procedure # property, plant, equipment, and intangibles · pdf fileprocedure # property,...

TRANSCRIPT

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 1 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

PROCEDURE # PROPERTY, PLANT, EQUIPMENT, and INTANGIBLES Date approved Date Policy will

take effect

Date of Next Review

Approved by

Senior Financial Accountant, Financial Services Unit

Custodian title & e-mail address

Senior Financial Accountant

Responsible Division

Financial Services Unit

Supporting documents, procedures & forms of this procedure

Key References & Legislation

Audience

Internet – public access Staff Intranet – UTS Staff Only

Expiry date

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 2 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

Contents 1 Introduction/Background 3 2 Scope / Purpose 3 3 Definitions 3 4 Register of Delegations 4 5 Capital Expenditure Overview 4 6 Instructions 6

6.1 Capital Approval Process 6 6.2 Capitalisation Policy 10 6.3 Capital Expenditure types (Capex) 11 6.4 Acquisitions – process and account coding 12 6.5 Disposals 15 6.6 Transfers 15 6.7 Depreciation and Amortisation 16 6.8 Stocktaking 16 6.9 Valuations 17 6.10 Motor Vehicles 18 6.11 Intangible Assets and Patents 20

7 Roles & Responsibilities 20 8 Version Control Table 21

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 3 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

1 Introduction/Background The Senior Financial Accountant in the Financial Services Unit at UTS has responsibility for oversighting compliance by UTS staff with all procedures relating to the acquisition, transfer, depreciation, disposal, financial management, classification and stock taking of all property, plant and equipment. In addition the Senior Financial Accountant is also responsible for oversighting compliance by staff with procedures relating to intangible assets. The services provided by the FSU in relation to these functions include: • Handling enquiries from staff on matters to do with accounting for property, plant, equipment, and

intangible assets; • Providing lists of capitalised assets belonging to Faculties/Units; and • Generating capital spending reports for Faculties/Units.

2 Scope / Purpose The aim of this procedure is to enable staff to promptly find answers to their questions regarding the financial processes relating to the acquisition, transfer, depreciation, disposal, financial management, classification, and stock taking of property, plant, and equipment, and to their questions relating to intangible assets. It should result in an improved awareness by individual staff of their responsibilities and obligations in relation to these matters, and as a consequence will save time and resources at Faculty or Unit level and within the FSU.

3 Definitions Word/Term/ Abbreviation Definition AVR Asset Verification Report

Capex

Capital expenditure and includes major refurbishments.

Capitalised equipment Items that are included on the UTS asset register. The cost of the asset is depreciated in the P&L over the life of the asset. E.g. equipment over $5,000, IT equipment leased for more than 2 years

Depreciation A term to describe the method of allocating an asset's purchase cost over its useful life, roughly corresponding to normal wear and tear. Depreciation is expensed in the P&L.

FAC Facilities Advisory Committee

FMU Facilities Management Unit

GL General Ledger

Infrastructure Items classified as Infrastructure include Lifts, Air-conditioning, Fire Safety Equipment, Electrical Fittings, Suspended Ceilings, Carpet and Carpet Tiles.

ITD IT Department

Non capitalised equipment

Items that are not included on the UTS asset register. The cost of the asset is expensed in the year of purchase, e.g. equipment under $5,000

Opex Operating expenditure

PP & E Property, Plant and Equipment

PIC Physical Infrastructure Committee

Refurbishment Includes improvements and/or replacement to walls, ceilings, plant, furniture etc

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 4 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

Word/Term/ Abbreviation Definition Straight Line Depreciation A depreciation method where the purchase cost is allocated evenly over

the life of the asset, so that the amount of depreciation expensed in the P&L is the same each month

ITCMP IT Capital Management Plan

4 Register of Delegations

These procedures should be read in conjunction with the Register of Delegations http://www.gsu.uts.edu.au/delegations/documents/standing-delegations-authority.pdf specifically the following sections;

• 1.2 - General expenditure • 1.3 - Capital Works • 1.4 - Real Property transactions

5 Capital Expenditure Overview The purchase of capital items within UTS commences with the budget process. Requests to purchase capital items by Faculties and Divisions are required to be submitted through the Budget process for evaluation and allocation of funding. The allocation of funding does not mean approval and staff are required to follow the Project Commencement Approval Process as per section 6 (b) below prior to purchasing the capital item. Capital items for UTS can be dissected into the following categories.

