product market competition and voluntary corporate social

TRANSCRIPT

1

Product Market Competition and Voluntary Corporate Social

Responsibility Disclosures

Ji Woo Ryou Robert C. Vackar College of Business & Entrepreneurship

University of Texas Rio Grande Valley Email: [email protected]

Albert Tsang

Schulich School of Business York University

E-mail: [email protected]

Kun (Tracy) Wang Research School of Accounting Australian National University E-mail: [email protected]

March 2018

Abstract

The objective of this study is to examine whether and how firms’ voluntary forward-looking non-financial disclosures, specifically corporate social responsibility (CSR) disclosures, are associated with the intensity of product market competition (PMC). Using multiple measures of PMC, including the level of non-price competition, product similarity, managers’ perceptions of competition, and reductions of industry-level import tariff, our study finds that the likelihood, frequency, and length of standalone CSR disclosures decrease with the intensity of PMC, and especially so for CSR disclosures containing product-related content. We also find that the intensity of PMC not only affects the level of CSR disclosures, but also the quality of CSR disclosures, as measured by the likelihood of CSR disclosure with external assurance and CSR disclosure following global reporting initiative (GRI) guidelines. Taken together, our findings suggest that although CSR reporting can be associated with various capital market benefits and/or even used as a marketing tool, especially when PMC is intense, the proprietary cost concern associated with such disclosures hinders firms’ CSR reporting incentives. Keywords: Proprietary costs; Voluntary disclosure; External Assurance; GRI; CSR Reporting Quality

2

Product Market Competition and Voluntary Corporate Social

Responsibility Disclosures

1. Introduction

Economic theory posits that proprietary cost is an important determinant inhibiting

firms’ voluntary disclosures (Verrecchia, 1983, 2001). 1 Despite the importance of the

proprietary cost argument in explaining firms’ disclosure incentives, prior studies typically

focus on, and examine its role in, financial disclosures (e.g., Ali et al., 2014; Chen et al., 2010;

Darrough & Stoughton, 1990; Dhaliwal et al., 2014; Li, 2010; Seavey et al., 2016; Skinner,

1994), and there is relatively little empirical evidence on the relationship between firms’

proprietary cost concern and their voluntary non-financial disclosure decisions. As such, the

objective of this study is to extend this literature and examine whether and how firms’ voluntary

non-financial disclosure decisions, specifically corporate social responsibility (CSR)

disclosures, are influenced by the intensity of product market competition (PMC).

Following the growing awareness of CSR activities in building social capital (Patten &

Zhao, 2014), reducing information asymmetry and the cost of equity capital (Crifo et al., 2015;

Dhaliwal et al., 2011, 2012), protecting firm value (Christensen, 2016), signaling firms’ future

financial perspectives (Lys et al., 2015), and creating a competitive advantage (e.g., KPMG,

2008, 2011, 2013; McWilliams & Siegel, 2011; Nikolaeva & Bicho, 2011), many corporations

have started to provide standalone CSR disclosures voluntarily during recent years, illustrating

the importance they attach to such activities and communicating their CSR initiatives to key

stakeholders, such as consumers (e.g., Luo & Bhattacharya, 2006; Muslu et al., 2017; Servaes

& Tamayo, 2013; Patten & Zhao, 2014). As a result, over the last few decades, information

1 Supporting the theory, anecdotal evidence also shows that concern regarding a firm’s competitive position is a major constraint on firms’ voluntary disclosures (Graham et al., 2005).

3

about a firm’s CSR activities and performance has become increasingly useful to customers

when making purchase decisions (Lev et al., 2010; Servaes & Tamayo, 2013).

Increased competition can also drive companies to go beyond a conventional marketing

mix to incorporate CSR attributes into their marketing initiatives in order to gain competitive

advantages (Fisman et al., 1998; Sen et al., 2006). Supporting this view, existing studies argue

that CSR engagement can be considered as an important product attribute with the potential to

increase the attractiveness of firms’ products, improve customer satisfaction and loyalty, and

ultimately lead to greater revenue and firm value (Baron, 2001; Bhattacharya & Sen, 2004;

Creyer & Ross, 1997; Navarro, 1998; Luo & Bhattacharya, 2006; Sen & Bhattacharya, 2001).

More directly supporting the importance of CSR in enhancing firms’ competitive

advantage, Flammer (2015) and Fernández-Kranz and Santaló (2010) find that increased PMC

leads to increased CSR engagement. In the same vein, Johnson (1966) and Fisman et al. (2008)

argue that the benefits of CSR can be more substantial in more competitive industries because

CSR can signal the quality of their products, thereby allowing firms to differentiate themselves

from rivals. Thus, to the extent that CSR activities have the potential to foster future sales

and/or create capital market benefits, especially when competition is intense, we predict a

positive association between the intensity of PMC and firms’ CSR reporting decisions.

On the other hand, although the literature suggests that voluntarily disclosing

information, such as non-financial CSR information, can be associated with various capital

market benefits (see Huang & Watson [2015] and Liu et al. [2017] for a review of CSR

reporting literature), the proprietary cost hypothesis suggests that managers face a trade-off

between the potential benefits associated with voluntary disclosures and the costs of revealing

proprietary information. While prior studies mainly tested the proprietary cost hypothesis using

the context of forward-looking financial disclosures such as management earnings forecasts

(see Hirst et al. [2008] for a review on major determinants of management earnings forecasts),

4

this hypothesis likely applies to forward-looking non-financial disclosure as well, as long as

the information concerned can aid firms’ current and potential rivals in competing with the

disclosing firms.

This concern is particularly pronounced for CSR reporting, given that many standalone

CSR disclosures contain information about the development process, technologies used, and

future plans of firms’ products, which can aid both potential and existing competitors to gain

competitive advantages. Consistent with our argument, Guo et al. (2004) examine the

disclosures of product-related information disclosed on the initial public offering (IPO)

prospectuses issued by biotech firms and find evidence in line with proprietary cost concern.

Following this discussion, to the extent that CSR disclosures contain competition-sensitive

information, we predict a negative positive association between the intensity of PMC and firms’

CSR reporting decisions.

Taken together, our discussion above suggests that ex ante, it is unclear whether and

how proprietary cost concern or pressure from PMC is associated with firms’ CSR reporting

incentives. Given the ambiguous relationship predicted above, whether and how voluntary

CSR disclosures are associated with the intensity of PMC is an empirical question which we

examine in this study.

Using the setting of voluntary standalone CSR disclosure to examine the effect of

proprietary cost on firms’ disclosure decisions offers several advantages. First, Leuz (2004)

notes that a major challenge in empirically testing the proprietary costs hypothesis is the lack

of settings in which proprietary disclosures are clearly voluntary. For example, Rogers and

Buskirk (2013) point out that although the management earnings forecasts literature spans

several decades, the question of whether management earnings forecasts are truly voluntary is

still an open question. In line with this view, other studies suggest that management earnings

forecasts may not be entirely voluntary because the institutional environments, such as

5

securities laws and stock exchange requirements, have a significant influence on managers’

earnings forecast decisions (Heitzman et al., 2010; Li et al., 2012). However, as opposed to

management earnings forecasts, or information disclosed in other mandatory corporate

reporting,2 standalone CSR disclosures are clearly more voluntary, especially given the fact

that they are subject to few specific reporting guidelines (Chen et al., 2016; Ramanna, 2013).

Second, compared to CSR information disclosed on firms’ annual reports or released

through other channels (e.g., corporate websites), standalone CSR disclosures tend to cover

topics that are broader in scope and provide more extensive information about CSR activities,

and often also contain information about the firm’s product development and differentiation

strategy.3 Because managers have substantial discretion over the disclosure of CSR reporting

in terms of both the quantity and the quality of the information (Muslu et al., 2017), our focus

on CSR reporting thus offers a clearer test of the existing theory (i.e., the proprietary cost

hypothesis) and its assertions on firms’ voluntary disclosure decisions. Moreover, by focusing

on standalone CSR disclosure, it not only fosters a better comparison across disclosing firms,4

but also the concern that the CSR information disclosed through other channels (e.g., in firms’

annual reports or on corporate websites) is likely bundled with other competition-sensitive

information (such as information about existing customers documented by Ellis et al. [2012])

can also be minimized. Indeed, it is common that firms release different types of information

in a bundle. For example, Liu et al. (2017) provide empirical evidence that firms tend to bundle

non-financial information strategically with negative earnings information to mitigate the

capital market consequences associated with their negative earnings news.

