product costing job order allocates costs to products that are readily identifiable common in...

TRANSCRIPT

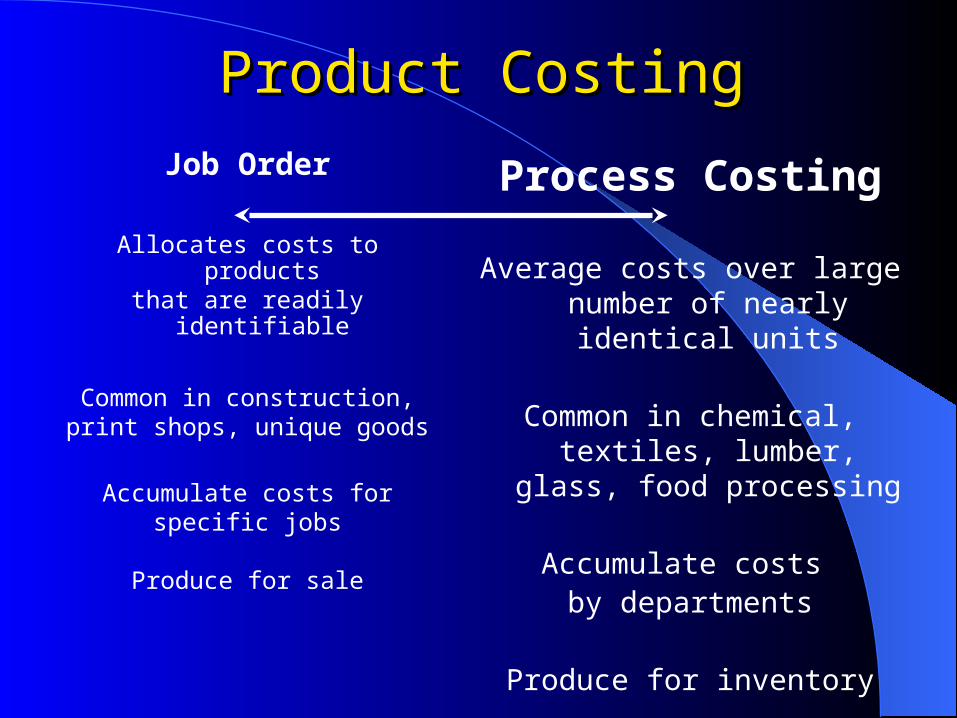

Product CostingProduct Costing

Job Order

Allocates costs to productsthat are readily identifiable

Common in construction,print shops, unique goods

Accumulate costs forspecific jobs

Produce for sale

Process Costing

Average costs over large number of nearly identical units

Common in chemical, textiles, lumber, glass, food processing

Accumulate costs by departments

Produce for inventory

Job-Order versus Process CostingJob-Order versus Process Costing

Direct materials

Direct labour

Factory overhead

Direct materials

Direct labour

Factory overhead

Job 100

Job 101

Job 102

FinishedGoods

Inventory

Cost of GoodsSold

Process A

FinishedGoods

Inventory

Cost of GoodsSold

Process B

Process C

Process Costing

Job-Order Costing

Similarities Between Job-Order and Process Similarities Between Job-Order and Process CostingCosting

• Both systems assign material, labour and overhead costs to products and they provide a mechanism for computing unit product cost.

• Both systems use the same manufacturing accounts, including Manufacturing Overhead, Raw Materials, Work in Process, and Finished Goods.

• The flow of costs through the manufacturing accounts is basically the same in both systems.

• Both systems assign material, labour and overhead costs to products and they provide a mechanism for computing unit product cost.

• Both systems use the same manufacturing accounts, including Manufacturing Overhead, Raw Materials, Work in Process, and Finished Goods.

• The flow of costs through the manufacturing accounts is basically the same in both systems.

Differences Between Job-Order and Process Differences Between Job-Order and Process CostingCosting

• Process costing is used when a single product is produced Process costing is used when a single product is produced on a continuing basis or for a long period of time. Job-order on a continuing basis or for a long period of time. Job-order costing is used when many different jobs are worked on costing is used when many different jobs are worked on each period.each period.

• Process costing systems accumulate costs by department. Process costing systems accumulate costs by department. Job-order costing systems accumulated costs by individual Job-order costing systems accumulated costs by individual jobs.jobs.

• Process costing systems use department production reports Process costing systems use department production reports to accumulate costs. Job-order costing systems use job to accumulate costs. Job-order costing systems use job cost sheets to accumulate costs.cost sheets to accumulate costs.

