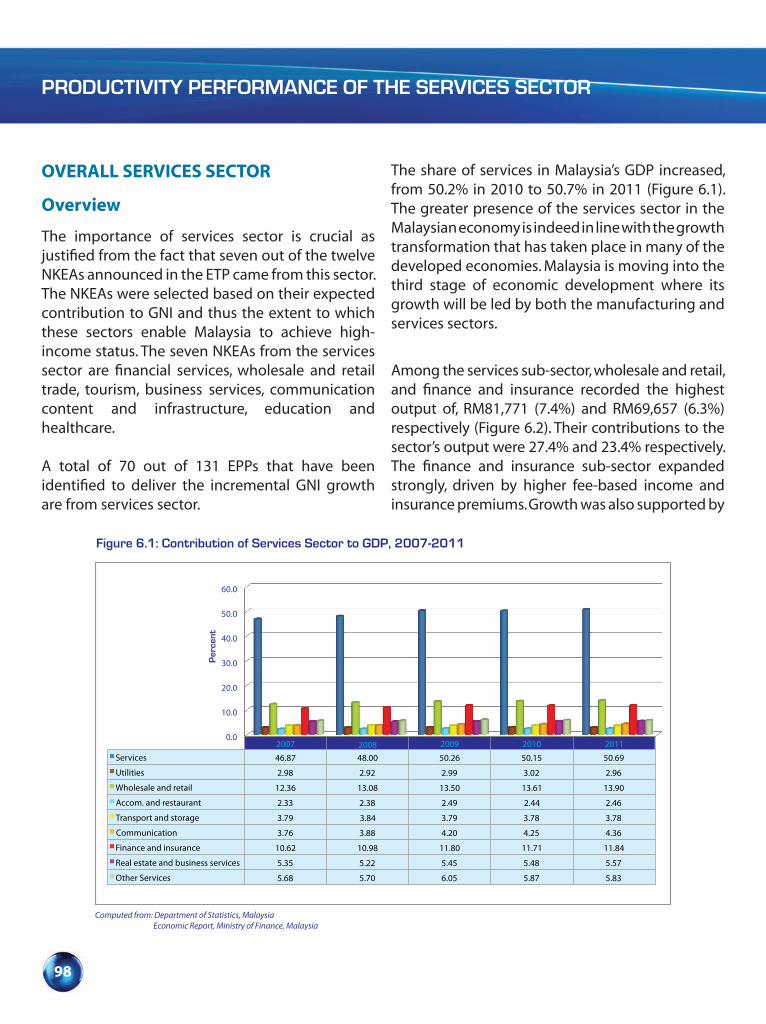

productivity performance of the services sector

TRANSCRIPT

MALAYSIA

MALAYSIA

STATUTORY REQUIREMENTS

In accordance with Section 7 of the Malaysia Productivity Council (Incorporation) (Amendment) Act 1991, Malaysia Productivity Corporation hereby publishes and submits to the Minister of International Trade and

Industry the status of productivity in Malaysia.

vi

“All things being equal, we need a bolder business community to achieve a high income

nation within the coming eight year timeframe. Considering the current pace can we

make it on time? More importantly, with the current rate of globalisation and growing

emerging economies, would the goalpost shift again?”

Malaysia’s economy continued to grow in 2011 with a GDP growth of 5.1% and employment growth of 0.6%. In tandem with this, the economy recorded a productivity growth of 4.6% to a productivity level of RM54,023. It is gratifying to note that Malaysia’s productivity had surpassed growth recorded by most OECD countries. Malaysia’s 4.6% productivity growth was ahead of Republic of Korea (2.1%), Finland (1.9%), USA (1.2%), UK (0.5%) and Japan (-0.2%).

According to the World Competitiveness Yearbook (WCY) 2011, Malaysia ranked among the top 20 countries with countries such as Canada, Denmark, Finland, Norway and Australia and ahead of China, New Zealand, South Korea and Japan.

There is a crucial need to continuously strive for higher productivity and raise the competitiveness of our economy. Our productivity level of USD14,217 was relatively lower than some OECD and Asian countries such as Korea (USD39,490), Singapore (USD55,702), Australia (USD58,683) and Hong Kong (USD65,174).

Intensified efforts to boost productivity growth by both the Government and industries based on technology and innovative transformation strategies are crucial to generate a quantum leap in productivity growth. The application of ICT-based technology at

MESSAGE FROM THE MINISTER OF INTERNATIONAL TRADE AND INDUSTRY MALAYSIA

vii

organisation level will further strengthen innovative efforts in production, services, marketing and ultimately, to the Nation. The Government will continue to assume a proactive role in creating an environment that serves the Nation’s drive for productivity. Some of the measures include the reduction in regulatory burden by modernising business regulation. The growth in productivity is critical to the success of the Economic Transformation Programme.

This Productivity Report 2011/2012 will be useful to decision makers in the public and private sectors; including investors, academicians and the business community at large. I would strongly encourage the public and private sector to use this Report as a reference for strategic planning and policy formulation to ensure that productivity is continuously enhanced at company, industry and national levels.

DATO’ SRI MUSTAPA MOHAMED

Minister of International Trade and Industry

Malaysia

viii

STATEMENT BY THE CHAIRMAN

“The future of productivity growth in Malaysia will depend on the capability to make more

productive use of skilled labour, improved innovative capacity of firms, facilitate the shift of

capital and other resources to the most productive sectors of the economy and reduced

regulatory barriers and simplify doing business through modernisation of business

regulatory review.”

This Productivity Report is the 19th edition published by MPC and provides a comprehensive analysis on productivity performance of key economic sectors. Three new chapters have been incorporated into this Report covering productivity initiatives to enhance national competitiveness ranking, modernising business regulation, enterprise innovation and business excellence.

Productivity growth is the impetus towards raising the living standards of an economy over the long-term. It is also a key indicator of the overall competitiveness and innovation of an economy. Productivity reflects the efficiency of a Nation’s economic system and the effectiveness of its economic policies. The strong economic fundamentals resulting from improved Government efficiency through its regulatory review and modernising business initiatives and improvement in the firm’s efficiency have enabled the economy to continue growing despite the challenging global economy that affected Eurozone, USA and Japan.

Malaysia recorded a productivity growth of 4.6% in 2011. The growth was broad-based across all major economic sectors except mining, which recorded a negative growth.

The agriculture sector recorded the highest productivity growth followed by the services sector. It is gratifying to note that the Malaysian productivity growth was higher than many OECD countries and the Asian developed economies such as Singapore, Taiwan, Hong Kong and Korea.

ix

Besides analysis on productivity performance at industry, sectoral, national and international levels, this Report also includes the achievements of some of the Entry Point Projects (EPPs) under the National Key Economic Areas (NKEAs), best practices observed and the proposed strategic directions for the various economic sectors.

This Report also provides key insight on Malaysia’s competitiveness ranking in comparison with major world players. Government initiatives in reducing the regulatory barriers and facilitating doing business through modernising business regulation as well as initiatives taken by the industries towards applying new technologies, adopting new business processes and upgrading workforce skills will also be discussed in this Report.

MPC continues to receive support, advice and contributions from various organisations and individuals in the preparation of this Report. On behalf of the MPC, I would like to thank all the various ministries and agencies, the experts for their contribution and the staff of MPC for their dedication and many others, who have contributed in one way or another to produce this Report.

TAN SRI AZMAN HASHIMChairman Malaysia Productivity Corporation

x

MALAYSIA PRODUCTIVITY CORPORATION

Malaysia Productivity Corporation (MPC) was established to assume an important role in the enhancement of productivity and quality of the country towards achieving a higher national economic growth.

To realise the above, MPC has formulated a strategic operation based on the following vision, mission and objectives.

VISION

The leading organisation in productivity enhancement for global competitiveness and innovation

MISSION

To deliver high impact services towards achieving performance excellence through innovation for the

betterment of life

OBJECTIVES

Our corporate objectives are:

Providing value-added information on productivity, quality, competitiveness and best practices through research

activities and databases;

Developing human capital and organisational excellence for building a knowledge-based society through training,

systems development and best practices; andNurturing innovative and creative culture for productivity and competitiveness through partnership programmes.

xi

CONTENTS

MESSAGE FROM MINISTER vi

STATEMENT BY THE CHAIRMAN viii

MALAYSIA PRODUCTIVITY CORPORATION Vision, Mission and Objectives x

REPORT HIGHLIGHTS xvii

PART 1: ENHANCING A PRODUCTIVE AND COMPETITIVE ECONOMY

Chapter 1: Productivity Performance of Malaysia Overall Productivity Performance 2Sectoral Productivity Performance 3

Services Sector 3Manufacturing Sector 9Agriculture Sector 9Construction Sector 10Mining Sector 10Way Forward 12Outlook for 2012 13

Chapter 2: Sources of Malaysia’s Economic GrowthOverview 18Sources of Economic Growth 18TFP of Selected Economic Growth 20International Total Factor Productivity Comparison 22Sources of Output Growth in Selected Countries 22Total Factor Productivity Growth for Future Direction 23Box 2.1: Productivity Measurement Using the KLEMS Approach 26Box 2.2: Wage Management Framework 28

Chapter 3: Malaysia and International Competitiveness Overview 32The Importance of Competitiveness 32Competitiveness Definitions 32Competitiveness Model 32Malaysia’s Overall Competitiveness Performance 33

xii

CONTENTS

Malaysia’s Performance with Selected Countries 35Economic Performance 36Government Efficiency 38Business Efficiency 38Infrastructure 40

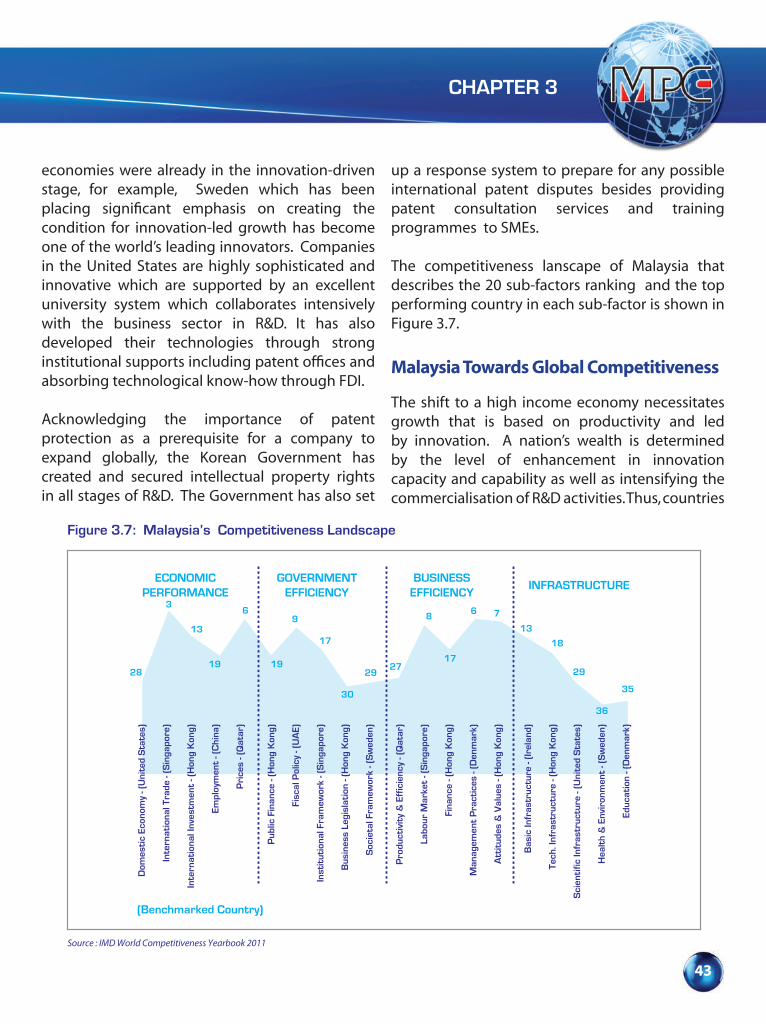

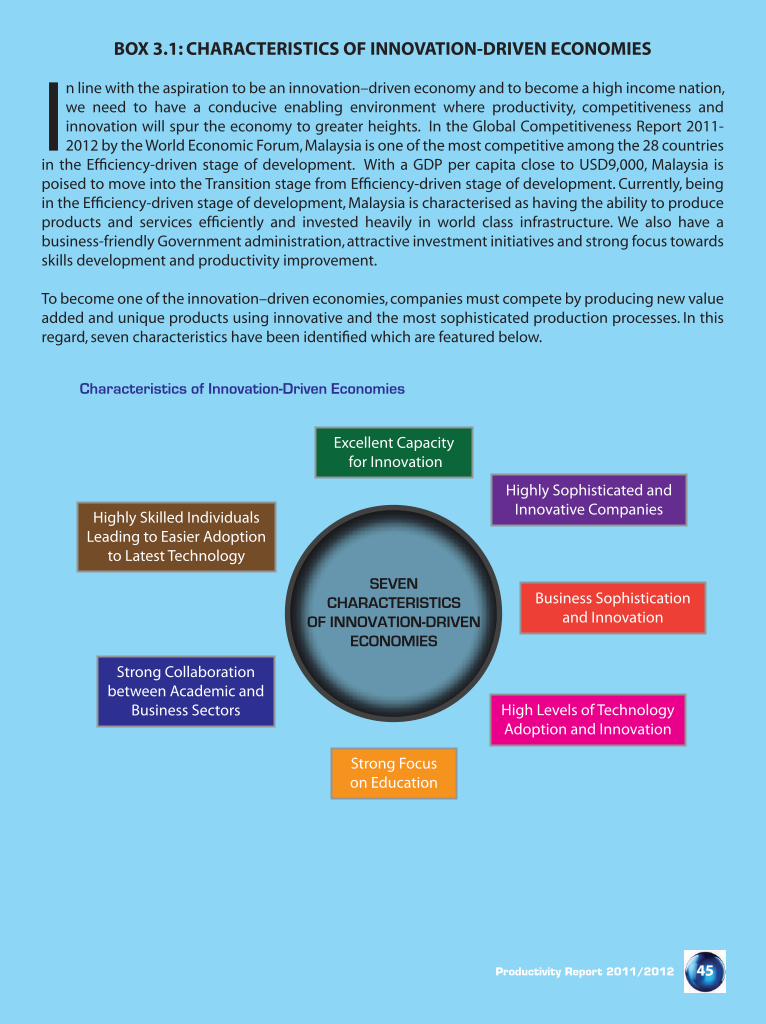

Malaysia Towards Global Competitiveness 43Box 3.1: Characteristics of Innovation-Driven Economies 45

PART 2: TRANSFORMATION TOWARDS BUSINESS EXCELLENCE

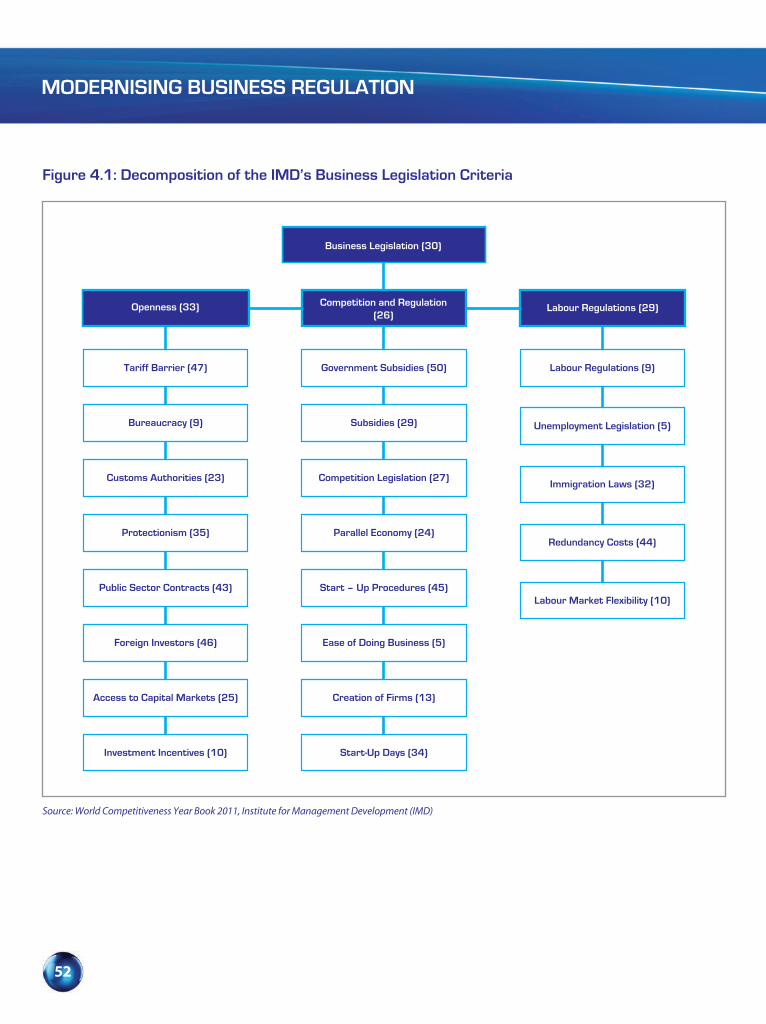

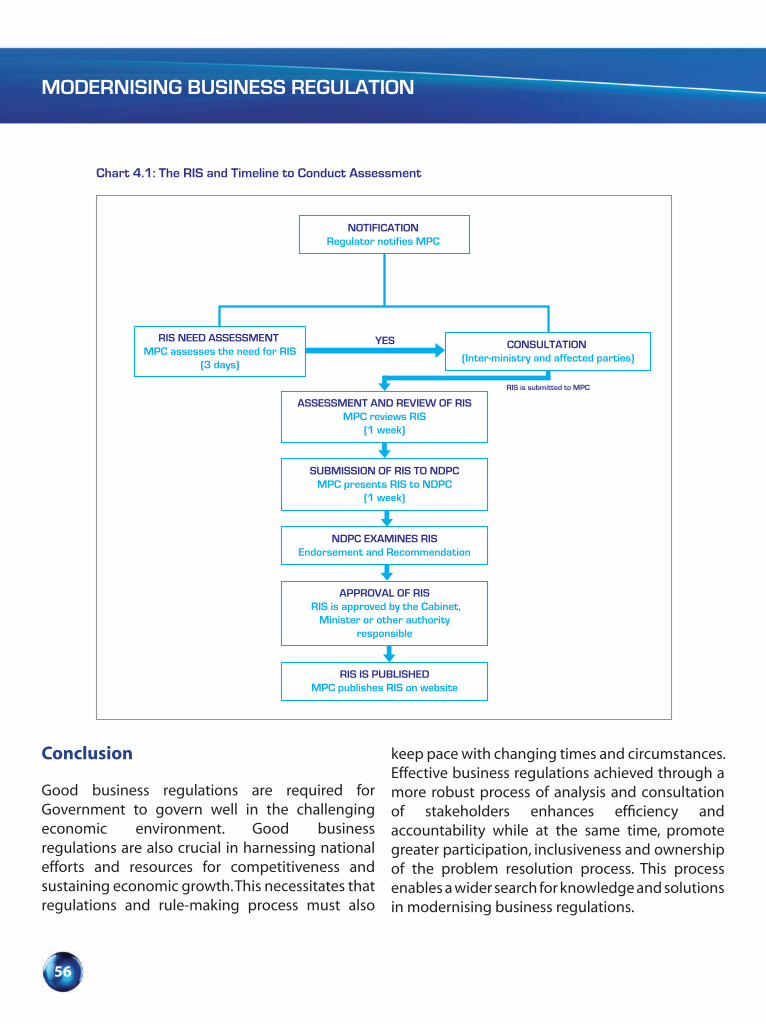

Chapter 4: Modernising Business Regulation Overview 50The Rationale of Regulatory Review 50International Comparison on Regulatory Performance 51Best Practices in Regulation Development Process 51Best Practice Regulation in Malaysia 54Conclusion 56Box 4.1: Enhancing Malaysia’s Competitiveness Through Modernising Business Regulation 57Box 4.2: Improving Efficiency in Dealing with Construction Permits in Kuala Lumpur 58Box 4.3: Modernising Trade Facilitation Through Business Process Improvement 62

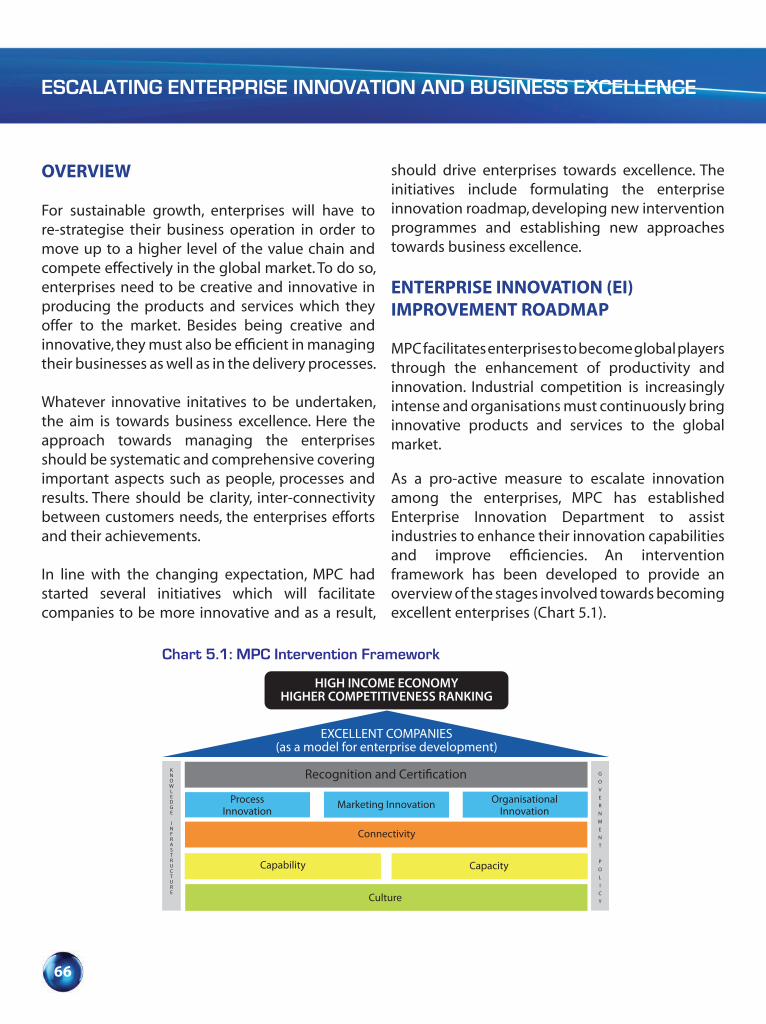

Chapter 5: Escalating Enterprise Innovation and Business Excellence Overview 66 Enterprise Innovation (EI) Improvement Roadmap 66