2 This information includes, for example, product-related information in IPO prospectuses (Guo et al., 2004), customer information in SEC filings (Ellis et al., 2012), and firms’ decision to redact material contract information from their IPO SEC registration filings (Boone et al. 2016) or financial reports (Verrecchia & Weber, 2006). 3 Examples of CSR disclosure containing product-related information are provided in Appendix B. 4 One clear advantage of providing standalone CSR reports is that it can better communicate CSR initiatives (Morsing & Schultz, 2006).

6

Data on standalone CSR disclosure of U.S. firms during the period from 1999 to 2011

were hand-collected from CorporateRegister.com. For each standalone CSR report collected,

we studied its content and identify whether or not a CSR report contains product-related

information, and if it does, how much space (e.g., the number of pages) is dedicated to such

content. Following previous studies, we use multiple proxies to measure the intensity of PMC

including (1) non-price competition (Chen et al., 2015), (2) product similarity (Hoberg &

Phillips, 2016), and (3) manager-perceived competition (Li et al., 2013).

Consistent with the prediction of the proprietary cost hypothesis, across all measures of

PMC, we find that the likelihood, frequency, and length of CSR disclosures decrease with the

intensity of PMC, and especially so for CSR disclosures containing product-related content.

To address the concern regarding the endogeneity of PMC, we further use the large reduction

of import tariff rates in the U.S. manufacturing sector during our sample period as an exogenous

shock to firms’ competitive environment (Fresard, 2010; Valta, 2012) and examine how firms’

CSR reporting practices differ following the tariff reduction. Using a difference-in-difference

methodology, consistent with the findings based on other competition measures, our result

shows that tariff reductions (i.e., a proxy for increased competitive pressure) lead to decreases

in CSR reporting.

More directly, our result shows that firms facing intensive competition pressure tend to

provide less competition-sensitive information on their CSR disclosures measured by the

number of pages containing product-related information on standalone CSR disclosure. In

addition to the level of CSR disclosure (i.e., likelihood, frequency, and length of CSR

reporting), we find that the intensity of PMC can also have a significant impact on the quality

of CSR disclosures measured by the likelihood of CSR disclosures with external assurance and

7

CSR disclosures following GRI reporting guideline.5 Together, these findings suggest that

proprietary cost is indeed an important consideration in firms’ voluntary CSR reporting

decisions.

Moreover, we document a robust positive association between the issuance of CSR

disclosure and firms’ future sales revenue after controlling for firms’ actual CSR performance,

suggesting that CSR reporting is associated with future financial performance. This finding is

consistent with the financial performance implications of CSR reporting documented by prior

studies (e.g., Lev et al., 2010; Lys et al., 2015). More importantly, our results also show that

the level of product-related information disclosures on CSR reporting (measured by the ratio

of total number of pages dedicated to product-related information in a CSR disclosure over the

total number of pages of a CSR disclosure) is positively associated with future sales revenue,

even after controlling for the issuance of firms’ CSR disclosure. This finding lends support to

the role of CSR in product market competition. Furthermore, following the argument that PMC

creates disincentives for transparent CSR disclosures, we interact the CSR reporting variable

measuring the level of product-related content on a CSR report with PMC variables in

examining the relationship between CSR reporting and future revenue. Consistent with our

finding that a higher level of PMC can have a negative effect on CSR reporting quality, the

untabulated results show that the intensity of PMC weakens the relationship between CSR

disclosure and future sales revenue.

Our paper contributes to the literature in several ways. First, one of the most notable

changes in corporate disclosure practices during recent years in countries around the world has

been the increasing number of companies that have voluntarily committed to publishing

standalone CSR reports (KPMG, 2008, 2011, 2013). However, we know relatively little about

5 We also find some, albeit relatively weak, evidence indicating that the intensity of PMC is negatively associated with the readability of standalone CSR disclosures.

8

the determinants of this emerging disclosure practice (Ramanna, 2013). The literature on CSR

reporting documents multiple firm-level characteristics as factors affecting firms’ CSR

reporting practices, such as external capital needs (Dhaliwal et al., 2011), and signaling firms’

future financial performance (Lys et al., 2015) and CEOs’ ability (Chen et al., 2017). By

providing evidence showing that the intensity of PMC attenuates firms’ CSR reporting

incentives, our study thus adds to the literature by identifying an important, yet previously

unidentified, determinant of CSR reporting—concern regarding revealing competition-

sensitive proprietary information to rivals. Examining this issue is also of contemporary

importance to regulators and other interested parties who are concerned about CSR reporting,

which is evidenced by the Securities and Exchange Commission’s (SEC) (2016) call for

feedback on the potential challenges and costs associated with disclosing CSR information.

Given the increasing trend of regulations of CSR reporting around the world (Chen, et al., 2018;

Ioannou & Serafeim, 2017), we believe it is timely and important to examine the factors that

constrain firms from voluntary CSR disclosures.

Additionally, managers frequently rank proprietary cost as one of their major concerns

in influencing their voluntary disclosure decisions (Graham et al., 2005). Despite the

prevalence of the proprietary cost argument in the accounting literature, existing studies

typically focus on the effect of proprietary costs on disclosures with a strong financial

implication,6 while other voluntary disclosures, such as the quantity and quality of CSR

disclosures, have not yet been explored. In this study, we directly examine the effect of

proprietary cost concern on firms’ CSR reporting practices, and thus our study extends research

on the role of PMC in determining managers’ reporting choices (e.g., Datta et al., 2013;

Dhaliwal et al., 2014; Ellis et al., 2012).

6 For example, prior studies examine the effect of proprietary cost on management earnings forecasts (Ali et al. 2014; Li, 2010), segment information (Botosan & Stanford, 2005), information about major customers (Ellis et al., 2012), and information about firms’ strategies (Bhojraj et al., 2004).

9

The rest of this paper is organized as follows. Section 2 summarizes the prior literature

and develops hypotheses. Section 3 describes the sample, variable definitions, and empirical

model specification. Section 4 presents the summary statistics and reports the main empirical

results. Section 5 discusses additional analyses. Finally, in Section 6, we draw our conclusions.

2. Background and Hypothesis Development

2.1. The importance of voluntary CSR disclosure

The importance of CSR activities to business has been acknowledged by both existing

research and anecdotal evidence. For example, Fombrun and Shanley (1990, p. 239) argue that

the CSR engagement of firms is an important element of product differentiation and reputation

building. Similarly, other studies (e.g., Bhattacharya & Sen, 2003; Bhattacharya et al., 2004;

Huang et al., 2017; Luo & Bhattacharya, 2006; Pérez & Del Bosque, 2015; Servaes & Tamayo,

2013) suggest that CSR is an important marketing strategy in promoting and differentiating

firms’ products, and in increasing customer satisfaction and loyalty. 7 In line with these

arguments, a survey by Cone/Ebiquity (2015) reports that 91% of global consumers expect

companies to act responsibly, and nine in ten are as likely to purchase responsible products and

services as to boycott irresponsible companies. Similarly, the Nielsen Global Survey on CSR

conducted during 2014 on more than 30,000 consumers in 60 countries suggests that 55% of

global consumers are willing to pay higher prices for products or services provided by

companies committed to positive CSR activities.8

With a growing understanding of corporate impact on both business and society,

stakeholders, such as consumers, not only expect businesses to operate responsibly, but also

7 On the basis of lab experiments, existing studies also show that CSR could affect, directly or indirectly, consumer company identification (Mohr & Webb, 2005; Sen & Bhattacharya, 2001), consumer product responses (Brown, 1998), and consumer product attitude (Beren et al., 2005). 8 See Global consumers are willing to put their money where their heart is when it comes to goods and services from companies committed to social responsibility (http://www.nielsen.com/ca/en/press-room/2014/global-consumers-are-willing-to-put-their-money-where-their-heart-is.html).

10

demand that firms robustly communicate their CSR efforts and results. Along with increasing

media coverage of CSR issues, survey evidence from Cone/Ebiquity (2015) also shows that

almost 88% of global consumers expect companies to report on the progress of their CSR

efforts. More specifically related to U.S. consumers, a recent report examining consumer

attitudes, perceptions, and behaviors around CSR reveals that 86% of U.S. consumers surveyed

expect companies not only to commit to good CSR activities, but also to communicate their

CSR actions publicly because public communication of CSR actions is perceived (by 79%

consumers) to increase the credibility of a firm’s CSR commitment.9

On the other hand, although capital market participants, such as investors, appear to be

more interested in firms’ financial information, recent evidence suggests that they are showing

increasing interest in, and paying greater attention to, how management deals with social and

environmental issues (PwC, 2017) and have increasingly considered CSR activities when

making investment decisions (Elliott et al., 2014). For example, 70% of the global investors

surveyed by PwC (2017) agree or strongly agree that it is more important for companies to

operate in a way that accounts for wide stakeholder expectations. Further supporting this view,

the recent accounting literature documents the growing importance of, and various benefits

associated with, voluntary CSR reporting for market participants, such as reducing information

asymmetry between firms and investors (Dhaliwal et al., 2011, 2012), protecting firm value

(Christensen, 2016), and signaling future financial performance (Chen et al., 2017; Lys et al.,

2015) and transparency (Chen et al., 2016; Kim et al., 2012).