(a) Land, Building and Infrastructure purchases; (b) Computer Hardware and Software purchases;

(c) Plant and Equipment purchases (includes scientific equipment, audio visual equipment etc);

(d) Library Book purchases;

(e) Works of Art purchases;

(a) Land, Building and Infrastructure purchases are required to be purchased as per the steps outlined in 6.1 below and are required to be coordinated by FMU. The process involves two stages;

i. Obtain budget approval as outlined in 6.1(a) The Project Funding Approval Process and

flow chart no 2: and

ii. If budget approval obtained then follow the process outlined in 6.1(b) The Project Commencement Approval Process and flow chart no 3:

(b) Computer Hardware and Software purchases

i. Major computer hardware or software purchases or the installation of a major software

system e.g. Oracle Payroll implementation, is required to be included in the IT Capital Management Plan (ITCMP).

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 5 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

ii. Computer Hardware and Software sourced via an ITCMP project are required to be purchased as per the steps outlined in 6.1 below and are required to be coordinated by ITD. The process involves two stages;

1. Obtain budget approval as outlined in 6.1(a) The Project Funding Approval

Process and flow chart no 2: and

2. If budget approval obtained then follow the process outlined in 6.1(b) The Project Commencement Approval Process and flow chart no 3

iii. Computer Hardware and Software originally submitted through ITCMP and not approved

cannot be resubmitted by the faculty or division in their capital expenditure budget.

iv. Computer Software and Hardware (Desktops, Laptops, Tablets etc) including access devices NOT classified as an ITCMP project are to be initially included in the Capital Expenditure Budget and submitted to FSU by the individual faculty or division. If budget approval is obtained the item can be purchased in accordance with the Register of Delegations: http://www.gsu.uts.edu.au/delegations/documents/standing-delegations-authority.pdf

All Purchases for Computer Software and Hardware are to be purchased via ITD Purchasing.

(c) Plant and Equipment purchases are to be initially included in the Capital Expenditure Budget and

submitted to FSU by the individual faculty or division. If budget approval is obtained the item can be purchased in accordance with the Register of Delegations http://www.gsu.uts.edu.au/delegations/documents/standing-delegations-authority.pdf

(d) Library Book purchases are to be initially included in the Capital Expenditure Budget and

submitted to FSU by the Library. If budget approval is obtained the item can be purchased in accordance with the Register of Delegations http://www.gsu.uts.edu.au/delegations/documents/standing-delegations-authority.pdf

(e) Works of Art purchases are to be initially included in the Capital Expenditure Budget and

submitted to FSU by the Art Gallery. If budget approval is obtained the item can be purchased in accordance with the Register of Delegations http://www.gsu.uts.edu.au/delegations/documents/standing-delegations-authority.pdf

The approval process for capital expenditure can be summarised by the following flow chart;

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 6 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

For further project approvals see Flow Charts 2 and 3 in Section 6 dealing with the processes for Project Funding Approval and Project Commencement Approval.

6 Instructions

6.1 Capital Approval Process The approval process for the acquisition of capital items will depend on the type of capital expenditure being purchased. • For Projects which include Land, Buildings, Infrastructure or computer equipment being purchased

through ITCMP the approval process per 6.1(a) The Project Funding Approval Process is required to be followed.

• For all other capital items as outlined in 5(b)iv and 5(c) to (e) above, the process as per 6(c) below

is required to be followed. Please note: All capital proposals/projects involving FMU and/or ITD i.e. buildings, building infrastructure, ITCMP must be submitted to FMU/ITD for inclusion in their annual budget submission. No building or IT project may go ahead without formal approval through these channels. If your proposal is not approved in that year’s budget cycle you cannot go ahead with that project of your own accord. Project proposals may be resubmitted for further consideration. (a) The Project Funding Approval Process

The procedure for Projects which include acquisitions of Land, Buildings, Infrastructure or computer equipment sourced through ITCMP, is outlined by the Flow Chart ‘Project Funding Approval Process”. There are a number of steps in the process which includes; • The relevant business unit develops the business case that requires funding approval and

submits it to the relevant Department – FMU for building works, and ITD for IT products and services.

• FMU/ITD collate and prioritise their respective programs and submit to FSU by the required

budget deadline which will be advised each year (e.g. 17 August 2007 for 2008 budget).

Is it a purchase of an asset or building/ ITCMP project?

Capex Approval Process – Flowchart 1

Building/ ITCMP Project

Business Unit

Asset Purchase Budget submission Project business case

submission to FMU/ITD

SEM/Council approval

Purchase asset subject to delegation

Yes

Project Funding Approval (see Flowchart 2)

Project Commencement Approval (see Flowchart 3)

Yes

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 7 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