Intervention Programmes 70Developing a Global Perspective 72

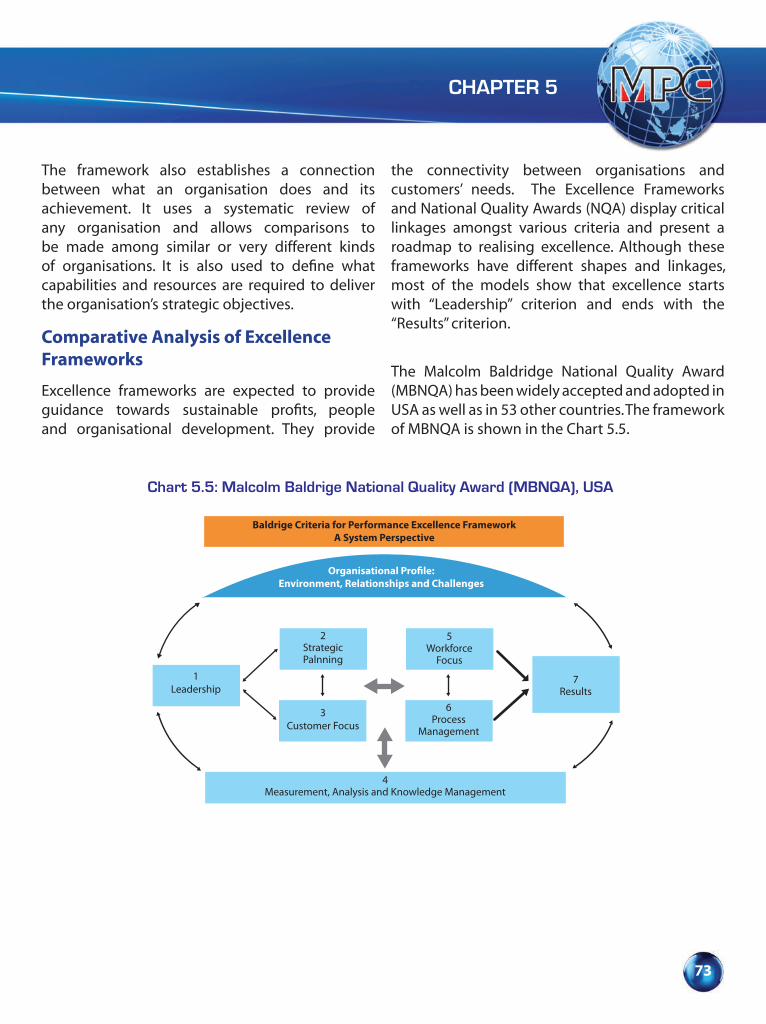

Business Excellent Framework 72Comparative Analysis of Excellence Frameworks 73New Malaysia Business Excellence Framework (MBEF) 76Benefits of Malaysia Business Excellence Framework (MBEF) for Organisations 77Business Excellence (BE) Community 78

Box 5.1: Knowledge Content Study in Enterprises (MyKE) 80Box 5.2: History and Development of ICQCC 83Box 5.3: Moving Quality Environment (QE)/5S to Lean Management 87Box 5.4: Green Productivity (GP) for Sustainable Development 90Box 5.5: Enhancing Productivity through Material Flow Cost Accounting (MFCA) 92Box 5.6: Achieving Excellence through Quality Management Excellence Award (QMEA) 94

xiii

CONTENTS

PART 3: SYNERGY THROUGH PUBLIC-PRIVATE COLLABORATION

Chapter 6: Productivity Performance of the Services Sector Overview 98Productivity Performance 99Total Factor Productivity 100 Strategies and Outlook 103Logistic Services 103

Overview 103Productivity Performance 104Innovation and Best Practices 105Progress of Entry Point Projects (EPPs) 106Strategies and Outlook 107

Information and Communication Technology (ICT) Services 109Overview 109Productivity Performance 109Innovation and Best Practices 110Progress of Entry Point Projects (EPPs) 111Strategies and Outlook 114

Wholesale and Retail Trade Services 115Overview 115Productivity Performance 116Innovation and Best Practices 117Progress of Entry Point Projects (EPPs) 118Strategies and Outlook 119

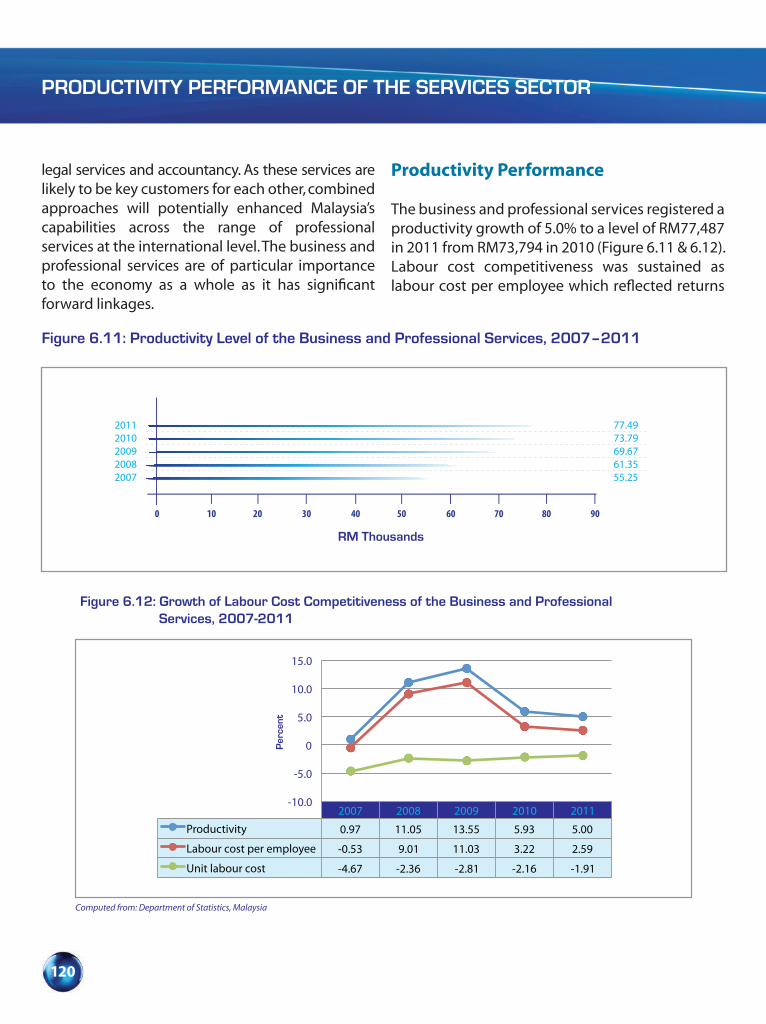

Business and Professional Services 119Overview 119Productivity Performance 120Innovation and Best Practices 121Progress of Entry Point Projects (EPPs) 121Strategies and Outlook 122

Tourism Services 122Overview 122

xiv

CONTENTS

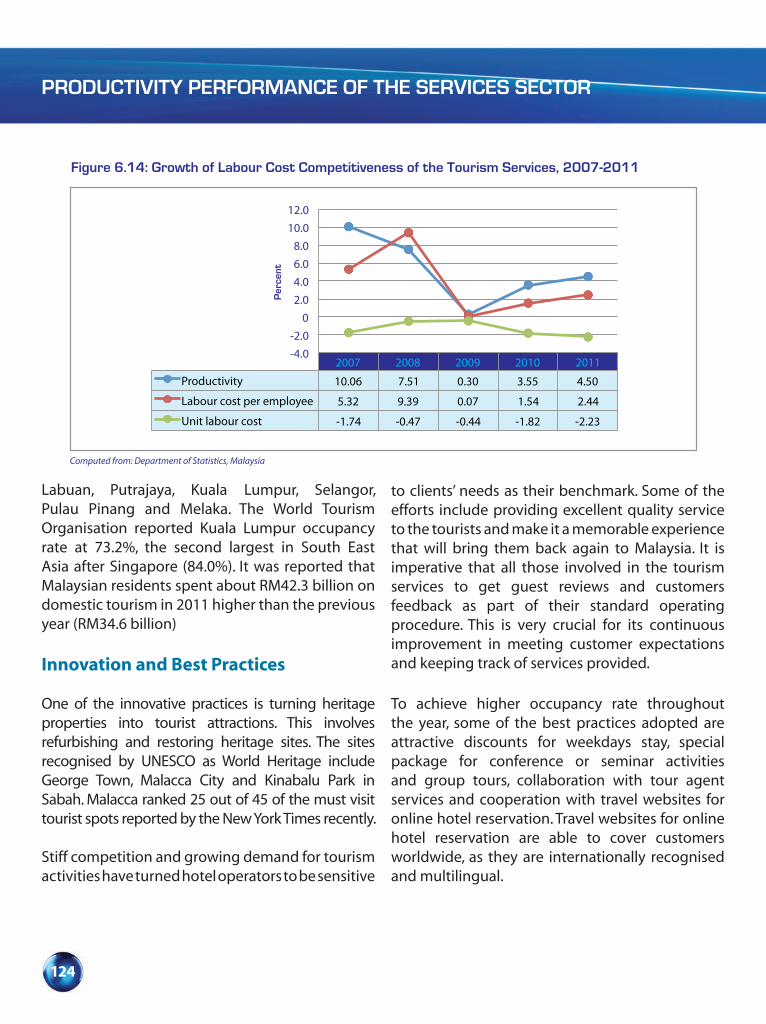

Productivity Performance 123Innovation and Best Practices 124Progress of Entry Point Projects (EPPs) 125Strategies and Outlook 125

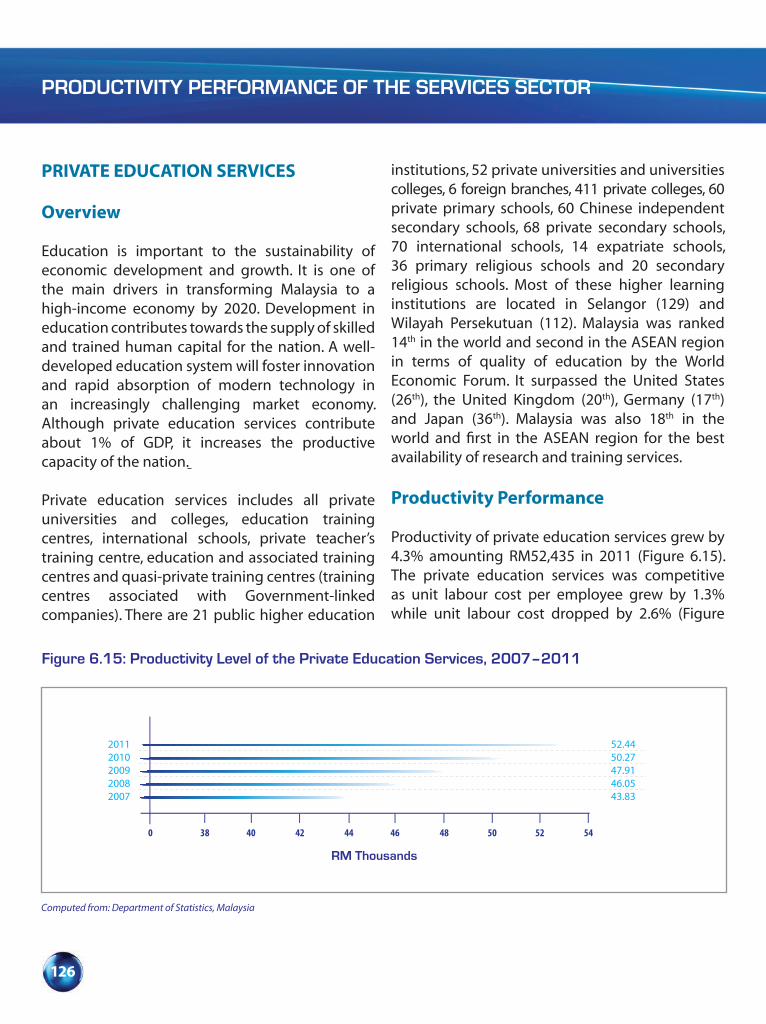

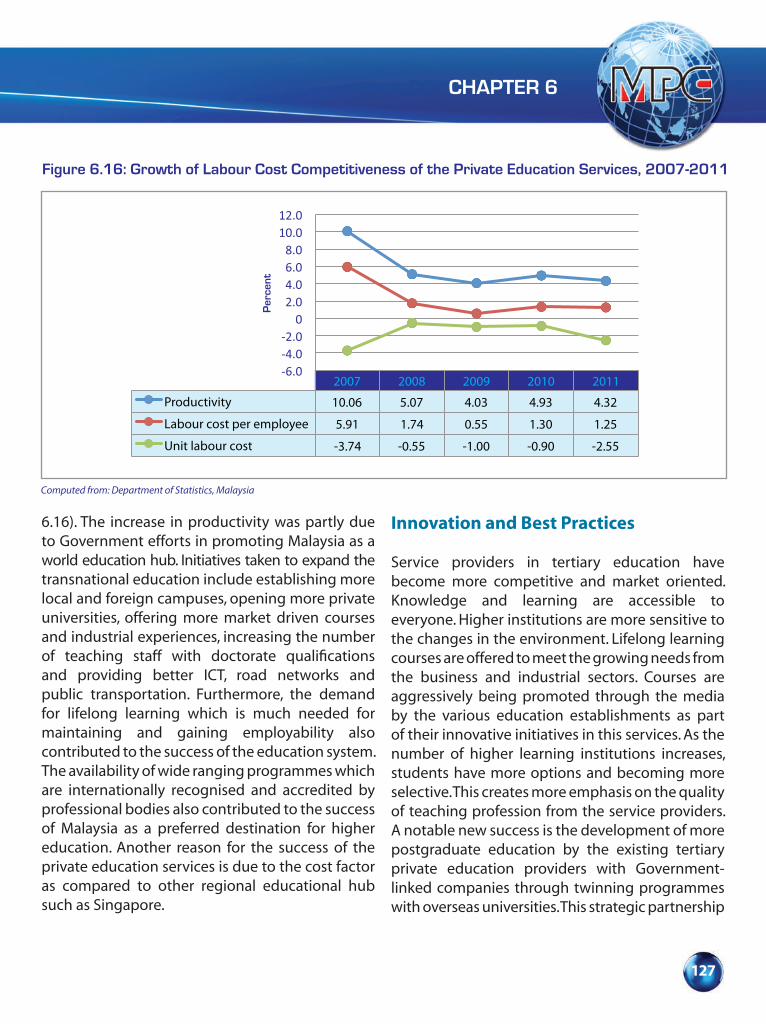

Private Education Services 126Overview 126Productivity Performance 126Innovation and Best Practices 127Progress of Entry Point Projects (EPPs) 128Strategies and Outlook 129

Healthcare Services 130Overview 130Productivity Performance 130Innovation and Best Practices 132Progress of Entry Point Projects (EPPs) 133Strategies and Outlook 134

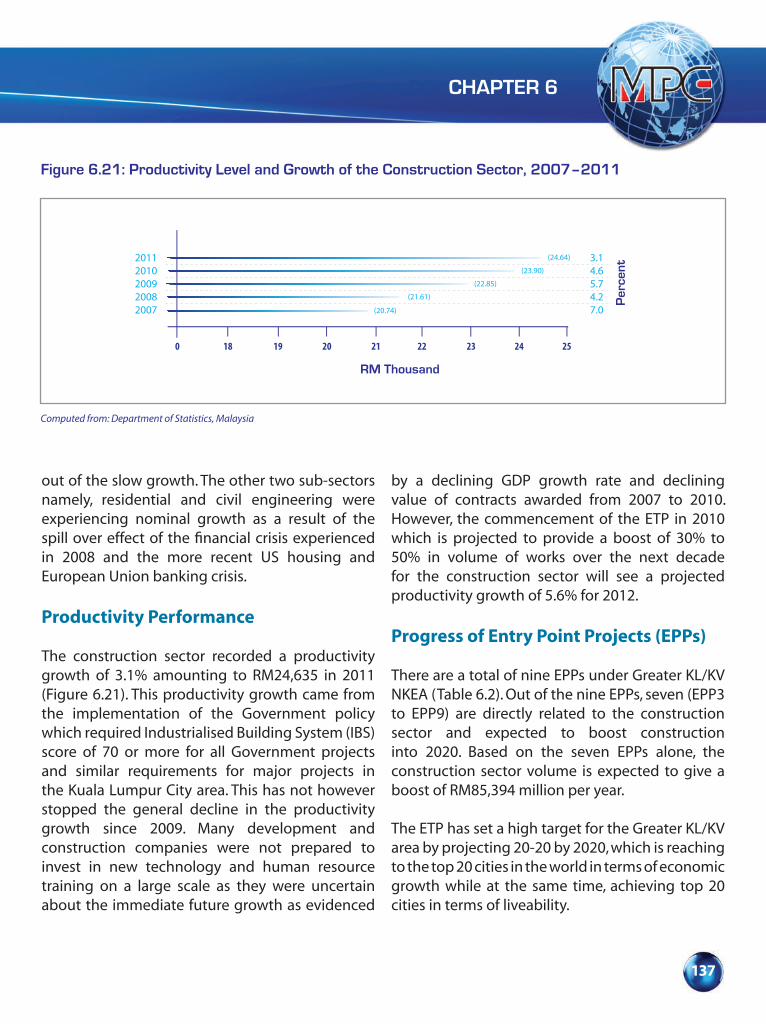

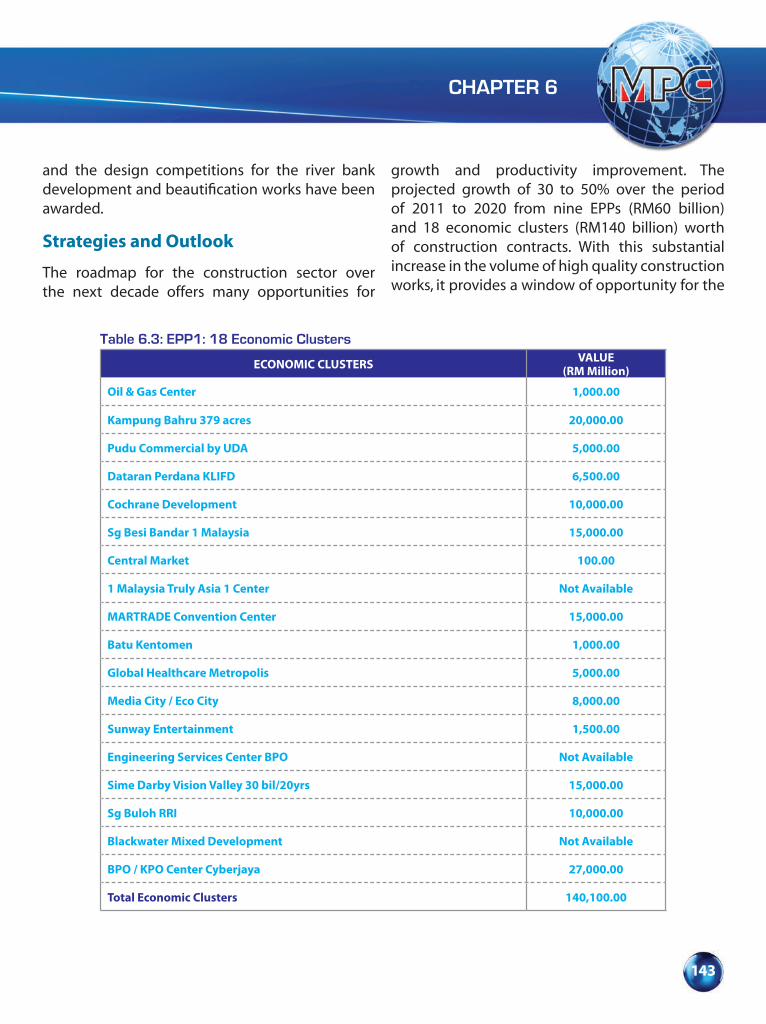

Construction Services 135 Overview 135Productivity Performance 137Progress of Entry Point Projects (EPPs) 137Strategies and Outlook 143

Box 6.1: Benchmarking for Education Excellence 146Box 6.2: Measuring Performance of Private Hospitals 148Box 6.3: Building Information Modelling for Greater Productivity of the