In view of the strong demand for CSR information, regulators around the world have

made increased commitments and efforts requiring or encouraging firms to make CSR

disclosures during recent years (Chen et al., 2016; KPMG, 2016). One of the high-profile

attempts to regulate CSR reporting is the European Union’s adoption of Directive 2014/95/EU

9 See 2017 Cone Communications CSR study (http://www.conecomm.com/research-blog/2017-csr-study).

11

on non-financial disclosure in 2014, which requires public interest entities of a certain size to

provide CSR disclosures. In the U.S., although CSR reporting is voluntary, in April 2016 the

SEC issued a Concept Release with a call for public comments on its consideration of including

CSR disclosures in its corporate disclosure requirements.

Despite the various benefits potentially associated with communicating CSR

engagement and results, and the unprecedented pressure companies are under to do so, many

firms choose not to publish CSR reports.10 The substantial deficit of useful CSR information

available to stakeholders is also reflected in Ernst and Young’s (2015) survey, which reports

that almost two-thirds of the institutional investors surveyed around the world say companies

do not adequately disclose CSR information, and nearly 40% call for companies to do so more

fully. The significant gap between the demand for, and the supply of, CSR reports highlights

the need to explore the underlying barriers to CSR reporting.

2.2. PMC and voluntary CSR disclosure

In the absence of other considerations, the unraveling argument (Grossman, 1981;

Grossman & Hart, 1980; Milgrom, 1981) suggests that managers will voluntarily make full

disclosure of their CSR information. In contrast, the proprietary cost hypothesis (e.g., Board,

2009; Clinch & Verrecchia, 1997; Verrecchia, 1983) predicts that disclosing proprietary

information might jeopardize disclosing firms’ competitive position in the product market if

rivals or other actors make strategic use of the information to the disadvantage of the disclosing

firms. Therefore, to the extent that CSR disclosures contain competition-sensitive information,

managers’ decisions as to whether and how to report CSR information voluntarily are likely to

be a trade-off between the benefits of informing market participants, such as customers and

10 Dhaliwal et al. (2011) note that CSR disclosing firms only account for a small fraction of the population of U.S. publicly listed firms.

12

investors, and the proprietary costs of informing existing and potential rivals in a competitive

environment.

2.2.1. The positive effects of PMC on voluntary CSR disclosure

From the consumer perspective, the literature finds that CSR activities can positively

affect consumers’ attitudes, perceptions, purchase intentions, and satisfaction (e.g., Brown &

Dacin, 1997; Olsen et al., 2014; Pomering & Dolnicar, 2009; Servaes and Tamayo, 2013; Sen

et al., 2006), which in turn, increase the premiums requested for products and services, attract

new customers, and improve customer loyalty and advocacy behaviors such as positive word-

of-mouth and resilience to negative company news (Du et al., 2007; Lev et al., 2010; Sen &

Bhattacharya, 2001). In line with these findings, survey evidence also shows that CSR can

create trust among customers, attract and retain customers, and increase sales and price

premiums (Cone/Ebiquity, 2015; PwC, 2016).

Recognizing consumers as a key driver of CSR who are more concerned about firms’

CSR initiatives (Bhattacharya & Sen, 2004; Manchiraju & Rajgopal, 2017; Servaes & Tamayo,

2013), CSR disclosure can be used as an important marketing tool for more effectively dealing

with today’s increasingly competitive business environment.11 Accordingly, Hildebrand et al.

(p1359, 2011) contend that CSR appears a “near-perfect vehicle” for corporate marketing,

which can reveal not only a firm’s fundamental and relatively enduring characteristics, but also

often more distinctive and evolving characteristics. In line with these views, Eccles et al. (2014)

observe a stronger positive association between CSR and financial performance in sectors

where firms mainly compete on the basis of brands and reputations. By examining an individual

component of CSR—corporate philanthropy—Lev et al. (2010) provide empirical evidence

11 The literature acknowledges that CSR can be used as a marketing tool for building brand equity, corporate image and reputation, which in turn increase the attractiveness of their products (e.g., Hoeffler & Keller, 2002; McWilliams & Siegel, 2011; Nikolaeva & Bicho, 2011). Similarly, other studies suggest that reputation and corporate/brand image are valuable intangible assets, which can produce numerous tangible benefits in the marketplace (e.g., Fombrun & Shanley, 1990; Lev et al., 2010; Sen & Bhattacharya, 2001) such as differentiating firms from their competitors.

13

that corporate philanthropic activities are positively associated with future sales revenue,

particularly for firms that are highly sensitive to consumer perception.

In addition, prior studies show that increased competition erodes growth opportunities,

increases firm risk and uncertainty, affects a firm’s relative position on the capital markets, and

increases firms’ cost of external financing (e.g., Fresard & Valta, 2013; Hoberg et al., 2014;

Hou & Robinson, 2006; Valta, 2012). Therefore, a greater level of PMC can also lead to more

CSR disclosure if firms use CSR disclosure as a means for reducing information asymmetry

between firms and investors in order to improve their access to external capital.12 Therefore, in

light of the above discussion, we expect that firms facing greater competition are more likely

to provide CSR disclosures voluntarily.

The positive impact of CSR disclosure in a competitive environment may not be

restricted to, or primarily manifested in, the consumer and capital market domains. The

stakeholder perspective suggests that CSR disclosure is a form of stakeholder management that

builds and strengthens beneficial stakeholder relationships, which can generate multifaceted

benefits and lead to improved competitive positions. Stakeholder theory emphasizes the need

to go beyond traditional fiduciary interests to take responsibilities toward a broad range of

stakeholders for obtaining their support, which is crucial to a firm’s survival and long-term

success (Clarkson, 1995; Freeman, 1984; Freeman et al., 2001). In particular, in the presence

of increased competition that weakens a firm’s grip on its stakeholders (Zingales, 2000),

establishing and maintaining close stakeholder relationships have increasingly substituted

traditional economies of scale and become a primary driver of sustained competitive advantage

12 For example, Mattei and Platikanova (2017) find that analysts’ earnings forecasts are less precise for firms facing greater competitive threats. Valta (2012) shows that firms operating in competitive product markets are more likely to experience higher cost of debt. To the extent that CSR reporting has the potential to create capital market benefits, such as reducing cost of debt or cost of equity capital (Cheng et al., 2013), the findings of existing studies suggests that firms in highly competitive industries can have higher incentives to adopt CSR reporting strategies.

14

for firms (Lev, 2000; Morsing & Schultz, 2006).13 The efficiency and importance of CSR in

strengthening stakeholder relationships, especially when facing intense competition, is further

magnified as firms often maintain multiple stakeholder relationships (e.g., employee, investor,

and customer) simultaneously (Maignan & Ferrel, 2004; Sen et al., 2006).

The literature also suggests that given sufficient awareness, a firm’s CSR initiative may

positively affect stakeholders’ overall beliefs and attitudes toward the firm, and their intentions

to purchase products or pay a premium price for its products, and invest in the firm (e.g., Brown

& Dacin, 1997; Pomering & Dolnicar, 2009; Sen et al., 2006; Trudel & Cotte, 2009). This

discussion suggests that firms are more likely to disclose standalone CSR reports to effectively

strengthen their long-lasting relationships with multiple stakeholders in a more competitive

environment, which leads to the following hypotheses:

H1a. The intensity of PMC is positively associated with standalone CSR disclosure. H1b. The intensity of PMC is positively associated with standalone CSR disclosure containing product-related information.