• Process costing systems compute unit costs by department. Process costing systems compute unit costs by department. Job-order costing systems compute unit costs by job on the Job-order costing systems compute unit costs by job on the job cost sheet.job cost sheet.

• Process costing is used when a single product is produced Process costing is used when a single product is produced on a continuing basis or for a long period of time. Job-order on a continuing basis or for a long period of time. Job-order costing is used when many different jobs are worked on costing is used when many different jobs are worked on each period.each period.

• Process costing systems accumulate costs by department. Process costing systems accumulate costs by department. Job-order costing systems accumulated costs by individual Job-order costing systems accumulated costs by individual jobs.jobs.

• Process costing systems use department production reports Process costing systems use department production reports to accumulate costs. Job-order costing systems use job to accumulate costs. Job-order costing systems use job cost sheets to accumulate costs.cost sheets to accumulate costs.

• Process costing systems compute unit costs by department. Process costing systems compute unit costs by department. Job-order costing systems compute unit costs by job on the Job-order costing systems compute unit costs by job on the job cost sheet.job cost sheet.

© 2012 Pearson Prentice Hall. All rights reserved.

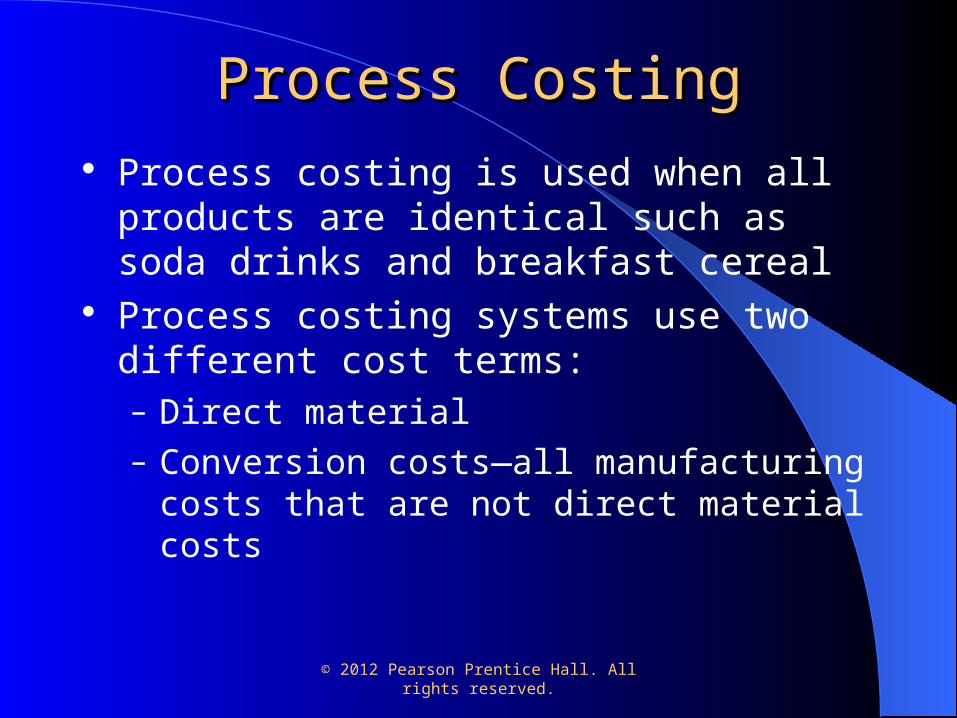

Process CostingProcess Costing Process costing is used when all products are

identical such as soda drinks and breakfast cereal Process costing systems use two different cost

terms:– Direct material– Conversion costs—all manufacturing costs that are

not direct material costs

Equivalent Units of ProductionEquivalent Units of Production

Equivalent units are the product of the number of partially completed units and the percentage completion of those

units.

We need to calculate equivalent units because a department usually has some partially completed units

in its beginning and ending inventory.

Equivalent Units Equivalent Units – The Basic – The Basic IdeaIdea

Two half completed products are equivalent to one completed product.

Two half completed products are equivalent to one completed product.

So, 10,000 units 70% completeare equivalent to 7,000 complete units.

So, 10,000 units 70% completeare equivalent to 7,000 complete units.