Construction Sector 150

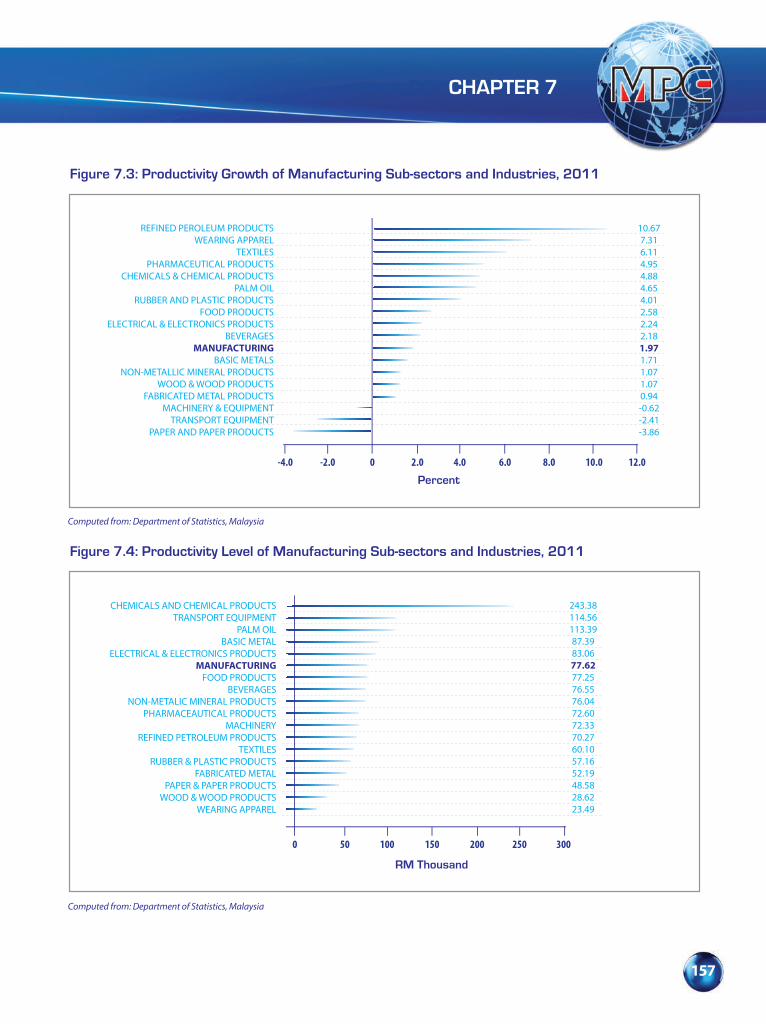

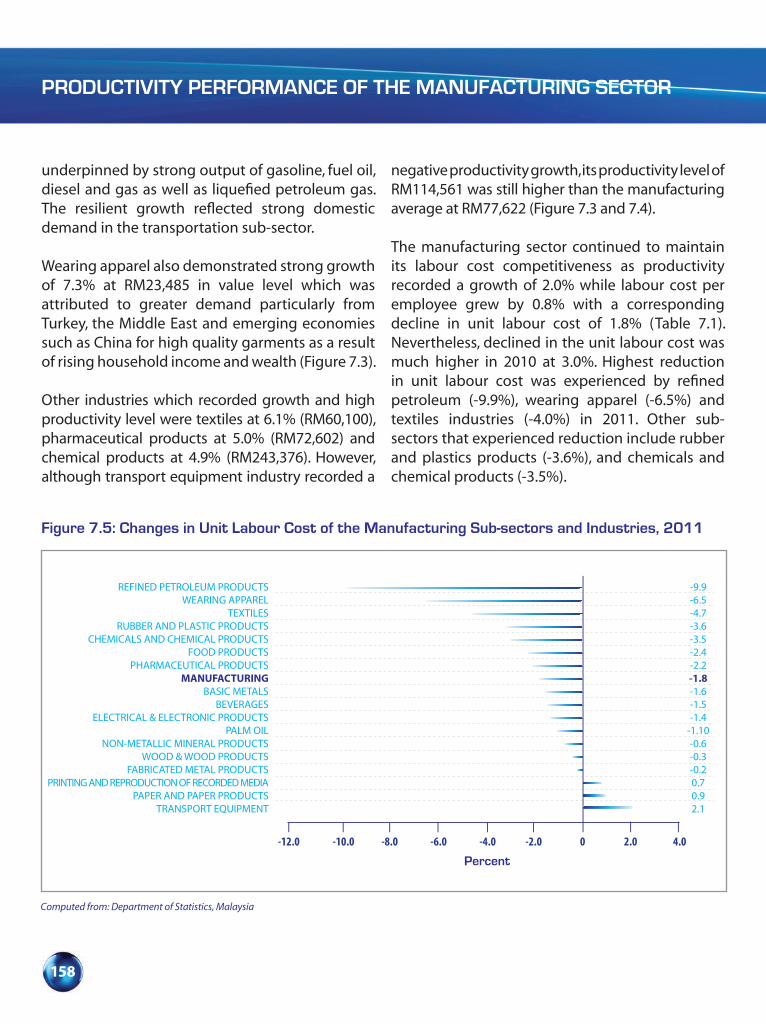

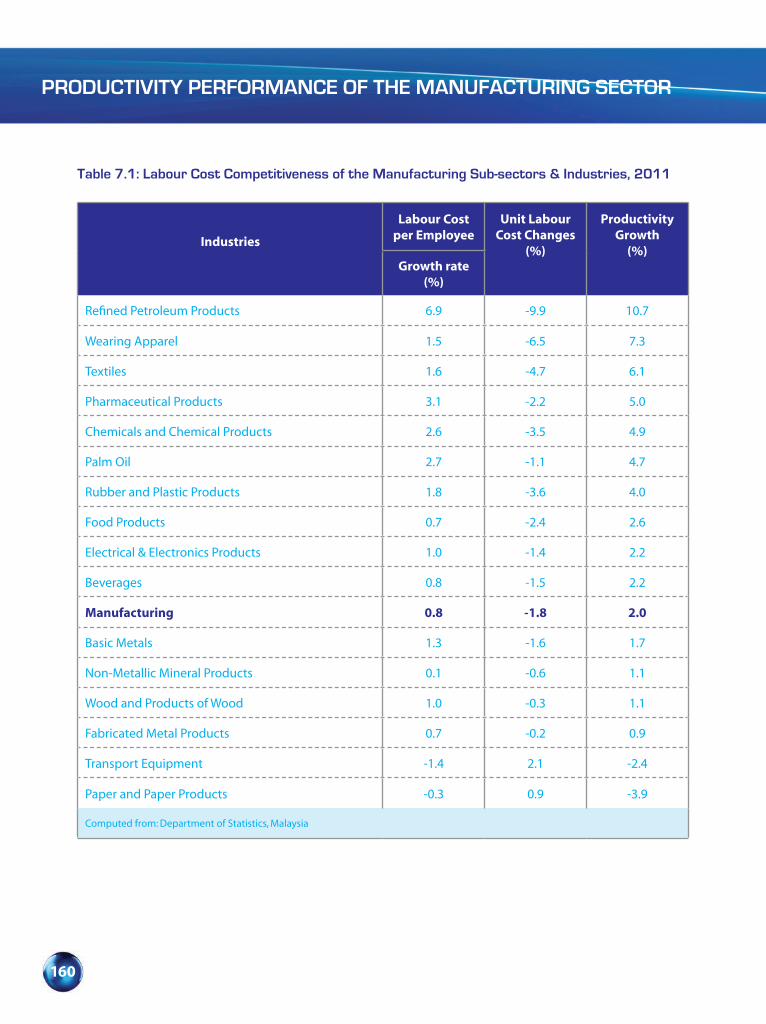

Chapter 7: Productivity Performance of the Manufacturing Sector Overview 154Productivity Performance of Sub-Sectors and Industries 156NKEAs Sub-Sector’s Performance Analysis 159Total Factor Productivity (TFP) of Selected Manufacturing Sub-Sectors 2007-2011 168Innovation and Best Practices 169Strategies and Outlook 170Box 7.1: Transforming the Traditional Job into Modern Job 172

xv

CONTENTS

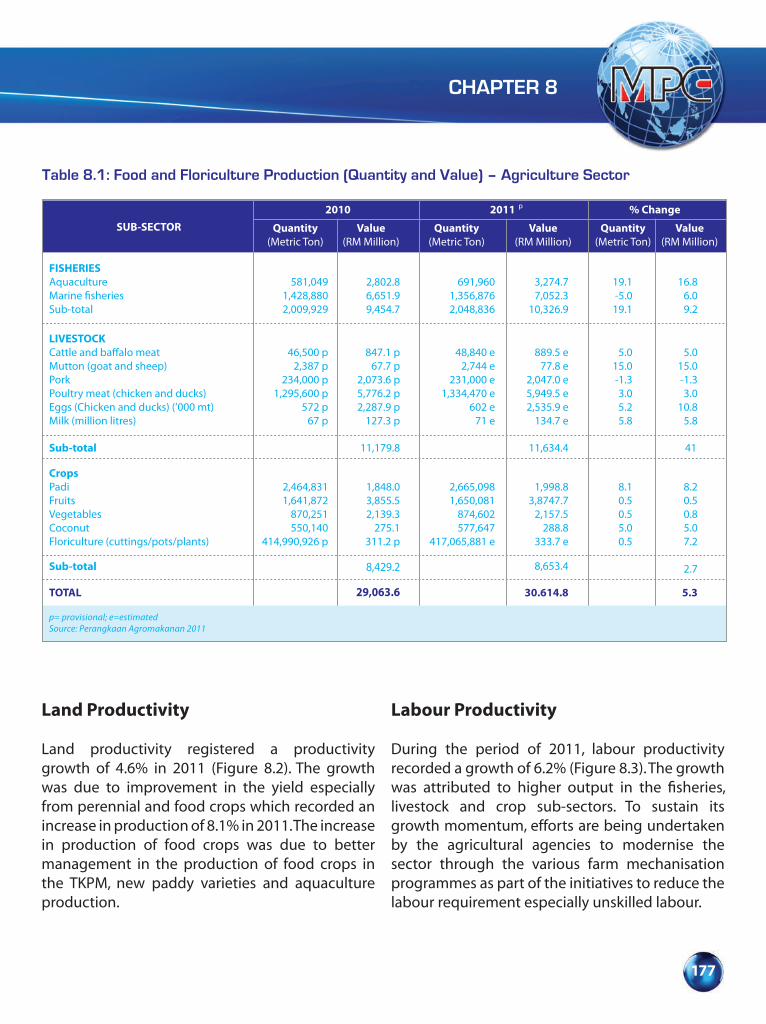

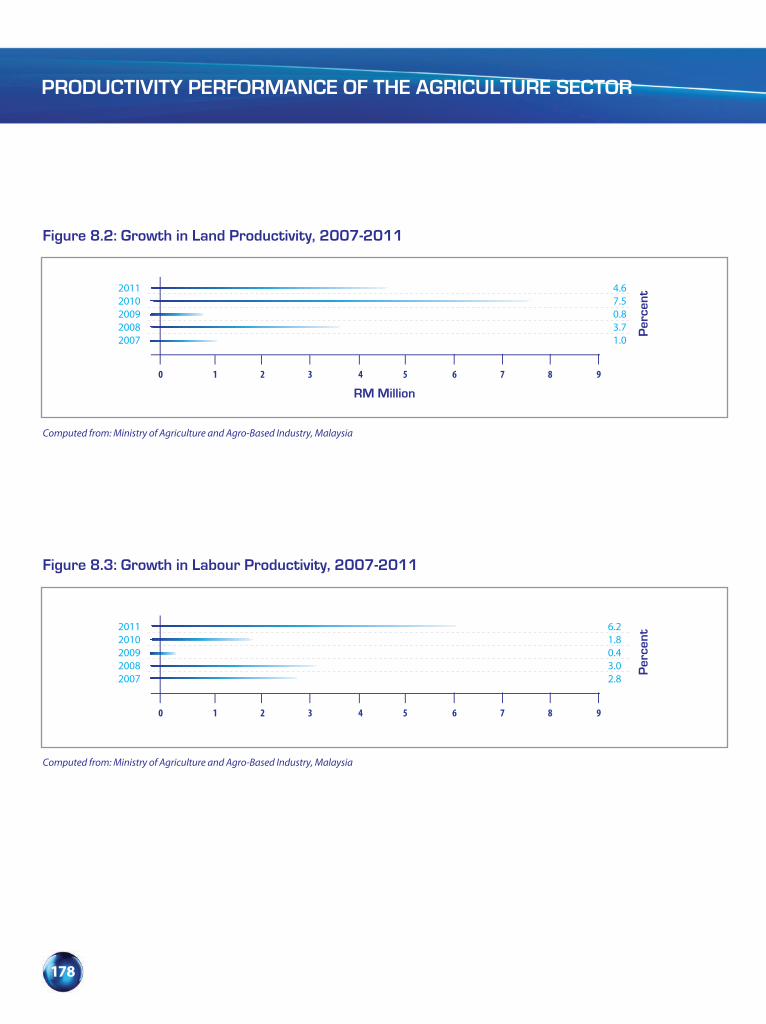

Chapter 8: Productivity Performance of the Agriculture Sector Overview 176Productivity Performance 176

Land Productivity 177Labour Productivity 177Capital Productivity

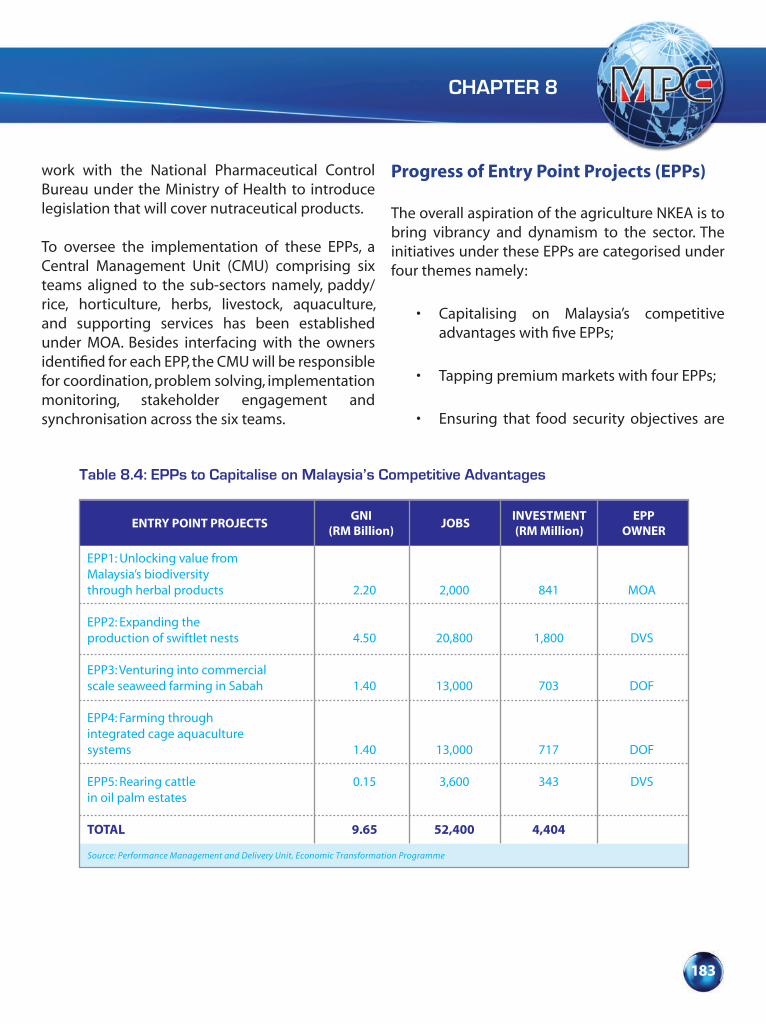

International Agricultural Productivity Comparison 179Human Resource Capacity Development 180Innovation and Best Practices 181Progress of Entry Point Projects (EPPs) 183

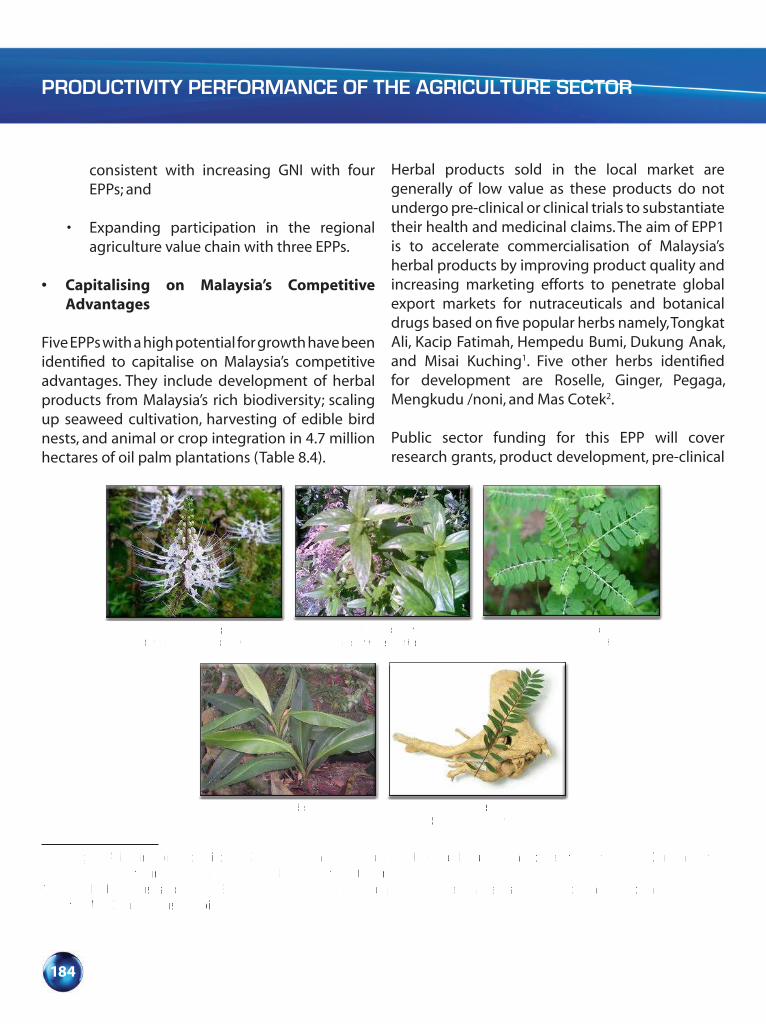

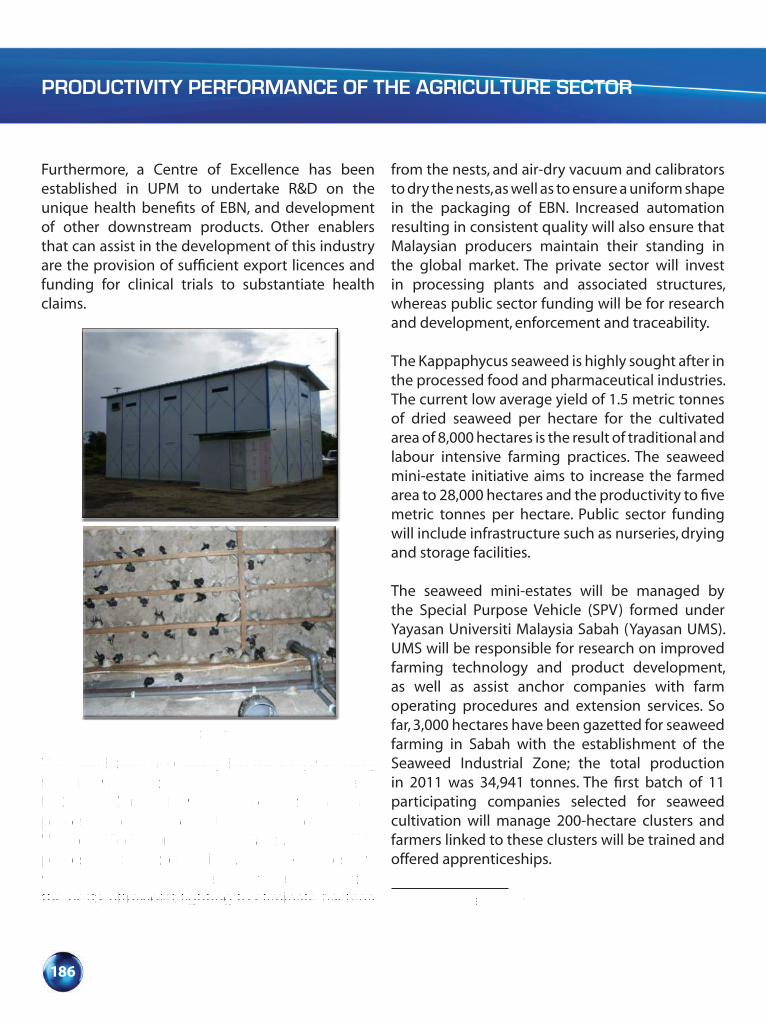

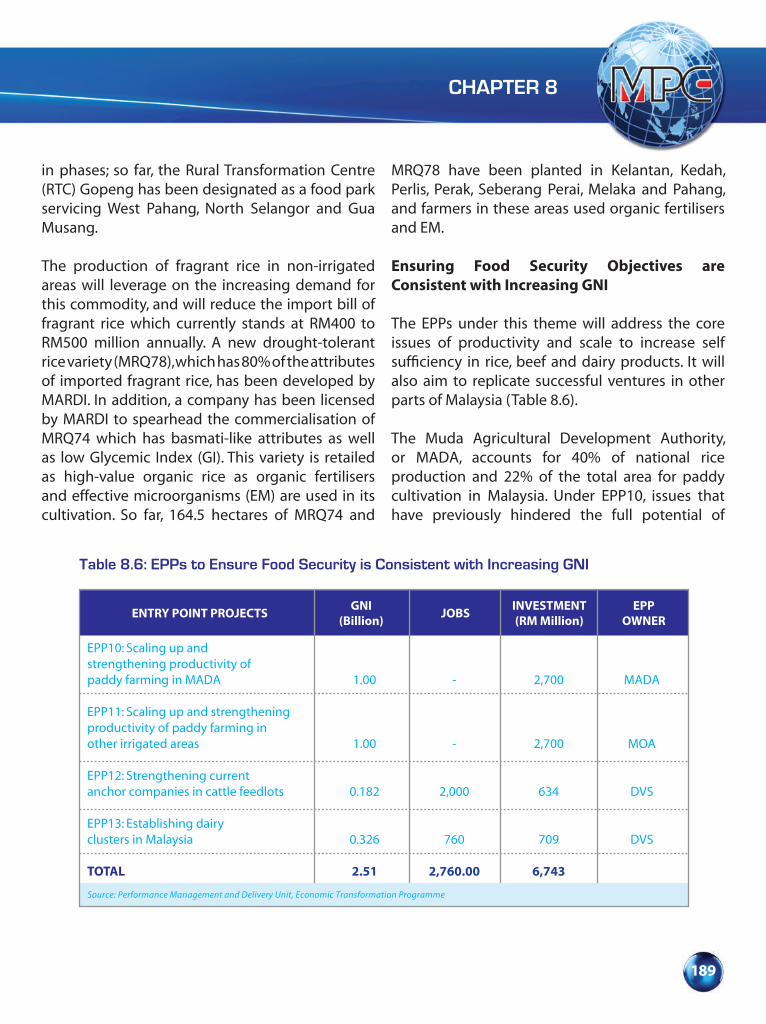

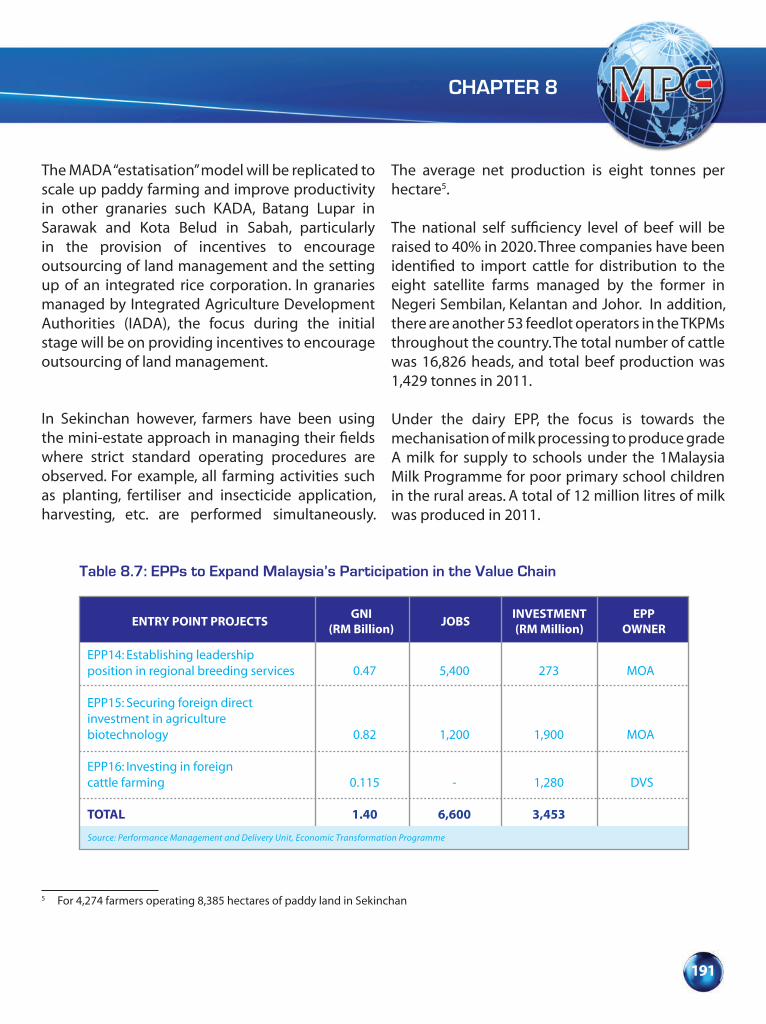

Capitalising on Malaysia’s Competitive Advantages 184Tapping Premium Markets 187Ensuring Food Security Objectives are Consistent with Increasing GNI 189Expanding Malaysia’s Participation in the Regional Value Chain 192