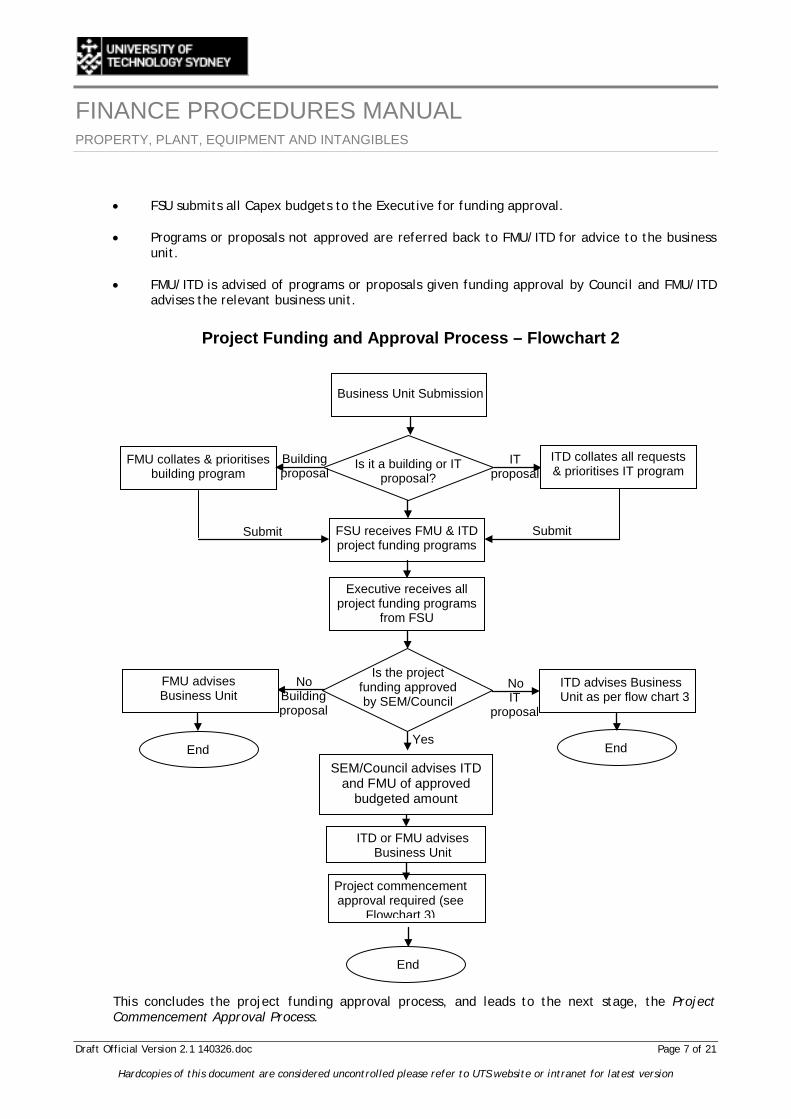

• FSU submits all Capex budgets to the Executive for funding approval. • Programs or proposals not approved are referred back to FMU/ITD for advice to the business

unit. • FMU/ITD is advised of programs or proposals given funding approval by Council and FMU/ITD

advises the relevant business unit.

This concludes the project funding approval process, and leads to the next stage, the Project Commencement Approval Process.

Is it a building or IT proposal?

Is the project funding approved by SEM/Council

Project Funding and Approval Process – Flowchart 2

IT proposal

No

Submit

ITD advises Business Unit as per flow chart 3

End

Business Unit Submission

FSU receives FMU & ITD project funding programs

Building proposal

FMU collates & prioritises building program

Submit

ITD collates all requests & prioritises IT program

Executive receives all project funding programs

from FSU

No

End

ITD or FMU advises Business Unit

Yes

FMU advises Business Unit IT

proposal Building proposal

Project commencement approval required (see

Flowchart 3)

End

SEM/Council advises ITD and FMU of approved

budgeted amount

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 8 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

(b) The Project Commencement Approval Process The granting of funding approval as described above for Land, Buildings, Infrastructure or computer equipment sourced through ITCMP triggers the next stage of the procurement process as illustrated by the Flow Chart ‘The Project Commencement Approval Process – Flow Chart 3’. There are a number of steps involved as follows: • Following receipt of advice of funding approval, FMU/ITD then refer the program or proposal

through separate processes for commencement approval. • ITD refers its proposals to the IT Committee. • The Director of FMU refers its Capex proposals to the DVC Resources who then refers (i) Capex

submissions and papers to the FAC for review and priority; and then (ii) refers the proposals to the PIC for review and approval. The PIC can approve project proposals that are valued at less than $5million otherwise they are referred for approval to the UTS Council (proposals valued in excess of $5million).

• If as a result of the above processes a proposal or any part of it is not approved, it is referred

back to either ITD or the Director FMU to review with the responsible business unit. • Following review the proposal may be resubmitted with further information being provided. • When approval to commence the proposal is received by ITD or FMU it advises the business

unit and proceeds with commencement action. • FSU opens account activity in the finance system and commences finance tracking. Activities

beginning with prefix '50' are designated capital activities.

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 9 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

Is it a building or IT project?