+ = 1

Compute and Apply CostsCompute and Apply Costs

The formula for computing the cost per equivalent unit is :

Cost perequivalent

unit

=

Cost of beginningwork in process

inventory Cost added during

the period

Equivalent units of production

+

Beginning work in process: 200 units

Materials: 55% complete $ 9,600Conversion: 30% complete 5,575

Production started during May 5,000 unitsProduction completed during May 4,800 units

Costs added to production in MayMaterials cost $ 368,600Conversion cost 350,900

Ending work in process 400 unitsMaterials: 40% completeConversion: 25% complete

Beginning work in process: 200 units

Materials: 55% complete $ 9,600Conversion: 30% complete 5,575

Production started during May 5,000 unitsProduction completed during May 4,800 units

Costs added to production in MayMaterials cost $ 368,600Conversion cost 350,900

Ending work in process 400 unitsMaterials: 40% completeConversion: 25% complete

Compute and Apply CostsCompute and Apply Costs

Weighted-Average ExampleWeighted-Average Example

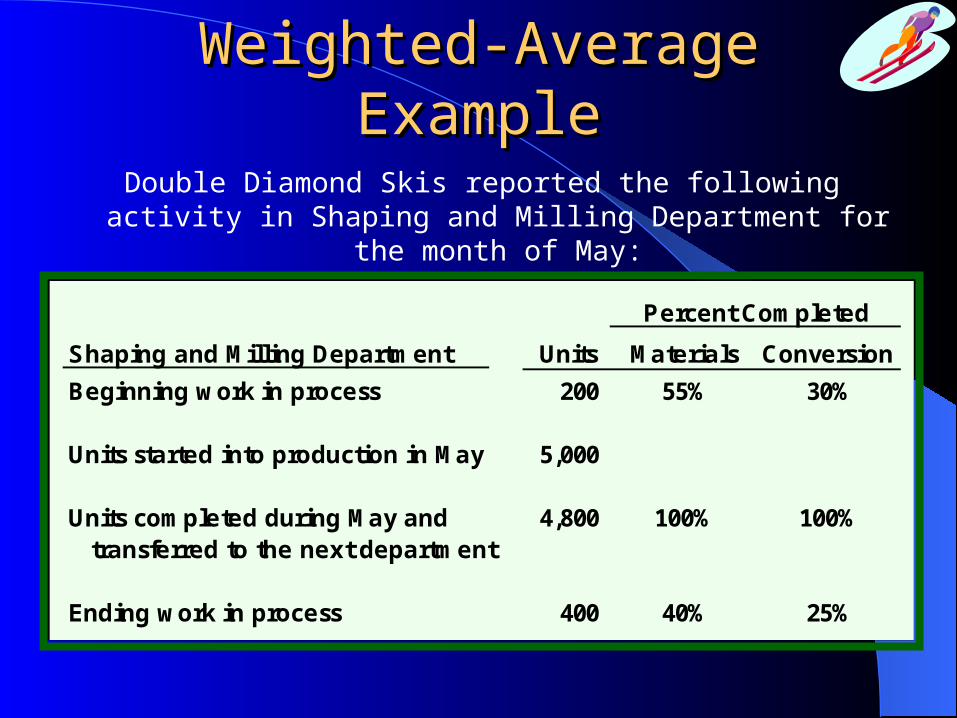

Double Diamond Skis reported the following activity in Shaping and Milling Department for the month of May:

Percent Completed

Shaping and Milling Department Units Materials Conversion

Beginning work in process 200 55% 30%

Units started into production in May 5,000

Units completed during May and 4,800 100% 100% transferred to the next department

Ending work in process 400 40% 25%

Weighted-Average ExampleWeighted-Average Example

Materials Conversion

Units completed and transferred to the next department 4,800 4,800

Work in process, June 30:

400 units × 40% 160

400 units × 25% 100

Equivalent units of Production in during the month of May 4,960 4,900

TotalCost Materials Conversion

Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900

Total cost 734,675$ 378,200$ 356,475$

Equivalent units 4,960 4,900

Cost per equivalent unit 76.25$ 72.75$ Total cost per equivalent unit = $76.25 + $72.75 = $149.00

Compute and Apply CostsCompute and Apply Costs

$356,475 ÷ 4,900 units = $72.75$356,475 ÷ 4,900 units = $72.75 $378,200 ÷ 4,960 units = $76.25

Here is a schedule with the cost and equivalent unit information.

Computing the Cost of Units Transferred Computing the Cost of Units Transferred OutOut

Materials Conversion TotalEnding work in process inventory: Equivalent units of production 160 100 Cost per equivalent unit 76.25$ 72.75$ Cost of ending work in process inventory 12,200$ 7,275$ 19,475$

Units completed and transferred out: Units transferred to the next department 4,800 4,800 Cost per equivalent unit 76.25$ 72.75$ Cost of units transferred out 366,000$ 349,200$ 715,200$

Shaping and Milling DepartmentCost of Ending Work in Process Inventory and the Units Transferred Out

© 2012 Pearson Prentice Hall. All rights reserved.

