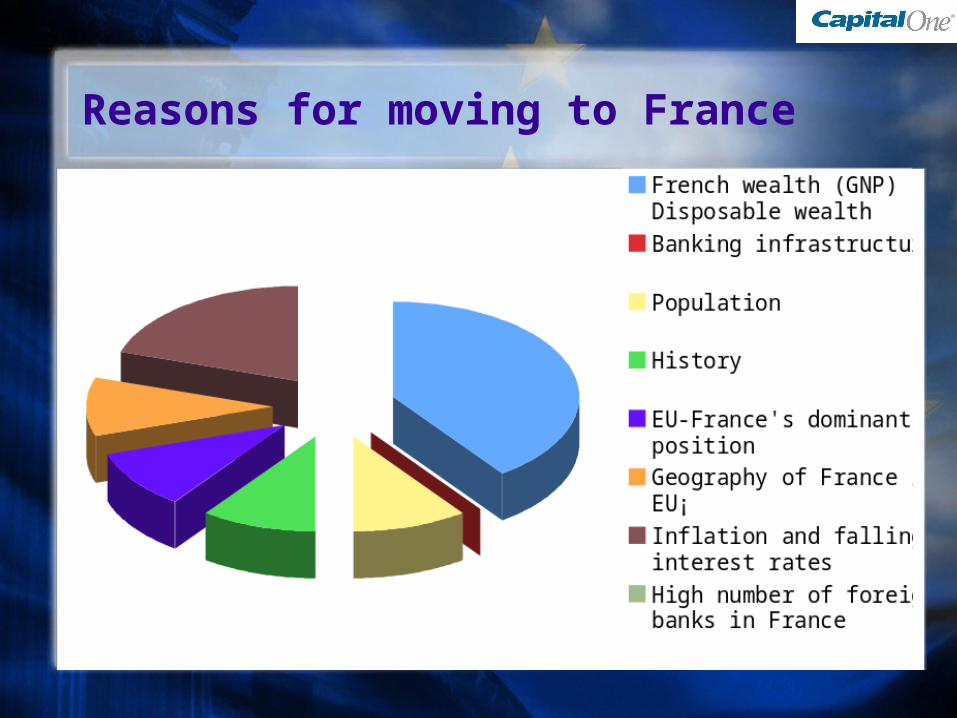

Why the move to France (Major points)?

France was the first country to be invested in after the UK French wealth (disposable income) Banking infrastructure Population History French GNP $1,550 billion (2nd in EU Market) EU 20% larger than the North-American market Inflation remains very low, less than that of Germany, Italy or Spain Falling interest rates Highest rate of growth in Europe. In ten years, between 1985 and

1995, the number of foreign banks and financial institutions established in Paris has increased from 260 to 420

Why the move to France (Minor points)?

Only country with both a direct link and a frontier with the six largest European markets (Germany, Italy, Spain, Benelux: Belgium, Luxembourg and the Netherlands). This meant access to 370 million European consumers

Capital One wanted to open Southern Europe in terms of Credit cards

Human capital, its motivation, quality and productivity. High level of education encourages responsibility, responsiveness, the ability to adapt and show initiative, competent and diversified public service which works

The balance of trade for the last few years equalled 20.3 billion dollars, thus creating an environment particularly favourable to buy in terms of shares

Quality of life

Specific company values around fairness, good corporate citizenship, transparency seemed to fit with French culture

Reasons for moving to France

Competitors

• Egg Banking• France 2002 - 2004 (ING, Netherlands)

• Barclaycard• France 1998 (1 million selling spots)

The French move

Sofinco (French credit card company) contacted Capital One regarding a joint venture. Capital One had not thought about France having only just entered the British market

Sofinco offered a company base in Paris, a great customer base and infrastructure. As well as their own bank branches, which Capital One could exploit

The negotiation took 18 months

Ready to sign contract……BUT Crédit Agricole bought Sofinco

Capital One believed that to enter European market effectively, they needed to enter the French or the German market. Capital One chose the French

Went alone, since they felt they had learnt enough from

Sofinco about the French market (Risk management

in France, French customers, etc.) Moved in 1997 Pulled out in 2002

Ready to sign contract……BUT Crédit Agricole bought Sofinco

Capital One believed that to enter European market effectively, they needed to enter the French or the German market. Capital One chose the French

Went alone, since they felt they had learnt enough from

Sofinco about the French market (Risk management

in France, French customers, etc.) Moved in 1997 Pulled out in 2002

The French move (2)

Why pull out of France?

