product pricing: the link between product … · james creedon, senior consultant tillinghast, a...

TRANSCRIPT

James Creedon, Senior ConsultantTillinghast, a business of Towers Perrin

© 2009 Towers Perrin

Product pricing: The Link between Product Development, Financial Reporting and Profits

Joint Regional Seminar 2009Practical Actuaries and Financial Reporting

Kuala Lumpur 13-14 JulyTaipei 15-16 JulyHong Kong 17 JulyShanghai 20-21 JulyBangkok 27-28 July

© 2009 Towers Perrin 2

James Creedon, FIAJames Creedon, FIA is a senior consultant with the Tillinghast insurance consulting practice of Towers Perrin, based in Hong Kong. He also has extensive experience of life insurance in Europe after spending seven years with Tillinghast in London.

James has worked with a number of European and Asian insurers on the application of market-consistent techniques for financial reporting, performance measurement and capital management. This has included using market-consistent embedded value and economic capital metrics to quantify and manage risks and as the basis for business decisions. In Asia, he has led MCEV implementation and review projects for six large multinational groups with operations across the region including China, Hong Kong, India, Korea, Malaysia, Singapore and Taiwan.

James’s areas of expertise include:Asset-liability management and modelling;Product development, pricing and risk management of investment-linked products with guarantees;Determination of economic capital requirements and capital management; andMerger and acquisitions, due diligence and capital raisings.

James has played a key role in developing Tillinghast’s intellectual capital in the area of Mark-Consistent and European Embedded Values. James has spoken at internal, client and professional events, including the recent Society of Actuaries Webinar on MCEV, and written a number of articles on European and Market-Consistent Embedded Values.

James holds a Bachelor in Actuarial and Financial Studies (BAFS) from University College, Dublin. He is a Fellow of the Institute of Actuaries.

© 2009 Towers Perrin 3

Agenda

The aims of product pricing

A worked example – The impact of metrics on pricing results

Turning “product cost” into “product price”

Conclusions

© 2009 Towers Perrin 4

An Efficient Product Development Process –The Components

Monitor, React and After-Sales

Feasibility/ViabilityAssessment

Identify Customer Needs

Idea Generation and Management

Marketing & Sales Process

Product DesignCommercialisation,

Implementation and Launch

Check-Points -- Ensure Viability -- Go/Adapt/No-Go

Learning Loop

Protecting and enhancing your position, documenting and disseminating

Accountability: Product Development CommitteeRewards/acknowledgements at key milestonesIn the end the products may look the same but it’s how we get there that makes the difference!

© 2009 Towers Perrin 5

What is product pricing trying to achieve?

Simple answer is to calculate premiums and charges so that product is “profitable”

However not necessarily the case….

Other things to consider may includeWhat are the company’s objectives for the product? Does the product design achieve these?Competition - should the “price” charged be the same as the “cost”?How risky is the product? How do we manage them?How much capital is required?How will the product affect our company’s external metrics?How is the policyholder being treated?Are there regulatory constraints?

© 2009 Towers Perrin 6

Key aims of product pricing

Work as part of the overall product development process to produce the product that best meets the objectives of the company

Specifically, analyse and communicate potentialeffects on company, including:

ProfitabilityCapitalRisk profile and management

© 2009 Towers Perrin 7

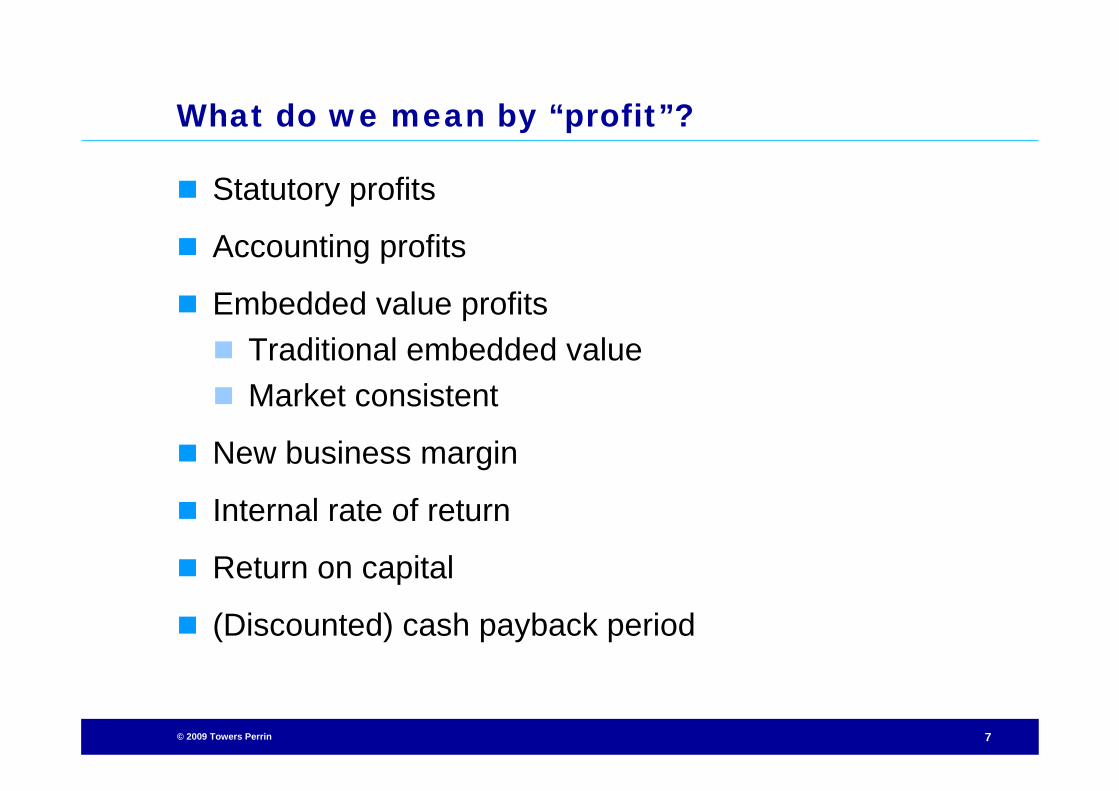

What do we mean by “profit”?

Statutory profits

Accounting profits

Embedded value profitsTraditional embedded valueMarket consistent

New business margin

Internal rate of return

Return on capital

(Discounted) cash payback period

© 2009 Towers Perrin 8

Pricing profitability metrics normally reflect reporting requirements

Key pricing metrics vary by region and company. In general, we see the following key metrics, although others will also be used:

U.S. Companies normally consider projected USGAAP earnings and internal rate of returnEuropean firms – (Market consistent) value of future profits and economic capital requirementsAsian firms – Traditional deterministic value of future profits and local statutory capital requirements. Also consider local accounting earnings

Pricing bases do not need to be exactly the same as reporting bases:

Market consistent pricingChoice of risk discount ratesTarget capital level versus regulatory minimum

© 2009 Towers Perrin 9

Pricing should go beyond just a point estimate of the product profitability…

As part of the pricing work, need to go beyond the expected profitability

Sensitivities should consider a wide range of possible events at the point of sale and in the future

Impact on capital position should consider initial and projectedcapital requirements..

…and potential requirements in adverse scenarios

Need to ensure that product risk and profitability profile is consistent with company’s overall risk appetite

How much capital does it require?

How risky is the product?

What is the impact on the overall financials?

Is it consistent with our risk appetite?

© 2009 Towers Perrin 10

…and provide full feedback to the product development team

The pricing work can support a range of other elements of the product development process, including:

Product feature alternativesAlignment with current product range Risk mitigationUnderwriting and claims managementCompetitor analysis

The pricing team needs to work closely with all the other parties involved in the product development

process

© 2009 Towers Perrin 11

The aims of product pricing

A worked example – The impact of metrics on pricing results

Turning “product cost” into “product price”

Conclusions

© 2009 Towers Perrin 12

A worked example – Market consistent versus traditional pricing

The purpose of this example is to show the impact of metrics on calculated profitability. This is to demonstrate:

How different companies may have different views of certain product typesHow certain metrics do not always reflect the actual risks in the productHow changes in reporting metrics can have a significant effect on the external view of your business

© 2009 Towers Perrin 13

The sample products cover a range of typical insurance products

We compare the value of new business for the following three products on a market-consistent and traditional embedded value basis:

Regular premium term assurance— Regular premium of 500 p.a.— 15 year termSingle premium investment-linked— SP of 3,000; 20 year term— Earnings are from annual management charge plus

administration fee less per policy expensesRegular premium traditional participating product— Regular premium of 3,150 p.a.; 15 year term— Pricing rate of 2.5% p.a.— 70:30 policyholder and shareholder split of investment and

mortality surplus

© 2009 Towers Perrin 14

Traditional pricing techniques

“Traditional” pricing based on:— Present value of future expected profits less cost

of statutory capital— Earned rate based on expected future return on

assets backing— Risk discount rate = earned rate + pricing margin— Pricing margin includes an implicit allowance for

risk that is intended to cover all risks inherent in the product

© 2009 Towers Perrin 15

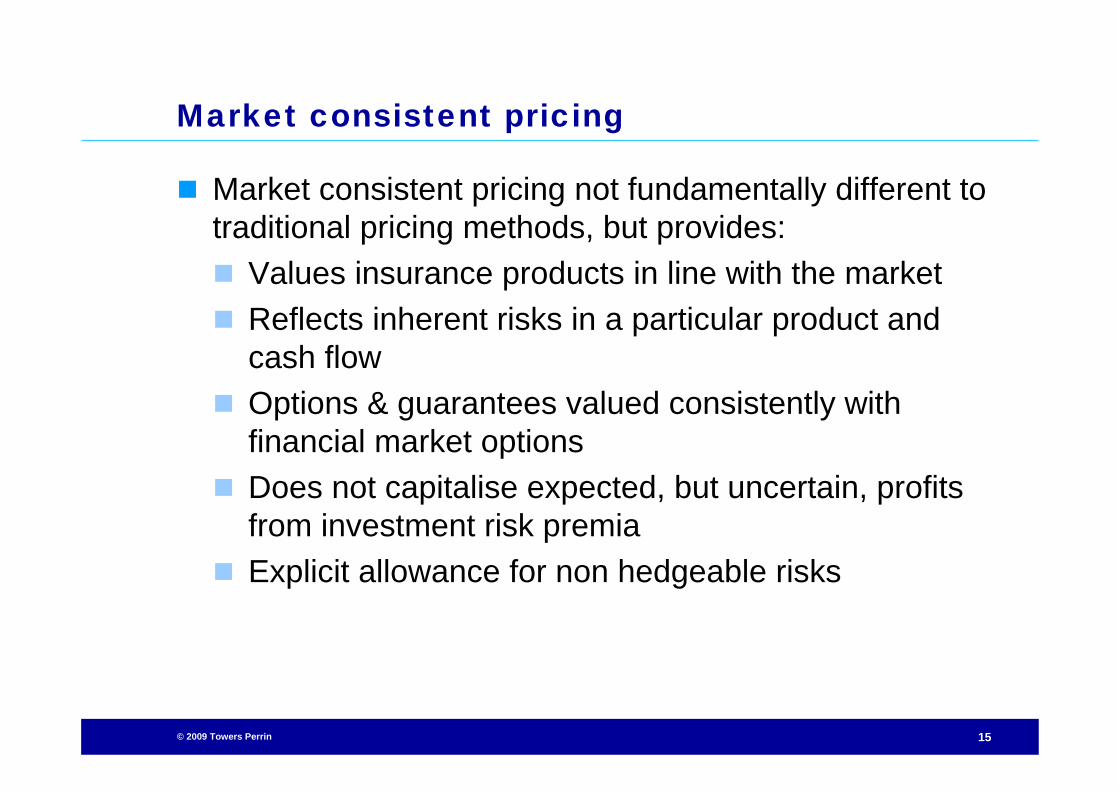

Market consistent pricing

Market consistent pricing not fundamentally different to traditional pricing methods, but provides:

Values insurance products in line with the marketReflects inherent risks in a particular product and cash flowOptions & guarantees valued consistently with financial market optionsDoes not capitalise expected, but uncertain, profits from investment risk premiaExplicit allowance for non hedgeable risks

© 2009 Towers Perrin 16

Economic assumptions

Traditional pricingInvestment return — 5% p.a. for term and participating product— 7% p.a. for investment-linked productRisk Discount Rate of 10%

Market consistent pricingReference rates of 2.5% in year 1 to 4.3% at year 20Implied swaption volatilities of between 10% and 30% by expiry date and tenor

© 2009 Towers Perrin 17

Term Assurance - The reporting basis has a significant effect on the expected profit pattern

Comparison of profit patterns on a Statutory and Embedded Value basis - Term Assurance

(1,000)

(800)

(600)

(400)

(200)

-

200

400

600

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 Y13 Y14 Y15

Year

Ann

ual P

rofit

TEV ProfitsStatutory Distributable Earnings

© 2009 Towers Perrin 18

Profit margins increase for term assurance business on a market consistent basis

338198Cost of Capital / allowance for NHR

7.2%6.4%New Business Margin as a percentage of PVNBP

60%38%New Business Margin as a percentage of APE

297188Value of New Business

607386PVFP before CoC

MCEVTraditional EV

© 2009 Towers Perrin 19

Sample term assurance - Profit margins are not sensitive to interest rates

29760%

18938%

Interest rates – 0.5%

Margin as a % of APE

29660%

18838%

Interest rates + 0.5%Margin as a % of APE

297188Base Case

MCEVTraditional EV

For the TEV sensitivities, we have assumed a +/- 0.5% change in the investment return and RDR assumptions