Activity-Based CostActivity-Based CostSystemsSystems

Chapter 5

Copyright 2010 Pearson Education Canada

Traditional CostingTraditional Costing Also called cost smoothing or peanut butter

costing Spread the costs of conversion uniformly among

products and services Appropriate if:

– Indirect costs are a small proportion of total costs– Activities are consumed uniformly in the

production process Inappropriate otherwise: leads to overcosting and

undercosting of products and services

© 2012 Pearson Prentice Hall. All rights reserved.

Traditional Manufacturing Traditional Manufacturing Costing SystemsCosting Systems

Typical volume-based cost drivers include:– Direct labor hours– Machine hours– Direct labor dollars

Adequate for companies with high-volume products with similar production volumes and batch sizes

Can lead to product cost distortion in an environment of high product variety

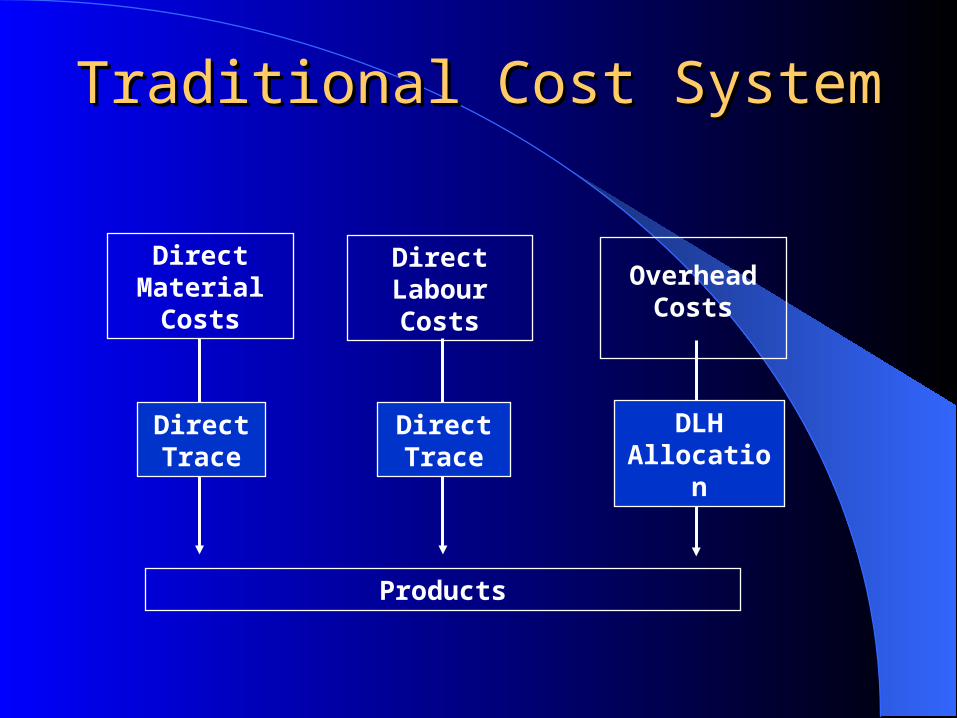

Traditional Cost SystemTraditional Cost System

DirectMaterialCosts

DirectLabourCosts

OverheadCosts

DirectTrace

DirectTrace

DLHAllocation

Products

ABC Cost SystemABC Cost System

DirectMaterialCosts

DirectLabourCosts

Overhead Costs

DirectTrace

DirectTrace

Products

Machiningactivitycosts

Assemblyactivitycosts

Inspectionactivitycosts

# of partsProcessing

Hours# of

inspections

© 2012 Pearson Prentice Hall. All rights reserved.

Activity-Based Cost SystemsActivity-Based Cost Systems Activity-based cost systems have been developed

to eliminate distortion

Time-driven activity-based costing systems (TDABC or Time-Driven ABC) estimate two parameters and then assign indirect costs similar to the way direct costs are assigned