Strategies and Outlook 192Box 8.1: Innovative Farming Practices: “From Ideas to Reality” 194

PART 4: SUSTAINING THE QUALITY OF LIFE

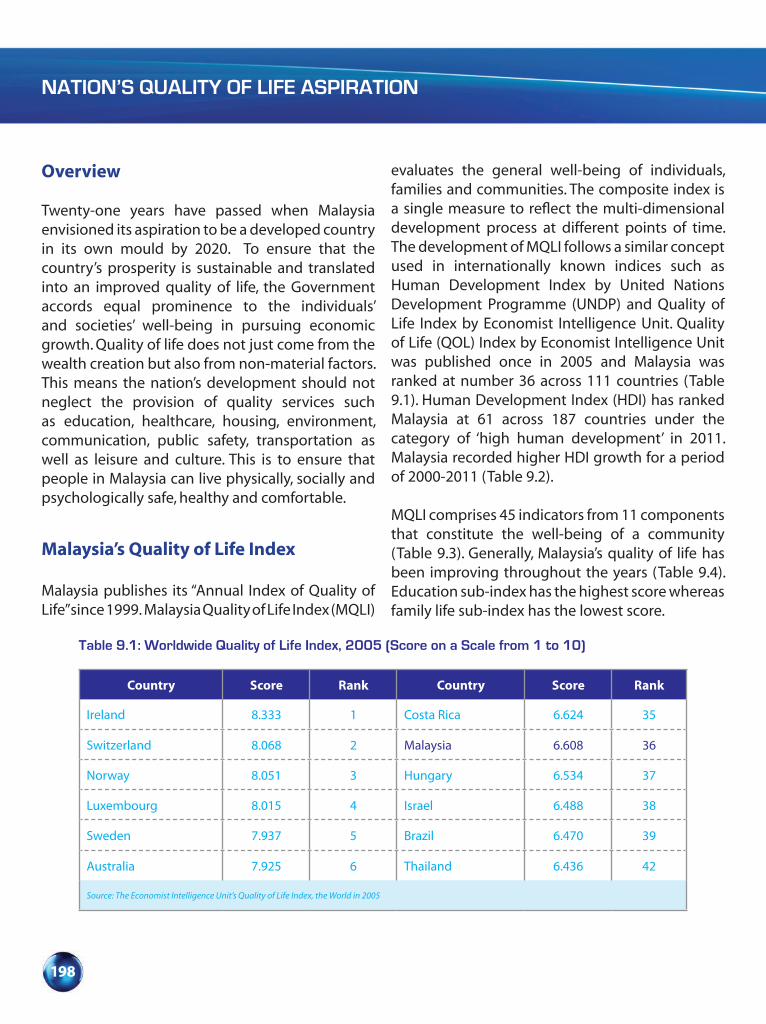

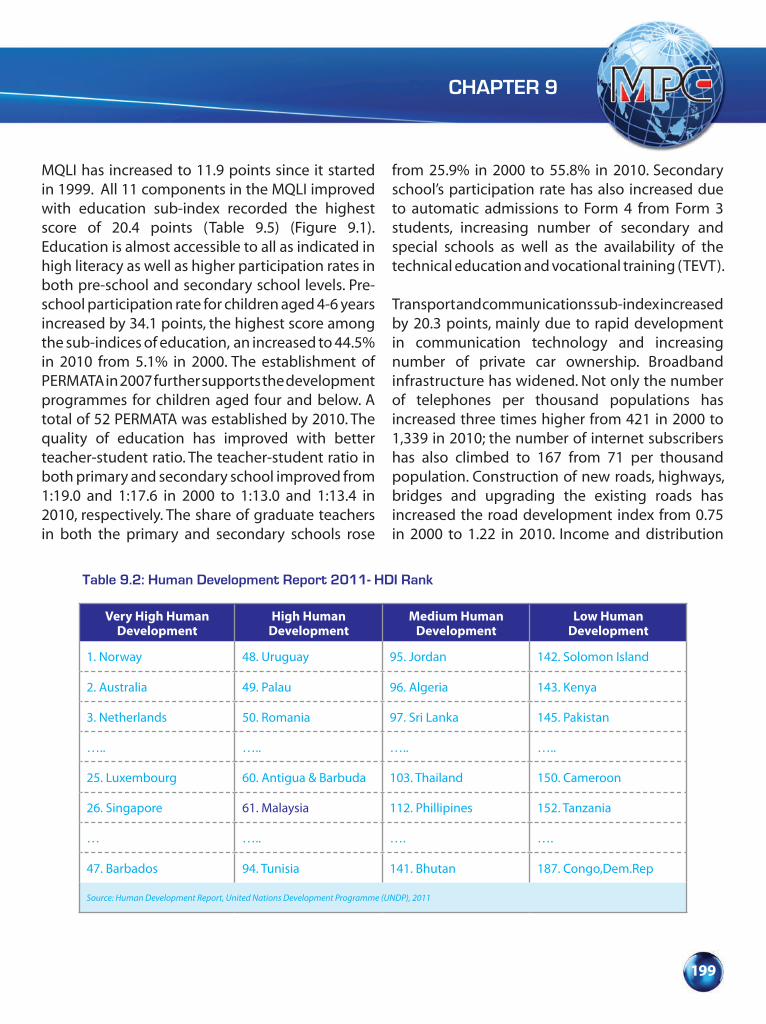

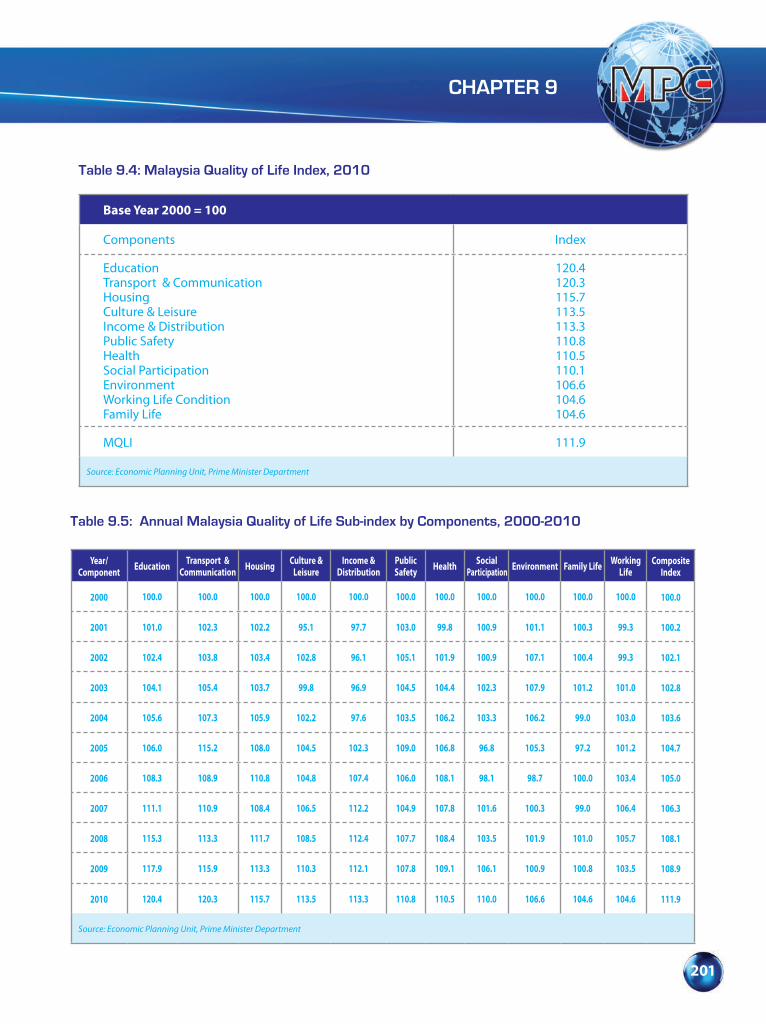

Chapter 9: Nation’s Quality of Life AspirationOverview 198Malaysia’s Quality of Life Index 198The Quality of Work Life (Malaysia) 2012 204

Theme 1: Perceptions of Organisation and Workplace 204Theme 2: Management and Leadership Styles 206Theme 3: Working Hours and the Effects of Working Hours

Have on Managers 210Theme 4: Strategic Performance of Organisations 210

Way Forward of Quality of Life 211MPC Way Forward 211

Enhancing Malaysia’s Competitiveness 212Modernising Business Regulations 213Expediting Enterprise Innovation 214Fast-Tracking Towards Business Excellence 214Institutionalising Knowledge Management Culture 215

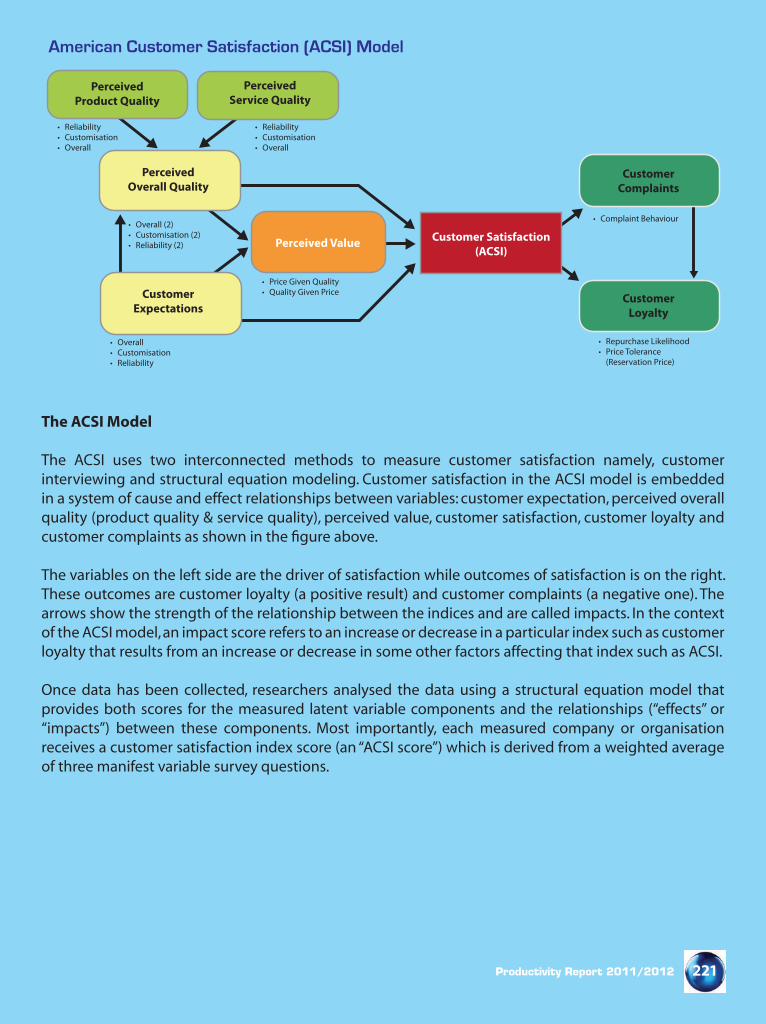

Box 9.1: Best Practices in Work Life Balance 218Box 9.2: National Customer Satisfaction Index 219

xvi

CONTENTS

APPENDICES Appendix A: Productivity 226Appendix B: Innovation 232Appendix C: Competitiveness 233Appendix D: Regulatory Review 235Appendix E: Technical Notes 239Appendix F: The Contribution by Sub-Sectors 2011 245

MPC BOARD OF DIRECTORS 246

MPC CONSULTATIVE PANELS 247

PARTNERSHIP 251

MPC MANAGEMENT TEAM 252

MPC OFFICE ADDRESSES 253

REFERENCES 255

ACRONYMS AND ABBREVIATIONS 257

INDEX 260

xvii

REPORT HIGHLIGHTS

PRODUCTIVITY PERFORMANCE OF MALAYSIA

Malaysia’s Productivity Performance

Productivity measurement using the ratio of output to the number of employees has reached 68% of the

target level of productivity in 2020. The target level of national productivity for a high income economy

by 2020 is RM78,800. If the projected growth is sustained at a rate of more than 4% per annum, the

target level of productivity can be achieved by 2020. Malaysia’s productivity performance grew by 4.6%

in 2011. Productivity level had increased from RM51,674 in 2010 to RM54,023 in 2011.

International Productivity Performance

Malaysia recorded a higher productivity growth as compared to most OECD countries such as Korea

(2.1%), Finland (1.9%) and Canada (0.6%). However, the growth was lower compared with emerging

countries such as the People’s Republic of China (8.7%), Indonesia (5.0%) and India (4.9%).

Among OECD countries, Malaysia’s productivity level of USD14,217 was lower than Ireland (USD96,559),

United States (USD92,369), Japan (USD74,258) and South Korea (USD34,490). Among selected Asian

countries, Malaysia registered a productivity level higher than Thailand (USD4,801), China (USD4,443), the

Philippines (USD3,341), Indonesia (USD3,040) and India (USD3,034). However, Malaysia’s productivity

level was lower than Hong Kong (USD65,174), Singapore (USD55,702) and Taiwan (USD43,827).

Sources of Growth

The main contributor to economic growth is capital (40.0%), followed by Total Factor Productivity (TFP)

growth (32.7%) and labour (27.3%). Malaysia has been using the KLEMS (Capital, Labour, Energy,

Materials & Services) approach to measure the growth of Total Factor Productivity (TFP) as practiced

by European Union (EU), Japan, Korea and the United States. KLEMS analyses each factor input such

as capital labour, energy, intermediate input, materials and services in terms of quality and efficiency.

Malaysia recorded a TFP growth rate of 1.7% in 2011, lower than Singapore (2.4%), South Korea (2.4%)

and India (2.3%).

xviii

Modernising Business Regulation

The burden of regulation on business was estimated at RM15 billion in 2011 (2.5% of GDP). Most

countries have set a 25% reduction in regulation cost as their targets. Malaysia plans to reduce by

RM 1 billion cost of unnecessary regulation a year until 2015. Programs involving Government and

private agencies have been implemented under the supervision of the Task Force to Facilitate Business

(PEMUDAH) to achieve the target reduction in regulatory burden.

A framework for quality management regulation and Best Practice Regulation Handbook was published to

encourage competitiveness, innovation, investment and skills that will contribute towards improvement.

Quality of Life

Quality of Life Index measures the qualitative aspects of productivity which complements the quantitative

measurement of the economy such as labor productivity. Malaysia Quality of Life Index, reached a score

of 111.9 points (based on year 2000 = 100). Happiness World Report compiled by the United Nations

also placed Malaysia in the second position among Southeast Asia countries behind Singapore and was

ranked 51 among 156 countries in the world.

Quality of Working Life includes having a more conducive working environment, job satisfaction and

individual well-being. The preliminary study found that more than 70% of employees love their work,

had high moral and showed loyalty and high job aspirations. Positive factors which support the welfare

and quality of work include guaranteed work, creativity and employee recognition and strong leadership,

vision, respect and setting a good example.

Outlook for 2012

The economy is anticipated to sustain its growth momentum in 2012 where productivity is expected to

grow by more than 4.0%. The growth in productivity is expected to benefit from the implementation of

some of the EPPs introduced under the NKEAs where the private sector will provide the impetus in driving

economic expansion while the Government will provide the supportive role in improving productivity.

xix

The productivity of the services sector is expected to grow by 4.9% in 2012 lead by communication and

other services sub-sectors. Growth in the communication sub-sector will be supported by advancement in

wireless technology, expansion in High-Speed Broadband infrastructure as well as Government initiatives

to promote broadband usage through-out the country.

The manufacturing sector’s productivity is targeted to grow moderately by 2.3% in 2012 caused by

the spillover effect of the Euro debt crisis and the unresolved structural adjustments experienced in

the US economy. However, the sector will also be supported by continuous growth in the domestic-

oriented industries attributed by the recovery of transport equipment sub-sector and expansion in the

construction-related cluster.

ENHANCING A PRODUCTIVE

AND COMPETITIVE

ECONOMYPART

1

CHAPTER 1

PRODUCTIVITY PERFORMANCE OF MALAYSIA

PRODUCTIVITY PERFORMANCE OF MALAYSIA

2

PRODUCTIVITY PERFORMANCE OF MALAYSIA

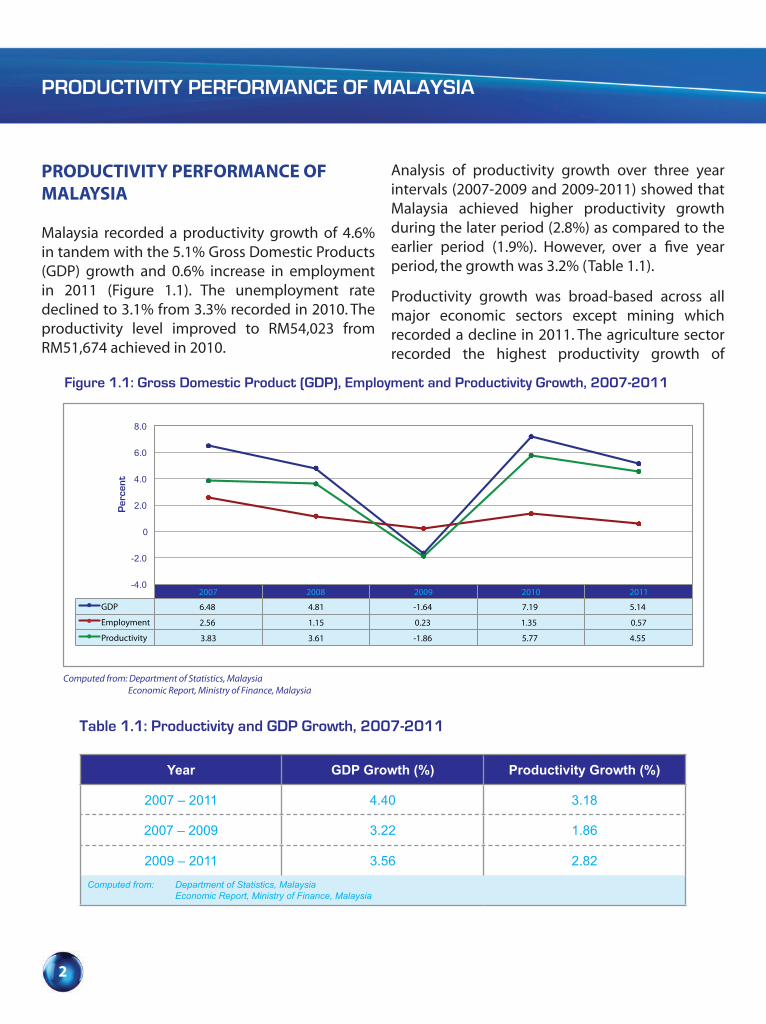

Malaysia recorded a productivity growth of 4.6% in tandem with the 5.1% Gross Domestic Products (GDP) growth and 0.6% increase in employment in 2011 (Figure 1.1). The unemployment rate declined to 3.1% from 3.3% recorded in 2010. The productivity level improved to RM54,023 from RM51,674 achieved in 2010.