© 2009 Towers Perrin 20

Investment linked example – Expected profit profile

Comparison of profit patterns on a Statutory and Embedded Value basis - Investment Linked product

(200)

(150)

(100)

(50)

-

50

100

150

200

250

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 Y13 Y14 Y15 Y16 Y17 Y18 Y19 Y20

Year

Ann

ual P

rofit

TEV ProfitsStatutory Distributable Earnings

© 2009 Towers Perrin 21

Investment linked - Effect of market consistent pricing depends on charging structure

8343Cost of Capital / allowance for NHR

3.6%4.6%New Business Margin as a percentage of PVNBP

36%46%New Business Margin as a percentage of APE

109137Value of New Business

192180PVFP before CoC

MCEVTraditional EV

© 2009 Towers Perrin 22

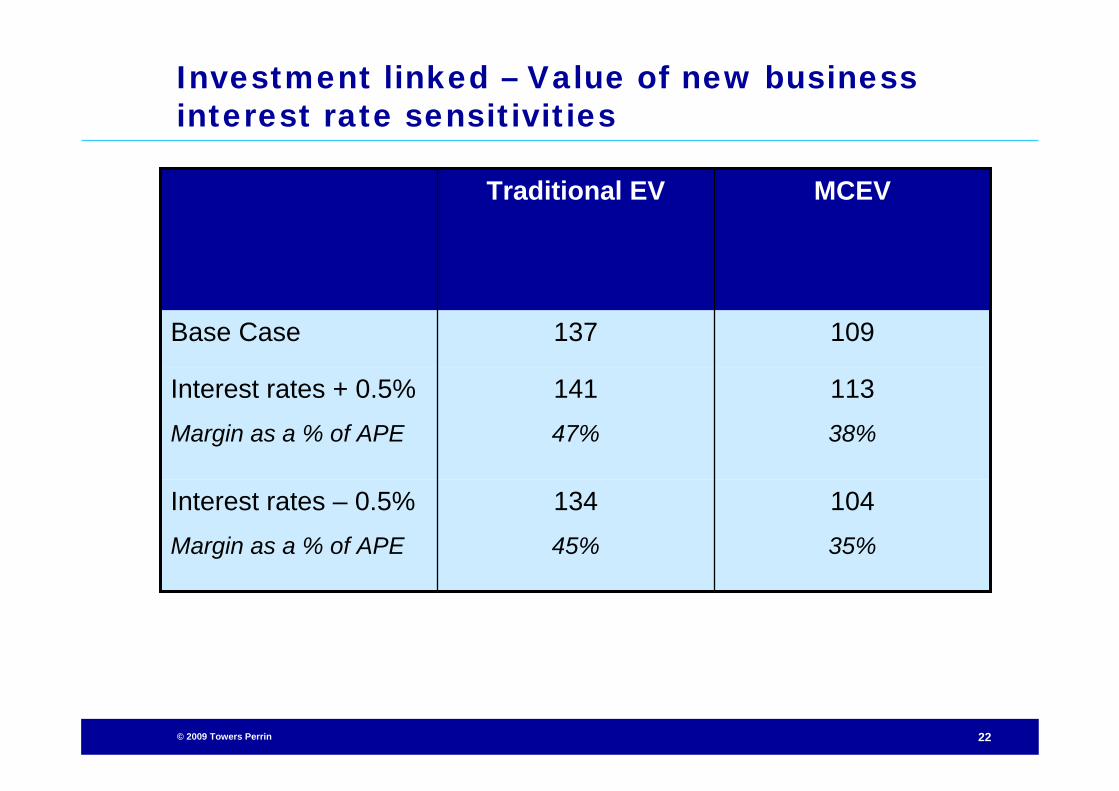

Investment linked – Value of new business interest rate sensitivities

10435%

13445%

Interest rates – 0.5%Margin as a % of APE

11338%

14147%

Interest rates + 0.5%Margin as a % of APE

109137Base Case

MCEVTraditional EV

© 2009 Towers Perrin 23

Participating product – Expected profit profile (on deterministic assumptions)

Comparison of profit patterns on a Statutory and Embedded Value basis - Par product

(200)