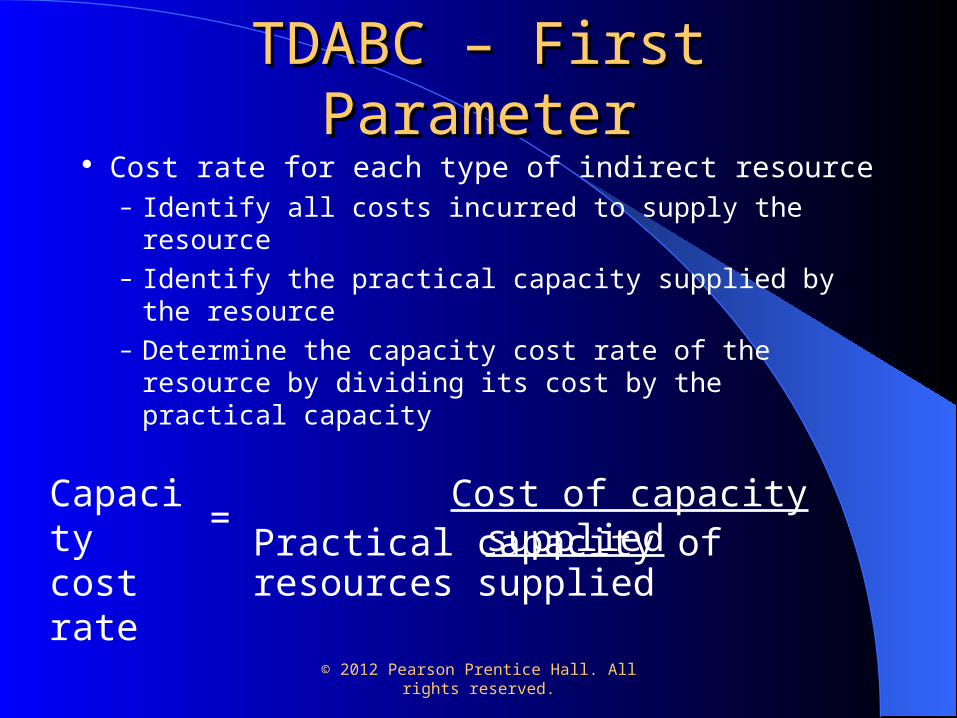

TDABC – First ParameterTDABC – First Parameter Cost rate for each type of indirect resource

– Identify all costs incurred to supply the resource– Identify the practical capacity supplied by the

resource– Determine the capacity cost rate of the resource by

dividing its cost by the practical capacity

© 2012 Pearson Prentice Hall. All rights reserved.

Capacity cost rate

Cost of capacity suppliedPractical capacity of resources supplied

=

© 2012 Pearson Prentice Hall. All rights reserved.

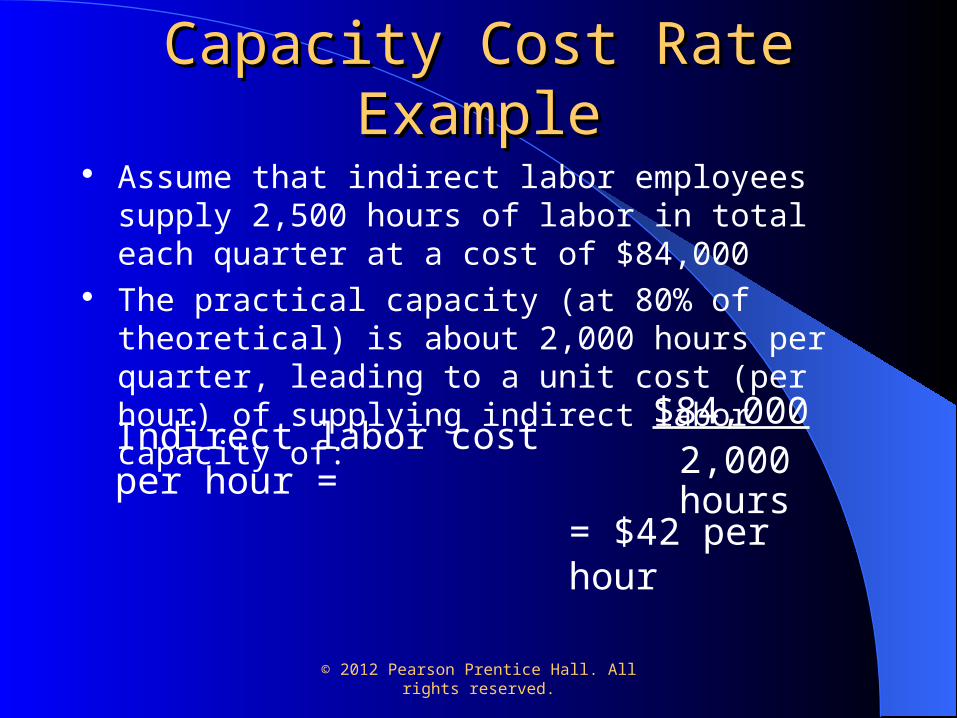

Capacity Cost Rate ExampleCapacity Cost Rate Example Assume that indirect labor employees supply 2,500 hours

of labor in total each quarter at a cost of $84,000 The practical capacity (at 80% of theoretical) is about

2,000 hours per quarter, leading to a unit cost (per hour) of supplying indirect labor capacity of:

Indirect labor cost per hour =$84,000

2,000 hours

= $42 per hour

TDABC – Second ParameterTDABC – Second Parameter Estimation of how much of each resource’s

capacity is used by the activities performed to produce the products and services

© 2012 Pearson Prentice Hall. All rights reserved.