2.2.2. The negative effects of PMC on voluntary CSR disclosure

Prior theoretical works (e.g., Board, 2009; Clinch & Verrecchia, 1997; Verrecchia,

1983) show that in a variety of circumstances imparting proprietary information might

jeopardize disclosing firms’ competitive position in the product markets if rivals make strategic

use of the information to their advantage. Consequently, companies have less incentive to

disclose when PMC is more intense given that the proprietary costs of voluntary disclosure are

high. This prediction is supported by a body of empirical studies in various contexts, including,

for instance, segment reporting (Bens et al., 2011; Leuz, 2004; Prencipe, 2004), management

13 For example, Hildebrand et al. (2011) note that a firm’s CSR engagements are likely to cause stakeholders to form strong and long-lasting bonds with the firm. These effective relationships with stakeholders, in turn, can generate intangible, socially complex, and imperfectly imitable resources that enhance a firm’s sustainable competitive advantage against its rivals (Hillman & Keim, 2001).

15

earnings forecasts (e.g., Ali et al., 2014; Huang et al., 2016), R&D information (Jones, 2007),

sales and costs information in public filings (Dedman & Lennox, 2009), product-related

information in IPO prospectuses (Guo et al., 2004), customer information in SEC filings (Ellis

et al., 2012), and material contract information in SEC filings (Boone et al., 2016; Verrecchia

et al., 2006).

In the context of CSR disclosure, it is plausible that voluntary disclosure of CSR

information can incur non-trivial proprietary costs. For example, CSR can be viewed as a form

of product innovation (e.g., the creation of new socially responsible product features or

categories) or process innovation (e.g., the use of a socially responsible production process),

which can differentiate a firm’s products from its competitors and contribute to a sustainable

competitive advantage (Flammer, 2015; Fernández-Kranz & Santaló, 2010; Fomburn &

Shanley, 1990; McWilliams & Siegel, 2001; 2011). Supporting this view, the opponents of

mandatory CSR disclosure rules argue that CSR disclosure regulation can decrease firm value

by forcing firms to disclose proprietary or competitively sensitive information (Ioannou &

Serafeim, 2017).

The concerns regarding the proprietary costs of CSR disclosure are evidenced by

companies’ responses to the SEC’s 2016 Concept Release, when industry commenters

expressed concerns that disclosing CSR information would be advantageous to competitors

(Thomas & Maguire, 2016). Furthermore, using a sequential game theoretical model to explain

firms’ observed reluctance to disclose environmental liability information, Li et al. (1997)

show that with stakeholders’ increasing awareness of environmental issues, the expected

proprietary costs of disclosing environmental liability information increase and thus companies

become less likely to disclose. The above discussion thus leads to our alternative hypotheses:

H2a. The intensity of PMC is negatively associated with standalone CSR disclosure.

16

H2b. The intensity of PMC is negatively associated with standalone CSR disclosure containing product-related information.

3. Sample, Variable Definitions, and Methodology

3.1. Sample selection

To test the empirical question of our study, we collect all standalone CSR disclosures

issued by U.S. firms during the period from 1999 to 2011 from the Corporate Register (an

online directory of corporate social responsibility reports), following prior studies (e.g., Chen

et al., 2016; Dhaliwal et al., 2011; Muslu et al., 2017). For each standalone CSR report collected,

we further manually collect information about whether a standalone CSR disclosure contains

product-related information disclosure, and if it does, how many pages of the disclosure are

dedicated to such information. 14 We then collect financial statement data from COMPUSTAT,

stock return data from the Center for Research in Security Prices (CRSP), the CSR performance

data from MSCI (formerly KLD), and management earnings guidance data from the First Call

database. Our final sample consists of 13,989 firm-years with no missing control variables,

associated with 2,565 distinct firms. Among them, a total of 1,120 firm-years are identified

with standalone CSR disclosure issuance during our sample period.15

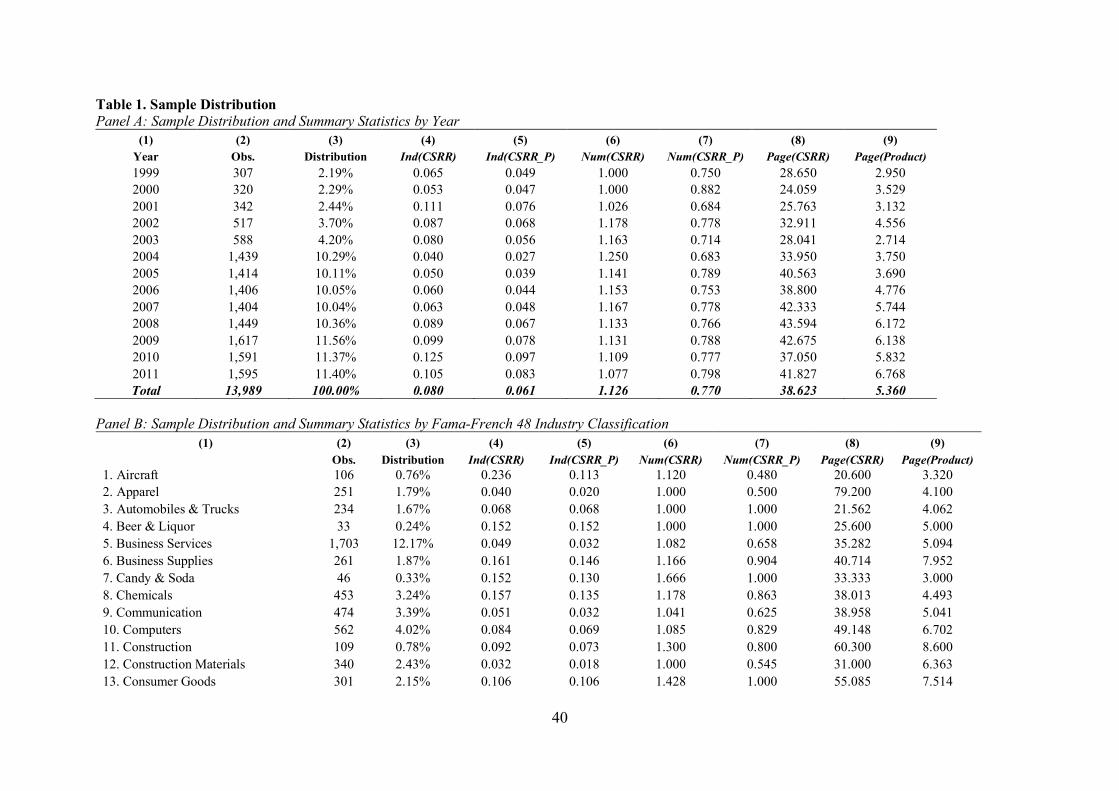

Panel A of Table 1 presents the sample distribution by year and reports the summary

statistics of our main measures of CSR disclosure. Our result indicates that during our sample

period, the percentage of firms publishing standalone CSR reports ranges between 4% (in 2004)

and 12.5% (in 2010), with an average 8% of firms providing standalone CSR reports (Column

4, Ind(CSRR)). Some firms do not disclose product-related information even though they do

publish standalone CSR reports. The percentage of firms disclosing standalone CSR reports

14 Because the hand collection of standalone CSR reports and identifying the total number of pages dedicated to product-related information on each CSR report required substantial effort and time, our sample period ends in 2011. 15 Specifically, a total of 319 distinct firms issuing 1,249 standalone CSR disclosures are identified as voluntary CSR reporters during our sample period. The total number of CSR disclosures is greater than the total number of firm-year observations because some firms issued more than one standalone CSR report in a year.

17

with product-related information disclosure in each year ranges between 2.7% (in 2004) and

9.7% (in 2010), with an average 6.1% of firms providing standalone CSR reports containing

product-related information (Column 5, Ind(CSRR_P)).

The results also suggest that on average, each standalone CSR report has 38.6 pages

(Column 8, Page (CSRR)), with 5.4 pages (14%) dedicated to product-related information

(Column 9, Page (Product)), indicating that the level of product-related contents reported in

CSR disclosures is indeed non-trivial.

Panel B of Table 1 presents the sample distribution and summary statistics by the

Fama–French 48 industry classifications. The business service industry (#5) constitutes the

largest proportion of the final sample (12.17%), followed by the retail industry (#32, 7.56%)

and the electronic equipment industry (#16, 7.46%). The precious metals industry has the

lowest number of firms in our sample; however, it has the highest proportion of firms within

the industry (#28, 35.7%) issuing CSR reports. Non-pollution-prone industries such as aircraft

(#1), business supplies (#6), consumer goods (#13), and food products (#18) also have a high

proportion of firms disclosing CSR reports, suggesting that CSR-disclosing firms are not

limited to firms in high-polluting industries.