Analysis of productivity growth over three year intervals (2007-2009 and 2009-2011) showed that Malaysia achieved higher productivity growth during the later period (2.8%) as compared to the earlier period (1.9%). However, over a five year period, the growth was 3.2% (Table 1.1).

Productivity growth was broad-based across all major economic sectors except mining which recorded a decline in 2011. The agriculture sector recorded the highest productivity growth of

Figure 1.1: Gross Domestic Product (GDP), Employment and Productivity Growth, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

Per

cent

2007 2008 2009 2010 2011

GDP 6.48 4.81 -1.64 7.19 5.14

Employment 2.56 1.15 0.23 1.35 0.57

Productivity 3.83 3.61 -1.86 5.77 4.55

-4.0

-2.0

0

2.0

4.0

6.0

8.0

Table 1.1: Productivity and GDP Growth, 2007-2011

Year GDP Growth (%) Productivity Growth (%)

2007 – 2011 4.40 3.18

2007 – 2009 3.22 1.86

2009 – 2011 3.56 2.82

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

Table 1.2: Productivity Level and Growth, 2011

Economic Activities Level (RM) Growth (%)

Agriculture 29,466 6.23

Mining 866,246 -6.14

Manufacturing 54,509 1.97

Construction 24,635 3.09

Services 53,938 4.92

Malaysia 54,023 4.55

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

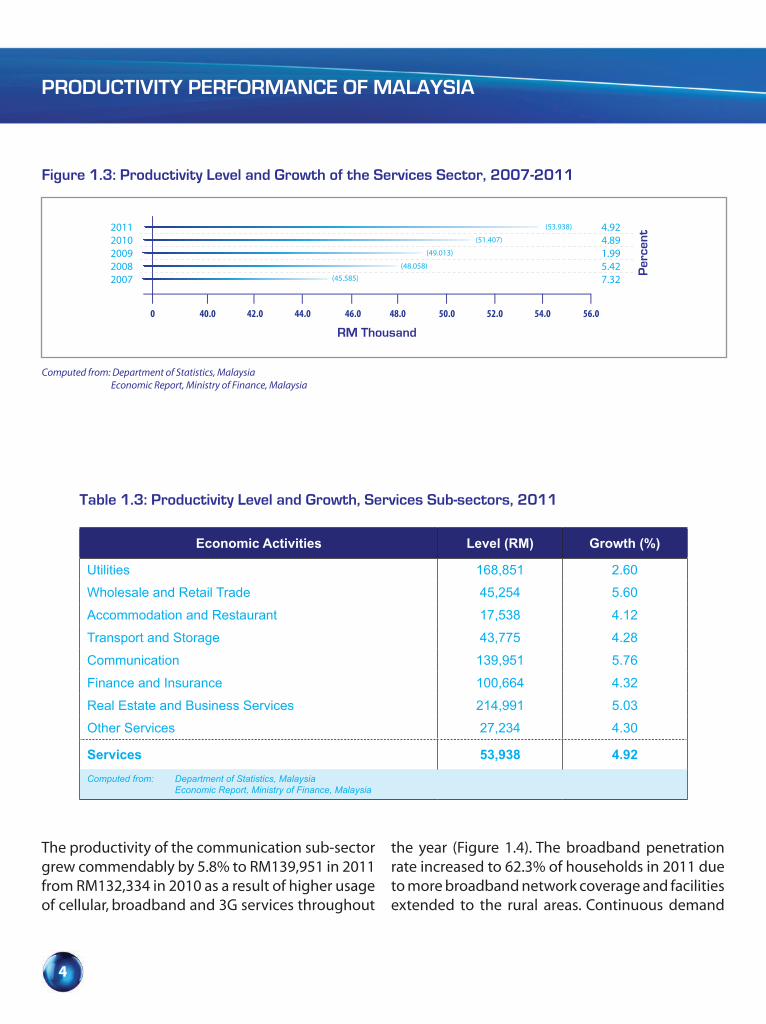

Table 1.3: Productivity Level and Growth, Services Sub-sectors, 2011

Economic Activities Level (RM) Growth (%)

Utilities 168,851 2.60

Wholesale and Retail Trade 45,254 5.60

Accommodation and Restaurant 17,538 4.12

Transport and Storage 43,775 4.28

Communication 139,951 5.76

Finance and Insurance 100,664 4.32

Real Estate and Business Services 214,991 5.03

Other Services 27,234 4.30

Services 53,938 4.92

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

CHAPTER 1

3

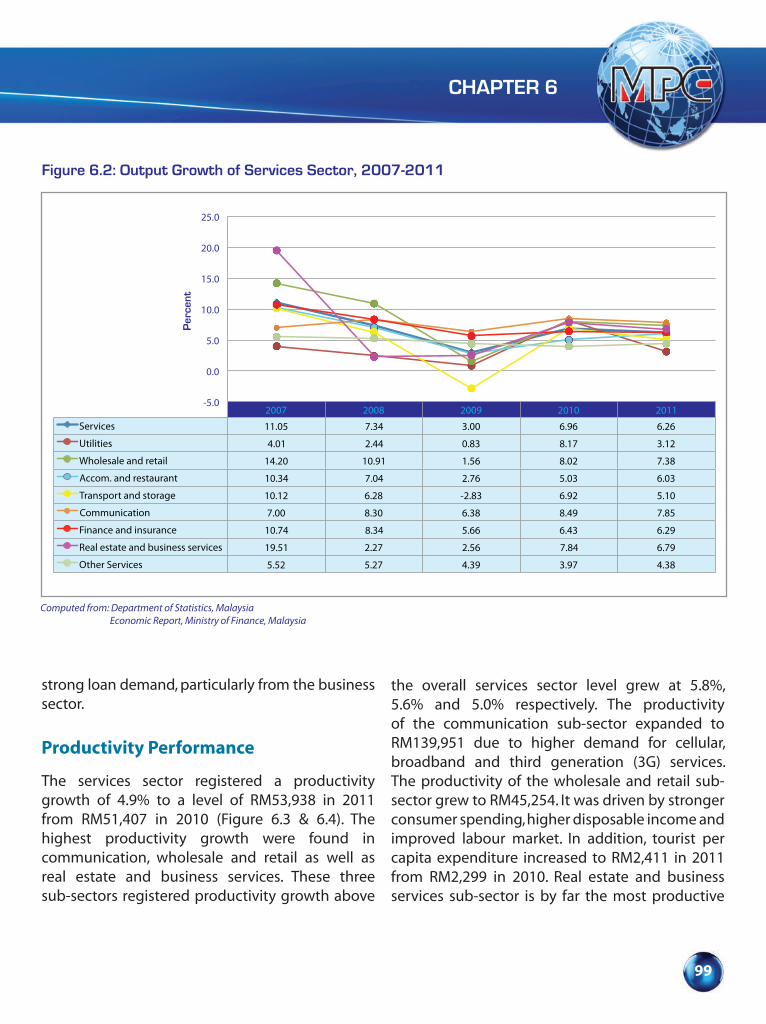

6.2% while the services sector which is the main economic contributor, also showed significant productivity gain of 4.9% (Figure 1.2 & Table 1.2).

Sectoral Productivity PerformanceServices sector

The productivity of the services sector expanded by 4.9% to RM53,938 in 2011 from RM51,407 in

2010. Communication sub-sector contributed the highest productivity growth of 5.8% followed by wholesale and retail trade (5.6%) and real estate and business services (5.0%) (Figure 1.3 & Table 1.3). The improvement in productivity performance was partly due to the results of the Economic Transformation Programme (ETP) initiatives focusing mainly on the services sub-sectors.

2007 2008 2009 2010 2011

Agriculture -2.29 9.26 1.78 1.80 6.23

Mining 1.08 -1.99 -5.61 0.04 -6.14

Manufacturing 2.29 1.93 -11.90 7.56 1.97

Construction 7.00 4.19 5.74 4.59 3.09

Services 7.32 5.42 1.99 4.89 4.92

-15.0

-10.0

-5.0

0

5.0

10.0

15.0

Figure 1.2: Productivity Growth by Economic Sectors, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

Per

cent

Table 1.1: Productivity and GDP Growth, 2007-2011

Year GDP Growth (%) Productivity Growth (%)

2007 – 2011 4.40 3.18

2007 – 2009 3.22 1.86

2009 – 2011 3.56 2.82

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

Table 1.2: Productivity Level and Growth, 2011

Economic Activities Level (RM) Growth (%)

Agriculture 29,466 6.23

Mining 866,246 -6.14

Manufacturing 54,509 1.97

Construction 24,635 3.09

Services 53,938 4.92

Malaysia 54,023 4.55

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

Table 1.3: Productivity Level and Growth, Services Sub-sectors, 2011

Economic Activities Level (RM) Growth (%)

Utilities 168,851 2.60

Wholesale and Retail Trade 45,254 5.60

Accommodation and Restaurant 17,538 4.12

Transport and Storage 43,775 4.28

Communication 139,951 5.76

Finance and Insurance 100,664 4.32

Real Estate and Business Services 214,991 5.03

Other Services 27,234 4.30

Services 53,938 4.92

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

PRODUCTIVITY PERFORMANCE OF MALAYSIA

4

The productivity of the communication sub-sector grew commendably by 5.8% to RM139,951 in 2011 from RM132,334 in 2010 as a result of higher usage of cellular, broadband and 3G services throughout

the year (Figure 1.4). The broadband penetration rate increased to 62.3% of households in 2011 due to more broadband network coverage and facilities extended to the rural areas. Continuous demand

Figure 1.3: Productivity Level and Growth of the Services Sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 40.0 42.0 44.0 46.0 48.0 50.0 52.0 54.0 56.0

4.924.891.995.427.32

Per

cent

(45.585)

(48.058)

(49.013)

(51.407)

(53.938)

Table 1.1: Productivity and GDP Growth, 2007-2011

Year GDP Growth (%) Productivity Growth (%)

2007 – 2011 4.40 3.18

2007 – 2009 3.22 1.86

2009 – 2011 3.56 2.82

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

Table 1.2: Productivity Level and Growth, 2011

Economic Activities Level (RM) Growth (%)

Agriculture 29,466 6.23

Mining 866,246 -6.14

Manufacturing 54,509 1.97

Construction 24,635 3.09

Services 53,938 4.92

Malaysia 54,023 4.55

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

Table 1.3: Productivity Level and Growth, Services Sub-sectors, 2011

Economic Activities Level (RM) Growth (%)

Utilities 168,851 2.60

Wholesale and Retail Trade 45,254 5.60

Accommodation and Restaurant 17,538 4.12

Transport and Storage 43,775 4.28

Communication 139,951 5.76

Finance and Insurance 100,664 4.32

Real Estate and Business Services 214,991 5.03

Other Services 27,234 4.30

Services 53,938 4.92

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

CHAPTER 1

5

for broadband services was also supported by aggressive marketing strategies carried out by telecommunication providers which had also contributed towards its productivity.

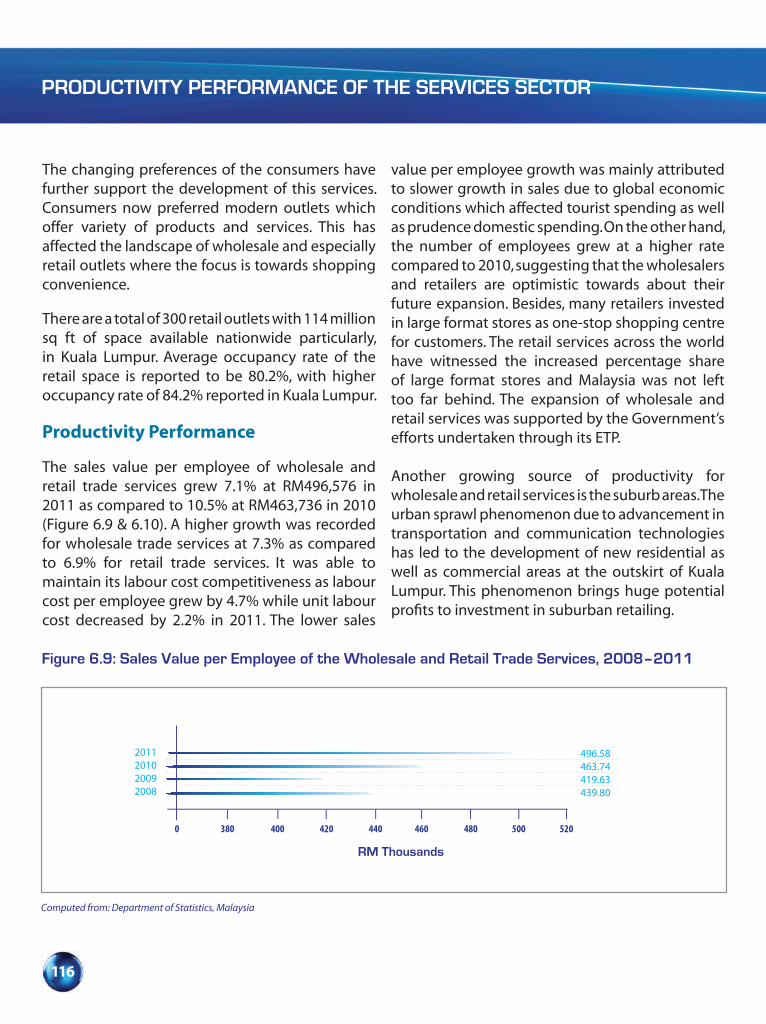

The wholesale and retail trade sub-sector recorded a productivity growth of 5.6% to RM45,254 in 2011

from RM42,856 in 2010 (Figure 1.5). The growth was mainly supported by strong expansion in domestic consumption as well as higher number of tourist arrivals that generated more retail spending especially during festive seasons and the year-end holiday.

Figure 1.4: Productivity Level and Growth of the Communication Sub-sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 20.0 40.0 60.0 80.0 100.0 120.0 140.0 160.0

5.76 6.71 6.4410.5710.14

Per

cent

(105.374)

(116.510)

(124.018)

(132.334)

(139.951)

Figure 1.5: Productivity Level and Growth of the Wholesale and Retail Trade Sub-sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0

5.60 5.28 1.42 9.8010.09

Per

cent

(36.552)

(40.135)

(40.705)

(42.856)

(45.254)

45.0 50.0

PRODUCTIVITY PERFORMANCE OF MALAYSIA

6

The productivity of the real estate and business services sub-sector grew by 5.0% in 2011 to a level of RM214,991 from RM204,686 recorded in 2010 (Figure 1.6). The growth was bolstered by strong real estate and equity market during the year. The increase in shared services and outsourcing (SSO) activities had stimulated the productivity in the business services segment.

The strong demand for loans especially from the industries as well as higher fee-based income and insurance premiums had led to the growth in productivity of the finance and insurance sub-sector by 4.3% to RM100,664 in 2011 from RM96,497 in 2010 (Figure 1.7).

Figure 1.6: Productivity Level and Growth of the Real Estate and Business Services Sub-sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 170.0 175.0 180.0 185.0 190.0 195.0 200.0 205.0

5.035.994.090.223.10

Per

cent

(185.137)

(185.535)

(193.125)

(204.686)

(214.991)

210.0 215.0 220.0

Figure 1.7: Productivity Level and Growth of the Finance and Insurance Sub-sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0 100.0

4.324.784.406.509.35

Per

cent

(82.837)

(88.218)

(92.099)

(96.497)

(100.664)

110.0 120.0

CHAPTER 1

7

The other services sub-sector recorded a productivity growth of 4.3% to RM27,234 in 2011 from RM26,112 in 2010 (Figure 1.8). The private healthcare and education were the main contributors to this sub-sector. The increase in productivity for healthcare was partly contributed by the improvement in specialised healthcare services to cater to the growing demand for health

tourism. The increase in productivity for education was due to the Government’s continuous efforts in promoting Malaysia as a hub in the global education network.

The productivity performance of transport and storage sub-sector expanded by 4.3% to RM43,775 in 2011 from RM41,980 in 2010 (Figure 1.9). Frequent

Figure 1.8: Productivity Level and Growth of the Other Services Sub-sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 22.5 23.0 23.5 24.0 24.5 25.0 25.5 26.0 26.5

4.301.672.393.142.69

Per

cent

(24.321)

(25.085)

(25.684)

(26.112)

(27.234)

27.0 27.5

Figure 1.9: Productivity Level and Growth of the Transport and Storage Sub-sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 37.0 38.0 39.0 40.0 41.0 42.0 43.0 44.0 45.0

4.285.76

-3.292.416.05

Per

cent

(40.082)

(41.046)

(39.693)

(41.980)

(43.775)

PRODUCTIVITY PERFORMANCE OF MALAYSIA

8

travel and trade-related activities especially in the air and sea transport segments contributed to the growth of this sub-sector. Besides, efficient and systematic land transport also contributed to the performance of the sub-sector.

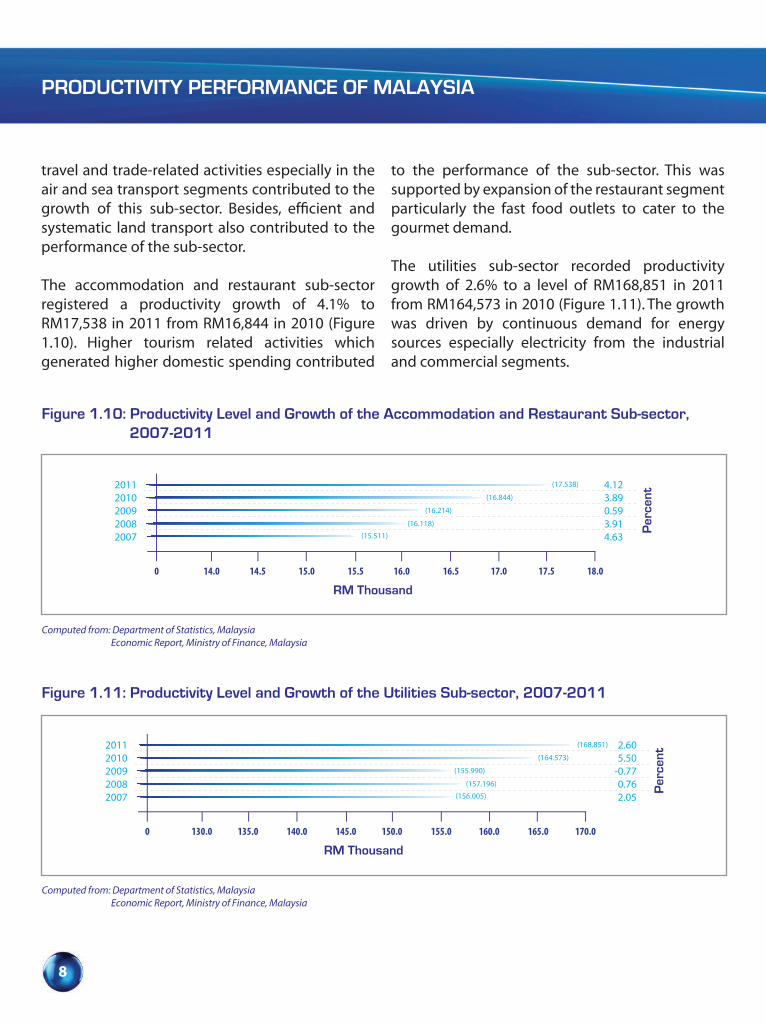

The accommodation and restaurant sub-sector registered a productivity growth of 4.1% to RM17,538 in 2011 from RM16,844 in 2010 (Figure 1.10). Higher tourism related activities which generated higher domestic spending contributed

to the performance of the sub-sector. This was supported by expansion of the restaurant segment particularly the fast food outlets to cater to the gourmet demand.

The utilities sub-sector recorded productivity growth of 2.6% to a level of RM168,851 in 2011 from RM164,573 in 2010 (Figure 1.11). The growth was driven by continuous demand for energy sources especially electricity from the industrial and commercial segments.

Figure 1.10: Productivity Level and Growth of the Accommodation and Restaurant Sub-sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 14.0 14.5 15.0 15.5 16.0 16.5 17.0 17.5 18.0

4.123.890.593.914.63

Per

cent

(15.511)

(16.118)

(16.214)

(16.844)

(17.538)

Figure 1.11: Productivity Level and Growth of the Utilities Sub-sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 130.0 135.0 140.0 145.0 150.0 155.0 160.0 165.0 170.0

2.60 5.50-0.77 0.76 2.05

Per

cent

(156.005)

(157.196)

(155.990)

(164.573)

(168.851)

CHAPTER 1

9

Manufacturing sector

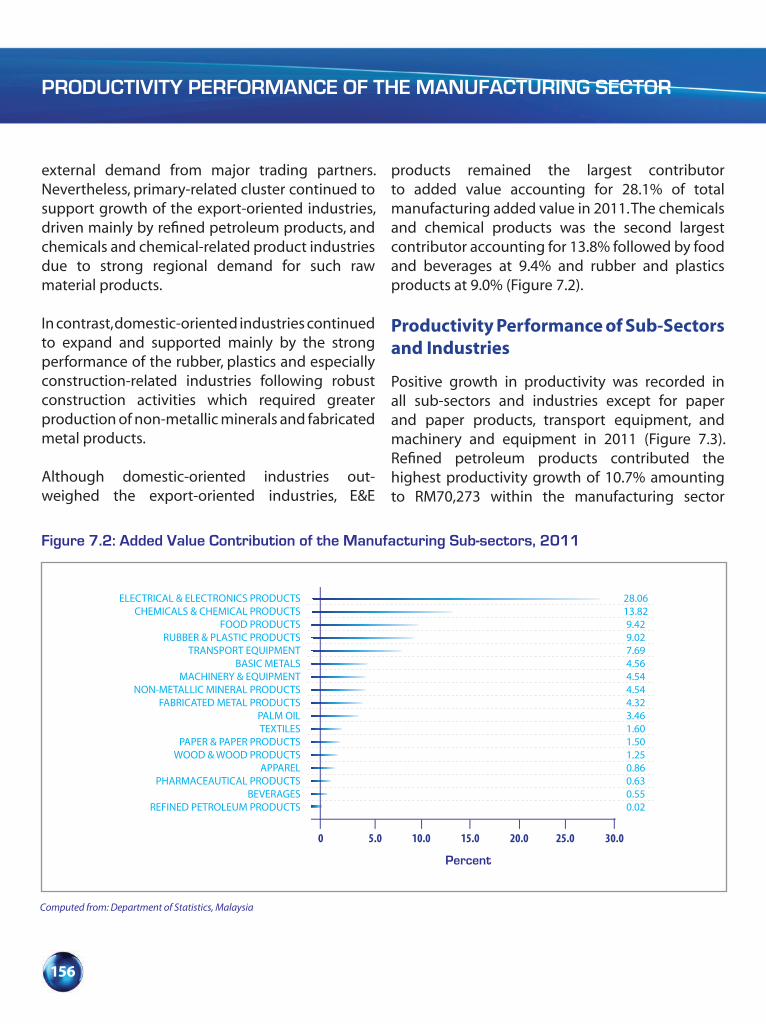

The productivity of the manufacturing sector grew by 2.0% amounting to RM54,509 in 2011 from RM53,459 in 2010 (Figure 1.12). Refined petroleum products sub-sector recorded the highest productivity growth of 10.7%, followed by wearing apparel sub-sector which registered strong productivity growth of 7.3%, attributed to greater demand particularly Turkey, Middle East and emerging economies such as China. The high value added contribution sub-sectors which

demonstrated strong growth in productivity were chemicals and chemical products (4.9%) as well as rubber and plastics products (4.0%). The productivity growth of these sub-sectors surpassed the manufacturing average.