Long history of failures in France of Financial Services companies

from outside of France. Ancient usury laws created a perception

of closing of ranks against outsiders, they prohibited the wide

extension of credit across the credit spectrum

One of the biggest perceived and actual constraints of anyone

coming to France is the labour laws. It is difficult to get rid of

employees if you need to move quickly (35 hour weeks!) Huge

redundancy costs created problems for speedy changes

Key constraint costs. Capital One’s key competitive

strength has been in its analytical abilities- its ability to lend

at the higher risk end of the market at a sensible price but

acceptable to the individual consumer. With usury laws

preventing Capital One going to that end of the market - its

market was limited

Experienced lobbying by big French banks to change

French legislation to directly and adversely affect what

Capital One were doing (e.g. Limits on penalties for late

payments)

Regulatory companies prohibited their actions

Why pull out of France? (2)

The Corporate and Usury laws of France are archaic. France has an exceptionally introverted attitude to external companies especially those from USA who could shake the status quo and the French Banks effectively block changes which would aid external companies.

There is no question that Capital One’s international strategy was adversely impacted by the inflexibility encountered in France.

Experienced discrimination, gender especially Other locations: Italy, Spain, South Africa are much more

flexible and willing to try new ideas France not willing to change

Why pull out of France? (3)

What Capital One think they did well in France?

Lived up to French expectations, culture, language, consumer and law adaptation

Call centres were staffed by French people in France in the initial stages with any new Financial product, explaining to the customers how things work is a must. At the beginning it worked

They spent years looking at every aspect of the marketing mix in any market, market-testing help a lot. (e.g. A mail shot where Capital One changed the colour of an envelope or write ‘Top Secret’ on it or change the credit limit or the interest rate)

In order to get their values ‘translated’ to be accepted in France, they had a French office with as many French people as possible; but also, blended other experienced Capital One managers and gave great freedom - what they did was ‘Frenchified’

One key Value is fairness and reward. In the world of credit, Capital One only wanted to give an appropriate amount of credit to individuals. Once individuals ‘proved’ their creditworthiness, an extension of amount of credit and deals were offered in terms of interest payable, Cash-back rewards, balance transfers etc. This did fit within the French culture.

Inclusion of French associates in as many international courses/seminars was done in order to encourage absorption of Capital’s One values.

In France, banks are under serious scrutiny especially when dealing with foreign countries- Capital One was no exception. Nevertheless for Capital One this was not as close as for other companies, due to the fact, that FED and FSA were already leading the scrutinising

What Capital One think they did well in France? (2)

Capital One’s views on similarities and differences in FrancePROCESS DIFFERENT SAME ADAPTABLE

Recruitment X (need experience in and outside of France)

Compensation X (flexibility to go for top quartile)

Management Development

X (inclusion of French associates to learn Values of Capital One)

Workforce planning

X (working life)

Performance Appraisal

X

Job design X

Motivation X (needed to communicate more)

Communication policies

X (more formal but translators used)

International Transfers

X (high calibre French nationals spent a year in USA to prepare them)

Hiring X

Real Estate X (cheaper than London)

Language X (associates were usually bilingual)

Introduction

Analysis

Recommendation

Conclusion

Introduction

Analysis

Recommendation

Conclusion

Advice: What would Capital One have done differently? They would have looked at taking deposits to help them to fund the lending

on credit They would also have looked at Auto loans perhaps through a partnership

with one of the car manufacturers in France or the distributors They should not have gone alone. Should have found another consumer

finance house to merge with. With no other company, it was too risky Their main area for expansion would have been in identifying a partnership

with a French financial services company. (e.g. COFIDIS of COFINOGA or with one of

the big supermarket chains e.g. CASTORAMA where as in the UK with TESCO they would start their own financial services company in partnership with us)

If Capital One would not have left the French market, expansion would have been into more and more credit cards with separation from instalment loans

Advice: What Capital One suggest for other banking companies?

It is important to be aware that France takes a highly protectionist

approach towards foreign companies. This is why there have not

been big external financial services companies from UK/USA working

in credit cards who have been successful in this country. Most

businesses must avoid France or at least not attempt to start a

Greenfield operation.