Time-Driven ABCTime-Driven ABC Use parameter estimates to assign indirect costs:

Cost of using resource i by product j =

Capacity cost rate of resource i

x Quantity of capacity of resource i used by product j

© 2012 Pearson Prentice Hall. All rights reserved.

© 2012 Pearson Prentice Hall. All rights reserved.

TDABC Profitability ReportTDABC Profitability Report Managers may use insights from TDABC cost

analysis to improve operations Possible actions include:

– Reduce setup times– Reduce time required for purchasing– Reduce time required for scheduling production

orders– Increase prices on unprofitable products– Impose minimum customer order sizes– Make decisions on desired product mix

© 2012 Pearson Prentice Hall. All rights reserved.

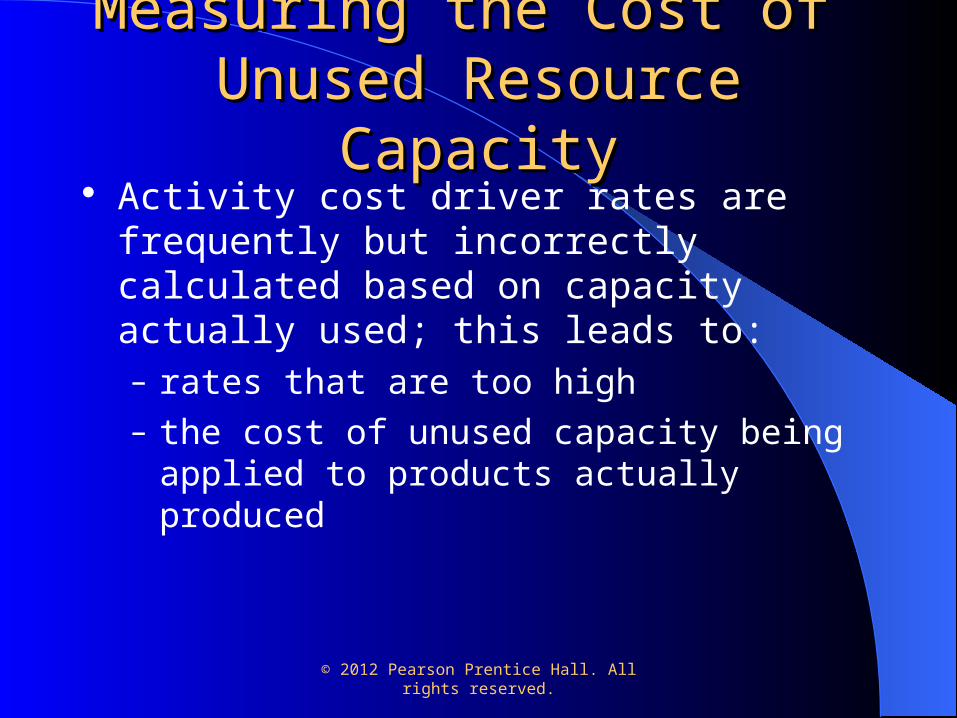

Measuring the Cost of Measuring the Cost of Unused Resource CapacityUnused Resource Capacity

Activity cost driver rates are frequently but incorrectly calculated based on capacity actually used; this leads to:– rates that are too high– the cost of unused capacity being applied to

products actually produced

© 2012 Pearson Prentice Hall. All rights reserved.