Insert Table 1 around here

3.2. Measurement of variables

3.2.1. PMC

Drawing on prior literature (Chen et al., 2015; Fresard, 2010; Hoberg & Philips, 2016;

Karuna, 2007; Li et al., 2013; Valta, 2012), we use several proxies to measure the intensity of

PMC to capture the different dimensions of competition faced by a company. First, following

Chen et al. (2015) we use non-price competition (Comp_NonPrice), calculated as the sum of

firm-level advertising expenses and R&D expenses divided by the sum of firm-level sales in

an industry, as our first proxy of PMC. This measure is developed based on the argument in

18

the economics literature that increasing advertising and R&D expenses is a non-price approach

to increase demand for a product or service (Chen et al., 2015). A higher value of

Comp_NonPrice corresponds to a greater extent of non-price competition.

The second proxy of PMC used by our study is the text-based product similarity scores

(Comp_ProdSimilarity). Hoberg and Phillips (2016) provide the product similarity vector and

firm-by-firm pairwise similarity scores by parsing the product descriptions from the firm 10-

Ks and forming word vectors for each firm to compute continuous measures of product

similarity for every pair of firms in our sample in each year. 16 A higher value of

Comp_ProdSimilarity refers to a greater extent of PMC.

The third proxy of PMC used by our study is managers’ perceived competition

(Comp_MgmPerception), as suggested by Li et al. (2013).17 The SEC recommends that the

management discussion and analysis (MD&A) section of a firm’s 10-K filing includes a

discussion of the firm’s competitive position, and thus the MD&A section provides a valuable

source for measuring managers’ perceptions of competition. Accordingly, they measure

management’s perceptions of the intensity of PMC that managers face by using textual analysis

of the firm’s 10-K filing. Specifically, Comp_MgmPerception is calculated as the number of

occurrences of “competition, competitor, competitive, compete, and competing” scaled by the

total number of words in a firm’s 10-K filing. This measurement responds to management’s

concern about PMC at the firm level. A higher value of manager perception refers to a greater

extent of PMC.

The last measure of PMC used in our study is created by exploiting an exogenous shock

to firms’ competitive environment to address endogeneity concerns (Fresard, 2010; Valta,

16 The product similarity vector data are downloaded from the Hoberg-Phillips Data Library (http://hobergphillips.usc.edu/). We thank Prof. Hoberg and Prof. Phillips for providing these data. 17 The data on managers’ perceived competition are downloaded from Prof. Li’s website: http://webuser.bus.umich.edu/feng/. We again thank Prof. Li for his generosity in providing these data to the public domain.

19

2012). Specifically, we use the reduction of import tariff rates to capture exogenous changes

to a firm’s PMC. The reduction of import tariff rates captures an unexpected reduction of trade

barriers, which facilitates the penetration of foreign rivals into a domestic product market,

resulting in intense PMC. Using tariff data for the U.S. manufacturing sector, we identify 54

industries that experienced a large import tariff rate reduction during our sample period. A

large import tariff rate reduction is defined as an import tariff reduction that is three times

greater than the median tariff reduction (Fresard, 2010; Valta, 2012). Accordingly, the

reduction of import tariff rates (Comp_TariffCut) is equal to one if an industry has experienced

a large tariff reduction at time t, and zero otherwise.18

3.2.2. CSR disclosure

We use several variables to measure firms’ voluntary CSR disclosures and their

attributes. For CSR disclosure, we use three variables including: (1) the incidence (Ind(CSRR)),

(2) frequency (Num(CSRR)), and (3) length (Page(CSRR)) of CSR reporting. Specifically,

Ind(CSRR) is an indicator variable equal to one if a firm provides any standalone CSR reporting

voluntarily in a given year, and zero otherwise. Num(CSRR) is the frequency (or total number)

of the standalone CSR reporting voluntarily issued by a firm in a given year. Page(CSRR) is

the total number of pages of all (if more than one) standalone CSR reporting voluntarily issued

by a firm in a given year.

Our discussion in Section 2 suggests that concerns regarding aiding competitors can

create a disincentive for voluntary CSR disclosures. To the extent that CSR disclosures contain

product-related information, such as future product development and innovative production

processes (see examples provided in Appendix B), these arguments should be more applicable

18 In additional analysis, following Li (2010), who classifies PMC into competition from potential versus existing rivals, we also employ two additional PMC measures (Comp_Potential and Comp_Existing). Comp_Potential is mainly derived from the three components: industry-average of property, plant and equipment, industry-average R&D expense and industry-average capital expenditures. Comp_Existing is mainly derived from the Herfindahl-Hirchman index, four-firm concentration ratio, and the total number of firms operating in an industry.

20

to CSR disclosures with product information disclosure. Thus, in our study, to tie our

arguments with our empirical designs more closely, we also introduce several additional CSR

reporting variables, including (1) Ind(CSRR_P), an indicator variable equal to one if a firm

provides product-related information/content in its standalone CSR reporting in a given year,

and zero otherwise; (2) Num(CSRR_P), the frequency (or total number) of the standalone CSR

reporting containing product-related contents voluntarily issued by a firm in a given year; (3)

Page(Product), the total number of pages of product-related information on a firm’s CSR

disclosure issued by the firm in a given year (only when the product-related information on a

single page accounts for more than half of the content of that page, we count it as one page);

and (4) Ratio(Product/Total), the ratio of total number of pages of CSR reporting dedicated to

product-related information to the total number of pages of CSR reporting.19

3.3. Methodology

To test our hypotheses, we use the following regression model to investigate whether

and how PMC is associated with standalone CSR reporting voluntarily issued by firms.

CSRRit= β0 + (β1 × COMPit) + (∑s βs × Controls) + (∑y βy × Year_Indicators) +

(∑n βn × Industry_Indicators) + ε

where CSRR is the CSR reporting variables and COMP is the PMC measures discussed above.

Following prior studies (e.g., Dhaliwal et al., 2011), we control for other factors influencing

standalone CSR disclosures, including: the total KLD score of CSR strengths (CSRPERF), firm

size (SIZE), litigation risk (LITIGATION), profitability (ROA), financial activities (FINANCE),

Tobin’s Q (TOBINQ), financial leverage (LEVERAHE), overseas income (GLOBAL), stock

liquidity (LIQUDITY), management forecast disclosure (FORECAST), and earnings quality

19 We do not find a significant relation between intensity of PMC and Ratio (Product/Total) (i.e., the ratio of total number of pages dedicated to product-related information to the total number of pages of CSR reporting) and thus these results are not tabulated. To the extent that greater levels of competition reduce the length of CSR disclosures in general and the number of pages dedicated to product related information in particular, such a finding is not surprising.

21

(ACCRUALS). All continuous variables are winsorized at the top and bottom one percentiles.

In all regressions, we also include industry and year fixed effects.

4. Results

4.1. Descriptive statistics

Panel A of Table 2 reports the descriptive statistics for all the major variables used in

the study. The lower percentage of firms providing standalone CSR disclosure (8%) during our

sample period is indeed surprising, given the significantly positive association between CSR

disclosure and the various capital market benefits documented by previous studies. The

likelihood of firms providing standalone CSR disclosures with product-related information is

even lower (6%), thereby supporting the possible higher proprietary cost concerns associated

with such disclosures. Table 2 also shows that the firms in our sample are profitable, with an

average ROA of 4.2%, and most have foreign income. Among the sample firm-years, less than

one-third (27.7%) operate in a high-litigation industry, and over 40% voluntarily issue earnings

forecasts.

Panel B of Table 2 presents the univariate comparison across firms with different levels

of competition across each of the four competition measures. We split the sample into high and

low competition subgroups based on the sample median of each competition measure. Across

all measures of competition, our CSR disclosure variables are generally smaller in the high

competition group compared to the low completion group, thereby providing initial and

preliminary support to Hypotheses 2a and 2b that PMC is negatively associated with standalone

CSR disclosures.

Insert Table 2 around here

Table 3 presents the correlation matrix of key variables, with Pearson’s correlation

coefficients in the lower triangle and Spearman’s rank correlations in the upper triangle. In

22

general, the CSR reporting variables are correlated negatively with our proxies of PMC, except

for Comp_NonPrice. Regarding the control variables, consistent with the literature, the CSR

disclosure variables tend to correlate positively with larger and globally oriented firms and

firms with more CSR strengths.