Project Commencement Approval Process – Flowchart 3

IT Project

No

Project Funding approved (see Flowchart 2)

ITD Building Project

FMU Director

Formal approval by UTS

Executive Yes/No

Finance tracking by FMU/ITD/FSU

Business Unit advised

ITD manage project

End

End

FSU opens account activity in finance

system

Yes

Yes

Report back for review and advise Business

Unit Project back for review

No

Projects prioritised and submitted to UTS Executive

Business Unit/FMU

DVC Resources

Finance Committee PIC is a sub committee

of FC

Project commences

Facility Advisory Committee (FAC) reviews & prioritises

projects

Are additional project details & timing

implications required? Yes/No

Physical Infrastructure Committee (PIC) reviews & approves projects up to $5m

Yes

Additional details

Is the project over $5m?

No

Yes

Formal project commencement

approval Yes/No

FMU manage project

Business Unit advised

End

Project commences

No

UTS Council approves projects

over $5m

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 10 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

(c) Capital approval and acquisitions – Non project

Capital acquisitions that are not for Land, Buildings, Infrastructure or computer equipment sourced through ITCMP are classified as general asset purchases and the approval and acquisition process is outlined as follows; • Business Unit includes items requested to be purchased in the capital budget tool within

the Cognos Budgeting system. • Budget requests/submissions forwarded to SEM/Council by FSU for approval.

• FSU advises Business Unit if submitted capital item is approved or rejected.

• Capital items approved are purchased in accordance with the Register of Delegations.

• Computer hardware and software are to be purchased through ITD Purchasing.

6.2 Capitalisation Policy

Capital items $5000 and over are capitalised into the University asset register. Capital projects which involve the purchase of multiple capital items will be capitalised regardless of the amount as long as the total project cost exceeds $5000. All items purchased as works of art are capitalised into the University asset register regardless of the amount. All items (except electronic serials) purchased as part of the library collection are capitalised into the University asset register regardless of the amount. Leases classified as finance leases are capitalised into the University asset register regardless of the amount as per AASB 117 – Leases.

General Asset Approval Process – Flowchart 4

Business Unit

Budget submission

SEM/Council approval

Purchase asset subject to delegation

Yes

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 11 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

6.3 Capital Expenditure types (Capex) Capital spending within the University consists of the following asset categories:

(a) Building works and IT expenditure - sourced through ITCMP as part of a capital project.

Projects undertaken by ITD and FMU that meet specific criteria are assessed as capital projects and are assigned an activity number with prefix "50". (See: Project Funding Approval Process, Section 6.1). Generally all expenditure under a capital project is Capex, including items of equipment that are less then $5,000. Some expenditure under a capital project may still be considered non-capital in nature and will be treated as Opex. Examples of typical Opex expenses are: • Afternoon/morning teas and cleaning charges; • Relocation costs and costs of removing obsolete equipment; • Demolition costs (unless part of capital refurbishment); • Backfill costs of replacing staff who have been transferred to a project; • For software projects, the cost of training staff to use the software; and • Repairs; and maintenance agreements

Feasibility studies, surveys, market research, etc. (b) General asset purchases of equipment by the faculty/unit which cost $5,000 or more per item.

Examples of purchased equipment include computer hardware, computer software, scientific equipment, furniture, motor vehicles, audio visual equipment, photocopiers, data projectors, security equipment, networking equipment and networking installations.

(c) IT equipment purchased and leased through IT purchasing where the lease term is for more than 2 years. The IT equipment is initially ordered by the faculty/unit, then purchased and leased by ITD. IT equipment that is leased for more than 2 years will usually qualify as a finance lease arrangement and the expenditure will be capital. Expenditure can be under $5,000 per item.

(d) Purchases of works of art All purchases of works of art will be capitalised regardless of their current purchase price/value.

(e) Library Collection All monographs, serials (excluding electronic serials), perpetual licences, theses and rare books purchases made by the UTS library including those purchases less than $5,000.

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 12 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

6.4 Acquisitions – process and account coding Refer section 6.1 Capital Approval Process for details on the approval process for (1) Project capital items or (2) general asset purchases. The UTS Purchasing Policy and Register of Standing Delegations need to be read in conjunction with these procedures, and reference should be made to the PP & E Identification and Classification Guidelines. The account coding rules for acquisition of capital items will depend on the capital expenditure type outlined in section 6.3 above. The acquisition process is as follows; (a) Building works and IT - sourced through ITCMP expenditure as part of a capital project.

Equipment or services acquired under a capital project are procured by FMU or ITD Purchasing section. (Refer to the UTS Finance Manual Purchasing and Payments Chapter for more details about purchasing procedures) Capital projects are assigned an Oracle activity number with prefix '50'. All purchase orders and invoices of a capital nature relating to this activity should be coded to an appropriate WIP natural account, in the range 17520 to 18395 e.g. 18215 WIP computer hardware. The expenditure under a capital project is held in the WIP accounts until the project has reached practical completion (i.e. until the project has reached a stage such that UTS can begin to use the end product even if there is more expenditure to be incurred before the project is completely finished). When the project has reached practical completion as advised by the project holder the total expenditure is transferred from the WIP accounts to appropriate asset clearing account and added to the UTS asset register.