No production of products in France – outsourcing Instalment loans – special products used Instalment loans

on a credit card

(so Capital One gave someone e.g. 20,000 euros on loan over two years which with interest might mean they repay 24,000 euros or 2,000 euros per capita monthly for two years. So the customer got their loan upfront which they can use for anything – new kitchen, holiday, etc. with a credit card on which they will have a small additional flexible credit facility. Each month they repay the instalment loan set amount plus the amount on the credit card. The idea is to get customers in France used to how a credit card works by starting them with what they are used to)

Advice: What Capital One suggest for other banking companies? (2)

Advice: What Capital One suggest for other banking companies? (3)

Design a Pan-European strategy France is not flexible or liberal enough. Aim for Spain

or better still - Poland Vary the interest rate charged dependant on the risk

profile of the individual consumer – that is true for all markets

Before coming –understand the extent of the cultural differences: work ethic, politics. There will be significant financial investment which will grow out of all proportions if you decide to get out - be very cautious regarding local human investment

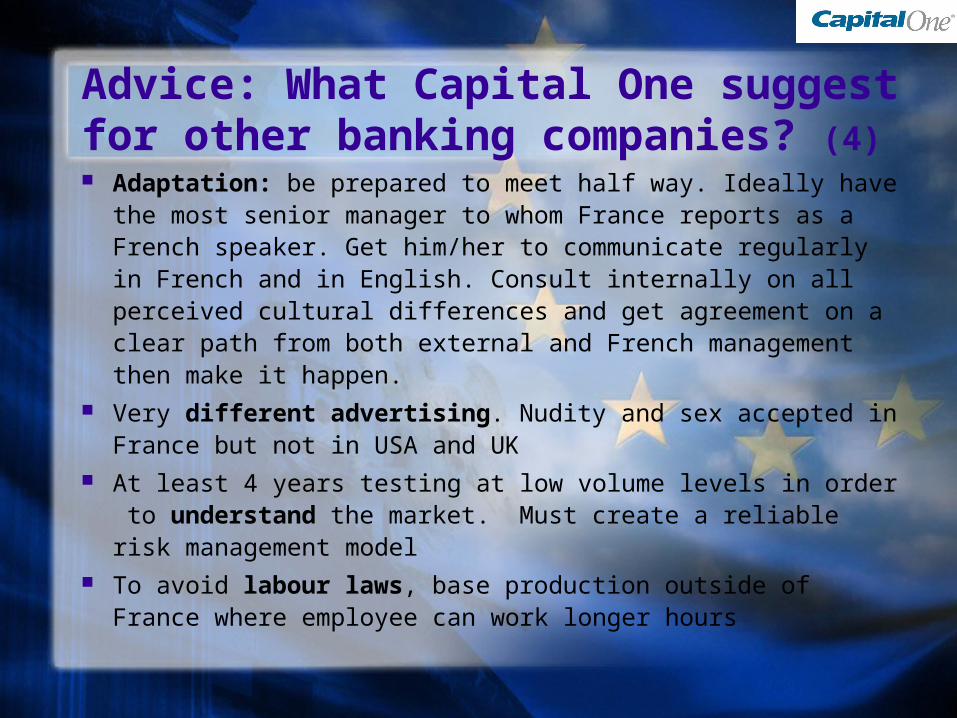

Adaptation: be prepared to meet half way. Ideally have the most senior manager to whom France reports as a French speaker. Get him/her to communicate regularly in French and in English. Consult internally on all perceived cultural differences and get agreement on a clear path from both external and French management then make it happen.

Very different advertising. Nudity and sex accepted in France but not in USA and UK

At least 4 years testing at low volume levels in order to understand the market. Must create a reliable risk management model

To avoid labour laws, base production outside of France where employee can work longer hours

Advice: What Capital One suggest for other banking companies? (4)

Introduction

Analysis

Recommendation

Conclusion

Introduction

Analysis

Recommendation

Conclusion

Conclusion

France offers a lot of benefits to foreign companies

Foreign companies need to be conscious of and

adapt to the French culture, norms and values

It is true that certain modifications should be made

(e.g. French Banks should be more accepting to

foreign banks entering the French Market)

And last but not least, DO NOT ENTER THE

FRENCH MARKET ALONE!

With thanks to:

Alan Wolfson, Former Managing Director, Capital One France

(7 Queen Alexandra Mansions,

3 Grape Street London WC28DX, UK)

Fergus Brownlee, Former Principal Managing Director and Executive Vice President, Capital One

Europe

(Streatley House, Streatley-on-Thames, Berkshire, RG89HY, UK)

Capital One