Insert Table 3 around here

4.2. Regression results

In our study, we predict that the intensity of PMC can either be positively or negatively

associated with voluntary CSR disclosure. Table 4 presents our main results using non-price

competition, Comp_NonPrice, as the proxy for PMC. Across all CSR reporting variables,

Comp_NonPrice is significantly and negatively associated with CSR disclosure, thus

supporting both Hypotheses 2a and 2b. Specifically, holding CSR performance and other

factors constant, when Comp_NonPrice increases by one unit, the log-odds of issuing

standalone CSR disclosure decreases by 8.8628 units, and the log-odds of being in a category

of higher frequency of CSR disclosure (Num(CSRR)) or longer CSR disclosure (Page(CSRR))

reduces by 7.8591 and 8.4199 units, respectively.20

The coefficients of the control variables generally have the expected signs, and are

consistent across different measures of CSR disclosure. Firms with larger size, more CSR

strengths, better profitability, higher leverage, and a global focus tend to provide more CSR

disclosures voluntarily. Conversely, firms with higher levels of external financing, Tobin’s Q,

and liquidity tend to issue less CSR disclosures. These findings are generally consistent with

those reported by prior studies (e.g., Dhaliwal et al., 2011).

Insert Table 4 around here

20 We obtain qualitatively similar results when we estimate the regressions of Page(CSRR) and Page(Product) using OLS specification instead of Ordered Logit model .

23

In our first multivariate test, we use non-price competition as the proxy for PMC. To

examine whether our results are sensitive to the measurement of competition, we employ two

alternative measures of competition based on textual analysis of firms’ 10-K filings: product

similarity (Comp_ProdSimilarity) and management’s perceptions of the intensity of

competition (Comp_MgmPerception). In contrast to the non-price competition measure, these

two measures do not rely on predetermined industry groups. To the extent that managers have

reasonably accurate perceptions of the type and level of competition they face, product

similarity and management’s perceptions of the intensity of competition should be able to

capture the dynamic competitive environment within which a firm operates.

Table 5 shows that the coefficients on Comp_ProdSimilarity are significantly negative

across all regressions with different measures of CSR disclosure. Since presumably firms with

higher product similarity are less able to differentiate their products from competitors and thus

tend to face more intense competition, our results strongly suggest that competition is

associated with lower levels of CSR disclosure. Similarly, Table 6 shows that the coefficients

on Comp_MgmPerception, i.e., management’s perceptions of the intensity of competition are

generally negative across all regressions, albeit less significant when Page(Product) is used as

the dependent variable. Together, these results again provide a strong support for our

Hypotheses 2a and 2b, suggesting a negative association between the intensity of competition

and CSR disclosures.

Insert Table 5 around here

Insert Table 6 around here

24

5. Additional Analyses

5.1. Alternative proxies of PMC

The results so far show that competition has the potential to reduce CSR disclosure.

However, a common concern is the potential endogeneity of PMC because the intensity of

competition and firms’ choice of CSR disclosure may be jointly determined. For example, a

firm could strategically use its financing policy to affect market competition by hurting its

rivals’ profitability and driving them out of the market (Valta et al., 2012); while in the

meantime, the firm’s probability of disclosing CSR information may also be affected by their

financing decisions (Dhaliwal et al., 2011). To address this concern, we explore a quasi-natural

experimental setting by examining firms’ CSR disclosure in response to an unexpected

reduction in industry import tariffs. Specifically, we use the tariff rate reduction as an

exogenous shock to firms’ competitive environment because presumably the reduction of tariff

rates can trigger competitive pressure due to the lowered barriers to entering product markets

and increased presence of foreign rivals on the domestic markets. For this purpose, we define

an indicator variable, Comp_TariffCut, which equals one if the industry has experienced a large

tariff reduction in year t and zero otherwise.

Table 7 reports the regression results. Albeit with a much smaller sample size due to

the focus on manufacturing firms, Comp_TariffCut is significantly negative in all regressions

with different measures of CSR disclosure as the dependent variable. These results substantiate

the main finding that a higher level of competition pressure significantly decreases firms’ CSR

reporting incentive.

Insert Table 7 around here

5.2. Disclosure of product-related information in CSR reporting and future sales revenues

Our results suggest that firms trade off the potential benefits of CSR disclosure against

the proprietary costs associated with such disclosure, and thus report less when facing greater

25

competitive pressures. In this section, we examine the potential implication of CSR disclosure

on future sales by empirically examining the relation between CSR disclosure and future sales

revenue measured by SALESt+1, SALESt+2, and SALESt+3, respectively.

Consistent with the positive relation between CSR disclosure and future financial

performance documented by prior studies (e.g., Lev et al., 2010; Lys et al., 2015), the results

presented in Columns 1–3 of Table 8 show a significantly positive association between CSR

disclosure measured by Ind(CSRR) and future sales across all models. More importantly, the

results also indicate a positive association between the level of product-related information on

a CSR report (measured by the ratio of total number of pages dedicated to product-related

information to the total number of pages of CSR reporting, i.e., Ratio(Product/Total)) and

future sales even after controlling for the issuance of CSR disclosure. Additionally, we do not

find a significant relation between CSR performance (CSRPERF) and future sales, which is

consistent with the mixed findings about the effect of CSR performance on future financial

performance reported in the literature (Margolis et al. 2009). Finally, in Columns 4–6, we

replace Ratio(Product/Total) by Ratio(Product/Total)_First, which is the Ratio(Product/Total)

measured from the first CSR report issued by a firm during our sample period, and rerun the

regressions to better address reverse causality concerns. We find our inferences unchanged.

As a further test, we examine the effect of competition on the relation between CSR

disclosure and future sales revenue. If proprietary cost concerns indeed affect the information

content or quality of CSR disclosure, one can predict that the relation between CSR disclosure

and future sales should be weakened when the intensity of PMC is high. To test this conjecture,

we interact the CSR disclosure variable Ratio(Product/Total) and an aggregated competition

variable Comp_Overall (created using the principal component of our competition measures

except Comp_TariffCut) which captures the overall level of PMC of each firm in our regression

models and find evidence supporting our conjecture. For example, while our results continue

26

to show a positive association between Ratio(Product/Total) and future sales, we find a

significantly negative estimated coefficient for the interaction term between

Ratio(Product/Total) and intensity of PMC measured by Comp_Overall. We do not tabulate

the results for the sake of brevity.

Insert Table 8 around here

5.3. PMC and properties/quality of CSR disclosure

In our main tests, we show that competition not only decreases the likelihood and

frequency of CSR disclosures, it also decreases the length of CSR disclosure in general and the

number of pages containing product-related information in particular. In this section, we further

examine the effect of competition on the characteristics of CSR reporting. Specifically, we

focus on the assurance of CSR reporting and the adoption of GRI guidelines, which are

arguably suggestive of the disclosure quality of CSR reports (Hahn & Kühnen, 2013; Laufer,

2003; Muslu et al., 2017).

When the verification of disclosed information is impossible or not available,

competition may reduce disclosure quality because firms may engage in a “cheap-talk”

communication game (Crawford & Sobel, 1982). Newman and Sansing (1993) show that firms

may distort their voluntary disclosures to discourage potential new competitors from entering

the market. The implication of these studies for CSR reporting is that firms may produce low

quality CSR disclosures when the competition is intense.

While the evidence from additional analysis presented above (i.e., a significant and

negative coefficient between Ratio(Product/Total) and Comp_Overall) appears to support this

conjecture, to directly and empirically test this conjecture, we obtain CSR reporting assurance

data (CSR_Assurance) and the adoption of GRI guidelines data (GRI_Report) for each

standalone CSR disclosure from Thomson Reuters ASSET4. CSR_Assurance is an indicator

variable that equals one if a firm publishes a standalone CSR report with external assurance in

27

a given year, and zero otherwise. GRI_Report is an indicator variable that equals one if a firm

publishes a standalone CSR report in accordance with GRI guidelines in a given year, and zero

otherwise. We replace the dependent variable in our regression models with CSR_Assurance

or GRI_Report, and rerun the regressions.21

Table 9 reports the regression results. Across all four measures of competition, we find

the intensity of product market competition is associated with a lower likelihood of CSR

reporting assurance and the adoption of GRI guidelines, except in Column 2. This finding is

consistent with the conjecture that the intensity of competition is likely associated with a lower

quality of CSR reporting practice.

Insert Table 9 around here

Recent studies argue that disclosure readability may also be indicative of disclosure

quality. For example, Li (2008), You and Zhang (2009) and Miller (2010) find that the level of

financial reporting readability affects investors’ willingness or ability to acquire information

from financial disclosures. Rennekamp (2012) further shows that disclosure readability affects

investors’ feelings of processing fluency, which in turn affects their related judgments and

decisions, even when disclosure readability does not affect the amount of information that they

acquire. As such, one conjecture is that when facing greater level of competition, firms are

more likely to provide less readable CSR reports in order to hide or obfuscate competition-

sensitive information. Following this argument, we examine whether and how competition is

associated with the readability of CSR disclosures.