(b) General asset purchases of equipment by the faculty/unit which cost $5,000 or more per item.

General assets purchased by the Faculty/Unit or by IT purchasing (for IT equipment) which are not part of a project outlined in (a) above. The equipment categories and accounting natural accounts that should be used when coding purchase orders and invoices are listed in the table below. If the item of equipment costs $5,000 or more the purchase order/invoice line item should be coded to the appropriate Asset CLEARING account. If the item of equipment costs less than $5,000, then the purchase order/invoice line item should be coded to the appropriate P&L account and the expense is treated as OPEX. Natural Accounts to use for equipment over $5,000 per item:

15620 Computer Hardware over $5,000 clearing 15630 Computer Software over $5,000 Clearing 15640 Photocopier over $5,000 Clearing 15650 Furniture over $5,000 Clearing 15660 Data Projectors over $5,000 Clearing

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 13 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

15670 Scientific Equipment over $5,000 Clearing 15680 Audio Visual over $5,000 Clearing 15690 Other Equipment over $5,000 Clearing 15820 Motor Vehicles - Cars Clearing 15830 Motor Vehicles - Other Clearing 15920 Works of Art -Clearing

Natural accounts to use where the cost is less than $5,000 per item:

70205 Furniture less than $5,000 70210 Fittings less than $5,000 70305 Purchase of Desktop less than $5,000 70310 Purchase of Laptops less than $5,000 70315 Purchase of Computer Peripherals less than $5,000 70320 Purchase of Printers less than $5,000 70328 Computer Network Equipment under $5,000 70335 Expensed IT equipment 70405 Computer Software Purchase of License < $5,000 70505 Other Equipment less than $5,000 70510 Purchase of Scientific Equipment < $5,000 70515 Purchase of Audio Visual less than $5,000 70610 Security - Equipment less than $5,000 70915 Telecommunications - Installations <$5,000 70916 Telecommunications - Minor Equipment < $5,000

The Asset Accountant sends details about transactions posted to the clearing accounts to the Asset Controller for approval. The Asset Controller will contact the Faculty/Unit to confirm the asset exists, has been received by UTS and to determine its location and serial number. After approval by the Asset Controller, the item of equipment is added to the Asset Register in Oracle. An Oracle system journal will transfer the asset from the clearing account to the actual asset account.

(c) IT Assets leased.

For computer equipment that is purchased by IT purchasing and is to be leased, the Natural Account to be used on the Purchase Order Requisition is:

15700 Computer Hardware to be leased Clearing (Refer UTS Finance Manual, Purchasing and Payments Chapter for more details about purchasing procedures.) IT purchasing will buy the equipment and organise delivery to the Faculty/Unit. The ITD lease administrator will contact the Faculty/Unit and ask them to complete a Request to Rent IT Equipment Form. This form asks for details about the required term of the lease and for the location and users by serial number of the leased equipment. The ITD lease administrator will organise leasing the equipment from the lease company. Note that at the end of the lease term the equipment must be returned to the leasing company. In general, as long as the term of the lease is for more than 2 years then the IT expenditure can be assessed as Capex even if the cost per item is less than $5,000. The greater than 2 year term is

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 14 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

important as it will ensure that the lease is assessed as a finance lease which then enables the expenditure to be viewed as Capex. Computer equipment that is purchased by IT purchasing and is leased for a period of 2 years or less, are generally classified as operating leases and are expensed. Recognition of Leased Assets Each quarter the leased assets are advised to the leasing company and the conditions of the lease are determined. The leased assets are added to the asset register and their value is calculated as the present value of the lease premiums paid to the leasing company over the term of the lease as per the accounting standards for leases. Amortisation of Finance Leases Each month a leased hardware amortisation charge (natural account 64445) and a lease interest charge (natural account 67010) will be charged to the Faculty/Unit. At the termination of the lease the sum of these charges over the life of the lease equals the total lease premiums paid to the leasing company.

(d) Purchases of works of art

Acquisitions of works of art by the University are capitalised into the asset register regardless of the amount. This is due to works of art appreciating in value over time.

(e) Library Collection

Library acquisitions are procured by the Library purchasing section. All monographs, serials and rare book purchases made by the UTS Library are recorded on the UTS Library Collection Register including those costing less than $5,000. Purchase Orders and invoices are coded to the following natural accounts:

16015 Serials Valuation (excluding electronic serials) 16025 Monographs Valuation 16040 Rare Books Valuation 16050 Theses Valuation 16235 Licences – Perpetual

Library assets can also be acquired by donation. Each quarter the library provides FSU with the number of serials, monographs and thesis donated in the current quarter. The library also provides FSU with a listing of the number of and expenditure on serials and monographs purchased in the current quarter and these amounts are reconciled to the general ledger.