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 Y13 Y14 Y15

Year

Ann

ual P

rofit

TEV Profits

Statutory DistributableEarnings

© 2009 Towers Perrin 24

Participating product – Margins may reduce if include significant options and guarantees

174173Cost of Capital / allowance for NHR

530-Cost of O&Gs

3.8%7.6%New Business Margin as a percentage of PVNBP

31%45%New Business Margin as a percentage of APE

9761,418Value of New Business

1,6551,591PVFP before CoC

MCEVTraditional EV

© 2009 Towers Perrin 25

…and the sensitivity to economic conditions is much greater

554-43%

1,350-5%

Interest rates – 0.5%Percentage change

1,76681%

1,559+10%

Interest rates + 1.25% Percentage change

(785)-180%

1,235-13%

Interest rates – 1.25% Percentage change

1,284+32%

1,479+4%

Interest rates + 0.5%Percentage change

9761,418Base Case

MCEVTraditional EV

© 2009 Towers Perrin 26

How much capital is required to support the business?

Traditionally, capital requirements and sufficiency have been measured relative to regulatory capital requirements

These measures are normally simple to calculate (e.g. 4% percentage of reserves and 0.3% of the sum-at-risk in this example) but do not always reflect the underlying risks in the product

Regulatory requirements are moving towards risk-based capital requirements, so…

How do traditional regulatory capital requirements compare to estimated economic capital requirements (on a stand-alone basis) for our worked example at the point of sale?

© 2009 Towers Perrin 27

Statutory vs economic capital requirements

Mkt. Value

of Assets

Assets Liabilities

Marketconsistentliabilities

Statutory

Liability

Solvency

Margin

Excesscapital

Economic capital requirementsStatutory

Basis

Availablestat. capital

Economic

Capital

requirements

Required

Capital

Greater of statutory and excess of economic over

statutory reserves

MCVIF

AvailableEcon Capital

© 2009 Towers Perrin 28

Comparison of statutory and regulatory capital requirements by product

577%50%118%Economic as a percentage of statutory

92160751Economic capital requirements

160120637Statutory capital requirements

Traditional participating

product

SP

Unit-linked

Term Assurance

© 2009 Towers Perrin 29

Analysis of economic capital requirements for sample participating policy

160

976

1,761

260

157 282

1,897

Statutoryrequiredcapital

Derivation of economic capital requirements

MCVNB Market

Risk

Underwriting

Risk

Operating

Risk

Diversification

Required

Capital

Required

EC

© 2009 Towers Perrin 30

Summary of findings from worked example

These examples show that “profitability” can depend as much on the metrics used as the underlying products

“Traditional” reporting metrics do not necessarily give the complete picture even with sensitivity analyses

Even if not reported, economic (market consistent) measures are relevant from a business management point of view:

Include the cost of options and guaranteesReflects appropriately the different risk profiles of different product types Helps to understand the risk in the product and is linked to risk management and mitigation

© 2009 Towers Perrin 31

Agenda

The aims of product pricing

A worked example – The impact of metrics on pricing results

Turning “product cost” into “product price”

Conclusions

© 2009 Towers Perrin 32

It is helpful to split out the elements of price

Cost of Liability

Cost of Capital

Profit margin

Reflectscost of liabilities taken on.

Breakeven price in absenceof capital costs

Reflects cost of holdingcapital.

Breakeven price

Cost of production.Price at which no value added

or destroyed.‘Mechanical’ calculation

Price charged.Reflects target margins and

constraints

Price charged.No ‘mechanical’ approach

possible

© 2009 Towers Perrin 33

Targets should reflect…

The profitability that has been promised (and demonstrated) to shareholders

Management objectives

Market expectations set by peers

Management’s view of the price that can be charged in a market

Subject to:

Maximum individual risk exposures

Regulatory constraints

Diversification limits

In general, not all of these are subject to rigorous calculation. Target setting cannot be reduced to a mechanical process

© 2009 Towers Perrin 34

Agenda

The aims of product pricing

A worked example – The impact of metrics on pricing results

Turning “product cost” into “product price”

Conclusions

© 2009 Towers Perrin 35

Conclusions

Move beyond “mechanical” product pricing

Pricing metrics need to be linked to how performance is measured, but…

External metrics changeUnderstand the limitations of your pricing and reporting metrics

Separate the price charged from the product cost

Need to understand and communicate effectively the risk and profitability profile of the product so that the product development process can meet the objectives of the company

Go beyond the minimum so you can play an effective part of the product development process

© 2009 Towers Perrin 36

Thank You!

James Creedon

Senior Consultant

Tillinghast

Phone: (852) 2593-4519