We use the Fog and Flesch-Kincaid indices obtained from textual analysis of CSR

narrative to measure the level of readability of CSR disclosure. Consistent with our conjecture,

21 The sample sizes for the regressions reduce substantially in these tests, because only the sample with CSR reporting can be included for this test.

28

the untabulated results show some suggestive evidence that competition is associated with less

readable CSR disclosures, although in most cases, the effect is only marginally significant.

5.4. Potential versus existing rivals and CSR disclosure

The effect of competition on disclosure may be different between competition from

potential entrants and that from existing rivals (Li, 2010). To explore whether the effect of

competition on CSR disclosure varies with different type of rivals, we follow Li (2010) and

distinguish between competition from potential entrants (Comp_Potential) and competition

from existing rivals (Comp_Existing), which are constructed based on principal component

analysis of multiple industry-level competition variables (the detailed variable definitions are

provided in Appendix A). We then replace the competition measure in our regression models

by Comp_Potential and Comp_Existing, and rerun the regressions.

The results are reported in Table 10. Consistent with Li (2010)’s study on voluntary

financial disclosure measured by management earnings forecasts, Comp_Existing is associated

with less CSR disclosure; however, the coefficients are not statistically significant at

traditionally levels. Therefore, we do not have convincing evidence that competition from

existing rivals significantly affects CSR reporting. On the other hand, the coefficients on

Comp_Potential are significantly negative in all of the regression models, indicating that

competition threats from potential rivals reduce CSR disclosure.22

While our results are different from those reported by Li (2010), who shows that higher

competition from potential entrants is associated with more voluntary disclosure in the context

of management forecasts on profits and investments, Li interprets this finding as due to firms

choosing to voluntarily disclose more financial information to deter potential entrants from

entering into the markets. However, unlike forecasts on profits and investments that can be

22 For example, a one unit increase in Comp_Potential leads to a 0.1729 unit decrease in the log-odds of disclosing CSR reports, and a 0.1889 unit decrease in the log-odds of disclosing product-related information in CSR reports.

29

considered as an early revelation of information before the public release of financial

statements, the information disclosed on CSR reports, for example, product-related information

can be more competition-sensitive. Under this circumstance, disclosing CSR information may

not be perceived as a good entry deterrence strategy by managers due to the high proprietary

costs of such disclosure.23

Insert Table 10 around here

6. Conclusion

During recent years, CSR disclosures have gained significant prominence and

increasing visibility in the business world. In this study, we examine firms’ decisions regarding

CSR disclosure in the presence of PMC. We find the likelihood, frequency, and length of

standalone CSR reporting decrease with the intensity of PMC. The negative effect of

competition on CSR reporting issuance and frequency is also magnified for CSR disclosure

specifically containing product-related information. These results are robust to different

measures of competition to capture the different dimensions of PMC, including non-price

competition, product similarity, and managers’ perceptions of competition. Using tariff rate

reductions as an exogenous shock to firms’ competitive environment, we show that our finding

is unlikely to be driven by endogenous PMC.

Additional analyses show that firms experience larger sales revenue following CSR

reporting, which is consistent with the argument that firms trade off the economic benefits and

the proprietary costs of CSR reporting. Moreover, our results show that competition attenuates

the positive relation between CSR disclosure and future sales revenue, suggesting that

23 A firm’s CSR disclosure of how to embed CSR activities into its business models, especially how to harness technology and innovation to deliver CSR-oriented products and services, may provide know-how to its competitors, enabling them to mimic the disclosing firm’s successful business models and diminish its competitive advantages. Indeed, survey evidence shows that CEOs increasingly view competitor information as important for them to gain competitive advantages, especially long-term oriented information such as new product initiatives and changes in corporate strategies (PwC, 2002).

30

proprietary cost concern reduces the information content of CSR disclosure, which affects the

predictive power of CSR disclosure for future financial performance.

Our further analysis of CSR reporting characteristics indicates that competition can also

be associated with lower CSR reporting quality, measured by the likelihood of providing

external assurance for CSR disclosure, the propensity of providing CSR disclosures prepared

under GRI reporting guidelines, and the level of readability of the CSR disclosure (albeit

weakly). Finally, in contrast to prior research on competition in the context of voluntary

financial disclosure, we find that competition threats from potential rivals reduce CSR

disclosure, suggesting that the disclosure of non-financial information is not perceived by firms

as an effective strategy to deter the entry of potential rivals due to the high proprietary costs

concerns about CSR reporting. Overall, the findings of our study add to the literature by

showing that proprietary costs concerns affect not only financial disclosures, as evidenced in

the literature, but also can have a significant effect on non-financial disclosures.

31

References Ali, A., Klasa, S., & Yeung, E., 2014. Industry concentration and corporate disclosure policy. Journal

of Accounting and Economics 58, 240-264. Baron, D.P., 2001. Private politics, corporate social responsibility, and intgreated strategy. Journal of

Economics & Management Strategy 10, 7–45. Beren, G., van Riel, C.B.M., van Bruggen, G.H., 2005. Corpoate associaotns and consumber product

responses: The moderating role of corpoate brand dominance. Journal of Marketing 69, 35–48. Bens, D.A., Berger, P.G., Monahan, S.J., 2011. Discretionary disclosure in financial reporting: An

examination comparing internal firm data to externally reported segment data. The Accounting Review 86, 417–449.

Bhattacharya, C.B., Sen, S., 2003. Consumber-company identfication: A framework for understanding consumbers’ relationships with companies. Journal of Marketing 67, 76–88.

Bhattacharya, C.B., Sen, S., 2004. Doing better at doing good: When, why, and how consumers respond to corporate social initiatives. California Management Review 47, 9–24.

Bhattacharya, C.B., Smith, N,C., Vogel, D., 2004. Integrating social responsibility and marketing strategy: An introdcution. California Management Review 47, 6–8.

Bhojraj, S., Blacconiere, W.G., S’Souza, J.D., 2004. Voluntary disclosure in a multi-audience setting: an empirical investigation. The Accounting Review 79, 921–947.

Board, O., 2009. Competition and disclosure. The Journal of Industrial Economics 57, 197–213. Boone, A.L., Floros, I.V., Johnson, S.A., 2016. Redacting proprietary information at the initial public

offering. Journal of Financial Economics 120, 102–123. Botosan, C.A., Stanford, M., 2005. Managers’ motives to withhold segment disclosures and the effect

of SFAS No. 131 on analysts’ information environment. The Acconting Review 80, 751–771. Brown, T.J., Dacin, P.A., 1997. The company and the product: Corporate associations and consumer

product responses. Journal of Marketing 61, 68–84. Brown, T.J., 1998. Corporate associations in marketing: Antecedents and consequences. Corporate

Reputation Review 1, 215–233. Chen, Y., Hung, M., Wang, Y., 2018. The effect of mandatory CSR disclosure on firm profitability and

social externalities: Evidence from China. Journal of Accounting and Economics 65, 169–190. Chen, S., Matsumoto, D., Rajgopal, S., 2010. Is silence golden? An empirical analysis of firms that stop

giving quarterly eranings quidance. Journal of Accounting and Economics 51, 134–150. Chen, C.X., Matsumura, E.M., Shin, J.Y., Wu, S.Y.C., 2015. The effect of competition intensity and

competition type on the use of customer satisfaction measures in executive annual bonus contracts. The Accounting Review 90, 229–263.

Chen, L., Srinidhi, B., Tsang, A., Yu, W., 2016. Audited financial reproting and voluntary disclosure of corporate social responsibility (CSR) reports. Journal of Management Accounting Research 28, 53–76.

Chen, L., Liao, C., Tsang, A., 2017. CEO tenure and corporate social responsibility (CSR) reporting. Working paper. George Mason Univerisity.

Cheng, B., Ioannou, I., Serafeim, G., 2013. Corporate social responsibility and access to finance. Strategic Management Journal 35, 1–23.

Christensen, D. M., 2016. Corporate accountability reporting and high-profile misconduct. The Accounting Review 91, 377-399.

Clarkson, M.E., 1995. A stakeholder framework for analyzing and evaluating corporate social performance. Academy of Management Review 20, 92–117.

Clinch, G., Verrecchia, R.E., 1997. Competitive disadvantage and discretionary disclosure in industries. Australian Journal of Management 22, 125–137.