For acquisitions of capital items please refer to the UTS Finance Manual Purchasing and Payments Chapter for more details about purchasing procedures.

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 15 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

6.5 Disposals (a) Disposal of capitalised and non-capitalised equipment (non-leased):

Where an item of equipment becomes obsolete an Asset Disposal Request Form http://www.fsu.uts.edu.au/pdfs/asset_disposal.xls should be completed and submitted to the Asset Control Officer in Central Services. The Asset Control Officer will firstly determine whether there is an alternative use for the asset within the UTS. In such cases the asset will be accounted for as an Asset Transfer. In the absence of an internal alternative use the asset will be either sold or donated to an outside organisation. The method of disposal will depend on the estimated value of the asset and could be disposed by auction, tender, negotiated sale, donation or trade-In. The Asset Control Officer is responsible for the method of Disposal and will take the necessary action to advertise internally in the Staff Notices or externally as appropriate to ensure principles of accountability, transparency, and fair value is satisfied. The asset will be removed from the UTS asset register with the sales proceeds and any remaining depreciation being coded to the Faculty/Unit organisation unit. The same procedures apply to non-capitalised assets, however no adjustment is made to the UTS asset register as these assets are expensed in their year of purchase.

(b) Disposal of leased IT equipment At the end of the lease term a leased asset must be returned to the leasing company. The ITD lease administrator will monitor what lease terms are expiring and contact the Faculty/Unit in advance of the lease expiring so that the equipment can be collected by ITD and returned to the vendor or the Faculty/Unit can exercise the option to continue the lease for a further period.

(c) Disposal of library assets

The library periodically reviews their collection and removes titles that are no longer required. Each quarter the library sends a report to FSU of the number of serials and monographs in the collection. FSU calculate the number and value of disposals and reflects these disposals in the GL.

6.6 Transfers Where a capitalised asset is transferred to another faculty or business unit within the UTS an Asset Advice and Transfer Form http://www.fsu.uts.edu.au/pdfs/asset_advice_and_transfer_form.xls should be completed and submitted to the Asset Control Officer in Central Services. The asset’s cost and depreciation reserve will be transferred to the new organisation code ensuring that any remaining depreciation charges are also charged to the new organisation unit. No form is required to be submitted for the transfer of non-capitalised assets. Where a capitalised asset is temporarily removed from campus, including where an asset is loaned to an outside organisation, an Asset Removal from Campus Form http://www.fsu.uts.edu.au/pdfs/asset_removal.xls should be completed and submitted to the Asset Control Officer in Central Services. This will ensure that the asset is correctly accounted for during the annual stocktaking process. The same procedures apply to non-capitalised assets.

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 16 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

6.7 Depreciation and Amortisation Land and Works of Art are not depreciated. Depreciation on other assets is calculated using the straight line method to allocate their cost or revalued amounts, net of their residual values over their estimated useful lives as follows:

Asset Class Depreciation Rate Depreciation Method Buildings 2.00% Straight - line Buildings Infrastructure 4.00% Straight - line Electrical Installations 4.00% Straight - line Suspended Ceilings 5.00% Straight - line Carpet and Carpet Tiles 6.66% Straight - line Motor Vehicles 20.00% Straight - line Computing and Audio Visual Equipment 20.00% Straight - line Photocopiers 25.00% Straight - line Office, Teaching & Research Equipment 10.00% Straight - line Library Collection 12.50% Straight line, 5% residual Software - Minor 33.33% Straight - line Software - Major 14.29% Straight - line Leased IT Hardware under Finance Lease 33.33% (for 3 year lease) Straight - line

Prior to 01.01.2014, the depreciation rate for Computing Equipment was 33.33%, and the depreciation rate for Office, Teaching and Research Equipment was 20% pa.

Stocktaking The Asset Register is used to record, track and manage UTS assets and to provide complete, accurate and timely data and information for internal management and external financial reporting purposes. A stocktake is undertaken to verify the existence of assets and confirm their location. All Faculties/Units are required to verify assets under their control at least once every Financial (Calendar) Year. An Asset Verification Report (AVR) containing a listing of assets on the UTS Asset Register for each Faculty/work unit is compiled by the Asset Controller. The AVR consists of a specific list of equipment, software and furniture that are deemed to be the capitalised assets of the UTS. The AVR details: • The asset number • Description of the asset • Number of items purchased • Value • Location • Date of purchase • Serial number • Custodian

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 17 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