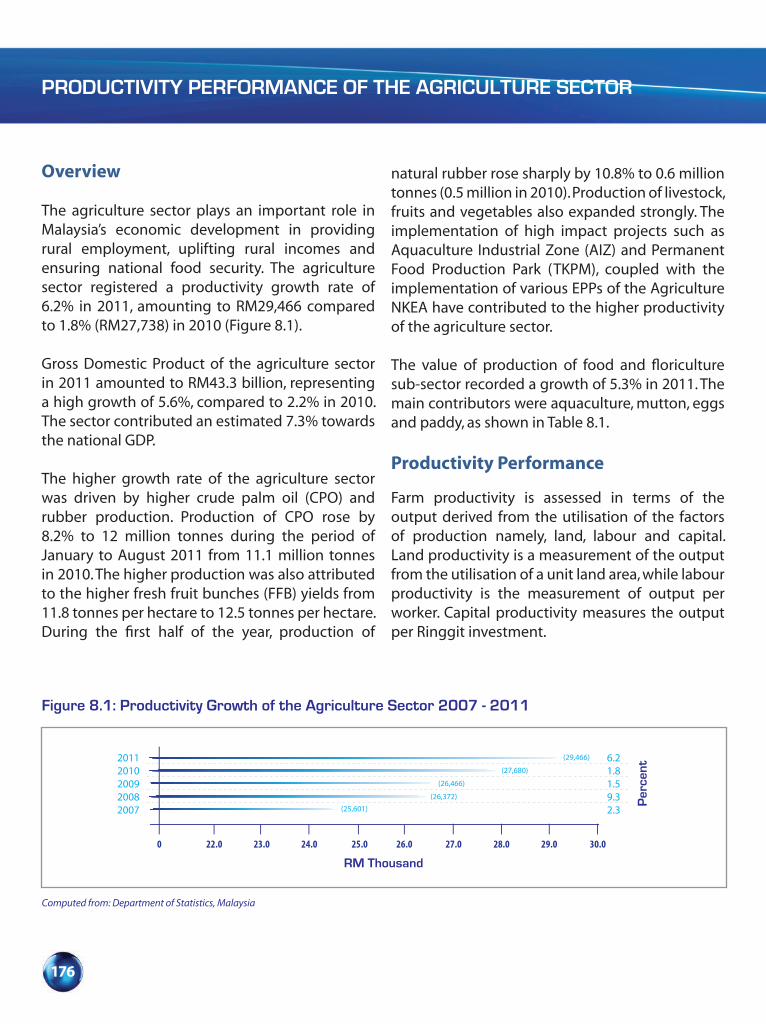

Agriculture sector

The agriculture sector recorded commendable productivity growth of 6.2% to RM29,466 in 2011 from RM27,738 in 2010 (Figure 1.13). The growth was attributed mainly by higher production of

Figure 1.12: Productivity Level and Growth of the Manufacturing Sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 44.0 46.0 48.0 50.0 52.0 54.0 56.0 58.0 60.0

1.97 7.56-11.90 1.93 2.29

Per

cent

(55.349)

(56.414)

(49.700)

(53.459)

(54.509)

Figure 1.13: Productivity Level and Growth of the Agriculture Sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0

6.231.801.789.26-2.29

Per

cent

(24.501)

(26.770)

(27.247)

(27.738)

(29.466)

PRODUCTIVITY PERFORMANCE OF MALAYSIA

10

crude palm oil and the implementation of some of the agriculture Entry Point Projects (EPPs) such as swiftlet breeding, herbal cultivation, aquaculture and large scale commercial farming with anchor companies spearheading these farming activities.

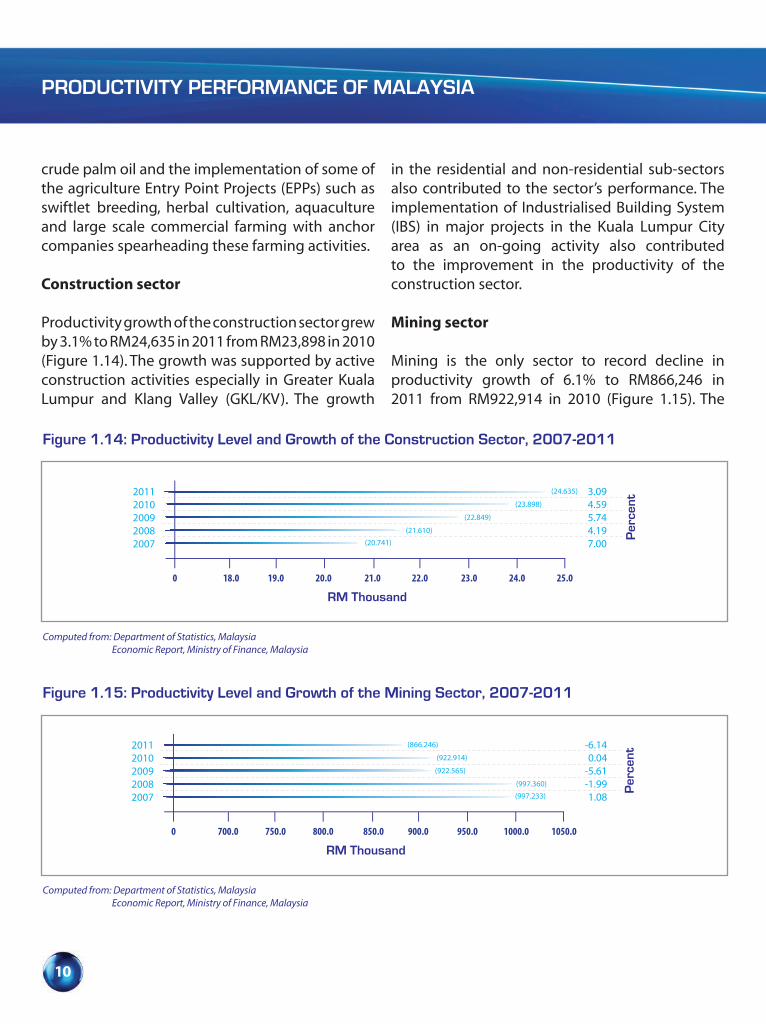

Construction sector

Productivity growth of the construction sector grew by 3.1% to RM24,635 in 2011 from RM23,898 in 2010 (Figure 1.14). The growth was supported by active construction activities especially in Greater Kuala Lumpur and Klang Valley (GKL/KV). The growth

in the residential and non-residential sub-sectors also contributed to the sector’s performance. The implementation of Industrialised Building System (IBS) in major projects in the Kuala Lumpur City area as an on-going activity also contributed to the improvement in the productivity of the construction sector.

Mining sector

Mining is the only sector to record decline in productivity growth of 6.1% to RM866,246 in 2011 from RM922,914 in 2010 (Figure 1.15). The

Figure 1.14: Productivity Level and Growth of the Construction Sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 18.0 19.0 20.0 21.0 22.0 23.0 24.0 25.0

3.094.595.744.197.00

Per

cent

(20.741)

(21.610)

(22.849)

(23.898)

(24.635)

Figure 1.15: Productivity Level and Growth of the Mining Sector, 2007-2011

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

RM Thousand

20112010200920082007

0 700.0 750.0 800.0 850.0 900.0 950.0 1000.0 1050.0

-6.140.04

-5.61-1.991.08

Per

cent

(997.233)

(997.360)

(922.565)

(922.914)

(866.246)

CHAPTER 1

11

productivity of the sector was impacted by the decline in the production of crude oil due to shutdowns of several facilities for maintenance as well as upgrading activities to expand oil and gas production capacity.

Regional Overview of Comparative Productivity Performance

Although affected by the global economic slowdown in terms of export performance, Malaysia’s productivity had surpassed growth recorded by most Organisation of Economic Cooperation Development (OECD) countries. Malaysia recorded a 4.6% productivity growth,

ahead of Republic of Korea (2.1%), Finland (1.9%), USA (1.2%), UK (0.5%) and Japan (-2.0%) (Figure.1.16). In terms of level, Malaysia’s productivity level at USD14,217 was lower than Republic of Korea (USD39,490), Finland (USD64,345), USA (USD92,369) UK (USD66,906) and Japan (USD74,258) (Figure 1.16). Strong economic fundamentals coupled with pragmatic macro economic policies and the implementation of ETP are among the initiatives taken by the Government to further enhance Malaysia’s productivity level.

Among the selected Asian countries, China recorded the highest productivity growth of

Figure 1.16: Productivity Levels and Growth of Malaysia and Selected OECD Countries, 2011

Computed from: OECD Economic Outlook, Vol. 90 Database : OECD Statistics : Country Data, The Economist Intelligent Unit

IRELANDUNITED STATES

JAPANUNITED KINGDOM

FINLANDAUSTRALIA

CANADAKOREA

NEW ZEALANDMALAYSIA

0 10 20 30 40 50 60 70 80 90 100

2.851.19

-0.200.501.880.300.592.07

-0.294.55

USD Thousand

Per

cent

(96.559)

(92.369)

(74.258)

(66.906)

(64.345)

(58.863)

(56.988)

(39.490)

(34.786)

(14.217)

PRODUCTIVITY PERFORMANCE OF MALAYSIA

12

8.7%, followed by Indonesia (5.0%) and India (4.8%). Malaysia’s productivity growth at 4.6% was ahead of Hong Kong (2.7%), Singapore (2.1%) and Taiwan (1.9%), while Thailand posted a decline in productivity by 1.1% (Figure 1.17).

Malaysia productivity level was at least three times higher as compared to its regional peers namely, Thailand (USD4,801), China (USD4,443), Philippines (USD3,341), Indonesia (USD3,040) and India (USD2,867), but lagging behind Hong Kong, Singapore and Taiwan.

Way Forward

In the context of an ailing global economy especially in the US and Eurozone, many exporting

countries including Malaysia were affected. As a small open economy which is dependent on export and vulnerable to major changes worldwide, concentration on domestic consumption is the best option to overcome this sluggish economy.

The current Budget 2012 is expected to spur domestic consumption. These include the one-off financial assistance to households in the low and middle-income groups, schooling assistance to all primary and secondary students and book vouchers to all local students in tertiary education institutions as well as increment in public sector wage.

Besides relying on domestic consumption, Malaysia must also diversify its efforts and initiatives to be on

Figure 1.17: Productivity Levels and Growth of Malaysia and Selected Asian Countries, 2011

HONG KONGSINGAPORE

TAIWANMALAYSIATHAILAND

CHINAPHILIPINESINDONESIA

INDIA

0 10 20 30 40 50 60 70

2.702.101.904.55-1.108.700.505.004.80

USD Thousand

Computed from: Country Data, The Economist Intelligent Unit

Per

cent

(65.174)

(55.702)

(43.827)

(14.217)

(4.801)

(4.443)

(3.341)

(3.040)

(2.867)

CHAPTER 1

13

target to become a high-income economy by 2020. Productivity-driven growth is what the country requires in order to achieve the high-income status. Achieving productivity improvements can be attained through five interlinked catalysing factors which would enable individuals and organisations to thrive. The five factors are organisational development, human capital management, the capability to innovate, the ability to acquire and use of technology and efficient management systems.

Enhancing business environment to be more conducive is among the factors that can improve productivity. Realising the need to enhance ease in the public delivery system and facilitate business investment, the Modern Business Licensing (MBL) is one of the initiatives implemented and facilitated by Special Taskforce to Facilitate Business (PEMUDAH). The ultimate aim of the MBL initiative is to abolish unnecessary licences and simplify business-related procedures in the country.

Outlook for 2012

The economy is anticipated to sustain its growth momentum in 2012 where productivity is expected to grow by more than 4.0%. The growth in productivity is expected to benefit from the implementation of some of the EPPs introduced

under the ETP where the private sector will provide the impetus in driving economic expansion while the Government will provide the supportive role in improving productivity.

The productivity of the services sector is expected to grow by 4.9% in 2012 lead by communication and other services sub-sectors. Growth in the communication sub-sector will be supported by advancement in wireless technology, expansion in High-Speed Broadband infrastructure as well as Government initiatives to promote broadband usage through out the country.

The manufacturing sector’s productivity is targeted to grow moderately by 2.3% in 2012 caused by the after effect of the Euro debt crisis and the subprime lending experienced in the US economy. However, the sector will also be supported by continuous growth in the domestic-oriented industries attributed by the recovery of transport equipment sub-sector and expansion in the construction-related cluster.

The agriculture sector is expected to register a productivity growth of 3.7% in 2012 supported by the food production segment. With the launching of the National Agro-Food Policy 2011-2020 where the objectives among others, are to increase value-

PRODUCTIVITY PERFORMANCE OF MALAYSIA

14

added of the agro-food sector, complementing and strengthening the food supply chain and providing skilled labour for the sector are expected to further enhance the productivity of the sector.

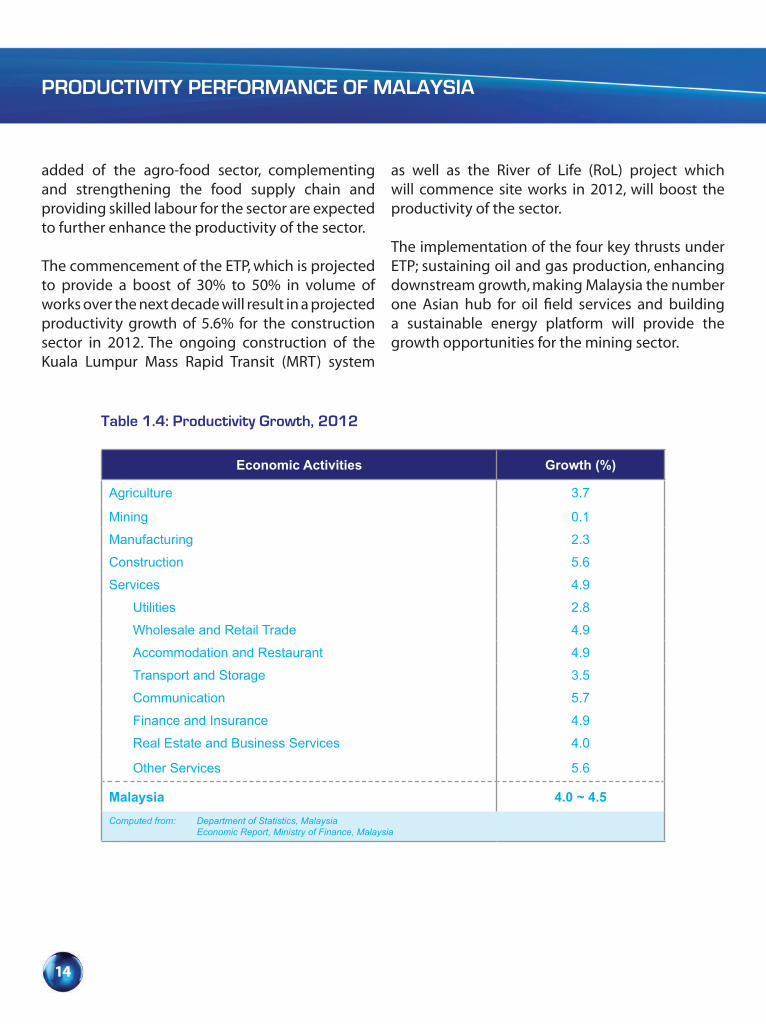

The commencement of the ETP, which is projected to provide a boost of 30% to 50% in volume of works over the next decade will result in a projected productivity growth of 5.6% for the construction sector in 2012. The ongoing construction of the Kuala Lumpur Mass Rapid Transit (MRT) system

as well as the River of Life (RoL) project which will commence site works in 2012, will boost the productivity of the sector.

The implementation of the four key thrusts under ETP; sustaining oil and gas production, enhancing downstream growth, making Malaysia the number one Asian hub for oil field services and building a sustainable energy platform will provide the growth opportunities for the mining sector.

Table 1.4: Productivity Growth, 2012

Economic Activities Growth (%)

Agriculture 3.7

Mining 0.1

Manufacturing 2.3

Construction 5.6

Services 4.9

Utilities 2.8

Wholesale and Retail Trade 4.9

Accommodation and Restaurant 4.9

Transport and Storage 3.5

Communication 5.7

Finance and Insurance 4.9

Real Estate and Business Services 4.0

Other Services 5.6

Malaysia 4.0 ~ 4.5

Computed from: Department of Statistics, Malaysia Economic Report, Ministry of Finance, Malaysia

CHAPTER 1

15

Towards A High Income Economy

CHAPTER 2

SOURCES OF MALAYSIA’S ECONOMIC GROWTH

SOURCES OF MALAYSIA’S ECONOMIC GROWTH

18

Overview

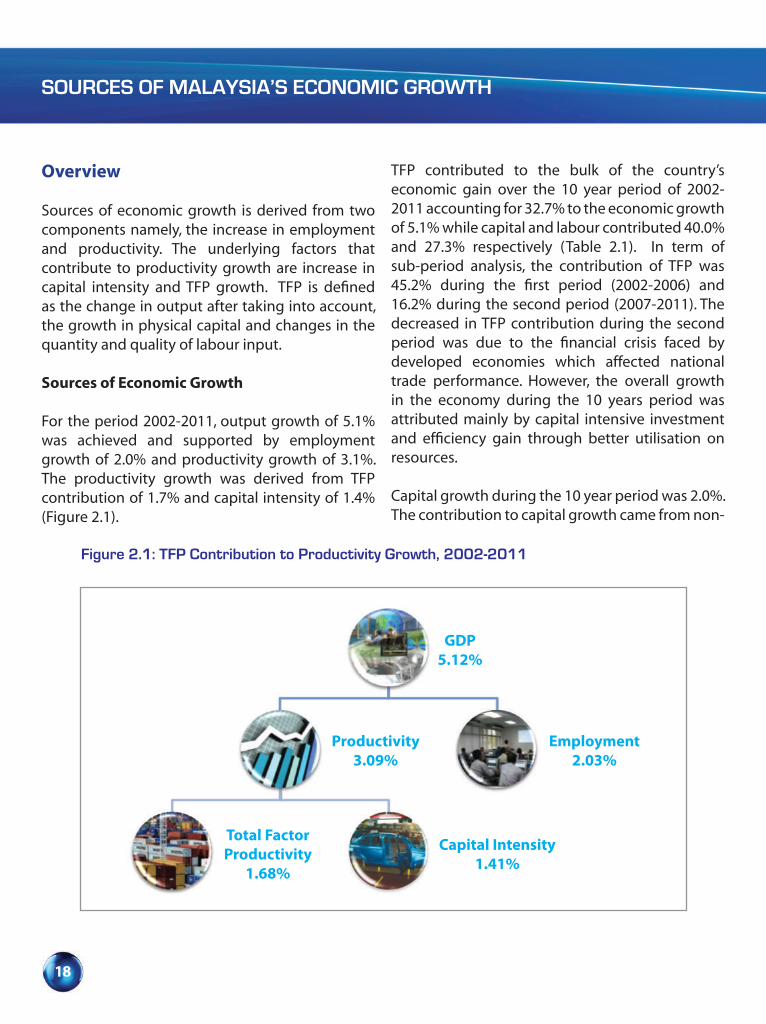

Sources of economic growth is derived from two components namely, the increase in employment and productivity. The underlying factors that contribute to productivity growth are increase in capital intensity and TFP growth. TFP is defined as the change in output after taking into account, the growth in physical capital and changes in the quantity and quality of labour input.

Sources of Economic Growth

For the period 2002-2011, output growth of 5.1% was achieved and supported by employment growth of 2.0% and productivity growth of 3.1%. The productivity growth was derived from TFP contribution of 1.7% and capital intensity of 1.4% (Figure 2.1).

TFP contributed to the bulk of the country’s economic gain over the 10 year period of 2002-2011 accounting for 32.7% to the economic growth of 5.1% while capital and labour contributed 40.0% and 27.3% respectively (Table 2.1). In term of sub-period analysis, the contribution of TFP was 45.2% during the first period (2002-2006) and 16.2% during the second period (2007-2011). The decreased in TFP contribution during the second period was due to the financial crisis faced by developed economies which affected national trade performance. However, the overall growth in the economy during the 10 years period was attributed mainly by capital intensive investment and efficiency gain through better utilisation on resources.

Capital growth during the 10 year period was 2.0%. The contribution to capital growth came from non-

GDP5.12%

Employment2.03%

Productivity3.09%

Total FactorProductivity

1.68%

Capital Intensity1.41%

Figure 2.1: TFP Contribution to Productivity Growth, 2002-2011

CHAPTER 2

19

ICT capital (1.2%) and ICT capital (0.8%). During the first period 2002-2006, capital growth was 1.9% of which non-ICT capital contributed 1.0% and ICT capital (0.9%). Likewise during the second period 2007-2011, capital growth had increased to 2.2% of which 1.4% by non-ICT capital and 0.8% by ICT capital (Table 2.1).