Cone/Ebiquity, 2015. Global CSR study. Cone Communications LLC. See http://www.conecomm.com/research-blog/2015-cone-communications-ebiquity-global-csr-study.

Creyer, E.H., Ross, W.T. Jr., 1997. The influence of firm behavior on purchase intension: Do consumers really care about business ethics. Journal of Consumer Marketing 14, 421–432.

Crifo, P., Forget, V.D., Teyssier, S., 2015. The price of environmental, social and governance practice disclosure: An experiment with professional private equity investors. Journal of Corporate Finance 30, 168–194.

32

Crawford, V. P., Sobel, J., 1982. Strategic information transmission. Econometrica 50, 1431–1451. Darrough, M.N., Stoughton, N.M., 1990. Financial disclosure policy in an entry game. Journal of

Accounting and Economics 12, 219–243. Datta, S., Iskandar-Datta, M., Singh, V., 2013. Product market power, industry structure, and corporate

earnings management. Journal of Banking and Finance 37: 3273–3285. Dedman, E., & Lennox, C., 2009. Perceived competition, profitability and the withholding of

information about sales and the cost of sales. Journal of Accounting and Economics 48, 210–230. Dhaliwal, D.S., Huang, S., Khurana, I.K., Pereira, R., 2014. Product market competition and conditional

conservatism. Review of Acounting Studies 19: 1309–1345. Dhaliwal, D.S., Li, O.Z., Tsang, A., Yang, Y.G., 2011. Voluntary nonfinancial disclosure and the cost

of equity capital: The initiation of corporate social responsibility reporting. The Accounting Review 86, 59–100.

Dhaliwal, D.S., Radhakrishnan, S., Tsang, A., Yang, Y.G., 2012. Nonfinancial disclosure and analyst forecast accuracy: International evidence on corporate social responsibility disclosure. The Accounting Review 87, 723–759.

Du, S., Bhattacharya, C.B., Sen, S., 2007. Reaping relational rewards from corporate social responsibility: The role of competitive positioning. International Journal of Research in Marketing 24, 224–241.

Eccles, R.G., Ioannou, I., Serafeim, G., 2014. The impact of corporate substainability on orgnaizational processes and performance. Management Science 60, 2835–2857.

Elliott, W.B., Jackson, K.E., Peecher, M.E., White, B.J., 2014. The unintended effect of corporate social responsibility performance on investors’ estimated of fundamental value. The Accounting Review 89, 275–302.

Ellis, J.A., Fee, C.E., Thomas, S.E., 2012. Proprietary costs and the disclosure of information about customers. Journal of Accounting Research 50, 685–727.

Ernst & Young, 2015. Tomorrow's Investment Rules 2.0. Ernst & Young LLP. Fernández�Kranz, D., Santaló, J., 2010. When necessity becomes a virtue: The effect of product market

competition on corporate social responsibility. Journal of Economics & Management Strategy 19, 453–487.

Fisman, R., Heal, G., Nair, V., 2008. A model of corporate philanthropy. Working paper. Columbia University.

Flammer, C., 2015. Does product market competition foster corporate social responsibility? Evidence from trade liberalization. Strategic Management Journal 36, 1469–1485.

Fombrun, C., Shanley, M., 1990. What's in a name? Reputation building and corporate strategy. Academy of Management Journal 33, 233–258.

Freeman, R.E., 1984. Strategic Management: A Stakeholder Approach. New York: Cambridge. Freeman, R.E., McVea, J.I., 2001. A stakeholder approach to strategic management. In: Hitt M,

Freeman RE & Harrison J (eds.) The Blackwell Handbook of Strategic Management. Blackwell, Malden, MA, pp. 189–207.

Fresard, L., 2010. Financial strength and product market behavior: The real effects of corporate cash holdings. The Journal of Finance 65, 1097–1122.

Frésard, L., Valta, P., 2013. Competitive pressure and corporate investment: evidence from trade liberalization. Working paper. University of Maryland.

Graham, J.R., Harvey, C.R., Rajgopal, S., 2005. The economic implications of corporate financial reporting. Journal of Accounting and Economics 40, 3–73.

Grossman, S.J., 1981. The informational role of warranties and private disclosure about product quality. The Journal of Law and Economics 24, 461–483.

Grossman, S.J., Hart, O.D., 1980. Disclosure laws and takeover bids. The Journal of Finance 35, 323–334.

Guo, R.J., Lev, B., Zhou, N., 2004. Competitive costs of disclosure by biotech IPOs. Journal of Accounting Research 42, 319–355.

Hahn, R., Kühnen, M., 2013. Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. Journal of Cleaner Production 59, 5–21.

33

Heitzman, S., Wasley, C., Zimmerman, J., 2010. The joint effects of materiality thresholds and voluntary disclosure incentives on firms’ disclosure decisions. Journal of Accounting and Economics 49, 109–132.

Hildebrand, D., Sen, S., Bhattacharya, C., 2011. Corporate social responsibility: A corporate marketing perspective. European Journal of Marketing 45, 1353–1364.

Hirst, D.E., Koonce, L., Venkataraman, S., 2008. Management earnings forecasts: A revew and framework. Accountng Horizons 22, 315–338.

Hillman, A.J., Keim, G.D., 2001. Shareholder value, stakeholder management, and social issues: what's the bottom line? Strategic Management Journal 22, 125–139.

Hoberg, G., Phillips, G., Prabhala, N., 2014. Product market threats, payouts, and financial flexibility. The Journal of Finance 69, 293–324.

Hoberg, G., Phillips, G., 2016. Text-based network industries and endogenous product differentiation. Journal of Political Economy 124, 1423–1465.

Hoeffler, S., Keller, K.L., 2002. Building brand equity through corporate societal marketing. Journal of Public Policy & Marketing 21, 78–89.

Hou, K., Robinson, D.T., 2006. Industry concentration and average stock returns. The Journal of Finance 61, 1927–1956.

Huang, M., Cheng, Z., Chen I., 2017. The importance of CSR in forming customer-company identification and long-term loyalty. Journal of Services Marketing 31, 63–72.

Huang, Y., Jennings, R., Yu, Y., 2016. Product market competition and managerial disclosure of earnings forecasts: Evidence from import rariff rate reductions. The Accounting Review 92, 185–207.

Huang, X B, Watson L., 2015. Corporate social responsibility research in accounting, Journal of Accounting Literature 34, 1–16.

Ioannou, I., Serafeim, G., 2017. The consequences of mandatory corporate sustainability reporting. Working paper. London Business School.

Johnson, O., 1966. Corporate philanthropy: An analysis of corporate contribution. Journal of Business 39: 489–504.

Jones, D., 2007. Voluntary disclosure in R&D-intensive industries. Contemporary Accounting Research 24, 489–522.

Karuna, C., 2007. Industry product market competition and managerial incentives. Journal of Accounting and Economics 43, 275–297.

Kim, Y., Park, M. S., & Wier, B., 2012. Is earnings quality associated with corporate social responsibility? The Accounting Review 87, 761-796.

KPMG, 2016. Carrots Sticks: Global trends in sustainability reporting regulation and policy. KPMG International.

KPMG, 2008. KPMG International Survey of Corporate Responsibility Reporting 2008. Zurich, Switzerland: KPMG International.

KPMG, 2011. KPMG International Survey of Corporate Responsibility Reporting 2011. Zurich, Switzerland: KPMG International.

KPMG, 2013. KPMG Internatinal Survey of Corporate Responsibility Reporting 2013. Zurich, Switzerland: KPMG International.

Laufer, W.S., 2003. Social accountability and corporate greenwashing. Journal of Business Ethics 43, 253–261.

Leuz, C., 2004. Proprietary versus non-proprietary disclosures: Evidence from Germany. In: Leuz C, Pfaff D & Hopwood A (eds.) The Economics and Politics of Accounting. Oxford University Press, Oxford, pp. 164–197.

Lev, B., 2000. Intangibles: Management, Measurement, and Reporting. Brookings Institution Press, Washington, DC.

Lev, B., Petrovits, C., Radhakrishnan, S., 2010. Is doing good good for you? How corporate charitable contributions enhance revenue growth. Strategic Management Journal 31, 182–200.

Li, Y., Richardson, G.D., Thornton, D.B., 1997. Corporate disclosure of environmental liability information: Theory and evidence. Contemporary Accounting Research 14, 435–474.

Li, F., 2008. Annual report readability, current earnings, and earnings persistence. Journal of Accounting and Economics 45, 221–247.

34