A representative nominated by each Faculty/Unit will be responsible to assist in the stocktaking of that Faculty/Unit’s Assets. The representative will be a senior person capable of signing off the stocktake for that Faculty/Unit. The Asset Controller conducts the stocktake in conjunction with a faculty/unit representative. One officer checks the description of the asset and serial number and the other officer checks and notes the details on the AVR. Verifying officers should indicate on the AVR that the asset has been sighted in the faculty/unit. The location should include Campus, Building and Room Number (e.g.CB01.4.02) as used in the internal Telephone Book. Assets owned and identified during the Stocktake but not appearing on the Stocktake report are to be recorded on an Asset Advice Form. http://www.fsu.uts.edu.au/pdfs/asset_advice_and_transfer_form.xls Assets on the report but not able to be found during the Stocktake are to be recorded on an Asset Disposal Form. http://www.fsu.uts.edu.au/pdfs/asset_disposal.xls. Every effort must be made to discover the reason for the loss or disappearance of this equipment. The Stocktake cover sheet (UTS Assets Register Reconciliation Sheet) is then signed and dated by the Asset Control Officer and the representative nominated by each Faculty/Unit. The Asset Control Officer keeps the original stocktake documents and a copy is given to the Faculty/Unit.

6.8 Valuations UTS engages external professional valuers to perform valuations for;

• Insurance renewal: • Statutory Account valuations to satisfy the requirements of AASB 116 - Property, Plant and

Equipment: Valuations - Insurance The university obtains yearly insurance valuations based on replacement values for Property, Plant and Equipment to ensure that adequate cover is obtained should an insurable event occur. The valuations are organised by the university’s Taxation and Insurance section. Valuations - Statutory Accounts Land, Buildings and Infrastructure UTS engages external professional valuers to carry out an annual valuation to determine the ‘Fair Value’ of the freehold interest of individual properties within the UTS property portfolio. This is done so that accurate values are obtained for balance sheet and annual financial reporting purposes. The term ‘Fair Value’ requires that the valuation is in accordance with the Australian Property Institute Practice Standard for Financial Reporting of Real Property and Related Assets PS9, and is also in accordance with the International Accounting Standard IAS16 (Australian equivalent AASB-116). ‘Fair Value’ is defined as the amount for which an asset could be exchanged between knowledgeable and willing parties in an arm’s length transaction. It is the most advantageous price reasonably obtainable by the seller and the most advantageous price reasonably obtainable by the buyer. The fair value of an asset is determined by reference to its highest and best use, that is, the use of an asset that is physically possible, legally permissible, financially feasible and which results in the highest value.

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 18 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

Where the ‘Fair Value’ of an item of property, plant and equipment cannot be reliably determined using market based evidence the asset’s fair value is measured at its market buying price and the best indicator of an asset’s market buying price is the depreciated replacement cost or an income approach. The depreciated replacement cost is the current replacement cost less the accumulated depreciation calculated to reflect the expired future economic benefits of the asset. Valuations within this category include installations integral with a building which would normally transfer with the sale of the freehold interest. They include all office and amenity partitions, lighting fixtures, toilet fittings, lifts, escalators, air conditioning systems, carpets, blinds, etc. Plant, Equipment and Intangibles Items of plant and equipment and intangibles assets such as software are valued at their cost less the accumulated depreciation calculated to reflect the expired future economic benefits of the asset. Library Collection and Works of Art Valuations are also undertaken every three years to determine the fair value of UTS’s art collection and the Library's rare book collection. Each year the value of the library's perpetual licenses are also determined and tested for impairment. The main body of the Library collection i.e. the monographs and paper based serials are valued using the Director’s valuation.

6.9 Motor Vehicles The UTS Parking Directive can be found at: http://www.gsu.uts.edu.au/policies/parking.html (a) Types of Motor vehicles arrangements

There are 3 types of motor vehicle arrangements from an assets perspective: • Novated leased vehicles in conjunction with a staff salary packaging arrangement; • Operating lease vehicles known as pooled vehicles; and • Owned pooled vehicles. (i) Leased vehicles in conjunction with a staff packaging arrangement – “Novated Lease”

For information on salary packaged novated leased vehicles go to the HR web page: http://www.hru.uts.edu.au/conditions/packaging/ and also the Financial Procedures Manual-Payroll Chapter, Salary Packaging or Deductions Pre-tax.

The individual staff member is liable for all costs associated with the provision of a leased novated vehicle under a salary packaging arrangement.

The leased vehicles are not treated as assets owned by the university and so are not included on the UTS asset register.

(ii) Operating Lease Pool Vehicles

A faculty/unit may require a vehicle for business purposes. If the vehicle is leased then these vehicles are known as operating leased pooled vehicles. The designated faculty/unit must pay for all rental and operating costs associated with the vehicle and determines who will be the authorised drivers of the vehicle.