The high contribution of non-ICT capital to GDP growth was reflected by higher investment in structural as well as machinery and equipment. Over the last two decades, share of investment in non-ICT capital had decreased from 88.8% in 1990 to 81.1% in 2010, while share of ICT capital workforce had shown increasing trend from 11.2% in 1990 to 18.9% in 2010 (Figure 2.2).

Table 2.1: Contribution of TFP, Capital and Labour to GDP (%)

2002-2006 2007-2011 2002-2011

GDP

Labour

Labour Quality

Labour Quantity

Capital

Non ICT Capital

ICT Capital

TFP

5.83

1.27 (21.80)

0.24

1.03

1.92(32.96)

1.04

0.88

2.64(45.24)

4.41

1.53(34.60)

0.17

1.36

2.17(49.19)

1.36

0.81

0.71(16.21)

5.12

1.40(27.31)

0.20

1.19

2.04(39.95)

1.20

0.84

1.68(32.74)

Computed from: Department of Statistics, Malaysia

10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0 100.0

Figure 2.2: Share of Non ICT Capital and ICT Capital

Computed from: Department of Statistics, Malaysia

Non ICT Captal ICT Capital

2010

2002

1990

0

Percent

81.318.7

84.915.1

88.812.2

SOURCES OF MALAYSIA’S ECONOMIC GROWTH

20

In contrast, the contribution of labour had shown a marginal increased from 1.3% (labour quality 0.2% and labour quantity 1.0%) during the first period to 1.5% (labour quality 0.2% and labour quantity 1.4%) during the second period (Table 2.1). This shows that the quantity of workforce was the major contributor to output growth. Share of higher skill workforce had marginally increased from 24.4% in 2001 to 27.9% in 2011 while share of low skill workforce had declined from 26.4% in 2001 to 23.2% in 2011 (Figure 2.3).

TFP of Selected Economic Sectors

Malaysia’s aspiration to advance towards a high-income economy requires higher TFP growth to be recorded in all economic sectors. This involves adopting an innovation-based economy to be globally competitive. By examining the TFP of the different economic sectors, it is possible to understand how the respective sectors have performed and to identify those sectors which require greater attention.

For the period 2002-2011, the services sector recorded the highest TFP growth of 3.3% attributed to high output growth due to higher demand from both external and domestic users. TFP growth contributed 55.1% to output growth as a result of the implementation of some of EPPs as seven of 12 NKEAs are from the services sector. Likewise, capital and labour contributed 14.1% and 30.8% respectively (Table 2.2). Some of outstanding contributors within the services sub sector include trade and finance services. Higher TFP growth can be achieved by shifting towards more ICT based operation such as e-business, besides of the personalised services offered to the customers.

The agriculture sector recorded a TFP growth of 2.5%, which is in line with the move to modernise and transform the sector and operate like a business venture. The higher TFP contribution was influenced by higher commodity prices in recent years as well as a successful implementation of some of EPPs focusing on high-value added crops, swiftlet breeding and aquaculture. This was

Figure 2.3: Share of Employment by Skill (%)

Computed from: Department of Statistics, Malaysia

High Skill Medium Skill Low Skill

2011

2006

2001

0 10.0 20.0 30.0 40.0 50.0 60.0

Percent

27.8948.9623.15

26.3149.2124.49

24.3549.2426.41

CHAPTER 2

21

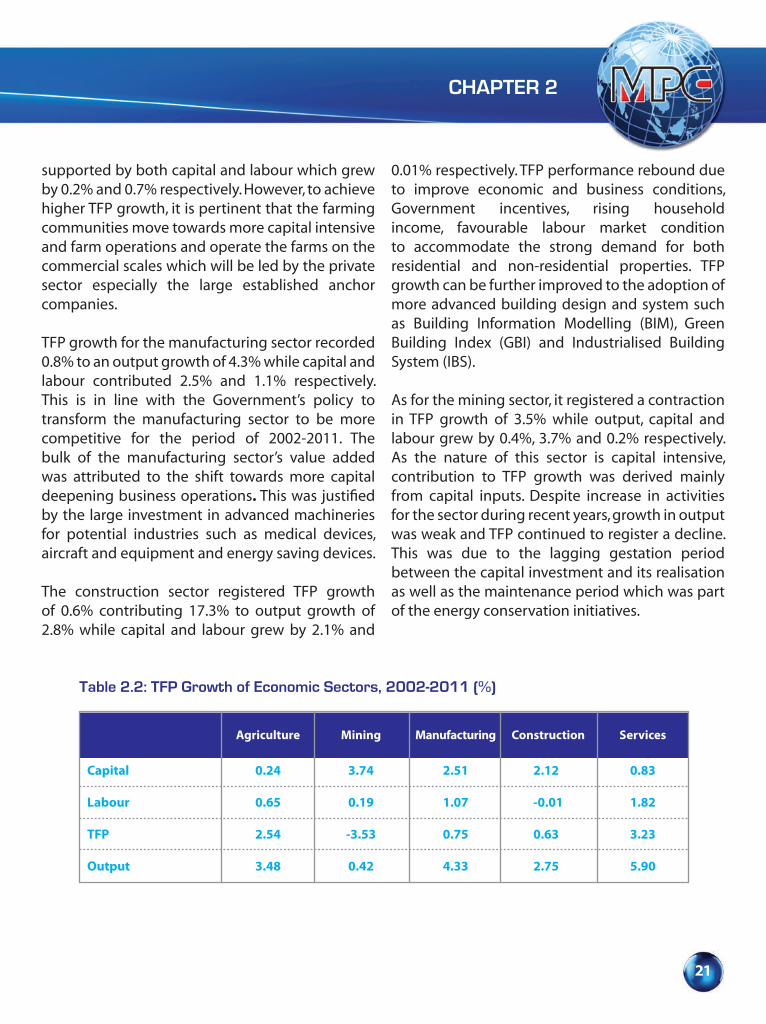

supported by both capital and labour which grew by 0.2% and 0.7% respectively. However, to achieve higher TFP growth, it is pertinent that the farming communities move towards more capital intensive and farm operations and operate the farms on the commercial scales which will be led by the private sector especially the large established anchor companies.

TFP growth for the manufacturing sector recorded 0.8% to an output growth of 4.3% while capital and labour contributed 2.5% and 1.1% respectively. This is in line with the Government’s policy to transform the manufacturing sector to be more competitive for the period of 2002-2011. The bulk of the manufacturing sector’s value added was attributed to the shift towards more capital deepening business operations. This was justified by the large investment in advanced machineries for potential industries such as medical devices, aircraft and equipment and energy saving devices.

The construction sector registered TFP growth of 0.6% contributing 17.3% to output growth of 2.8% while capital and labour grew by 2.1% and

0.01% respectively. TFP performance rebound due to improve economic and business conditions, Government incentives, rising household income, favourable labour market condition to accommodate the strong demand for both residential and non-residential properties. TFP growth can be further improved to the adoption of more advanced building design and system such as Building Information Modelling (BIM), Green Building Index (GBI) and Industrialised Building System (IBS).

As for the mining sector, it registered a contraction in TFP growth of 3.5% while output, capital and labour grew by 0.4%, 3.7% and 0.2% respectively. As the nature of this sector is capital intensive, contribution to TFP growth was derived mainly from capital inputs. Despite increase in activities for the sector during recent years, growth in output was weak and TFP continued to register a decline. This was due to the lagging gestation period between the capital investment and its realisation as well as the maintenance period which was part of the energy conservation initiatives.

Table 2.2: TFP Growth of Economic Sectors, 2002-2011 (%)

Agriculture Mining Manufacturing Services

Capital

Labour

TFP

Output

0.24

0.65

2.54

3.48

2.51

1.07

0.75

4.33

2.12

-0.01

0.63

2.75

0.83

1.82

3.23

5.90

3.74

0.19

-3.53

0.42

Construction

SOURCES OF MALAYSIA’S ECONOMIC GROWTH

22

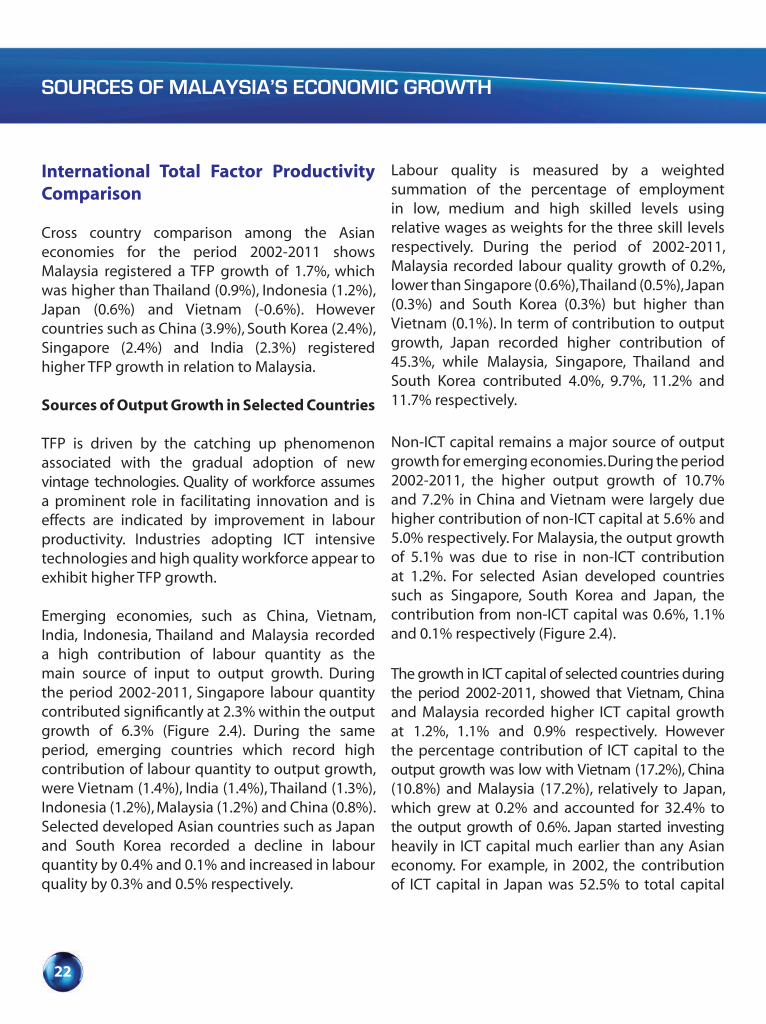

International Total Factor Productivity Comparison

Cross country comparison among the Asian economies for the period 2002-2011 shows Malaysia registered a TFP growth of 1.7%, which was higher than Thailand (0.9%), Indonesia (1.2%), Japan (0.6%) and Vietnam (-0.6%). However countries such as China (3.9%), South Korea (2.4%), Singapore (2.4%) and India (2.3%) registered higher TFP growth in relation to Malaysia.

Sources of Output Growth in Selected Countries

TFP is driven by the catching up phenomenon associated with the gradual adoption of new vintage technologies. Quality of workforce assumes a prominent role in facilitating innovation and is effects are indicated by improvement in labour productivity. Industries adopting ICT intensive technologies and high quality workforce appear to exhibit higher TFP growth.

Emerging economies, such as China, Vietnam, India, Indonesia, Thailand and Malaysia recorded a high contribution of labour quantity as the main source of input to output growth. During the period 2002-2011, Singapore labour quantity contributed significantly at 2.3% within the output growth of 6.3% (Figure 2.4). During the same period, emerging countries which record high contribution of labour quantity to output growth, were Vietnam (1.4%), India (1.4%), Thailand (1.3%), Indonesia (1.2%), Malaysia (1.2%) and China (0.8%). Selected developed Asian countries such as Japan and South Korea recorded a decline in labour quantity by 0.4% and 0.1% and increased in labour quality by 0.3% and 0.5% respectively.

Labour quality is measured by a weighted summation of the percentage of employment in low, medium and high skilled levels using relative wages as weights for the three skill levels respectively. During the period of 2002-2011, Malaysia recorded labour quality growth of 0.2%, lower than Singapore (0.6%), Thailand (0.5%), Japan (0.3%) and South Korea (0.3%) but higher than Vietnam (0.1%). In term of contribution to output growth, Japan recorded higher contribution of 45.3%, while Malaysia, Singapore, Thailand and South Korea contributed 4.0%, 9.7%, 11.2% and 11.7% respectively.

Non-ICT capital remains a major source of output growth for emerging economies. During the period 2002-2011, the higher output growth of 10.7% and 7.2% in China and Vietnam were largely due higher contribution of non-ICT capital at 5.6% and 5.0% respectively. For Malaysia, the output growth of 5.1% was due to rise in non-ICT contribution at 1.2%. For selected Asian developed countries such as Singapore, South Korea and Japan, the contribution from non-ICT capital was 0.6%, 1.1% and 0.1% respectively (Figure 2.4).

The growth in ICT capital of selected countries during the period 2002-2011, showed that Vietnam, China and Malaysia recorded higher ICT capital growth at 1.2%, 1.1% and 0.9% respectively. However the percentage contribution of ICT capital to the output growth was low with Vietnam (17.2%), China (10.8%) and Malaysia (17.2%), relatively to Japan, which grew at 0.2% and accounted for 32.4% to the output growth of 0.6%. Japan started investing heavily in ICT capital much earlier than any Asian economy. For example, in 2002, the contribution of ICT capital in Japan was 52.5% to total capital

CHAPTER 2

23

investment. Investment in ICT capital is vital in order to benefit from advancement in ICT. Unlike technological advancement in the past, which were largely confined to manufacturing, ICT capital is a technology that can permeate the economy and bring about significant production gains in trade, finance, transport and communication.

Total Factor Productivity Growth for Future Direction

The transformation to a high-income nation will be supported with TFP growth. As the economy moves towards an innovation-based economy, it is imperative that competitiveness and higher economic growth be sustained. TFP growth in turn, requires several factor inputs to be fulfilled such as:

• Human Capital Development

In order to obtain a high level of TFP growth, it is necessary to have competitive and highly skilled human capital. In the era of rapid changes, human capital development programmes emphasising on training skilled workers with a mix of critical and applied skills required by the industries and ‘lifelong learning’ in the economy is pertinent. Other factors to consider in driving toward a strong TFP growth include examining the business hiring and training practices, the structure of its operations and its systems for rewarding their employees for their contributions and efforts. Hence a flexibility labour market and promoting greater understanding between employers and employees are crucial to improve long-term TFP performance.

Figure 2.4: Contribution of TFP, Labour, Non-ICT Capital and ICT Capital to the Economic Growth (%)

Source: The Conference Board Total Economy Data based

China India Indonesia Japan Malaysia Singapore South Korea Thailand Vietnam

Labour Quantity 0.75 1.39 1.08 -0.55 1.19 2.34 -0.15 1.26 1.41

Non-ICT Capital 5.36 3.22 2.35 0.12 1.20 0.64 1.05 1.29 5.03

ICT Capital 1.14 0.84 0.67 0.21 0.84 0.36 0.33 0.53 1.20

Labour Quality 0.18 0.18 0.20 0.31 0.20 0.61 0.48 0.50 0.13

TFP 3.90 2.26 1.20 0.60 1.68 2.39 2.42 0.92 -0.62

VIETNAMTHAILAND

SOUTH KOREASINGAPORE

MALAYSIAJAPAN

INDONESIAINDIA

CHINA

-2.0 0 2.0 4.0 6.0 10.08.0 12.0Percent

SOURCES OF MALAYSIA’S ECONOMIC GROWTH

24

• Enhancing Technological Capabilities

ICT technology can permeate the economy and bring significant productivity gains in all economic sectors. Malaysia’s continued economic growth depends upon improvement in technological progress and capital deepening. This means that more investment of new technologies such as ICT capital have to be allocated to each unit of labour as well as to broaden the knowledge-based of the workers.

• Intensifying Demand

Malaysia’s future prosperity is inextricably linked to its long-term productivity and its trade performance in the global market. The increasingly competitive nature of the global market demands that our businesses must operate at a optimum level in order to be efficient and effectively. To compete at the global arena, industries must adopt effective marketing strategies, develop new innovative products and services and branding to develop consumer loyalty. This can be achieved only through a knowledge-based workforce who are able to conduct research, innovate and introduce new production methods and organisational systems that will lead to higher TFP.

• Efficient Allocation of Resources Among the Sector

Better allocation of resources implies more output from a given amount of input leading to higher TFP. The financial and global economic crisis of 2008 had shown the need for Malaysia to adopt a rebalancing strategy. This means that the Malaysian economy has to be oriented towards domestic demand and a

more efficient allocation of resources among the various sectors have to be undertaken. While the export-oriented industries cannot be ignored, it is imperative that the small and medium sized industries (SMIs) be encouraged to continue serving the domestic market and if possible, the export market.

• Reducing Business Rule and Regulation

Rules and regulations help to correct market failures in striving towards achieving broader social objectives. However excessive regulation can distort and impede sound business decisions to the detriment of economic performance. The effect of excessive regulation is reflected through consumers having to pay higher prices and being offered with lesser choice of products; for employees, it means fewer jobs and lower real wages and for shareholders, it results in lower return on investment and fewer funds for retirement. As such, it is essential that Government establishes a regulatory framework which promotes competition, innovation, investment, supports the formation of skills in the labour market and contributes to TFP growth.

• Innovation and Creativity

Innovation is another key driver of TFP growth. Developed countries such as Finland, Sweden, Japan and United State have achieved higher levels of R&D intensity and are leaders in innovation leading to higher TFP achievement. Innovation includes the development of new technology, adaptation of existing technology to new use. Innovative and creativity activities help to produce higher value added products and services which enhance competitiveness.

CHAPTER 2

25

“Capital investment and team spirit towards higher TFP growth”

26 Productivity Report 2011/2012

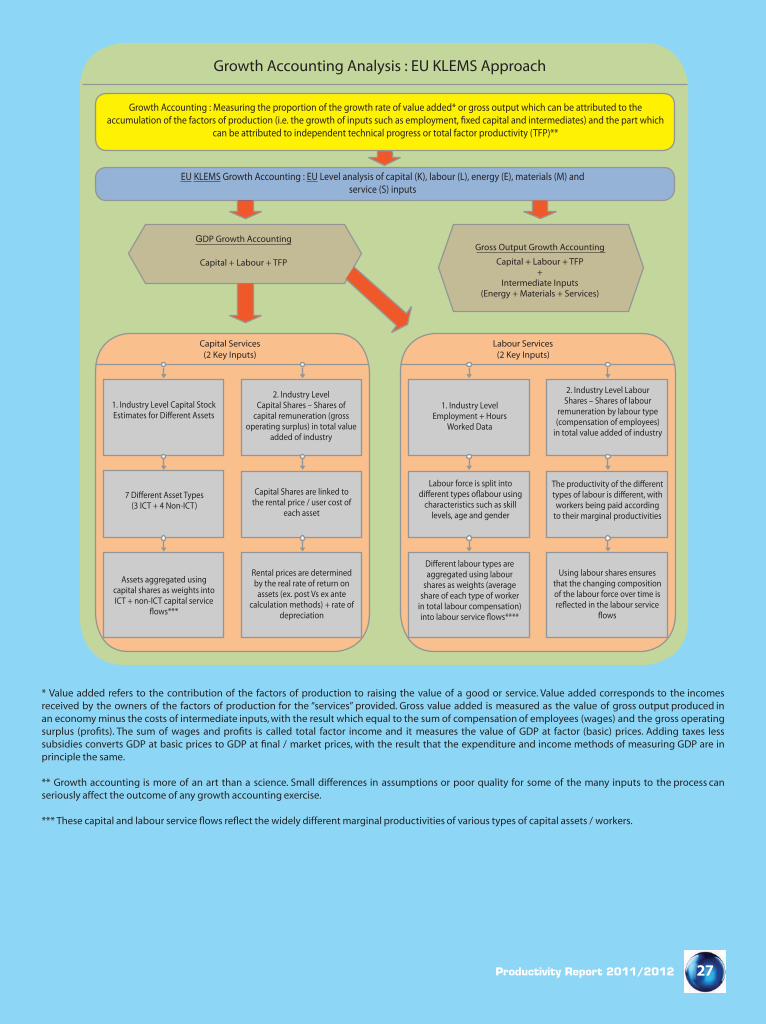

Box 2.1: Productivity Measurement Using the KLEMS Approach

Malaysia’s productivity and competitiveness depends on new initiatives driven by improvement in quality of capital and the quality of her workforce. With intense competition for Foreign Direct Investment (FDI) and the rising of new market economies, this would compel Malaysia to source for new areas of growth in generating more value added to the economy.

Currently, output and employment are expanding in high-technology industries such as computers and electronics as well as knowledge-based services such as financial and other business services. More resources are being utilised in the production and development of new technologies, in particular, on ICT. Computers and related equipment are now the fastest growing segments of tangible investment. At the same time, a polarisation in Malaysia labour markets is taking place as skilled labour is in demand whereas demand for low-skilled workers is declining.

As such, new methods to measure TFP and its contributing factors is imperative so that more effective strategic measures can be identified to provide inputs for policy evaluation, in particular, for the assessment of the goals concerning competitiveness and economic growth. In view of these dynamic changes, TFP analysis will require a new paradigm and methodology for its measurement.

Measuring TFP using the KLEMS (Capital (K), Labour (L), Energy (E), Material (M) and Services (S)) approach will able to identify the contribution of other input factors, such as material, energy and bought in services besides capital and labour. Detailed analysis of these factors such as impact of investment in education, shift in economic activities can be further analysed by using this methodology. KLEMS is based on the growth accounting methodology which allows the users to assess the relative importance of labour, capital and intermediate inputs to growth and to derive measures of TFP growth.

Accurate measures of labour and capital inputs are based on a breakdown of aggregate hours worked or employment and the aggregate capital stock into various components. Employment is cross classified by various categories of labour types such as high, semi-skilled and low skilled labour. Similarly, capital stock is classified into different asset types. Short-term assets like computers have a much higher productivity to fixed assets assets such as buildings. The contribution of intermediate inputs is broken down into the contribution of energy goods, materials and services.