Cost of Unused Capacity Cost of Unused Capacity The cost of unused capacity should not be

assigned to products produced or customers served during a period

The cost of unused capacity remains someone’s, or some department’s, responsibility

Usually you can assign the cost of unused capacity after analyzing the decision that authorized the level of capacity supplied

Such an assignment is done on a lump-sum basis; it will not be assigned to individual units of products

Copyright 2010 Pearson Education Canada

Activity-Based Costing Activity-Based Costing SystemsSystems

Three things to consider to improve an existing costing system:

1. Direct-cost tracing– Reduce indirect costs by classifying more costs as direct

2. Indirect-cost pools– Expand the number of indirect-cost pools until the costs in each pool

are homogeneous – the amount varies directly as activity varies

3. Activity-cost drivers– A measure of the activity performed for each cost driver– The denominator that is divided into the indirect cost pool to

calculate the activity cost rate

Define Activities, Activity Cost Pools,Define Activities, Activity Cost Pools,and Activity Measuresand Activity Measures

At Classic Brass, the ABC team, selected the followingactivity cost pools and activity measures:

At Classic Brass, the ABC team, selected the followingactivity cost pools and activity measures:

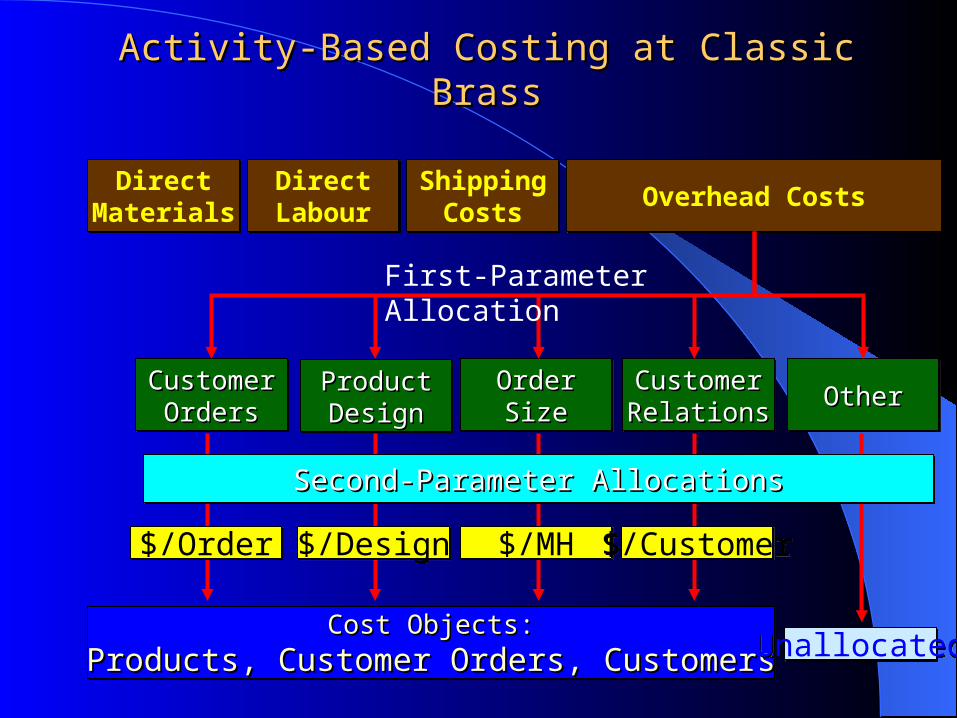

Customer Orders - assigned all costs of resources that are consumed by taking and processing customer orders.

Product Designs - assigned all costs of resources consumed by designing products.

Order Size - assigned all costs of resources consumed as a consequence of the number of units produced.

Customer Relations – assigned all costs associated with maintaining relations with customers.

Other – assigned all overhead costs that are not associated with the other cost pools.

Customer Orders - assigned all costs of resources that are consumed by taking and processing customer orders.

Product Designs - assigned all costs of resources consumed by designing products.

Order Size - assigned all costs of resources consumed as a consequence of the number of units produced.

Customer Relations – assigned all costs associated with maintaining relations with customers.

Other – assigned all overhead costs that are not associated with the other cost pools.

Define Activities, Activity Cost Pools,Define Activities, Activity Cost Pools,and Activity Measuresand Activity Measures

TracedTraced TracedTraced TracedTraced

Activity-Based Costing at Classic BrassActivity-Based Costing at Classic Brass

DirectMaterials

DirectMaterials

DirectLabourDirect

LabourShipping

CostsShipping

Costs Overhead CostsOverhead Costs

Cost Objects:Cost Objects:

Products, Customer Orders, CustomersProducts, Customer Orders, CustomersCost Objects:Cost Objects:

Products, Customer Orders, CustomersProducts, Customer Orders, Customers

Activity-Based Costing at Classic BrassActivity-Based Costing at Classic Brass

DirectMaterials

DirectMaterials

DirectLabourDirect

LabourShipping

CostsShipping

Costs

Cost Objects:Cost Objects:

Products, Customer Orders, CustomersProducts, Customer Orders, CustomersCost Objects:Cost Objects:

Products, Customer Orders, CustomersProducts, Customer Orders, Customers

OrderOrderSizeSize

OrderOrderSizeSize

CustomerCustomerOrdersOrders

CustomerCustomerOrdersOrders

ProductProductDesignDesignProductProductDesignDesign

CustomerCustomerRelationsRelationsCustomerCustomerRelationsRelations OtherOtherOtherOther

Overhead CostsOverhead Costs

First-Parameter Allocation

Activity-Based Costing at Classic BrassActivity-Based Costing at Classic Brass

DirectMaterials

DirectMaterials

DirectLabourDirect

LabourShipping

CostsShipping

Costs

Cost Objects:Cost Objects:

Products, Customer Orders, CustomersProducts, Customer Orders, CustomersCost Objects:Cost Objects:

Products, Customer Orders, CustomersProducts, Customer Orders, Customers

CustomerCustomerOrdersOrders

CustomerCustomerOrdersOrders

OrderOrderSizeSize

OrderOrderSizeSize

CustomerCustomerRelationsRelationsCustomerCustomerRelationsRelations OtherOtherOtherOther

Overhead CostsOverhead Costs

First-Parameter Allocation

Second-Parameter AllocationsSecond-Parameter AllocationsSecond-Parameter AllocationsSecond-Parameter Allocations

$/Order$/Order $/Design$/Design $/MH$/MH $/Customer$/Customer

UnallocatedUnallocated

ProductProductDesignDesignProductProductDesignDesign

Calculate Activity RatesCalculate Activity Rates

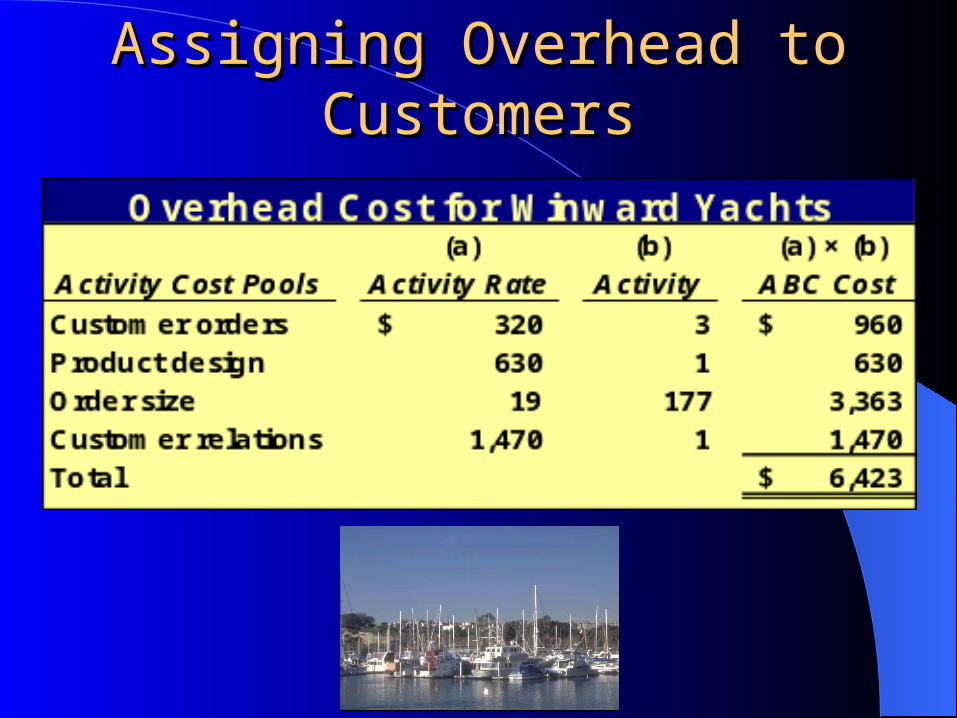

Assigning Overhead to Assigning Overhead to CustomersCustomers

© 2012 Pearson Prentice Hall. All rights reserved.

ABC at Service CompaniesABC at Service Companies Although ABC had its origins in manufacturing

companies, many service organizations today are obtaining great benefits from this approach– In practice, the actual construction of an ABC

model is nearly identical for both types of companies

– This should not be surprising since, in manufacturing companies, the ABC system focuses on the “service” component of the company

© 2012 Pearson Prentice Hall. All rights reserved.

ABC at Service Companies ABC at Service Companies Service companies in general are ideal candidates

for activity-based costing– Virtually all costs are indirect and appear to be

fixed– They often do not have direct, traceable costs to

serve as convenient allocation bases– They must supply virtually all their resources in

advance to provide the capacity to perform work for customers during each period