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 19 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

Once approval for commencement of an operating lease is provided via the appropriate Senior DVC or CVD, the faculty / unit liaises direct with the university’s designated vehicle leasing supplier for quotes until an appropriate lease arrangement is agreed. Details of the designated vehicle leasing supplier can be found in the UTS Buying Guide at http://www.fsu.uts.edu.au/procurement/staff-only/UTS_Buying_Guide_index.html A ‘Quote Acceptance Form’ is sent to the faculty / unit by the supplier and signed by the appropriate delegated authority. The quote acceptance form along with a copy of the signed Snr DVC / CVD authorisation is sent to a Financial Services Unit delegated officer for co-signature to complete the approval process and commitment of UTS funds. FSU will scan and email a copy to sgfleet and return the original to the leasing faculty / unit. If a staff member uses the vehicle for personal use e.g. borrowing the vehicle for a week night or weekend then FBT may apply. For more information on vehicle FBT go to http://www.fsu.uts.edu.au/tax/manual/fbt.html#pool_vehicle Vehicles that are leased for a term that is substantially less than the economic life of the vehicle will not be classed as owned by the university and therefore not added to the asset register. The faculty / unit will liaise directly with the leased vehicle supplier at lease end for all reconciliation and disposal matters.

(iii) Owned pooled vehicles

A faculty/unit may require a vehicle for business purposes, if the vehicle is purchased by the university then these vehicles are known as UTS- owned pooled vehicles. The designated faculty/unit must pay for all operating costs associated with the vehicle. The faculty/unit determines who the authorised drivers of the vehicle will be. If a staff member uses the vehicle for personal use e.g. borrowing the vehicle for a week night or weekend then FBT will apply. For more information on vehicle FBT go to http://www.fsu.uts.edu.au/tax/manual/fbt.html#pool_vehicle UTS owned vehicles are added to the UTS asset register. Depreciation is charged to the owning faculty/unit. Vehicles are depreciated over 5 years.

(b) Disposal of Motor Vehicles

If the vehicle is a UTS-owned pooled vehicle, contact the Asset Controller on x7485 to organise disposal.

Disposal of leased pool vehicles is arranged directly between the leasing faculty /unit and the leased vehicle supplier.

(c) Traffic Infringements

All traffic infringements (including speeding, parking, toll infringements and red light cameras) for all leased and owned pool vehicles are a personal cost to the driver and not a UTS cost.

t he drive r is ident ifie d by t he regist ra t ion numbe r of the motor vehicle.

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 20 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

t he le a sed pool vehicle supplie r will forward t he infringement not ice t o t he nomina t ed contact person for the vehicle who will arrange for the driver to pay the fine directly.

(d) Accidents and insurance

For information about insurance and what to do in an accident, see the following link http://www.fsu.uts.edu.au/insurance/types/motorvehicle.html Also see the Financial Procedures Manual- Insurance Management Chapter, Motor Vehicle Claims.

6.10 Intangible Assets and Patents An intangible asset is an asset that is without physical substance. Where software is not an integral part of hardware it is treated as an intangible asset. All purchased software that is not an integral part of the hardware is also treated as an intangible asset. Where the software is an integral part of the related hardware (for example the operating system), it is to be treated as Property, Plant and Equipment. To assess an internally generated intangible asset the project needs to be identified at the earliest possible stage. No intangible assets from research will be recognised. Internally generated assets arising from development of an internal project must demonstrate that the asset will generate probable future economic benefit. Software development can be undertaken with in-house software and include activities such as design and construction, testing, specifications works, pre-production use, alternatives, improved products, processes or service.

7 Roles & Responsibilities The key persons responsible are: Harvinder Singh, Senior Financial Accountant, tel 9514 7885 Email [email protected] Murray Gibbons, Financial Accountant Assets, tel 9514 4820 Email [email protected]

Officers Responsibilities

UTS Staff • Complete Asset Verification Reports (AVR) in the time frames given. • Provide any information that is missing from the AVR. • Complete Asset Acquisition/Adjustment form when asset items are

acquired. • Note the AVR for assets sold, transferred or written off.

Head of Department/Unit • Sign AVR as to correctness prior to return to Asset Control Officer, Central Services.

Asset Control Officer, • Issue AVRs in accordance with the UTS perpetual stocktake program.

FINANCE PROCEDURES MANUAL

PROPERTY, PLANT, EQUIPMENT AND INTANGIBLES

Draft Official Version 2.1 140326.doc Page 21 of 21

Hardcopies of this document are considered uncontrolled please refer to UTS website or intranet for latest version

Officers Responsibilities

Central Services • Enter details of changes from completed AVRs.

Financial Accountant – Assets

• Perform regular monthly reconciliation of the Asset Register system to the General Ledger.

8 Version Control Table Version Control Date Released Approved By Amendment

Start from 1.0 YYMMDD (the date the procedure takes effect)

Contact person – full name & title.

Include any superseded procedures and what the amendment is to the document.