MPC KLEMS project is an on-going effort in which the data are regularly updated and make available for public usage as well as for international comparison. International comparisons also reveal sizeable disparities in investments with regard to quality and quantity of capital and labour. The benefit of KLEMS is to provide better understanding for policy makers on the performance of each of the five inputs. Restrictions concerning labour and product markets, lack of openness to trade and FDI as well as barriers in terms of access to new technologies and in relation to the diffusion of innovations are the constraint towards TFP growth. Below is a chart shown the KLEMS approach used by many European countries for computing their respective TFP growth which Malaysia is adopting.

27Productivity Report 2011/2012

* Value added refers to the contribution of the factors of production to raising the value of a good or service. Value added corresponds to the incomes received by the owners of the factors of production for the “services” provided. Gross value added is measured as the value of gross output produced in an economy minus the costs of intermediate inputs, with the result which equal to the sum of compensation of employees (wages) and the gross operating surplus (profits). The sum of wages and profits is called total factor income and it measures the value of GDP at factor (basic) prices. Adding taxes less subsidies converts GDP at basic prices to GDP at final / market prices, with the result that the expenditure and income methods of measuring GDP are in principle the same.

** Growth accounting is more of an art than a science. Small differences in assumptions or poor quality for some of the many inputs to the process can seriously affect the outcome of any growth accounting exercise.

*** These capital and labour service flows reflect the widely different marginal productivities of various types of capital assets / workers.

Box 2.1: Productivity Measurement Using the KLEMS Approach

Growth Accounting Analysis : EU KLEMS Approach

Growth Accounting : Measuring the proportion of the growth rate of value added* or gross output which can be attributed to the

can be attributed to independent technical progress or total factor productivity (TFP)**

EU KLEMS Growth Accounting : EU Level analysis of capital (K), labour (L), energy (E), materials (M) and service (S) inputs

GDP Growth Accounting

Capital + Labour + TFP

Gross Output Growth Accounting

Capital + Labour + TFP+

Intermediate Inputs(Energy + Materials + Services)

Capital Services(2 Key Inputs)

Labour Services(2 Key Inputs)

1. Industry Level Capital Stock 1. Industry Level Employment + Hours

Worked Data

(3 ICT + 4 Non-ICT)

Labour force is split into

characteristics such as skill levels, age and gender

2. Industry Level Capital Shares – Shares of

capital remuneration (gross operating surplus) in total value

added of industry

2. Industry Level LabourShares – Shares of labour

remuneration by labour type (compensation of employees)

in total value added of industry

Capital Shares are linked to the rental price / user cost of

each assetworkers being paid according

to their marginal productivities

Assets aggregated using capital shares as weights into ICT + non-ICT capital service

Rental prices are determined by the real rate of return on assets (ex. post Vs ex ante

calculation methods) + rate of depreciation

aggregated using labour shares as weights (average

share of each type of worker in total labour compensation)

Using labour shares ensures that the changing composition of the labour force over time is

28 Productivity Report 2011/2012

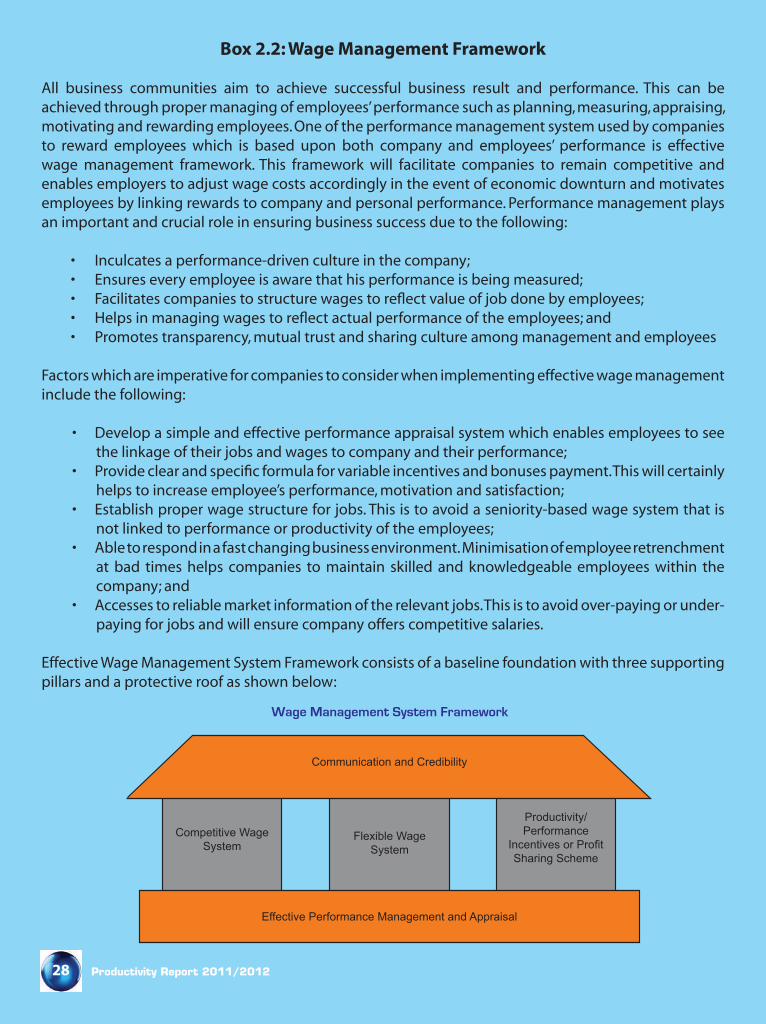

Box 2.2: Wage Management Framework

All business communities aim to achieve successful business result and performance. This can be achieved through proper managing of employees’ performance such as planning, measuring, appraising, motivating and rewarding employees. One of the performance management system used by companies to reward employees which is based upon both company and employees’ performance is effective wage management framework. This framework will facilitate companies to remain competitive and enables employers to adjust wage costs accordingly in the event of economic downturn and motivates employees by linking rewards to company and personal performance. Performance management plays an important and crucial role in ensuring business success due to the following:

• Inculcates a performance-driven culture in the company;• Ensures every employee is aware that his performance is being measured; • Facilitates companies to structure wages to reflect value of job done by employees;• Helps in managing wages to reflect actual performance of the employees; and • Promotes transparency, mutual trust and sharing culture among management and employees

Factors which are imperative for companies to consider when implementing effective wage management include the following:

• Develop a simple and effective performance appraisal system which enables employees to see the linkage of their jobs and wages to company and their performance;

• Provide clear and specific formula for variable incentives and bonuses payment. This will certainly helps to increase employee’s performance, motivation and satisfaction;

• Establish proper wage structure for jobs. This is to avoid a seniority-based wage system that is not linked to performance or productivity of the employees;

• Able to respond in a fast changing business environment. Minimisation of employee retrenchment at bad times helps companies to maintain skilled and knowledgeable employees within the company; and

• Accesses to reliable market information of the relevant jobs. This is to avoid over-paying or under-paying for jobs and will ensure company offers competitive salaries.

Effective Wage Management System Framework consists of a baseline foundation with three supporting pillars and a protective roof as shown below:

Steps in Developing Effective Baseline Foundation

1Establish company

Key Performance Indicators (KPls)

ò2

Cascade & align the KPls within all levels in the company

ò3

Communicate performance matters regularly

ò4

Document performancematters properly

ò5

Review performance and monitor reward framework

ò6 Determine performance/productivity-based reward system

Competitive Wage System

Flexible Wage System

Productivity/ Performance

Sharing Scheme

Communication and Credibility

Effective Performance Management and Appraisal

Wage Management System Framework

Box 2.2: Wage Management Framework

29Productivity Report 2011/2012

Baseline foundation refers to effective and motivational performance appraisal system that links individual wage to organsational performance. There are six steps in developing the baseline foundation as shown in the chart below:

• Supporting pillars ensure effective and successful implementation of Wage Management System. There are three supporting pillars namely, competitive wage system; flexible wage system and productivity/performance incentive or profit-sharing scheme. i) Competitive wage system has the following characteristics:

a. Market Benchmarking of wage policy in similar industry is made available;b. Competitive Wage Structure whereby salary is based on employees performance and

productivity and not seniority based; andc. Productivity-linked Wage System where wage increase is based on individual performance

and incentive payment linked to company and individual performance.ii) Flexible wage system to respond to changes in business environment with the following attributes:

a. Flexible wage system which is susceptible to changing business environment; andb. It rewards employees based on performance which incorporates flexible incentives that is

linked individual performance and productivity.iii) Productivity/Performance Incentives or Profit-Sharing Scheme has the following characteristics:

a. Motivates employees to achieve their goals and creates wealth for the company; andb. Incorporates variable components that include variable bonus based on profitability,

performance or productivity measurement and done annually.

• Protective Roof where wage is an important component and any change to the wage system should be managed with utmost care and sensitivity. It involves two main characteristics such as:• Management practices an open door policy to ensure that all employees or union understand

how their wages are linked to the company’s performance and productivity; and• Credibility where productivity or performance based wage system is implemented with consensus

from both management and employees. Any change to the remuneration will be discussed and agreed upon by various stakeholders before implementation.

Steps in Developing Effective Baseline Foundation

1Establish company

Key Performance Indicators (KPls)

ò2

Cascade & align the KPls within all levels in the company

ò3

Communicate performance matters regularly

ò4

Document performancematters properly

ò5

Review performance and monitor reward framework

ò6 Determine performance/productivity-based reward system

Competitive Wage System

Flexible Wage System

Productivity/ Performance

Sharing Scheme

Communication and Credibility

Effective Performance Management and Appraisal

Wage Management System Framework

Box 2.2: Wage Management Framework

CHAPTER 3

MALAYSIA AND INTERNATIONAL COMPETITIVENESS

MALAYSIA AND INTERNATIONAL COMPETITIVENESS

32

Overview

As a result of globalisation, countries are competing with each other to maintain its global competitiveness. They compete for export market, technology, skills, and investment for economic growth and to improve their standard of living. The current global uncertainty has compelled Malaysia to strive for economic resilience in order to sustain its competitiveness in the global economy.

Looking ahead, Malaysia is now on a journey towards achieving a developed nation by 2020. The Government has been implementing various transformation programmes in major areas of economics and social to be more competitive for long-term sustainability which is clearly stated in the Tenth Malaysia Plan (2011 – 2015).

The Importance of Competitiveness

A competitive nation incorporates an efficient Government delivery system, efficient business operation which is supported by modern infrastructure. This helps to boost the confidence level of investors to the country. The investment flows would spur the economic growth through creating new business opportunities, expanding the existing business and providing more jobs. (Chart 3.1).

Competitiveness Definitions

According to the International Institute for Management Development (IMD) based in Switzerland, “competitiveness is a field of economic theory which analyses the facts and policies that shape the ability of a nation to create and maintain an environment that sustains more value creation

for its enterprise and more prosperity for its people”. It illustrates the relationship on the well-being of people. Competitiveness is how a nation manages the totality of its resources and competencies to increase the prosperity of its people.

World Economic Forum (WEF) defines competitiveness as “the set of institutions, policies and factors that determine the level of productivity of a country. The level of productivity in turn, set the sustainable level of prosperity than can be earned by the economy”. Competitiveness is thus about achieving efficiency, productivity and sustainability towards better quality of life and the ultimate goal is to raise the overall level of prosperity of a nation and its people.

Competitiveness Model

Competitiveness model by IMD explains that firms generate economic added value while nation provides the appropriate framework to

Chart 3.1: The Impact of Competitiveness

CHAPTER 3

33

maximise economic added value. In this context, competitiveness is a field of economic theory which analyses the facts and policies that shapes the ability of a nation to create and maintain an environment which sustains more value creation for its enterprises.

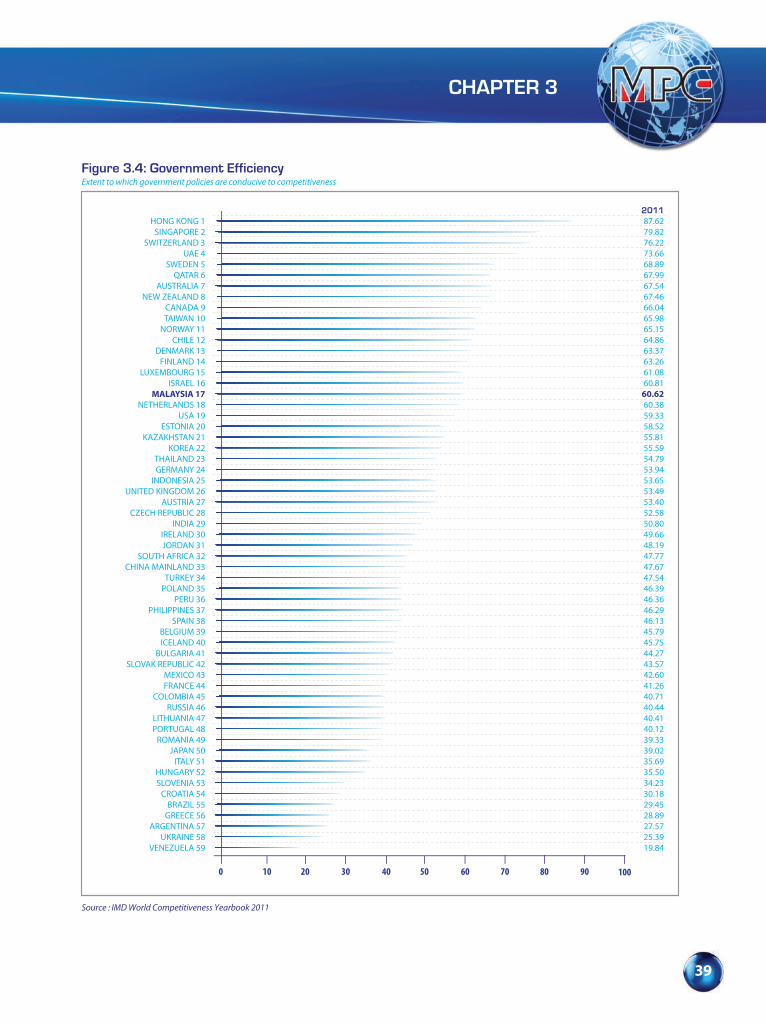

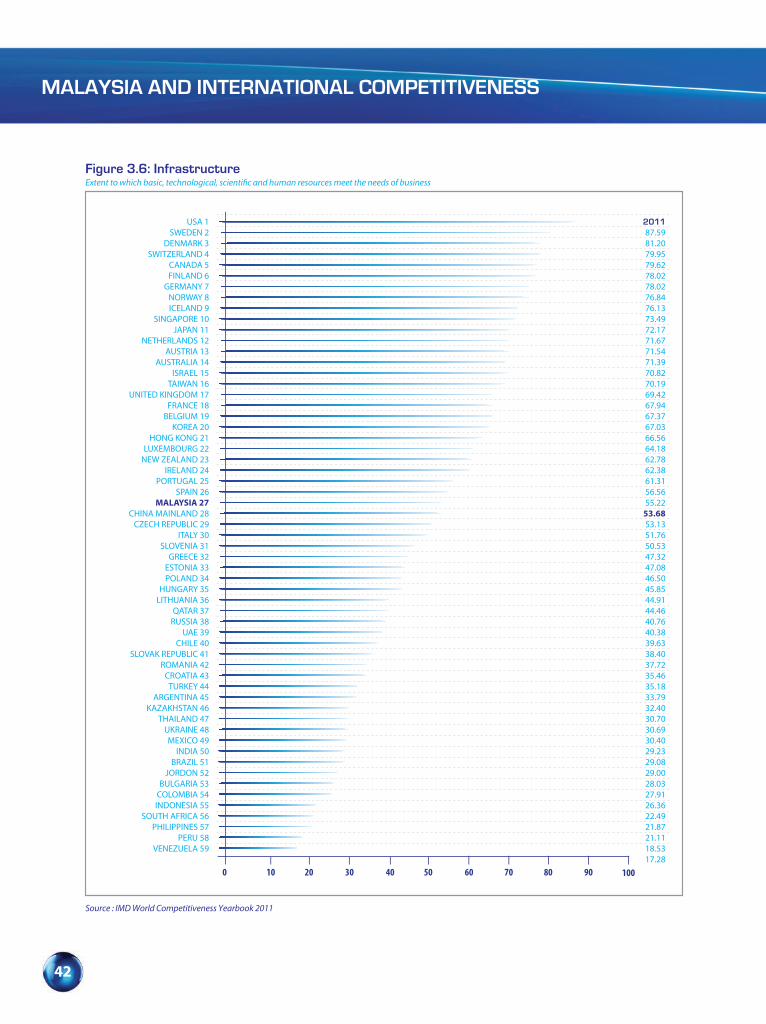

IMD measures competitiveness of a nation based on four major competitiveness input factors namely, Economic Performance, Government Efficiency, Business Efficiency and Infrastructure (Chart 3.2). The Economic Performance factor considers the macro economic performance of the domestic economy; Government Efficiency focuses on the extent to which Government

policies are conducive to competitiveness; Business Efficiency is concerned with the extent to which organisations are performing in an innovative, profitable and responsible manner and Infrastructure measures the extent to which basic technological, scientific and human resources meet business needs.

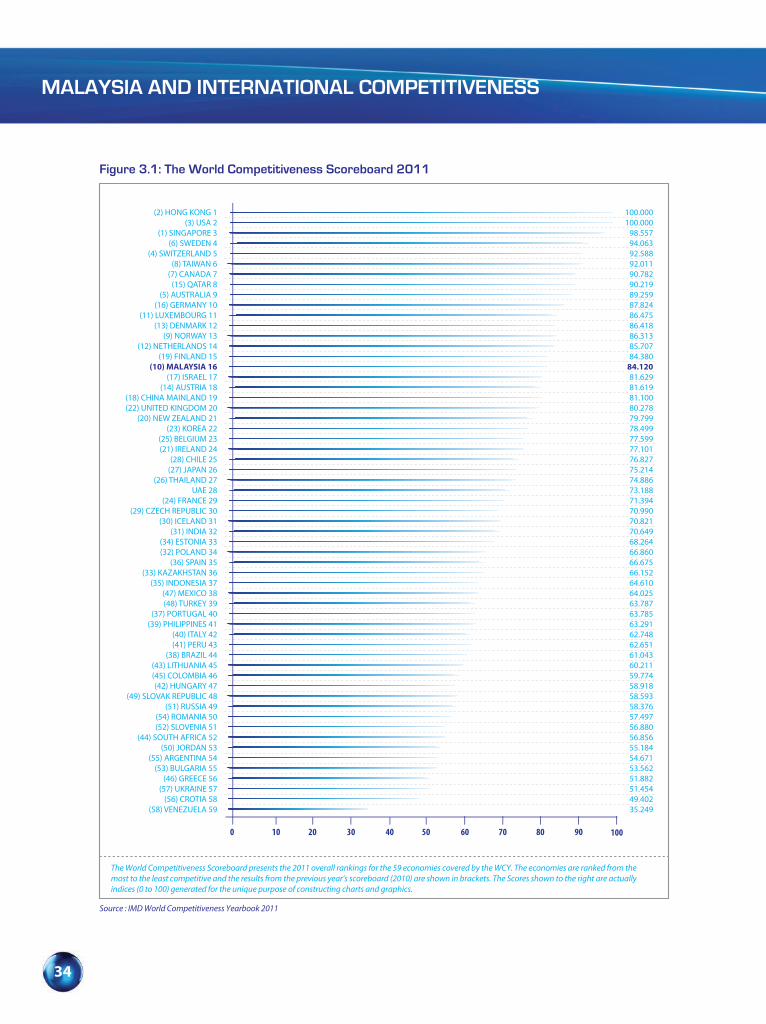

Malaysia’s Overall Competitiveness Performance

In the IMD World Competitiveness Yearbook 2011, the overall performance of Malaysia was ranked at 16th position out of 59 economies. This placed

Source : World Competitiveness Yearbook, 2010

ECONOMICPERFORMANCE

GOVERNMENTEFFICIENCY

BUSINESSEFFICIENCY

INFRASTRUCTURE

SUSTAINABILITY

COMPETITIVENESSOF NATIONS

Chart 3.2: IMD Competitiveness Model

VALUEADDED CRATION

COMPETITIVENESSOF COMPANIES

MALAYSIA AND INTERNATIONAL COMPETITIVENESS

34

The World Competitiveness Scoreboard presents the 2011 overall rankings for the 59 economies covered by the WCY. The economies are ranked from themost to the least competitive and the results from the previous year’s scoreboard (2010) are shown in brackets. The Scores shown to the right are actuallyindices (0 to 100) generated for the unique purpose of constructing charts and graphics.

Figure 3.1: The World Competitiveness Scoreboard 2011

(2) HONG KONG 1(3) USA 2

(1) SINGAPORE 3(6) SWEDEN 4

(4) SWITZERLAND 5(8) TAIWAN 6

(7) CANADA 7(15) QATAR 8

(5) AUSTRALIA 9(16) GERMANY 10

(11) LUXEMBOURG 11(13) DENMARK 12

(9) NORWAY 13(12) NETHERLANDS 14

(19) FINLAND 15(10) MALAYSIA 16

(17) ISRAEL 17(14) AUSTRIA 18

(18) CHINA MAINLAND 19(22) UNITED KINGDOM 20

(20) NEW ZEALAND 21(23) KOREA 22

(25) BELGIUM 23(21) IRELAND 24

(28) CHILE 25(27) JAPAN 26

(26) THAILAND 27UAE 28

(24) FRANCE 29(29) CZECH REPUBLIC 30

(30) ICELAND 31(31) INDIA 32

(34) ESTONIA 33(32) POLAND 34

(36) SPAIN 35(33) KAZAKHSTAN 36

(35) INDONESIA 37(47) MEXICO 38(48) TURKEY 39

(37) PORTUGAL 40(39) PHILIPPINES 41

(40) ITALY 42(41) PERU 43

(38) BRAZIL 44(43) LITHUANIA 45(45) COLOMBIA 46(42) HUNGARY 47

(49) SLOVAK REPUBLIC 48(51) RUSSIA 49